Australia Irrigation Machinery Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

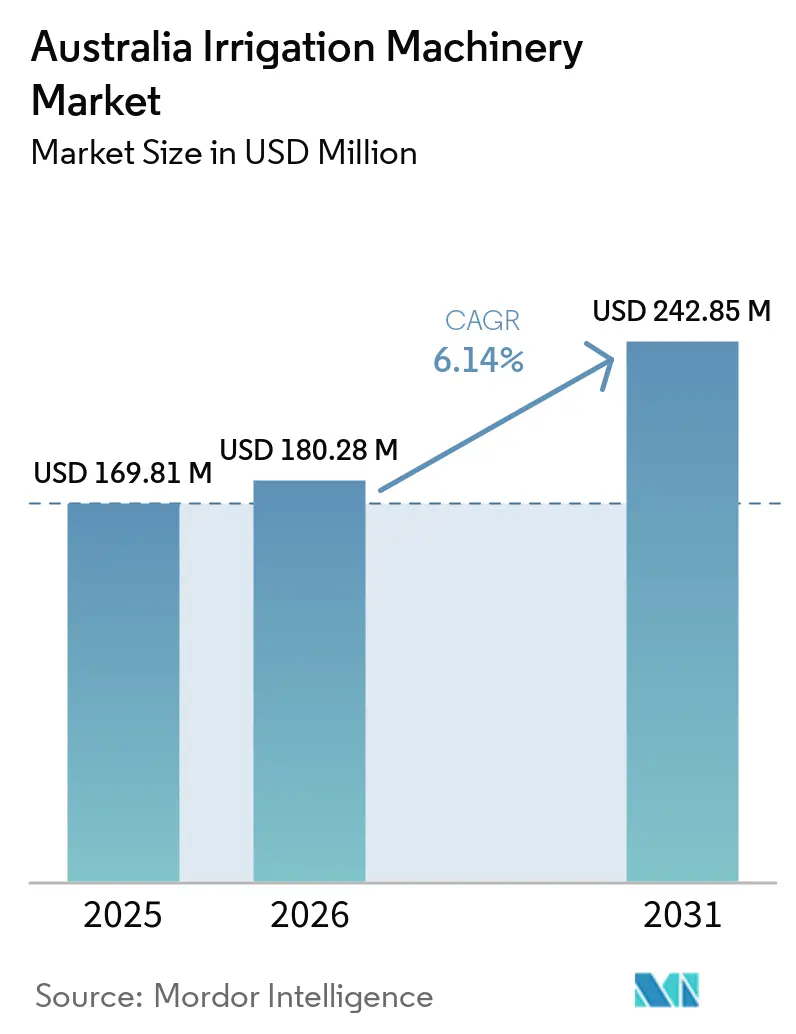

| Base Year Market Size (2025) | USD 169.81 Million |

| Market Size (2026) | USD 180.28 Million |

| Market Size (2031) | USD 242.85 Million |

| Growth Rate (2026 - 2031) | 6.14% CAGR |

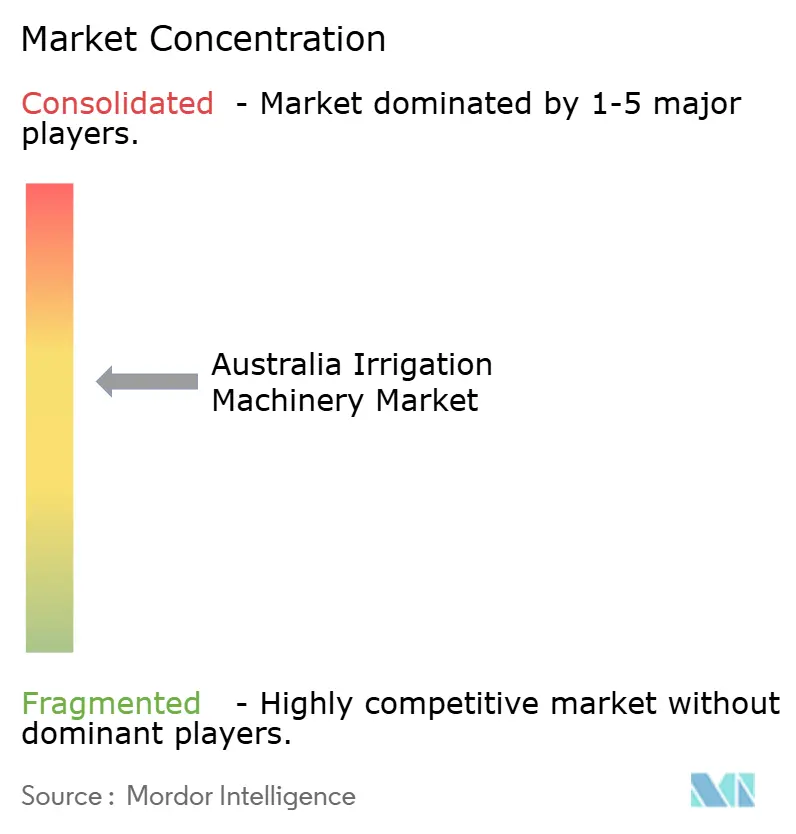

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Australia Irrigation Machinery Market Analysis by Mordor Intelligence

The Australia irrigation machinery market size is anticipated to grow from USD 169.81 million in 2025 to USD 180.28 million in 2026 and is forecast to reach USD 242.85 million by 2031 at 6.14% CAGR over 2026-2031. Agriculture used 74% of Australia’s total fresh water supply in 2021-22, which keeps irrigation equipment close to essential capital spending for growers across the main farming belts in the east and south[1]Source: Australian Bureau of Agricultural and Resource Economics and Sciences, “Snapshot of Australian Agriculture 2025,” agriculture.gov.au. The industry is being shaped by tighter water allocations, the continued shift away from gravity-fed systems, and stronger demand from export-oriented horticulture for precise, reliable water delivery. Compliance activity in the Murray-Darling Basin (MDB) is also supporting purchases of telemetry-ready meters, control hardware, and related system upgrades that do not depend only on seasonal farm income. This gives the market a more stable replacement and upgrade cycle than many farm equipment categories, even when crop prices soften. It also leaves room for suppliers to combine water-delivery hardware with automation, fertigation, and remote monitoring in a practical package.

Key Report Takeaways

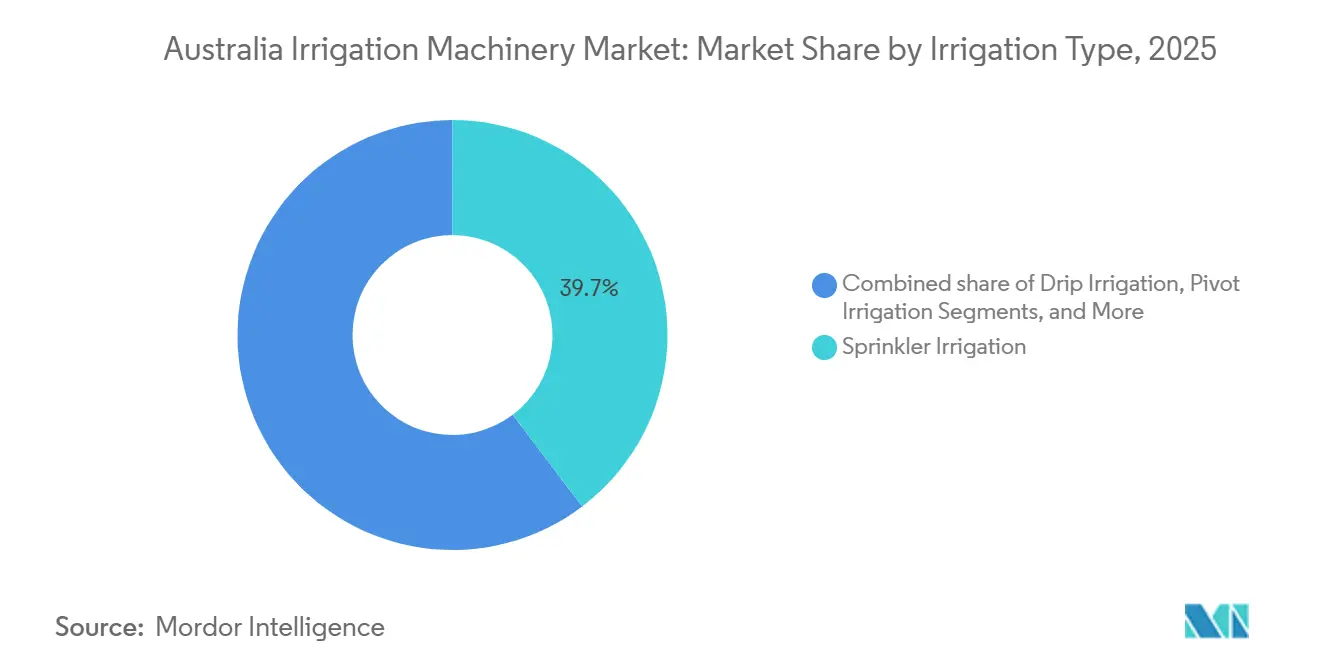

- By irrigation type, sprinkler irrigation was the largest segment, and accounted for 39.7% of Australia irrigation machinery market size in 2025, while drip irrigation is forecast to be the fastest-growing segment, expanding at a 8.3% CAGR over 2026-2031.

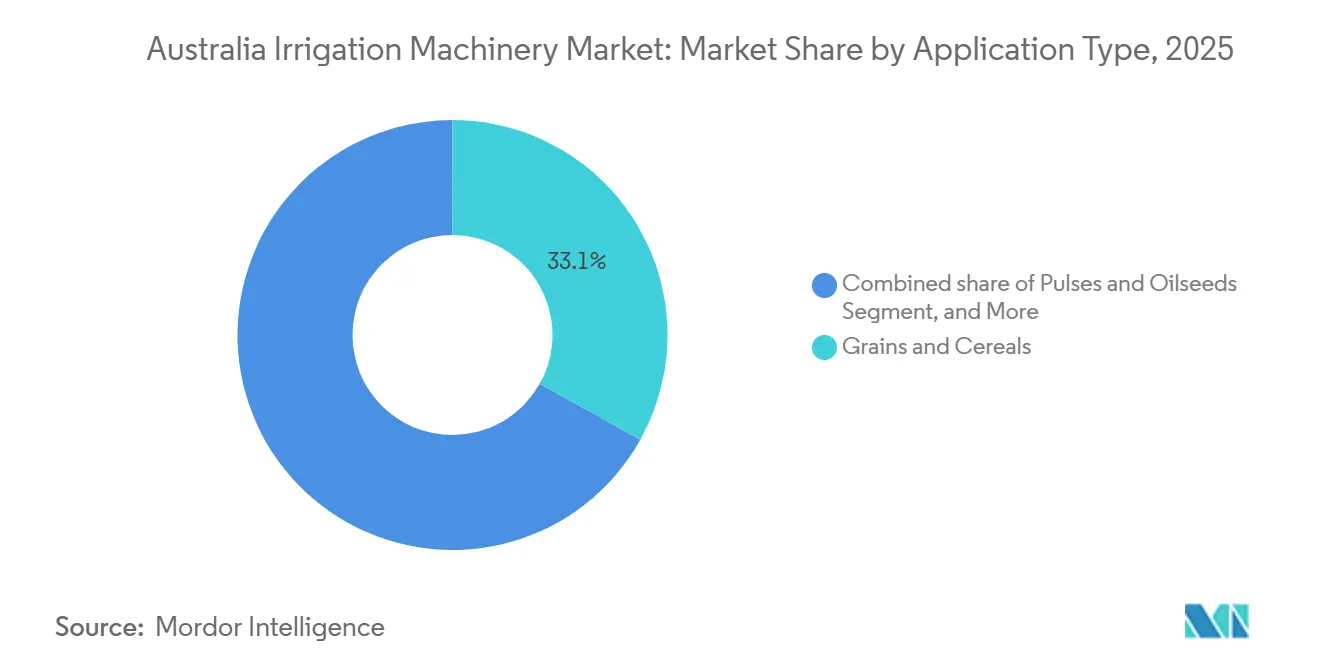

- By application type, grains and cereals were the largest segment with 33.1% of Australia irrigation machinery market share in 2025, while fruits and vegetables are the fastest segment and forecast to expand at 9.1% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Australia Irrigation Machinery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Water-scarcity-led irrigation upgrades | +1.50% | National, with the strongest pull in NSW, Victoria, and Queensland where water access and system efficiency are central to farm planning | Medium term (2-4 years) |

| Government irrigation efficiency incentives | +1.00% | National, with concentrated support in Queensland, NSW, and Victoria through rebate and financing programs | Short term (≤ 2 years) |

| Export horticulture and permanent crop expansion | +1.30% | NSW, Victoria, South Australia, and Queensland where orchard and horticulture investment is expanding installed drip demand | Medium term (2-4 years) |

| Labour scarcity driving automation | +0.90% | National, with stronger relevance in broadacre and horticulture regions facing labor and technical skill shortages | Medium term (2-4 years) |

| Reef runoff compliance retrofits in Queensland Cane | +0.30% | Queensland, especially reef catchments where water quality rules are encouraging irrigation efficiency upgrades | Short term (≤ 2 years) |

| Murray-Darling network digitalisation spillover | +0.40% | Murray-Darling Basin states including NSW, Victoria, South Australia, and Queensland where meter and telemetry rollout is expanding compatible on-farm demand | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Water-Scarcity-Led Irrigation Upgrades

Water scarcity remains a key driver of the shift toward replacing and modernizing irrigation systems. The Australian Bureau of Statistics (ABS) reported agricultural water consumption of 11,760 gigalitres in 2023-24, while Murray-Darling Basin storages were at 77% of accessible capacity in the same reporting cycle. In response, growers are moving further toward efficient systems, and drip irrigation had already reached 75% of the permanently planted area in the Lower Murray-Darling by 2024, while surface irrigation had fallen below 1% in that same planted base. This shift is changing not only the volume of equipment sold, but also the type of equipment that farms now specify. The Australian irrigation machinery market is therefore seeing stronger demand for systems that can combine water application with sensors, software, and telemetry needed for tighter water management.

Government Irrigation Efficiency Incentives

Government support is lowering the effective cost of system upgrades and is helping the Australia irrigation machinery market convert postponed purchases into current orders. In November 2025, the Queensland Government launched a 15% discount on irrigation water costs, backed by USD 32.2 million (AUD 51 million) over 2 years, with the program administered by the Queensland Rural and Industry Development Authority (QRIDA) through December 2027[2]Source: Queensland Ministerial Media Statements, “Crisafulli Government Delivers Cost Relief for Irrigators,” statements.qld.gov.au. QRIDA also approved USD 62.3 million (AUD 100 million) in sustainability and productivity enhancement loans in 2024-25, including irrigation infrastructure. The Australian Government’s On-Farm Connectivity Program committed USD 33.4 million (AUD 53 million) across 2 rounds and delivered rebates to more than 1,300 producers, with a third round scheduled in the second half of 2026. This matters because support is now helping farmers fund the digital layer that makes smart irrigation practical, which supports broader technology adoption in the country.

Export Horticulture and Permanent Crop Expansion

Export-oriented horticulture is driving demand for equipment and increasing system complexity nationwide. Hort Innovation reported a record farmgate production value of USD 12.1 billion in the year to June 2025, with output of 6.9 million metric tons of fruit, vegetables, and nuts. Horticulture exports also reached USD 2.2 billion (AUD 3.5 billion) in fiscal year 2025 and are anticipated to exceed USD 2.8 billion (AUD 4.4 billion) in fiscal year 2026[3]Source: Hort Innovation, “Australia’s Horticulture Exports Surge to Record-Breaking AUD 3.5 Billion,” horticulture.com.au. In 2025, almond orchards in Australia had 99% adoption of drip irrigation, and many growers were already using climate data with plant- and soil-based sensors for irrigation scheduling. The market benefits because permanent crops usually need tighter pressure control, fertigation compatibility, and better monitoring than broadacre grain systems.

Labour Scarcity Driving Automation

Labor pressure is pushing growers to buy systems that reduce manual irrigation work, which is lifting automation content in the market. The Australian Agritech Association reported in March 2025 that 45% of agritech companies that needed horticulturalists could not fill those roles in 2024, with similar shortages for engineers and field technicians. Remote valve control, automated scheduling, and sensor-based responses reduce field visits and lower the number of repetitive irrigation tasks on the farm. In a 2025 case study near Mildura, Water Dynamics supported a citrus grower using 90 fully automated valves and 21 soil moisture probes with support from the On-Farm Connectivity Program. As a result, the Australia irrigation machinery market is shifting toward integrated packages that combine hardware, controls, and connectivity rather than stand-alone irrigation components.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront capex for pressurized systems | -1.10% | National, with the greatest pressure on small and mid-scale farms where upfront financing remains difficult | Medium term (2-4 years) |

| Water entitlement and allocation volatility | -0.70% | Murray-Darling Basin states, especially NSW and Victoria where water availability and pricing shape investment timing | Long term (≥ 4 years) |

| Rural connectivity gaps for smart irrigation | -0.50% | Remote and peri-regional areas across Queensland, Western Australia, and South Australia where data coverage is uneven | Medium term (2-4 years) |

| Installer and service technician bottlenecks | -0.40% | Regional Australia, with stronger friction in inland Queensland, western NSW, and the Northern Territory | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Upfront Capex for Pressurised Systems

High upfront costs remain one of the clearest limits to adoption, as drip and center-pivot systems can cost 3 to 5 times more per hectare than gravity-fed alternatives, stretching payback periods beyond the planning horizons used by many growers. Queensland Rural and Industry Development Authority data showed that approved applications under the Horticultural Irrigation Pricing Rebate Scheme declined from 666 in 2023-24 to 628 in 2024-25 despite available funding. New South Wales also continued to offer the Drought Ready and Resilient Fund loan program in 2025, with loans up to USD 315,000 (AUD 500,000) per borrower, but access to financing still depends on borrower eligibility and security conditions[4]Source: New South Wales Government, “Drought Ready and Resilient Fund Loan,” nsw.gov.au. The Australia irrigation machinery market, therefore, still depends heavily on rebates, concessional finance, and strong farm cash flow when pressurized systems are involved.

Water Entitlement and Allocation Volatility

Water entitlement risk reduces investment certainty and remains a structural restraint for the Australia irrigation machinery market. Murray-Darling Basin accessible storages declined from 93% to 77% between June 2023 and June 2024, while Victorian Murray allocation prices exceeded AUD 340/ML in October 2025. Uncertainty surrounding future water availability and allocation costs makes growers more cautious about committing capital to irrigation infrastructure, particularly projects with long payback periods. The Basin Plan review scheduled for 2026 continues to create uncertainty for permanent crop producers that rely on secure water access to justify major irrigation investments. As a result, water entitlement and allocation volatility can delay irrigation machinery purchases, postpone system upgrades, and slow the development of new irrigation projects, even though the long-term demand for water-efficient irrigation technologies remains strong.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Irrigation Type: Drip Systems Reshape Permanent Crop Infrastructure

Sprinkler irrigation was the largest irrigation type, and held 39.7% of the Australia irrigation machinery market share in 2025. Its broad position reflects demand from grain, pasture, and vegetable farms that need flexible coverage across wide production areas. Center pivot and lateral move systems remain central in Murray-Darling Basin broadacre zones because large paddocks make mechanized movement cost-effective for growers. Pivot irrigation also plays a clear role in cotton and cereal districts in NSW and Queensland, where automated coverage across large areas supports labor and water management needs. This makes sprinkler equipment the main installed base in broadacre agriculture in Australia.

Drip irrigation is the fastest irrigation type and is forecast to grow at a 8.3% CAGR over 2026-2031 in the Australia irrigation machinery market. By 2024, drip irrigation had already reached 75% of the permanently planted area in the Lower Murray-Darling, which shows how far orchards and similar crops have already moved toward precise water delivery. Growth from here is tied not only to more hectares, but also to higher system specifications, including filters, pressure regulators, emitters, fertigation equipment, and soil moisture monitoring. Antelco Pty Ltd added new products in 2026, including the SPEC Drip self-piercing emitter in May 2026 and the CETA Dripper in April 2026, demonstrating active product development to address serviceability and installation needs in permanent crops. The Australia irrigation machinery industry is therefore seeing a stronger move toward complete drip packages rather than simple component replacement alone.

By Application Type: Horticulture Export Premium Lifts Equipment Specification

Grains and cereals were the largest application segment and accounted for 33.1% of the Australia irrigation machinery market size in 2025. This position is supported by the large broadacre footprint in the Murray-Darling Basin, where New South Wales surface water take alone reached 6,559 gigalitres in 2023-24. Demand in this application usually centers on center pivot systems, lateral move equipment, and high-volume sprinkler components with long operating lives. Replacement cycles in grains and cereals are often shaped by aging equipment, efficiency targets, and compliance requirements rather than by rapid growth in planted area. This keeps the broadacre side of the industry steady and important, even as horticulture becomes more technically demanding.

Fruits and vegetables are the fastest application segment and are projected to expand at 9.1% CAGR over 2026-2031. Horticulture exports reached USD 2.2 billion (AUD 3.5 billion) in fiscal year 2025 and are anticipated to exceed USD 2.8 billion (AUD 4.4 billion) in fiscal year 2026, supporting continued investment in higher-performing irrigation systems. The United States Department of Agriculture Foreign Agricultural Service (USDA FAS) projected orange production at 590,000 metric tons and mandarin production at 270,000 metric tons in marketing year 2025-26, both of which support reliable demand for precise irrigation scheduling. Rural Research and Development Corporation noted in 2025 that 19% of almond orchards had not yet reached bearing age, which leaves a committed forward pipeline for drip system installation and optimization. The Australia irrigation machinery industry gains here because export horticulture typically demands stronger irrigation precision, better nutrient delivery control, and more active monitoring than staple crop systems.

Geography Analysis

New South Wales (NSW) was the largest state market in the Australia irrigation machinery market, supported by agricultural water consumption of 4,679 gigalitres in 2023-24, which accounted for 39.8% of national agricultural water use. The state combines broadacre irrigation in the Murray-Darling Basin with major permanent horticulture zones in the Murray Valley and Riverina. That mix supports both sprinkler systems for grains and cotton and drip systems for almonds, citrus, and wine grapes. The depth of installed irrigation infrastructure also keeps replacement demand active as farms move from older equipment to more efficient, connected systems. For this reason, NSW remains the broad base of the Australia irrigation machinery market even as newer growth pockets emerge elsewhere.

Victoria remains a major state, combining a mature installed base with ongoing modernization in northern irrigation districts. Agricultural water consumption in Victoria increased by 29.3% to 2,666 gigalitres in 2023-24, and the Mallee Catchment Management Authority reported that pressurized systems reached 98% of the irrigable area in the Mallee and Goulburn-Murray districts by 2024. The West Gippsland Catchment Management Authority offered irrigation efficiency rebates of up to USD 6,300 (AUD 10,000) per farm plan in February 2026, which supports continued system improvement. Victoria’s demand is helped by permanent horticulture and by practical upgrades that improve metering, control, and water-use efficiency. This keeps the state important for suppliers that need a mix of replacement work and premium horticulture demand.

Queensland is the fastest-growing state in the Australia irrigation machinery market over 2026-2031 because subsidy support, compliance needs, and crop mix are all moving in the same direction. The Queensland Government introduced a USD 32.2 million (AUD 51 million) Irrigation Pricing Rebate Scheme in November 2025, while Reefwise Farming support is also directing funds toward irrigation efficiency in the reef catchments. Broadacre cotton modernization and sugarcane water management are adding to this demand, especially where labor-saving and water productivity have become more important. Tasmania also recorded a 78.2% increase in agricultural water consumption to 481 gigalitres in 2023-24, suggesting rising irrigation intensity from a smaller base. South Australia and Western Australia remain medium-growth markets with narrower but stable demand bases, while the Northern Territory and the Australian Capital Territory stay limited in scale within the overall irrigation machinery market in the country.

Competitive Landscape

The Australia irrigation machinery market is moderately consolidated, with Netafim Ltd., Valmont Industries, Inc., Rivulis Irrigation Limited, Lindsay Corporation, and Rubicon Water Ltd. as the key players. Competition is shaped by dealer reach, crop-specific design, installation support, and the ability to combine hardware with digital monitoring tools. Global suppliers of drip and micro-irrigation compete strongly in permanent horticulture, where precision water control and fertigation management matter most. Large mechanized systems for broadacre farming remain concentrated around established brands with strong pivot and linear move capabilities. In this setting, differentiation increasingly comes from service quality, software compatibility, and system integration rather than from basic hardware alone.

Several strategic moves in 2025 and 2026 show how vendors are sharpening that position in the Australia irrigation machinery market. In May 2026, Antelco Pty Ltd launched the SPEC Drip Self-Piercing Emitter Compensating dripper, while in April 2026, it also introduced the CETA Dripper with a take-apart design to simplify maintenance in orchard and vine settings. In January 2026, Hunter Industries, Inc. introduced the i-Wob2 Part-Circle sprinkler under its Senninger brand, expanding its low-intensity application offering for pivot towers and hose boom uses. In September 2025, Netafim Australia worked with dealer Irripro to deploy UniRam dripline at Stibbards Creek Macadamias in northern New South Wales, pairing product supply with local technical agronomy support. These moves show that competition in the Australia irrigation machinery market now depends on both product innovation and on-farm service depth.

White space remains meaningful in solar-assisted pumping, fertigation-ready drip packages, and telemetry-compatible control equipment for farms connected to regulated water systems. Domestic specialists still have room where local manufacturing, installer familiarity, and service response matter more than global scale. In July 2024, Rivulis Irrigation Limited (Temasek Holdings) announced a strategic partnership with Phytech to connect Rivulis’s Observant precision irrigation platform with a wider digital farming stack. That step matters because the Australia irrigation machinery market is moving toward connected operating systems rather than isolated irrigation hardware. Suppliers that can support the full chain from hardware to agronomy-linked data use are likely to hold a stronger position as upgrade cycles continue.

Australia Irrigation Machinery Industry Leaders

Netafim Ltd. (Orbia Advance Corporation)

Valmont Industries, Inc. (Valley Irrigation)

Lindsay Corporation

Rivulis Irrigation Limited (Temasek Holdings)

Rubicon Water Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Antelco Pty Ltd launched the SPEC Drip Self-Piercing Emitter Compensating dripper, a new Australian-made pressure-compensating emitter designed for uniform flow performance and simplified installation in tree and vine crop applications.

- January 2026: Hunter Industries, Inc. introduced the i-Wob2 Part-Circle sprinkler under its Senninger brand, completing the i-Wob2 product family. The device uses a patent-pending Hydrofoil multi-trajectory deflector for low-intensity water application at pivot towers and hose boom applications.

- November 2025: Queensland’s Crisafulli Government launched the Irrigation Pricing Rebate Scheme, committing USD 32.20 million (AUD 51 million) over 2 years to deliver a 15% water cost discount for owner-operated irrigation businesses, administered by QRIDA with applications open until December 31, 2027

Australia Irrigation Machinery Market Report Scope

The Australia irrigation machinery market covers equipment used to apply, control, measure, and optimize water delivery in agricultural production across irrigated farming systems. It includes sprinkler, drip, and pivot irrigation, and related control and monitoring equipment used across broadacre crops, horticulture, and other irrigated applications in Australia.

The Australia Irrigation Machinery Market is segmented by irrigation type (sprinkler, drip, pivot, and other types) and by application type (grains and cereals, pulses and oilseeds, fruits and vegetables, and other applications). Forecasts are provided in terms of value (USD).

| Sprinkler Irrigation | Pumping Unit |

| Tubing | |

| Couplers | |

| Spray or Sprinkler Heads | |

| Fittings and Accessories | |

| Sensors | |

| Controllers | |

| Injectors | |

| Flow Meters | |

| Drip Irrigation | Valves |

| Backflow Preventers | |

| Pressure Regulators | |

| Filters | |

| Emitters | |

| Tubing | |

| Other Drip Irrigation Components | |

| Pivot Irrigation | |

| Other Irrigation Types |

| Grains and Cereals |

| Pulses and Oilseeds |

| Fruits and Vegetables |

| Other Applications |

| By Irrigation Type | Sprinkler Irrigation | Pumping Unit |

| Tubing | ||

| Couplers | ||

| Spray or Sprinkler Heads | ||

| Fittings and Accessories | ||

| Sensors | ||

| Controllers | ||

| Injectors | ||

| Flow Meters | ||

| Drip Irrigation | Valves | |

| Backflow Preventers | ||

| Pressure Regulators | ||

| Filters | ||

| Emitters | ||

| Tubing | ||

| Other Drip Irrigation Components | ||

| Pivot Irrigation | ||

| Other Irrigation Types | ||

| By Application Type | Grains and Cereals | |

| Pulses and Oilseeds | ||

| Fruits and Vegetables | ||

| Other Applications | ||

Key Questions Answered in the Report

What is the projected value and growth rate of the Australia irrigation machinery market by 2031?

The Australia irrigation machinery market is projected to reach USD 242.85 million by 2031 while growing at 6.14% CAGR over 2026-2031.

Which irrigation type is the largest in Australia?

Sprinkler irrigation was the largest irrigation type in 2025 with a 39.7% revenue share, supported by broad use across grains, pasture, and vegetable production.

Which application is growing the fastest in Australia?

Fruits and vegetables is the fastest application segment, with projected growth of 9.1% CAGR over 2026-2031 as export horticulture expands and permanent crop irrigation becomes more precise.

Why is Queensland anticipated to grow faster than other states?

Queensland benefits from the 2025 irrigation pricing rebate scheme, reef-related efficiency spending, and crop-specific modernization in sugarcane and cotton.

What is pushing growers toward drip and smart irrigation systems?

Water scarcity, compliance-linked metering upgrades, labor shortages, and the need for precise irrigation in horticulture are all pushing farms toward drip, automation, and sensor-linked systems.

Page last updated on: