Smart Irrigation Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

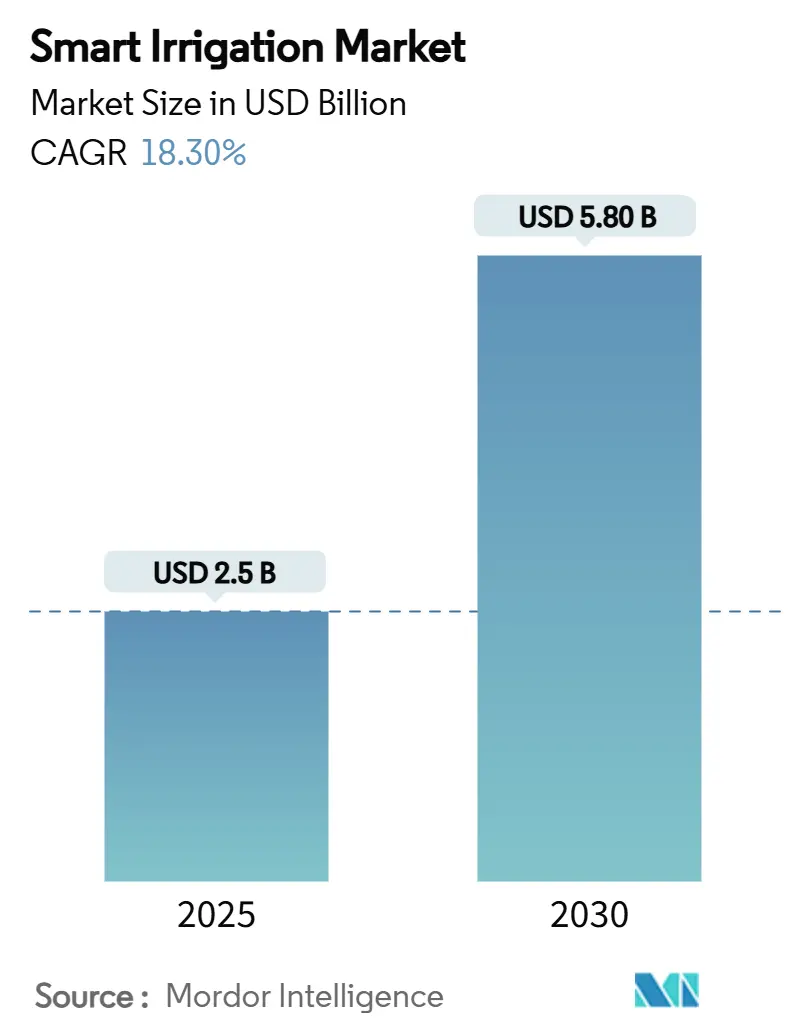

| Market Size (2025) | USD 2.5 Billion |

| Market Size (2030) | USD 5.80 Billion |

| Growth Rate (2025 - 2030) | 18.30% CAGR |

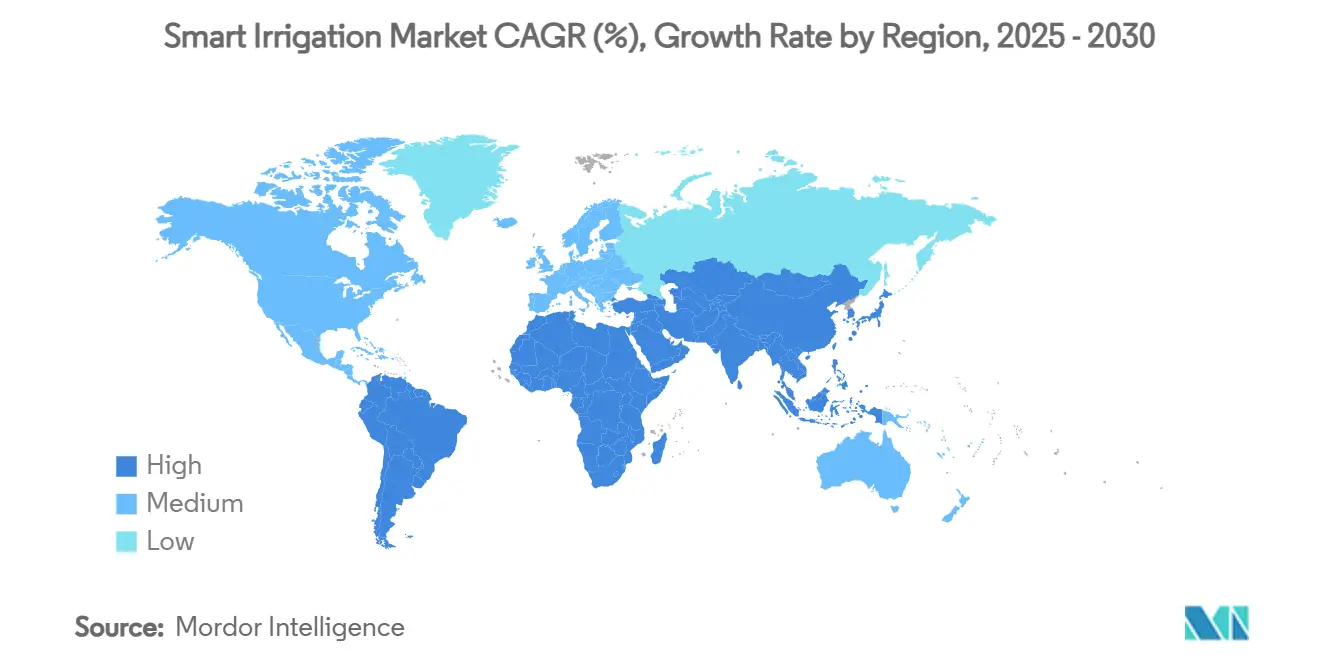

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Smart Irrigation Market Analysis by Mordor Intelligence

The smart irrigation market size is estimated at USD 2.5 billion in 2025, and is projected to reach USD 5.8 billion by 2030, at a CAGR of 18.30% during the forecast period. Water-scarcity policies, rapid sensor innovation, and service-based business models are converging to accelerate technology roll-out across farm and landscape settings. State-level regulations in California that mandate annual water budgets, the European Union’s Water Reuse Regulation, and the United States Environmental Protection Agency’s infrastructure outlays are together creating an enforceable framework that favors data-driven irrigation equipment[1]Source: California State Water Resources Control Board, “Urban Water Use Objective: Adopted Regulations,” waterboards.ca.gov. Agricultural growers seeking stable crop yields during weather uncertainties, turf managers following municipal water restrictions, and financial institutions valuing water-efficiency carbon credits drive market demand. Technology suppliers are responding with integrated platforms that combine soil-moisture probes, satellite evapotranspiration feeds, and AI scheduling engines, which lower operating costs and boost return on investment. The competitive field, therefore, rewards companies that offer open, cyber-secure architectures and service subscriptions that minimize up-front capital outlays for smallholder farmers.

Key Report Takeaways

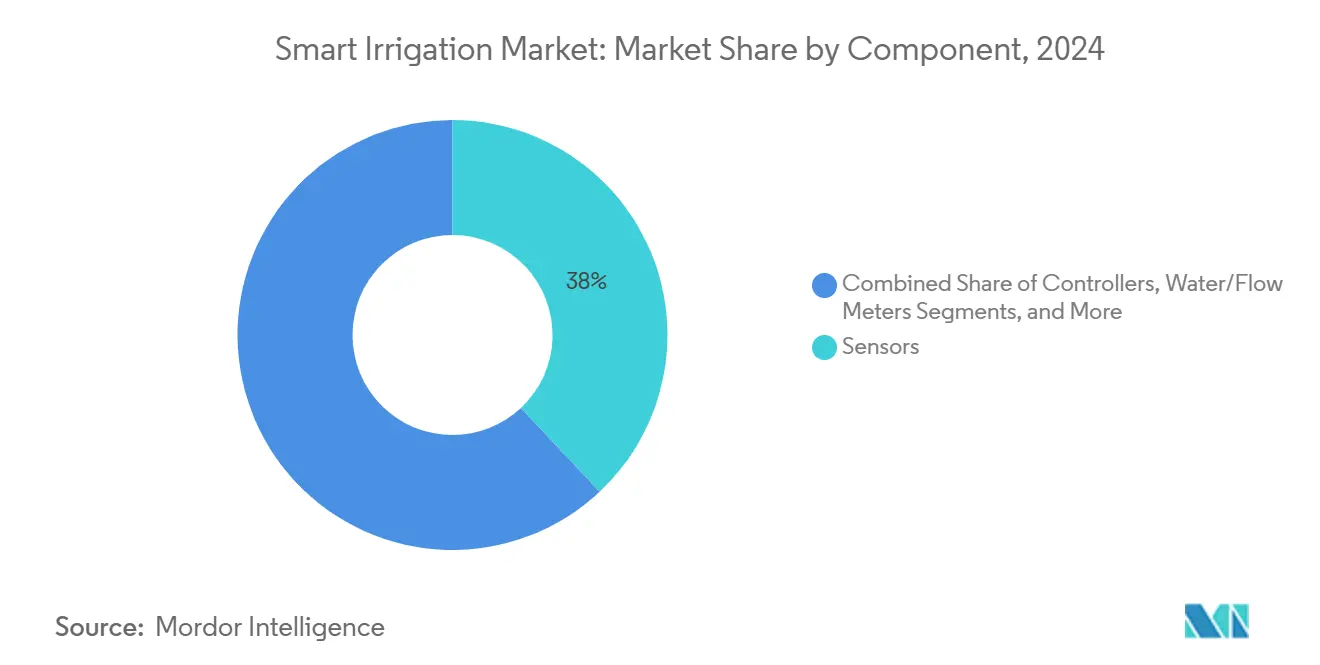

- By component, sensors held 38% of the smart irrigation market share in 2024, while soil-moisture sensors are forecast to grow at 21.4% CAGR through 2030.

- By system type, sensor-based systems captured 56% revenue share of the smart irrigation market size in 2024 and are projected to expand at 19.8% CAGR to 2030.

- By application, agriculture accounted for 62% of the smart irrigation market demand in 2024, and the greenhouse automation is set to rise at a 20.3% CAGR to 2030.

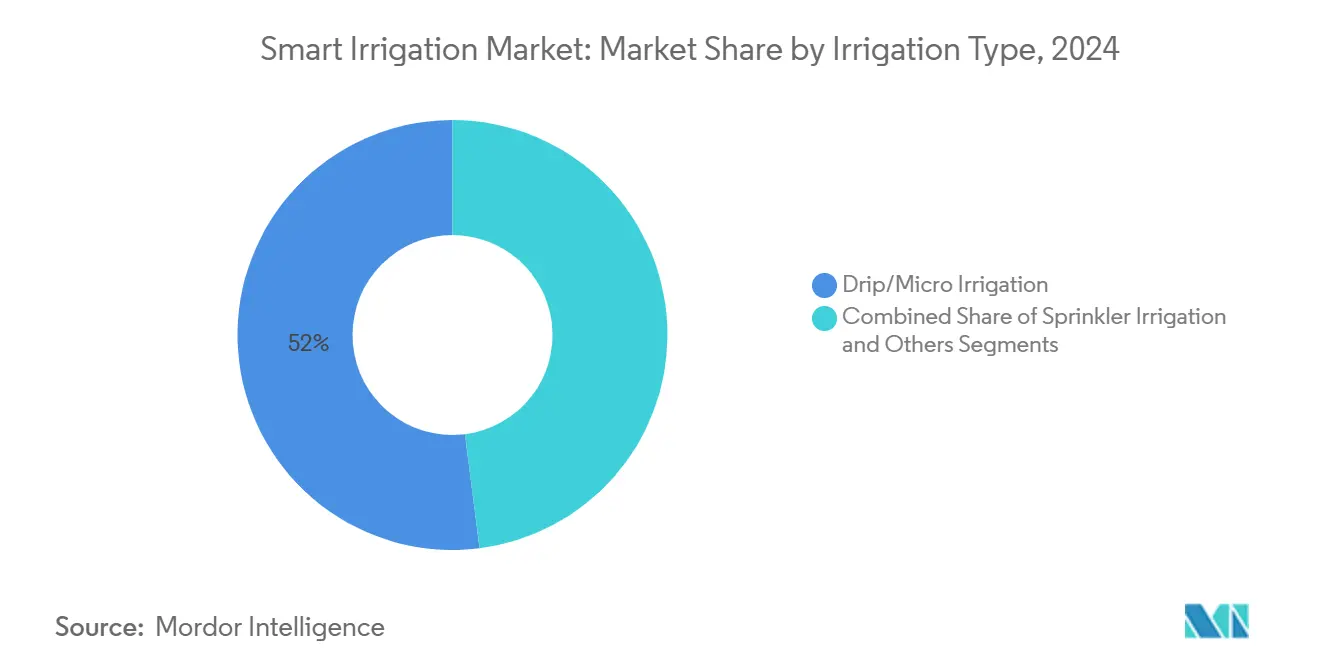

- By irrigation type, drip and micro-irrigation recorded 52% of the smart irrigation market size in 2024, while subsurface drip irrigation is anticipated to advance at a 20% CAGR through 2030.

- By geography, North America led with a 45% share of the smart irrigation market in 2024, and Asia-Pacific represents the fastest-growing region at 19.2% CAGR to 2030.

- The Toro Company, Rain Bird Corporation, Lindsay Corporation, Valmont Industries, Inc., and Netafim (Orbia) together commanded 45.2% combined market share in 2024.

Global Smart Irrigation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government water-use regulations and subsidies | +4.2% | Global, with strongest impact in North America and EU | Medium term (2-4 years) |

| Rapid adoption of IoT sensors and cloud analytics | +3.8% | Global, with Asia-Pacific leading adoption velocity | Short term (≤ 2 years) |

| Rising demand for high-value horticulture and turf management | +2.9% | North America, Europe, with expansion to Asia-Pacific urban centers | Medium term (2-4 years) |

| Satellite-driven evapotranspiration scheduling adoption | +2.1% | Global, with early deployment in water-stressed regions | Long term (≥ 4 years) |

| Emergence of irrigation-as-a-service business models | +1.8% | Asia-Pacific core, spill-over to Middle East and Africa, and South America | Medium term (2-4 years) |

| Carbon-credit monetization for water-efficient farming | +1.4% | Global, with regulatory frameworks developing in EU and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government Water-Use Regulations and Subsidies

Policy mandates such as California’s permanent landscape budgeting rules and the EU Water Reuse Regulation compel utilities and growers to adopt precision controllers, sensors, and compliant distribution hardware. Federal guidelines under 18 CFR 806.25 specify site-specific irrigation design, effectively displacing conventional flood practices. Similar frameworks in the United Kingdom’s Greater Cambridge program aim for a 20% cut in municipal water demand by 2038. Financial incentives widen technology access, the United States Environmental Protection Agency is channeling USD 50 billion toward modern water infrastructure that includes smart irrigation upgrades, while the European Parliament’s 2025 Water Resilience Strategy links irrigation efficiency directly to agricultural carbon programs. These aligned regulations are embedding smart irrigation procurement criteria in water-stressed regions[2]Source: European Commission, “Water Reuse Regulation (EU) 2020/741,” ec.europa.eu.

Rapid Adoption of IoT Sensors and Cloud Analytics

Bluetooth-low-energy probes, narrowband IoT modules, and cloud dashboards enable real-time scheduling that reduces water use by up to 30% without yield penalties. Low-power wide-area networks and 5G backhaul now transmit high-resolution soil data every five minutes, a cadence that was impractical two years ago. Cloud platforms consolidate sensor feeds with localized weather forecasts and satellite imagery, generating prescription maps delivered to valve controllers in seconds. Edge-enabled firmware cuts latency and ensures continued operation during outages, an advantage for remote ranches in Australia and the western United States[3]Source: United States Department of Agriculture Agricultural Research Service, “ISSCADA Variable Rate Irrigation Research,” ars.usda.gov.

Rising Demand for High-Value Horticulture and Turf Management

Premium greenhouse vegetables, ornamentals, and golf course turf tolerate little deviation from optimal moisture levels, creating demand for sensor density far above that required in commodity row crops. Wireless networks inside poly-covered structures relay temperature, humidity, carbon dioxide, and soil-water data to AI controllers that modulate misting and fertigation valves. Research on hybrid bermudagrass indicates that autonomous irrigation can maintain professional-grade turf quality while reducing water consumption by 25% compared to timer-based systems by 2025. Controlled-environment agriculture operators are layering atmospheric water harvesters and superabsorbent polymers with drip lines to form closed-loop systems that cut external withdrawals. Those high-margin end markets raise the spending ceiling for integrated smart irrigation suites.

Satellite-Driven Evapotranspiration Scheduling Adoption

Platforms such as OpenET combine Landsat, Sentinel, and ECOSTRESS data with surface energy balance models to estimate field-scale evapotranspiration daily. Validation studies in Nevada’s Diamond Valley show a 7% deviation from meter readings, giving regulators and growers confidence to issue water credits and schedule irrigation remotely. Variable rate pivots now ingest evapotranspiration layers to adjust application within a single rotation, resulting in 90% application efficiency on high-value alfalfa acreage. The United States Department of Agriculture is testing sensor-satellite fusion through its Supervisory Control and Data Acquisition (ISSCADA) project across four states to improve crop water productivity under drought declarations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront capital cost for small farmers | -2.8% | Global, with acute impact in Sub-Saharan Africa and South Asia | Medium term (2-4 years) |

| Limited technical skills and awareness in emerging markets | -2.1% | Asia-Pacific developing regions, Sub-Saharan Africa, South America | Long term (≥ 4 years) |

| Cybersecurity risks in connected irrigation controllers | -1.4% | Global, with heightened concerns in North America and EU | Short term (≤ 2 years) |

| Lack of open data standards for device interoperability | -1.2% | Global, affecting system integration and scalability | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Capital Cost for Small Farmers

Even as sensor prices decline, a full eight-hectare deployment of probes, weather stations, a controller, and a solar pump can equal the annual income of a Kenyan smallholder. In 2025, the studies in Mozambique and Zimbabwe highlight a cycle whereby low-value crops and limited financing keep irrigation schemes underutilized. Leasing models pioneered by Jain Irrigation now bundle equipment, agronomic support, and software into multi-year service contracts, shifting the spend from capital to operating budgets. Pay-as-you-grow platforms that charge per liter delivered are emerging around India’s PM-KUSUM solar pump subsidy, yet scale remains constrained by mobile-money penetration and credit scoring challenges.

Limited Technical Skills and Awareness in Emerging Markets

Surveyed growers in Indonesia and the Philippines cite uncertainty over sensor calibration and controller programming as primary deterrents. Regional extension centers are therefore embedding digital agriculture curricula into vocational programs, with Brazil’s Semear Digital Center reporting 40% average yield gains among trainees who adopted data-driven irrigation. Development agencies now pair equipment grants with multi-season coaching, an approach that has doubled the retention rates of smart irrigation systems versus equipment-only interventions[4]Source: Empresa Brasileira de Pesquisa Agropecuária (Embrapa), “Digital Agriculture Capacity Building,” embrapa.br.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Sensors Underpin the Data Layer While Software Value Grows

Sensor suites delivered 38% of the smart irrigation market share in 2024 and remain indispensable because they translate field conditions into actionable data. Soil-moisture probes, tensiometers, and dielectric sensors are reaching 21.4% CAGR on the strength of multi-depth, Bluetooth-enabled designs that cut installation time. Controllers followed with a 35% share as growers rely on algorithmic decision engines to automate pump and valve sequences. Water and flow meters round out the hardware stack, providing compliance records for regulators and off-take verification for carbon credit issuance. Software and services, though smaller today, are achieving double-digit growth as subscription dashboards deliver analytics and predictive maintenance alarms.

Growing preference for integrated kits is fostering joint ventures between sensor manufacturers and analytics firms. Netafim’s 2025 alliance with Sentek brings high-resolution moisture profiles into the NetBeat platform, allowing variable fertigation by root-zone depth. Edge computing modules attached to probes now preprocess raw voltages, sending only actionable thresholds to the cloud, which lowers bandwidth by 70% and ensures resilience when cellular coverage lapses. Taken together, these advances demonstrate how sensors have evolved from discrete components to intelligent nodes within an orchestrated platform, a trend that will continue to dominate the smart irrigation market.

By System Type: Sensor-Based Architectures Take Center Stage

Sensor-centric architectures accounted for 56% of the revenue share in the smart irrigation market in 2024, highlighting growers' preference for detailed field data. With a projected CAGR of 19.8%, their installed base is expected to more than double by 2030. Weather-based systems held a 44% share, providing a cost-effective option through evapotranspiration programs that utilize external weather stations. Hybrid offerings that fuse in-field moisture data with on-site climatic readings are emerging as the performance leader under highly variable weather patterns.

Machine-learning algorithms embedded in sensor firmware are pushing predictive accuracy toward agronomist-grade recommendations while freeing operators from manual data interpretation. Weather-linked controllers, once limited to evapotranspiration estimates, now integrate satellite-derived rainfall gain factors that localize irrigation runtime down to individual zones. Development teams are also prioritizing cybersecurity hardening with secure boot loaders and encrypted firmware updates to mitigate intrusion risks identified by the Institute of Electrical and Electronics Engineers (IEEE) research. As a result, system choice is increasingly dictated by data richness, integration openness, and security posture rather than by initial hardware cost, positioning sensor-based suites for sustained dominance within the smart irrigation market.

By Application: Agriculture Commands Volume as Greenhouse Builds Momentum

Agriculture accounted for 62% of the 2024 smart irrigation market share, underpinned by open-field cereal, oilseed, and specialty crop acreage that rely on drip laterals and pivot sprinklers. The segment’s vast scale ensures a base level of demand regardless of commodity price cycles. Within that volume, greenhouse cultivation is forecast to expand at a 20.3% CAGR as controlled-environment farms leverage nutrient film and fogging systems that respond in seconds to sensor triggers. Non-agricultural settings, including municipal parks, sports turf, and residential landscapes, supply a steady 38% share but act as early adopters of consumer-grade smart controllers, which later migrate to commercial agriculture once proven.

Greenhouse operators prioritize full-stack control, integrating irrigation with climate, lighting, and CO₂ enrichment to maximize photosynthetic efficiency. Multi-parametric sensors detect fine fluctuations in vapor pressure deficit, prompting micro-pulse irrigation that preserves fruit quality. Turf managers at golf courses employ soil-moisture grids to target irrigation only where needed, meeting stringent municipal water allotments. Homeowners are attracted to app-based systems that connect with smart speakers and weather Application Programming Interface's (APIs), a convergence that is nudging consumer expectations upward and influencing feature roadmaps across the entire smart irrigation market.

By Irrigation Type: Drip Leads Precision Delivery While Subsurface Systems Accelerate

Drip/Micro irrigation lines generated 52% of the market share in 2024, owing to their water efficiency and compatibility with sensor-triggered on-off cycles. Subsurface drip systems are emerging at a 20% CAGR because below-ground emitters curtail evaporation and reduce disease pressure on leaf surfaces. Sprinkler and center-pivot formats maintain relevance through upgrades like variable rate nozzles that adjust flow in real time according to soil texture maps derived from electromagnetic surveys.

IoT-enabled drip lines now feature pressure monitoring every 10 meters, flagging clogging before yield impact occurs. Smart valves modulate pressure differentials throughout long laterals, achieving uniform distribution even on undulating terrain. Subsurface drip kits combine geomembranes and root-intrusion barriers to secure longevity, a factor critical for perennial orchards where replacement downtime is unacceptable. Sprinkler makers are incorporating shape memory alloys in heads that adapt arc and radius dynamically, ensuring that landscape edges receive the correct dose. The steady infusion of sensors and actuators across all irrigation types underscores the technology’s trajectory from passive plumbing to responsive, data-driven infrastructure within the smart irrigation market.

Geography Analysis

North America preserved the leading 45% revenue position in 2024 and continues to scale installations under federal infrastructure grants that reimburse utilities for smart controller rebates. California’s budgeting rules oblige urban suppliers to enforce consumption limits, a dynamic that pulls manufacturers, dealers, and certified installers into a robust regional ecosystem. The United States Department of Agriculture’s Conservation Innovation Grants further subsidize sensor deployments on row-crop acreage, boosting adoption across the Corn Belt. Canada mirrors these trends through provincial water stewardship programs and collaborations with agronomic research stations that validate smart irrigation benefits across canola and pulse crops.

Asia-Pacific represents the fastest growth vector at a 19.2% CAGR to 2030 as governments channel digital agriculture funds toward smallholder modernization. China’s Ministry of Agriculture champions sensor-based fertigation trials across protected tomato and pepper houses, while India’s Pradhan Mantri Kisan Urja Suraksha evam Utthan Mahabhiyan (PM-KUSUM) scheme couples solar pumps with mobile-managed drip kits that qualify for a 60% subsidy. Japan and South Korea leverage robotics and edge-AI controllers to mitigate labor shortages in aging rural communities. Australia’s Murray-Darling Basin growers integrate satellite evapotranspiration layers into variable-rate pivots to improve water allocations, demonstrating how arid zones accelerate best-practice adoption.

Europe maintains a steady expansion path driven by the EU Water Reuse Regulation, Water Framework Directive, and Common Agricultural Policy eco-schemes that reward verified irrigation savings. Mediterranean vineyards incorporate subsurface drip to combat prolonged droughts, and the Dutch greenhouse clusters push sensor density to extreme levels for predictive crop steering. The United Kingdom’s water scarcity initiatives in Greater Cambridge showcase urban pilots that link smart meters, landscape controllers, and nature-based recharge zones. Middle East and Africa, while smaller in absolute value, exhibit sharp uptake in high-tech drip and pivot systems as Gulf states and Israel export knowledge into arid African markets under food security partnerships.

Competitive Landscape

The market remains moderately fragmented, with the five largest firms accounting for only 45.2% of combined revenue in 2024, providing significant opportunities for specialists and new entrants. The Toro Company topped the chart with a significant share through an array of residential and commercial controllers, sensors, and drip lines. Rain Bird Corporation, leveraging brand equity and global distribution. Valmont Industries, Inc. and Lindsay Corporation blend hardware with telematics on center-pivot platforms, while Netafim Ltd. (Orbia Advance Corporation, S.A.B. de C.V.)’s agronomic advisory service underpins its drip leadership.

Consolidation appears mostly in strategic technology acquisitions rather than large-scale mergers. Valmont’s 2025 unification of four digital platforms into AgSense 365 exemplifies a move to improve user experience and customer retention. Rain Bird’s purchase of solar-powered controller start-up OtO broadens its homeowner portfolio and shortens innovation cycles. The Toro Company’s acquisition of Xiamen Xiangfeng strengthens cost competitiveness in micro-irrigation manufacturing. Start-ups such as Irrigreen and CropX secure venture funding by targeting robotics and sensor analytics niches, introducing competitive tension that pushes incumbents to accelerate R&D.

Suppliers now prioritize software and subscription revenues over one-time hardware sales. Service contracts that bundle monitoring, crop consulting, and carbon credit verification expand gross margins and lock in customers. Firms also differentiate through cybersecurity certifications as farms become recognized attack surfaces. Satellite partnerships, evidenced by Netafim Ltd. (Orbia Advance Corporation, S.A.B. de C.V.) linking with OpenET imagery, create data moats that are hard to replicate. Collectively, these dynamics indicate a contest where algorithm quality, platform openness, and service agility shape competitive advantage in the smart irrigation market.

Smart Irrigation Industry Leaders

The Toro Company

Rain Bird Corporation

Lindsay Corporation

Valmont Industries, Inc.

Netafim Ltd. (Orbia Advance Corporation, S.A.B. de C.V.)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Rain Bird Corporation acquired OtO Inc., a Toronto-based company specializing in solar-powered smart lawn care technology, expanding Rain Bird's homeowner automation offerings through OtO's app-controlled sprinkler systems.

- January 2025: Valmont Industries announced strategic consolidation of four irrigation management platforms into AgSense 365 app, streamlining technology offerings and enhancing user experience for precision irrigation management.

- November 2024: CropX launched sustainable irrigation technology initiatives in Australia and New Zealand, expanding precision agriculture capabilities and environmental sustainability programs.

- October 2024: Almanac and WiseConn announced a global strategic partnership to expand AI-enabled smart irrigation access for farmers, integrating DropControl systems with agricultural technology platforms.

Global Smart Irrigation Market Report Scope

| Controllers |

| Sensors |

| Water/Flow Meters |

| Software and Services |

| Weather-based Systems |

| Sensor-based Systems |

| Agriculture | Greenhouses |

| Open-field Crops | |

| Non-Agriculture | Residential Lawns and Gardens |

| Golf Courses | |

| Sports Turf and Public Parks |

| Drip/Micro Irrigation |

| Sprinkler Irrigation |

| Other Irrigation Types |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| Israel | |

| Rest of Middle East | |

| Africa | South Africa |

| Kenya | |

| Rest of Africa |

| By Component | Controllers | |

| Sensors | ||

| Water/Flow Meters | ||

| Software and Services | ||

| By System Type | Weather-based Systems | |

| Sensor-based Systems | ||

| By Application | Agriculture | Greenhouses |

| Open-field Crops | ||

| Non-Agriculture | Residential Lawns and Gardens | |

| Golf Courses | ||

| Sports Turf and Public Parks | ||

| By Irrigation Type | Drip/Micro Irrigation | |

| Sprinkler Irrigation | ||

| Other Irrigation Types | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| Israel | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Kenya | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current size of the smart irrigation market?

The smart irrigation market size stands at USD 2.5 billion in 2025 and is on course to reach USD 5.8 billion by 2030.

Which region leads the smart irrigation market?

North America leads, holding 45% revenue share in 2024 owing to supportive regulations and mature precision-agriculture infrastructure.

What component segment is growing the fastest?

Soil-moisture szensors are the fastest, expanding at a 21.4% CAGR through 2030 due to their critical data role in precision scheduling.

How fragmented is the competitive landscape?

The top five vendors control 45.2% of revenue, indicating moderate fragmentation with ample room for specialized entrants.

Why are greenhouse applications growing quickly?

Controlled-environment agriculture demands precise water and climate management, driving a 20.3% CAGR in greenhouse smart irrigation adoption.

How are small farmers overcoming high capital costs?

Irrigation-as-a-service contracts and government subsidies, such as India’s PM-KUSUM, reduce up-front expenses by converting equipment purchases into manageable operating fees.

Page last updated on: