Employee Wellbeing Platform Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

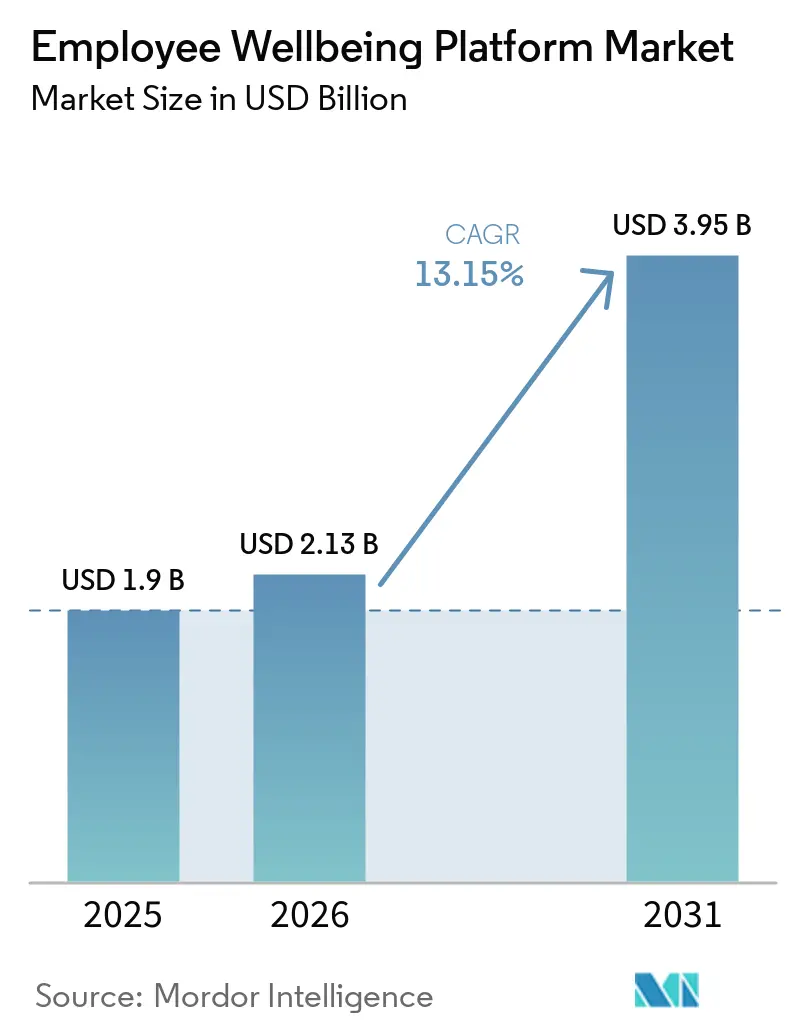

| Market Size (2026) | USD 2.13 Billion |

| Market Size (2031) | USD 3.95 Billion |

| Growth Rate (2026 - 2031) | 13.15% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Employee Wellbeing Platform Market Analysis by Mordor Intelligence

The Employee Wellbeing Platform Market size is projected to be USD 1.90 billion in 2025, USD 2.13 billion in 2026, and reach USD 3.95 billion by 2031, growing at a CAGR of 13.15% from 2026 to 2031. The employee well-being platform market is expanding because employers now treat workforce health as a measurable business issue tied to productivity, retention, and medical spending rather than as a discretionary HR benefit. Buyer expectations are also changing, and vendors are under greater pressure to demonstrate reductions in claims, absenteeism, presenteeism, and care friction rather than reporting simple participation rates. The market is also moving away from isolated wellness tools toward platforms that connect mental health, coaching, benefits navigation, and broader care journeys in a single workflow. Regulatory attention to psychosocial risk, privacy controls, and multinational data handling is raising the standard for platform selection, especially in large enterprise deals. This is creating space for vendors that can demonstrate outcomes, integrate with existing HR systems, and adapt their models for both large employers and the fast-growing mid-market segment of the employee wellbeing platform market.

Key Report Takeaways

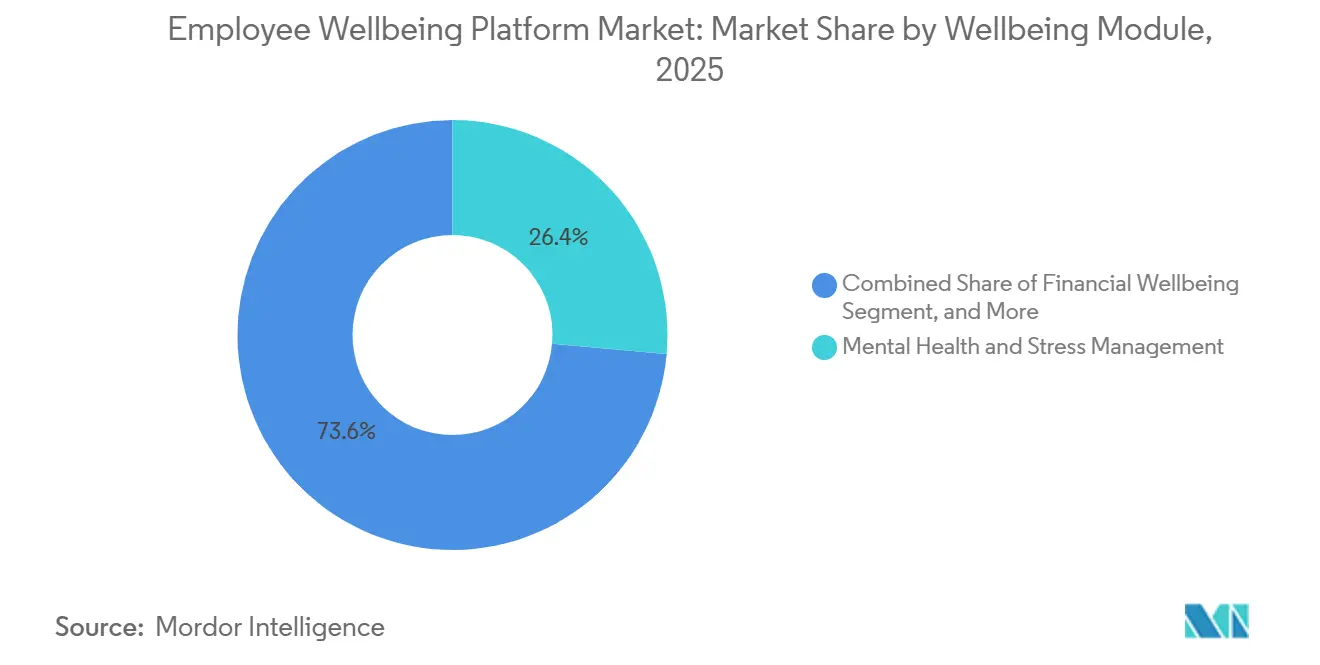

- By wellbeing module, mental health and stress management led with 26.41% share in Employee Wellbeing Platform Market in 2025, and financial wellbeing is projected to expand at a 15.92% CAGR through 2031.

- By deployment model, cloud-based platforms held 71.23% share in 2025, and hybrid deployment is projected to advance at a 14.38% CAGR through 2031.

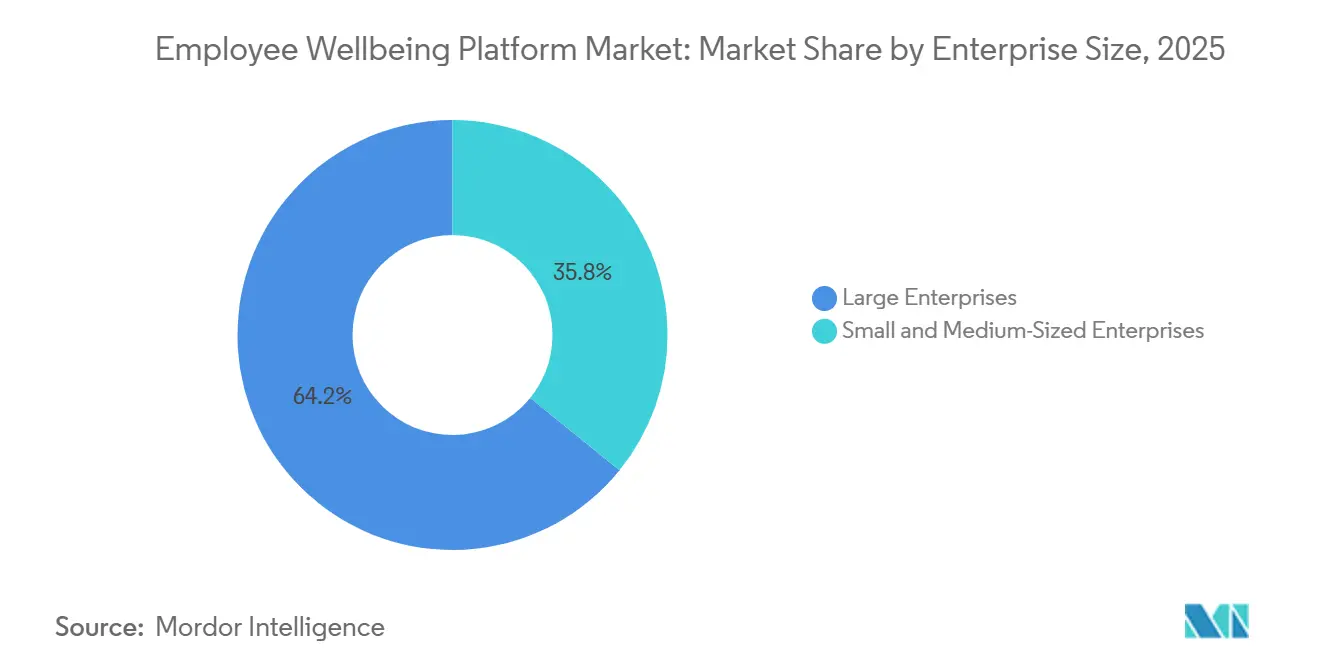

- By enterprise size, large enterprises held 64.17% share in 2025, and small and medium-sized enterprises are projected to grow at a 16.44% CAGR through 2031.

- By end-user industry vertical, healthcare and life sciences accounted for 21.88% of the market share in 2025, and retail and e-commerce are projected to expand at a 13.67% CAGR through 2031.

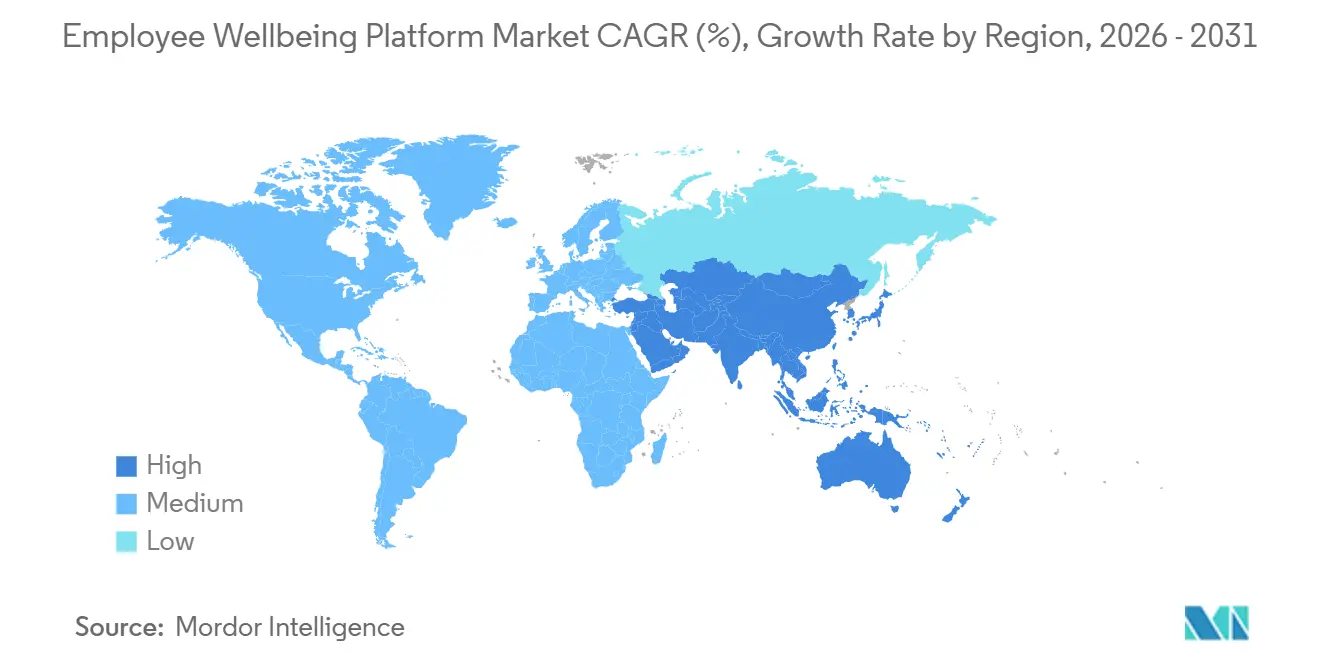

- By geography, North America held 37.92% share in 2025, and Asia-Pacific is projected to grow at a 16.73% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Employee Wellbeing Platform Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Workplace Stress and Burnout Across Knowledge and Frontline Roles | +2.8% | Global, with elevated intensity in North America, the UK, and APAC core markets | Short term (≤ 2 years) |

| Employer Demand to Reduce Healthcare Claims, Absenteeism, and Presenteeism Costs | +2.3% | North America and Europe, spill-over to APAC | Medium term (2-4 years) |

| Hybrid and Distributed Work Models Favoring Digital-First Wellbeing Delivery | +1.9% | Global, strongest in North America, Western Europe, and Southeast Asia | Short term (≤ 2 years) |

| AI, Analytics, and Wearables Enabling Personalized Interventions and Measurable Outcomes | +1.6% | North America, EU, South Korea, and Japan | Medium term (2-4 years) |

| Psychosocial Risk Governance Turning Wellbeing Metrics Into Procurement Criteria | +1.2% | EU and UK, expanding to Australia and Middle East and Africa | Long term (≥ 4 years) |

| GLP-1 and Chronic Condition Benefit Management Expanding Platform Scope | +0.8% | North America, with early adoption in Western Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Workplace Stress And Burnout Across Knowledge And Frontline Roles

Rising stress remains the strongest near-term growth driver in the employee wellbeing platform market, as employers now face a much clearer record of harm tied to work conditions. In April 2026, it was reported that more than 840,000 deaths each year were linked to psychosocial workplace risks, with annual economic losses equal to 1.37% of global GDP.[1]International Labour Organization, “840,000 Deaths a Year Linked to Psychosocial Risks at Work,” ILO, ilo.org In January 2026, surveys showed that 91% of UK adults experienced high or extreme stress in the previous year, and 35% of workers remained uncomfortable disclosing their stress to line managers, which strengthens the case for private digital pathways. Global data has also shown why employers place mental health near the center of spending decisions, since depression and anxiety cause 12 billion lost working days each year and result in USD 1 trillion in lost productivity. The employee well-being platform market is benefiting because buyers no longer see burnout as an abstract cultural issue and increasingly want tools that can identify risk, guide members into care, and connect program use with business outcomes.

Employer Demand To Reduce Healthcare Claims, Absenteeism, And Presenteeism Costs

The employee well-being platform market is also gaining support from employers seeking a more direct handle on the hidden costs of poor health at work. A 2025 study estimated burnout costs to U.S. employers at USD 3,999 to USD 20,683 per worker each year, and 89% of that burden came from presenteeism rather than absence.[2]Marie F. Martinez et al., “The Health and Economic Burden of Employee Burnout to U.S. Employers,” American Journal of Preventive Medicine, ajpmonline.org That cost mix matters because it shifts platform evaluation away from benefit participation and toward measurable change in care use, productivity, and short-term disability patterns. Employers are therefore asking for proof that a platform can help lower claims pressure and reduce lost output, which is raising the bar for vendors that only offer content libraries or basic wellness challenges. In practice, the stronger vendors in the employee wellbeing platform market are those that can translate engagement into auditable value, since buyers want a finance-ready case that holds up during renewal cycles and cost reviews.

Hybrid And Distributed Work Models Favoring Digital-First Wellbeing Delivery

The employee well-being platform market has also been boosted by the fact that digital delivery now aligns with how many employees actually work. Hybrid and distributed work patterns have reduced the usefulness of site-bound wellness models, as many employers need a single access model that works across home, office, and field settings. This has pushed employers toward cloud-first tools, embedded communication flows, and simple user journeys that do not depend on location or local program staff. The model becomes even more attractive when well-being services are built into familiar work software, because that lowers friction and improves visibility for employees who would not seek support on their own. Microsoft’s rollout of Thrive Global’s wellbeing app through Microsoft Teams in August 2025 demonstrated how distribution within daily workflow tools can expand reach and make digital support easier to use at scale.

AI, Analytics, And Wearables Enabling Personalized Interventions And Measurable Outcomes

AI and analytics are changing the employee wellbeing platform market because buyers increasingly care whether interventions are timed and tailored to the member, rather than simply being available. Personalization is becoming increasingly important in enterprise buying, as employers seek platforms that can guide members toward the right support path, reduce dropout, and demonstrate whether usage is linked to clinical or cost improvements. This is also increasing interest in wearable connections and ongoing data capture, because continuous signals are more useful than occasional self-reported check-ins for many high-risk populations. In April 2026, one launch illustrated this shift, with reports of up to 25% greater symptom improvement for high-need members and 60% consistent therapy engagement inside its AI-led care experience. The result is that the employee wellbeing platform market is moving toward platforms that combine care navigation, predictive analytics, and measurable outcomes rather than broad catalogs of wellness content.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Low Sustained Employee Engagement and ROI Proof Gaps | -1.8% | Global | Short term (= 2 years) |

| Sensitive Workforce Health Data Privacy and Cybersecurity Concerns | -1.4% | Global, most acute in the EU, the US, and Singapore | Medium term (2-4 years) |

| Works Council Reviews and Data Localization Slowing Multicountry Rollouts | -0.9% | EU, particularly Germany, France, and the Netherlands | Long term (= 4 years) |

| HCM Suite Bundling and AI Feature Copycats Compressing Standalone Platform Budgets | -0.7% | North America and Western Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Low Sustained Employee Engagement And ROI Proof Gaps

The largest commercial restraint in the employee well-being platform market remains the gap between platform availability and regular employee use. In late 2025, only 29% of employees rated their company’s wellness programs as good, down from 41% in 2022, even though employer spending continued to rise. In March 2026, it was also noted that older employee assistance models typically achieved only 5% to 10% utilization, and many newer platforms still struggle to maintain monthly engagement above 30%. That ceiling weakens the business case at renewal because low usage makes it harder to credibly demonstrate reductions in claims or improvements in productivity. Vendors that cannot connect engagement with finance-grade outcomes are more likely to fall back into discretionary budget discussions when employers tighten spending.[3]Spring Health, “Introducing Guide, Spring Health’s AI-Led Experience for Employer Mental Health,” Spring Health, springhealth.com This issue slows the employee wellbeing platform market because growth depends not only on adoption, but also on whether employers believe employees will keep using the service after launch.

Sensitive Workforce Health Data Privacy And Cybersecurity Concerns

Data privacy is another meaningful restraint because these platforms often sit close to health, behavioral, and employment information. In December 2024, it was stated that HIPAA privacy and security obligations apply when workplace wellness programs are offered through or on behalf of a group health plan, which creates a more demanding compliance standard for part of the buyer base.[4]Wellhub Editorial Team, “Wellness Solutions for International and Distributed Workforces, A Global HR Playbook,” Wellhub, wellhub.com In June 2025, mental health apps were also highlighted as expected to support strong controls, such as encryption and compliance with HIPAA and GDPR, reflecting how privacy design has become part of product credibility. These concerns lengthen sales cycles because buyers in healthcare, financial services, and public institutions often require formal documentation, security reviews, and strict internal approvals before deployment. The employee well-being platform market, therefore, faces a practical growth limit when smaller vendors lack the certifications, legal readiness, or architecture needed to pass enterprise privacy reviews.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Wellbeing Module: Mental Health Leads As Financial Wellbeing Gains Speed

Mental health and stress management accounted for 26.41% of the employee wellbeing platform market in 2025, making it the largest module, as employers see a direct connection between untreated mental health issues and lost work output. A stronger evidence base than many other modules supports that position. In 2024, it was reported that depression and anxiety lead to 12 billion lost working days every year and cost USD 1 trillion in productivity, which helps explain why employers keep prioritizing this part of the offer. In the employee wellbeing platform market, this module also benefits from a clearer pathway to clinically guided therapy, coaching, and digital triage, making it easier for buyers to justify spend in terms of outcomes.

Financial well-being is the fastest-growing module and is projected to expand at a 15.92% CAGR from 2026 to 2031, because employee financial strain increasingly affects performance, retention, and benefit use. Employers are broadening the scope of support beyond physical activity and nutrition, especially where debt pressure, inflation sensitivity, and out-of-pocket healthcare concerns weigh on the workforce. This change is pushing vendors to offer budgeting support, debt guidance, and benefit navigation alongside mental and physical health services. Fitness and physical activity, nutrition and weight management, and health risk assessment modules still matter, but they face more competition from benefit programs tied to chronic condition management and medication support. Other modules, including sleep health and social connection, are also gaining attention as the employee wellbeing platform industry moves toward a fuller view of burnout that includes recovery, isolation, and daily stress exposure, rather than focusing solely on workload.

By Deployment Model: Cloud Delivery Stays Dominant As Hybrid Models Advance

Cloud-based deployment held 71.23% of the employee wellbeing platform market share in 2025, and that lead reflects both workforce distribution and the practical advantages of software delivered as a service. Employers prefer cloud delivery because updates are easier to manage, user access is simpler to extend across locations, and integration with HR systems is more straightforward than in heavily customized local environments. This model also aligns with current buying patterns of faster rollouts, lighter internal IT lift, and more consistent employee access across offices and remote settings. In the employee wellbeing platform market, cloud deployment has become the standard for organizations seeking broad coverage without building local infrastructure in each geography.

On-premises deployment still has a place in parts of government, defense, and regulated financial services where data-handling rules are stricter and internal controls remain a hard requirement. Even so, hybrid deployment is emerging as the most dynamic architecture and is projected to grow at a 14.38% CAGR through 2031, as multinational employers seek both reach and tighter control over sensitive data. Hybrid configurations let vendors keep the employee-facing experience simple while giving buyers more say over where certain records are processed or stored. That balance matters in Europe, where data sovereignty and employee data rights have become part of the buying conversation, not just an issue for legal review after selection. The result is a more layered deployment picture in which the employee wellbeing platform industry still runs on cloud delivery, but growth increasingly comes from architectures that reduce cross-border risk and shorten internal approval cycles.

By Enterprise Size: Large Employers Hold Scale, SMEs Change The Growth Mix

Large enterprises accounted for 64.17% of the employee wellbeing platform market size in 2025, and their lead comes from earlier investment, broader benefit structures, and stronger internal ability to measure health-related cost outcomes. These employers usually have more mature HR technology stacks, more complex workforce needs, and more resources to connect wellbeing programs with claims, absence, and retention metrics. That combination supports larger contracts and longer relationships, even when competition intensifies. It also makes large buyers more demanding, since they expect deep integration, stronger privacy controls, and clearer evidence that a vendor can support multiple countries and workforce types.

Small and medium-sized enterprises are the fastest-growing segment and are projected to expand at a 16.44% CAGR from 2026 to 2031, shifting the growth mix of the employee wellbeing platform market. This expansion is being enabled by modular pricing, narrower product bundles, and simpler delivery models that lower the barrier to entry for employers without large internal teams. Smaller buyers are not following the same program design as large enterprises, and they tend to choose a focused mix centered on mental health and financial wellbeing where the link to retention and day-to-day stress is easiest to explain. In October 2025, one partnership reflected this shift by extending clinical-grade mental health access to employers with 50 to 1,000 employees, which widened access to services that had previously been easier for very large organizations to secure. As this part of the market expands, vendors will need to balance shorter contract cycles and simpler deployments with the same expectation for measurable results that larger buyers already demand.

By End User Industry Vertical: Healthcare Leads While Retail And E-Commerce Builds Momentum

Healthcare and life sciences held 21.88% share in 2025, the highest among verticals in the employee wellbeing platform market, because the sector faces both severe burnout exposure and a stronger ability to use outcome-based benefit models. Clinical and care delivery workforces operate under sustained stress, and many organizations in this vertical already have the data infrastructure needed to connect platform use with claims, productivity, and care access. In 2026, burnout among frontline clinical staff was reported at very high levels in recent workforce reviews, which helps explain why this vertical remains a priority buyer group. BFSI and government also represent meaningful demand pools, since financial firms carry high talent replacement costs and public sector employers face persistent pressure from workload, absence, and mental health exposure.

Retail and e-commerce are the fastest-growing verticals and are projected to rise at a 13.67% CAGR through 2031 as employers put more structure around frontline worker support. This shift matters because many earlier wellness programs were built for desk-based workforces and did not account for shift patterns, pay volatility, or the physical demands of roles in stores, fulfillment, and service. The category is now broadening because employers see these workers as an identifiable source of turnover cost and operational disruption rather than as a difficult population to engage. Education is also gaining pace as faculty and administrative burnout remains a live issue after years of strain, and industrial manufacturing is adopting more gradually as firms connect psychosocial risk management with broader safety programs. The public sector case is also clear, since the UK Office for National Statistics reported a 2.9% sickness absence rate in 2025 for the public sector compared with 1.7% in the private sector, which reinforces the cost case for structured support.

Geography Analysis

North America held 37.92% of the employee wellbeing platform market share in 2025, making it the largest regional market, as employer-sponsored healthcare and workforce cost management are closely linked across the region. The United States remains the anchor market, and its buyer behavior favors platforms that can show value in terms of medical cost pressure, mental health access, and daily productivity support. That pattern has pushed vendors to broaden their offerings beyond classic wellness content to include care navigation, chronic condition support, and more direct integration with benefits workflows. Canada is also important to the employee wellbeing platform market because scale is rising through acquisitions that expand covered lives and provider reach. In May 2025, a CAD 500 million acquisition (USD 350 million net of assumed debt) showed that regional scale is becoming increasingly important as buyers seek broader service depth and multinational support.

Mexico is moving into a more compliance-driven phase as employers respond to psychosocial risk obligations, which is widening the local buyer pool beyond very large organizations. This matters because the regional story is no longer limited to large U.S. employers and multinational headquarters, and it increasingly includes medium-sized employers that need easier deployment and localized support. The employee well-being platform market in North America, therefore, combines mature enterprise demand with newer adoption paths tied to regulation and workforce stabilization. Asia-Pacific is the fastest-growing region, projected to expand at a 16.73% CAGR from 2026 to 2031, making it the most important growth corridor for many vendors. Growth in India is being supported by formal compliance changes and by employer interest in preventive health, gig worker support, and digital service delivery, even though product depth and ROI measurement remain uneven across buyers.

The broader Asia-Pacific picture is strengthened by persistent burnout exposure across both office and frontline workforces, which keeps demand elevated across Southeast Asia, Japan, South Korea, Australia, and New Zealand. In March 2026, multiple acquisitions in Australia showed that vendors see the region as large enough to justify consolidation and platform scale-building. Europe presents a more regulated demand environment, where data handling, employee consultation, and GDPR expectations shape vendor selection as much as product breadth. That creates a practical opening for providers that can offer regional data processing, formal privacy documentation, and a more localized deployment model. Outside Europe, the Middle East is gaining relevance as well-being tools become part of broader workforce development agendas, while Africa remains earlier in adoption and depends more heavily on insurers, multinationals, and digital employee assistance services to build the first layer of demand in the employee well-being platform market.

Competitive Landscape

The employee well-being platform market remains moderately fragmented, with a group of scaled specialists holding visible enterprise positions but no single provider controlling the category. Lyra Health, Spring Health, Wellhub, Headspace, and BetterUp remain the most recognized names across mental health, coaching, and broader employee support, yet the market still contains many regional and module-led providers competing in narrower use cases. This structure means buyers can still choose between focused specialists and broader platforms, but it also means vendors face pressure to prove why they should remain part of a crowded benefits stack. Competitive advantage increasingly comes from clinical depth, data security readiness, integration with HR systems, and the ability to demonstrate outcome evidence rather than simple engagement counts. As a result, the employee well-being platform market is shifting from product availability to execution quality and buyer trust.

One of the clearest strategic themes has been movement toward broader care continuity. In January 2026, Spring Health announced its agreement to acquire Alma, a step that expanded its access to provider networks and pushed its platform further beyond standalone digital support. Lyra Health has followed a similar path, combining acquisitions with partnerships, and in January 2026, linked its platform to Carrum Health to connect mental health services with specialty care pathways for surgery, cancer, and substance use disorder treatment. These moves matter because large employers increasingly prefer fewer vendors that can coordinate across care needs rather than separate tools that each solve only one part of the problem. The employee well-being platform market, therefore, rewards vendors that can extend from coaching and therapy into navigation, provider access, and recovery support.

Another source of competitive pressure comes from HR software ecosystems, because those vendors already sit within benefits administration and employee workflows. Specialist platforms still have room to win, but they now need stronger partnerships and deeper integrations to avoid being pushed to the edge of the decision process. Lyra Health’s designation as the Workday Wellness Preferred Mental Health Partner in March 2026 showed how specialist vendors are responding by linking clinical depth with the reach of established HR platforms. At the same time, CoreHealth Technologies launched CoreHealth NOW in September 2025 to reduce implementation complexity and lower adoption barriers for buyers who wanted faster deployment. White space remains strongest in frontline worker support, smaller employer packages, and programs tied to chronic condition management, which means the next stage of competition in the employee wellbeing platform market is likely to be shaped as much by distribution and usability as by clinical breadth.

Employee Wellbeing Platform Industry Leaders

Personify Health, Inc.

WellSteps, LLC

Headspace Inc.

Gympass US, LLC

Spring Care, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Spring Health launched Guide, an AI-led care tool showing 25% better symptom improvement and 60% therapy engagement.

- March 2026: Spectrum.Life entered Australia via acquisitions (MindFit at Work, We Lysn, Valion Health), adding 100 new roles.

- January 2026: Lyra Health and Carrum Health integrated specialty care with mental health, linking navigation to recovery pathways.

- November 2025: Lyra Health partnered with Thatch to offer therapy and coaching through ICHRAs for 2026 plans.

Global Employee Wellbeing Platform Market Report Scope

The Employee Wellbeing Platform Market comprises digital platforms and services that help organizations promote and manage employee health, wellness, and overall well-being. These solutions typically cover modules such as health risk assessments, mental health and stress management, fitness and physical activity, nutrition and weight management, and financial wellbeing. Available through cloud-based or on-premises deployment models, they serve both large enterprises and SMEs across industries, including BFSI, healthcare, retail, manufacturing, government, and education. The primary goal is to enhance employee engagement, reduce absenteeism, and foster a healthier, more productive workforce.

The Employee Wellbeing Platform Market is segmented by Wellbeing Module (Health Risk Assessment and Screening, Mental Health and Stress Management, Fitness and Physical Activity, Nutrition and Weight Management, Financial Wellbeing, and Other Wellbeing Modules), Deployment Model (Cloud-Based and On-Premises), Enterprise Size (Large Enterprises and Small and Medium-Sized Enterprises), End-user Industry Vertical (BFSI, Healthcare and Life Sciences, Retail and E-commerce, Industrial Manufacturing, Government and Public Sector, Education, and Other End-user Industries), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Health Risk Assessment and Screening |

| Mental Health and Stress Management |

| Fitness and Physical Activity |

| Nutrition and Weight Management |

| Financial Wellbeing |

| Other Wellbeing Modules |

| Cloud-Based |

| On-Premises |

| Large Enterprises |

| Small and Medium-Sized Enterprises |

| BFSI |

| Healthcare and Life Sciences |

| Retail and E-commerce |

| Industrial Manufacturing |

| Government and Public Sector |

| Education |

| Other End-user Industries |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia and New Zealand | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Rest of Africa |

| By Wellbeing Module | Health Risk Assessment and Screening | |

| Mental Health and Stress Management | ||

| Fitness and Physical Activity | ||

| Nutrition and Weight Management | ||

| Financial Wellbeing | ||

| Other Wellbeing Modules | ||

| By Deployment Model | Cloud-Based | |

| On-Premises | ||

| By Enterprise Size | Large Enterprises | |

| Small and Medium-Sized Enterprises | ||

| By End User Industry Vertical | BFSI | |

| Healthcare and Life Sciences | ||

| Retail and E-commerce | ||

| Industrial Manufacturing | ||

| Government and Public Sector | ||

| Education | ||

| Other End-user Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia and New Zealand | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current and forecast value of the employee wellbeing platform market?

The employee wellbeing platform market stands at USD 2.13 billion in 2026 and is projected to reach USD 3.95 billion by 2031, growing at a CAGR of 13.15%.

Which wellbeing module leads demand today?

Mental health and stress management held the largest share at 26.41% in 2025 because employers now link mental health support more directly to productivity, retention, and cost control.

Which buyer segment is expanding the fastest?

Small and medium-sized enterprises are the fastest-growing enterprise group, with a projected CAGR of 16.44% from 2026 to 2031 as modular SaaS pricing and simpler delivery lower adoption barriers.

Why is North America still the largest regional opportunity?

North America held 37.92% share in 2025 because employer-sponsored healthcare costs, claims management, and wellbeing investment are closely connected, especially in the United States.

Which industry vertical is creating the strongest near-term growth opening?

Retail and e-commerce is the fastest-growing vertical at a 13.67% CAGR through 2031 as employers put more focus on turnover, financial stress, and frontline worker support.

What is the biggest challenge vendors still face?

Sustained engagement remains the main hurdle because many employers still struggle to move usage beyond the first launch phase, which makes ROI proof harder at renewal time.

Page last updated on: