Frontline Worker Technology Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

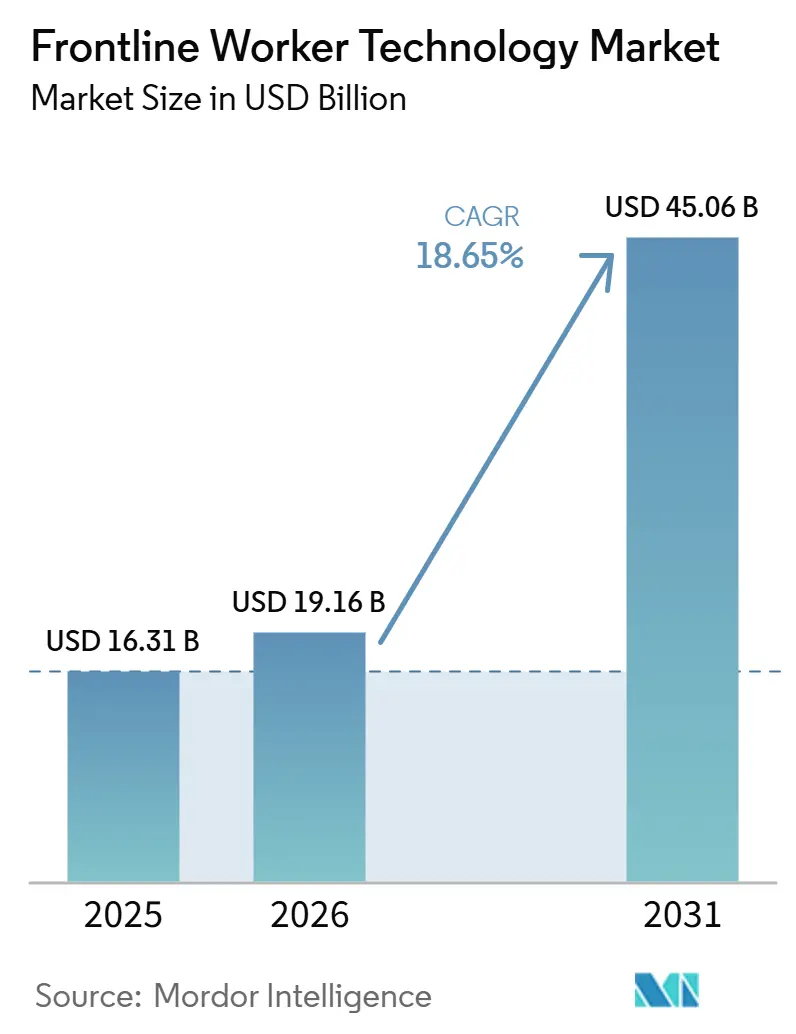

| Market Size (2026) | USD 19.16 Billion |

| Market Size (2031) | USD 45.06 Billion |

| Growth Rate (2026 - 2031) | 18.65% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Frontline Worker Technology Market Analysis by Mordor Intelligence

The frontline worker technology market size is expected to increase from USD 16.31 billion in 2025 to USD 19.16 billion in 2026 and reach USD 45.06 billion by 2031, growing at a CAGR of 18.65% over 2026-2031. The frontline worker technology market is expanding as enterprise software budgets shift toward the 2.7 billion deskless workers, who represent 80% of the global workforce but have historically received a smaller share of digital investment. AI at the operational edge, lower wearable entry costs, and stronger pressure to prove workforce productivity are bringing forward decisions that many employers had delayed for years. Tight labor conditions in logistics, retail, and manufacturing are also pushing employers to fund digital task guidance, automation, and connected workflows with clearer payback periods. Safety, traceability, and environmental health requirements are turning compliance budgets into a practical demand channel for the frontline worker technology market, especially where real-time reporting and field-level documentation matter. Competition remains active between hardware-led vendors and software-first platforms, and that keeps product development fast, even though legacy integration, worker training, and data governance still slow large rollouts in some deployments.

Key Report Takeaways

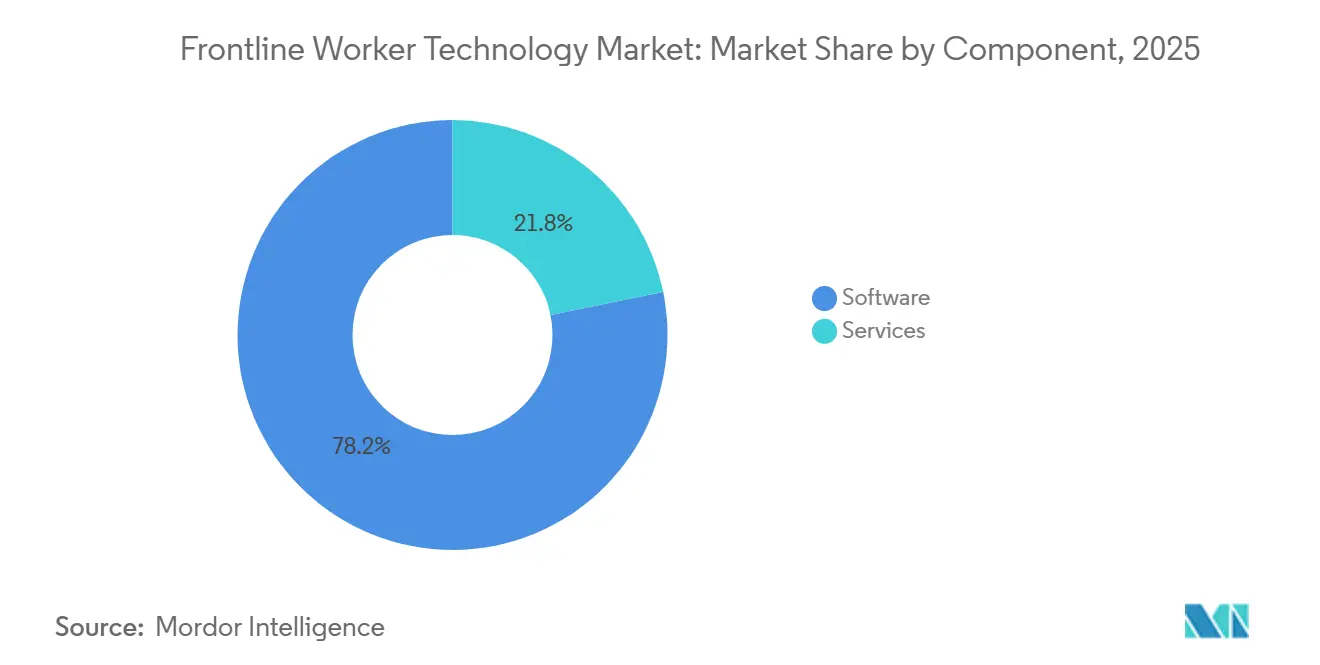

- By component, software led with 78.21% of the frontline worker technology market revenue share in 2025, while services are projected to expand at a 21.86% CAGR through 2031.

- By deployment, cloud-based held 72.49% of the frontline worker technology market in 2025 and is projected to expand at a 21.14% CAGR through 2031.

- By organization size, large enterprises held 71.23% of the frontline worker technology market in 2025, while SMEs are projected to record the highest CAGR of 21.58% through 2031.

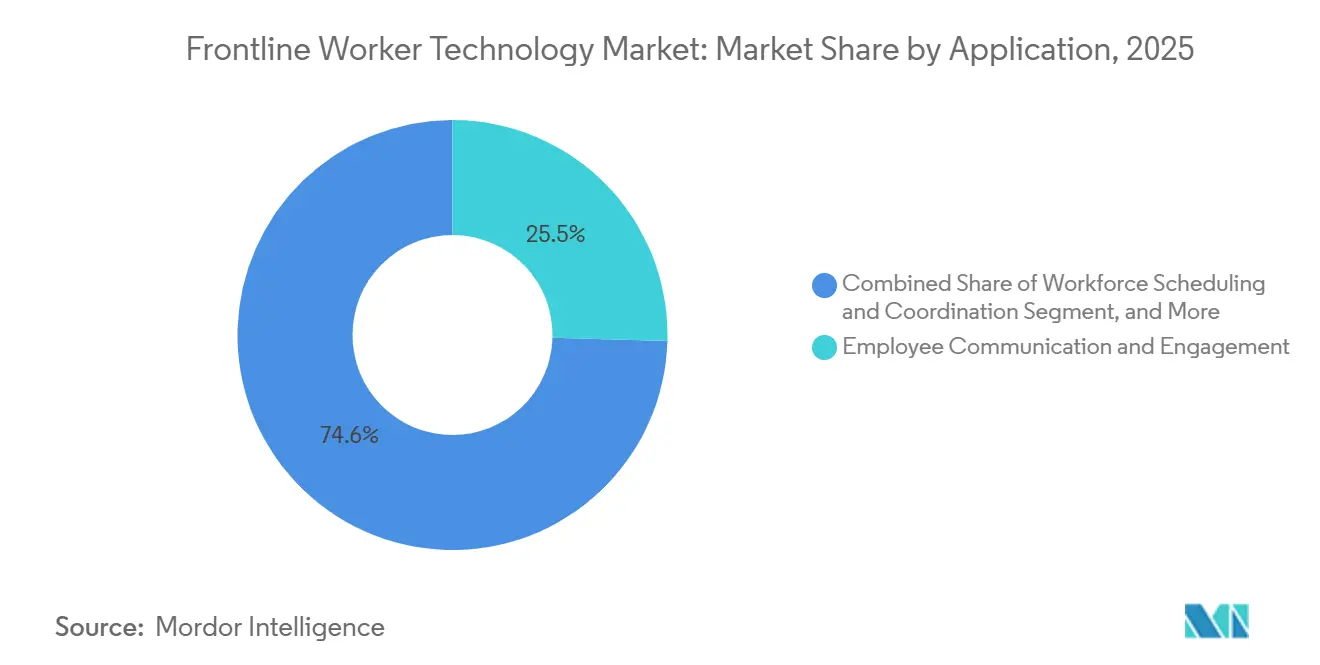

- By application, employee communication and engagement accounted for 25.45% of the frontline worker technology market in 2025, while workforce analytics and performance management are projected to grow at a 20.36% CAGR through 2031.

- By end-user industry, retail and e-commerce held 24.05% of the frontline worker technology market in 2025, while transportation and logistics is projected to expand at a 20.04% CAGR through 2031.

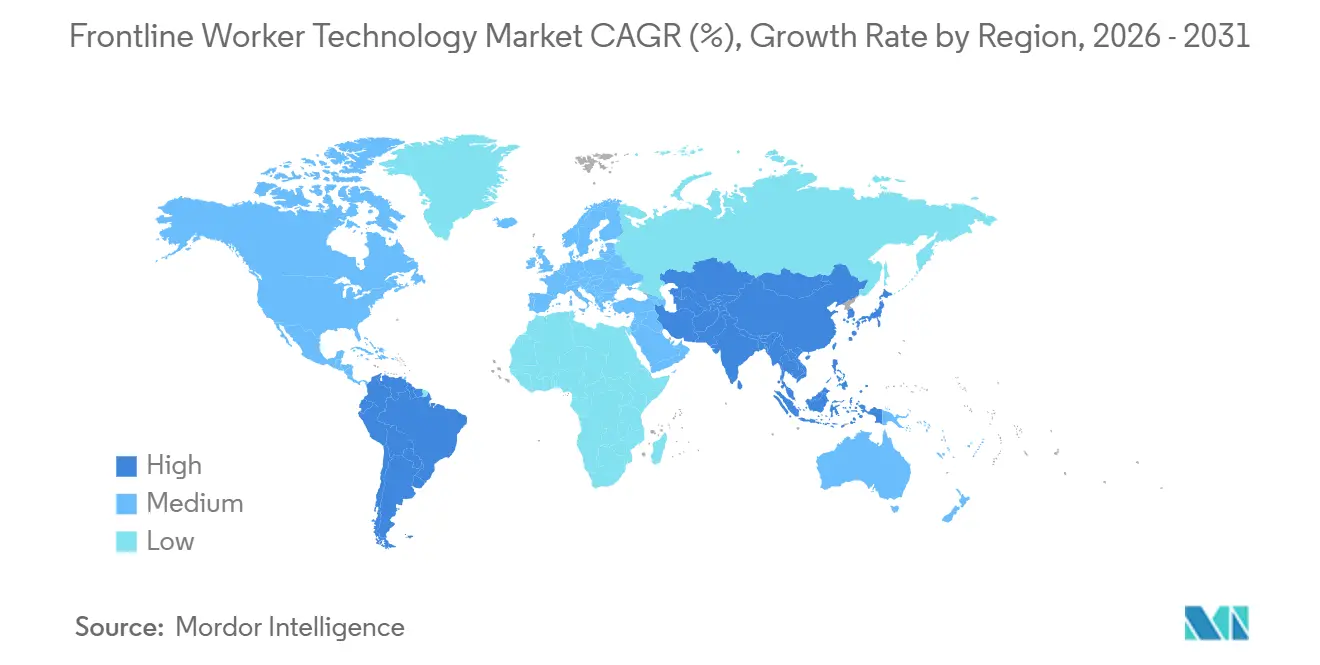

- By geography, North America held 37.51% of the frontline worker technology market in 2025, while Asia-Pacific is projected to record the fastest CAGR of 20.72% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Frontline Worker Technology Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI-Enabled Productivity Gains in Frontline Operations | +5.2% | Global, with concentrated early gains in North America and East Asia | Short term (≤ 2 years) |

| Rising Demand for Real-Time Task Orchestration | +3.8% | Global, strongest in North America, Europe, and APAC manufacturing corridors | Short term (≤ 2 years) |

| Tight Labor Markets Accelerating Task Automation | +2.9% | North America, Europe, Japan, South Korea, with spillover to Southeast Asia | Medium term (2-4 years) |

| Expansion of Rugged Mobile and Wearable Device Adoption | +2.3% | Global, with rapid penetration in APAC, Middle East and Africa, and South America field operations | Medium term (2-4 years) |

| Regulatory Push for Worker Safety and Traceability | +1.6% | North America and core Europe, with ripple effects in the Middle East and Southeast Asia | Medium term (2-4 years) |

| Multilingual Digital Enablement for Distributed Workforces | +1.1% | APAC, Middle East and Africa, and South America, including multiethnic urban logistics hubs globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

AI-Enabled Productivity Gains in Frontline Operations

AI has moved from an add-on feature to a central buying criterion in the frontline worker technology market. Walmart rolled out a GenAI-powered conversational tool for 1.5 million associates, and the platform was handling more than 3 million daily queries by mid-2025, demonstrating that adoption can scale quickly when the use case is tied to routine floor work. In manufacturing, ServiceNow introduced Industrial Connected Workforce in 2026, with AI-powered root-cause analysis that turns incident data into reusable operational knowledge for plant teams. This changes the role of frontline platforms from simple communication systems to context-aware tools that can support decisions, preserve expertise, and improve execution in real time. As the frontline worker technology market matures, those capabilities also raise switching costs because employers become more dependent on historical data, role-based workflows, and embedded operational logic.

Rising Demand for Real-Time Task Orchestration

The frontline worker technology market is shifting away from static scheduling tools toward platforms that can direct work as conditions change during a shift. Modern systems now pull data from inventory feeds, sensors, point-of-sale systems, and other enterprise applications, enabling workers to be reassigned based on live operational signals. Zebra introduced Workcloud IO in 2026 as a standardized integration layer that connects frontline workflows with enterprise systems in real time, which shows how vendors are moving beyond stand-alone task applications. That change matters because it places frontline execution much closer to the center of store, warehouse, and plant operations. It also means the competitive boundary is widening, since ERP, supply chain, and workflow vendors are now competing more directly for budgets that once sat mainly inside workforce management software.

Tight Labor Markets Accelerating Task Automation

Persistent labor pressure is making it harder to postpone digital enablement across the frontline worker technology market. Employers in labor-intensive sectors are using task automation and guided workflows to maintain output with leaner staffing and less on-the-job trial-and-error. Hitachi moved forward with AI agent development for frontline workers in power, rail, and manufacturing, and the company linked the initiative to the need to transfer expert knowledge to less experienced employees in live operating settings. That is especially important in markets where retirements, skill shortages, and higher turnover are changing the balance of experience on the shop floor. The result is a broader role for the frontline worker technology market, as many deployments are now framed as workforce continuity tools rather than solely as productivity software.

Expansion of Rugged Mobile and Wearable Device Adoption

The frontline worker technology market is also benefiting from improvements in rugged mobility, voice guidance, and wearable workflow support. Honeywell introduced Performance+ for Guided Work in 2026, with voice-guided workflows, multilingual support across 48+ languages, and real-time workforce analytics, bringing execution, training, and reporting into a single operating layer. Zebra also expanded into adjacent vision-led workflows through its machine vision ecosystem in 2026, indicating a growing connection between worker-facing applications and machine inspection environments. These developments widen the set of use cases that can justify frontline deployments, especially in warehouses, factories, and field operations where hands-free work, data capture, and guided execution can be combined. Over time, that broadens the revenue base of the frontline worker technology market because value is no longer tied solely to devices or software, but to the full workflow stack.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Total Cost of Ownership Across Hardware, Software, and Integration | -2.6% | Global, most acute in SME-heavy markets such as South America, Southeast Asia, and the Middle East and Africa | Medium term (2-4 years) |

| Interoperability Challenges With Legacy Systems and OT Networks | -1.9% | Industrial-heavy geographies such as Europe, North America, Japan, and South Korea | Long term (≥ 4 years) |

| Change Management Friction Among Non-Desk Workers | -1.3% | Global, most pronounced in high-turnover industries such as hospitality and construction | Medium term (2-4 years) |

| Data Privacy and Workforce Monitoring Concerns | -0.9% | Europe under GDPR, North America under state-level AI employment laws, and APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Total Cost of Ownership Across Hardware, Software, and Integration

Total cost of ownership remains one of the clearest limits on how fast the frontline worker technology market can spread across sectors and employer sizes. UK government research in 2025 found that licensing fees and technology costs were the most frequently cited barriers to adoption, with staff training following closely behind, mirroring the practical issues seen in broader frontline digitization programs.[1]UK Government DSIT, “Findings from the 2025 Adult Social Care Provider Technology Survey,” GOV.UK, gov.uk Cost pressure is not limited to software subscriptions, since employers also face rugged device refresh cycles, integration work, training for new and existing staff, and continuing support for high-turnover teams. In more complex rollouts, the payback case can weaken further, as operations often need time to regain productivity while employees adjust to new workflows. That cost structure slows adoption in parts of the frontline worker technology market where budgets are tighter and deployment scale is harder to spread across large workforces.

Interoperability Challenges With Legacy Systems and OT Networks

Interoperability is another persistent barrier for the frontline worker technology market, especially in manufacturing, transportation, energy, and other asset-heavy environments. Many operational technology networks still rely on proprietary protocols and older control systems, so frontline applications cannot always connect to machine data without added middleware, testing, and security review. This makes large deployments slower because the value of real-time workflow tools depends on reliable links between the field, enterprise software, and plant systems. It also raises the burden on vendors, since connected devices and applications increasingly have to meet cybersecurity and industrial control expectations before buyers will scale a deployment. As a result, the frontline worker technology market can move quickly in cloud-native service environments, but the path is still longer in settings where legacy OT infrastructure remains central to daily operations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Anchors Revenue, Services Scale With Enterprise Adoption

Software captured 78.21% of the frontline worker technology market share in 2025, and that lead reflects employers' preference for platform-first deployments over one-off device purchases. The software layer often combines communication, task execution, analytics, and compliance management into a single subscription, making it easier for employers to standardize work across dispersed teams. That structure provides software vendors with stronger retention, as workflows, historical data, and user habits become embedded in daily operations. It also shows that buying behavior in the frontline worker technology market is moving toward systems of execution rather than isolated productivity tools. Once a platform is adopted across multiple sites, the operational burden of changing vendors becomes much higher.

Services are projected to expand at a 21.86% CAGR from 2026 to 2031, which confirms that implementation work remains central to the value chain. Large deployments still require integration with ERP, warehouse management, and HR systems, as well as change management, analytics support, and workflow design. Honeywell’s 2026 Performance+ for Guided Work clearly shows this shift by pairing voice-guided execution with analytics and a broader connected workforce framework, rather than selling a narrow device-led offer. That approach suggests that the frontline worker technology industry is placing greater value on recurring service relationships than on single-deployment events. It also means the frontline worker technology market is becoming harder to serve with hardware-only strategies, since buyers increasingly want long-term operational support around the platform.

By Deployment: Cloud Consolidates Across Verticals, Hybrid Bridges OT Complexity

Cloud-based deployment accounted for 72.49% of the frontline worker technology market in 2025 and is projected to record the fastest CAGR of 21.14% through 2031. Employers continue to favor cloud delivery because it reduces upfront infrastructure requirements and allows new functionality to be rolled out across sites with less delay. The leadership of cloud also shows that many new projects in retail, logistics, healthcare, and field services are being designed around subscription access rather than local server ownership. In the frontline worker technology market, this makes adoption easier for organizations that need fast scaling, multi-site coordination, and lower initial capital commitments. It also supports broader use across mobile devices, kiosks, and shared access points that are common in non-desk settings.

Hybrid deployment remains an important bridge for employers that still need closer control over data flows from industrial or regulated environments. Many manufacturers and utilities cannot move everything at once, so hybrid models allow them to keep sensitive systems anchored while bringing selected workflows into cloud governance. ServiceNow’s EmployeeWorks illustrates how cloud-native platforms are being built for mixed frontline access environments, as the product is available via Teams, Slack, shared workstation browsers, and plant-floor kiosks. That flexibility matters because the frontline worker technology industry serves workforces that do not operate from a single device type or work context. On-premises demand remains present in defense, utilities, and national infrastructure settings, but the wider direction of the frontline worker technology market still points toward cloud-led expansion.

By Organization Size: Enterprise Scale Anchors Spend, SMEs Lead Growth Rate

Large enterprises accounted for 71.23% of the frontline worker technology market in 2025, reflecting their stronger budgets, existing IT infrastructure, and greater need for standardized workflows across sites and functions. They are also better positioned to absorb integration costs, pilot multiple use cases, and extend existing enterprise software into frontline settings. In many cases, adoption is being supported by established vendor relationships rather than stand-alone buying cycles. SAP’s integration with Microsoft 365 created a more unified AI experience for business data and daily collaboration, helping reduce friction for managers and supervisors working across systems.[2]SAP Community, “SAP + Microsoft 365, A Unified AI Experience That Works Where You Work,” SAP Community, sap.com That pattern favors the frontline worker technology market because large employers can scale deployments faster when new tools sit inside platforms their workforce already uses.

SMEs are projected to record the highest CAGR of 21.58% from 2026 to 2031, reflecting lower entry barriers than in earlier phases of digitization. Mobile-first tools, simpler subscription plans, and more focused use cases are allowing smaller employers to adopt without the same burden of legacy system redesign. This part of the frontline worker technology market is important because many smaller operations need communication, scheduling, and task-execution tools but do not require enterprise-scale complexity. The stronger SME growth rate also shows that the addressable base is widening beyond the employers that first drove market formation. As that expands, the frontline worker technology industry is likely to see more competition on usability, deployment speed, and affordability than on the breadth of enterprise features.

By Application: Communication Establishes The Digital Foundation, Analytics Drives Optimization

Employee communication and engagement accounted for 25.45% in 2025, making it the largest application area in the frontline worker technology market. That position reflects the fact that many employers began digitization by replacing paper notices, informal messaging channels, and radio-based coordination with auditable digital communication tools. Communication platforms often serve as the first formal layer because they can be deployed broadly and deliver early, visible operational benefits. Their lead also indicates that much of the frontline worker technology market is still shaped by foundation-building rather than by advanced optimization alone. Once that foundation is in place, it becomes easier to add task orchestration, scheduling, analytics, and safety workflows on top of the same user base.

Workforce analytics and performance management are projected to expand at a 20.36% CAGR through 2031, indicating that employers are moving from visibility to measurable optimization. As organizations gather more activity, compliance, and task data, they gain a stronger basis for productivity management and cost control. NomadGo’s deployment across more than 11,000 Starbucks locations by September 2025 showed how AI-driven workflow execution can raise speed and counting accuracy in a high-frequency operating environment. Workforce execution and task management, along with scheduling and coordination, continue to play a central role in retail, logistics, and healthcare, where labor demand shifts quickly during the day. Safety and compliance management is also gaining weight in the frontline worker technology market because digital documentation and incident capture are becoming more valuable in regulated and high-risk settings.

By End-User Industry: Retail Anchors Demand, Logistics Captures Growth Momentum

Retail and e-commerce accounted for 24.05% of the frontline worker technology market size in 2025, and that leadership reflects scale, measurable task outcomes, and the direct impact of frontline execution on customer experience. Store networks, fulfillment operations, and omnichannel workflows all create daily coordination needs that digital frontline tools can address visibly. Retail buyers also tend to value faster deployment, simple user experiences, and repeatable execution across many locations, which fits the strengths of the current platform mix. That is why the frontline worker technology market has seen many of its most visible use cases emerge first in stores and consumer-facing logistics settings. The sector remains a strong anchor because its workforce size and operating pace make productivity gains easier to measure than in some other verticals.

Transportation and logistics are projected to grow at a 20.04% CAGR through 2031, and that momentum is tied to e-commerce fulfillment, denser last-mile networks, and greater interest in hands-free and mobile workflow support. Shoprite’s use of YOOBIC across more than 3,600 stores demonstrated how distributed operations are moving toward unified task, communication, and engagement platforms rather than separate tools for each function. Healthcare and life sciences also remain important because staffing pressure, handoff quality, and clinical coordination all benefit from better frontline communication and documentation. Google Cloud’s work with HCA Healthcare on a nurse handoff application showed how structured AI support can fit into sensitive care workflows without treating frontline needs as a back-office problem. Construction, hospitality, government, and industrial manufacturing are still developing at different speeds, but each adds to the breadth of the frontline worker technology market as use cases become more specialized and easier to deploy.

Geography Analysis

North America accounted for 37.51% of the frontline worker technology market share in 2025, maintaining the region's leading position. That leadership reflects a high concentration of large enterprise buyers, stronger SaaS adoption patterns, and more mature procurement structures for digital workplace tools. The region also benefits from broad demand for safety, reporting, communication, and workflow visibility across retail, logistics, healthcare, and field services. In the frontline worker technology market, those conditions support faster scaling because many buyers already have the IT governance, vendor relationships, and multi-site operating structures needed for enterprise rollouts.

Asia-Pacific is projected to record the fastest CAGR of 20.72% through 2031 in the frontline worker technology market. Public digitization efforts, mobile-first workforce behavior, and stronger AI adoption in manufacturing settings are supporting growth in the region. China and Japan are adding momentum through factory-oriented use cases, where digital guidance, operational visibility, and worker support tools align with broader automation priorities. Hitachi’s work on frontline AI agents in power, rail, and manufacturing highlights how knowledge transfer and live operational assistance are becoming central themes in Japanese deployments.[3]Hitachi, “Hitachi Advances Strategic Alliance with Google Cloud to Accelerate Frontline Worker AI Agents,” Hitachi, hitachi.com The region’s scale matters because even moderate penetration across large labor pools can create a sizable long-term revenue base for the frontline worker technology market.

Europe remains important because product adoption is shaped not only by demand but also by strict rules around worker data, consultation, and AI oversight. That regulatory structure influences how vendors design monitoring features, data flows, and user permissions before they can expand into industrial and service environments. Healthcare and industrial settings stand out because workforce shortages, compliance needs, and remote support requirements all increase the appeal of connected worker tools. South America, the Middle East, and Africa, and emerging Southeast Asian markets are early-stage regions, but they are advancing as retail formalization, labor management programs, and mobile-first deployments gather pace. Together, those regions expand the geographic reach of the frontline worker technology market beyond its current core demand centers.

Competitive Landscape

The frontline worker technology market remains moderately fragmented at the hardware level, while platform competition is becoming more concentrated around vendors that can combine workflow software, analytics, and enterprise integration. Zebra Technologies, Honeywell, RealWear, and Getac compete through rugged devices and ecosystem depth, while software-led players such as ServiceNow, Microsoft, and specialized vendors compete through AI features, workflow design, and user experience. This creates a two-layer competitive structure in which devices still matter, but long-term value is shifting toward platforms that can orchestrate work and connect data across environments. In that setting, the frontline worker technology market rewards vendors that can sell both operational relevance and lower deployment friction. It also favors suppliers that can support large customers over multiple years rather than only win one-time hardware contracts.

Several strategic moves show how quickly vendor positioning is evolving in the frontline worker technology market. Zebra launched Zebra Nucleus, Workcloud BI, and Workcloud IO in 2026, expanding its offering from rugged mobility to fleet oversight, role-based analytics, and real-time systems integration. Honeywell added Performance+ for Guided Work in 2026, tying voice-led execution more closely to analytics and adding multilingual support for warehouse and logistics users.[4]Honeywell, “Honeywell Launches New Performance+ for Guided Work to Enable Faster, Smarter Supply Chain Operations,” Honeywell, honeywell.com ServiceNow also moved deeper into plant-floor use cases through Industrial Connected Workforce and EmployeeWorks, showing how enterprise workflow vendors are pushing into roles once served by more specialized frontline tools.

White-space opportunities remain visible in SME-focused cloud platforms, healthcare-oriented frontline coordination, and emerging markets that have less legacy workforce software to replace. Those openings matter because many smaller or less digitized employers want simple deployment, mobile-first access, and limited integration effort rather than broad enterprise suites. The frontline worker technology market also leaves room for disruptors that solve specific operational pain points through standard smartphones, light wearables, or focused engagement tools. At the same time, rising compliance expectations and buyer demand for proven integrations can still protect larger vendors with broader product stacks, stronger certification readiness, and deeper channel reach.

Frontline Worker Technology Industry Leaders

Zebra Technologies Corporation

Honeywell International Inc.

Datalogic S.p.A.

Kontron AG

Advantech Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Zebra Technologies unveiled its machine vision ecosystem on June 22, 2026, including the CV70 CXP camera, at Automate 2026 in Chicago. The. The portfolio supports AI-based anomaly detection, 3D inspection, and RFID-integrated automated staging, targeting EV battery assembly and semiconductor inspection workflows.

- June 2026: Zebra Technologies launched Zebra Nucleus, Workcloud BI, and Workcloud IO on June 2, 2026, at its ZONE 2026 customer conference in Nashville. Zebra Nucleus provides unified device fleet oversight, while Workcloud BI delivers AI-powered, role-based dashboards, and Workcloud IO creates a standardized integration layer that connects frontline workflows to enterprise systems.

- May 2026: ServiceNow launched Industrial Connected Workforce and EmployeeWorks at Knowledge 2026 in Las Vegas. Industrial Connected Workforce digitizes frontline work with AI-powered root-cause analysis, while EmployeeWorks delivers a conversational AI interface for plant-floor employees via Teams, Slack, kiosks, and shared workstations.

- January 2026: Honeywell launched Performance+ for Guided Work, a connected workforce solution combining voice-driven task guidance with advanced analytics. The platform supports 48+ languages and provides real-time workforce performance insights for warehousing, retail, and logistics operations.

Global Frontline Worker Technology Market Report Scope

The Frontline Worker Technology Market includes digital solutions, software platforms, connected devices, and productivity tools that support employees working outside traditional office environments. These technologies enable communication, task execution, workforce management, training, collaboration, safety monitoring, and operational decision-making for workers in industries such as manufacturing, retail, healthcare, logistics, construction, energy, and field services. Increasing digital transformation initiatives, rising demand for workforce productivity, and the need to improve operational visibility and employee engagement drive the market. The market focuses on connecting frontline employees with enterprise systems, workflows, and real-time operational data to improve efficiency, safety, and business performance.

The Frontline Worker Technology Market Report is Segmented by Component (Software, and Services), Deployment (Cloud-Based, Hybrid, and On-Premises), Organization Size (Large Enterprises, and Small and Medium Enterprises), Application (Employee Communication and Engagement, Workforce Execution and Task Management, Workforce Scheduling and Coordination, Learning and Knowledge Enablement, Workforce Analytics and Performance Management, Safety and Compliance Management, and Other Applications), End-User Industry (Retail and E-Commerce, Industrial Manufacturing, Healthcare and Life Sciences, Transportation and Logistics, Hospitality, Construction, Government and Public Administration, and Other End-User Industries), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud-Based |

| Hybrid |

| On-Premises |

| Large Enterprises |

| Small and Medium Enterprises |

| Employee Communication and Engagement |

| Workforce Execution and Task Management |

| Workforce Scheduling and Coordination |

| Learning and Knowledge Enablement |

| Workforce Analytics and Performance Management |

| Safety and Compliance Management |

| Other Applications |

| Retail and E-Commerce |

| Industrial Manufacturing |

| Healthcare and Life Sciences |

| Transportation and Logistics |

| Hospitality |

| Construction |

| Government and Public Administration |

| Other End-User Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Southeast Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Component | Software | ||

| Services | |||

| By Deployment | Cloud-Based | ||

| Hybrid | |||

| On-Premises | |||

| By Organization Size | Large Enterprises | ||

| Small and Medium Enterprises | |||

| By Application | Employee Communication and Engagement | ||

| Workforce Execution and Task Management | |||

| Workforce Scheduling and Coordination | |||

| Learning and Knowledge Enablement | |||

| Workforce Analytics and Performance Management | |||

| Safety and Compliance Management | |||

| Other Applications | |||

| By End-User Industry | Retail and E-Commerce | ||

| Industrial Manufacturing | |||

| Healthcare and Life Sciences | |||

| Transportation and Logistics | |||

| Hospitality | |||

| Construction | |||

| Government and Public Administration | |||

| Other End-User Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Southeast Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current and forecast value of frontline worker technology?

The frontline worker technology market size was USD 16.31 billion in 2025, reaches USD 19.16 billion in 2026, and is forecast to reach USD 45.06 billion by 2031 at an 18.65% CAGR.

What is driving adoption of frontline digital tools across enterprises?

The main demand factors are AI-enabled productivity, real-time task orchestration, labor shortages, wearable and rugged device adoption, and stronger safety and traceability requirements.

Which component category leads spending on frontline worker technology?

Software led with 78.21% of revenue in 2025, which reflects demand for platform-based communication, execution, analytics, and compliance tools.

Which deployment model is growing fastest for frontline operations software?

Cloud-based deployment led the market in 2025 and is also projected to expand at a 21.14% CAGR through 2031 because it supports easier scaling and lower upfront infrastructure needs.

Which end-user sectors are creating the biggest revenue opportunities?

Retail and e-commerce led with 24.05% in 2025, while transportation and logistics is projected to grow fastest at a 20.04% CAGR through 2031.

Which region is expanding fastest in frontline worker technology adoption?

Asia-Pacific is projected to record the fastest CAGR of 20.72% through 2031, supported by public digitization efforts and stronger manufacturing-related AI adoption.

Page last updated on: