South America Irrigation Pumps Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

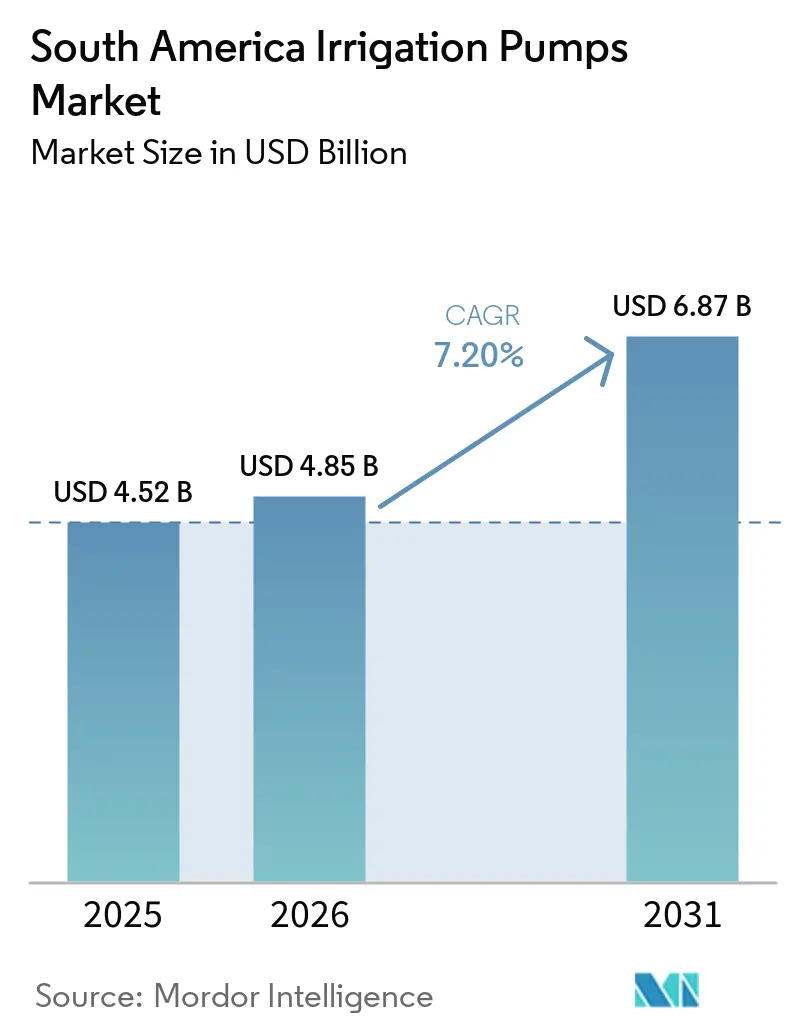

| Base Year Market Size (2025) | USD 4.52 Billion |

| Market Size (2026) | USD 4.85 Billion |

| Market Size (2031) | USD 6.87 Billion |

| Growth Rate (2026 - 2031) | 7.20% CAGR |

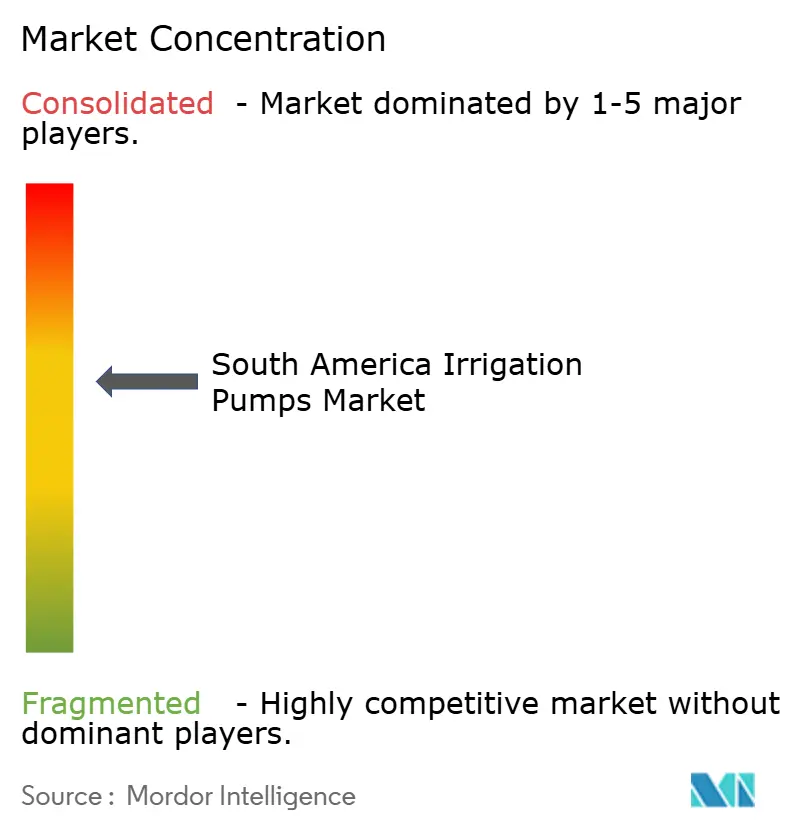

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Irrigation Pumps Market Analysis by Mordor Intelligence

The South America irrigation pumps market size was valued at USD 4.52 billion in 2025 and is estimated to grow from USD 4.85 billion in 2026 to reach USD 6.87 billion by 2031, at a CAGR of 7.20% during the forecast period (2026-2031). The South America irrigation pumps market is being supported by agricultural intensification across Brazil’s Cerrado and MATOPIBA corridors and by Peru’s large irrigation buildout, which is extending procurement cycles for centrifugal, submersible, and displacement pumps. Recurring drought conditions are lifting the need for reliable water access, yet they are also creating operating limits in groundwater-based systems, which keeps replacement and upgrade demand active in parallel. The South America irrigation pumps market is also moving toward more packaged offerings as solar, hybrid, controller, and battery-linked systems become more common on off-grid farms. The South America irrigation pumps market remains moderately fragmented, but stricter project specifications in Peru and recent acquisition activity are favoring suppliers that combine certified equipment, engineering support, and service reach.

Key Report Takeaways

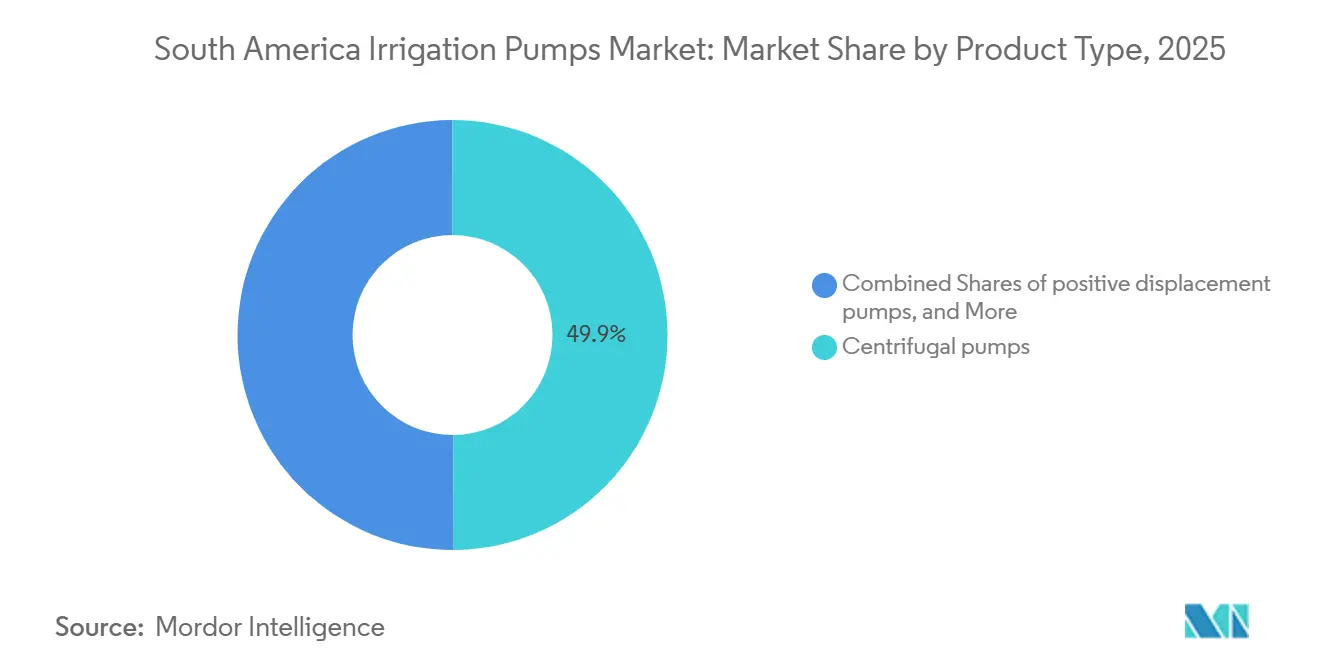

- By product type, centrifugal pumps were the largest segment with 49.9% of the South America irrigation pumps market share in 2025, while positive displacement pumps are the fastest segment and are forecast to expand at a 5.2% CAGR through 2031.

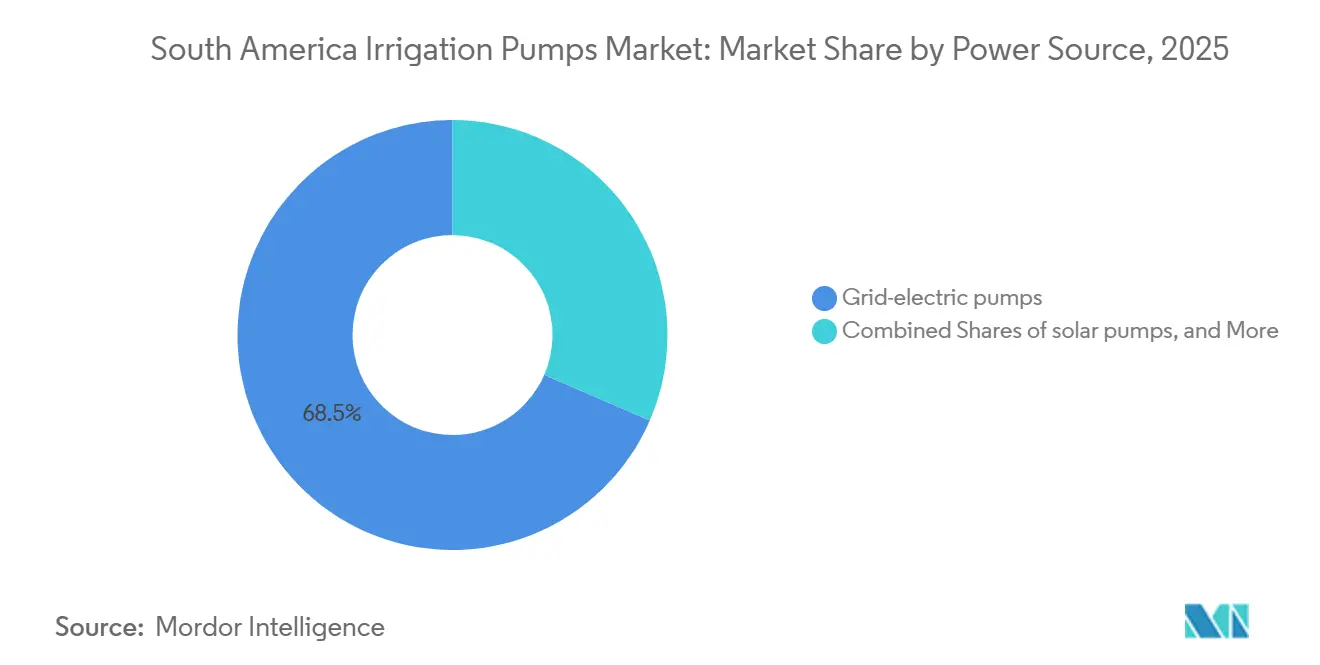

- By power source, grid-electric pumps were the largest segment with 68.5% of the South America irrigation pumps market size in 2025, while solar pumps are the fastest segment and are projected to grow at a 9.2% CAGR through 2031.

- By geography, Brazil held the largest segment with 46% of revenue in 2025, while Peru was the fastest segment and is projected to advance at a 5.1% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South America Irrigation Pumps Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Irrigation network expansion and modernization | +1.8% | Brazil, Peru, and Argentina | Medium term (2-4 years) |

| Water scarcity driving demand for irrigation infrastructure | +1.2% | Brazil, Peru, and Argentina | Short term (≤ 2 years) |

| Subsidized government pump financing programs | +1.0% | Brazil, Peru, and Chile | Short term (≤ 2 years) to Medium term (2-4 years) |

| Solar and hybrid pumping adoption on off-grid farms | +1.0% | Brazil, Peru, Bolivia, and Colombia | Medium term (2-4 years) |

| Diesel-to-solar pump transitions | +0.8% | Brazil, Argentina, and Chile | Medium term (2-4 years) |

| PPP-led co-investment in rural water infrastructure | +0.9% | Peru, Brazil, and Colombia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Irrigation Network Expansion and Modernization

Expansion of irrigated land remains the clearest growth driver for the South America irrigation pumps market because new canals, lift stations, and field systems require a broad mix of pump types from the start. The Food and Agriculture Organization (FAO) showed that South America sustained strong irrigated area growth over the last decade, which supports long planning cycles for irrigation equipment across row crops and export agriculture. Peru’s government presented 22 irrigation projects in 2025 with total investment of USD 24 billion, a target of 1 million additional hectares, and a delivery model led mainly by public-private partnerships (PPPs)[1]Source: Ministry of Agrarian Development and Irrigation, “Government will promote 22 irrigation projects worth more than USD 24 billion,” gob.pe.. Brazil also expanded the institutional base for irrigation investment through new public programs and state-level frameworks, which makes pump procurement more repeatable across both commercial farms and smaller operations. Each new network also creates a long service cycle for station upgrades, controls, and replacement units, which gives vertically integrated suppliers a steadier aftermarket opportunity than firms focused only on first-time sales. That pattern is keeping the South America irrigation pumps market tied not only to greenfield projects, but also to recurring maintenance spending.

Water Scarcity Driving Demand for Irrigation Infrastructure

Water stress is shifting irrigation spending from a yield improvement choice into a risk management requirement for many farms, and that is changing the demand profile of the South America irrigation pumps market. According to Assessment Capacities Project (ACAPS), drought conditions affected 59% of Brazil during the 2023 to 2024 cycle, which underlines why producers are placing more weight on secure water access and installed pumping capacity[2]Source: ACAPS, “Brazil, Impact of Drought in the Brazilian Amazon and 2025 Outlook,” reliefweb.int.. In Brazil, recurring drought from 2023 through 2025 pushed more farms in exposed states toward fully irrigated or partially irrigated production systems, which increased interest in borehole and submersible units. The same pressure is visible in Peru’s coastal belts and in drier parts of Argentina, where dependable pumping is becoming central to crop planning rather than a backup option. A second effect is less favorable, because aquifer drawdown can reduce the working life of submersible installations and raise annual replacement demand. That means drought is supporting near-term equipment sales while also creating a harder operating environment for some pump assets.

Subsidized Government Pump Financing Programs

Government-backed credit programs are reducing the adoption barrier for irrigation systems, and this remains one of the most direct demand supports for the South America irrigation pumps market. Under Brazil’s Programa Nacional de Irrigação Sustentável (PRONISAF), family farmers can access credit from BRL 40,000 to BRL 250,000 (USD 7,920 to USD 49,500) at annual rates of 2.5% to 3% with repayment terms of up to 10 years for integrated irrigation, water, and energy solutions[3]Source: News Agency of the Government of the State of São Paulo, “The Irriga+ program expands access to credit with subsidized interest rates for rural producers,” agenciasp.sp.gov.br. Banco do Nordeste do Brasil is also supporting irrigation through the FNE Irrigação line, while São Paulo’s Irriga+ SP program is widening access to subsidized credit for farms of different sizes. These mechanisms matter because they convert interest from farmers into executed purchases, especially where energy integration and water-saving systems raise upfront system cost. They also favor suppliers that can package equipment, financing support, and installation guidance together. As a result, the South America irrigation pumps market is seeing some share pressure on suppliers that compete only on standalone pump pricing.

Solar and Hybrid Pumping Adoption on Off-Grid Farms

Solar and hybrid pumping are becoming more practical across remote agricultural areas, and this is opening a new demand layer for the South America irrigation pumps market beyond conventional electric and diesel systems. Peru’s Fondo de Cooperación para el Desarrollo Social (FONCODES) deployed 324 photovoltaic modules in highland communities in Puno, supporting year-round irrigation at elevations close to 4,000 meters and showing that solar-linked water systems can work under difficult field conditions. In Brazil, public financing programs now explicitly include renewable energy integration, which is helping solar pumping move from a niche solution into a standard technology option for eligible users. This shift is important because solar-ready systems often require controllers, variable frequency drives, storage, and monitoring components in addition to the pump itself. That lifts the bill of materials and broadens the revenue pool for suppliers with a systems approach. The South America irrigation pumps market is therefore gaining value from the wider equipment stack around each installation, not only from pump unit volumes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront capital costs | -1.5% | Colombia, Bolivia, Ecuador, and Northeast Brazil | Short term (≤ 2 years) to Medium term (2-4 years) |

| Rural grid limitations constraining electric pump deployment | -0.8% | Peru, Brazil, Bolivia, and Paraguay | Medium term (2-4 years) |

| Basin configuration and hydrology constraints | -0.6% | Chile, Peru, and Argentina | Long term (≥ 4 years) |

| Water-right allocation and regulatory barriers | -0.5% | Brazil, Peru, and Chile | Medium term (2-4 years) to Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Capital Costs

High capital cost remains a clear brake on demand, especially where growers need high-head borehole systems or larger centrifugal units and do not qualify for subsidized financing. In practical terms, the issue is strongest for smallholders and medium farms in Colombia and Argentina, where pump investment often competes with working capital needs and seasonal cash flow pressure. The South America irrigation pumps market therefore does not convert all latent demand into purchases, even when water stress makes irrigation more necessary. This funding gap is less severe in parts of Brazil, where public credit programs are more developed, but it still limits adoption where borrowers exceed concessional program thresholds or cannot provide the supporting structure required by lenders. The result is a tiered regional pattern in which larger commercial farms upgrade sooner while smaller operators delay replacement and postpone new installations. That imbalance slows the broadening of the customer base even as demand from large farms remains resilient.

Rural Grid Limitations Constraining Electric Pump Deployment

Grid-electric pumps were the largest power source segment in 2025, yet the practical reach of that segment is being capped by uneven rural electricity access and reliability in interior and highland zones. Communities in Peru’s highlands and other remote farming areas often lack stable supply, which is one reason off-grid solar-linked systems are gaining traction in the first place. For operators lifting groundwater from deep wells or moving water across difficult terrain, power interruption can create crop risk that exceeds the direct value of the pump asset itself. That makes reliability, not just access cost, a deciding factor in equipment choice. The South America irrigation pumps market is therefore supporting a parallel niche for hybrid systems that retain diesel or storage backup even when farms are moving away from fully diesel operations. Manufacturers that can design controllers compatible with multiple power inputs should remain better positioned in these areas than firms offering only standard electric packages.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Centrifugal Pumps Dominate Installed Base, While Displacement Pumps Grow Faster

Centrifugal pumps held the largest market share at 49.9% in 2025, and that leadership reflects their fit with the surface irrigation systems and canal-linked layouts used across large grain and sugarcane areas in Brazil and Argentina. In the South America irrigation pumps market, end-suction and split-case centrifugal models remain the standard choice where high volumes and horizontal delivery matter more than compact installation. Vertical turbine units also hold an important place in Peru’s coastal irrigation projects because those systems often need water lifted from river intakes or aquifers into canal networks. Submersible pumps are gaining use where groundwater development is expanding, especially in Peru’s valleys and in drier parts of northeastern Brazil. Vortex pumps remain smaller in volume, but they retain relevance where water carries sediment and basic surface units face operating limits.

The South America irrigation pumps market size for positive displacement pumps is projected to grow at a 5.2% CAGR through 2031, making them the fastest product category over the forecast period. That growth is tied to fertigation, drip systems, and subsurface irrigation layouts where accurate flow control matters more than bulk transfer. Peru approved irrigation projects across 15 regions in 2025 with a technified irrigation focus, which supports demand for pump types suited to controlled application systems. Positive displacement equipment is also benefiting from export-oriented horticulture in Peru and Chile, where water efficiency supports the case for higher-value irrigation hardware. The South America irrigation pumps industry is therefore seeing faster growth in applications where water delivery precision is closely linked to crop quality and fertilizer management. International Organization for Standardization (ISO) 9906 compliance is also becoming more relevant in projects that favor certified hydraulic performance, which gives larger suppliers an advantage in specification-heavy tenders.

By Power Source: Grid-Electric Pumps Remain the Largest Base While Solar Systems Set the Pace for New Adoption

Grid-electric pumps held the largest market share at 68.5% in 2025, supported by the concentration of large commercial irrigation in areas where power infrastructure is comparatively mature, including central-west Brazil, the Pampas in Argentina, and Chile’s Central Valley. In the South America irrigation pumps market, that installed base still gives grid-connected systems an advantage in established farming corridors with predictable pumping schedules and manageable electricity tariffs. Diesel pumps remain important in remote locations and in backup roles, but their long-term position is under pressure from rising fuel costs and from cleaner energy alternatives. Hybrid systems are also gaining acceptance because they reduce operating risk in places where full solar deployment is not always practical. This keeps the power source segment more diverse than a simple shift from one technology to another would suggest.

The South America irrigation pumps market size for solar pumps is projected to advance at a 9.2% CAGR through 2031, which makes solar the fastest power source category. Brazil’s PRONISAF structure explicitly includes solar integration for irrigation projects, and that policy support is helping normalize solar pumping within financed system packages. A further change is that local controller and drive adaptation is reducing dependence on imported sub-assemblies and making system economics more workable for end users. The South America irrigation pumps industry is therefore moving beyond single-component selling toward energy-linked packages that combine the pump, controls, storage, and service support. That is expanding opportunity for vertically integrated suppliers while raising execution demands on smaller distributors.

Geography Analysis

Brazil held the largest share at 46% in 2025, and that position reflects the scale of irrigated farming across the Cerrado, MATOPIBA, the São Francisco Valley, and parts of the Northeast. Brazil also benefits from a mature route to market, which gives the South America irrigation pumps market its deepest distribution base and the broadest service coverage in the region. In May 2025, the federal government approved BRL 491.3 million (USD 85 million) to double pumping capacity on the São Francisco River Eixo Norte from 24.75 cubic meters per second to 49 cubic meters per second, widening the long-term requirement for pumping infrastructure and related maintenance. Public financing support is also stronger in Brazil than in many neighboring markets, which helps commercial operators and some smaller farms move forward with equipment purchases. These factors keep Brazil central to regional pump demand even as energy mix and system design continue to change.

Peru is the fastest country segment, and the South America irrigation pumps market size for Peru is projected to grow at a 5.1% CAGR through 2031. Peru also advanced the release of major irrigation projects including Chavimochic III, Chinecas, Iruro, Majes Siguas, and Alto Piura, which together reinforce long-term demand for high-head centrifugal and vertical turbine equipment. Peru’s project mix matters because specification requirements are tighter than in many routine farm replacement purchases, which raises the role of certified multinational suppliers in large tenders.

Argentina remains the second-largest country market in volume terms because soybean and corn production continue to support irrigation demand in the Pampas, even though farm finances still limit the timing of upgrades in some areas. Chile remains a smaller but important specialty market where viticulture and fruit production support demand for drip-compatible centrifugal and displacement systems. Colombia and the rest of South America contribute lower individual country shares, but together they generate meaningful demand for submersible and small centrifugal pumps in cooperative and smallholder irrigation schemes. The South America irrigation pumps market therefore shows clear concentration in Brazil and Peru for scale and project activity, while the rest of the region adds breadth through a wider mix of smaller applications. That mix supports both multinational manufacturers with specification strength and regional suppliers that can deliver short lead times and local service.

Competitive Landscape

The South America irrigation pumps market is moderately fragmented, with a leading group of multinational original equipment manufacturers and a second layer of regional firms competing across price, specification, and service depth. KSB SE & Co. KGaA, Grundfos Holding A/S, Xylem Inc., Franklin Electric Co., Inc., Sulzer Ltd., and EBARA Corporation are among the established names active across the region’s agricultural and water infrastructure applications. The larger multinational suppliers retain an edge in projects that require proven hydraulic performance, energy efficiency, and engineering support. Regional manufacturers, including Hidromecânica Germek Ltda. before its acquisition, have remained relevant where standardized product lines, local customization, and delivery speed matter most. This keeps the competitive field active across both premium and volume-driven categories.

Consolidation is becoming more visible and is narrowing the number of independent distribution platforms available to large suppliers. Franklin Electric Co. Inc. signed a definitive agreement in February 2025 to acquire Barnes de Colombia S.A., adding manufacturing, assembly, and warehousing capacity across several South American markets. EBARA Corporation also expanded through back-to-back deals, first acquiring Asanvil S.A. in Uruguay in December 2024 and then completing the acquisition of Hidromecânica Germek Ltda. in January 2026, strengthening its footprint in south-central South America and in Brazilian agricultural pump applications. These moves show that market access and service reach are becoming as important as product specification in winning business. They also suggest that larger companies want direct control over regional channels rather than relying only on third-party distributors.

The next competitive shift is likely to center on integrated controls, solar compatibility, and remote monitoring rather than on pump hardware alone. Patent activity and product direction among larger suppliers point to closer integration between pumps, inverters, and solar controller logic, which can simplify installation and reduce system cost in off-grid agriculture. Sulzer Ltd. opened a third rotating equipment service center in Argentina in July 2025, which shows how service capacity is becoming part of competitive positioning rather than a support function alone. Local manufacturers still hold defensible positions where non-standard fabrication, field service, and shorter lead times are important. Even so, the South America irrigation pumps market is rewarding suppliers that can combine packaged systems, technical support, and stronger regional operating coverage.

South America Irrigation Pumps Industry Leaders

Franklin Electric Co., Inc.

KSB SE & Co. KGaA

Grundfos Holding A/S

Xylem Inc.

EBARA Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: EBARA Corporation completed 100% equity acquisition of Hidromecânica Germek Ltda., a São Paulo State-based manufacturer of pump units for fire fighting and agriculture, following an equity transfer agreement signed in October 2025. The acquisition extends EBARA's customized pump unit capabilities in Brazil and strengthens its position in the South American agricultural pump segment as part of the E-Plan 2025 medium-term management strategy and long-term E-Vision 2030 roadmap.

- May 2025: Brazil's federal government, under the Novo PAC program, approved BRL 491.3 million (USD 85 million) for the doubling of pumping capacity on the São Francisco River Eixo Norte, increasing volumetric delivery from 24.75 cubic meters per second to 49 cubic meters per second and expanding supply coverage to 8.1 million beneficiaries across Pernambuco, Ceará, Paraíba, and Rio Grande do Norte.

- February 2025: Franklin Electric Co. Inc. signed a definitive agreement to acquire Barnes de Colombia S.A., adding 2 manufacturing facilities and a foundry in Colombia plus assembly operations in Brazil and Argentina, along with warehouse facilities in Ecuador, Peru, Chile, Guatemala, and Panama. The transaction materially expanded Franklin Electric Co. Inc.'s manufacturing footprint and distribution network across key South American markets.

South America Irrigation Pumps Market Report Scope

An irrigation pump is a mechanical device used to draw water from a source, such as a well, river, or pond, and move it under pressure to agricultural fields. It powers watering systems like sprinklers, drips, or canals to provide crops with a controlled and consistent water supply.

The South America Irrigation Pumps Market Report is Segmented by Product Typem(Centrifugal Pumps, Submersible Pumps, Positive Displacement Pumps, and Vortex Pumps), by Power Source (Grid-Electric Pumps, Diesel Pumps, Solar Pumps, and Hybrid Solar-Diesel and Solar-Battery Pumps), and by Geography (Brazil, Argentina, Chile, Peru, Colombia, and Rest of South America). The Market Forecasts are Provided in Terms of Value (USD).

| Centrifugal Pumps |

| Submersible Pumps |

| Positive Displacement Pumps |

| Vortex Pumps |

| Grid-electric Pumps |

| Diesel Pumps |

| Solar Pumps |

| Hybrid Solar-Diesel and Solar-Battery Pumps |

| Brazil |

| Argentina |

| Chile |

| Peru |

| Colombia |

| Rest of South America |

| By Product Type | Centrifugal Pumps |

| Submersible Pumps | |

| Positive Displacement Pumps | |

| Vortex Pumps | |

| By Power Source | Grid-electric Pumps |

| Diesel Pumps | |

| Solar Pumps | |

| Hybrid Solar-Diesel and Solar-Battery Pumps | |

| By Geography | Brazil |

| Argentina | |

| Chile | |

| Peru | |

| Colombia | |

| Rest of South America |

Key Questions Answered in the Report

What is the current size of the South America irrigation pumps sector?

It was valued at USD 4.52 billion in 2025 and is estimated at USD 4.85 billion in 2026, with expansion to USD 6.87 billion by 2031.

What is driving pump demand across South America?

The main demand drivers are irrigation network expansion, recurring drought pressure, subsidized financing, and faster adoption of solar and hybrid pumping systems.

Which product type leads demand in 2025?

Centrifugal pumps are the largest product segment, holding 49.9% of revenue in 2025 because they fit large surface and canal irrigation systems.

Which power source is growing the fastest through 2031?

Solar pumps are the fastest-growing power source, with a forecast CAGR of 9.2% as off-grid farms shift away from fully diesel-based systems.

Which country offers the strongest growth outlook?

Peru shows the fastest outlook at a 5.1% CAGR through 2031, supported by a USD 24 billion irrigation project portfolio and continued project unlocking.

How competitive is the supplier landscape?

Competition is moderate to high. Large multinational manufacturers lead in certified and engineered applications, while local and regional firms remain relevant in standardized agricultural segments.

Page last updated on: