Employee Data Privacy and Compliance Platform Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.42 Billion |

| Market Size (2031) | USD 6.31 Billion |

| Growth Rate (2026 - 2031) | 13.02% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Employee Data Privacy and Compliance Platform Market Analysis by Mordor Intelligence

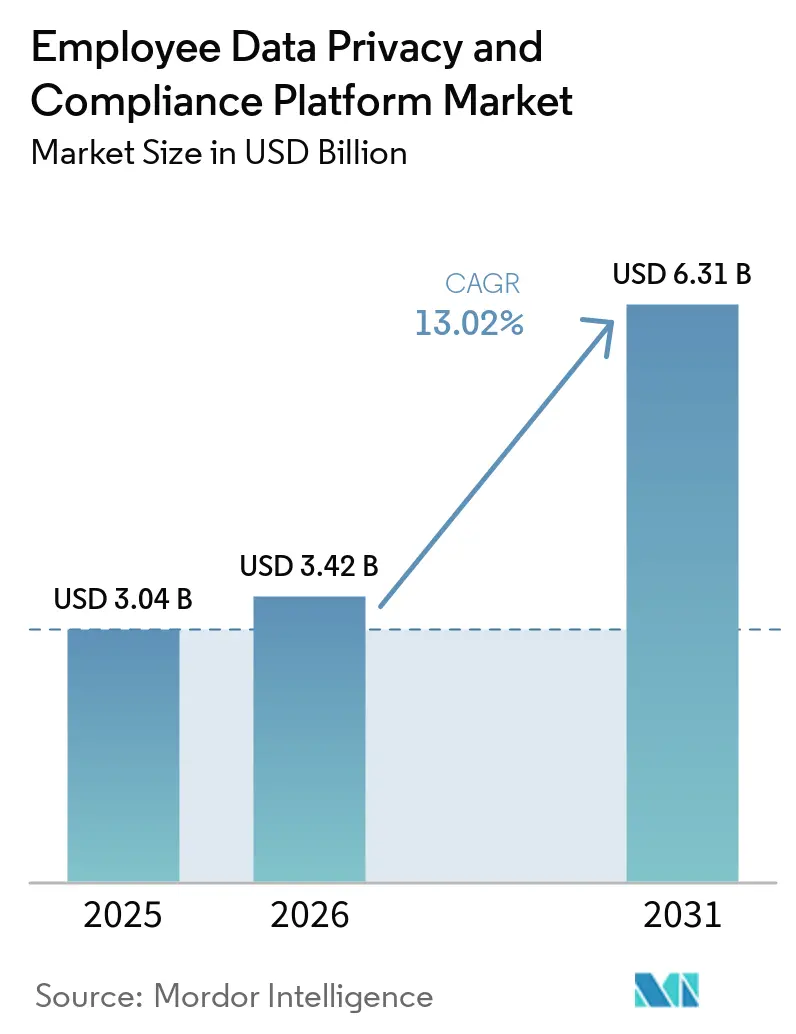

The employee data privacy and compliance platform market size is projected to be USD 3.04 billion in 2025, USD 3.42 billion in 2026, and reach USD 6.31 billion by 2031, growing at a CAGR of 13.02% from 2026 to 2031. The employee data privacy and compliance platform market is being shaped by the steady expansion of employee data rights across major jurisdictions, which is making workforce privacy compliance more operational and less discretionary. European enforcement widened in 2025 and 2026 to include AI-supported hiring and employee monitoring, raising compliance urgency for employers that had relied on broad governance, risk, and compliance tools rather than purpose-built systems. Demand is also moving toward platforms that can integrate data discovery, consent handling, rights management, documentation, and audit trails into a single workflow, because fragmented compliance processes are harder to maintain across jurisdictions. Consolidation among established vendors and private equity-backed platforms shows that buyers are increasingly favoring durable vendors that can keep pace with legal change, product updates, and integration requirements. The clearest commercial opportunity remains with organizations that need to manage multi-country employee data obligations across cloud HR systems, AI-enabled employment tools, and data residency constraints.

Key Report Takeaways

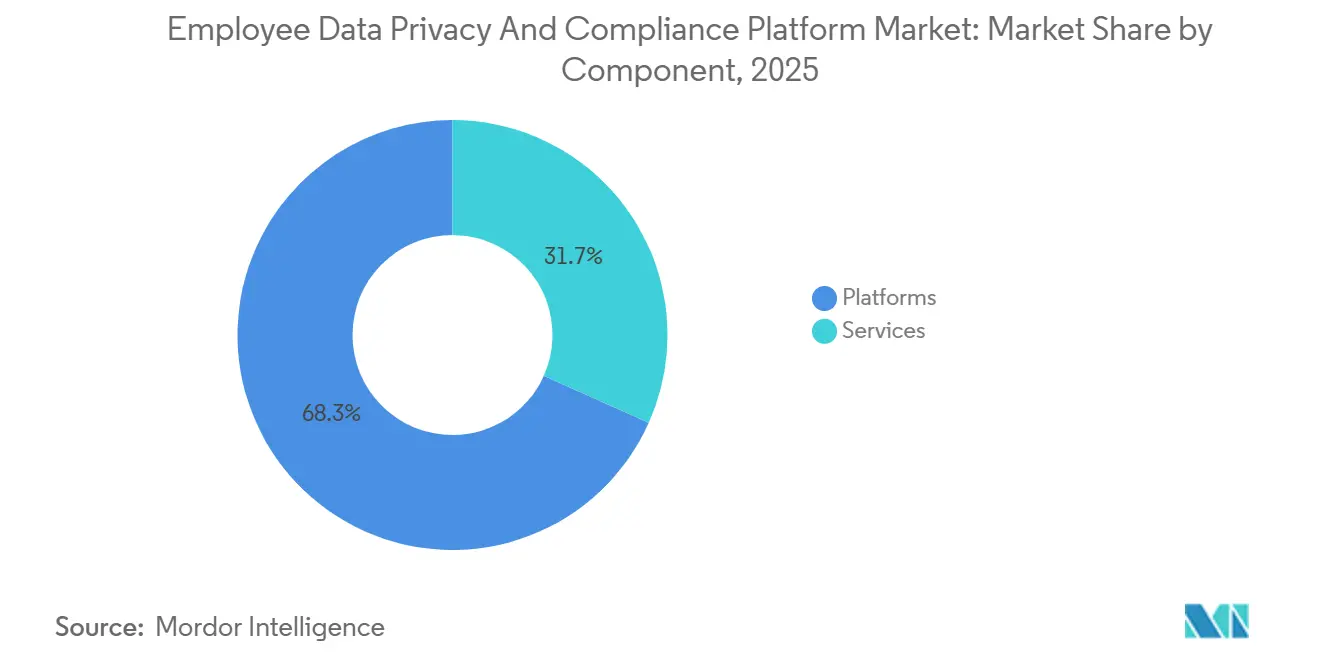

- By component, platforms led with 68.31% revenue share in 2025, while services are projected to expand at a 14.98% CAGR through 2031.

- By deployment mode, cloud-based deployment held 66.23% of the employee data privacy and compliance platform market in 2025, while hybrid deployment is projected to grow at a 14.56% CAGR through 2031.

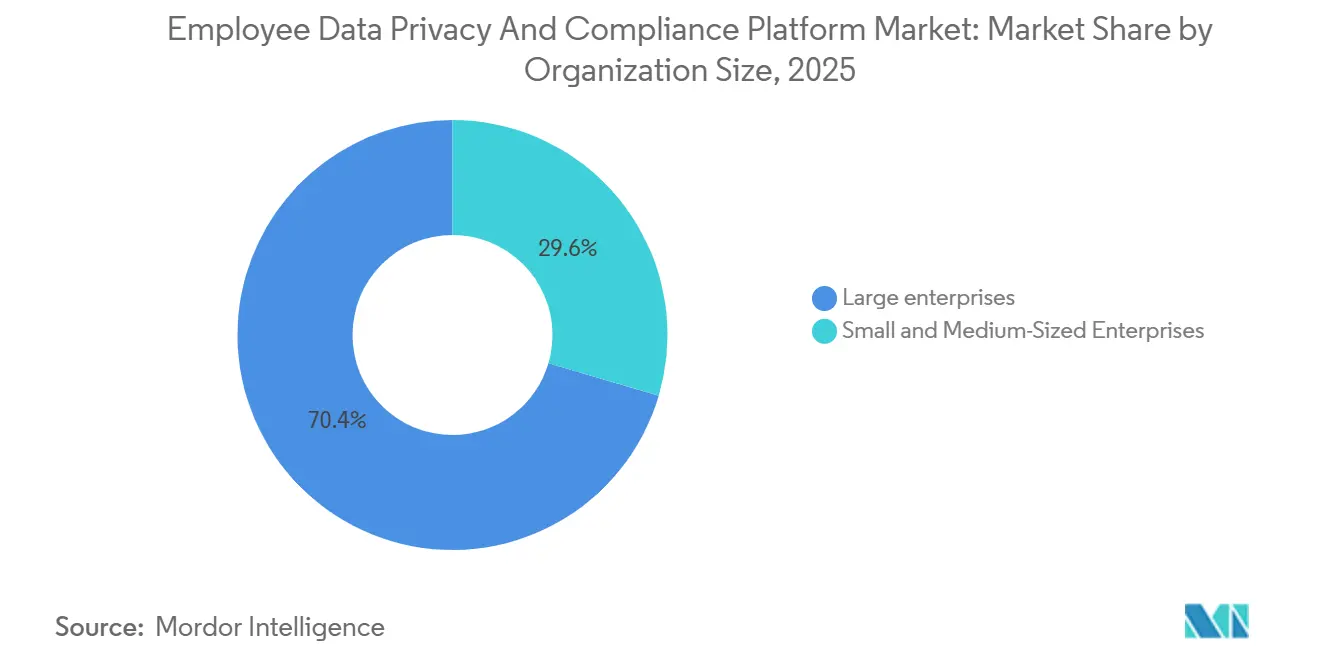

- By organization size, large enterprises accounted for 70.44% of the market share in 2025, while SMEs are projected to record the fastest growth at a 15.31% CAGR through 2031.

- By end-user industry, IT and telecommunications held 30.41% share in 2025, while healthcare and life sciences are projected to expand at a 13.66% CAGR through 2031.

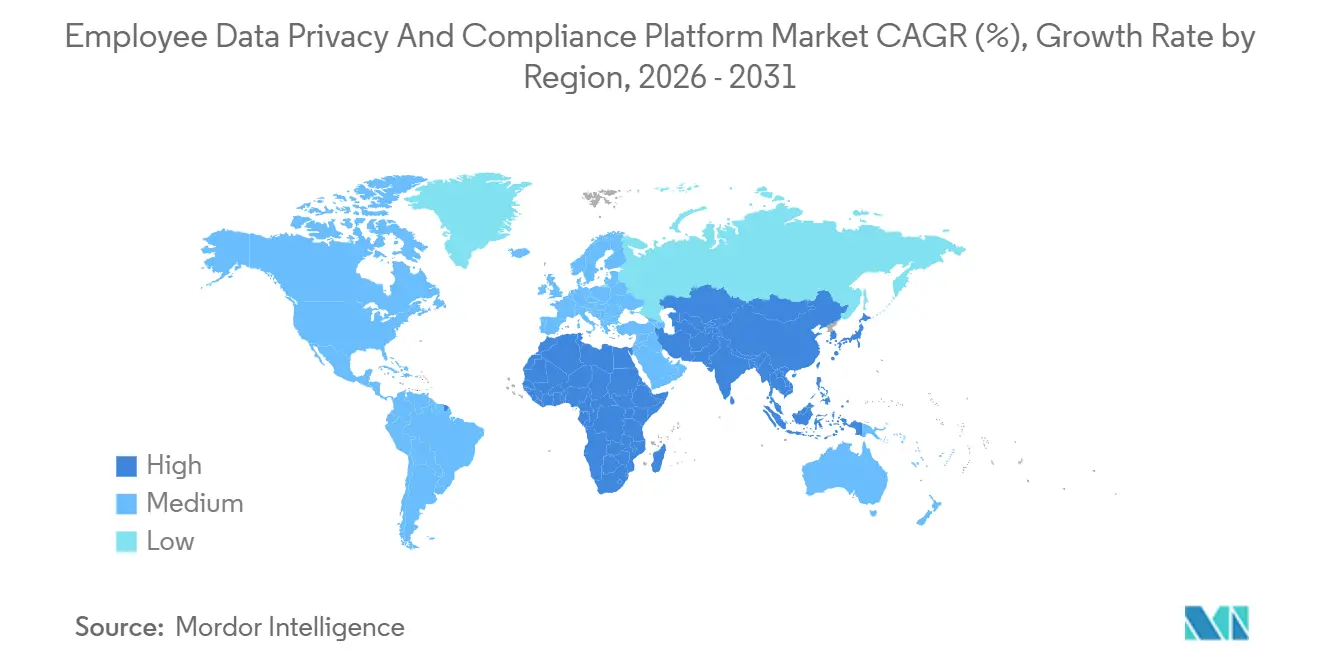

- By geography, North America held 37.29% of the employee data privacy and compliance platform market share in 2025, while Asia-Pacific is projected to grow at a 14.09% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Employee Data Privacy and Compliance Platform Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of Employee Privacy Rights Across Jurisdictions | +3.1% | Global | Medium term (2-4 years) |

| AI Hiring, Monitoring, and ADMT Governance Requirements | +2.7% | North America and Europe, with growing APAC spillover | Short term (≤ 2 years) |

| Automation of RoPA, DPIA, and Retention Workflows | +2.3% | Global, strongest in EU-regulated enterprises | Medium term (2-4 years) |

| Shift toward Cloud-Native Privacy Operations | +1.8% | Global, led by North America and APAC | Short term (≤ 2 years) |

| Cross-Border Transfer and Data Residency Compliance Needs | +1.4% | EU, APAC, with North America and South America exposure | Long term (≥ 4 years) |

| Rising Volume and Complexity of Employee Rights Requests | +1.0% | Global, concentrated in EU, UK, and APAC | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Expansion of Employee Privacy Rights Across Jurisdictions

The strongest structural support for the employee data privacy and compliance platform market comes from the widening legal definition of what employers must govern and document. Organizations now face a broader set of obligations regarding accuracy, notice, grievance handling, retention, and breach response when processing employee information across multiple countries. The compliance challenge is not only that more rules exist, but also that they do not align neatly across jurisdictions, which makes standardized manual processes less effective. This has pushed privacy compliance from a legal review exercise into a daily operational requirement for HR, legal, security, and IT teams. As a result, the employee data privacy and compliance platform market is benefiting from budget decisions that increasingly favor dedicated workflow systems over spreadsheets or general controls tooling. The change is especially important for employers operating across 2 or 3 jurisdictions, because they must now manage non-overlapping obligations on consent, purpose limitation, documentation, and employee rights requests.

AI Hiring, Monitoring, and ADMT Governance Requirements

Rules for AI-assisted hiring, performance monitoring, and employment decision-making are becoming a direct driver of spending in the employee data privacy and compliance platform market. Employers are being asked to document risk, provide notice, assess fairness, and maintain oversight when automated systems influence recruitment or worker management. The UK Information Commissioner's Office reported in March 2026 that its recruitment review led to nearly 300 recommendations and stated that DPIAs are likely required when automated decision-making tools are used in hiring.[1]Information Commissioner's Office, “Automated Decisions Can Streamline the Hiring Process With the Right Safeguards in Place,” Information Commissioner's Office, ico.org.uk These obligations are difficult to manage through legal review alone because employers need repeatable workflows, evidence trails, and ongoing reassessment after deployment. That is why vendors in the employee data privacy and compliance platform market are emphasizing embedded assessment tools, automated triggers, and audit-ready documentation, rather than focusing solely on policy libraries. The demand uplift is strongest where AI is already active in hiring, productivity scoring, workforce analytics, and employee monitoring, because those use cases generate immediate governance exposure.

Automation of RoPA, DPIA, and Retention Workflows

Automation is becoming more central because the cost of incomplete records and missed assessments is rising across enterprise privacy programs. TrustArc stated in 2025 that automation can reduce manual RoPA by up to 80%, underscoring why documentation-heavy processes are moving toward platform-based execution. This matters in the employee data privacy and compliance platform market because records of processing, impact assessments, and retention schedules depend on current visibility into where employee data sits and how it changes. As HR applications, AI tools, collaboration systems, and identity platforms evolve, manually maintained registers can quickly become outdated. Vendors that combine continuous discovery with workflow automation are reducing that gap and helping compliance teams demonstrate readiness during operations rather than during an audit scramble. The employee data privacy and compliance platform market is therefore gaining from a shift in buyer preference toward tools that can automate detection, trigger assessments, and preserve evidence without relying on periodic manual reviews.

Shift toward Cloud-Native Privacy Operations

The move of HR systems toward SaaS delivery is also supporting the employee data privacy and compliance platform market because privacy tooling is following the same architectural path. Cloud-based privacy operations are easier to update, connect, and manage across distributed compliance teams than older on-premises deployments. This is important when regulations and employment-related AI obligations change quickly, because vendors can update regulatory libraries and connectors without forcing customers into long upgrade cycles. The model also aligns with the needs of smaller buyers without large internal implementation teams, which helps explain why the SME segment is expanding quickly. At the same time, large employers are not moving only to pure cloud, because some still need local storage or country-specific controls for workforce data. That is why the employee data privacy and compliance platform market is seeing rising interest in hybrid operating models that preserve cloud management benefits while supporting data residency and localized control.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Complex Integration Across HR, Identity, and IT Systems | -2.4% | Global, most acute in large enterprises | Medium term (2-4 years) |

| Fast-Changing Local Rules Create Configuration and Liability Risk | -1.9% | Global, especially US state-level and APAC | Short term (≤ 2 years) |

| Budget Competition with Broader GRC and Security Platforms | -1.5% | North America and Europe | Medium term (2-4 years) |

| Employee Surveillance Sensitivities and Works Council Pushback | -0.9% | Europe, especially Germany, France, and Nordics | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Complex Integration Across HR, Identity, and IT Systems

The main operational restraint in the employee data privacy and compliance platform market is that employee data is rarely stored in one system. It spans HRMS environments, payroll tools, identity platforms, collaboration software, monitoring tools, and regional databases with varying schemas and access controls. Connecting a privacy platform to this environment often requires API work, normalization, permissions review, and cross-functional project time that buyers may underestimate at the start. The challenge becomes more severe in large enterprises that operate separate systems across business units or countries, as a single compliance workflow may depend on multiple disconnected sources. This increases implementation costs and slows time to value, which can delay buying decisions in the mid-market and complicate rollouts in multinational organizations. Vendors with pre-built connectors, certified integrations, and API-first product design, therefore, hold a meaningful execution advantage in the employee data privacy and compliance platform market.

Fast-Changing Local Rules Create Configuration and Liability Risk

Frequent legal changes are another restraint, as each new employment or AI-related rule can trigger a review of notices, logic, workflows, and evidence requirements. Buyers are not only paying for software but also for the recurring configuration work that follows when rules shift across states or countries. This raises a real liability concern for employers that want consistency, because a system configured for one version of a rule may need to be rapidly revised when the legal standard changes. The result is that some organizations move more slowly than planned, even when they recognize the need for specialized platforms. In the employee data privacy and compliance platform market, vendors that maintain dynamic regulatory libraries and provide customer support for rule updates are better positioned than those that place most of the configuration burden on clients. Even so, there can still be a lag between enactment, product update, and client deployment, which keeps this restraint relevant in the near term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Platforms Anchor Enterprise Compliance, Services Accelerate Fastest

Platforms accounted for 68.31% of the 2025 market, indicating that buyers still favor integrated systems over fragmented point tools. That share reflects a preference for a single operating layer that connects data discovery, rights management, consent handling, privacy assessments, and cross-border compliance controls. In the employee data privacy and compliance platform industry, this matters because the underlying workflows are interdependent, and value drops when teams manage them in separate applications. Data discovery and classification remain the foundation because organizations cannot maintain reliable records or trigger impact assessments without knowing where employee information resides. Consent and preference workflows are also becoming more relevant inside employment settings as AI-supported tools create new notice and transparency requirements.

Workforce identity and access governance tools are gaining traction because access to employee records is now treated as both a security and a privacy issue. Privacy risk and impact assessment modules are also in stronger demand, especially where organizations must document high-risk processing and maintain evidence for internal review or regulator scrutiny. The services segment is the fastest-growing component, with a 14.98% CAGR from 2026 to 2031, indicating that many buyers still need external support after the initial software purchase. This segment of the employee data privacy and compliance platform market is expanding because clients often outsource configuration, policy tuning, workflow design, and ongoing monitoring rather than building those capabilities internally. Demand is especially evident among SMEs and highly regulated enterprises, where privacy teams are often lean due to the complexity of the rules they face. BigID’s March 2026 launch of integrated AI governance for employee AI use also showed how product vendors are moving closer to service-led delivery by packaging monitoring, access controls, and policy enforcement into broader enterprise programs. This shift highlights the growing emphasis on comprehensive solutions to address enterprise AI governance needs.

By Deployment Mode: Cloud Dominates, Hybrid Emerges as the Compliance Bridge

Cloud-based deployment accounted for 66.23% of the 2025 market, confirming that this category has moved in step with the broader migration of HR and compliance systems to SaaS environments. Buyers favor cloud deployment because vendors can issue regulatory updates, connector improvements, and workflow enhancements more quickly than in traditional on-premises models. The employee data privacy and compliance platform market also benefits from the lower maintenance burden of cloud delivery, especially for organizations that need distributed access across legal, HR, privacy, and security teams. On-premises deployment still matters in some regulated settings, including defense, certain financial institutions, and public sector environments where localized control remains non-negotiable. Even so, its role is narrowing because cloud-based administration now offers stronger oversight, easier upgrades, and better visibility across global privacy programs.

Hybrid deployment is the fastest-growing model with a 14.56% CAGR through 2031, and that growth reflects a practical compromise rather than a temporary transition stage. Multinationals are using hybrid models to keep sensitive or residency-bound data in local environments while managing policies, reporting, and workflow coordination through cloud control layers. This architecture is especially useful when organizations operate across APAC and Europe, where residency requirements and operational flexibility must coexist. The employee data privacy and compliance platform market for hybrid environments is being driven by employers seeking centralized governance without sacrificing country-level control over employee records and logs. Hybrid also aligns with the growing use of AI-related compliance workflows, as employers may want local handling of inference records while still coordinating assessments and documentation globally. That mix of flexibility and control is why hybrid is evolving from a niche deployment option into a durable architecture choice for global workforce privacy programs.

By Organization Size: Large Enterprises Lead, SMEs Drive the Next Growth Wave

Large enterprises held 70.44% of the 2025 market share, consistent with their earlier adoption of dedicated workforce privacy systems. These organizations manage multi-jurisdictional employee data, larger privacy teams, more complex vendor stacks, and a wider mix of AI-supported employment tools than smaller companies. Their buying preference has favored broad platform coverage because fragmented tooling creates gaps when compliance, documentation, and employee rights workflows must be coordinated across regions. Within the employee data privacy and compliance platform industry, large employers also tend to accept more complex deployment projects if that helps them reduce long-term operational risk. This explains why full-suite vendors have built much of their position around multinational buyers with large employee footprints and broad compliance obligations.

SMEs are the fastest-growing cohort, with a 15.31% CAGR through 2031, indicating that the addressable base is widening beyond large multinational companies. Smaller firms are being drawn in by lower legal thresholds, broader processing obligations, and the spread of cloud-based HR tools that formalize the handling of employee data. Many of these buyers prefer modular subscriptions and faster deployment because they need compliance support without a large internal privacy function. That is helping SME-focused platforms and lighter implementation models gain traction across the employee data privacy and compliance platform market. The employee data privacy and compliance platform market share remains concentrated in larger organizations today, but growth is shifting toward smaller buyers that now face more formal recordkeeping and governance expectations. TrustArc, a provider in the compliance space, is actively addressing these needs with tailored solutions for SMEs.[2]TrustArc, “Automate ROPAs Fast: Cut Manual Work by 80%,” TrustArc, trustarc.com Consequently, vendors are recalibrating their strategies, placing greater emphasis on mid-market positioning. Simplified bundles and expedited onboarding processes have emerged as pivotal competitive advantages, a shift that is more pronounced than just a few years ago.

By End-User Industry: IT Sector Anchors Demand, Healthcare Scales Fastest

The IT and telecommunications sector held 30.41% of the 2025 end-user base, making it the largest industry buyer group in the employee data privacy and compliance platform market. These organizations combine large global workforces, cloud-native operating models, and early adoption of AI-supported hiring and performance systems, thereby increasing their exposure to workforce privacy obligations. They also serve as practical pilot environments because their internal teams are often more familiar with SaaS integration, automated controls, and data governance workflows. In the employee data privacy and compliance platform industry, this vertical has influenced product development by pushing vendors toward stronger automation, better integrations, and more detailed access controls. The sector’s buying behavior often sets the pattern that later expands into adjacent verticals with similar workforce data complexity.

Healthcare and life sciences are the fastest-growing verticals, with a 13.66% CAGR through 2031, and their growth stems from a layered compliance burden rather than digital adoption alone. Employers in this segment must govern workforce information in environments where staff credentials, scheduling, role performance, and operational data intersect with sensitive healthcare settings. That creates a more complex privacy surface when AI tools are used for scheduling, performance management, or workforce allocation. Banking, financial services, and insurance remain important because cross-border employee data flows and internal control expectations stay high in that sector. Government and public-sector demand is also rising, where sovereignty and local storage matter more in workforce systems. Manufacturing, retail, and e-commerce complete the picture, as biometric attendance data, shift management, and gig-workforce records are drawing more attention across the employee data privacy and compliance platform market.

Geography Analysis

North America held 37.29% of the employee data privacy and compliance platform market share in 2025, making it the largest regional market. The region’s lead came from its dense base of enterprise technology buyers, broad use of cloud HR systems, and an expanding compliance burden tied to state-level privacy frameworks. Employers in the United States are also dealing with a more active governance agenda around AI-supported hiring, promotion, and monitoring decisions, which is turning policy review into system-level spending. That dynamic has made multi-jurisdictional workflow management more valuable than one-off legal interpretation, especially for employers operating across several states. The employee data privacy and compliance platform market, therefore, remains anchored in North America, where buyers often need platforms that can coordinate notices, documentation, risk assessments, and employee rights processes across overlapping legal requirements.

Europe remained the second-largest regional cluster, led by the United Kingdom, Germany, France, Italy, and Spain. Regional demand stayed strong because both general data protection rules and employment-specific expectations around monitoring, proportionality, and collective arrangements shape workforce privacy in Europe. The legal environment has become more exacting for employers seeking to use AI-supported productivity or monitoring tools, as documentation, necessity, and governance standards are being applied more tightly across the region. This keeps Europe central to the employee data privacy and compliance platform market, not only because of enforcement pressure, but also because employers need systems that can sustain evidence, local adaptation, and internal accountability over time.

Asia-Pacific is projected to expand at a 14.09% CAGR through 2031, giving the region the fastest growth rate in the employee data privacy and compliance platform market. Growth is being driven by the rollout of tighter privacy expectations across India, Japan, South Korea, and Australia, which is increasing procurement among both local employers and multinationals with regional delivery centers. India is important because enforcement and implementation are pushing employers to formalize consent, grievance handling, and breach response for employee data. Japan also matters because privacy reform is broadening the compliance load around employee information and biometric data in workplace settings. South America is still at an earlier stage, but Brazil is generating demand among large employers that must govern workforce data under more structured privacy rules. The Middle East and Africa are also emerging, with interest rising as localization and sovereign hosting requirements shape deployment choices. Across these geographies, the employee data privacy and compliance platform market is gaining from the same pattern: employers want systems that can adapt locally without losing central oversight.

Competitive Landscape

The employee data privacy and compliance platform market was moderately consolidated at the top tier, with OneTrust, BigID, and TrustArc standing out for breadth of modules and enterprise reach. A second layer of vendors, including Securiti, DataGrail, Transcend, Relyance AI, Usercentrics, Ketch, and regional specialists, kept competition active by focusing on automation depth, consent workflows, or AI-native controls.[3]DataGrail, “DataGrail Product Updates, April 2026,” DataGrail, datagrail.io This structure means the market has recognizable leaders, but it still allows room for entry because no single vendor has closed off the field across enterprise, mid-market, and regional use cases. The employee data privacy and compliance platform market also showed a clear split between large-platform competition at the enterprise level and a more fragmented contest for SMEs. That fragmentation is especially visible in lower-complexity deployments, where pricing, speed, and ease of configuration can outweigh broad feature breadth.

Strategic moves in 2025 and 2026 showed that vendors were trying to widen their role from privacy tooling into broader governance and operational control. Main Capital Partners completed its acquisition of TrustArc in October 2025, reinforcing the view that established privacy software assets still have room to scale and expand into platforms. OneTrust announced a collaboration with Snowflake on April 28, 2026, to make consent enforceable within data-cleaning room workflows, demonstrating how vendors are moving privacy controls closer to data use rather than leaving them only at the point of collection. Usercentrics also acquired MCP Manager on January 14, 2026, extending consent and trust controls into AI agent workflows and highlighting how governance is shifting toward machine-mediated interactions with sensitive data. These moves suggest that product scope in the employee data privacy and compliance platform market is broadening from classic privacy administration toward AI governance, data use controls, and automated decision support.

Innovation is now centered on agentic automation, AI governance, and better handling of sensitive workforce data inside new enterprise workflows. BigID extended Data Access Governance to AI agents in March 2026, which applied human-equivalent access controls to autonomous agents operating in enterprise systems. Transcend launched Agentic Assist and the MCP Server in March 2026, giving privacy teams a way to initiate requests, assessments, and consent workflows from AI assistant interfaces. Relyance AI also brought Lyo to commercial availability in March 2026, with a focus on explaining not only what data is moving but also why it is moving, which matters for defensible documentation in high-risk AI settings. Didomi’s acquisition of Sourcepoint in July 2025 showed that even the consent management layer is consolidating as vendors try to build enough scale to compete with broader suites. The employee data privacy and compliance platform market still leaves space for specialists, but the direction of competition is moving toward integrated platforms that combine privacy operations, AI governance, and automation into a single client proposition.

Employee Data Privacy and Compliance Platform Industry Leaders

OneTrust LLC

BigID, Inc.

TrustArc Inc.

Securiti, LLC

DataGrail, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: OneTrust announced a collaboration with Snowflake (April 28) to embed consent signals directly into Snowflake Data Clean Rooms, enabling organizations to make consent enforceable at the point of data use rather than solely at collection, a material shift in how workforce data sharing between business units is governed. Separately, BigID was named a Leader in The Forrester Wave: Sensitive Data Discovery and Classification Solutions, Q2 2026, recognized in part for its Integrated Employee AI Governance module, which addresses sensitive data flows through employee AI tool usage.

- April 2026: BigID extended its Data Security Posture Management (DSPM) to Markdown files, becoming the first platform to discover and classify sensitive employee data embedded in AI instruction and agent framework files, closing a previously unaddressed governance gap for organizations deploying coding agents across engineering and compliance teams.

- March 2026: BigID launched integrated AI governance for employee AI use (March 26), combining Data Loss Prevention, Data Access Governance, and Data Activity Monitoring into a single platform purpose-built for organizations where employee AI tool adoption is outpacing security controls. Separately, BigID extended Data Access Governance to AI agents, applying human-equivalent access policies to non-human autonomous entities operating inside enterprise environments.

- March 2026: Relyance AI announced the commercial availability of Lyo, its next-generation AI-native data security product, at RSAC 2026. Lyo contextualizes data visibility by explaining not only what data is moving but why, a capability relevant to enforcement-grade DPIA documentation for high-risk AI systems under the EU AI Act.

Global Employee Data Privacy and Compliance Platform Market Report Scope

The Employee Data Privacy and Compliance Platform Market encompasses platforms that help organizations manage and protect employee data in compliance with data protection regulations such as GDPR and other regional privacy laws. These platforms provide capabilities such as data governance, consent management, access controls, compliance monitoring, and audit reporting. They enable organizations to ensure secure handling, storage, and processing of sensitive workforce data. The market focuses on mitigating data privacy risks and ensuring regulatory compliance across employee data ecosystems.

The Employee Data Privacy and Compliance Platform Market Report is Segmented by Component (Platforms [Data Discovery and Classification Platforms, Consent and Preference Management Platforms, Workforce Identity and Access Governance Platforms, Privacy Risk and Impact Assessment Platforms, Data Residency and Cross-Border Compliance Platforms, and Other Platforms], and Services [Professional services, and Managed services]), Deployment Mode (Cloud-based, On-premises, and Hybrid), Organization Size (Large enterprises, and Small and Medium-Sized Enterprises), End-user Industry (Banking, Financial Services and Insurance, Healthcare and Life Sciences, Information Technology and Telecommunications, Retail and E-Commerce, Government and Public Sector, Manufacturing, and Other End-User Industries), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Platforms | Data Discovery and Classification Platforms |

| Consent and Preference Management Platforms | |

| Workforce Identity and Access Governance Platforms | |

| Privacy Risk and Impact Assessment Platforms | |

| Data Residency and Cross-Border Compliance Platforms | |

| Other Platforms | |

| Services | Professional services |

| Managed services |

| Cloud-based |

| On-premises |

| Hybrid |

| Large enterprises |

| Small and Medium-Sized Enterprises |

| Banking, Financial Services and Insurance |

| Healthcare and Life Sciences |

| Information Technology and Telecommunications |

| Retail and E-Commerce |

| Government and Public Sector |

| Manufacturing |

| Other End-User Industries |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Component | Platforms | Data Discovery and Classification Platforms |

| Consent and Preference Management Platforms | ||

| Workforce Identity and Access Governance Platforms | ||

| Privacy Risk and Impact Assessment Platforms | ||

| Data Residency and Cross-Border Compliance Platforms | ||

| Other Platforms | ||

| Services | Professional services | |

| Managed services | ||

| By Deployment Mode | Cloud-based | |

| On-premises | ||

| Hybrid | ||

| By Organization Size | Large enterprises | |

| Small and Medium-Sized Enterprises | ||

| By End-user Industry | Banking, Financial Services and Insurance | |

| Healthcare and Life Sciences | ||

| Information Technology and Telecommunications | ||

| Retail and E-Commerce | ||

| Government and Public Sector | ||

| Manufacturing | ||

| Other End-User Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current and forecast value of the employee data privacy and compliance platform market?

The employee data privacy and compliance platform market was valued at USD 3.04 billion in 2025, is projected at USD 3.42 billion in 2026, and is forecast to reach USD 6.31 billion by 2031 at a 13.02% CAGR.

Why are employers increasing spending on employee privacy compliance platforms?

Spending is rising because employers now face more formal requirements around employee data rights, documentation, AI governance, and audit readiness across multiple jurisdictions.

Which component leads demand in this space?

Platforms led with 68.31% share in 2025 because buyers preferred integrated workflows for data discovery, consent handling, rights management, and privacy assessments.

Which deployment model is growing the fastest for workforce privacy software?

Hybrid deployment is projected to grow the fastest at a 14.56% CAGR through 2031, as organizations balance cloud-based management with data residency and local control requirements.

Which end-user sector is adopting these platforms the fastest?

Healthcare and life sciences is the fastest-growing end-user vertical, with a projected 13.66% CAGR through 2031, as workforce privacy obligations and AI-assisted operational tools overlap.

Which region offers the strongest near-term expansion opportunity?

Asia-Pacific shows the strongest growth outlook with a 14.09% CAGR through 2031, while North America remained the largest regional market with 37.29% share in 2025.

Page last updated on: