Employee Benefits Technology Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.76 Billion |

| Market Size (2031) | USD 5.98 Billion |

| Growth Rate (2026 - 2031) | 9.72% CAGR |

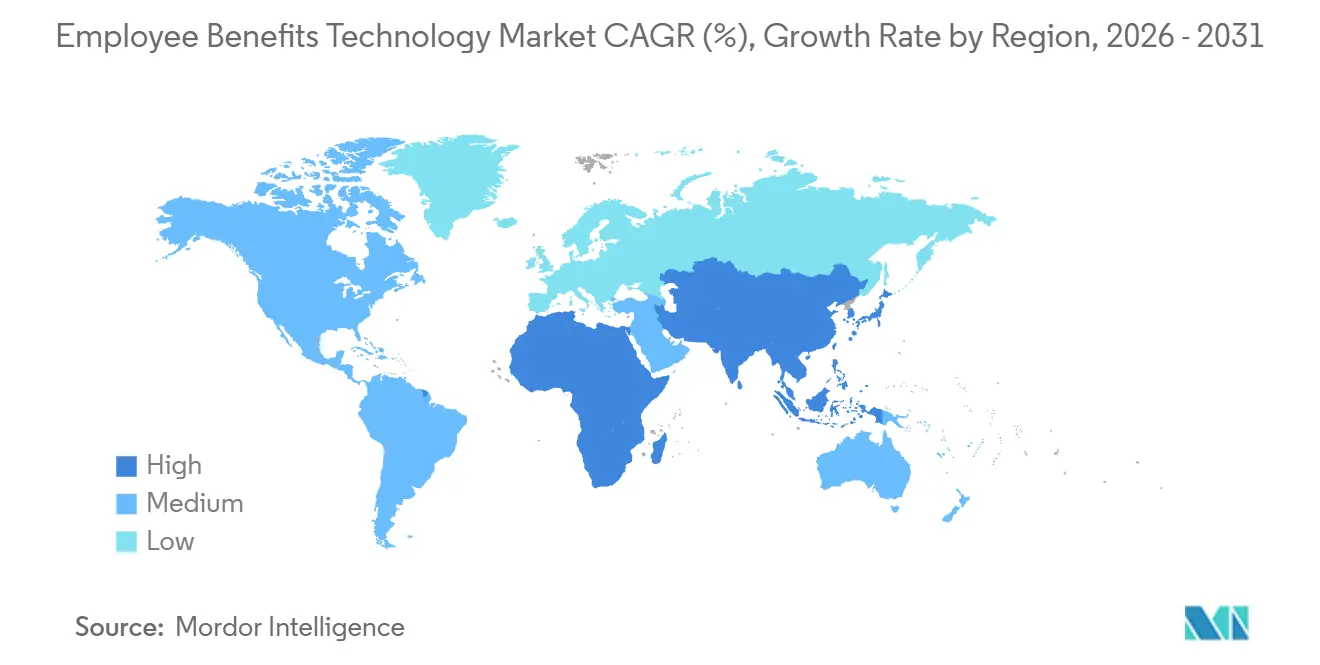

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

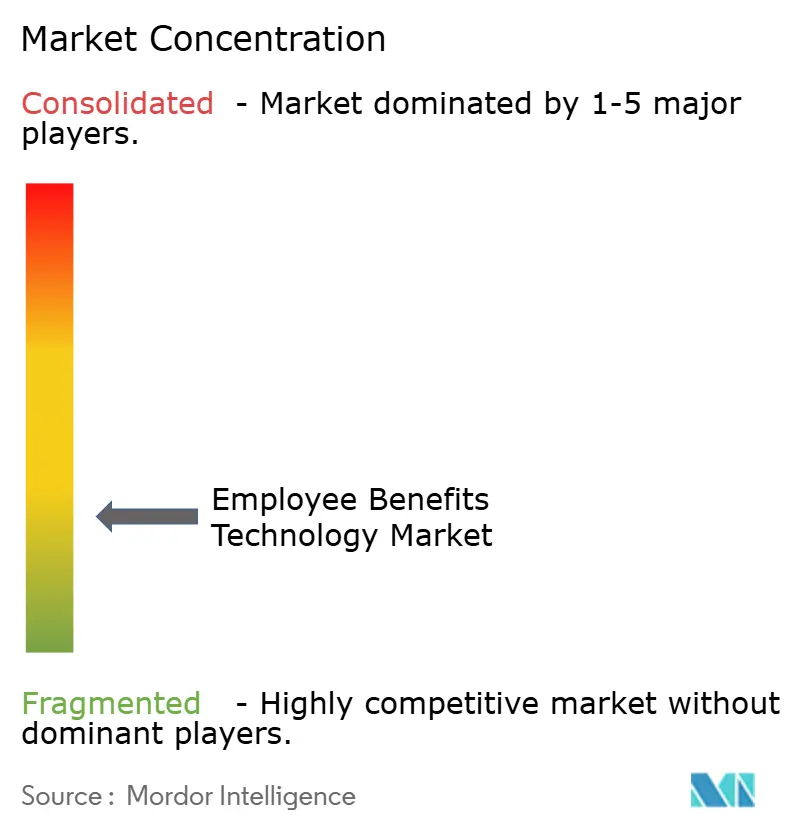

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Employee Benefits Technology Market Analysis by Mordor Intelligence

The employee benefits technology market size was valued at USD 3.46 billion in 2025 and is expected to reach USD 3.76 billion in 2026 and USD 5.98 billion by 2031, growing at a CAGR of 9.72% from 2026 to 2031. The employee benefits technology market is expanding as employers move away from manual administration and toward systems that handle compliance, plan changes, and cost control within a single workflow. Rising health benefit costs are pushing HR teams to act more like operating units that monitor spend, which is raising demand for platforms with stronger reporting and decision support. Regulatory pressure is also making it harder to delay automation, especially when employers must manage coverage eligibility, filing accuracy, and data security across multiple rules simultaneously. Competition is sharpening as specialist vendors defend their benefits-specific depth while broader HCM platforms leverage existing payroll relationships to win bundled deals. Near-term adoption still faces drag from difficult HRIS and payroll integrations and from a shortage of staff who can configure complex rules across multiple carriers and plan designs.

Key Report Takeaways

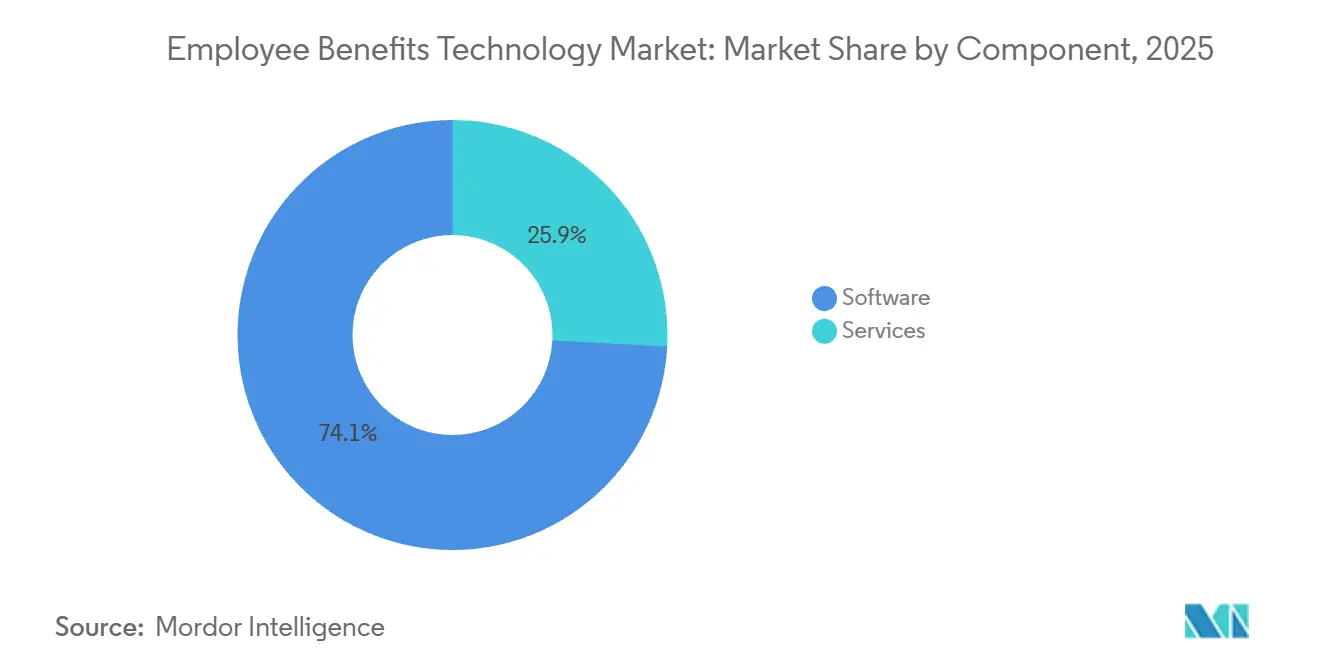

- By component, software led with 74.14% share in 2025 of the employee benefits technology market, while services is forecast to grow at a 10.06% CAGR through 2031.

- By deployment model, cloud-based platforms held 71.62% share in 2025 and also remain the fastest-growing segment with a 9.88% CAGR through 2031.

- By organization size, large enterprises accounted for 67.38% share in 2025, while SMEs are projected to expand at a 10.74% CAGR through 2031.

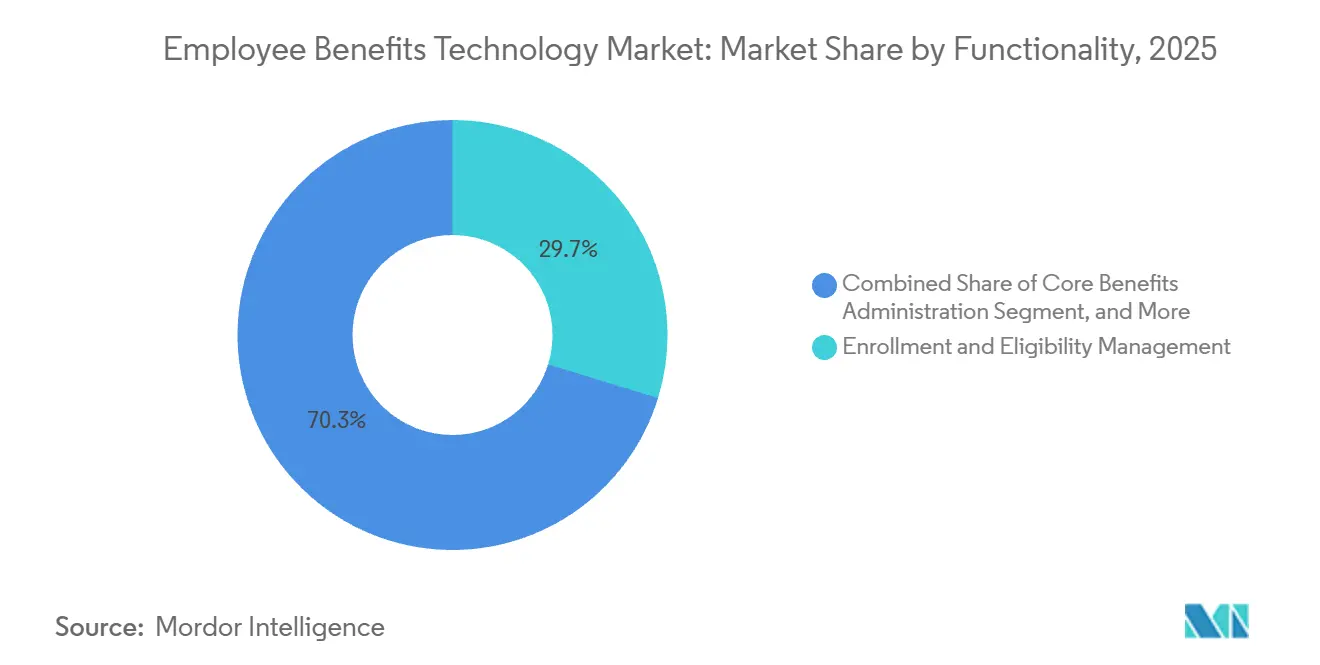

- By functionality, enrollment and eligibility management captured 29.74% share in 2025 of the employee benefits technology market, while analytics and reporting is expected to grow at an 11.26% CAGR through 2031.

- By end-user industry, BFSI held 21.28% share in 2025, while healthcare and lifesciences is projected to advance at a 10.63% CAGR through 2031.

- By geography, North America led with 40.36% share in 2025, while Asia-Pacific is forecast to grow at an 11.92% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Employee Benefits Technology Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Benefits Complexity And Compliance Automation Demand | +2.2% | North America and Europe primarily, global spill-over | Medium term (2-4 years) |

| Cloud Migration Across HR And Benefits Stacks | +1.9% | Global, led by North America and Asia-Pacific | Short term (≤ 2 years) |

| Growing Demand For Employee Self-service And Personalized Guidance | +1.7% | Global | Short term (≤ 2 years) |

| Small And Medium Enterprise Adoption Through SaaS Pricing | +1.5% | North America, Europe, India, Southeast Asia | Medium term (2-4 years) |

| Embedded Benefits APIs Inside Payroll And HCM Ecosystems | +1.1% | Global, led by North America | Medium term (2-4 years) |

| Expansion Of Wallet-based And Lifestyle Benefit Programs | +0.8% | North America, Europe, Asia-Pacific urban markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Benefits Complexity And Compliance Automation Demand

The employee benefits technology market is gaining support from the rising complexity of benefit rules across national and sub-national jurisdictions. In the United States, the ACA Employer Shared Responsibility Penalty B stood at USD 4,350 per employee for non-compliant coverage offerings in 2026, which keeps compliance exposure high for employers that still rely on manual tracking. Employers also have to manage a wider compliance stack that includes ACA reporting, leave tracking, COBRA administration, ERISA processes, and HIPAA-linked data handling, which increases the value of unified automation tools. AI-enabled compliance engines are increasingly being used to automate ACA 1095-C generation, FMLA eligibility tracking, and live penalty-risk monitoring, and documented deployments have reduced manual monitoring time by 70-80%. That shift is helping the employee benefits technology market move from a back-office software category toward a control layer for employer risk management.

Cloud Migration Across HR And Benefits Stacks

The employee benefits technology market is also being lifted by cloud migration across HR and benefits systems as employers replace fragmented tools with unified platforms. Alight Solutions completed its AWS migration in February 2025, and the move resulted in USD 75 million in annual savings, a 40% reduction in server footprint, and 43% faster enrollment response times. These results matter because cloud migration is no longer limited to infrastructure cost savings, and it now pushes employers to clean up carrier links, eligibility rules, and data definitions that had been sustained through manual reconciliation. That cleanup phase often increases service demand for implementation, integration, and ongoing plan configuration, which supports a larger services opportunity inside the employee benefits technology market. Hybrid deployment models are also becoming more relevant in regulated settings where employers want cloud economics but still need local data handling and tighter legal oversight of HR information flows.

Growing Demand For Employee Self-service And Personalized Guidance

The employee benefits technology market is benefiting from stronger demand for self-service tools that help employees make better enrollment choices. TriNet reported in October 2025 that 42% of employees rolled over prior-year benefit elections without reviewing plan costs, while only 15% analyzed cost-effectiveness before choosing coverage.[1]TriNet Team, “Personalization in Employee Benefits, Data Reveals Opportunity for Small Businesses,” TriNet, trinet.com AI-based guidance tools are starting to close that gap, and Nayya stated that 88% of users found benefit decisions easier and 72% reached the right cost-coverage balance through its platform. PlanSource said employers spent USD 13.8 billion on generative AI tools in 2024, a 600% increase over 2023, and part of that spend is being directed toward benefits personalization and decision support. Conversational tools are also lowering service costs, as bswift’s Emma Chat has demonstrated the ability to resolve 80% or more of enrollment queries without human escalation while improving first-time enrollment accuracy by 35-45%.

Small And Medium Enterprise Adoption Through SaaS Pricing

The employee benefits technology market is widening as SaaS pricing makes advanced administration tools more accessible to smaller employers. The core change is not just lower cost, but also the ability to start with narrower needs, such as enrollment, leave coordination, lifestyle benefits, or account administration, without taking on a full enterprise implementation. SMEs also carry less legacy system debt than large employers, which shortens deployment cycles and allows vendors to prove value faster in this customer group. Vendors using per-employee-per-month pricing and sub-45-day implementation models are winning share because they align better with the cash flow and staffing limits common in smaller firms. Professional employer organizations are extending that reach further by embedding benefits technology into pooled arrangements, which gives micro and small employers access to tools they would not have bought on a stand-alone basis.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Legacy HRIS And Payroll Integration Complexity | -2.0% | Global, most acute in large enterprises across North America and Europe | Long term (≥ 4 years) |

| Data Privacy And Cybersecurity Exposure | -1.7% | Global, particularly EU and US | Medium term (2-4 years) |

| Multi-country Carrier Data Fragmentation | -1.1% | Europe, Middle East and Africa, Asia-Pacific | Long term (≥ 4 years) |

| Shortage Of Benefits Configuration And Implementation Talent | -0.8% | Global, most acute in North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Legacy HRIS And Payroll Integration Complexity

The employee benefits technology market still faces its largest operational barrier in HRIS and payroll integration complexity. Align HCM stated in April 2026 that organizations with disconnected benefits and payroll systems can spend 40 hours per month on manual data re-entry, and poor data quality has been shown to cost organizations an average of USD 12.9 million annually in productivity loss and error remediation. Many legacy systems were built before modern API standards became common, so benefits platforms still depend on batch file transfers that create eligibility lags and billing mismatches.[2]Maher El-Abdallah, “Common Challenges with HCM Implementations,” Align HCM, alignhcm.com Align HCM also reported in December 2025 that 37% of project failures were tied to unclear requirements, and 29% of firms experienced critical payroll discrepancies after migration. This is slowing the employee benefits technology market because employers often judge the value of a platform through implementation outcomes rather than through product features alone.

Data Privacy And Cybersecurity Exposure

Data privacy and cybersecurity exposure remain a serious restraint because these platforms store sensitive health, financial, and identity information in one operating environment. The HIPAA Security Rule NPRM published in January 2025 proposed moving encryption, multi-factor authentication, and network segmentation from addressable practices to required standards, with first-year industry-wide compliance costs estimated at USD 9 billion. Medical ITG reported in March 2026 that healthcare ransomware attacks increased 36% in 2026, while average breach costs reached USD 7.42 million in 2025 . The result is that security standards such as encryption, access controls, and attestation frameworks are becoming board-level procurement criteria rather than technical preferences. That pressure raises operating costs for vendors and can lengthen buying cycles, especially when employers need country-specific controls and legal review before approving deployment.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Dominance Shifts As Services Scale

Software accounted for 74.14% of the employee benefits technology market size in 2025, and this lead reflected the central role of enrollment engines, eligibility management, and AI-guided decision support in employer deployments. The software layer remains the foundation of the employee benefits technology market because employers still begin modernization through a platform purchase before they expand into deeper service relationships. That said, services is projected to grow at a 10.06% CAGR through 2031, which is faster than the overall market and shows that software adoption is creating a second demand wave rather than closing the buying cycle. Implementation support, carrier connectivity, plan configuration, and ongoing compliance maintenance are becoming harder to manage internally as benefit structures become more specialized.

This shift matters because the boundary between product and service is starting to blur across the employee benefits technology industry. Businessolver’s July 2025 acquisition of ProView Global assets added back-end administration capacity and reflected direct client demand for human support alongside AI-driven tools. As more employers ask vendors to manage implementation and daily exceptions, services is becoming a source of stickiness rather than a peripheral revenue stream. This is why the employee benefits technology market is likely to keep rewarding vendors that can combine strong core software with reliable operational delivery.

By Deployment Model: Cloud Consolidation Accelerates

Cloud-based deployment held 71.62% of the employee benefits technology market share in 2025, and it is forecast to grow at a 9.88% CAGR through 2031. Cloud systems are leading because employers want faster upgrades, lower infrastructure burden, and easier connectivity across payroll, HRIS, and carrier systems. The employee benefits technology market has moved beyond simple hosting changes, and current projects increasingly rebuild enrollment, eligibility, and reporting layers around API-first designs instead of moving old logic into new servers. On-premises deployments still hold relevance in government and heavily regulated settings where external hosting remains difficult, but this segment faces ongoing structural compression.

The stronger pull toward the cloud also comes from measurable performance gains. Alight’s AWS migration delivered 43% faster enrollment response times and USD 75 million in annual savings, which set a benchmark that traditional on-premises environments struggle to match without major reinvestment. In Europe, deployment choice is also shaped by legal scrutiny of where employee data resides, which is helping private-cloud and regional-hosting models stay relevant for larger employers. That mix of cost, performance, and legal control keeps the cloud at the center of the employee benefits technology market even when the final architecture is not fully public cloud.

By Organization Size: SMEs Emerge As The Growth Engine

Large enterprises held 67.38% of the employee benefits technology market share in 2025 because they manage more complex benefit structures, broader carrier relationships, and higher compliance exposure. They remain the largest buyers in the employee benefits technology market, and they continue to need enterprise-grade tools for eligibility control, audit readiness, and reporting at scale. Even so, SMEs are projected to expand at a 10.74% CAGR through 2031, which makes them the fastest-growing organization-size segment. This growth reflects the spread of SaaS pricing, lighter implementation models, and rising benefit complexity for firms that previously depended on brokers and spreadsheets.

The appeal of the SME segment is growing because these buyers can often adopt faster than large employers. Smaller firms usually carry less integration debt, which shortens deployment timelines and reduces the internal resistance that can slow enterprise rollouts. Vendors such as PeopleKeep and Employee Navigator have built simpler onboarding paths for sub-250-employee accounts, which fits a part of the employee benefits technology industry that values time-to-value over heavy customization. Over time, this segment can become strategically valuable because high-frequency data from smaller employer cohorts can deepen personalization models and raise platform engagement.

By Functionality: Enrollment Foundations Support Analytics Buildout

Enrollment and eligibility management accounted for 29.74% of the employee benefits technology market size in 2025, which reflects its role as the functional base of most deployments. Employers still start with enrollment because it connects benefit choice, eligibility rules, carrier transmission, and employee experience in one high-visibility workflow. The rest of the market is spread across core administration, self-service and decision support, compliance and audit management, analytics and reporting, and other functions that support the full benefits cycle. The analytics and reporting segment is forecast to grow at an 11.26% CAGR through 2031, making it the fastest-growing functionality as employers want stronger visibility into benefit cost trends and utilization patterns.

The rise of analytics is important because buyers are no longer satisfied with systems that only process transactions. Businessolver said in January 2025 that its AI-driven technology saved clients an average of USD 3 million through plan design optimization and data-led decision support. Compliance and audit management is also gaining importance as employers look for automated Form 5500 flagging, audit trails, and control documentation within the same platform. This keeps the employee benefits technology market focused on measurable operating value instead of feature breadth alone.

By End-user Industry: Healthcare Vertical Outpaces BFSI Leadership

BFSI held 21.28% of the employee benefits technology market size in 2025, which kept it as the largest end-user segment. Financial institutions have long used rich benefit packages as a retention tool, and they also operate under strict administrative and privacy expectations that support demand for specialized platforms. The employee benefits technology market continues to find steady demand in BFSI because these employers need accurate eligibility control, audit support, and secure handling of employee financial and health data. Healthcare and lifesciences, however, is projected to grow at a 10.63% CAGR through 2031, making it the fastest-growing end-user vertical.

That expansion is tied to both regulation and workforce complexity. The proposed HIPAA Security Rule amendments raised the need for stronger encryption, multi-factor authentication, and network segmentation, which pushes healthcare employers to upgrade older benefits and HR workflows. Post-acute care settings and distributed clinical workforces also make benefits administration harder because eligibility, location, and schedule patterns change more often than in many office-based sectors. Businessolver’s 2025 push toward WCAG 2.2 AA compliance also showed how public and healthcare-adjacent buyers are raising the bar on accessibility and digital control requirements.

Geography Analysis

North America held 40.36% of the employee benefits technology market size in 2025, which made it the largest regional market. The region benefits from a dense compliance environment that includes ACA, COBRA, ERISA, HIPAA, and a growing list of state benefit mandates. The United States remains the core demand center because self-insured employers need stronger eligibility management, cost tracking, and coordination across carriers and stop-loss structures. Canada and Mexico are also expanding their role as employers standardize administration and connecting local benefit obligations to broader HR systems. This keeps North America central to the employee benefits technology market because platform depth matters more here than basic digitization alone.

Asia-Pacific is forecast to grow at an 11.92% CAGR through 2031, which is the fastest regional rate in the employee benefits technology market. The region is expanding through different paths, with India favoring cost-efficient domestic HR technology, Southeast Asia leaning toward mobile-first access, and China showing stronger traction for local platforms tied to enterprise communication ecosystems. Adoption is rising because many employers in the region still have room to digitize benefits administration, enabling vendors to grow through access, usability, and localized compliance workflows rather than through replacement alone. At the same time, Japan and South Korea show a more measured pace because employers and employees still place a higher value on human intermediation in benefits decisions. The result is strong regional growth, but not a single regional operating model.

Europe is seeing a compliance-led upgrade cycle across the employee benefits technology market, even though the drivers differ by country. The EU Pay Transparency Directive and wider regulatory scrutiny are pushing employers to revisit compensation, reporting, and benefit data systems before gaps become operational problems. SD Worx launched Legal Watch in April 2026 to track legal changes across Germany, Luxembourg, Spain, Sweden, and the Netherlands, which shows how vendors are turning regulatory intelligence into a core product feature.[3]SD Worx, “SD Worx Simplifies Regulatory Complexity for Employers Across Europe with AI Driven SD Worx Legal Watch,” SD Worx, sdworx.com Outside Europe, South America, the Middle East, and Africa remain earlier-stage opportunities where adoption is led mainly by large multinational employers that want standardized administration across operating units.

Competitive Landscape

The employee benefits technology market remains moderately fragmented, with specialist vendors such as Businessolver, bswift, Nayya, Benefex, and Forma competing alongside broader HCM providers including SAP, Workday, and Oracle. Specialists usually win on benefits-specific depth, user guidance, and carrier connectivity, while broader suites use payroll and workforce management relationships to sell benefits administration as part of a wider package. This creates a market where product breadth alone is not enough, and vendors also need strong implementation, delivery, and credible compliance controls. The employee benefits technology market is, therefore, rewarding firms that can combine benefits expertise with platform scale. It is also pushing weaker mid-tier vendors into a harder position because they often lack both specialist depth and suite-level distribution.

Strategic moves in 2025 and 2026 show how quickly competitive lines are shifting. TriNet announced the acquisition of Cocoon in April 2026 to strengthen leave management for SMBs with AI-enabled workflows that address growing state-paid leave complexity. Vestwell completed the acquisition of Accrue 401k in early 2026, adding retirement, emergency savings, and student debt support capabilities to its platform.[4]Vestwell, “Vestwell Completes Accrue 401k Acquisition, Expanding Platform Capabilities,” PRWeb, prweb.com Businessolver had already expanded its service depth through the acquisition of ProView Global assets in July 2025, and that move directly addressed employer demand for human support wrapped around AI-led administration. These moves suggest that scale is now being built through both feature expansion and operational capability.

A second area of competition is AI-native guidance and flexible account infrastructure. Nayya’s acquisition of Northstar and the rollout of its SuperAgent platform in 2025 and 2026 pushed the market toward more autonomous benefits support. Benepass also showed the strength of wallet-based and account-led models, with revenue more than doubling between January 2025 and January 2026 and more than USD 900 million in benefits funding processed for over 250 global employers. Buyers are also treating ISO 27001, SOC 2 Type II, and accessibility standards as baseline requirements rather than premium differentiators, which shifts real competition toward benefits functionality, AI usefulness, and integration execution. That combination supports continued consolidation without pointing to a near-term winner-take-most structure.

Employee Benefits Technology Industry Leaders

bswift LLC

Aptia Group Limited

Selerix Systems, Inc.

Benefitfocus.com, Inc.

Benefex Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Benepass raised USD 40 million in Series B funding led by Centana Growth Partners. Revenue more than doubled since January 2025, the platform has processed 4.5 million-plus card transactions across USD 900 million in benefits funding for 250-plus global employers.

- April 2026: TriNet announced the acquisition of Cocoon, a compliance-driven leave management platform backed by Index Ventures. The deal strengthened TriNet's leave of absence offering for SMBs with AI-enabled workflows that navigate expanding state-level paid leave mandates.

- April 2026: SD Worx launched SD Worx Legal Watch, an AI-driven tool monitoring legislative changes across Germany, Luxembourg, Spain, Sweden, and the Netherlands. It uses a hybrid AI-plus-legal-expert model to translate regulatory shifts into actionable payroll and HR compliance guidance.

- March 2026: Vensure Employer Solutions secured USD 450 million in senior secured financing from Stone Point Capital Markets to accelerate M&A and AI-driven workforce innovation. Recent AI acquisitions included recruiting platform Distro and HR technology firm CreAI.

Global Employee Benefits Technology Market Report Scope

The Employee Benefits Technology Market refers to the global ecosystem of software platforms and related services that digitize, automate, administer, manage, and optimize employee benefits programs across organizations. These platforms enable employers, HR teams, insurers, brokers, payroll providers, and employees to manage the full lifecycle of benefits administration, including plan enrollment, eligibility verification, benefits communication, compliance management, employee self-service, decision support, carrier connectivity, payroll synchronization, analytics, and ongoing benefits engagement through centralized digital systems.

The Employee Benefits Technology Market Report is Segmented by Component (Software, and Services), Deployment Model (Cloud-based, and On-premises), Organization Size (Large Enterprises, and SMEs), Functionality (Enrollment and Eligibility Management, Core Benefits Administration, Employee Self-service and Decision Support, Compliance and Audit Management, Analytics and Reporting, and Other Functionalities), End-user Industry (BFSI, IT and Telecommunications, Healthcare and Lifesciences, Retail and E-commerce, Industrial Manufacturing, Government and Public Sector, and Other End-user Industries), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud-based |

| On-premises |

| Large Enterprises |

| SMEs |

| Enrollment and Eligibility Management |

| Core Benefits Administration |

| Employee Self-service and Decision Support |

| Compliance and Audit Management |

| Analytics and Reporting |

| Other Functionalities |

| BFSI |

| IT and Telecommunications |

| Healthcare and Lifesciences |

| Retail and E-commerce |

| Industrial Manufacturing |

| Government and Public Sector |

| Other End-user Industries |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Rest of Africa |

| By Component | Software | |

| Services | ||

| By Deployment Model | Cloud-based | |

| On-premises | ||

| By Organization Size | Large Enterprises | |

| SMEs | ||

| By Functionality | Enrollment and Eligibility Management | |

| Core Benefits Administration | ||

| Employee Self-service and Decision Support | ||

| Compliance and Audit Management | ||

| Analytics and Reporting | ||

| Other Functionalities | ||

| By End-user Industry | BFSI | |

| IT and Telecommunications | ||

| Healthcare and Lifesciences | ||

| Retail and E-commerce | ||

| Industrial Manufacturing | ||

| Government and Public Sector | ||

| Other End-user Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the 2026 value of the employee benefits technology space?

The market is estimated at USD 3.76 billion in 2026 and is forecast to reach USD 5.98 billion by 2031 at a 9.72% CAGR.

Which product type leads demand today?

Software led with 74.14% share in 2025 because enrollment, eligibility, and decision-support functions remain the core of employer deployments.

Which customer group is expanding the fastest?

SMEs are the fastest-growing organization-size segment, with a 10.74% CAGR through 2031, supported by SaaS pricing and lighter implementation models.

Why is analytics becoming more important in benefits platforms?

Analytics and reporting is projected to grow at an 11.26% CAGR because employers want better visibility into benefit costs, utilization, and renewal planning.

Which region offers the strongest growth outlook?

Asia-Pacific has the highest forecast regional CAGR at 11.92% through 2031, while North America remains the largest region by 2025 share at 40.36%.

Page last updated on: