Effervescent Drink Tablets Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 8.72 Billion |

| Market Size (2031) | USD 12.59 Billion |

| Growth Rate (2026 - 2031) | 7.62% CAGR |

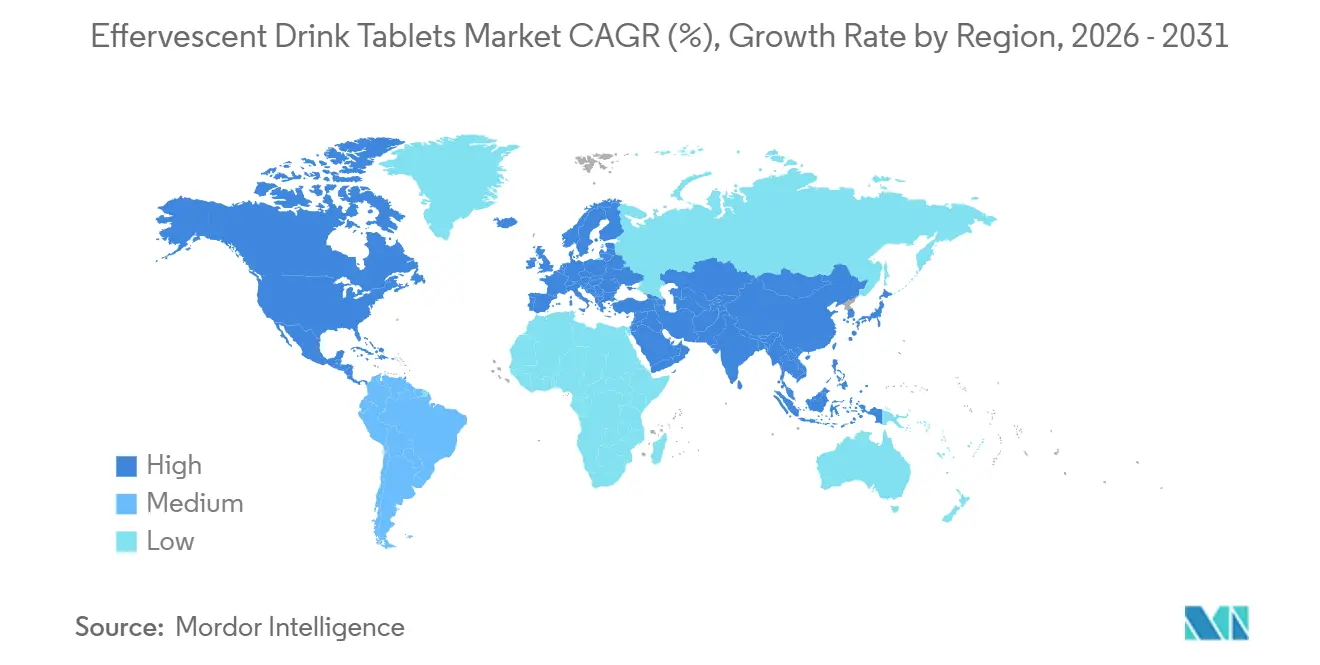

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Europe |

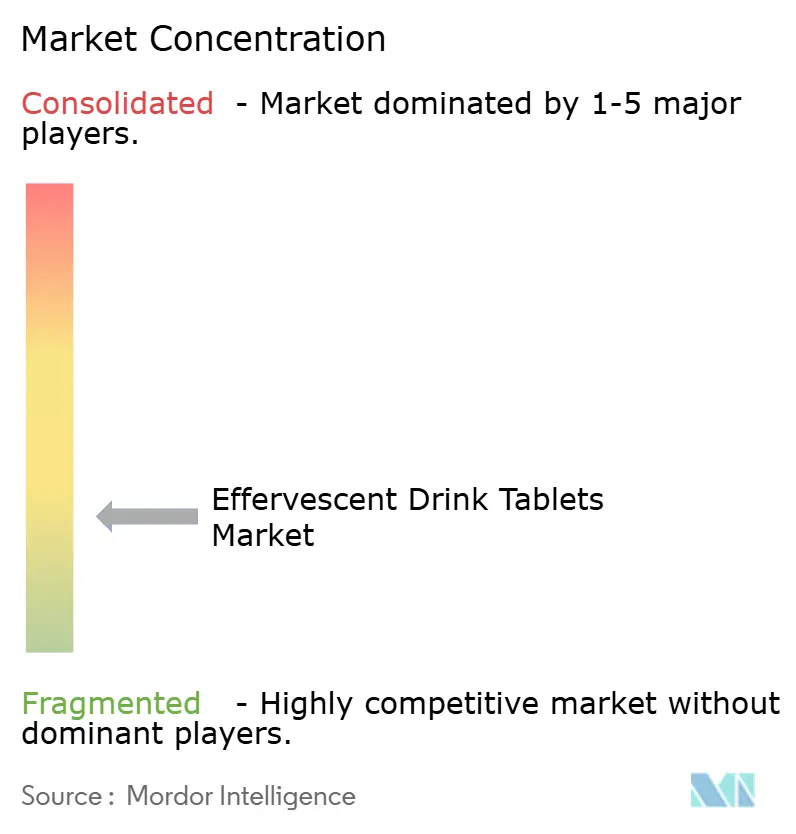

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Effervescent Drink Tablets Market Analysis by Mordor Intelligence

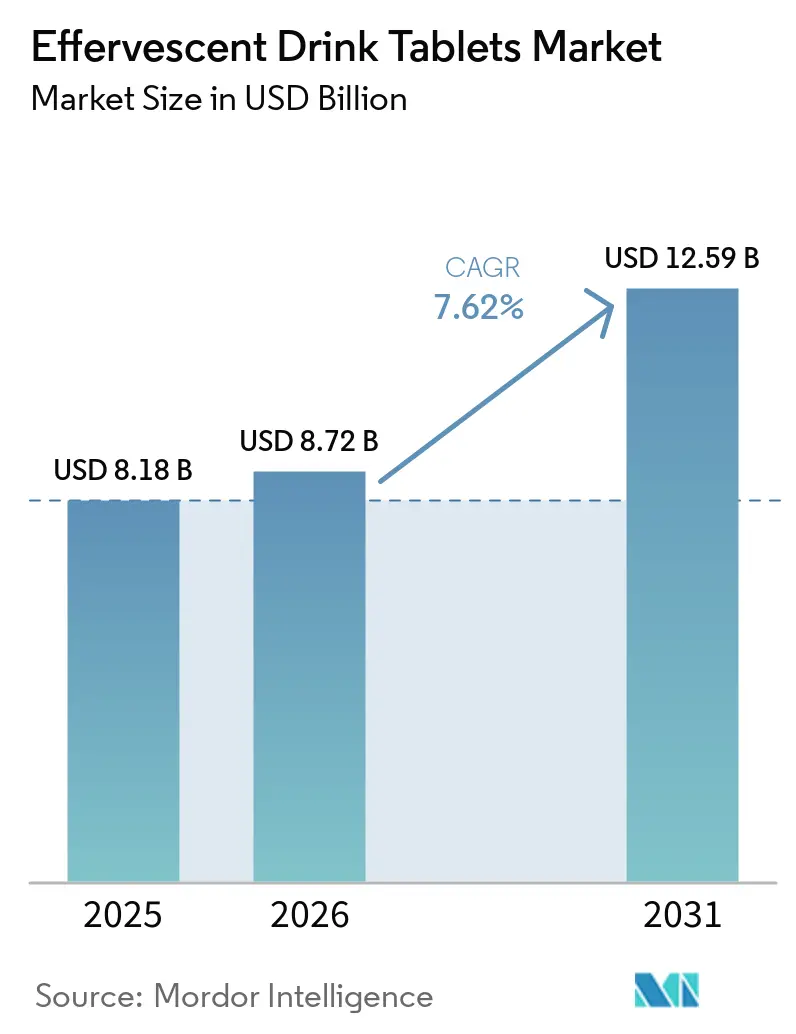

The effervescent drink tablets market size is projected to be USD 8.18 billion in 2025, USD 8.72 billion in 2026, and reach USD 12.59 billion by 2031, growing at a CAGR of 7.6% from 2026 to 2031. The effervescent drink tablets market is moving beyond its traditional vitamin C and antacid base into sports recovery, daily immunity, beauty nutrition, and on-the-go hydration, which is widening its consumer base. Demand is being supported by stronger preventive health habits, preference for convenient dosage forms, and rising interest in cleaner ingredient profiles. Europe remains the largest regional base because consumer familiarity is high and distribution is broad across pharmacies, supermarkets, and health-focused retail. Asia-Pacific is setting the fastest pace as younger consumers in India and Southeast Asia adopt portable wellness products through modern retail and digital channels. The effervescent drink tablets market is also seeing faster product refresh cycles as brands compete through multi-benefit formulations, cleaner labels, and more targeted positioning, while regulatory scrutiny, moisture sensitivity, and private-label pressure continue to shape strategy.

Key Report Takeaways

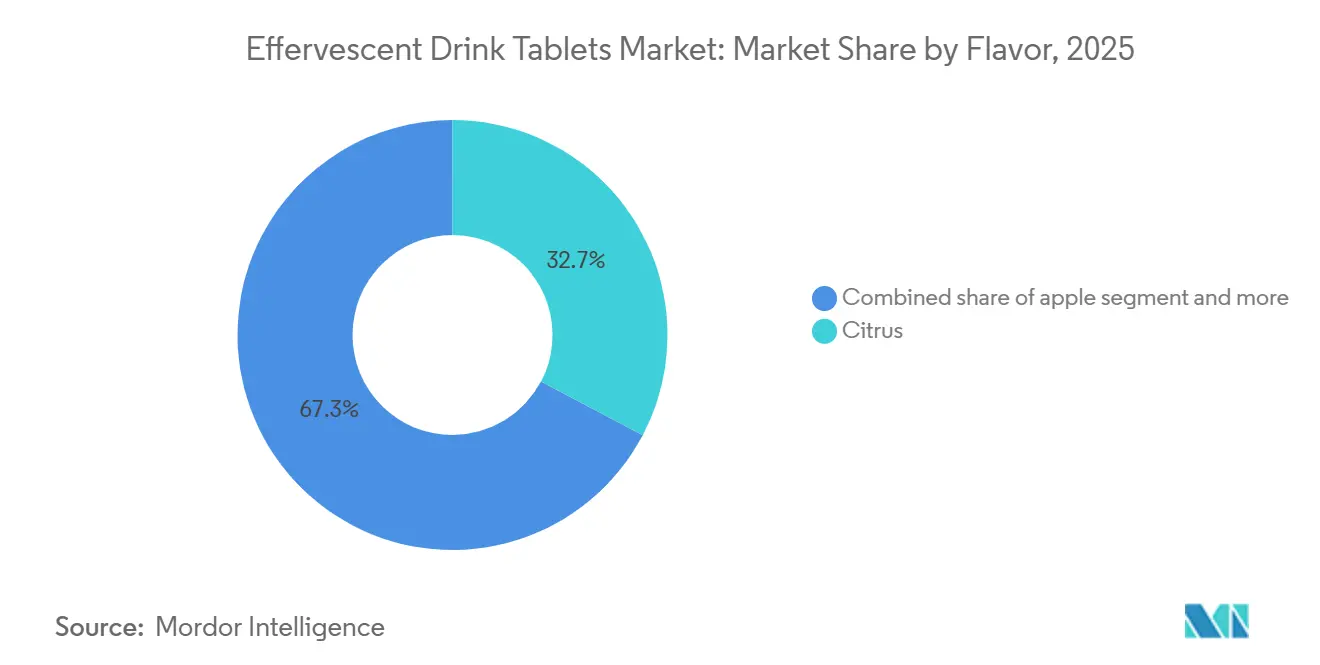

- By flavor, Citrus held 32.7% of the effervescent drink tablets market share in 2025, while Apple is forecast to expand at an 8.5% CAGR through 2031.

- By category, Conventional accounted for 59.6% of the effervescent drink tablets market size in 2025, while Zero Sugar recorded the highest projected CAGR at 9.1% through 2031.

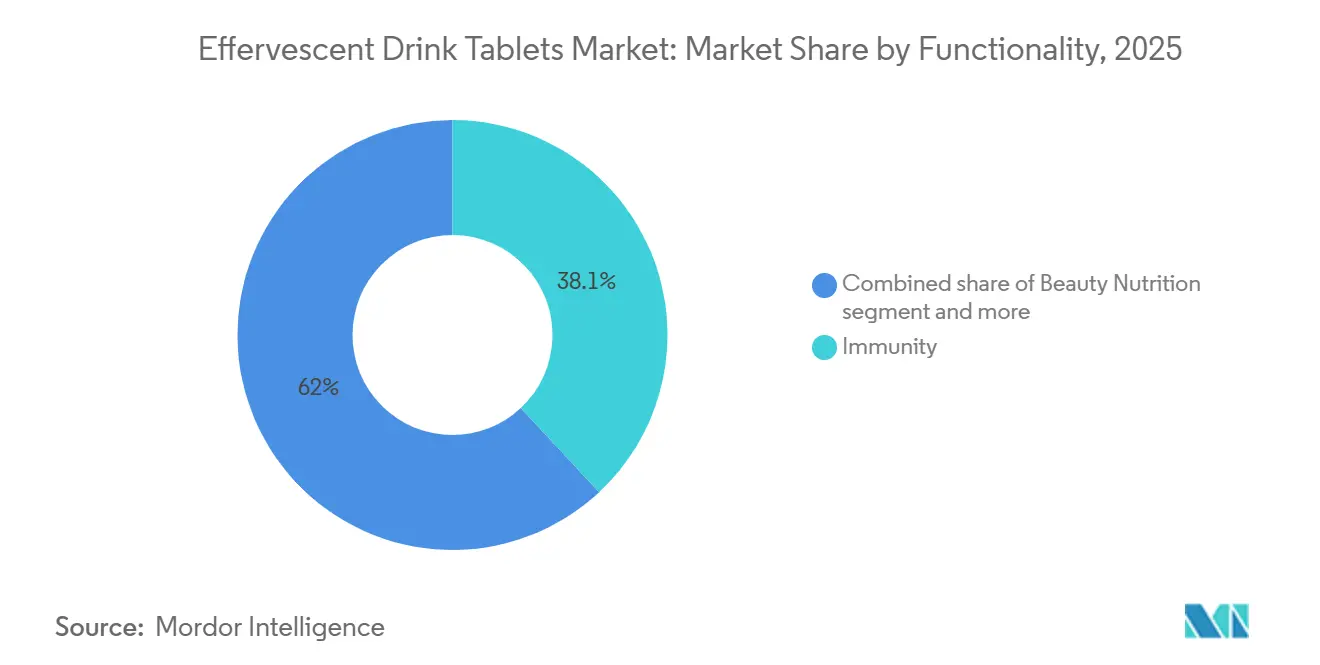

- By functionality, Immunity captured 38.1% of the effervescent drink tablets market share in 2025, while Beauty Nutrition is advancing at a 9.5% CAGR through 2031.

- By distribution channel, Supermarkets and Hypermarkets commanded 44.1% share of the effervescent drink tablets market size in 2025, while Online Retail Stores are forecast to grow at a 9.2% CAGR through 2031.

- By geography, Europe held 36.4% of the effervescent drink tablets market share in 2025, while Asia-Pacific is projected to grow at a 9.4% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Effervescent Drink Tablets Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Convenient Hydration and Nutritional Delivery | +2.0% | Global | Short term (≤ 2 years) |

| Aging Consumer Adoption of Easy-To-Consume Supplement Formats | +1.5% | Europe, North America, Japan | Medium term (2–4 years) |

| Expansion of Sports Nutrition and Recovery Use Cases | +1.2% | The Asia-Pacific and North America | Medium term (2–4 years) |

| Growth in Zero Sugar and Clean-Label Effervescent Formulations | +1.0% | North America and Europe | Medium term (2–4 years) |

| Under-Served Travel, Outdoor, and On-The-Go Rehydration Use Cases | +0.6% | Global, with early traction in the Asia-Pacific, the Middle East, and Africa | Short term (≤ 2 years) |

| Rising Premiumization Through Functional Blends and Multi-Benefit Tablets | +0.7% | Europe, North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising demand for convenient hydration and nutritional delivery

The rising demand for convenient hydration and nutritional delivery is a key factor driving growth in the global effervescent drink tablets market, as consumers increasingly seek portable, easy-to-consume solutions that support hydration, energy, immunity, and overall wellness. Effervescent tablets offer rapid dissolution, improved nutrient absorption, precise dosing, and greater convenience compared to traditional tablets and ready-to-drink beverages, making them particularly attractive for active lifestyles, travel, and workplace consumption. Government and public health agencies worldwide continue to promote adequate hydration and preventive nutrition, while growing participation in fitness and outdoor activities further supports demand for electrolyte and vitamin-based formulations. Industry analyses indicate that electrolyte tablets and powders remain among the most widely adopted hydration supplement formats, benefiting from increasing use in sports nutrition and daily wellness routines. Product innovation is reinforcing this trend; in April 2025, Phizz launched Phizz Daily Energy Hydration Tablets, combining electrolytes, vitamins, and natural caffeine for enhanced hydration and energy support. In 2026, manufacturers expanded portfolios with advanced electrolyte, collagen, magnesium, and multivitamin effervescent tablets targeting hydration and functional nutrition needs, reflecting growing consumer preference for multifunctional wellness products.

Aging consumer adoption of easy-to-consume supplement formats

Demographic shifts are quietly steering the demand in this market. The World Health Organization, in an October 2025 announcement, highlighted a significant milestone: by 2030, a mere four years away, 1 in 6 individuals globally will be aged 60 or older, totaling approximately 1.4 billion. Fast forward to 2050, and that number is set to double, reaching 2.1 billion[1]Source: World Health Organization, “Ageing and Health,” World Health Organization, who.int. Delving deeper, a 25-year study from the US National Health and Nutrition Examination Survey, published in JAMA, unveiled a notable trend: supplement usage among adults aged 65 and older surged from 62% in 1999 to 78% in 2023, outpacing every other age demographic. This trend has a subtle yet significant implication for effervescent tablets: a 2025 review in RSC Pharmaceutics highlighted that up to 15% of older adults in community settings face dysphagia, or swallowing difficulties[2]Source: Royal Society of Chemistry, “Pharmaceutics Review on Dysphagia and Dosage Forms,” RSC Pharmaceutics, rsc.org. This makes effervescent drinks, which dissolve easily, a clinically preferred choice over traditional tablets. Brands that strategically market effervescent products as a solution for healthy aging, bolstered by clinical evidence on their bioavailability and ease of swallowing, are capitalizing on a demand that conventional supplement formats struggle to meet.

Expansion of sports nutrition and recovery use cases

The sports nutrition segment is increasingly driving demand for effervescent drink tablets, particularly in Asia-Pacific and other high-growth fitness markets. Electrolyte effervescent tablets are gaining preference over ready-to-drink isotonic beverages because they offer portability, customizable concentration, longer shelf life, and reduced reliance on preservatives. Athletes and active consumers can tailor hydration levels by dissolving tablets in different volumes of water, enhancing convenience and value. Reflecting this trend, Nuun Hydration reformulated its Nuun Energy tablets in March 2026, incorporating 80 mg of plant-based caffeine from green tea extract, optimized electrolytes, and B vitamins to deliver hydration, energy, and recovery benefits in a single product. This shift toward multifunctional formulations supports premium pricing and broader consumer appeal. Moreover, sports nutrition is increasingly serving as an entry point, with users extending tablet consumption beyond workouts into daily hydration, travel, and wellness routines, thereby increasing long-term market penetration.

Growth in zero sugar and clean-label effervescent formulations

As consumers increasingly scrutinize ingredient lists, conventional effervescent products, often reliant on sucrose, saccharin, or synthetic colorants, face a significant barrier to trial. Meanwhile, the zero-sugar effervescent segment, currently growing at a 9.11% CAGR, is on track to close the 40-point gap that separates it from Conventional's dominant 59.62% market share during the forecast period. Amerilab Technologies, Inc. boasts several US patents, including Patent 10,912,733 (Rapid Disintegrating Effervescent Tablets) and Patent 11,826,459 (Effervescent Tablets with Natural Lubricant). These patents cover clean-label formulations that utilize gum acacia and crystalline sugar binders, allowing for the elimination of synthetic additives while ensuring rapid dissolution. Adding to the urgency, the EU's regulatory landscape is shifting. In June 2026, the European Commission announced a call for evidence on Maximum Permitted Levels (MPLs) for vitamins and minerals in supplements. With consultation documentation anticipated in late Q3 2026, experts in compliance have labeled this move as potentially the most pivotal structural change since the 2006 Nutrition and Health Claims Regulation. Brands that proactively invest in clean-label reformulation today position themselves advantageously, creating a compliance buffer that could set them apart if the EU opts for conservative MPL thresholds.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Moisture Sensitivity and Packaging Complexity | -0.4% | Global | Short term (≤ 2 years) |

| Sodium Load Concerns in Frequent Use Products | -0.3% | Europe and North America | Medium term (2–4 years) |

| Manufacturing Variability in Acid-Base Stability and Dosage Uniformity | -0.3% | Global, intensified in developing markets | Long term (≥ 4 years) |

| Limited Reimbursement and Cost Pressure Versus Conventional Dosage Forms | -0.2% | Europe and North America | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

High moisture sensitivity and packaging complexity

Effervescent tablets are naturally prone to moisture absorption. When the sodium bicarbonate-citric acid system, responsible for carbonation, comes into contact with ambient humidity, it reacts prematurely. This not only diminishes the sensory experience but also the nutritional quality of the tablets. As a result, these tablets require primary packaging that maintains humidity levels below 25%. This requirement significantly raises material and logistics costs compared to standard tablet formats. This is especially pronounced for brands operating in tropical regions of Southeast Asia and Sub-Saharan Africa, where humidity levels often soar above 80%. In July 2025, Aptar CSP Technologies introduced a groundbreaking dual-active material science technology[3]Source: Aptar CSP Technologies, “Dual-Active Moisture and Oxygen Control Technology,” Aptar CSP Technologies, aptar.com. This innovation adeptly manages both moisture and oxygen levels in packaging, offering effervescent manufacturers an extended shelf life without the need for excessive packaging. However, the adoption of premium moisture-barrier tubes and desiccant closures poses a challenge. These advanced solutions, while beneficial, strain profitability margins. This is particularly true for private-label and contract-manufactured SKUs that cater to budget-conscious consumers. As a result, smaller players find it challenging to scale without facing margin pressures.

Sodium load concerns in frequent use products

Sodium, a natural by-product of the acid-bicarbonate effervescence process, has seen inconsistent regulation in supplement product disclosures. A 2023 cross-sectional study in BMJ Open analyzed 39 effervescent dietary supplements from Germany. The study revealed an average sodium content of 283.9 mg per tablet, accounting for 14% of the World Health Organization's recommended daily sodium limit. Alarmingly, only 12.8% of these products indicated sodium content on their packaging. For consumers with conditions like hypertension, heart failure, or renal insufficiency, daily use of these effervescent supplements could lead to sodium intake surpassing clinically significant levels. This poses a reputational risk for the entire category, especially as media spotlight "hidden sodium" in functional beverages, fostering consumer skepticism and reducing trial rates. The European Medicines Agency, alongside national health entities like the NHS Specialist Pharmacy Service, has provided guidance on sodium in soluble formulations, exerting informal compliance pressure even within the food supplement arena. Brands that take the initiative to reformulate, such as incorporating potassium bicarbonate as a partial substitute, stand to benefit. As front-of-pack sodium labeling transitions from rarity to norm, these brands could enjoy a notable trust premium.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Flavor: Citrus Dominance Intact as Apple Flavours Gain Momentum

With an 8.46% CAGR, the apple flavor segment has emerged as the market's fastest-growing choice. This surge has seen it eclipse more established profiles, particularly as consumers in the US and Europe increasingly associate Apple with a clean, natural sweetness, distancing it from the artificial tartness often linked to citrus. While citrus commands the largest market share at 32.71% in 2025, its dominance is anchored in a historical association with Vitamin C effervescence. This connection, deeply embedded in pharmacy buyer repertoires, spans from Bayer's Redoxon to Vitabiotics' Feroglobin Fizz. Meanwhile, in the APAC markets, the berry and mango flavor segments are gaining momentum. Here, tropical fruit profiles resonate more with younger consumers, driving a higher purchase intent, even if they lag in global volume.

The "Other Flavors" sub-segment is evolving into a diverse innovation hub. It encompasses everything from unflavored electrolyte tablets aimed at clinical hydration to proprietary botanical blends and caffeinated flavor systems. Another trend to monitor: as brands increasingly stack functional benefits, like immunity, energy, and beauty, into single tablets, the flavor preference hierarchy is evolving. This shift favors profiles that can credibly signal multiple benefits, such as elderberry-citrus for immunity, over a singular focus on pure citrus. Brands that prioritize flavor portfolios solely for volume, rather than these nuanced functional signals, may find themselves facing commoditization as the market matures.

By Category: Conventional Share Under Pressure from Zero Sugar Uptake

Conventional effervescent tablets, holding a 59.62% share in 2025, continue to lead the market, buoyed by a loyal consumer base that values familiar tastes over minimalist ingredients. Meanwhile, the Zero Sugar segment is rapidly gaining ground, boasting a 9.11% CAGR. This growth trajectory not only mirrors the aspirational values of today's consumers. favoring clean labels and low calories, but is also bolstered by innovations in natural sweeteners. Notably, blends of erythritol and stevia are now achieving the same mouthfeel and sweetness as sucrose, but without the glycaemic repercussions. The primary threat to Conventional tablets isn't from current users switching allegiance, but from the brand's struggle to attract newcomers: first-time buyers are increasingly gravitating towards zero sugar options as their go-to choice.

In a notable industry shift, Reckitt Benckiser reformulated its Airborne effervescent tablets in September 2024, spotlighting a rich blend of micronutrients, Vitamin C, D, Zinc, A, E, Manganese, and Selenium, each at over 20% of daily values, all while steering clear of added sugars. This move underscores a broader trend: even traditional Conventional products are pivoting towards cleaner nutritional profiles. Manufacturers who overlook the zero-sugar trend and delay line extensions until 2027 may find themselves losing valuable shelf space. Newer entrants are not just dabbling in clean labels; they're embedding it as a core principle across their entire product portfolios.

By Functionality: Immunity Anchors Volume as Beauty Nutrition Reaches Inflection

Immunity functionality accounted for 38.05% of the global effervescent drink tablets market in 2025, reflecting the normalization of immune-support supplementation as part of everyday wellness routines rather than a seasonal response to illness. Consumers increasingly incorporate vitamin C, zinc, multivitamins, and antioxidant-based effervescent products into their daily health regimens. The segment also benefits from growing preventive healthcare awareness and convenient nutrient delivery. Meanwhile, Energy and Hydration products continue to generate substantial demand through their applications in sports nutrition, active lifestyles, and workplace productivity.

Beauty Nutrition is projected to grow at a 9.51% CAGR from 2026 to 2031, supported by the accelerating “beauty from within” trend across Western Europe and East Asia. Effervescent formulations containing collagen, biotin, and hyaluronic acid appeal to consumers seeking skin, hair, and nail health benefits in a convenient format. Beyond strong consumer demand, the segment benefits from premium positioning, with beauty-focused effervescent tablets typically commanding 20–30% higher retail prices than conventional vitamin or electrolyte products, enhancing revenue growth potential.

By Distribution Channel: Physical Retail Commands Share as Online Accelerates

In 2025, Supermarkets and Hypermarkets commanded a 44.13% share of the distribution landscape. This trend underscores the impulse buying behavior adjacent to pharmacies, where consumers often grab effervescent tablets at checkout, alongside other health and wellness items during their grocery runs. Convenience Stores, along with Pharmacies and Drug Stores, account for the remaining brick-and-mortar distribution. Notably, pharmacies uphold a premium quality image, a factor especially crucial for older adults who prioritize assurance regarding supplement quality and dosage.

Online Retail Stores are leading the charge with a robust 9.18% CAGR, outpacing all other channels. This surge aligns with the overarching trend in nutritional supplement purchases: by 2025, e-commerce platforms claimed a significant slice of the total US supplement market value, outpacing traditional mass market growth. The strategic insight here is that online retail isn't merely siphoning off sales from pharmacies. Instead, it's carving out a unique niche: subscription-based daily wellness purchases. These not only foster a distinct buying occasion but also yield annual revenues per customer that surpass those from one-off pharmacy transactions. A testament to this shift is iHerb, boasting a record USD 2.9 billion in sales for FY2025, with its subscription enrollments skyrocketing by 370% year-over-year, highlighting the trend's significance for brands strategizing in the effervescent tablet e-commerce realm.

Geography Analysis

Europe's 36.40% share of the global effervescent drink tablets market in 2025 highlights structural advantages that competitors in other regions are still developing. These include strong pharmacist recommendation networks, consumer familiarity with effervescent formats (e.g., Berocca and Redoxon), and a regulatory framework requiring formulation disclosures, which enhance product credibility. The European Commission's harmonization of Maximum Permitted Levels for vitamins and minerals in food supplements, with a formal evidence call expected in Q3 2026, could reshape competition as compliance frameworks tighten ingredient thresholds under Directive 2002/46/EC, amended by Commission Regulation (EU) 2025/352. Key markets like Germany, the UK, and France sustain premium pricing in pharmacy channels, while Poland, Sweden, and the Netherlands are emerging as faster-growth sub-markets due to modern trade expansion. Innovation investment remains strong, with Germany and the UK serving as launch hubs for global brands testing new functional stack formulations.

Asia-Pacific is growing at a 9.38% CAGR, the fastest globally, driven by rising sports participation in India and China, rapid e-commerce growth in Southeast Asia, and a youth demographic discovering effervescent formats via social commerce. India offers a distinct opportunity, highlighted by Bayer Consumer Health's June 2026 launch of Alka-Seltzer as the country's first probiotic-supported antacid under the AYUSH category, targeting 100 million households within four years. Domestic brands like Fast&Up and Wellbeing Nutrition are scaling rapidly. Wellbeing Nutrition projects revenue growth from INR 110 crore (USD 13.2 million) in FY2024 to INR 400 crore (USD 48 million) in FY2026, with effervescent formats central to its identity. Australia and South Korea add a premium-market dimension, with consumers willing to pay more for clinically validated, clean-label formulations.

North America, led by the U.S., holds a strong second-place position. Consumers favor sports electrolyte formats (e.g., Nuun) and immunity tablets (e.g., Airborne). South America, particularly Brazil, Argentina, and Colombia, is an emerging market where rising middle-class incomes are driving effervescent tablet purchases, though distribution gaps limit rural penetration. The Middle East and Africa, with opportunities in the UAE, Saudi Arabia, and South Africa, show niche but premium demand driven by health-conscious urban consumers and high tourist traffic in travel retail. In both South America and MEA, online retail and quick-commerce platforms are expected to accelerate adoption, bypassing slower pharmacy distribution expansion.

Competitive Landscape

The global effervescent drink tablets market remains moderately fragmented, characterized by the presence of multinational consumer healthcare companies, pharmaceutical firms, and specialized wellness brands competing across diverse functional categories. Major players such as Bayer AG, Haleon plc, and Reckitt Benckiser Group plc leverage extensive distribution networks, strong pharmacy relationships, and well-established brand recognition to maintain significant market presence across North America and Europe. Simultaneously, emerging and category-focused brands including Nuun Hydration, Vitabiotics Ltd., Fast&Up, and Wellbeing Nutrition are gaining traction through innovation-led portfolios, sports nutrition offerings, and direct-to-consumer sales channels. This balance between established corporations and agile specialist brands sustains competition across premium and mass-market segments while preventing any single participant from exerting substantial control over pricing, distribution, or innovation trends.

Competition within the market is intensifying as manufacturers shift beyond basic vitamin and hydration products toward multifunctional formulations that combine hydration, energy, immunity, recovery, beauty, and wellness benefits in a single tablet. Product differentiation increasingly depends on clean-label ingredients, sugar-free formulations, plant-based actives, and scientifically backed health claims. Reflecting this trend, Nuun Hydration reformulated its Nuun Energy product in March 2026, incorporating plant-based caffeine sourced from green tea extract, optimized electrolytes, and B vitamins to deliver hydration and energy support simultaneously. Such developments illustrate how brands are enhancing perceived value and targeting specific consumer needs rather than competing solely on price. In parallel, formulation specialists such as Amerilab Technologies have strengthened their competitive position through proprietary technologies and patents related to rapid-disintegrating, cleaner-label effervescent systems. These capabilities are particularly valuable as demand rises for natural ingredients, zero-sugar formulations, and premium wellness products where taste, efficacy, and label transparency must align.

Packaging innovation is also emerging as a critical competitive differentiator because effervescent tablets are highly sensitive to moisture and oxygen exposure. In 2025, Aptar CSP Technologies introduced advanced dual-active moisture and oxygen control solutions designed to improve product stability, shelf life, and performance. While such technologies enhance quality assurance and support premium positioning, they also increase packaging costs, creating challenges for smaller manufacturers. Looking ahead, rising regulatory requirements, growing private-label competition, and escalating research, development, and packaging investments are expected to intensify competitive pressures. As a result, strategic partnerships, acquisitions, product repositioning, and market consolidation are likely to become increasingly common as companies seek scale, innovation capabilities, and stronger market positioning.

Effervescent Drink Tablets Industry Leaders

Bayer AG

Haleon plc

Reckitt Benckiser Group plc

Vitabiotics Ltd.

Abbott Laboratories

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Bayer Consumer Health launched Alka-Seltzer in India as an effervescent powder sachet, the country's first antacid in the AYUSH category with probiotic support. The product targets the OTC digestive health category across e-pharmacies, quick-commerce, and traditional outlets, with Bayer aiming to reach 100 million households within four years.

- March 2026: Nuun Hydration reformulated and relaunched Nuun Energy Caffeine + B Vitamins as a streamlined effervescent tablet combining 80 mg plant-based caffeine from green tea extract, 5 optimized electrolytes, and B vitamins (B6 and B12) in a single tube of 10 tablets. The reformulation discontinues two legacy caffeine-adjacent products (Nuun Daily Energy and Nuun Sport + Caffeine) and consolidates the energy hydration offer into one clean-label, vegan, and gluten-free format.

- December 2025: Abbott Laboratories launched two new Ensure Max Protein shakes (Ensure Max Protein 42g and Ensure Max Protein 2 in 1 Muscle Support), exclusively available at Walmart in the United States, marking a push into the fast-growing functional nutrition for muscle health segment and underscoring Abbott's intent to expand its convenient nutritional delivery formats portfolio.

Global Effervescent Drink Tablets Market Report Scope

Effervescent drink tablets are tightly compressed blocks of active ingredients designed to dissolve rapidly upon contact with water, creating a fizzy, carbonated beverage. The global effervescent drink tablets market is segmented by flavor, category, functionality, distribution channel, and geography. By flavor, the market is segmented into citrus, apple, berries, mango, and others. By category, the market is segmented into conventional and zero-sugar. By functionality, the market is segmented into energy and hydration, immunity, weight management, beauty nutrition, and other functionalities. By distribution channel, the market is segmented into supermarkets and hypermarkets, convenience stores, pharmacies/drug stores, online retail stores, and other distribution channels. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. The Market Forecasts are Provided in Terms of Value (USD).

| Citrus |

| Apple |

| Berries |

| Mango |

| Other Flavors |

| Conventional |

| Zero Sugar |

| Energy and Hydration |

| Immunity |

| Weight Management |

| Beauty Nutrition |

| Other Functionalities |

| Supermarkets and Hypermarkets |

| Convenience Stores |

| Pharmacies/Drug Stores |

| Online Retail Stores |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Sweden | |

| Belgium | |

| Poland | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Thailand | |

| Singapore | |

| Indonesia | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Peru | |

| Chile | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Saudi Arabia | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| Flavor | Citrus | |

| Apple | ||

| Berries | ||

| Mango | ||

| Other Flavors | ||

| Category | Conventional | |

| Zero Sugar | ||

| Functionality | Energy and Hydration | |

| Immunity | ||

| Weight Management | ||

| Beauty Nutrition | ||

| Other Functionalities | ||

| Distribution Channel | Supermarkets and Hypermarkets | |

| Convenience Stores | ||

| Pharmacies/Drug Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Sweden | ||

| Belgium | ||

| Poland | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Thailand | ||

| Singapore | ||

| Indonesia | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Peru | ||

| Chile | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Saudi Arabia | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the effervescent drink tablets space?

The effervescent drink tablets market size stands at USD 8.72 billion in 2026 and is forecast to reach USD 12.59 billion by 2031 at a 7.62% CAGR.

Which region leads global demand for effervescent drink tablets?

Europe led with 36.4% of global value in 2025, supported by strong consumer familiarity and broad retail distribution.

Which region is growing the fastest through 2031?

Asia-Pacific is the fastest-growing region, with the draft projecting a 9.38% CAGR through 2031.

Which product category is expanding the fastest?

Zero Sugar is the fastest-growing category, with a projected 9.11% CAGR through 2031, even though Conventional remained the largest in 2025.

Page last updated on: