Workforce Intelligence Platform Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

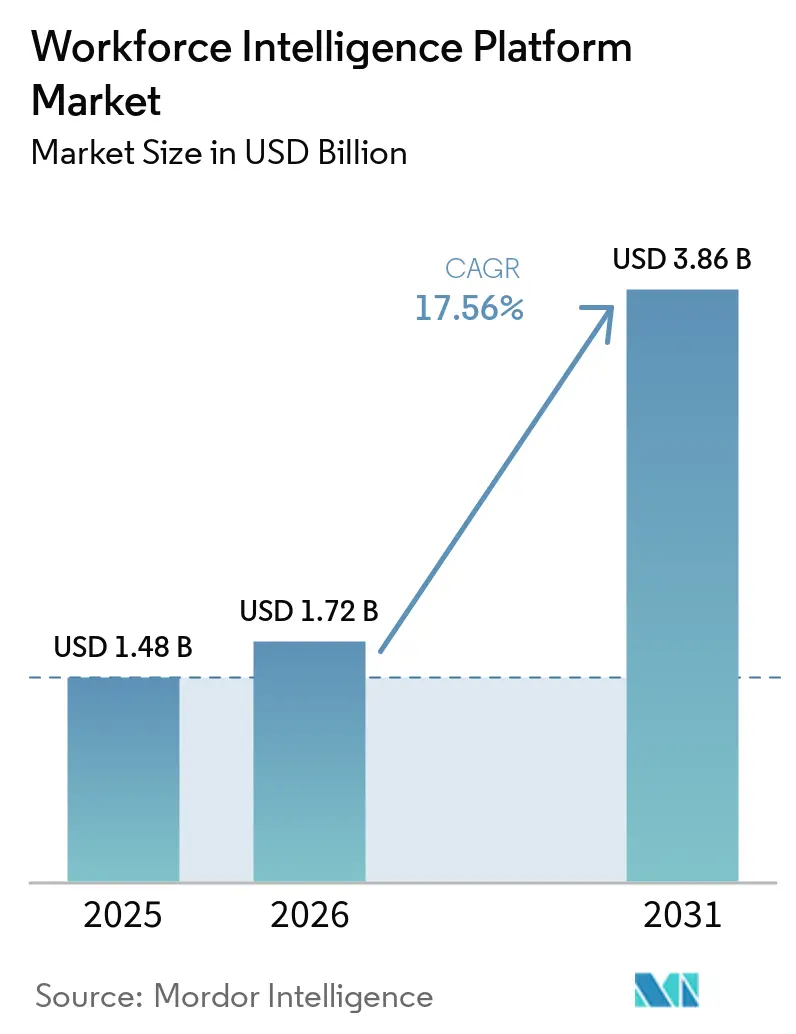

| Market Size (2026) | USD 1.72 Billion |

| Market Size (2031) | USD 3.86 Billion |

| Growth Rate (2026 - 2031) | 17.56% CAGR |

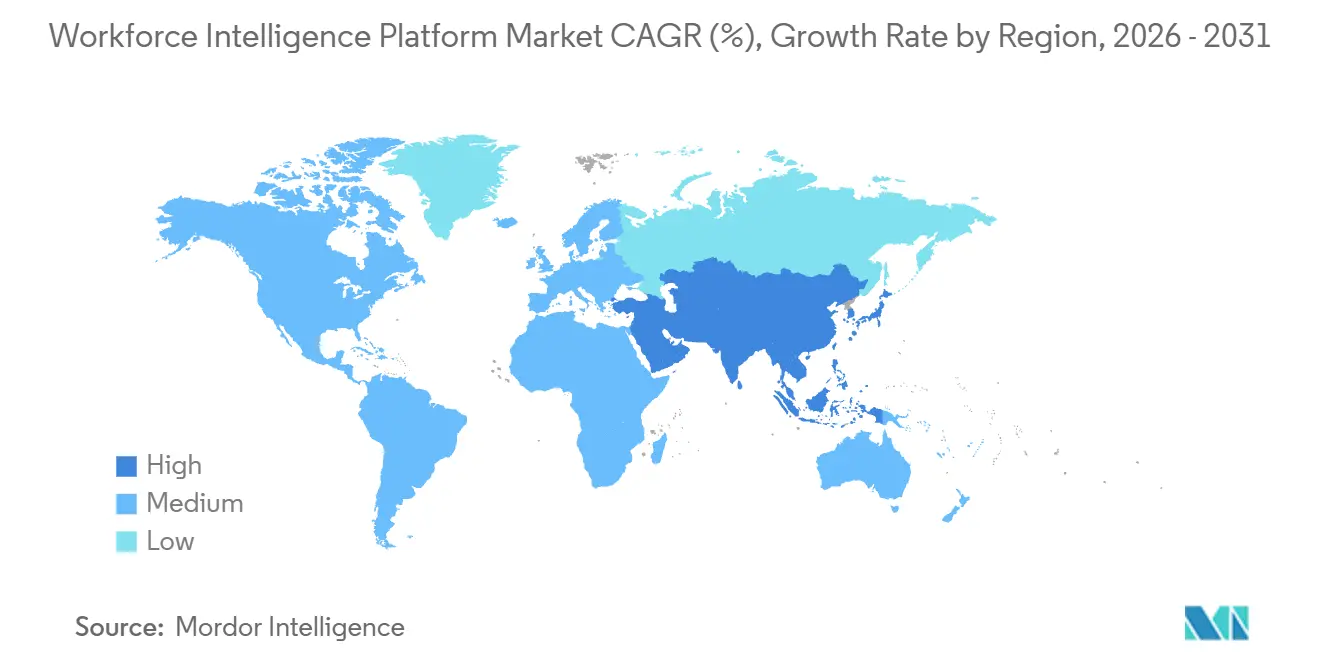

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Workforce Intelligence Platform Market Analysis by Mordor Intelligence

The workforce intelligence platform market was valued at USD 1.48 billion in 2025 and estimated to grow from USD 1.72 billion in 2026 to reach USD 3.86 billion by 2031, at a CAGR of 17.56% during the forecast period (2026-2031). This growth reflects a clear shift in how buyers define the role of these systems, as the workforce intelligence platform market is moving beyond periodic HR reporting and toward always-on decision support tied to business performance. Budget control is also broadening, because platform spending is now being evaluated by both HR and finance teams instead of sitting only within headcount administration. Demand is being shaped by predictive planning tools, skills-based operating models, and stronger pressure to connect labor decisions with productivity, cost, and restructuring outcomes. The workforce intelligence platform market is also gaining support from organizations that need internal mobility tools, scenario modeling, and governed AI outputs inside daily enterprise software. At the same time, adoption still depends on data quality, integration depth, and the ability of vendors to handle privacy rules and implementation complexity across different regions.

Key Report Takeaways

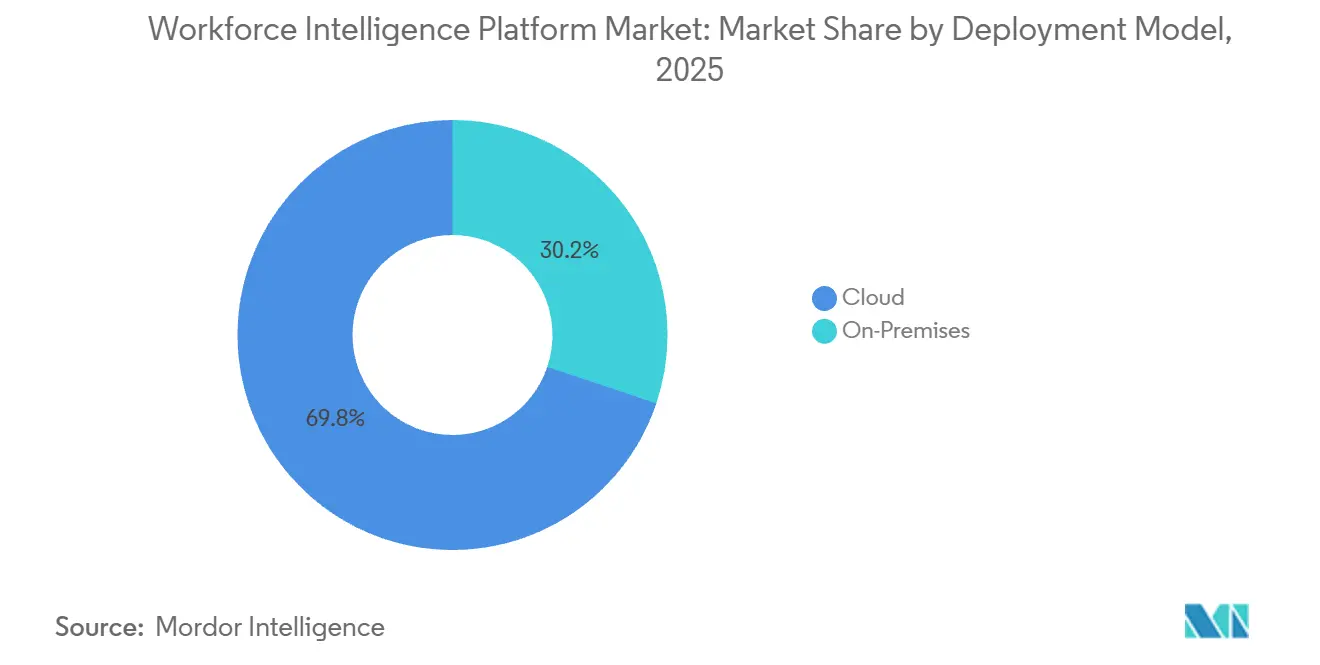

- By deployment model, cloud held 69.84% of the workforce intelligence platform market size in 2025, and cloud is also projected to expand at a 17.92% CAGR through 2031.

- By functionality, workforce analytics and reporting held 29.42% of the workforce intelligence platform market share in 2025, while talent mobility and skills intelligence is projected to grow at a 20.18% CAGR through 2031.

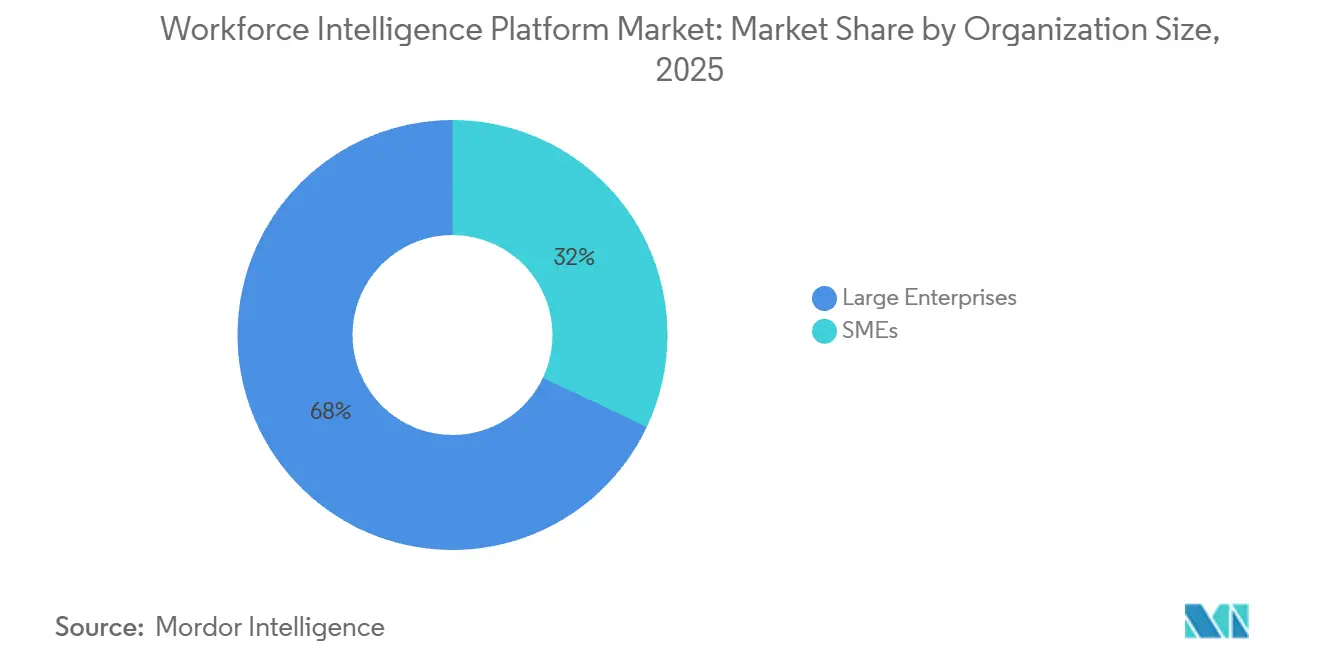

- By organization size, large enterprises accounted for 67.96% of revenue in 2025, while SMEs are expected to expand at an 18.44% CAGR through 2031.

- By end-user industry, IT and telecom led with 23.68% revenue share in 2025, while healthcare and life sciences is projected to advance at an 18.82% CAGR through 2031.

- By geography, North America held 40.74% of global revenue in 2025, while Asia-Pacific is projected to record the fastest regional CAGR at 19.64% through 2031 in the workforce intelligence platform market.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Workforce Intelligence Platform Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI-Enabled Predictive Workforce Planning in Core HR Workflows | +3.8% | Global, strongest in North America and Western Europe | Medium term (2-4 years) |

| Skills-Based Organization Programs Need Dynamic Skills Graphs | +3.2% | Global, rapid traction in India, UK, and Northern Europe | Long term (≥ 4 years) |

| Internal Talent Marketplaces Shift Spend from External Hiring | +2.6% | North America and Europe, accelerating in Asia-Pacific core | Medium term (2-4 years) |

| Strategic Workforce Planning Needs Rise Amid Labor and AI Disruption | +2.2% | Global, highest urgency in manufacturing-heavy markets | Short term (≤ 2 years) |

| CHRO-CFO Pressure for Workforce ROI and Capacity Visibility | +1.8% | North America and EU, spill-over to Asia-Pacific core | Short term (≤ 2 years) |

| HR-Finance-Payroll Integration Becomes a Buying Trigger | +1.4% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

AI-Enabled Predictive Workforce Planning in Core HR Workflows

The workforce intelligence platform market is being reshaped by buyer demand for planning tools that look ahead instead of only summarizing what has already happened. Betterworks' April 2026 Talent Intelligence Survey finds that only 16% of organizations operate with a truly predictive HR posture, which leaves a large opening for vendors that can move customers beyond dashboard-based reporting.[1]Betterworks, “2026 Talent Intelligence Survey: The Confidence Gap,” Betterworks, betterworks.com The same survey shows that 36% of respondents identified AI-driven skills inference from work and performance data as the single capability most likely to improve workforce decision-making, ranking it ahead of other options. SAP SuccessFactors' 1H 2026 release also treats skills governance as a core data discipline, which indicates that predictive capabilities are becoming expected platform features rather than optional premium add-ons. For the workforce intelligence platform market, this raises the standard for standalone vendors, because they now need stronger model accuracy, broader integrations, and better external data enrichment to defend pricing as suite vendors expand their native functionality.

Skills-Based Organization Programs Need Dynamic Skills Graphs

The workforce intelligence platform market is also benefiting from the wider move away from static job architecture and toward skills-based operating models. Skills-base finds that high-functioning organizations using verified skills data at scale maintain skill libraries that are 94.4% hard skills and reach a median 82% workforce assessment coverage, which shows how difficult it is to keep skills data current without machine-assisted inference. The workforce intelligence platform market is gaining from this gap because enterprises need platforms that can infer, refresh, and connect employee capabilities across distributed teams, local systems, and changing role structures. The business case is also growing in Europe, where evidence on structured workforce development is becoming more relevant for disclosure and governance processes tied to human capital reporting.

Internal Talent Marketplaces Redirect Spend from External Hiring

The workforce intelligence platform market is gaining support from finance leaders as internal talent marketplaces shift the discussion from talent programs to cost control. Gloat states that internal hires typically cost 50-70% less than external recruits and also reach full productivity faster, giving finance teams a direct way to model savings against open requisition pipelines.[2]Gloat, “Internal Mobility Agent,” Gloat, gloat.comBetterworks reports that more than 37% of survey respondents estimated annual avoidable losses from missed internal mobility at USD 500,000 to USD 2 million, while another 37% placed those losses at USD 2 million or more. Those figures often sit well above annual license costs, which changes how the workforce intelligence platform market is evaluated during procurement. Vendors such as Gloat, Eightfold AI, and Phenom are responding by tightening the connection between internal marketplace tools and skills inference engines, so matching can rely on inferred capabilities, project history, and adjacent skills instead of simple profile matching. This strengthens adoption because it connects workforce intelligence outputs directly to redeployment, internal hiring, and capacity planning.

Rising Strategic Workforce Planning Needs Amid Labor and AI Disruption

The workforce intelligence platform market is also being lifted by a planning environment that has become more continuous and less tied to the annual budget cycle. This change is more complex because employers now need to model the FTE effect of AI agents alongside conventional headcount decisions, which creates hybrid planning requirements that older HRIS architectures were not designed to manage. TalentNeuron's April 2026 launch of an Organizational Design capability reflects this need by linking internal structure to live labor market intelligence across 200+ markets and 65,000+ tracked skills. WTW notes in its 2026 Asia-Pacific workforce analysis that AI is helping HR teams build a unified source of truth for jobs, levels, and skills, while also supporting pay governance and internal mobility. For the workforce intelligence platform market, that means demand is no longer limited to reporting use cases, because organizations now need scenario tools that connect workforce redesign to changing labor availability and AI adoption.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Employee Data Privacy and Algorithmic Bias Scrutiny | -1.8% | EU and UK core, spill-over to North America and Asia-pacific | Short term (≤ 2 years) |

| Fragmented HR, Payroll, And Collaboration Data | -1.5% | Global, most acute in mid-market and Asia-pacific emerging markets | Medium term (2-4 years) |

| EU AI Act and Works Council Review Delays | -1.2% | EU member states, especially Germany, France, Belgium, Netherlands | Short term (≤ 2 years) |

| Vendor Service Pullback Extends Time to Value | -0.8% | Global, highest impact in mid-market deployments | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Employee Data Privacy and Algorithmic Bias Scrutiny

The workforce intelligence platform market faces procurement friction where employee monitoring, automated decision-making, and model explainability sit under close review. The EU AI Act, in force since August 2024, prohibits AI systems that infer emotions from biometric data in workplace settings, with penalties reaching EUR 35 million (USD 39.6 million) or 7% of annual global turnover for prohibited-practice violations. The same guidance explains that workforce intelligence systems tied to behavioral monitoring or fully automated personnel decisions can fall under high-risk classification, which brings stricter requirements for documentation, human oversight, and employee transparency. Bias concerns add another layer because models trained on historical HR records can reproduce long-standing inequality in pay, promotion, and work allocation. The workforce intelligence platform market, therefore, has a higher burden of proof in Europe and the UK, and that burden is increasingly affecting architecture choices, sales cycles, and buyer demand for governance controls.

Fragmented HR, Payroll, and Collaboration Data

The workforce intelligence platform market also faces a persistent technical barrier in the form of fragmented data across HRIS, payroll systems, collaboration tools, and learning platforms. Betterworks finds a large confidence gap in this area, with 90% of HR leaders saying their skills data is complete and accurate, even though three-quarters estimate that fewer than 75% of employee skills are actually captured in their systems. Only 20.9% of organizations update skills data continuously or in real time, which means many deployments rely on stale inputs that weaken the performance of predictive models. This problem becomes more severe when platforms use natural language processing across collaboration systems, because API inconsistency, access restrictions, and employee consent requirements can break the intelligence layer. In the workforce intelligence platform market, the impact is strongest in mid-market organizations and emerging Asia-Pacific environments, where local systems are often less interoperable, and vendors need heavier data engineering work before analytics can deliver business value.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Cloud Infrastructure Drives Platform Standardization

Cloud accounted for 69.84% of the workforce intelligence platform market in 2025, underscoring that buyers are prioritizing multi-tenant delivery models that support a common release cycle for AI features, connectors, and compliance updates. The workforce intelligence platform market has leaned toward the cloud because vendors can refresh models across the installed base without waiting for customers to run local upgrade projects. That release speed matters more as privacy requirements, skills taxonomies, and integration standards keep changing across enterprise environments. Cloud is also the fastest-growing deployment model, with the workforce intelligence platform market size for cloud projected to rise at a 17.92% CAGR through 2031. This growth is being supported by SME demand and by cloud-first organizations in Asia-Pacific that are adopting these platforms without carrying legacy on-premises architecture into the implementation cycle.

On-premises deployments still hold a defined role in the workforce intelligence platform industry, especially in government bodies, financial services institutions, and large enterprises working under strict sovereignty or security rules. These customers often delay full migration because raw HR records, payroll files, and access control requirements remain tied to older internal systems. Vendors are addressing that gap with hybrid approaches that keep sensitive data in local environments while shifting analytics and AI layers into the cloud for scale and model performance. ISO 27001 and SOC 2 Type II certifications have therefore become standard procurement signals rather than optional credentials for cloud vendors. In the workforce intelligence platform market, deployment choice now says as much about governance posture and integration readiness as it does about hosting preference.

By Functionality: Analytics Leads While Skills Intelligence Expands Faster

Workforce analytics and reporting held 29.42% of the workforce intelligence platform market share in 2025, which reflects the continued demand for headcount dashboards, attrition tracking, and manager self-service analytics across complex HR environments. This segment remains the anchor of the workforce intelligence platform market because it is often the first category that enterprises adopt before adding planning, mobility, and performance layers. Many organizations still need better visibility across fragmented systems, so reporting tools remain a practical entry point even when buyers plan to expand functionality later. At the same time, talent mobility and skills intelligence is projected to advance at a 20.18% CAGR through 2031, making it the fastest-growing functional segment in the workforce intelligence platform market. That faster growth shows that employers increasingly want tools that can map and act on workforce capability in real time instead of relying only on historical reporting.

Skills-base reports that organizations actively using verified skills data at scale maintain an average of 89 skills per role, achieve a median 82% workforce assessment coverage, and refresh skills data on a median 6-month cycle.[3]Skills-base, “Skills in Practice 2026: Evidence for Skills-Based Transformation,” Skills-base, skills-base.com Those benchmarks help explain why the workforce intelligence platform industry is moving toward richer skills engines and away from static profile databases. Workforce planning and forecasting is also gaining weight because employers need scenarios that include both headcount and AI agents inside the same workforce model. Eightfold AI's May 2026 launch of Workforce Readiness, which gives CHROs real-time visibility into employee AI tool adoption and productivity, shows how vendors are expanding functionality into new intelligence categories.

By Organization Size: Enterprise Scale Anchors Demand While SMEs Catch Up

Large enterprises accounted for 67.96% of the workforce intelligence platform market size in 2025, supported by complex operating models, larger HR technology budgets, and stronger pressure to connect labor data with financial planning. In the workforce intelligence platform market, these buyers often need platforms that can process very large employee populations across multiple countries, payroll engines, and systems of record. That requirement narrows the viable vendor pool and favors providers with deep integration capability, mature security controls, and proven deployment records in complex enterprise settings. Large organizations also tend to have stronger executive sponsorship because the discussion increasingly includes capital allocation, restructuring, and productivity planning rather than only workforce administration. This makes enterprise demand more durable even when buying cycles become stricter.

SMEs are projected to expand at an 18.44% CAGR through 2031, which makes them the fastest-growing organization size segment in the workforce intelligence platform market. HR Partner reports in 2026 that 41% of small-business HR professionals across Australia, the UK, and the United States identified HR reporting and analytics as the area where AI would have the greatest impact. Intuit's May 2026 launch of QuickBooks Workforce, built on payroll infrastructure serving 18 million U.S. workers and extended through GoCo technology, also shows that horizontal software providers are packaging workforce intelligence into broader SME operations stacks. Vendors serving this tier are differentiating less on deep feature breadth and more on short deployment periods, simpler packaging, and consumption-based pricing. That is gradually widening access to the workforce intelligence platform market beyond the large organizations that shaped the category in its earlier phase.

By End-User Industry: IT and Telecom Leads as Healthcare Moves Fastest

IT and telecom accounted for 23.68% of workforce intelligence platform revenue in 2025, which gave the sector the leading vertical position in the workforce intelligence platform market. The sector's strong share reflects high employee churn, rapid skill obsolescence, and better data infrastructure than many other industries, which reduces the work needed to launch new analytics programs. It also gives vendors a clearer route into enterprise accounts because many IT and telecom employers already operate mature HRIS and collaboration environments that support richer skills inference and reporting. This makes the sector a natural early adopter for platforms that connect internal labor visibility with workforce redeployment and future capability needs. It also explains why many vendor product examples and customer stories continue to center on digital and technology-intensive employers.

Healthcare and life sciences is projected to grow at an 18.82% CAGR through 2031, making it the fastest-moving vertical in the workforce intelligence platform market. The U.S. Bureau of Labor Statistics continues to show significant demand growth for registered nurses through the early 2030s, which reinforces the staffing pressure behind healthcare demand. Symplr states that Smart Square, recognized as Best in KLAS for Scheduling in both 2025 and 2026, can forecast patient volume up to 120 days in advance at 96% accuracy, showing the value of highly specialized workforce planning in clinical settings. Healthcare demand is also supported by labor compliance expectations, including staffing standards and reporting needs that conventional dashboards cannot meet. Beyond healthcare, the workforce intelligence platform market is also drawing broader interest from BFSI, manufacturing, retail and e-commerce, and government and public sector organizations as AI-led role redesign changes workforce requirements across each of those environments.

Geography Analysis

North America held 40.74% of global workforce intelligence platform market share in 2025, making it the largest regional contributor. The workforce intelligence platform market is strongest in this region because large enterprises already operate mature HR technology estates and have more established practices for linking workforce decisions with financial performance. The United States remains the main demand center, supported by public company disclosure expectations around human capital resources and by stronger CHRO-CFO co-sponsorship of workforce technology spending. Canada adds a secondary center of demand, with Vancouver standing out as an important base for people analytics innovation through companies such as Visier. In the workforce intelligence platform market, that combination of buyer maturity, vendor presence, and larger contract scope continues to support North America's leading position.

Europe operates under a more compliance-driven model in the workforce intelligence platform market. The Corporate Sustainability Reporting Directive has increased the need for structured disclosure on workforce composition, skills development, and pay equity, which supports investment in platforms that can formalize those data flows. At the same time, works council consultation obligations in Germany, France, Belgium, and the Netherlands can slow deployments because employee representatives may need to review systems before activation. Eversheds Sutherland's 2026 employment guidance also shows why buyers in this region remain cautious, since AI systems used in workplace settings can trigger high-risk obligations under the EU AI Act. The Nordics and the UK remain relatively faster-moving sub-markets because enterprise HR analytics practices are more mature and data governance processes are more established than in some parts of continental Europe.

Asia-Pacific is projected to expand at a 19.64% CAGR through 2031, which makes it the fastest-growing region in the workforce intelligence platform market. Growth is being supported by government-backed AI programs, the expansion of Global Capability Centers, and the fact that many organizations are moving directly into cloud-led architectures instead of carrying older HR stacks forward. India stands out as a high-velocity market where generative AI is already being applied to workforce planning, attrition prediction, and skills inference in IT services and financial services environments. Japan remains a major regional SaaS market, while Australia and South Korea function as mature secondary markets with strong digitization and compliance needs. WTW also reports that AI is helping Asia-Pacific HR teams build a unified source of truth for jobs, levels, and skills, which supports both pay governance and internal mobility within the same operating model. South America, the Middle East, and Africa remain earlier-stage regions for the workforce intelligence platform market, with adoption concentrated in multinational subsidiaries, large financial institutions, and government-linked employers. Brazil and South Africa anchor regional demand, while Saudi Arabia and the UAE stand out because workforce nationalization mandates require auditable tracking of workforce composition against policy targets.

Competitive Landscape

The workforce intelligence platform market is moderately fragmented, with no single company controlling the category across all major functions. Broad platforms such as Visier and Eightfold AI compete with mid-stack specialists, including Gloat, ChartHop, and Beamery, while focused providers such as TechWolf, Syndio, and Crunchr remain relevant through narrower but differentiated use cases. Large HCM suite vendors also influence the workforce intelligence platform market by extending native analytics within existing enterprise software contracts, which gives them budget access even when standalone usage is still limited. This competitive setup keeps the market open, but it also raises the bar for differentiation because buyers can compare specialist precision against suite convenience in almost every deal.

A clear pattern in the workforce intelligence platform market is expansion from an original specialist use case into a broader platform role. Gloat, which helped define the internal talent marketplace category, now positions its Loomra Workforce Context Engine as a vendor-agnostic semantic AI layer above existing HR systems, and in April 2026, it brought that capability into Microsoft 365 Copilot and Microsoft Teams. Eightfold AI made a similar move in May 2026 when it launched TalentForge and introduced Workforce Readiness, pushing its brand further toward AI infrastructure and governed intelligence rather than only packaged HR applications.[4]Eightfold AI, “Eightfold Ushers in the Golden Age of HR Software with Launch of TalentForge,” Eightfold AI, eightfold.ai Lattice also accelerated in this direction through its March 2026 acquisition of Mandala Technology, which added AI-native coaching to its People + AI strategy. These moves show that vendors are trying to deepen daily relevance and expand wallet share instead of staying tied to a single workflow.

Another competitive theme in the workforce intelligence platform market is the push to place governed workforce data inside the AI environments that employees already use. Visier highlighted this path in April 2026 through a Glean MCP connection and an Amazon Quick integration with its Vee agent, both aimed at surfacing workforce intelligence through natural language access inside broader enterprise workflows. That matters because sustained engagement in the workforce intelligence platform market has historically weakened when users had to open a separate specialist application for every query. Smaller European vendors are also gaining room by emphasizing GDPR-native architecture and strong regional system integration, especially in markets where U.S.-based platforms face extra compliance scrutiny. The field still offers white space where few vendors can link workforce scenarios directly to P&L and balance sheet effects in real time, which keeps the competitive race open even as the market becomes more crowded.

Workforce Intelligence Platform Industry Leaders

Visier, Inc.

Eightfold AI, Inc.

Phenom People, Inc.

One Model, Inc.

OrgVue Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Eightfold AI launched TalentForge at Cultivate 2026, a new platform enabling enterprises to custom-build HR applications on Eightfold's talent intelligence foundation. The release simultaneously introduced Workforce Readiness, providing CHROs with real-time visibility into employee AI tool adoption and productivity, and a 360 Interview for AI Interviewer, available on a SOC 2 and ISO 42001 certified framework with full audit logs and score explainability, marking a strategic shift from application vendor to AI infrastructure provider.

- April 2026: Phenom acquired Plum, adding psychometric and behavioral validation to its talent intelligence platform. The acquisition followed Phenom's February 2026 acquisition of Be Applied, consolidating cognitive, situational, and behavioral assessment onto a single agentic platform, positioning Phenom as the only end-to-end system validating both candidate capability and behavioral predictors of performance across the full talent lifecycle.

- April 2026: Gloat launched its Agentic HR capabilities within Microsoft 365 Copilot and Microsoft Teams, making the Gloat Copilot Agent available through the Microsoft Agent Store and Marketplace. Powered by the Loomra Workforce Context Engine, the integration enables talent redeployment recommendations, career development guidance, and internal sourcing within the daily workflows of Microsoft 365 environments, bringing workforce intelligence directly into the flow of work for the first time at enterprise scale.

- March 2026: Lattice acquired Mandala Technology, adding AI-native coaching capabilities and positioning the combined product as the industry's first AI-native people intelligence platform. The acquisition accelerated Lattice's People + AI strategy, which includes AI-embedded performance reviews and expanded calibration tools in its Spring/Summer 2026 product release.

Global Workforce Intelligence Platform Market Report Scope

The workforce intelligence platform market refers to software platforms and integrated analytical solutions that leverage artificial intelligence, machine learning, predictive analytics, graph intelligence, and workforce data modeling to help organizations optimize workforce planning, talent mobility, employee performance, skills intelligence, organizational design, and strategic workforce decision-making.

The Workforce Intelligence Platform Market Report is Segmented by Deployment Model (Cloud, and On-premises), Functionality (Workforce Analytics and Reporting, Talent Mobility and Skills Intelligence, Workforce Planning and Forecasting, Employee Experience and Performance Intelligence, and Other Functionality Types), Organization Size (Large Enterprises, and SMEs), End-User Industry (IT and Telecom, BFSI, Healthcare and Life Sciences, Manufacturing, Retail and E-commerce, Government and Public Sector, and Other End-user Industries), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Cloud |

| On-premises |

| Workforce Analytics and Reporting |

| Talent Mobility and Skills Intelligence |

| Workforce Planning and Forecasting |

| Employee Experience and Performance Intelligence |

| Other Functionality Types |

| Large Enterprises |

| SMEs |

| IT and Telecom |

| BFSI |

| Healthcare and Life Sciences |

| Manufacturing |

| Retail and E-commerce |

| Government and Public Sector |

| Other End-user Industries |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Nordics | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Rest of Africa |

| By Deployment Model | Cloud | |

| On-premises | ||

| By Functionality | Workforce Analytics and Reporting | |

| Talent Mobility and Skills Intelligence | ||

| Workforce Planning and Forecasting | ||

| Employee Experience and Performance Intelligence | ||

| Other Functionality Types | ||

| By Organization Size | Large Enterprises | |

| SMEs | ||

| By End-User Industry | IT and Telecom | |

| BFSI | ||

| Healthcare and Life Sciences | ||

| Manufacturing | ||

| Retail and E-commerce | ||

| Government and Public Sector | ||

| Other End-user Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Nordics | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current and forecast value of the workforce intelligence platform market?

The workforce intelligence platform market stands at USD 1.72 billion in 2026 and is projected to reach USD 3.86 billion by 2031, growing at a 17.56% CAGR over 2026-2031.

Which deployment model leads workforce intelligence platform adoption?

Cloud leads adoption, holding 69.84% of revenue in 2025, supported by faster updates, easier integration management, and lower infrastructure friction for buyers.

Which functionality is growing the fastest in workforce intelligence platforms?

Talent mobility and skills intelligence is the fastest-growing functionality, with a projected 20.18% CAGR through 2031, while workforce analytics and reporting remained the largest segment in 2025.

Why are finance teams becoming more involved in platform buying decisions?

Buyers are increasingly linking workforce tools to internal hiring savings, capacity planning, and business performance. Better internal mobility economics and stronger ROI visibility are bringing CFO teams into procurement.

Which region is expanding the fastest for workforce intelligence platforms?

Asia-Pacific is the fastest-growing region, with a projected 19.64% CAGR through 2031, supported by AI programs, Global Capability Center growth, and cloud-first deployment patterns.

Which end-user sector offers the strongest near-term growth opportunity?

Healthcare and life sciences offers the strongest growth outlook, with an 18.82% CAGR through 2031, driven by staffing shortages, compliance needs, and demand for predictive workforce scheduling.

Page last updated on: