Privacy Management Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

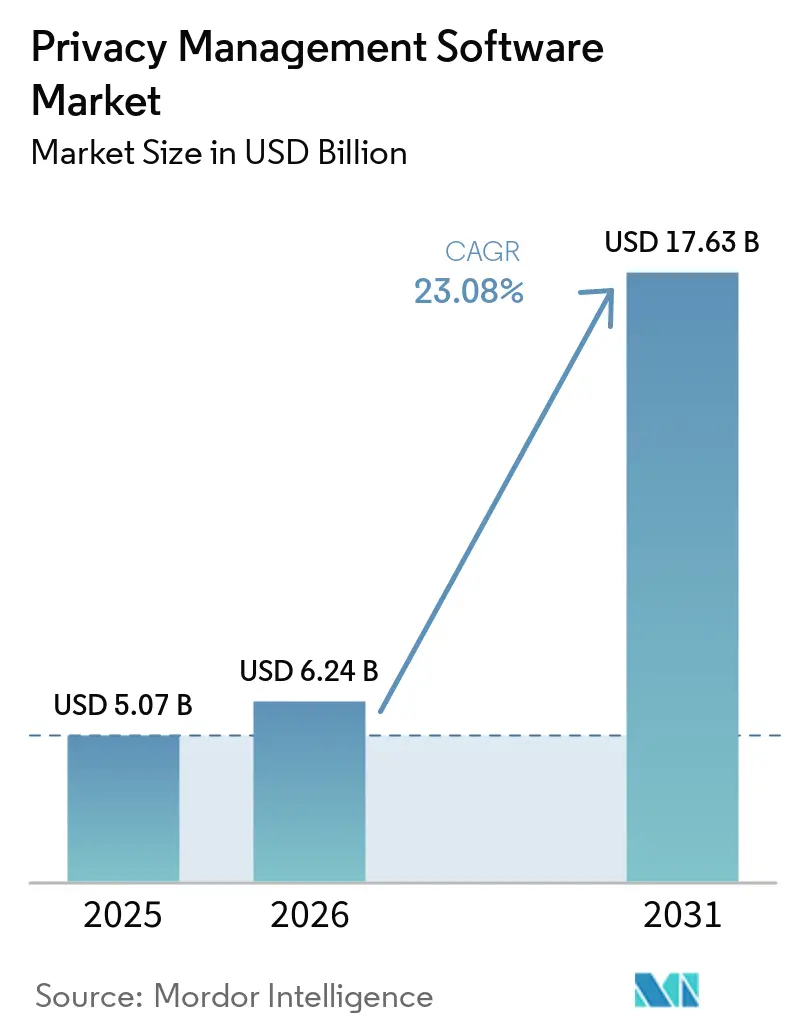

| Market Size (2026) | USD 6.24 Billion |

| Market Size (2031) | USD 17.63 Billion |

| Growth Rate (2026 - 2031) | 23.08% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Privacy Management Software Market Analysis by Mordor Intelligence

The privacy management software market size is expected to grow from USD 5.07 billion in 2025 to USD 6.24 billion in 2026 and is forecast to reach USD 17.63 billion by 2031 at 23.08% CAGR over 2026-2031. Heightened regulatory activity, the embrace of cloud-native architectures, and the need to embed privacy guardrails into artificial-intelligence workflows are combining to pull spending forward. Chief information and compliance executives regard privacy management less as a cost of doing business and more as a trust-building lever that shields revenue streams while enabling data-driven initiatives. Platform consolidation is gaining pace because buyers want one orchestration layer that can update rule libraries in real time and support multi-jurisdictional data flows. The preference for cloud delivery has become decisive, particularly among North American firms that must keep pace with California’s evolving statutes and among Asia-Pacific companies addressing new data-localization laws. Vendor differentiation now hinges on automation depth, AI-ready modules, and the ability to serve both large enterprises and resource-constrained small and mid-size businesses, which are entering the compliance arena at speed.

Key Report Takeaways

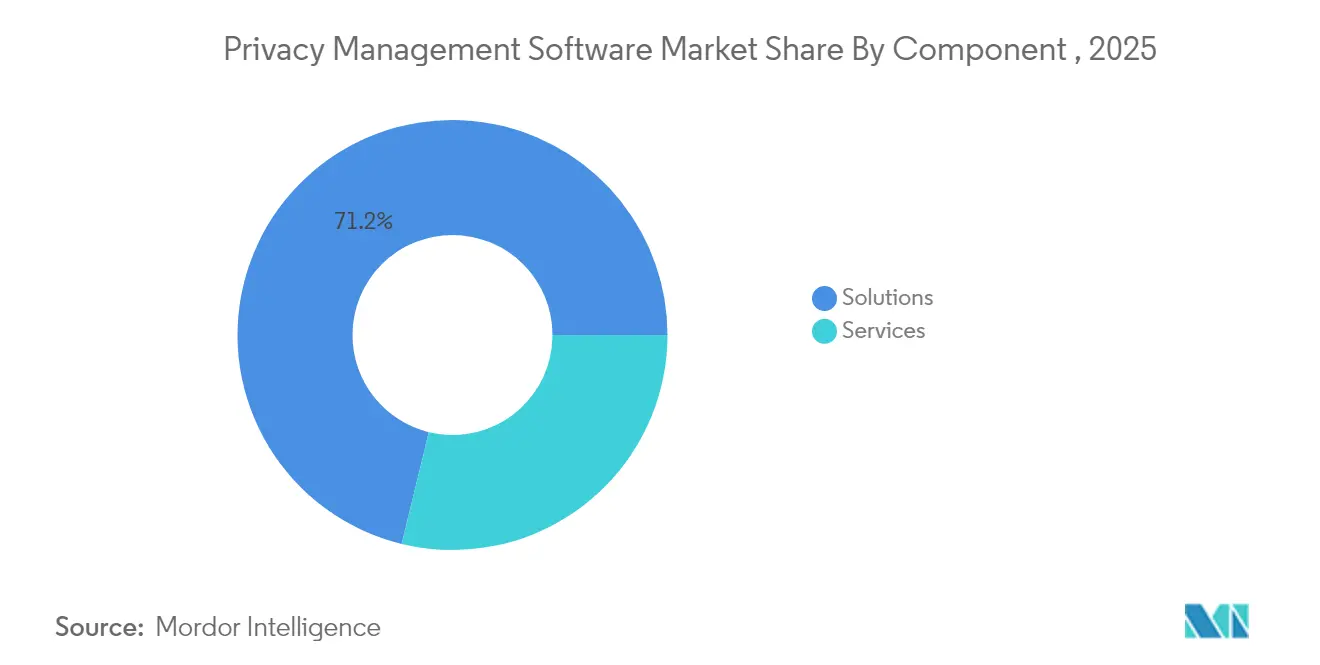

- By component, solutions led with 71.20% of privacy management software market share in 2025, while services are tracking a 24.3% CAGR to 2031.

- By deployment mode, cloud models controlled 66.30% of the privacy management software market in 2025; on-premise lags as cloud use expands at a 26.1% CAGR through 2031.

- By organization size, large enterprises held 57.40% revenue share in 2025, whereas SMBs represent the fastest growing cohort with a 23.2% CAGR to 2031.

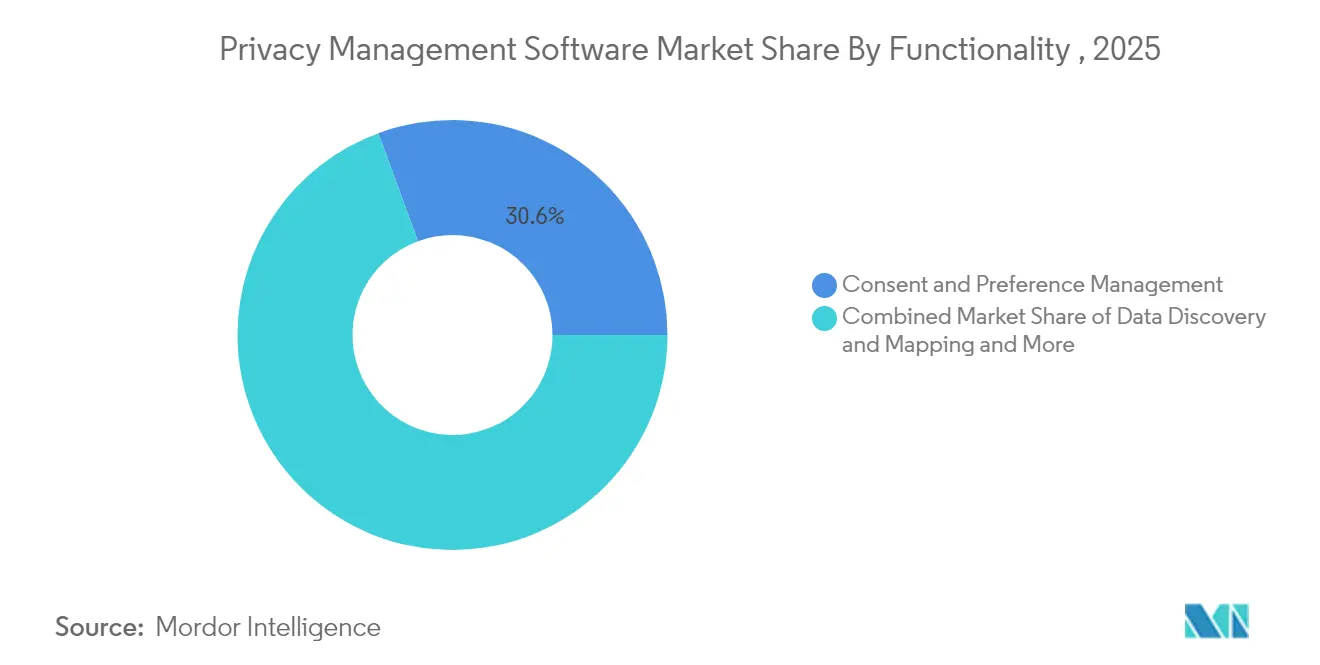

- By functionality, consent and preference management accounted for 30.60% of the privacy management software market size in 2025; AI-driven data discovery is scaling at a 28.1% CAGR.

- By vertical, BFSI dominated with 23.70% revenue share in 2025, while healthcare and life sciences show the strongest outlook at a 20.3% CAGR through 2031.

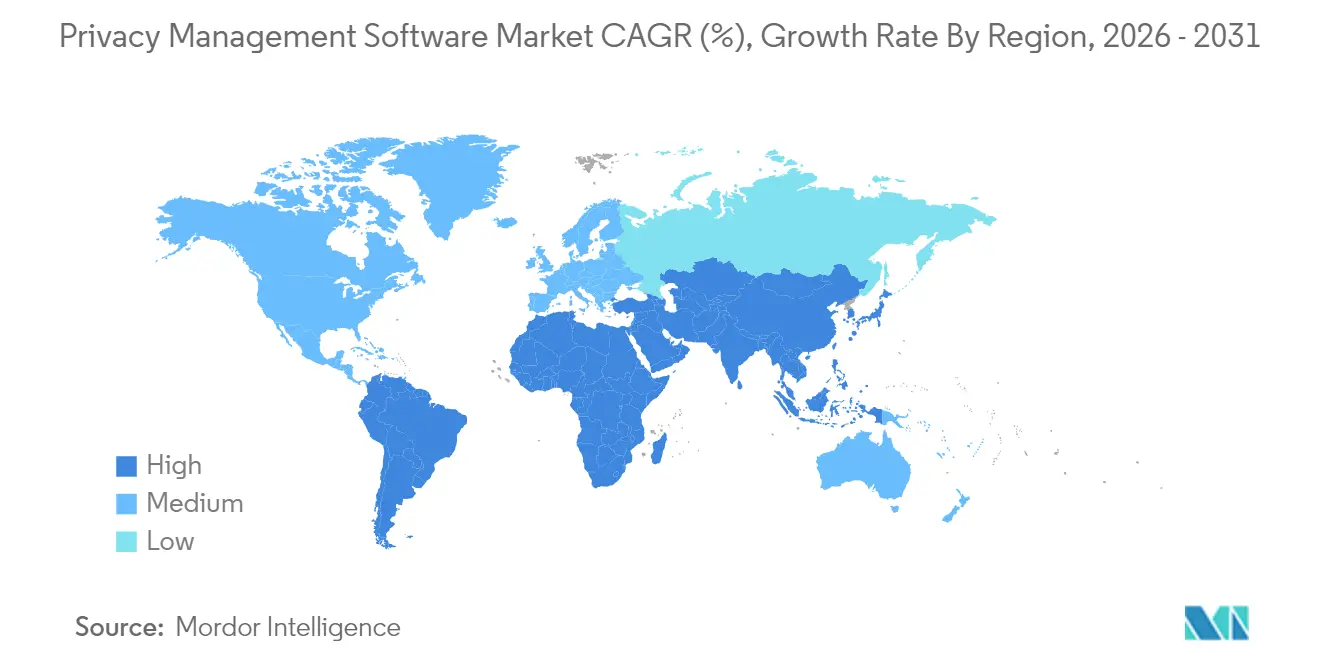

- By geography, North America retained 37.60% share in 2025; Asia-Pacific is rising at a 27.2% CAGR and is expected to close the gap by 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Privacy Management Software Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating global privacy regulations | +8.2% | EU, North America, India, Brazil | Medium term (2-4 years) |

| Need to avoid heavy non-compliance penalties | +4.1% | EU, California | Short term (≤ 2 years) |

| Shift to cloud and SaaS delivery models | +3.8% | North America, APAC | Medium term (2-4 years) |

| Rapid SaaS adoption by SMBs | +2.9% | APAC, Latin America, MEA | Long term (≥ 4 years) |

| Country-level data-localization mandates | +2.1% | APAC core, spill-over to MEA & Latin America | Long term (≥ 4 years) |

| Integration of privacy tooling with Gen-AI governance | +1.4% | North America, EU, APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Escalating Global Privacy Regulations Drive Market Acceleration

The widening net of data-protection statutes is reshaping governance roadmaps. India’s Digital Personal Data Protection Act 2023, which tightens rules on model storage and cross-border data transfers, obliges companies to deploy platforms that can choreograph multiple regulatory workflows simultaneously. Brazil and several African nations are following suit, causing multinationals to favor solutions that update once and syndicate rule changes to every business unit. Regulators are also moving beyond personal-data rights into algorithmic transparency, reinforcing the need for unified software that can monitor AI pipeline activities in lockstep with classic privacy tasks.[1]NIST, Privacy Framework, National Institute of Standards and Technology, nist.gov

Cloud and SaaS Delivery Models Transform Market Dynamics

Cloud-native rollouts answer the demand for rapid rule updates, cross-border performance, and elastic scaling. With 67% share in 2024, cloud deployment became the baseline rather than an alternative. Shared-compliance infrastructure lowers entry costs and delivers instant access to new controls when laws change.[2]Broadcom, Private Cloud Outlook 2025, Broadcom, news.broadcom.com Nevertheless, cloud reliance forces firms to weigh sovereignty constraints; hybrid topologies are therefore rising where data-localization laws require in-country processing yet the enterprise still wants the efficiency of centralized orchestration.

SMB Market Expansion in Emerging Digital Economies

Regulatory parity between large enterprises and smaller firms is expanding the customer base. SMBs, lacking privacy officers, need automation-first tools that mask complexity. Affordable SaaS plans combined with quick-start templates are driving a 24% CAGR for this group, with Asia-Pacific and Latin America leading uptake as digital-commerce volumes climb and governments extend privacy protections to all business tiers.[3]GSMA, Regional Privacy Frameworks and Cross-Border Data Flows, GSM Association gsma.com

AI Governance Integration Reshapes Privacy Management Architecture

The arrival of generative-AI workflows pushes privacy tooling into new terrain. California’s AB 1008 now classifies AI-processed insights as personal data, compelling platforms to map not only source records but also model outputs and derived attributes. Vendors are integrating risk scoring for training sets, model-audit logs, and consent checks for AI-based decisions, turning the software into the backbone for algorithmic accountability across jurisdictions.

Restraints Impact Analysis of Privacy Management Software Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Complex multi-jurisdiction compliance requirements | -2.8% | Multinational enterprises | Medium term (2-4 years) |

| Budget constraints for SMB segment during tech-spend pullbacks | -1.9% | Emerging markets / SMB-focused regions | Short term (≤ 2 years) |

| Platform fatigue due to overlap with broader GRC suites | -1.5% | North America and Western Europe enterprise segment | Medium term (2-4 years) |

| Shortage of experienced privacy engineers and DPO talent | -2.2% | Global, especially high-growth digital economies | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Complex Multi-Jurisdiction Compliance Creates Implementation Barriers

Divergent rules on cross-border transfers and storage force enterprises to bolt together localized and global instances, inflating project timelines and costs. In markets such as Indonesia, strict localization mandates clash with the appeal of centralized SaaS, pushing firms toward hybrid deployments that are harder to maintain. The burden is heavier for mid-market companies that lack in-house legal and engineering talent.

Budget Constraints in SMB Segment Limit Market Penetration

Macroeconomic headwinds are squeezing discretionary IT budgets, delaying privacy projects among smaller firms despite looming statutory deadlines. The shortage of certified privacy engineers amplifies cost pressures because external advisory fees climb when internal skills are scarce. Vendors that automate onboarding and provide managed services are best positioned to capture latent demand once capital spending loosens.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Privacy Management Software Market Segment Analysis

By Component:

Solutions Maintain Scale Leadership, Services Accelerate Value DeliveryPrivacy management software market size for solutions commanded 71.20% of revenue in 2025, underscoring the indispensable role of centralized orchestration suites. Growth now pivots toward configuration and optimization expertise, evidenced by professional and managed services expanding 24.3% annually as enterprises fine-tune rule engines and integrate adjacent governance modules. The services curve steepens in regions introducing first-time privacy laws, where local firms rely on external specialists to navigate unfamiliar frameworks.

The up-market shift in service demand reflects a maturing customer base that has moved from basic deployment to continuous-improvement cycles. Managed-service packages are winning contracts by bundling regulatory monitoring, policy updates, and runtime analytics, easing internal head-count constraints. Providers that combine deep legal knowledge with automation toolkits are securing multi-year retainer agreements, strengthening switching barriers

By Deployment Mode:

Cloud Dominance Mirrors Architectural ModernizationCloud implementations represented 66.30% of the privacy management software market in 2025 and are expanding at a 26.1% CAGR as firms chase instant upgrades and elastic compute. Private-cloud configurations appeal to highly regulated verticals that need isolation yet still want orchestration benefits. On-premise estates persist in pockets where data cannot exit national borders, but the pattern is shifting toward hybrid overlays that sync local vaults with global policy engines.

Innovation is clustering around micro-services and API extensions that let privacy controls embed directly into DevSecOps pipelines. Vendors promoting infrastructure-agnostic clusters—deploy-once, run-anywhere—lower exit barriers and help customers comply with evolving localization clauses without rewriting code, accelerating time-to-value.

By Organization Size:

Enterprise Spending Leads, SMB Momentum BuildsLarge enterprises held 57.40% revenue share in 2025 as multi-regional corporations invested in cross-border compliance hubs. Their requirements for intricate workflow routing, granular role-based access, and deep system integrations sustain high average deal sizes. In parallel, SMB contracts are scaling at 23.2% annually, fueled by simplified subscription tiers that include pre-built legal templates and automated DSAR processing.

Market entrants are tailoring lightweight dashboards and wizard-driven setup flows to keep training needs low. Flexible per-record or per-user pricing models align spend with usage patterns, allowing SMBs to phase deployments alongside revenue growth. As smaller firms integrate privacy metrics into board-level risk registers, purchase decisions increasingly involve CEOs and founders rather than only IT managers.

By Functionality:

Consent Management Anchors Adoption, AI Discovery Gains VelocityConsent and preference tools secured 30.60% of 2025 revenue, reflecting global laws that obligate granular disclosure and opt-in transparency. Customers demand flexible design libraries that harmonize preference centers across web, mobile, and connected-device channels. In contrast, AI-powered discovery is the breakout category, leaping 28.1% each year as enterprises grapple with sprawling data lakes. Automatic classification engines that surface personally identifiable information within structured and unstructured sources cut manual inventory cycles dramatically.

DSAR automation and data-mapping modules are following close behind, each posting double-digit growth as individuals exercise access rights more frequently. Vendors embedding natural-language interfaces into discovery dashboards shorten the analytics learning curve, broadening usage beyond privacy teams to security and data-governance groups.

By Vertical Industry:

BFSI Sets the Pace, Healthcare Surges on Data-Intensive R&DFinancial institutions controlled 23.70% of expenditure in 2025, owing to stringent banking secrecy codes, cybersecurity mandates, and high transaction-data velocity. Integrated privacy-plus-security controls help lenders satisfy overlapping supervisory audits while sustaining digital-banking rollouts. Healthcare and life sciences are tracking a 20.3% CAGR as genomic research, telehealth expansion, and clinical-trial digitization amplify data-subject-rights exposure.

Government agencies are modernizing citizen-service portals, driving uptake of modules that document purpose limitation and lawful-basis evaluations. Telecom operators, acting as processors for multiple industries, invest in federated-consent frameworks to reassure enterprise customers that personal data crosses their networks under strict policy governance.

Geography Analysis

North America Privacy Management Software Market

North America captured 37.60% of global revenue in 2025, propelled by California’s evolving privacy statutes, sector-specific rules, and escalating federal discourse on a national privacy bill. Large enterprises in technology, retail, and healthcare continue to recalibrate data-monetization models by using privacy credentials to differentiate products, reinforcing vendor demand for integrated orchestration suites. State-level advances in algorithmic accountability are steering investment toward platforms that can govern AI training data and inference outputs side by side with conventional record repositories.

Europe Privacy Management Software Market

Europe held 28.80% share in 2025 on the back of GDPR’s continued influence and the bloc’s strict approach to cross-border transfer adequacy. Corporate buyers prioritize privacy-by-design capabilities and favor suppliers that pass rigorous data-protection-impact-assessment benchmarks. Divergence between EU rules and post-Brexit UK provisions adds complexity, stimulating interest in multi-regime policy engines that maintain end-to-end audit trails without duplicating infrastructure. Fines issued under GDPR have sharpened board-level focus, translating into sustained budget protection for compliance modernisation projects.

APAC Privacy Management Software Market

Asia-Pacific is expanding at a 27.2% CAGR, underpinned by India’s DPDP Act, Indonesia’s localization mandates, and broad digitization across Southeast Asian consumer markets. Governments are layering AI ethics guidelines onto existing privacy norms, accelerating spending on platforms that can adapt rule sets dynamically. Hybrid deployment strategies satisfy sovereignty clauses while giving companies the flexibility of scale-out SaaS. Rising e-commerce penetration and multinational hyperscale cloud investments are further amplifying demand, positioning the region to narrow the revenue gap with North America over the next five years.

Competitive Landscape

The privacy management software market exhibits moderate concentration. OneTrust, TrustArc, and Securiti remain top-tier in installed base but face sustained challenges from AI-focused entrants. Relyance AI attracted USD 32 million Series B backing to deepen automated policy-translation and model-risk scoring capabilities, signaling that investors reward AI-native architectures. BigID’s USD 60 million raise feeds a roadmap that blends data hygiene, classification, and remediation into a single control pane, seeking wallet share from security budgets that overlap with privacy mandates.

Platform consolidation is the strategic north-star for buyers weary of point solutions. Vendors with extensible APIs, policy-as-code libraries, and pre-built connectors into DevOps pipelines win proof-of-concept races. Price discipline matters, particularly in the SMB corridor, prompting suppliers to release modular SKUs that allow phased expansion. Managed-service overlays are emerging as a competitive differentiator, especially where local talent shortages make full SaaS self-service impractical.

Strategic alliances are also reshaping the field. Cloud-service providers are embedding privacy accelerators within their marketplaces, giving software vendors expanded reach while capturing consumption revenue. Consulting integrators partner with platform leaders to bundle regulatory interpretation with technical rollout, streamlining complex multinational deployments. M&A chatter is intensifying as mid-size specialists seek scale advantages to withstand pricing pressure from established suites.

Privacy Management Software Industry Leaders

OneTrust LLC

TrustArc Inc.

Securiti Inc.

BigID Inc.

SAP SE (Privacy Mgmt module)

- *Disclaimer: Major Players sorted in no particular order

Privacy Management Software Market Companies Covered in this Report

- OneTrust LLC

- TrustArc Inc.

- Securiti Inc.

- SAI360 (Pty Ltd)

- SAP SE

- Syrenis Ltd

- Crownpeak Technology Inc.

- Exterro Inc.

- WireWheel Inc.

- BigID Inc.

- Smart Global Governance

- Privacy Company

- Nymity (by TrustArc)

- Collibra NV

- IBM Corporation

- Microsoft Corporation

- Cisco Systems Inc.

- Informatica LLC

- DataGuard GmbH

- 2B Advice GmbH

- Privacera Inc.

Recent Industry Developments in Privacy Management Software Market

- April 2025: NIST updated its Privacy Framework to align with cybersecurity guidance and incorporate AI risk management, prompting enterprises to reassess governance architectures.

- March 2025: BigID raised USD 60 million in a Riverwood Capital–led round to expand data-hygiene automation and prepare for targeted acquisitions in data-security adjacencies.

- January 2025: Egnyte secured patents for its Copilot generative-AI assistant and added more than 300 features aimed at centralizing user access and automating DSAR fulfillment.

- October 2024: Tata Consultancy Services released a strategic framework for generative-AI adoption in BFSI, underscoring the need for integrated privacy and bias-mitigation controls.

Privacy Management Software Market Report Scope and Research Methodology

Market Definition and Coverage

Our study defines the privacy management software market as commercially packaged suites that help data controllers locate, classify, govern, and evidence the lawful processing of personal information across cloud and on-premise environments. Functions span discovery, consent and preference capture, request workflow, impact assessment, reporting, and audit logging.

Scope exclusion: bespoke consulting projects and spreadsheet-based compliance trackers that are not licensed as repeatable software are outside this estimate.

Segments Covered in This Report

- By Component

- Solutions

- Services

- By Deployment Mode

- Cloud / SaaS

- On-Premise

- By Organization Size

- Small and Medium Enterprises

- Large Enterprises

- By Functionality

- Consent and Preference Management

- Data Discovery and Mapping

- DSAR / Rights-Request Automation

- PIA / DPIA and Risk Assessment

- Incident Response Workflow

- By End-User Vertical Industry

- BFSI

- Healthcare and Life Sciences

- IT and Telecom

- Retail and e-Commerce

- Government and Public Sector

- Other End-User Vertical Industries (Media, Education, etc.)

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of Asia Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Primary Research

Mordor Intelligence conducted structured interviews and online questionnaires with data-protection officers, privacy engineers, cybersecurity distributors, and regional regulators across North America, Europe, and Asia Pacific. These conversations clarified pricing bands, license churn, and regional regulatory triggers, filling the blind spots that public filings leave.

Desk Research

Analysts began with authoritative public records such as the EU GDPR enforcement portal, the U.S. Federal Register's rule updates, and statistics from NIST, ENISA, and the U.K. ICO, which outline the addressable installation base and penalty trends. Trade associations including the IAPP and BSA furnished adoption ratios by industry, while company 10-Ks, investor presentations, and patent filings showed vendor revenue splits and product rollouts. Paid repositories, such as Dow Jones Factiva for deal flow and D&B Hoovers for private-firm billings, supplemented visibility. The sources cited above are illustrative; many additional references informed data cleaning, cross-checks, and context building.

Market-Sizing & Forecasting

A top-down reconstruction started with worldwide information-security spend, split by the share earmarked for privacy tooling in each region, before being further filtered through sector-level compliance intensity. Results were corroborated with sampled bottom-up rollups of leading vendor billings and average selling price multiplied by user-seat calculations. Key variables in the model include (1) number of regulated enterprises above 50 employees, (2) average privacy-tech spend per employee, (3) volume of data-subject access requests, (4) count and value of regulatory fines, and (5) migration rate from on-premise to SaaS. Forecasts apply an ARIMA time-series that adjusts for regulation timelines and macro IT spending elasticity; expert feedback guides scenario selection.

Data Validation & Update Cycle

Outputs pass a two-step analyst peer review, variance thresholds trigger re-work, and anomalies are re-checked with respondents. Reports refresh annually, with interim updates released when major regulations, material vendor M&A, or fine announcements move the needle. Before shipment, an analyst reruns the model so clients receive the latest view.

How Mordor Intelligence's Privacy Management Software Market Size Compares to Other Published Estimates

Published estimates vary because firms choose different product scopes, currency conversions, and refresh cadences.

Key gap drivers include narrower functional scope that drops on-premise modules, aggressive SaaS growth assumptions without historical anchoring, or reliance on single-vendor revenue extrapolations that our team challenges through multi-source triangulation and annual scope audits.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 5.07 B (2025) | Mordor Intelligence | - |

| USD 4.10 B (2024) | Global Consultancy A | Focuses on AI-driven risk modules only; omits legacy deployments |

| USD 3.84 B (2024) | Trade Journal B | Excludes small-enterprise uptake and discounts hybrid pricing tiers |

In short, Mordor's disciplined scope setting, transparent variable list, and annual refresh cadence yield a balanced, reproducible baseline that decision-makers can rely on with confidence.

Key Questions Answered in the Report

What is the current size of the privacy management software market?

The market totals USD 6.24 billion in 2026 and is projected to reach USD 17.63 billion by 2031.

Which deployment model leads this market?

Cloud delivery accounts for 66.30% of revenue and is expanding at a 26.1% CAGR as buyers favor real-time updates and scalable compliance.

Why are SMBs becoming an important growth segment?

New regulations apply to firms of all sizes, and affordable SaaS subscriptions give smaller companies enterprise-grade privacy controls without large upfront costs.

How are AI regulations influencing product roadmaps?

Statutes such as California’s AB 1008 now treat AI-generated insights as personal data, pushing vendors to add model-risk tracking and algorithmic-transparency features.

Which region shows the fastest growth?

Asia-Pacific is advancing at a 27.2% CAGR, driven by India’s DPDP Act, Indonesia’s localization rules, and rapid digital-commerce expansion.

Page last updated on: