Canada Irrigation Machinery Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

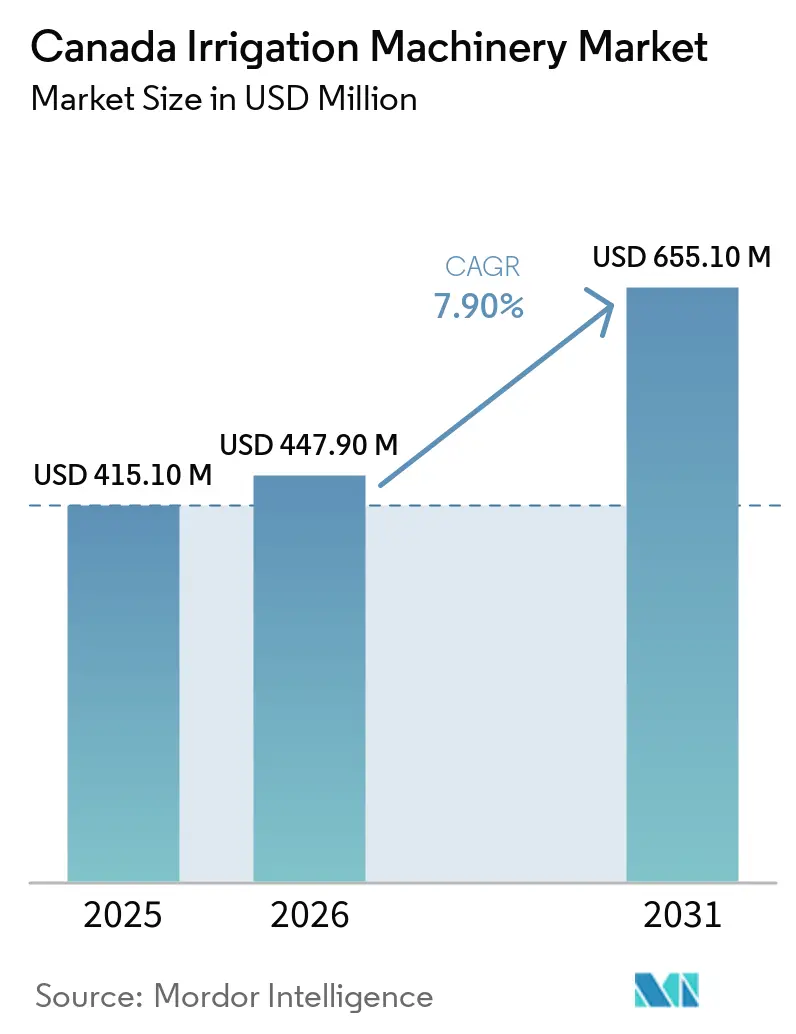

| Base Year Market Size (2025) | USD 415.10 Million |

| Market Size (2026) | USD 447.90 Million |

| Market Size (2031) | USD 655.10 Million |

| Growth Rate (2026 - 2031) | 7.90% CAGR |

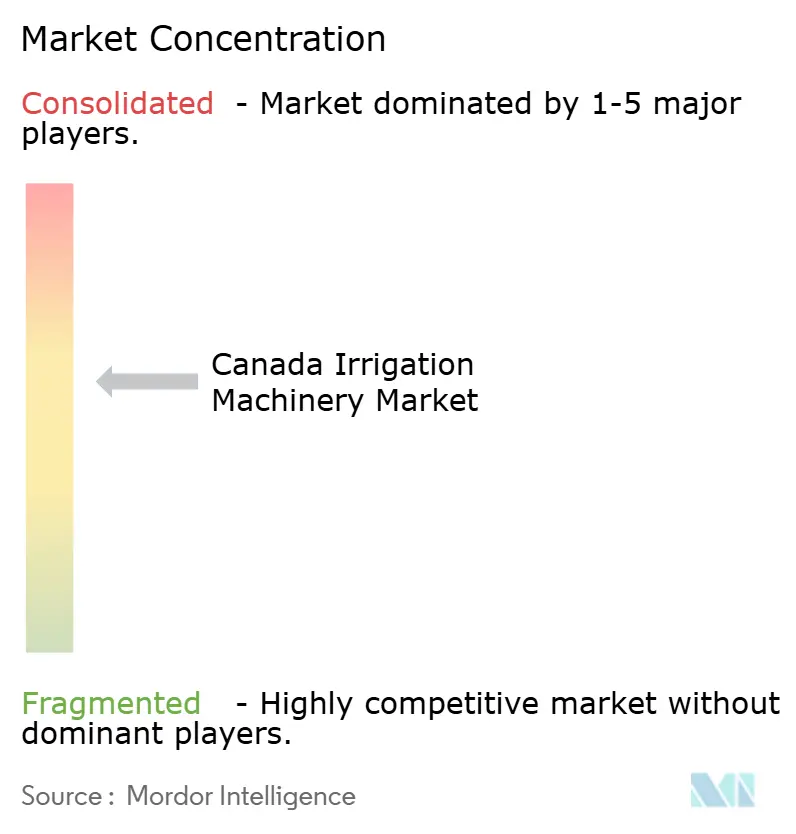

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Canada Irrigation Machinery Market Analysis by Mordor Intelligence

The Canada irrigation machinery market was valued at USD 415.10 million in 2025, and is forecasted to grow from USD 447.90 million in 2026 to USD 655.10 million by 2031, growing at a CAGR of 7.9% from 2026 to 2031. According to Statistics Canada, the expansion of irrigated acreage across the Prairies continues to drive the market, with the national irrigated area projected to reach 769,117 hectares in 2024, of which Alberta accounts for 74.3%. Drought conditions, particularly in Saskatchewan and Manitoba during spring 2025, have emphasized the importance of irrigation equipment as a critical production safeguard rather than a discretionary farm investment. Provincial support is contributing to shorter payback periods, while advancements in digital controls, sensor-linked systems, and greenhouse expansion are increasing the average system value and broadening market opportunities. Competition remains intense among global pivot and drip irrigation suppliers. However, channel differentiation is increasingly focused on software capabilities, system integration, and service execution, as growers demand solutions that enhance water use documentation and operational efficiency.

Key Report Takeaways

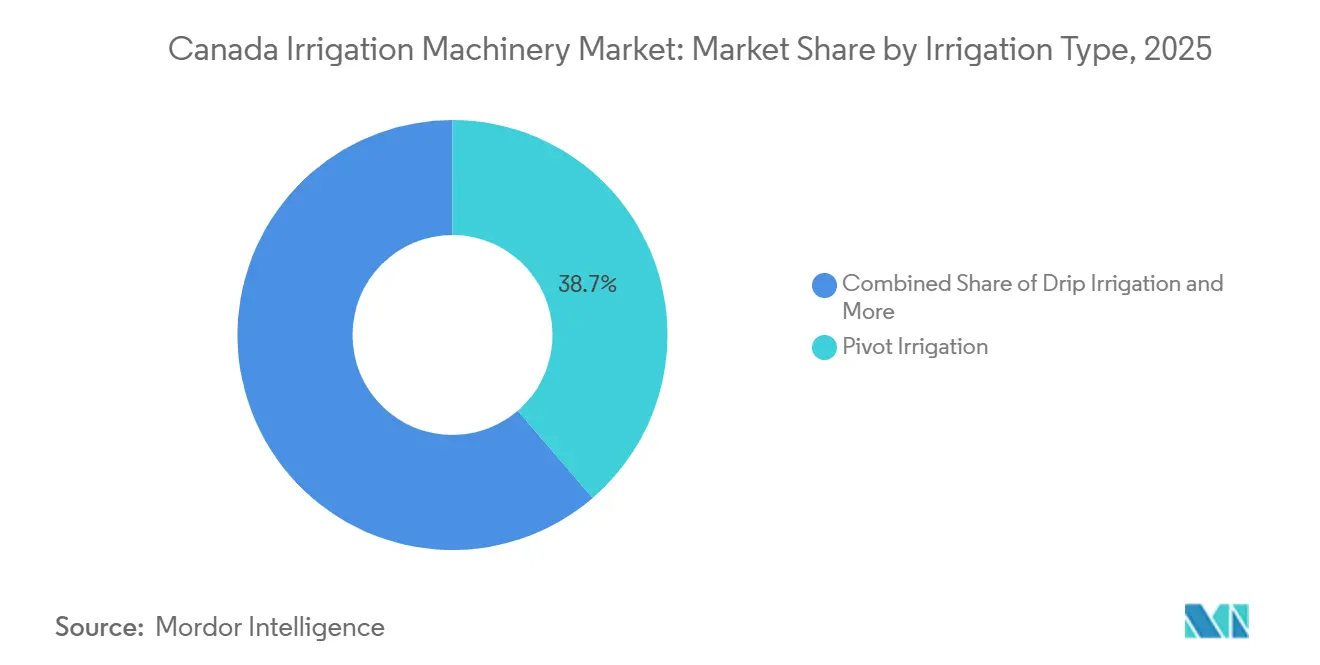

- By irrigation type, the Canada irrigation machinery market share for the pivot irrigation segment held the largest 38.7% in 2025, while the Canada irrigation machinery market size for the drip irrigation segment is forecast to grow at the fastest CAGR of 12.1% from 2026 to 2031.

- By application, the field crops segment accounted for the largest 58.5% share in 2025, while the fruits and vegetables segment is projected to grow at the fastest CAGR of 10.2% from 2026 to 2031.

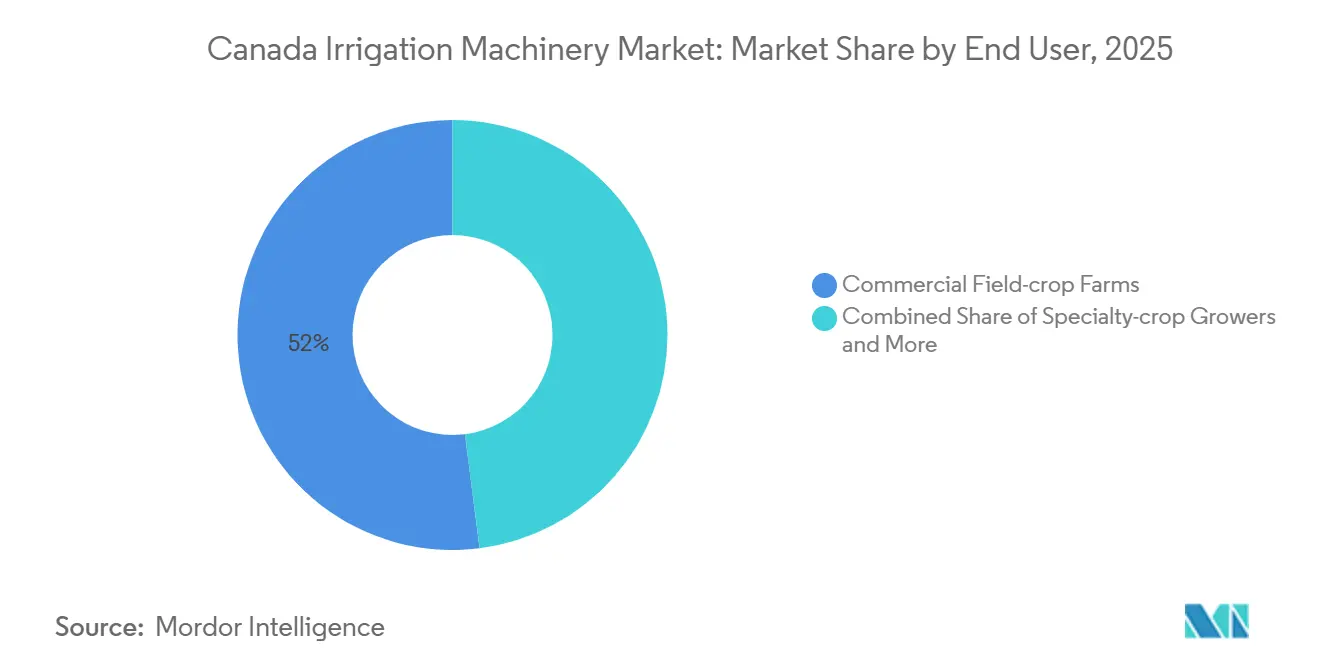

- By end user, the commercial field-crop farms segment held the largest 52.0% share in 2025, while the greenhouse and nursery operators segment is projected to grow the fastest CAGR of 10.6% from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Canada Irrigation Machinery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Prairie drought risk and irrigation intensity expansion | +1.8% | Alberta, Saskatchewan, and Manitoba | Short term (≤ 2 years) |

| Provincial cost-share funding for on-farm upgrades | +1.4% | National, with early gains in Alberta and Saskatchewan | Short term (≤ 2 years) |

| Precision irrigation digitization on large field-crop farms | +1.2% | Prairie core, Alberta and Saskatchewan | Medium term (2-4 years) |

| Specialty-crop and greenhouse water-efficiency adoption | +1.0% | Ontario, British Columbia, and Quebec | Medium term (2-4 years) |

| Retrofit demand from aging high-pressure pivot fleets | +0.9% | Alberta and Saskatchewan | Short term (≤ 2 years) |

| Water-quality monitoring needs favor sensor-linked systems | +0.7% | Global, with spill-over to British Columbia and Saskatchewan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Prairie Drought Risk and Irrigation Intensity Expansion

Persistent drought conditions across the Prairies remain a significant factor influencing the Canada irrigation machinery market. According to Environment and Climate Change Canada’s Spring 2025 drought outlook, severe and extreme drought conditions were reported in central Saskatchewan and west-central Manitoba, with some areas receiving less than 45% of the normal seasonal precipitation. These extended dry periods are driving increased reliance on irrigation systems to stabilize crop yields and mitigate production risks, thereby sustaining demand for irrigation machinery in Prairie farming regions[1]Source: National Integrated Drought Information System, “Prairies and High Plains Outlook – Spring 2025,” drought.gov..

Provincial Cost-Share Funding for On-Farm Upgrades

Provincial support programs are driving growth in the Canadian irrigation machinery market by alleviating the financial challenges of irrigation development projects. For instance, the Government of Saskatchewan's Irrigation Development Program, running through May 2025, covers the lesser of 67% of eligible costs or CAD 1,675 (USD 1,230) per irrigable acre developed, with a maximum limit of CAD 500,000 (USD 367,000) over the program's duration[2]Source: Government of Saskatchewan, “Irrigation Development Program,” saskatchewan.ca.. This funding support is fostering investments in new irrigation infrastructure and boosting demand for irrigation machinery and water management equipment within the province.

Precision Irrigation Digitization on Large Field-Crop Farms

The growing adoption of digital agriculture technologies on large farms is driving the expansion of the irrigation machinery market in Canada. According to a 2025 briefing published by Toronto Metropolitan University, farms with more than 5,000 acres reported 81% adoption of at least one digital agriculture tool, compared to 36% adoption among farms below 2,000 acres[3]Source: Toronto Metropolitan University, “Sustainable Agriculture Technology Adoption,” torontomu.ca.. This significant adoption rate among large-scale farms is fueling demand for precision irrigation systems equipped with advanced features such as remote monitoring, soil moisture sensing, and data-driven water management technologies. These systems enable farmers to optimize water usage, reduce waste, and improve overall crop productivity, further contributing to the market's growth.

Retrofit Demand from Aging High-Pressure Pivot Fleets

The increasing need for water quality and water use monitoring is driving the demand for advanced irrigation systems in the Canadian irrigation machinery market. In 2024, the Saskatchewan Water Security Agency initiated a satellite soil moisture monitoring pilot project in collaboration with Nave Analytics and Planet Labs. The project aims to assess irrigation volume estimation using satellite-based data. This initiative is fostering interest in sensor-integrated and data-driven irrigation technologies, which facilitate water-use measurement, reporting, and precision irrigation management in Canadian agricultural operations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront equipment and installation cost | -1.5% | National | Short term (≤ 2 years) |

| Water licensing and irrigation certification complexity | -0.8% | British Columbia, Saskatchewan, and Alberta | Medium term (2-4 years) |

| Shortage of irrigation technicians and control specialists | -0.6% | National, concentrated in Prairie provinces | Medium term (2-4 years) |

| Imported component exposure to tariff and resin volatility | -0.5% | National | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Upfront Equipment and Installation Cost

High upfront investment costs remain a significant barrier to growth in the Canada irrigation machinery market, particularly for small and medium-sized farming operations. The Westside Irrigation Rehabilitation Project (WIRP) Economic Analysis, published in 2024, estimated a total one-time capital expenditure of CAD 1.15 billion to develop approximately 90,000 irrigated acres in Saskatchewan. The substantial capital required for irrigation infrastructure, water delivery systems, and field equipment places financial strain on growers, hindering the adoption of advanced irrigation machinery across Canada, even as demand for irrigated agricultural production continues to rise.

Water Licensing and Irrigation Certification Complexity

Complex water licensing and approval processes are hindering the growth of the irrigation machinery market in Canada by delaying new irrigation projects and associated equipment purchases. As reported in the Province of British Columbia’s Water Science Series published in 2024, over 4,000 active water licence applications were pending decisions as of March 2024, with an additional 5,000 submissions yet to be processed. These permitting delays extend project timelines and create uncertainty for growers planning irrigation investments, thereby slowing the adoption of irrigation machinery and water management systems across the country.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Irrigation Type: Precision Digital Upgrades Reshaping the Pivot Fleet

The Canada irrigation machinery market share for the pivot irrigation segment held the largest 38.7% in 2025. This dominance is attributed to the reliance of large-scale field crop operations in Alberta and Saskatchewan on mechanized irrigation systems for cereals, oilseeds, forage crops, and potato production. Center pivot and lateral move systems remain commercially appealing due to their ability to provide broad-acre irrigation coverage, compatibility with automation, and operational efficiency across extensive farming areas. Additionally, demand is bolstered by the ongoing modernization of irrigation districts and the increasing adoption of retrofit technologies, such as remote monitoring, precision nozzles, and automated water-application controls, aimed at enhancing irrigation performance and resource efficiency.

The Canada irrigation machinery market size for the drip irrigation segment is projected to grow at the fastest CAGR of 12.1% from 2026 to 2031. The adoption of drip irrigation is rising as greenhouse operators, specialty-crop growers, and high-value horticulture producers focus on water efficiency and precision nutrient management systems. Subsurface drip installations are also gaining popularity among Prairie producers seeking improved water use and crop diversification. Manufacturers are expanding their product offerings to include features such as fertigation compatibility, automated scheduling, and soil moisture integration technologies, which support precision agriculture practices. This growth is driving demand for advanced drip systems across greenhouse operations, orchards, vineyards, berry cultivation, and specialty vegetable production throughout Canada.

By Application: Field Crop Volume Anchors Revenue, Specialty Crops Drive Value Growth

The field crops segment held the largest 58.5% share in 2025. This dominance is attributed to Canada’s irrigated agriculture infrastructure, which is primarily focused on cereals, oilseeds, pulses, forage crops, and potatoes cultivated in the Prairie provinces. Large commercial farms are increasingly investing in mechanized irrigation systems to enhance yield consistency and improve water management efficiency under varying climate conditions. Within this segment, irrigation demand is shifting towards system modernization, automation upgrades, and improvements in district-linked infrastructure, rather than the installation of entirely new stand-alone systems. Potato cultivation remains a significant irrigation-intensive category, as crop quality and productivity are highly dependent on controlled moisture application throughout the growing cycle.

The fruits and vegetables segment is projected to grow at the fastest CAGR of 10.2% from 2026 to 2031. This growth is driven by the expansion of greenhouse cultivation, increased berry and orchard production, and the rising adoption of drip and micro-irrigation technologies in specialty crop farming systems. Producers are focusing on precise irrigation scheduling and fertigation systems to enhance crop quality while meeting water-efficiency goals. Additionally, greenhouse operations are driving demand for automated, climate-responsive irrigation technologies integrated with nutrient-delivery systems and recirculation infrastructure. These developments are bolstering investments in advanced irrigation equipment tailored for horticulture, greenhouse vegetables, vineyards, orchards, nurseries, and controlled-environment agriculture operations across Canada.

By End User: Greenhouse Operators Set the Technology Pace

The commercial field-crop farms segment accounted for the largest 52.0% share in 2025. Large-scale commercial farms dominate as the primary end-user category due to their substantial purchases of center pivot and large-field irrigation systems across the Prairie provinces. Investment decisions in this segment are heavily influenced by factors such as commodity pricing, provincial irrigation programs, water availability, and long-term infrastructure planning. Operators in this segment prioritize irrigation automation, remote monitoring, and system efficiency upgrades to enhance productivity across extensive farming areas. Additionally, the modernization of district irrigation infrastructure is driving the adoption of digitally connected irrigation systems, which support precision water management and compliance with regulatory requirements.

The greenhouse and nursery operators segment is forecast to grow at the fastest CAGR of 10.6% from 2026 to 2031. This growth is driven by the expansion of controlled-environment agriculture, stricter water-efficiency requirements, and increased adoption of closed-loop irrigation and fertigation technologies. Greenhouse operators are investing in automated drip irrigation systems, moisture-monitoring technologies, and recirculation infrastructure to enable year-round crop production and optimize resource use. Similarly, nursery operators and specialty-crop growers are adopting advanced irrigation controls integrated with climate management systems to enhance operational consistency. These developments are boosting demand for precision irrigation technologies designed for high-value horticulture and controlled-environment agricultural applications across Canada.

Geography Analysis

Alberta remains the largest provincial market due to its extensive installed irrigation infrastructure and the highest concentration of mechanized irrigation systems in the country. Large irrigation districts in southern Alberta continue to drive demand for center pivots, lateral move systems, and digitally connected irrigation controls, which support field crop production. Saskatchewan is also strengthening its position through irrigation expansion initiatives aimed at supporting cereal, oilseed, and specialty crop development. British Columbia contributes significantly to the demand for drip and micro-irrigation systems, as orchard, berry, and vineyard operations require precision water management technologies. Manitoba is expanding its irrigated agriculture, particularly for potato and vegetable production systems.

Ontario represents a key eastern market, driven by greenhouse operations, nursery production, and specialty-crop farming, which continue to increase demand for precision irrigation systems and fertigation technologies. According to Statistics Canada, Ontario accounted for 63.9% of Canada’s total greenhouse area in 2024, creating strong demand for high-specification drip irrigation, recirculation systems, and automated climate-responsive water-management technologies. Quebec is also contributing to the growth in demand for greenhouse irrigation equipment through the expansion of controlled-environment agriculture and specialty horticulture production. Atlantic Canada, while smaller in total irrigated area, generates meaningful equipment demand through concentrated potato, berry, and vegetable cultivation systems, supporting the adoption of precision irrigation technologies.

Eastern Canadian provinces continue to support demand for precision irrigation technologies due to the requirements of greenhouse cultivation, specialty-crop farming, and nursery production for consistent water management and nutrient-delivery systems. Commercial growers are increasingly adopting automated scheduling technologies, fertigation systems, and climate-responsive irrigation controls to enhance water-use efficiency and operational productivity. Provincial modernization initiatives and a stronger focus on sustainable agricultural practices are further encouraging investment in digitally connected irrigation infrastructure. Specialty crop producers across Ontario, Quebec, Nova Scotia, and New Brunswick are prioritizing advanced drip and micro-irrigation systems to enable controlled water application, improve crop quality, and achieve long-term agricultural sustainability objectives.

Competitive Landscape

The Canada irrigation machinery market is moderately consolidated, with key players such as Lindsay Corporation, Valmont Industries, Inc., Netafim Ltd., and Reinke Manufacturing Co., Inc. These companies maintain their market positions through extensive dealer networks, advanced precision irrigation technologies, remote-monitoring platforms, and integrated water-management systems. Competitive differentiation is increasingly driven by automation capabilities, digital irrigation controls, sensor integration, and alignment with provincial water-efficiency initiatives, rather than solely focusing on conventional irrigation hardware performance for large-scale agricultural operations in Canada.

Below the leading original equipment manufacturers (OEMs), competition remains highly fragmented among regional dealers, installation companies, irrigation-service providers, and agricultural technology integrators. Local suppliers compete by leveraging crop-specific expertise, customized irrigation-system designs, and stronger alignment with provincial licensing and water-management requirements. Growers are increasingly opting for integrated irrigation solutions that combine pumps, pivots, drip systems, soil-moisture monitoring, and digital reporting capabilities within unified operational platforms. This trend is fostering greater collaboration between irrigation-equipment suppliers and precision-agriculture technology providers. Companies that offer installation support, technical services, regulatory compliance, and long-term operational optimization are enhancing their competitive positioning within Canada’s evolving irrigation infrastructure market.

Digital platform expansion and precision water-management technologies are central to competitive strategies in the irrigation equipment sector. In January 2025, Lindsay Corporation acquired a minority interest in Pessl Instruments GmbH to enhance its environmental monitoring and precision agriculture capabilities within its irrigation technology portfolio. Manufacturers are increasingly incorporating analytics, remote monitoring, automation, and soil-moisture sensing into irrigation systems to improve water-use efficiency and support operational decision-making. Competitive positioning is now heavily influenced by the ability to deliver integrated digital irrigation ecosystems that enable performance measurement, predictive management, and long-term agricultural sustainability objectives for commercial farming operations.

Canada Irrigation Machinery Industry Leaders

Lindsay Corporation

Valmont Industries, Inc.

Netafim Ltd. (Orbia Advance Corporation, S.A.B. de C.V.)

The Toro Company

Reinke Manufacturing Co., Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Netafim Ltd. (Orbia Advance Corporation, S.A.B. de C.V.) collaborated with Treetoscope to incorporate plant-sensing sap-flow technology into its GrowSphere platform. This partnership enhances precision irrigation capabilities across North America, including Canada, and promotes data-driven water management for agricultural producers.

- August 2025: Valmont Industries, Inc.'s Valley Irrigation introduced a USD 100,000 irrigation innovation grant program for commercial growers in North America, including Canada. The program aims to support the adoption of advanced irrigation equipment and precision irrigation technologies.

- July 2025: Water Ways Technologies Inc. has formed a strategic partnership to develop exclusive tomato hybrids specifically for vertical farming applications in Canada. This initiative supports the growth of controlled-environment agriculture and facilitates opportunities for advanced irrigation and water management systems.

Canada Irrigation Machinery Market Report Scope

The irrigation machinery market encompasses equipment and systems designed to efficiently deliver water to agricultural crops using methods such as pivot, drip, sprinkler, and micro-irrigation. These systems enhance water management, crop productivity, irrigation accuracy, and operational efficiency in applications including field crops, greenhouses, orchards, and specialty farming. The Canada irrigation machinery market is segmented by irrigation type (pivot irrigation, sprinkler irrigation, and drip irrigation), by application (field crops, fruits and vegetables, greenhouses and nurseries, and turf and ornamentals), and by end user (commercial field-crop farms, specialty-crop growers, greenhouse and nursery operators, and turf and landscape operators). The market forecasts are provided in terms of value (USD).

| Pivot Irrigation | Center Pivot Systems |

| Linear and Lateral Move Systems | |

| Sprinkler Irrigation | Solid-set Sprinklers |

| Travelers and Hose Reel Systems | |

| Micro-sprinklers | |

| Drip Irrigation | Surface Drip Systems |

| Subsurface Drip Systems | |

| Greenhouse Drip Systems |

| Field Crops | Cereals and Grains |

| Oilseeds and Pulses | |

| Potatoes | |

| Forage Crops | |

| Fruits and Vegetables | Open-field Vegetables |

| Orchards and Vineyards | |

| Berries | |

| Greenhouses and Nurseries | |

| Turf and Ornamentals |

| Commercial Field-crop Farms |

| Specialty-crop Growers |

| Greenhouse and Nursery Operators |

| Turf and Landscape Operators |

| By Irrigation Type | Pivot Irrigation | Center Pivot Systems |

| Linear and Lateral Move Systems | ||

| Sprinkler Irrigation | Solid-set Sprinklers | |

| Travelers and Hose Reel Systems | ||

| Micro-sprinklers | ||

| Drip Irrigation | Surface Drip Systems | |

| Subsurface Drip Systems | ||

| Greenhouse Drip Systems | ||

| By Application | Field Crops | Cereals and Grains |

| Oilseeds and Pulses | ||

| Potatoes | ||

| Forage Crops | ||

| Fruits and Vegetables | Open-field Vegetables | |

| Orchards and Vineyards | ||

| Berries | ||

| Greenhouses and Nurseries | ||

| Turf and Ornamentals | ||

| By End User | Commercial Field-crop Farms | |

| Specialty-crop Growers | ||

| Greenhouse and Nursery Operators | ||

| Turf and Landscape Operators | ||

Key Questions Answered in the Report

What is the 2031 value outlook for irrigation equipment demand in Canada?

The Canada irrigation machinery market is forecast to reach USD 655.10 million by 2031.

Which irrigation type is growing the fastest in Canada?

Drip irrigation is projected to grow at the fastest, with a 12.1% CAGR from 2026 to 2031.

Which application generates the most revenue for irrigation machinery suppliers?

Field crops remain the largest application base, accounting for 58.5% of total demand in 2025.

Why is Alberta so important for equipment sales?

Alberta accounted for 74.3% of national irrigated land in 2024 and is also supported by district modernization backed by CAD 466 million (USD 341 million) from the Canada Infrastructure Bank.

What is the current market size for Canada irrigation machinery market in 2026?

Canada irrigation machinery market size is currently valued at USD 447.90 million in 2026.

What is the market value of irrigation equipment in Canada in 2026?

In 2025, the Canadian irrigation machinery market hit USD 415.10 million.

Page last updated on: