Electrolyte Drinks Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

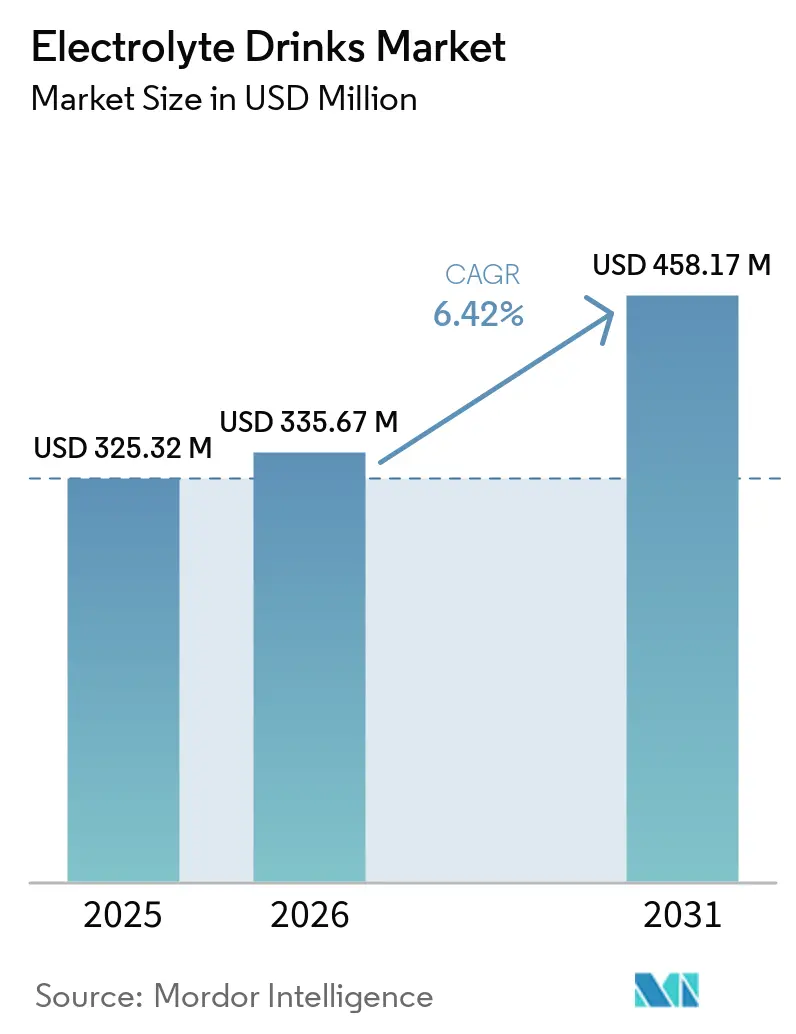

| Market Size (2026) | USD 335.67 Million |

| Market Size (2031) | USD 458.17 Million |

| Growth Rate (2026 - 2031) | 6.42% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Electrolyte Drinks Market Analysis by Mordor Intelligence

The electrolyte drinks market size is projected to be USD 325.32 million in 2025, USD 335.67 million in 2026, and reach USD 458.17 million by 2031, growing at a CAGR of 6.42% from 2026 to 2031. The electrolyte drinks market is moving beyond workout recovery, and it is now tied more closely to daily hydration, routine wellness, and broader functional beverage use. The World Health Organization reported that physical inactivity affected 31% of adults globally, equal to 1.8 billion people, which keeps public institutions and consumer brands focused on preventive health behavior that can widen the buyer base for the electrolyte drinks market. WHO also set a target of a 15% relative reduction in inactivity by 2030, and that policy direction supports more investment in fitness participation and wellness programs that can sustain category demand over time. The competitive setting in the electrolyte drinks market remains semi-consolidated, with large beverage companies using reformulation, cleaner ingredient profiles, and broader format expansion to defend shelf space and daily consumption occasions. Regulatory scrutiny around labeling and health claims, along with premium pricing for specialized formulas in price-sensitive regions, continues to limit how fast some parts of the electrolyte drinks market can scale, even as the category shows durable demand through 2031.

Key Report Takeaways

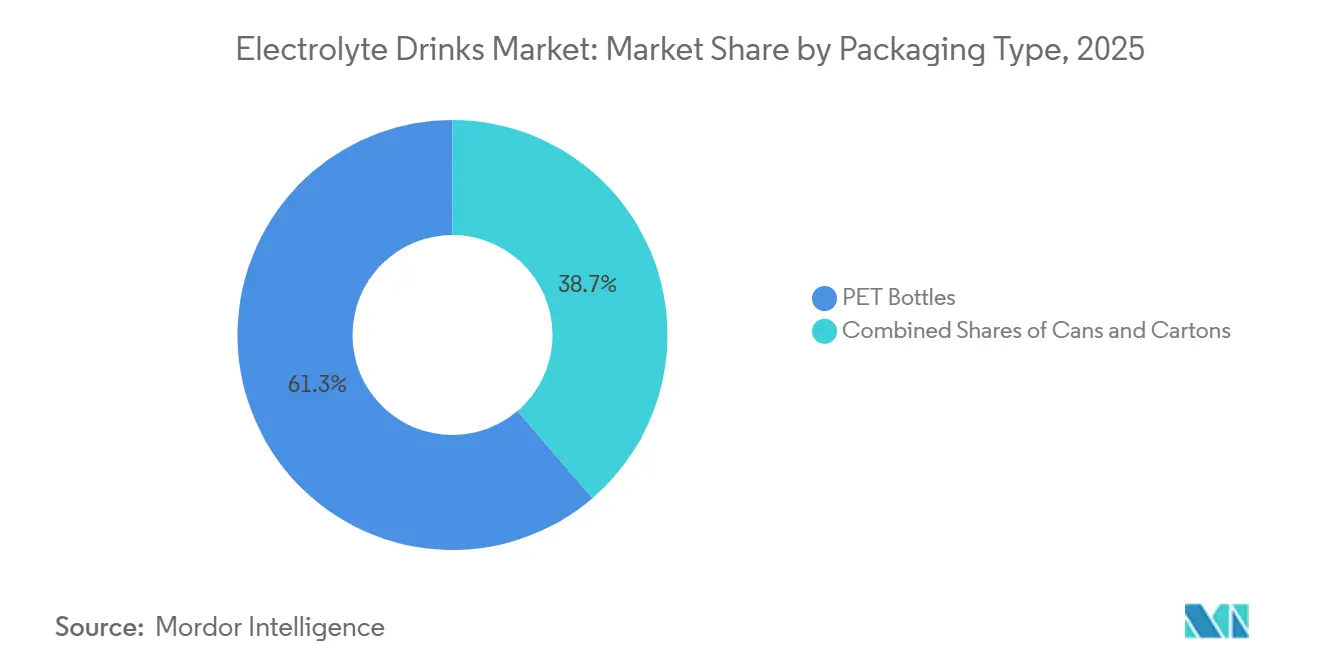

- By packaging type, PET bottles held 61.28% share in 2025, while cans are forecast to expand at 8.11% CAGR from 2026 to 2031.

- By ingredient type, conventional formulations retained 78.57% share in 2025, while clean-label variants are forecast to grow at 8.02% CAGR from 2026 to 2031.

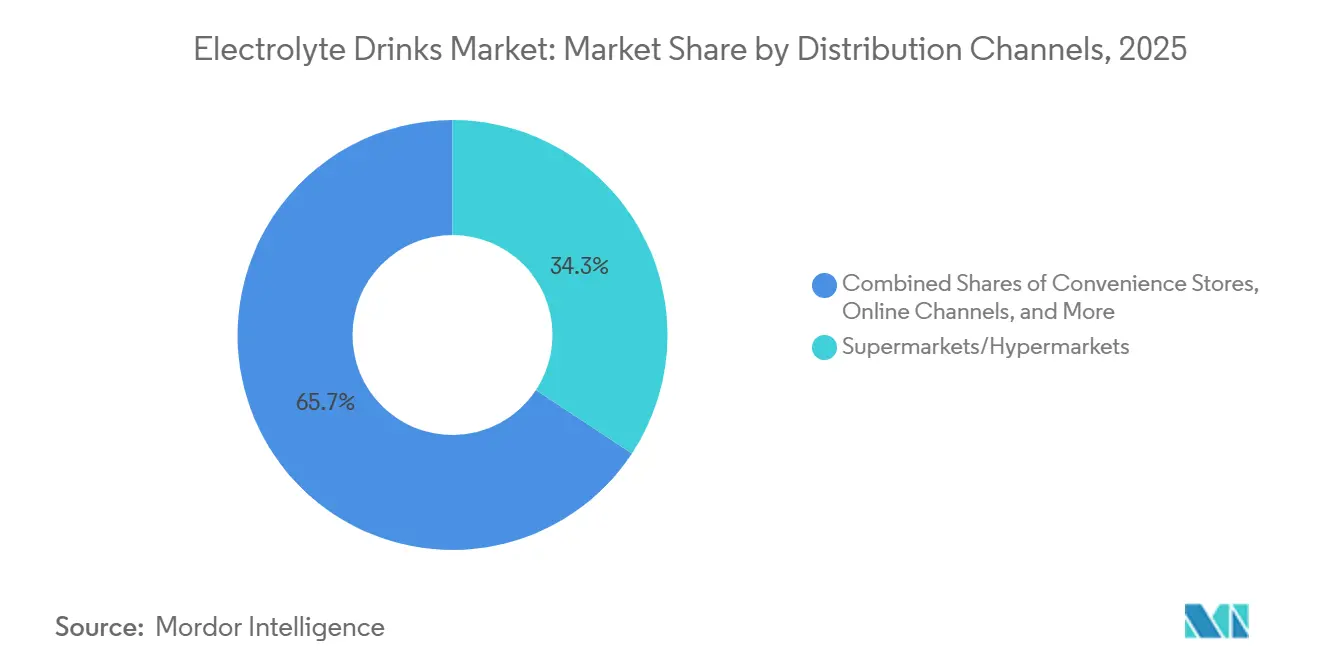

- By distribution channel, supermarkets and hypermarkets accounted for 34.28% share in 2025, while online retail is projected to grow at 7.72% CAGR through 2031.

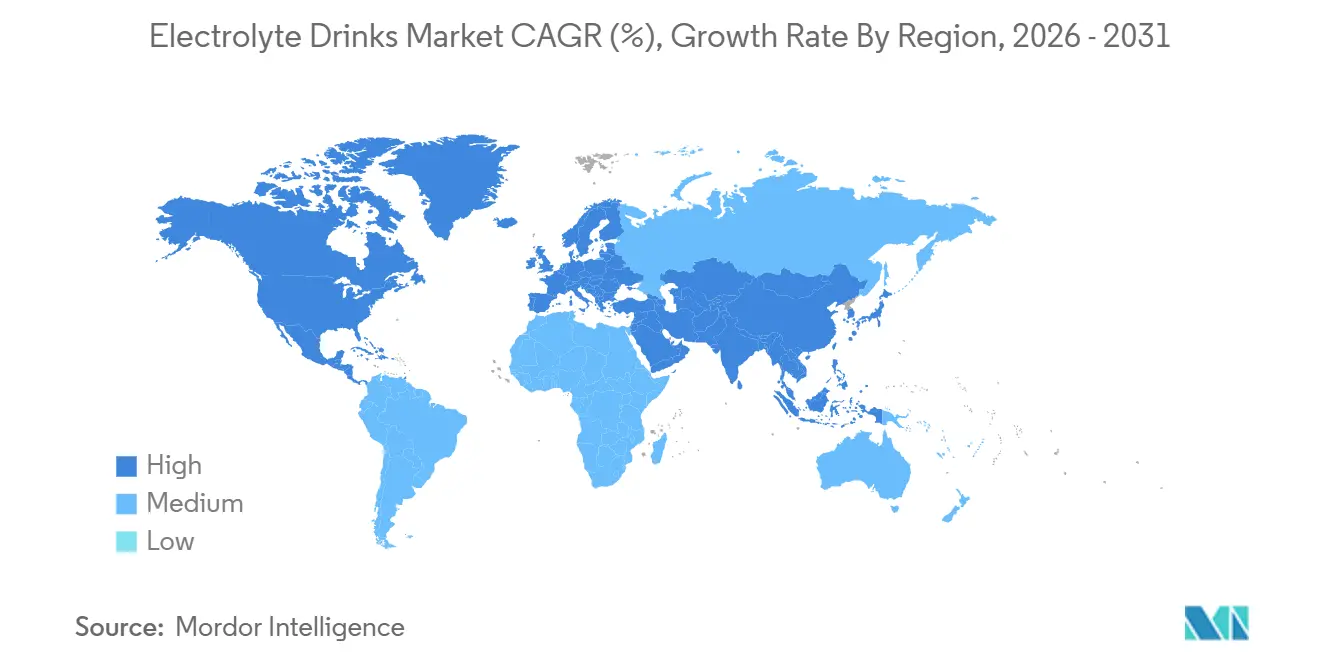

- By geography, North America led with 42.38% share in 2025, while Asia-Pacific is forecast to expand at 7.65% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Electrolyte Drinks Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Consumer Focus on Hydration and Preventive Health Management | +1.4% | Global, strongest in North America & Europe | Medium term (2-4 years) |

| Increasing Participation in Sports, Fitness, and Endurance Activities | +1.2% | Global, Asia-Pacific acceleration most notable | Medium term (2-4 years) |

| Growing Demand for Functional Beverages with Health Benefits | +1.0% | North America, Europe, APAC | Medium term (2-4 years) |

| Rising Popularity of Low-Sugar and Better-for-You Hydration Solutions | +0.8% | North America, Western Europe | Short term (≤ 2 years) |

| Product Innovation in Natural, Clean-Label, and Plant-Based Electrolyte Formulations | +0.6% | Global | Long term (≥ 4 years) |

| Growth of Ready-to-Drink (RTD) Beverage Consumption | +0.5% | Asia-Pacific, North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Consumer Focus on Hydration and Preventive Health Management

Hydration has moved beyond post-exercise use, and that shift is expanding the electrolyte drinks market into routine daily consumption. The World Health Organization stated that 31% of adults globally were physically inactive, which means a large share of the population remains within the reach of public-health messaging built around preventive behavior and better daily wellness habits[1]Source: World Health Organization, “Physical Activity,” WHO Fact Sheet, who.int . WHO's Global Action Plan on Physical Activity set a 15% relative reduction target by 2030, and this keeps governments and health systems focused on broader participation and health engagement rather than only elite sports activity. In the electrolyte drinks market, that change matters because brands can position hydration for routine use, heat management, and general wellness, not only for intense performance recovery. This broader use case supports steadier repeat purchasing and opens the category to older adults, occasional exercisers, and other consumers who do not identify as athletes.

Increasing Participation in Sports, Fitness, and Endurance Activities

The electrolyte drinks market still depends heavily on participation in sports, exercise, and endurance activity, and that base is becoming wider across regions. China's National Fitness Plan set a target for 38.5% of the population to engage in regular exercise by 2025, up from 37.2% in 2020, which reflects direct policy support for activity-based consumption categories[2]Source: State Council of the People’s Republic of China, “National Fitness Plan (2021–2025),” State Council of the People’s Republic of China, gov.cn. WHO also showed that global inactivity remained high through 2022, which keeps pressure on governments to support exercise, wellness, and public participation programs that can create new users for functional hydration products. For the electrolyte drinks market, mass participation matters because it expands usage far beyond professional or serious athletes and creates more frequent replenishment occasions across daily routines. This pattern is especially relevant in Asia-Pacific, where public investment in fitness and broader urban participation can support sustained volume growth through the forecast period.

Growing Demand for Functional Beverages with Health Benefits

The electrolyte drinks market now sits inside a broader functional beverage space where consumers expect more than simple hydration. PepsiCo launched Propel Clear Protein in May 2026 with 20 g of protein, dietary fibre, and electrolytes in one RTD, showing how major companies are combining multiple benefits in one format instead of treating hydration as a stand-alone need. This product design matters because it supports premium positioning and makes the electrolyte drinks market more competitive with adjacent categories such as protein beverages and daily wellness drinks. The same direction is visible in ongoing formulation work, where zero-calorie electrolyte systems using monk fruit extract were shown to be viable in research published in February 2026. As the electrolyte drinks market absorbs more functional benefits, product development is likely to center on convenience, credible efficacy, and broader daily use rather than single-occasion sports performance alone.

Rising Popularity of Low-Sugar and Better-for-You Hydration Solutions

Low-sugar positioning is becoming a core competitive standard in the electrolyte drinks market rather than a niche premium attribute. PepsiCo launched Gatorade Lower Sugar in March 2026 with 75% less sugar than Gatorade Thirst Quencher and without artificial flavors, sweeteners, or colors, which shows how large incumbents are moving quickly to reset mainstream expectations. Kraft Heinz also introduced Capri Sun Hydrate in April 2026 with 50% less sugar than leading regular sports drinks and no artificial flavors, colors, or preservatives, extending the cleaner hydration approach into children's formats. Research published in the Journal of Drug Delivery and Therapeutics in February 2026 showed viable zero-calorie electrolyte formulations using monk fruit extract, which supports further product reformulation without giving up sweetness delivery. For the electrolyte drinks market, the move toward lower sugar raises the bar for formulation quality because brands must preserve taste, electrolyte performance, and clean-label positioning at the same time.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intense Competition from Bottled Water, Functional Water, and Sports Drink Alternatives | -0.8% | Global, particularly North America & Europe | Short term (≤ 2 years) |

| Regulatory Scrutiny of Health Claims and Product Labeling Requirements | -0.5% | North America, European Union | Medium term (2-4 years) |

| Growing Consumer Concerns Regarding Sugar Content and Artificial Ingredients | -0.4% | North America, Western Europe | Short term (≤ 2 years) |

| Premium Pricing of Specialized and Functional Hydration Products | -0.4% | South America, Middle East and Africa, parts of Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Intense Competition from Bottled Water, Functional Water, and Sports Drink Alternatives

The electrolyte drinks market faces direct competition from bottled water, functional water, powders, tablets, RTDs, and adjacent hydration formats that can satisfy similar use cases. This pressure is structural because many of these alternatives ask for less consumer commitment and can be positioned as simpler daily hydration choices. In the electrolyte drinks market, that wide format overlap narrows the category's room for pricing separation and makes it harder for brands to defend premium shelf positions. The risk becomes stronger when consumers compare hydration formats on convenience, flavor tolerance, or routine affordability rather than on technical performance alone. As electrolytes spread across more delivery systems, the category faces reference-price pressure that can pull some demand toward lower-cost or less specialized options.

Regulatory Scrutiny of Health Claims and Product Labeling Requirements

Regulatory scrutiny remains a clear restraint on the electrolyte drinks market because the category depends heavily on on-pack communication and benefit-led positioning. The US FDA finalized its updated definition of the "Healthy" nutrient content claim on December 27, 2024, with the rule taking effect on April 28, 2025 and a compliance deadline of February 25, 2028, which places tighter limits on added sugars and sodium[3]Source: U.S. Food and Drug Administration, “FDA Finalizes Updated ‘Healthy’ Nutrient Content Claim,” FDA Constituent Update, fda.gov. This matters because sugar reduction and sodium content sit close to the category's core performance claims, so reformulation choices can affect both compliance and product efficacy. The US International Trade Commission also launched Investigation No. 337-TA-1435 in February 2025 involving electrolyte beverage labeling and packaging, which signals a more exacting legal environment around presentation and packaging conduct. For the electrolyte drinks market, these rules can slow product cycles, raise compliance costs, and limit how aggressively brands translate formulation benefits into commercial claims.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Packaging Type: Can Format Challenges PET Bottle Dominance

PET bottles held 61.28% of the electrolyte drinks market share in 2025, which reflects their fit with mainstream beverage merchandising, broad consumer familiarity, and cost efficiency in high-volume retail distribution. The electrolyte drinks market still relies on PET because supermarkets and hypermarkets remain important channels for planned purchases, larger shelf sets, and established brand blocks. Bottles also support both single-serve and take-home use, which helps brands cover workout recovery, commute consumption, and general daily hydration with the same core format. Cartons remain much smaller in the electrolyte drinks market and are more closely tied to niche positioning, family formats, or institutional usage than to mainstream sports hydration demand. Their limited role suggests that format growth is being decided more by convenience, portability, and lifestyle appeal than by novelty alone.

Cans are projected to grow at 8.11% CAGR from 2026 to 2031, which makes them the fastest-moving packaging format in this part of the electrolyte drinks industry. The Coca-Cola Company expanded BodyArmor Sports Nutrition in June 2026 with BodyArmor FIT, the brand's first sparkling sports drink in a 12 oz slim can, showing that a major incumbent now sees the can format as commercially relevant for active hydration. In the electrolyte drinks market, cans fit well with premium daily hydration positioning because they align with energy-drink adjacencies, chilled convenience displays, and a more lifestyle-led visual identity. They also give brands another route to attract trial outside traditional sports occasions, especially when sparkling, zero-sugar, or caffeine-added variants are involved. That shift does not remove PET bottle leadership, but it does show that packaging strategy in the electrolyte drinks market is becoming more tied to usage occasion, merchandising context, and premium brand expression.

By Ingredient Type: Clean-Label Formulations Outpace Conventional Segment Growth

Conventional formulations retained 78.57% share in 2025, which shows that the electrolyte drinks market still depends on established taste profiles, familiar sodium-potassium systems, and mainstream pricing. These products remain important in mass retail because they are easy to understand, widely available, and linked to decades of consumer habit built by large beverage brands. In many price-sensitive environments, conventional products continue to anchor the electrolyte drinks market because lower average selling prices matter more than ingredient purity or advanced formulation language. Their leadership also reflects how deeply legacy formulations are embedded in sports hydration routines, school sports settings, and general retail distribution. Even so, the dominance of the conventional segment now coexists with clear pressure to improve labels, reduce sugar, and remove artificial ingredients.

Clean-label variants are forecast to grow at 8.02% CAGR from 2026 to 2031, and that rate places them ahead of every other segment covered in this electrolyte drinks market review. The FDA's updated "Healthy" nutrient content claim rule has reinforced the commercial value of sugar reduction and clearer formulations for brands that want label differentiation. Research published in February 2026 also demonstrated viable zero-calorie electrolyte formulations using monk fruit extract, which supports more credible clean-label product development without losing sweetness delivery. In the electrolyte drinks market, this trend is shifting investment toward formulations that can meet taste, hydration, and ingredient-transparency expectations at the same time. The result is a clearer split inside the electrolyte drinks industry, where conventional products still hold scale but cleaner formulations are capturing more of the innovation pipeline and more of the premium growth narrative.

By Distribution Channel: Online Retail Reshapes Channel Economics

Supermarkets and hypermarkets accounted for 34.28% share in 2025, which keeps them as the largest sales route in the electrolyte drinks market. Their scale matters because these outlets combine broad assortment, established traffic, planned basket purchases, and shelf visibility that favors large beverage portfolios. Convenience stores also remain important in the electrolyte drinks market because they fit immediate consumption needs near gyms, workplaces, travel corridors, and urban commute routes. Other distribution channels, including specialty fitness retailers, pharmacies, and foodservice points, play a smaller but still useful role by reinforcing wellness positioning and serving targeted consumption moments. This channel structure shows that physical retail still anchors the electrolyte drinks market even as digital routes gain speed.

Online retail is projected to grow at 7.72% CAGR from 2026 to 2031, which makes it the fastest-growing route to market in this category. The electrolyte drinks market is benefiting from online channel mechanics such as broader flavor assortment, direct access to niche consumer groups, and less dependence on crowded physical shelf sets. Digital commerce also supports repeat-order behavior, bundle selling, and subscription models that suit products used in weekly fitness, travel, and household hydration routines. For newer brands, the online path can reduce entry friction because it allows targeted positioning before wider retail expansion becomes necessary. As a result, the electrolyte drinks market is likely to keep a mixed channel structure, where supermarkets and hypermarkets preserve scale while online retail shapes discovery, retention, and premium consumer engagement.

Geography Analysis

North America held 42.38% share in 2025, which kept it as the largest regional bloc in the electrolyte drinks market. This position reflects a large fitness-active consumer base, dense convenience retail access, and long-established brand recognition across sports and functional beverages. PepsiCo reported nearly USD 94 billion in net revenue in 2025, which underlines the scale of portfolio and distribution support available to major hydration brands operating in the region. The North American electrolyte drinks market is also seeing a fast pace of reformulation and line extension, which shows that incumbent brands are defending the category through product refresh rather than only through scale. Gatorade Lower Sugar launched in March 2026 with 75% less sugar than Gatorade Thirst Quencher, and Propel Clear Protein launched in May 2026 with 20 g of protein, dietary fibre, and electrolytes, both reinforcing the region's push toward broader functional hydration. These launches indicate that the North American electrolyte drinks market is being shaped by lower-sugar expectations, multifunctional formats, and large-scale commercial execution.

Europe remains a mid-tier region in the electrolyte drinks market, with slower scale than North America but a consumer base that is attentive to formulation, labeling, and product quality. The region's demand profile supports premium entries, but regulatory expectations can narrow how brands communicate benefits and how quickly they harmonize products across countries. That raises localization costs for the electrolyte drinks market because flavor preferences, retail norms, and compliance needs differ across major European economies. As a result, scale in Europe depends not only on brand recognition but also on disciplined product adaptation and careful claim management. This makes Europe commercially attractive, though less straightforward than more mature single-market environments.

Asia-Pacific is forecast to grow at 7.65% CAGR from 2026 to 2031, giving it the fastest regional growth rate in the electrolyte drinks market. Public support for exercise remains important in this region, and China's National Fitness Plan targeted 38.5% of the population to engage in regular exercise by 2025. Japan also shows continued breadth in sports drink supply, with the Japan Soft Drink Association recording an increase from 238 sports drink products in 2020 to 333 in 2024. These patterns support the view that the electrolyte drinks market in Asia-Pacific is expanding through a mix of broader participation, higher product availability, and deeper everyday use. South America and the Middle East and Africa remain smaller contributors, and premium pricing continues to slow adoption in parts of those regions where affordability is a more immediate purchase filter. The regional picture therefore shows a category with mature leadership in North America, measured opportunity in Europe, and the strongest forward momentum in Asia-Pacific.

Competitive Landscape

The electrolyte drinks market remains semi-consolidated, with PepsiCo and The Coca-Cola Company holding the strongest positions through brand reach, shelf access, and product breadth. Their portfolios give them an advantage across mainstream sports drinks, functional hydration, and adjacent formats that can serve both workout and daily-use occasions. Abbott Laboratories also holds a differentiated place in the electrolyte drinks market through Pedialyte, where medical credibility and consumer wellness usage intersect in a way many lifestyle-first brands cannot easily match. Regional strength matters as well, with Otsuka Pharmaceutical and Suntory Holdings retaining meaningful competitive relevance in Asia because distribution depth and local brand familiarity still shape category access. At the same time, challenger names such as LMNT, DripDrop, Nuun Hydration, and Hydrant continue to influence the electrolyte drinks market by pushing more targeted formulations and narrower community-led brand positioning.

Competition is becoming more intense because incumbent companies are now responding directly to the cleaner-label and multifunctional expectations that once helped challengers stand out. PepsiCo launched Gatorade Lower Sugar in March 2026, a move that addresses sugar concerns in a flagship hydration platform rather than in a niche extension alone. PepsiCo followed with Propel Clear Protein in May 2026, which combined hydration with 20 g of protein and dietary fibre in one RTD format. The Coca-Cola Company then extended BodyArmor in June 2026 with BodyArmor FIT in a 12 oz slim can, bringing sparkling format innovation into the sports hydration space. These strategic moves show that the electrolyte drinks market is no longer competing only on flavor and familiarity, because packaging, sugar profile, and added functional benefits now shape commercial differentiation.

Innovation is also widening the set of addressable users inside the electrolyte drinks market. Kraft Heinz introduced Capri Sun Hydrate in April 2026 as one of the first electrolyte drinks designed specifically for children, which shows that family hydration and age-specific positioning are becoming more relevant. That move suggests remaining whitespace in child-focused hydration, older-adult usage, and other underdeveloped use cases where dehydration risk is clear but branded solutions are still limited. Regulatory discipline and formulation competence are also becoming competitive assets, especially as labeling standards tighten and sugar reduction becomes more central to brand credibility. In practice, that means the electrolyte drinks market is being shaped by a mix of scale advantages, reformulation speed, and the ability to build clearer product logic for distinct consumer occasions.

Electrolyte Drinks Industry Leaders

PepsiCo Inc.

The Coca-Cola Company

Abbott Laboratories

Suntory Holdings Limited

Otsuka Pharmaceutical Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Instant Hydration introduced its new Electrolytes Drink, expanding its portfolio of hydration-focused wellness products. The beverage is formulated to support daily hydration, electrolyte balance, energy levels, and active lifestyles, targeting not only athletes but also travelers, office workers, students, and wellness-conscious consumers.

- July 2025: Evocus expanded its functional beverage portfolio by launching Hydration IV Electrolytes Drink, marking the company's entry into India's rapidly growing sports hydration and ready-to-drink (RTD) hydration market. Positioned as a clean-label hydration solution, the product contains essential electrolytes such as sodium, potassium, and chloride while remaining free from added sugar, caffeine, preservatives, and artificial colors.

- April 2025: Hindustan Unilever Limited (HUL) introduced Liquid I.V. in India, bringing the leading U.S. powdered hydration brand to one of the world's fastest-growing wellness and functional beverage markets. Backed by Unilever's Health & Wellbeing Collective, Liquid I.V. offers a science-based electrolyte hydration formulation designed for active and health-conscious consumers.

Global Electrolyte Drinks Market Report Scope

| PET Bottles |

| Cartons |

| Cans |

| Conventional |

| Clean Label |

| Supermarkets/Hypermarkets |

| Convenience Stores |

| Online Retail Stores |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Rest of Middle East and Africa |

| Packaging Type | PET Bottles | |

| Cartons | ||

| Cans | ||

| Ingredient Type | Conventional | |

| Clean Label | ||

| By Distribution Channels | Supermarkets/Hypermarkets | |

| Convenience Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the 2031 outlook for electrolyte drinks?

The electrolyte drinks market is projected to reach USD 458.17 million by 2031, up from USD 335.67 million in 2026, with a CAGR of 6.42% over 2026 to 2031.

Which packaging format is growing the fastest in this category?

Cans are the fastest-growing packaging format, with an 8.11% CAGR from 2026 to 2031, even though PET bottles still held 61.28% share in 2025.

Why are low-sugar launches becoming so important for hydration brands?

Lower-sugar products are becoming central because major brands are reformulating quickly, including Gatorade Lower Sugar with 75% less sugar and Capri Sun Hydrate with 50% less sugar than leading regular sports drinks.

Which sales channel still matters most for electrolyte drink brands?

Supermarkets and hypermarkets remained the largest distribution channel with 34.28% share in 2025, although online retail is growing faster at 7.72% CAGR through 2031.

Page last updated on: