United States Frontline Worker Technology Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

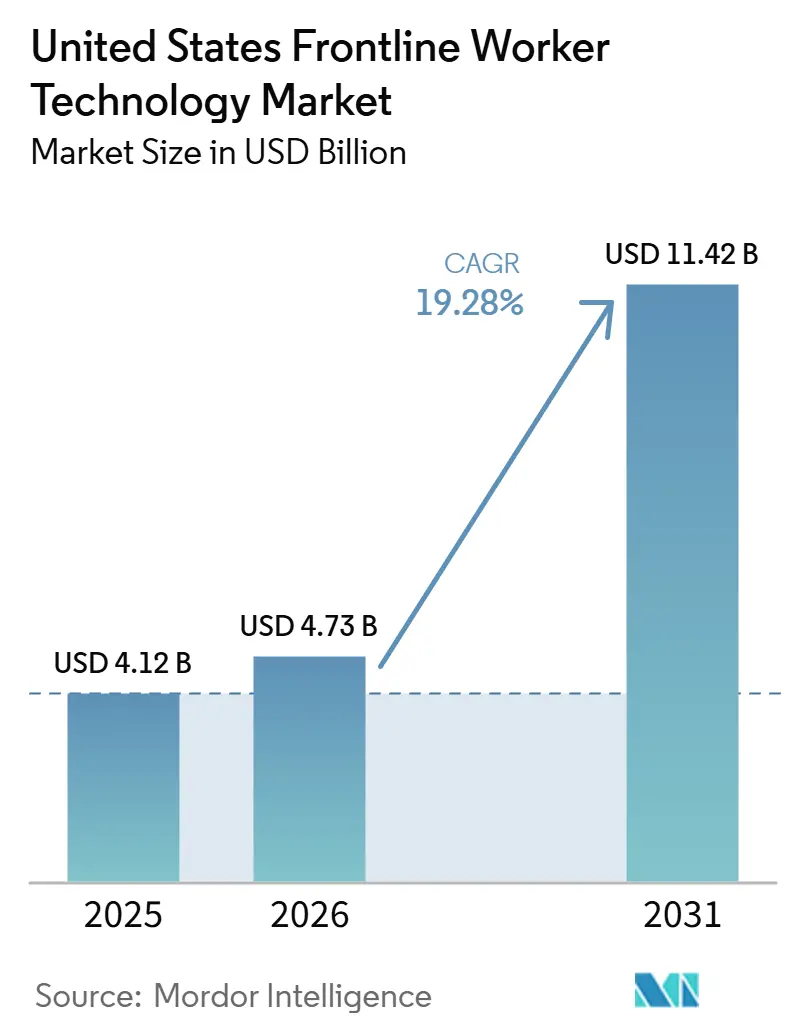

| Base Year Market Size (2025) | USD 4.12 Billion |

| Market Size (2026) | USD 4.73 Billion |

| Market Size (2031) | USD 11.42 Billion |

| Growth Rate (2026 - 2031) | 19.28% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Frontline Worker Technology Market Analysis by Mordor Intelligence

The United States frontline worker technology market size was valued at USD 4.12 billion in 2025 and estimated to grow from USD 4.73 billion in 2026 to reach USD 11.42 billion by 2031, at a CAGR of 19.28% during the forecast period (2026-2031). The market is expanding because U.S. employers are under pressure to raise productivity across distributed locations while serving a workforce that received less software investment than desk-based teams for many years. AI, mobile-first application design, and tighter workplace oversight are pushing buyers to treat frontline systems as core operating tools rather than optional add-ons. Procurement decisions now favor platforms that can support fast rollout, simple daily use, and clearer operating accountability across stores, plants, warehouses, and field locations. Competitive behavior is also shifting as software vendors add automation and guidance tools, while hardware companies build more intelligence into their device portfolios. Growth in the United States frontline worker technology market now depends not only on demand, but also on how well vendors help employers convert deployment into measurable worker, site, and workflow outcomes.

Key Report Takeaways

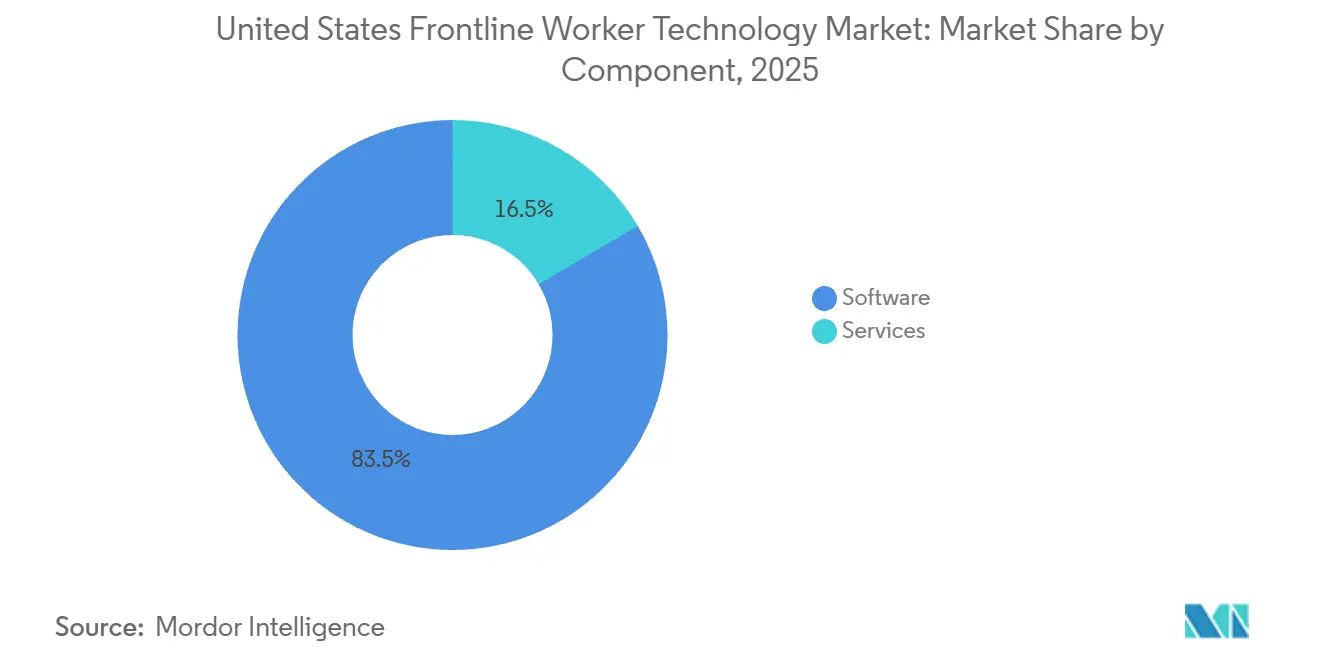

- By component, software held 83.47% of the United States frontline worker technology market share in 2025, while services are projected to expand at 22.36% CAGR through 2031.

- By deployment, cloud-based deployment accounted for 82.63% of revenue in 2025 and is projected to grow at 19.84% CAGR through 2031.

- By organization size, large enterprises held 72.18% of revenue in 2025, while SMEs are projected to expand at 21.41% CAGR through 2031 in the United States frontline worker technology market.

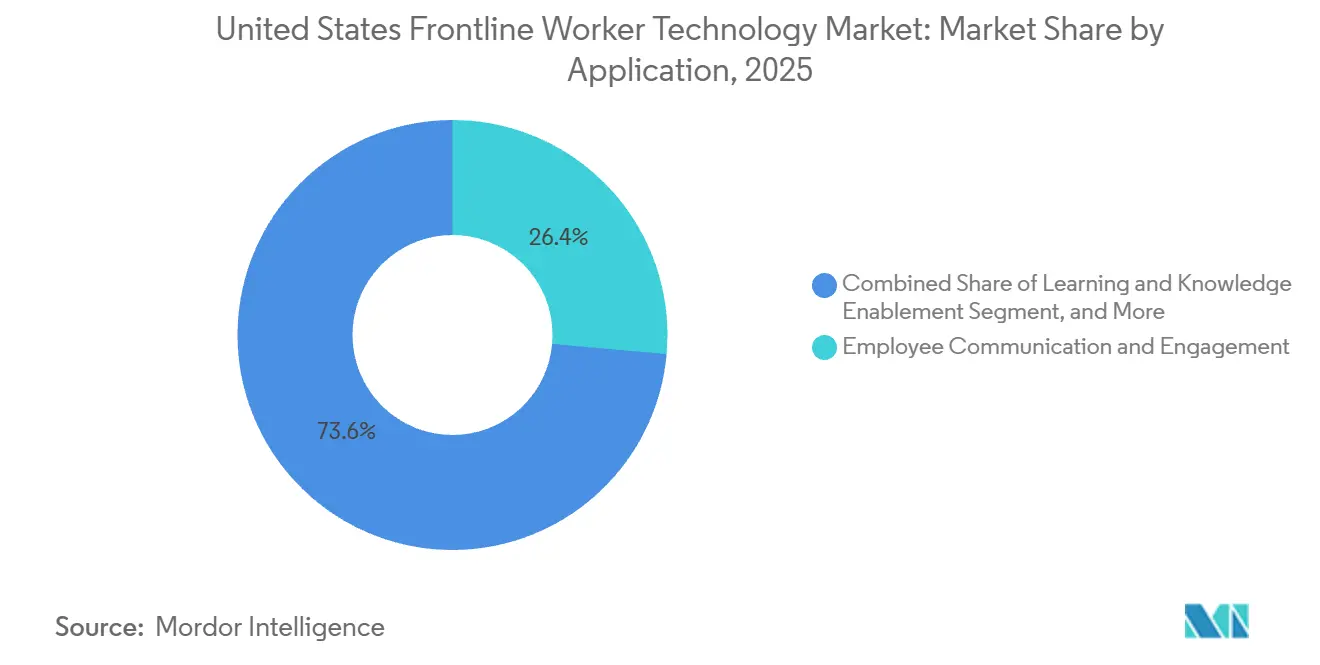

- By application, employee communication and engagement held 26.42% of revenue in 2025, while workforce analytics and performance management is projected to grow at 22.81% CAGR through 2031.

- By end-user industry, retail and e-commerce held 28.14% of revenue in 2025, while transportation and logistics is projected to expand at 21.93% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Frontline Worker Technology Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Real-Time Frontline Visibility | +4.2% | National, with concentrated gains in industrial and retail corridors across the Midwest and Sun Belt | Short term (≤ 2 years) |

| Increasing Adoption of Mobile-First Task Execution | +3.8% | National, with early momentum in Sun Belt logistics hubs, Northeast healthcare, and West Coast retail | Short term (≤ 2 years) |

| AI-Enabled Workforce Guidance and Knowledge Capture | +3.5% | National, particularly in manufacturing-dense states including Michigan, Ohio, Texas, and North Carolina | Medium term (2-4 years) |

| Expansion of Wearables in Safety-Critical Workflows | +2.9% | National, with early gains in oil and gas, utilities, construction, and chemical processing | Medium term (2-4 years) |

| Compliance Pressure in Multi-Site Operations | +2.1% | National, with regulatory influence most acute in California, New York, Illinois, and Colorado | Medium term (2-4 years) |

| Labor Productivity Gap Across Deskless Workforces | +1.8% | National, most acute in U.S. manufacturing, logistics, and agriculture | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Real-Time Frontline Visibility

Operational blind spots between frontline work settings and enterprise reporting systems remain a major cost issue, which is pushing companies to move visibility tools from isolated pilots into broader operating use. Zebra Technologies reported in June 2026 that 51% of U.S. retailers were piloting AI for inventory optimization and 45% were piloting it for cost optimization, both of which depend on live data flowing from frontline settings into management systems.[1]Zebra Technologies, “Zebra Technologies Empowers Frontline Workers With New DNA Software Platforms and AI-Powered Solutions,” Zebra Technologies, zebra.com This shift is changing management practice because performance can now be linked to a specific site, shift, task, or event instead of relying on delayed weekly or monthly summaries. Honeywell said in March 2026 that Experion Operations Assistant generated alarm predictions 5-10 minutes before incidents during pilot work with Chevron and TotalEnergies, showing how earlier visibility can support avoided downtime and faster operator response. Buyers, therefore, view visibility software as an operating control layer with direct payback rather than as a reporting add-on used after a process failure. In the United States frontline worker technology market, that change is helping compress evaluation cycles in settings where a short delay can affect service levels, worker output, inventory accuracy, or safety performance.

Increasing Adoption of Mobile-First Task Execution

The mobile device is replacing paper forms, static checklists, and radio-based instructions as the main workflow interface for many frontline workers across U.S. operations. Modern mobile applications are gaining traction because they support offline use, voice input, guided task routing, and simple daily workflows that reduce friction for workers who spend little time at a desk. Honeywell launched Performance+ for Guided Work in January 2026, combining voice-directed workflow tools with analytics for retail, transportation, logistics, and healthcare operators that need faster execution and better frontline visibility. Microsoft reported in its 2026 Work Trend Index that active AI agents in the Microsoft 365 ecosystem grew 15x from March 2025 to March 2026, with manufacturing showing deeper deployment per organization than other sectors in the study.[2]Microsoft, “2026 Work Trend Index Report, Agents, Human Agency, and Opportunity,” Microsoft WorkLab, microsoft.com The same study said organizational factors such as manager adoption, cultural permission to experiment, and incentives explained more than 2x the reported AI impact compared with individual tool usage alone. For the United States frontline worker technology market, this means the mobile-first advantage depends as much on rollout design and operating discipline as it does on the application itself.

AI-Enabled Workforce Guidance and Knowledge Capture

AI-enabled guidance tools are gaining ground because many employers need to preserve know-how while turnover and retirement continue to disrupt daily work in frontline roles. These systems convert repair instructions, safety steps, operating procedures, and compliance routines into searchable digital workflows that less experienced workers can follow while the work is taking place. ServiceNow said in February 2026 that its Autonomous Workforce handled more than 90% of employee IT requests internally and resolved support cases 99% faster than human agents, giving buyers a visible benchmark for scaled AI guidance in enterprise environments. That result matters because buyers in the United States frontline worker technology market increasingly want systems that can complete guided work or support decisions at the point of use, not software that only surfaces information after a delay. SHRM reported in 2025 that 90% of U.S. CHROs expected AI integration in frontline environments to intensify, while only 19% of organizations were using AI specifically for upskilling and reskilling. The gap between expected adoption and current workforce development use leaves strong room for platforms that can capture operational knowledge and deliver it at the moment of need.

Expansion of Wearables in Safety-Critical Workflows

Connected wearables are moving from limited trials into broader safety programs in sectors where delayed response, lone work, or poor situational awareness can create serious operating risk. The EEOC stated in 2024 that workplace wearables and biometric tools can violate federal anti-discrimination laws if employers use them without appropriate safeguards, which has made governance review part of many buying processes. That guidance has not blocked adoption, but it has changed vendor evaluation by making consent, data use, monitoring boundaries, and documentation more visible during procurement. Blackline Safety said Liberty Utilities deployed 300 connected devices across its gas, water, and electric divisions to protect lone workers across North America, showing that safety and compliance requirements can directly trigger enterprise purchase decisions. Vendors are also reducing adoption friction by shifting rugged wearable offerings toward subscription-based delivery and broader software support rather than one-time hardware sales. In the United States frontline worker technology market, that mix of safety pressure and easier commercial models is widening the use case for connected frontline equipment across field and industrial settings.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Integration Complexity with Legacy Systems | -3.2% | National, most acute in mid-market manufacturing and retail with installed ERP or WMS systems aged 10+ years | Medium term (2-4 years) |

| Frontline User Adoption and Change Resistance | -2.8% | National, with elevated friction in unionized industries and multi-generational workforces | Medium term (2-4 years) |

| Data Privacy and Continuous Monitoring Concerns | -1.9% | National, with compliance factors concentrated in California, New York, Colorado, and Illinois | Long term (≥ 4 years) |

| Device Durability, Battery Life, and Support Cost Constraints | -1.4% | National, most acute in outdoor, heavy industrial, and cold-chain environments | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Integration Complexity with Legacy Systems

High integration complexity remains one of the clearest limits on adoption because many employers still run ERP, warehouse, manufacturing, and operational systems that were not built for real-time exchange. When new frontline tools must connect through custom middleware, project timelines often get longer, internal IT pressure rises, and the total cost of ownership becomes harder to defend. This issue is sharper in the mid-market because many companies do not have dedicated integration engineers and must depend on vendor services for even basic system connectivity. That burden helps explain why services is the fastest-growing component in the United States frontline worker technology market, since buyers often need implementation, training, workflow design, and managed support together with software licenses. Hybrid deployment also remains important for this reason, because many firms keep core systems on-site while layering cloud communication, analytics, or guidance applications around them. Vendors that reduce the integration load inside the product itself are better positioned to secure larger multi-site contracts and renewals over time.

Frontline User Adoption and Change Resistance

Technology deployment still underperforms when frontline employees do not see an immediate personal benefit in the first workflow they receive. UKG reported in 2026 that 76% of frontline employees experienced burnout in 2025, which means many workforces approach new tools with limited patience for disruptive change or poorly sequenced rollout plans. Microsoft reported in its 2026 Work Trend Index that 65% of AI users feared falling behind without AI, yet 45% felt safer focusing on current goals than redesigning their work, which highlights the tension between curiosity and daily work pressure. That tension is especially relevant for hourly roles where workers are judged on output, service, or safety, not on experimentation with unfamiliar digital tools. Programs tend to perform better when the first use case solves a direct employee need, such as schedule visibility, pay access, or next-task guidance, before management pushes deeper analytics goals. In the United States frontline worker technology market, adoption therefore depends as much on rollout design, training rhythm, and workflow relevance as it does on the platform itself.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Leads the Revenue Base While Services Drive the Fastest Expansion

Software held 83.47% of revenue in 2025, which gave it the largest position in the United States frontline worker technology market share. That lead reflects a steady shift toward unified suites that combine communication, task execution, analytics, and safety management in one operating layer instead of scattered point tools. Buyers increasingly want fewer worker-facing applications because too many apps add confusion, slow adoption, and weaken data consistency across sites. Zebra highlighted this issue as app overload at its June 2026 ZONE conference, pointing to customer demand for simpler frontline digital environments that reduce operating friction. In practical terms, the strength of software comes from its role as the control layer that links workers, devices, site activity, and enterprise decision-making.

Services is projected to expand at 22.36% CAGR from 2026 to 2031, making it the fastest-growing component in the United States frontline worker technology market. The strength of services follows from the implementation work required to configure workflows, connect systems, train users, and support live operations after launch. Many employers are not buying software as a standalone product, because deployment success often depends on process design, user support, policy alignment, and continuing optimization after the contract is signed. This is especially true in large deployments where multi-site rollout creates variation in worker routines, hardware conditions, language needs, and system readiness across locations. As a result, recurring services revenue is becoming more important to vendors that want stronger retention, deeper account penetration, and better deployment outcomes. The component mix is therefore led by software today, but a growing share of future value will come from the services needed to make that software work at scale.

By Deployment: Cloud-Based Platforms Anchor Scalability While Hybrid Models Stay Relevant

Cloud-based deployment held 82.63% of revenue in 2025 and is projected to grow at 19.84% CAGR through 2031, which keeps it central to the United States frontline worker technology market size. That position reflects the needs of retailers, logistics operators, healthcare networks, and field-intensive organizations that manage many locations and need shared data across all of them. Cloud delivery reduces the infrastructure duplication that would come with maintaining separate local setups for each warehouse, store, clinic, plant, or service branch. It also fits subscription spending models that make platform entry easier and software updates more manageable over time. For many buyers, cloud deployment now represents the most practical way to scale frontline tools across a broad operating footprint without rebuilding local IT support at every site.

Hybrid deployment still has a meaningful role because many large organizations continue to keep core systems such as MES, EHR, POS, or ERP environments on-site while adding cloud communication or analytics layers around them. This layered approach allows companies to modernize worker-facing workflows without forcing immediate replacement of deeply embedded operational systems. On-premises deployment is losing share overall, but it still matters in settings where worker activity data, procurement rules, or security requirements support tighter local control. Microsoft reported in its 2026 Work Trend Index that active AI agents in the Microsoft 365 ecosystem grew 15x from March 2025 to March 2026, reinforcing how strongly the next wave of automation depends on cloud-based infrastructure. Within the United States frontline worker technology industry, deployment choice is now less about a simple cloud versus on-site decision and more about how quickly companies can connect users, sites, and workflows without disrupting existing operations. Buyers are increasingly selecting the model that minimizes rollout friction while preserving access to critical legacy systems.

By Organization Size: Large Enterprises Dominate Current Spend While SMEs Gain Speed

Large enterprises accounted for 72.18% of 2025 revenue, reflecting their earlier access to capital, IT staffing, and integration capacity. Their scale makes the return from better communication, task coordination, compliance tracking, and analytics easier to measure across hundreds or thousands of workers and locations. In the United States frontline worker technology market, large organizations have usually moved first because they can support longer procurement cycles and more complex rollout requirements. They also tend to prefer broad platforms rather than single-use tools, which has favored vendors that can package workflow, intelligence, and governance in one environment. This dominance shows that complex enterprise accounts remain the main revenue base for the category even as adoption spreads more widely.

SMEs are projected to expand at 21.41% CAGR from 2026 to 2031, which gives them a faster growth path in this segmentation. Cloud delivery and mobile-first application design are lowering entry barriers for smaller operators that want frontline tools without long implementation cycles or large internal IT teams. This matters in retail, food service, and construction, where a high deskless workforce mix makes simple communication and task applications useful even without full enterprise integration. Blink said in July 2026 that it raised USD 17 million and entered a global partnership with Shake Shack, underscoring continued vendor focus on multi-unit service businesses that can scale through repeatable smaller-site deployments.[3]Blink, “Blink Raises $17 Million and Partners With Shake Shack,” Blink, joinblink.com Smaller firms are also attractive because they often adopt quickly when a platform solves one immediate operating problem with limited setup. The growth profile suggests that SMEs will contribute a larger share of new revenue to the United States frontline worker technology market over time, even though large enterprises remain the biggest current spenders.

By Application: Communication Holds the Largest Base While Analytics Gains the Fastest Pace

Employee communication and engagement held 26.42% of revenue in 2025, making it the largest application category in the United States frontline worker technology market. That lead reflects a basic operating need that cuts across industries, because distributed workers need fast updates, clear instructions, and reliable two-way contact with supervisors and headquarters teams. Communication tools are also often the first workflow that employers can deploy quickly while showing visible value to both management and hourly employees. SHRM reported in 2025 that organizations using AI were 16 times more likely to enhance jobs than to displace them, which supports the role of communication platforms as an early layer in broader frontline digital change. The segment remains important because it creates the daily usage pattern that can later support analytics, learning, scheduling, and compliance functions.

Workforce analytics and performance management is projected to grow at 22.81% CAGR through 2031, making it the fastest-growing application segment. Employers are placing more weight on applications that connect worker activity to productivity, compliance, safety, and service outcomes in real time. Safety and compliance management is also gaining ground as organizations look for stronger audit trails, incident records, and workflow evidence in warehousing, industrial, and construction settings. Scheduling, coordination, learning, and knowledge enablement continue to benefit as automation reduces manual work in shift changes, training assignments, and competency tracking. Across the United States frontline worker technology industry, demand is moving from simple communication toward systems that can both guide work and measure results. That progression is raising the value of platforms that can collect operational signals and turn them into usable frontline decisions without adding unnecessary administrative burden.

By End-User Industry: Retail Maintains the Lead While Logistics Delivers the Fastest Growth

Retail and e-commerce held 28.14% of the United States frontline worker technology market share in 2025, which gave the segment the leading end-user position. Major retail chains adopted frontline communication, task management, and inventory visibility tools earlier than many other sectors, which helped establish this lead. Ongoing upgrades in the segment are now focused more on AI-enabled analytics, device intelligence, and clearer in-store execution across large store networks. That history gives retail a mature installed base, but it also means vendors must prove additional value rather than basic digitization alone. The segment remains important because retail environments offer both a large frontline workforce and frequent, measurable operating moments where digital tools can affect labor use, stock accuracy, and service quality.

Transportation and logistics is projected to expand at 21.93% CAGR from 2026 to 2031, making it the fastest-growing end-user group. Growth in this segment reflects persistent driver shortages, greater last-mile delivery complexity, and rising expectations for fast and accurate fulfillment. Honeywell launched Performance+ for Guided Work in January 2026 for sectors including transportation and logistics, and Zebra introduced AI-powered mobile solutions in 2026 aimed at improving route, tracking, and proof-of-delivery workflows. Manufacturing and healthcare remain major demand centers because connected worker tools, mobile communication, and compliance management address real coordination and documentation gaps in both sectors. Hospitality, construction, and government are earlier in adoption, which leaves open demand pockets for vendors that can offer simpler rollout, multilingual design, and stronger governance controls. This gives the end-user mix in the United States frontline worker technology market a combination of mature high-volume segments and newer areas where penetration can still rise meaningfully.

Geography Analysis

The United States defines the full geographic scope of the United States frontline worker technology market, but adoption patterns still differ widely across the country’s operating regions. The Northeast corridor, including Massachusetts, New York, New Jersey, and Pennsylvania, concentrates demand in healthcare and other complex multi-site environments where mobile workflow and communication tools support tightly managed daily operations. SHRM reported in 2025 that 90% of U.S. CHROs expected AI integration in frontline environments to intensify, a view that aligns with the region’s higher digital maturity and dense enterprise headquarters base.[4]Society for Human Resource Management, “Using Technology to Transform the Front-Line Workforce,” SHRM, shrm.org Illinois is also influencing procurement behavior across the broader Midwest because its workplace AI and biometric privacy framework has raised the standard for consent, oversight, and data handling in employer systems. That matters for manufacturers across the industrial corridor, where employers are using guided workflows and knowledge tools to preserve experienced worker know-how and standardize execution across sites.

The Sun Belt, covering Texas, Florida, Georgia, and the broader Southeast, is emerging as a faster-growth zone within the United States frontline worker technology market. High warehouse absorption, strong e-commerce fulfillment activity, and expanding field operations are creating dense demand for task management, route optimization, safety, and communication platforms. Construction demand is also rising with housing activity and infrastructure work, although frontline technology adoption in that sector still trails retail and logistics in maturity. The region’s large Spanish-speaking workforce is pushing vendors to improve language support, mobile usability, and training design for diverse site teams. These localization needs are becoming a real buying factor rather than a secondary product feature, especially for employers managing large service, field, and seasonal labor pools.

The West Coast and Mountain West, especially California, Washington, and Colorado, combine high adoption rates with some of the country’s most demanding policy conditions. UC Berkeley Labor Center documented in December 2025 that state activity around algorithmic management, electronic monitoring, and AI-based employment decisions was expanding, with California and Colorado standing out as major regulatory reference points. As a result, employers in these states are placing more weight on audit readiness, transparency, and human oversight when they select vendors for scheduling, monitoring, and task assignment systems. The Pacific Northwest also serves as a visible test ground for new frontline tools because large technology-led employers can influence product roadmaps that later spread across the national market.

Competitive Landscape

The United States frontline worker technology market remains moderately fragmented, and no single vendor leads across every application, deployment model, and end-user setting. Large software vendors are moving toward broader platform suites that combine communication, workflow, analytics, and AI guidance in one environment. ServiceNow reinforced this direction in February 2026 when it launched Autonomous Workforce after adding Moveworks, giving enterprise buyers a more automated path for natural language requests, enterprise search, and governed workflow execution.[5]ServiceNow, “ServiceNow Launches Autonomous Workforce That Thinks and Acts, Adds Moveworks to the ServiceNow AI Platform,” ServiceNow Investor Relations, investor.servicenow.com The company said the platform could handle more than 90% of employee IT requests and resolve cases 99% faster than human agents, which raised the competitive standard for AI-led support and guidance. This move matters because buyers now compare vendors on how much work they can complete inside existing systems, not only on the number of features they offer.

Hardware-centered companies are also broadening their role as the United States frontline worker technology market shifts from devices alone toward connected software ecosystems. Zebra launched Zebra Nucleus, Workcloud Business Intelligence, and Workcloud Integration and Orchestration in June 2026 to link device management, analytics, and enterprise system connectivity in one architecture. That strategy turns installed hardware fleets into a base for recurring software revenue and deeper operational integration. Honeywell followed a similar path in 2026 through Performance+ for Guided Work and the commercial launch of Experion Operations Assistant, tying worker execution, real-time visibility, and predictive safety functions more closely together. As these product lines expand, the boundary between frontline infrastructure and frontline intelligence continues to narrow.

Open demand remains in hospitality, construction, government, and other mid-market verticals where penetration still trails retail, logistics, and manufacturing. Relevant specialist competition in these spaces includes vendors such as Tulip Interfaces and Samsara, which are closer to frontline operating workflows than consulting-led participants that do not sell core product platforms. Vendors that build audit trails, bias controls, and data minimization into their systems are likely to win more enterprise accounts as compliance review becomes a stricter purchase filter. Competitive advantage in the United States frontline worker technology market is therefore shifting toward integration depth, governance readiness

United States Frontline Worker Technology Industry Leaders

Augmentir, Inc.

IBM Corporation

Blackline Safety Corp.

Dozuki, Inc.

Honeywell International Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Zebra Technologies launched Zebra Nucleus, Workcloud Business Intelligence, and Workcloud Integration and Orchestration at its annual ZONE conference in Nashville, June 1-4, 2026, consolidating device fleet management, AI-powered operational analytics, and enterprise system integration into a unified software architecture for frontline environments.

- June 2026: Salesforce announced general availability of Agentforce Contact Center Workforce Engagement Management at Customer Contact Week, combining workforce management, quality management, and visibility of both human and AI agent activity in a single integrated platform for frontline contact center operations.

- May 2026: ServiceNow launched Employee Slate within the EmployeeWorks platform on May 5, 2026, an AI-powered employee experience interface enabling frontline and desk-based workers to interact with enterprise systems through natural language, incorporating enterprise search, unified inbox, and personalized workflow capabilities.

- March 2026: Honeywell commercially launched Experion Operations Assistant on March 19, 2026, an AI-powered industrial solution that generated alarm predictions 5-10 minutes before incidents during pilot deployments with Chevron and TotalEnergies, extending predictive safety capabilities to industrial operators market-wide.

United States Frontline Worker Technology Market Report Scope

The United States frontline worker technology market comprises software platforms, connected applications, and associated services designed to digitally enable deskless and field-based employees across industries such as retail, industrial manufacturing, healthcare, transportation and logistics, hospitality, construction, and the public sector. These solutions improve frontline productivity, communication, task execution, workforce coordination, learning, operational visibility, safety, and compliance by integrating mobile devices, wearable technologies, artificial intelligence (AI), Internet of Things (IoT) sensors, cloud platforms, and enterprise business systems. The market includes revenue from software subscriptions and licenses, as well as professional and managed services supporting deployment, integration, customization, training, and ongoing support.

The United States Frontline Worker Technology Market Report is segmented by Component (Software, and Services), Deployment Mode (Cloud-Based, Hybrid, and On-Premises), Organization Size (Large Enterprises, and Small and Medium Enterprises), Application (Employee Communication and Engagement, Workforce Execution and Task Management, Workforce Scheduling and Coordination, Learning and Knowledge Enablement, Workforce Analytics and Performance Management, Safety and Compliance Management, and Other Applications), and End-user Industry (Retail and E-Commerce, Industrial Manufacturing, Healthcare and Life Sciences, Transportation and Logistics, Hospitality, Construction, Government and Public Administration, and Other Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud-Based |

| Hybrid |

| On-Premises |

| Large Enterprises |

| Small and Medium Enterprises |

| Employee Communication and Engagement |

| Workforce Execution and Task Management |

| Workforce Scheduling and Coordination |

| Learning and Knowledge Enablement |

| Workforce Analytics and Performance Management |

| Safety and Compliance Management |

| Other Applications |

| Retail and E-Commerce |

| Industrial Manufacturing |

| Healthcare and Life Sciences |

| Transportation and Logistics |

| Hospitality |

| Construction |

| Government and Public Administration |

| Other Industries |

| By Component | Software |

| Services | |

| By Deployment | Cloud-Based |

| Hybrid | |

| On-Premises | |

| By Organization Size | Large Enterprises |

| Small and Medium Enterprises | |

| By Application | Employee Communication and Engagement |

| Workforce Execution and Task Management | |

| Workforce Scheduling and Coordination | |

| Learning and Knowledge Enablement | |

| Workforce Analytics and Performance Management | |

| Safety and Compliance Management | |

| Other Applications | |

| By End-User Industry | Retail and E-Commerce |

| Industrial Manufacturing | |

| Healthcare and Life Sciences | |

| Transportation and Logistics | |

| Hospitality | |

| Construction | |

| Government and Public Administration | |

| Other Industries |

Key Questions Answered in the Report

What is the projected size of the United States frontline worker technology market by 2031?

The United States frontline worker technology market is projected to reach USD 11.42 billion by 2031, rising from USD 4.73 billion in 2026 at a CAGR of 19.28% over 2026-2031.

Which segment currently generates the most revenue in frontline worker technology in the United States?

Software generated the largest revenue share in 2025 at 83.47%, reflecting strong demand for workflow, communication, analytics, and safety management platforms.

Which deployment model is growing fastest for frontline worker technology platforms?

Cloud-based deployment remained the leading model with 82.63% revenue share in 2025 and is projected to grow at 19.84% CAGR through 2031 because multi-site scalability is a major buying priority.

Why are employers investing more in analytics and performance management for frontline teams?

Employers are placing more weight on tools that connect worker activity to productivity, compliance, safety, and service results, which is why workforce analytics and performance management is projected to grow at 22.81% CAGR.

Which end-user group offers the strongest growth opportunity through 2031?

Transportation and logistics is projected to expand at 21.93% CAGR through 2031 due to driver shortages, last-mile complexity, and the need for faster, more accurate fulfillment.

What is the main barrier to wider frontline technology rollout in the United States?

The biggest barriers are integration complexity with legacy systems and worker adoption challenges, because many employers still need support with system connectivity, change management, and training.

Page last updated on: