Europe HR Compliance And General Data Protection Regulation (GDPR) Platform Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

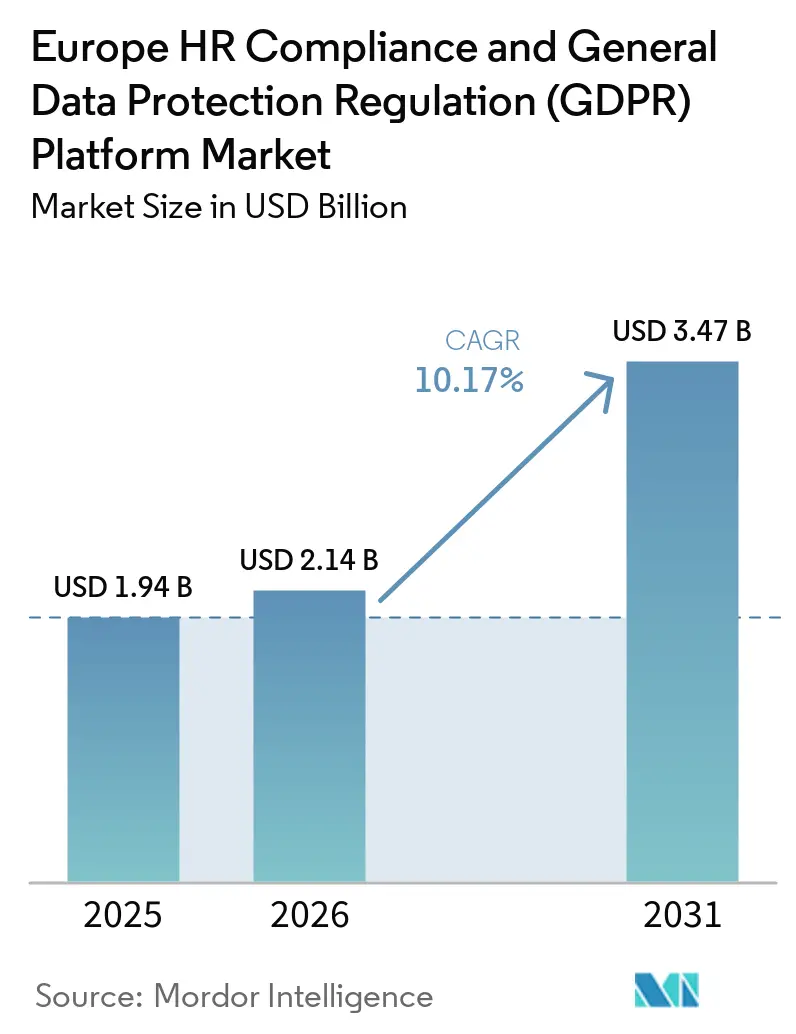

| Base Year Market Size (2025) | USD 1.94 Billion |

| Market Size (2026) | USD 2.14 Billion |

| Market Size (2031) | USD 3.47 Billion |

| Growth Rate (2026 - 2031) | 10.17% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe HR Compliance And General Data Protection Regulation (GDPR) Platform Market Analysis by Mordor Intelligence

The Europe HR compliance and General Data Protection Regulation (GDPR) platform market size was valued at USD 1.94 billion in 2025 and is projected to reach USD 3.47 billion by 2031, expanding at a CAGR of 10.17% from 2026 to 2031. Persistent GDPR enforcement pressure has moved compliance platform spending beyond a discretionary IT decision into core enterprise budgeting, especially as fines remained very high in 2025. The August 2, 2026, enforcement deadline for Annex III high-risk AI systems under the EU AI Act, together with the June 7, 2026, entry into force of the EU Pay Transparency Directive, shortened the period in which employers could delay platform upgrades. These overlapping obligations across privacy, labor law, payroll governance, and algorithm oversight gave the Europe HR compliance and General Data Protection Regulation platform market a demand profile distinct from that of other regions. Hybrid deployment demand, sovereign-cloud availability, and rising mid-market buying activity also widened the addressable customer base during the period. At the same time, the Europe HR compliance and GDPR platform market remained moderately fragmented, which supported room for both enterprise suites and regionally focused specialists that can deliver automated updates and country-specific configurations.

Key Report Takeaways

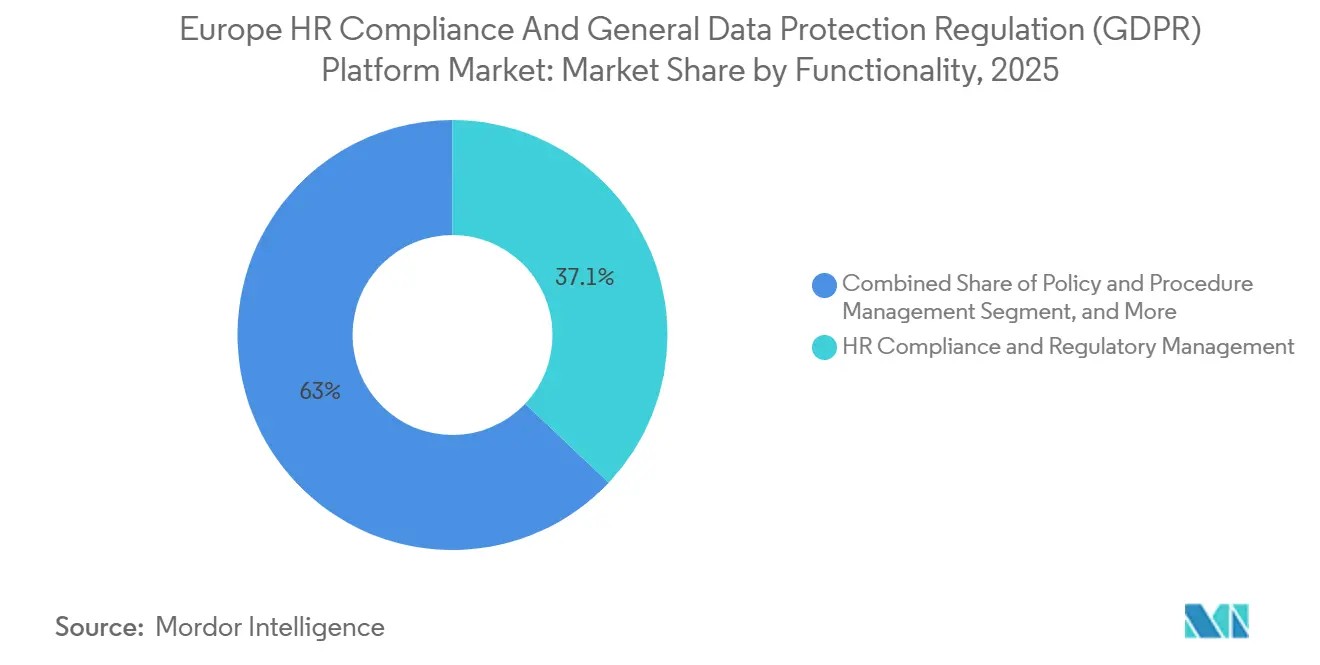

- By functionality, HR Compliance and Regulatory Management held 37.05% of the Europe HR compliance and General Data Protection Regulation (GDPR) platform market in 2025, while Time and Attendance Compliance is projected to expand at an 11.38% CAGR through 2031.

- By deployment mode, Cloud accounted for 68.11% of spending of the Europe HR compliance and GDPR platform market in 2025, while Hybrid is expected to record the fastest growth, with a 11.71% CAGR from 2026 to 2031.

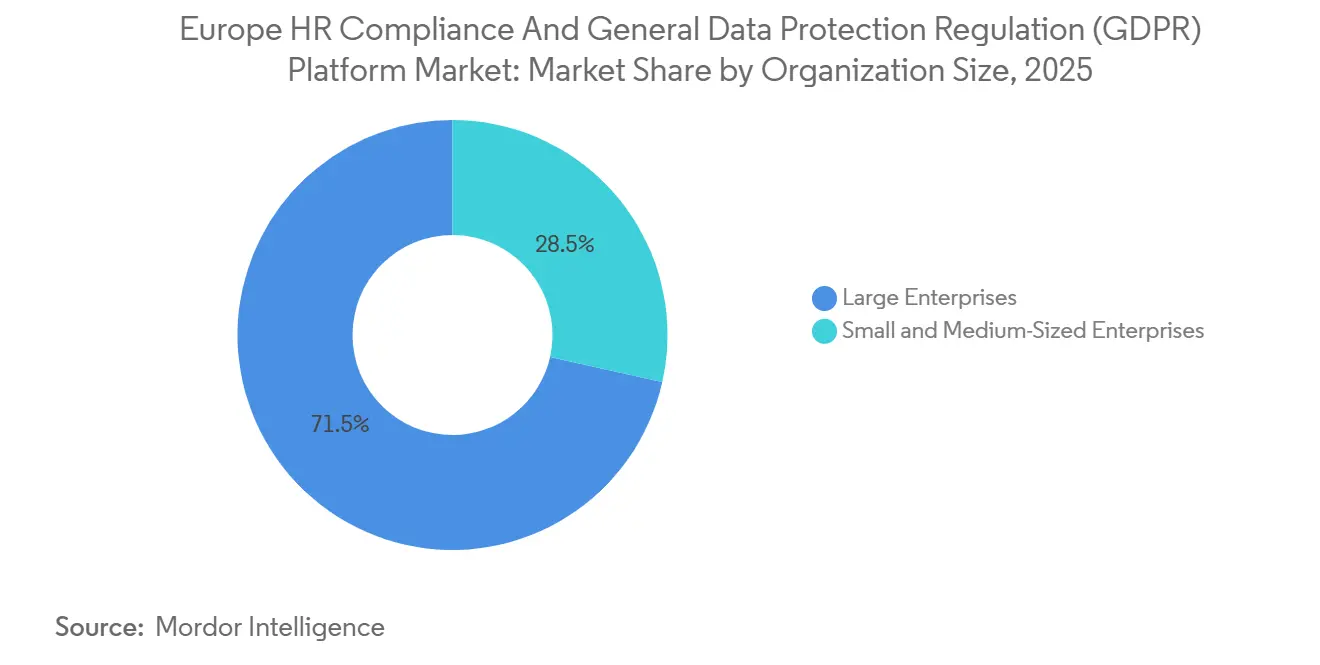

- By organization size, Large Enterprises represented 71.49% of demand of the Europe HR compliance and GDPR platform market in 2025, while SMEs are projected to grow at a 12.09% CAGR through 2031.

- By end-user, Information Technology and Telecommunications captured 29.41% of demand of the Europe HR compliance and General Data Protection Regulation platform market in 2025, while Healthcare and Life Sciences are forecast to advance at a 10.56% CAGR through 2031.

- By geography, the United Kingdom held 30.16% of the Europe HR compliance and General Data Protection Regulation (GDPR) platform market in 2025, while Germany is projected to expand at a 10.91% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe HR Compliance And General Data Protection Regulation (GDPR) Platform Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent GDPR Enforcement and Rising Non-Compliance Penalties | +2.3% | EU-wide, with enforcement concentration in Ireland, France, and Germany | Medium term (2-4 years) |

| Multi-Country Labor-Law and Payroll Localization Complexity | +2.0% | EU Core, Germany, France, Italy, Spain, Netherlands, with spill-over to CEE | Long term (≥ 4 years) |

| Cloud Migration and Digitization of HR and Privacy Workflows | +1.7% | EU-wide, with early adoption gains in UK, Nordics, and Benelux | Short term (≤ 2 years) |

| Rising Data Subject Access Request and Consent-Management Volumes | +1.4% | EU-wide, with elevated volumes in UK, Germany, and France | Medium term (2-4 years) |

| EU Pay Transparency Directive Expanding Audit-Ready HR Data Requirements | +1.1% | EU-27, with early compliance activity in Belgium, France, and Spain | Short term (≤ 2 years) |

| EU AI Act Obligations For Recruitment and Worker-Management Systems | +0.8% | EU-wide, with concentration in IT, Financial Services, and Healthcare sectors | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent GDPR Enforcement and Rising Non-Compliance Penalties

National data protection authorities across Europe imposed EUR 1.14 billion (USD 1.28 billion) in GDPR fines in 2025, keeping enforcement risk at a level few employers could ignore. The same annual report recorded 414 new cross-border cases and 1,299 One-Stop-Shop procedures in 2025, indicating that enforcement activity is broad and costly. This environment pushed the Europe HR compliance and General Data Protection Regulation (GDPR) platform market toward tools that can document controls, decisions, and audit trails at the workflow level rather than only in policy files. Vendors also had stronger reasons to tighten security design, contractual safeguards, and evidence management, as customers increasingly evaluated products through the lens of regulatory scrutiny. The result was a buying pattern that favored platforms able to show continuous governance, cleaner records of processing, and easier proof of technical and organizational measures. That shift supported adoption even in organizations that had already completed an earlier round of privacy tooling and now needed something more integrated.

Multi-Country Labor-Law and Payroll Localization Complexity

Managing compliance across 27 EU member states remained a major reason employers invested in broader platforms instead of single-country tools. This pressure went beyond GDPR because labor laws, payroll rules, collective agreements, and employee data expectations varied widely across jurisdictions and changed at different paces. The Europe HR compliance and General Data Protection Regulation (GDPR) platform market, therefore, rewarded vendors that could maintain country-level legislative content and deliver updates without long customer-side deployment cycles. SD Worx reinforced this direction in April 2026 when it launched Legal Watch, an AI-based monitoring platform initially covering Germany, Luxembourg, Spain, Sweden, and the Netherlands. Buyers increasingly treated regulatory depth as a primary product feature because weak localization creates exposure across payroll, leave management, compensation reporting, and worker documentation. That dynamic helped multi-country platforms defend higher pricing and stronger retention than narrower alternatives.

Cloud Migration and Digitization of HR and Privacy Workflows

Cloud adoption in this space was no longer driven only by cost or convenience, because employers also needed faster compliance updates and cleaner evidence trails. SD Worx reported in 2025 that 3 in 10 European companies used AI in payroll and that 47% increased investment to keep up with changing labor legislation. That shift supported the Europe HR compliance and General Data Protection Regulation platform market because subscription architectures are better suited to ongoing rule changes than static deployments. Workday strengthened the sovereign-cloud option in November 2025 by launching Workday EU Sovereign Cloud with EU-hosted infrastructure, EU-based personnel, and independent audit oversight. The AWS European Sovereign Cloud also went live in Brandenburg in January 2026, and aconso positioned HR document management on that infrastructure with end-to-end encryption, role-based controls, and compliant archiving. As a result, cloud-native and hybrid models became easier to justify for regulated employers that had previously kept sensitive HR workloads on-premises.

Rising Data Subject Access Request and Consent-Management Volumes

The right of access remained a practical workload issue for employers because regulators continued to test whether organizations could respond accurately and on time. The EDPB's coordinated enforcement work on the right of access identified implementation gaps following the action, involving 764 controllers across 32 data protection authorities.[1]European Federation of Data Protection Officers, “CEF 2024, EDPB Identifies Challenges to the Full Implementation of the Right of Access,” EFDPO, efdpo.eu That pattern mattered for the Europe HR compliance and GDPR platform market because employee requests often involve HR records, disciplinary files, and identity data that span several systems. It also increased the appeal of unified governance layers that handle permissions, access, consent records, and request workflows across environments. Over time, this reduced the case for maintaining separate privacy tools and separate HR compliance tools when both sets of data had to be governed together. The demand moved toward integrated suites that can connect access rights, policy controls, and data location across the full employee record.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Integration Costs Across Legacy HRIS, Payroll, and ERP Stacks | -1.6% | EU-wide, most acute in Germany, Italy, and France where legacy ERP penetration is highest | Medium term (2-4 years) |

| Shortage of Privacy, Payroll, and Compliance Specialists | -1.3% | EU-wide, most acute in CEE and Southern Europe, moderate impact in UK and Germany | Long term (≥ 4 years) |

| NIS2 and DORA Vendor-Assurance Burdens Raising Proof-and-Control Costs | -0.9% | EU-wide, most acute in Financial Services, Healthcare, and digital infrastructure sectors | Medium term (2-4 years) |

| German Works Council and Employee-Data Transfer Scrutiny Slowing Rollouts | -0.6% | Germany, Austria, and Netherlands, co-determination jurisdictions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Integration Costs Across Legacy HRIS, Payroll, and ERP Stacks

Integration remained the clearest near-term brake on adoption because many employers still ran mixed estates of HRIS, payroll, ERP, and time systems from different generations. That problem was especially evident in multi-country rollouts, where compliance data had to be consistently moved across legacy payroll engines, local attendance tools, and central reporting layers. The Europe HR compliance and General Data Protection Regulation (GDPR) platform market, therefore, favored vendors with stronger native connectors, pre-built country packs, and simpler implementation paths. Buyers were also more cautious after the May 2025 ruling by the German Federal Labor Court, which awarded an employee EUR 200 (USD 224.6) in non-material damages for a cloud-based HR system that transferred personal data beyond the scope of an applicable works agreement. The case reinforced that integration is not only a technical issue because weak governance around transfers can create direct legal risk during deployment. That kept purchasing interest strong, but it also slowed the pace at which projects could move from contract signing to full operation.

Shortage of Privacy, Payroll, and Compliance Specialists

A structural shortage of privacy, payroll, and compliance specialists continued to extend implementation timelines across the region. The issue was more severe in Central and Southern Europe, where specialist labor pools were thinner than in the UK or Germany, and mid-sized employers had less room to absorb consulting costs. This created an unusual pattern in the Europe HR compliance and GDPR platform market, as the same skills shortage raised demand for automation while also making deployment more difficult. Vendors that embedded guided onboarding, policy templates, and country-specific workflows were better placed to keep projects moving with smaller customer teams. The shortage also strengthened demand for platforms that could reduce manual interpretation work across pay reporting, privacy responses, and HR recordkeeping. In practice, products that reduced reliance on scarce specialists became more attractive than those that offered broad functionality but required deep in-house expertise.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Functionality: HR Compliance Leads Amid Growing Specialty Demand

HR Compliance and Regulatory Management held 37.05% of the Europe HR compliance and General Data Protection Regulation (GDPR) market share in 2025, making it the largest functional category. That position reflected the fact that labor-law tracking, employee recordkeeping, and GDPR accountability are baseline requirements for nearly every employer in the region. The Europe HR compliance and General Data Protection Regulation (GDPR) platform market continued to direct first-time platform budgets toward this category, as one license can support multiple statutory obligations simultaneously. That breadth gave the segment an advantage over narrower tools that solve only one issue in isolation.

Time and Attendance Compliance is projected to grow at a 11.38% CAGR from 2026 to 2031, making it the fastest-growing functionality during this period. Growth came from working-time documentation needs, more detailed leave governance, and rising pressure to keep auditable records across countries with different rules. Vendors increasingly added locally compliant leave configuration and gender pay gap analytics templates, demonstrating how attendance, compensation, and reporting requirements are starting to overlap within the same workflow. GDPR Data Privacy Management, Policy, and Procedure Management also continued to attract replacement demand as employers consolidated single-point tools into broader suites. Pay Transparency and Compensation Compliance remained smaller in current revenue terms, but the June 2027 reporting cycle for employers with 150 or more employees kept near-term buying interest firm.

By Deployment Mode: Cloud Holds the Lead While Hybrid Gains Speed

Cloud deployment accounted for 68.11% of the Europe HR compliance and General Data Protection Regulation (GDPR) market size in 2025, which kept it as the leading delivery model. This reflected the clear operating advantage of subscription SaaS platforms, where vendors can push regulatory content updates without waiting for customer-side IT release cycles. The Europe HR compliance and General Data Protection Regulation (GDPR) platform market also benefited from a better sovereign-cloud foundation, which reduced a long-standing obstacle around data residency. Workday EU Sovereign Cloud and the AWS European Sovereign Cloud both helped shift the discussion from whether cloud could meet compliance expectations to how cloud should be structured for regulated HR workloads.

Hybrid deployment is forecast to grow at an 11.71% CAGR from 2026 to 2031, which made it the fastest-growing mode. This pattern fit employers in financial services and healthcare that wanted cloud flexibility for newer compliance modules while retaining tighter control over their most sensitive data layers. Hybrid is also suited to organizations subject to country-level scrutiny of employee data transfers, especially where local review bodies expect more detailed governance of processing arrangements. On-premises demand continued to decline as a standalone preference, even though it remained relevant in the most tightly controlled environments. Security certifications such as ISO 27001 and SOC 2 Type II also became stronger procurement filters, narrowing the field to vendors that could evidence infrastructure controls and application features.

By Organization Size: Large Enterprises Still Dominate While SMEs Expand Faster

Large Enterprises captured 71.49% of the Europe HR compliance and General Data Protection Regulation (GDPR) market in 2025, reflecting their broader geographic exposure and larger software budgets. Their position also came from the fact that scale increases the operational weight of GDPR accountability, internal reporting, and cross-border workforce governance. The Europe HR compliance and General Data Protection Regulation (GDPR) platform market, therefore, remained anchored in organizations that manage high volumes of employee data across multiple jurisdictions. These buyers were more likely to pursue integrated platforms because the cost of fragmented controls grows quickly when HR, payroll, and privacy obligations intersect.

SMEs are projected to expand at a 12.09% CAGR from 2026 to 2031, making them the fastest-growing segment by organization size. The main reason was regulatory equalization, as the EU Pay Transparency Directive's 100-employee threshold brought many mid-market firms within formal audit and reporting requirements once associated mainly with larger groups. That change widened the addressable base for the Europe HR compliance and General Data Protection Regulation (GDPR) industry, especially among employers that needed practical templates more than deep customization. SME uptake also had room to rise because AI-enabled HR tools were still less common in smaller firms than in large companies. Vendors that combined lower per-employee pricing with faster onboarding and pre-built EU labor-law templates were in a stronger position to convert this demand into signed contracts.

By End-User Industry: IT and Telecom Leads While Healthcare and Life Sciences Moves Ahead

Information Technology and Telecommunications held 29.41% of the Europe HR compliance and General Data Protection Regulation (GDPR) market share in 2025, making it the largest end-user segment. This sector processes high volumes of employee and candidate data and has been early in adopting AI-enabled recruiting and workforce tools, which increased compliance workload across privacy and algorithm governance. The Europe HR compliance and General Data Protection Regulation (GDPR) industry therefore saw some of its earliest demand from employers that had to connect GDPR controls with AI-related documentation and operational monitoring. That mix kept IT and telecom at the front of spending even as other sectors increased their buying activity.

Healthcare and Life Sciences are projected to grow at a 10.56% CAGR from 2026 to 2031, making it the fastest-growing vertical. The EHDS Regulation 2025/327 entered into force in March 2025 and added a sector-specific governance layer on top of baseline GDPR obligations.[2]European Commission, “European Health Data Space Regulation,” European Commission, health.ec.europa.eu That pushed healthcare organizations toward platform setups that can align HR data governance with broader organizational data responsibilities. BFSI also faced dense obligations through privacy, operational resilience, and third-party control requirements, which kept compliance spend per employee high. Manufacturing, Retail and E-commerce, and Government and Public Sector remained important demand pools, although many buyers in those sectors stayed more price-sensitive and often preferred to extend existing enterprise software relationships rather than buy a new standalone platform.

Geography Analysis

The United Kingdom accounted for 30.16% of the Europe HR compliance and General Data Protection Regulation (GDPR) market in 2025, making it the largest national market in the region. Its position reflected a strong corporate compliance foundation and the ongoing complexity of aligning UK and EU GDPR requirements for employers with cross-border operations. Germany is projected to grow at a 10.91% CAGR from 2026 to 2031, giving it the fastest expansion rate in the Europe HR compliance and General Data Protection Regulation (GDPR) market size over the forecast period. That momentum came from the combined pressure of GDPR accountability, co-determination rights over HR technology, NIS2 transposition, and DORA obligations for financial-sector employers. The German Federal Labor Court's May 2025 ruling strengthened this pressure by confirming that works agreements cannot legitimize GDPR-non-compliant employee data transfers, thereby increasing the value of auditable transfer governance at the platform level.

France remained one of the most heavily enforced GDPR jurisdictions in Europe, with the EDPB reporting fines totaling EUR 486.85 million (USD 546.6 million) across 84 cases in 2025. This level of enforcement supported steady demand for tooling that can handle privacy governance and audit readiness in large French organizations. France also requires a BDESE database covering pay and workforce data, underscoring the need for a country-specific HR data architecture beyond a standard GDPR module. Italy and Spain represented meaningful mid-market openings because many employers are now building pay-gap audit capacity for the June 2027 reporting cycle. Spain added urgency with a high volume of enforcement activity in 2025, reinforcing demand from regulated employers for cleaner compensation records and stronger controls.

Russia remained structurally different because domestic data localization rules create separate deployment demands for multinationals operating there. This made Russia-related data flows one of the more sensitive compliance issues in the wider Europe HR compliance and General Data Protection Regulation (GDPR) platform market. The Rest of Europe group, including the Nordics, Benelux, Central and Eastern Europe, and the Baltics, showed a different growth mix, with mature digital infrastructure in the north and a lower installed base in CEE. That combination enabled faster adoption of SME-focused platforms that can localize quickly and keep pricing within reach for employers who historically underused enterprise compliance software.

Competitive Landscape

The Europe HR compliance and General Data Protection Regulation (GDPR) platform market remained moderately fragmented, and no vendor held a dominant position across all functional categories. OneTrust remained prominent in privacy governance and expanded further into AI-ready compliance in March 2026, introducing real-time monitoring and enforcement across AI agents, models, and data. Personio, SD Worx People Solutions NV, and Deel served different parts of the market, with Personio focused on SMEs, SD Worx stronger in multi-country payroll compliance, and Deel addressing distributed-workforce needs across a broad geographic footprint. This kept competition active across both customer size and product scope. It also meant buyers could choose between platforms built for regional regulatory depth and platforms built for broader cross-border workforce administration.

Competitive positioning is increasingly split between full-suite vendors that emphasize regulatory breadth and specialists that focus on the most time-intensive workflows. BigID used this opening in March 2026 by launching Unified Privacy Management for People Data and AI, combining people-data discovery, rights automation, consent enforcement, and AI privacy governance into a single audit-ready environment. Transcend was followed by Agentic Assist and the Transcend MCP Server, which enabled enterprises to initiate requests, run assessments, and manage consent configurations for AI tools. Workday also made a strategic move with its EU Sovereign Cloud, which gave regulated employers a stronger route into cloud deployment without stepping outside EU-hosted control and support structures.[3]Workday, “Workday Launches Workday EU Sovereign Cloud to Unlock Enterprise AI with Full EU Data Residency and Control,” Workday Newsroom, newsroom.workday.com These moves raised the bar on what buyers expect from platform evidence, integration, and data-sovereignty design.

White-space opportunities remained visible in employee-facing consent orchestration, contingent-workforce payroll compliance, and affordable bundles that combine Pay Transparency, AI governance, and GDPR tooling. Papaya Global addressed part of that opportunity in January 2026 with the launch of its Banco Wallet, enabling compliant, real-time workforce payments across multiple countries. Remote also expanded its proposition in June 2025 by launching an HRIS built for local labor law compliance across globally distributed teams. As the August 2026 EU AI Act deadline approached, buyers increasingly sought vendors that could provide a single, audit-ready interface across multiple compliance categories, giving multi-module platforms a practical advantage over narrow point solutions.

Europe HR Compliance And General Data Protection Regulation (GDPR) Platform Industry Leaders

OneTrust, LLC

Deel Inc.

Papaya Global Ltd.

TrustArc Inc.

Securiti, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: SD Worx launched SD Worx Legal Watch, an AI-powered regulatory monitoring platform developed with AI specialist Faktion, initially covering Germany, Luxembourg, Spain, Sweden, and the Netherlands. The solution translates labor-law changes into actionable compliance insights in near real time, directly addressing multi-country regulatory localization complexity for large enterprise HR and payroll teams.

- March 2026: OneTrust expanded its AI-Ready Governance Platform to include real-time monitoring and enforcement across AI agents, models, and data, enabling organizations to shift AI governance from static compliance workflows to a continuous control plane, a capability directly aligned with EU AI Act Annex III deployer obligations effective August 2026.

- March 2026: BigID announced Unified Privacy Management for People Data and AI, combining personal data discovery, data subject rights automation, consent enforcement, and AI privacy governance in a single audit-ready platform, targeting the employee data compliance gap between GDPR recordkeeping and emerging AI Act documentation requirements.

- March 2026: Transcend launched Agentic Assist and the Transcend MCP Server, enabling enterprises to initiate data subject requests, run privacy assessments, and manage consent configurations directly from AI tools, including Copilot and Claude, reducing manual DSAR processing overhead and compressing compliance cycle times for privacy and HR operations teams.

Europe HR Compliance And General Data Protection Regulation (GDPR) Platform Market Report Scope

The Europe HR Compliance and General Data Protection Regulation (GDPR) Platform provides solutions to help organizations navigate workforce regulations and data protection laws, especially under the EU’s GDPR. These platforms oversee employee data privacy, consent, and rights, as well as compliance reporting, while also managing broader HR compliance tasks such as policy oversight and case tracking. They guarantee the secure management of employee data across the EU's cross-border operations. The market's growth is propelled by stringent regulatory enforcement, heightened data privacy concerns, and a surge in demand for systems ready for audits.

The Europe HR Compliance and General Data Protection Regulation (GDPR) Platform Market Report is Segmented by Functionality (HR Compliance and Regulatory Management, Time and Attendance Compliance, Policy and Procedure Management, GDPR Data Privacy Management, Pay Transparency and Compensation Compliance, and Other Functionalities), Deployment Mode (Cloud, On-Premises, and Hybrid), Organization Size (Large Enterprises, and Small and Medium-Sized Enterprises), End-User Industry (Banking, Financial Services and Insurance, Healthcare and Life Sciences, Information Technology and Telecommunications, Manufacturing, Retail and E-commerce, Government and Public Sector, and Other End-User Industries), and Geography (United Kingdom, Germany, France, Italy, Spain, Russia, and Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).

| HR Compliance and Regulatory Management |

| Time and Attendance Compliance |

| Policy and Procedure Management |

| GDPR Data Privacy Management |

| Pay Transparency and Compensation Compliance |

| Other Functionalities |

| Cloud |

| On-Premises |

| Hybrid |

| Large Enterprises |

| Small and Medium-Sized Enterprises |

| Banking, Financial Services and Insurance |

| Healthcare and Life Sciences |

| Information Technology and Telecommunications |

| Manufacturing |

| Retail and E-commerce |

| Government and Public Sector |

| Other End-User Industries |

| United Kingdom |

| Germany |

| France |

| Italy |

| Spain |

| Russia |

| Rest of Europe |

| By Functionality | HR Compliance and Regulatory Management |

| Time and Attendance Compliance | |

| Policy and Procedure Management | |

| GDPR Data Privacy Management | |

| Pay Transparency and Compensation Compliance | |

| Other Functionalities | |

| By Deployment Mode | Cloud |

| On-Premises | |

| Hybrid | |

| By Organization Size | Large Enterprises |

| Small and Medium-Sized Enterprises | |

| By End-User Industry | Banking, Financial Services and Insurance |

| Healthcare and Life Sciences | |

| Information Technology and Telecommunications | |

| Manufacturing | |

| Retail and E-commerce | |

| Government and Public Sector | |

| Other End-User Industries | |

| By Geography | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe |

Key Questions Answered in the Report

What is the size outlook for the Europe HR compliance and General Data Protection Regulation (GDPR) platform market?

The Europe HR compliance and General Data Protection Regulation (GDPR) platform market was valued at USD 1.94 billion in 2025 and is projected to reach USD 3.47 billion by 2031 at a 10.17% CAGR.

Which functionality leads spending in Europe HR compliance and GDPR platforms?

HR Compliance and Regulatory Management led functionality demand with a 37.05% share in 2025 because it covers the broadest set of overlapping labor-law and privacy obligations.

Which deployment model is gaining the most momentum across European employers?

Cloud remained the largest deployment type with 68.11% of spending in 2025, while Hybrid is projected to grow fastest at an 11.71% CAGR through 2031.

Why are SMEs becoming a more important customer group in this space?

SMEs are projected to grow at a 12.09% CAGR because the EU Pay Transparency Directive and wider compliance obligations now affect more mid-market employers than before.

Which end-user sector is spending the most on these platforms?

Information Technology and Telecommunications held 29.41% of demand in 2025, while Healthcare and Life Sciences is forecast to post the fastest growth at 10.56% through 2031.

Which European country offers the strongest near-term growth opportunity?

Germany is expected to grow fastest at a 10.91% CAGR through 2031, supported by overlapping GDPR, co-determination, NIS2, and DORA requirements.

Page last updated on: