Instant Beverage Premix Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

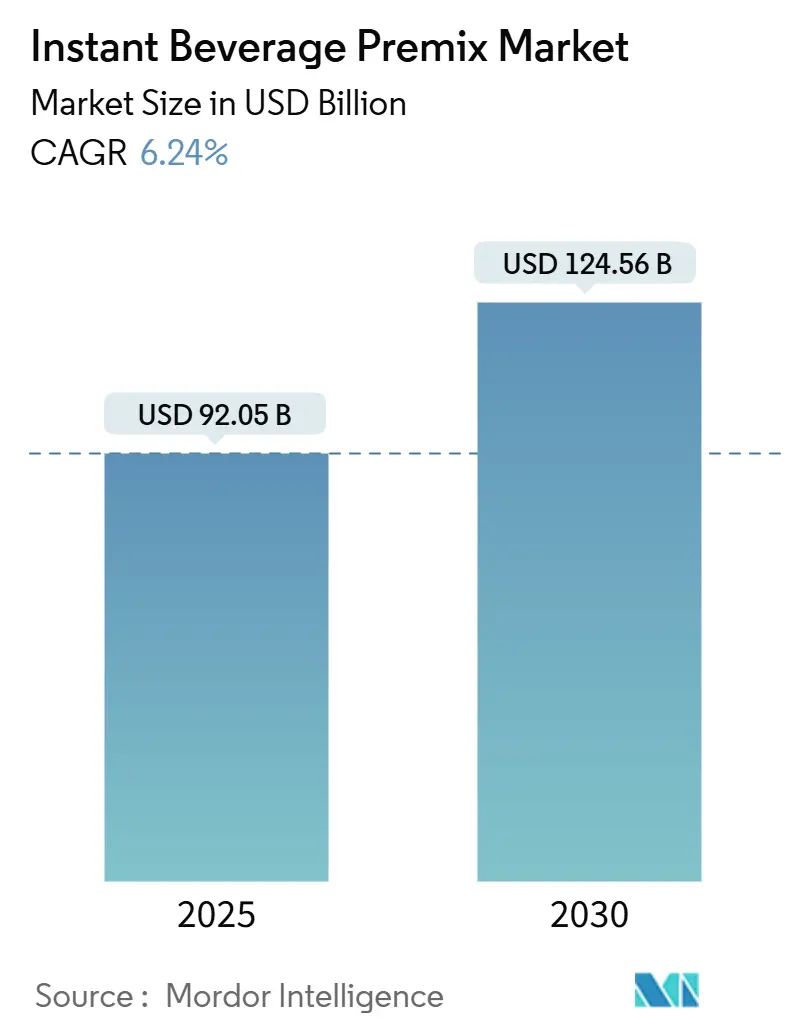

| Market Size (2025) | USD 92.05 Billion |

| Market Size (2030) | USD 124.56 Billion |

| Growth Rate (2025 - 2030) | 6.24% CAGR |

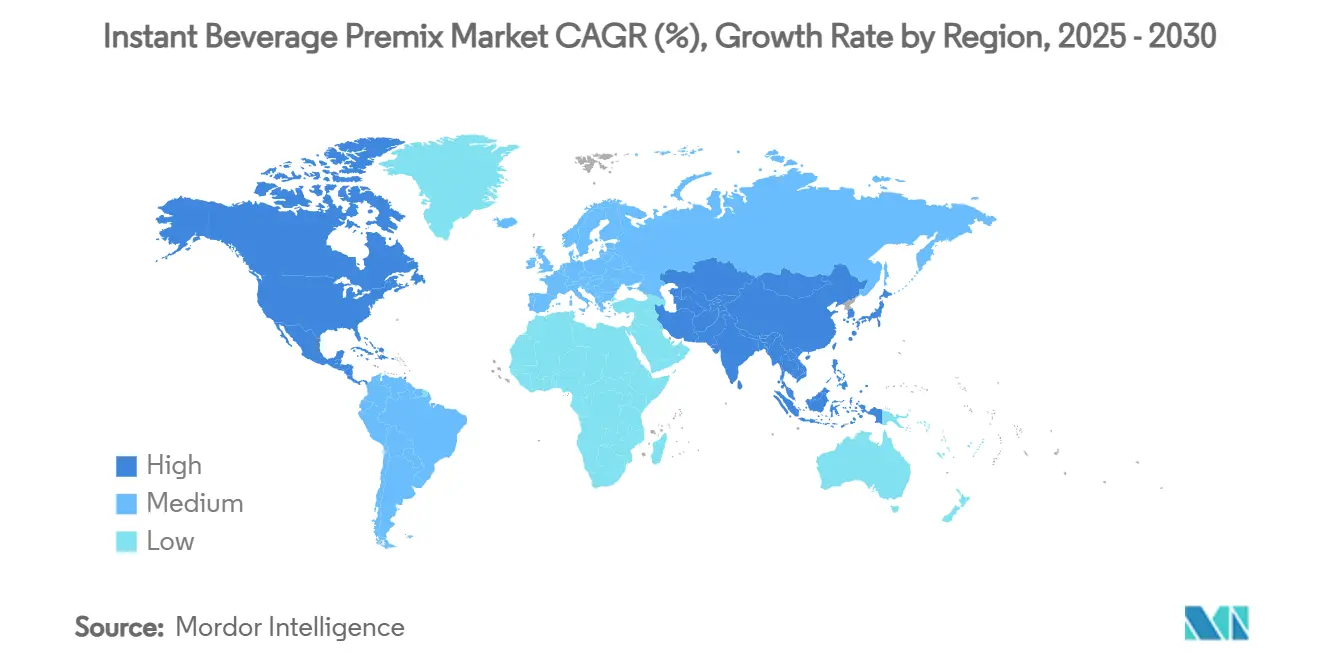

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

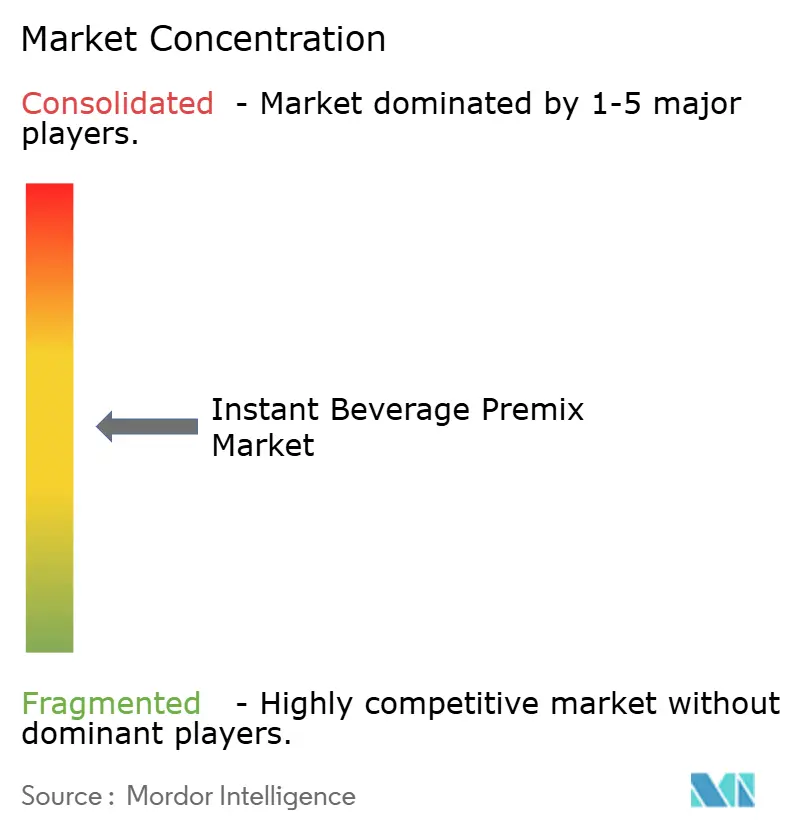

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Instant Beverage Premix Market Analysis by Mordor Intelligence

The instant beverage mixes market size is estimated at USD 92.05 billion in 2025 and is projected to reach USD 124.56 billion by 2030, growing at a CAGR of 6.24% during the forecast period. This growth trajectory reflects the convergence of urbanization, time-pressed lifestyles, and evolving consumer preferences toward convenient yet premium beverage experiences. The market's expansion is underpinned by regulatory frameworks that increasingly favor functional ingredients, with the FDA's updated allergen labeling requirements including sesame as a major allergen creating new compliance pathways for manufacturers[1]Source: U.S. Food and Drug Administration, "updated allergen labeling", trumbull-ct.gov.Chief among these is the increasing consumer demand for convenience and time-saving solutions, as instant mixes allow for quick preparation of drinks at home, work, or on the go. Shifting lifestyle patterns, particularly urbanization and the expanding working population, have amplified this need for easy, portable beverage options. There is also rising interest in health and wellness: consumers increasingly favor instant beverage mixes that offer functional benefits, contain natural or reduced-sugar ingredients, and cater to specific dietary preferences such as vegan or gluten-free. However, one notable restraint is the fluctuation in raw material prices, especially for key ingredients like sugar and natural additives, which can impact both the profitability and pricing strategies of manufacturers. In summary, while the instant beverage mixes market is well-positioned for continued growth driven by convenience, health trends, and product innovation, manufacturers must navigate challenges such as raw material cost volatility and evolving consumer demands to maintain a competitive edge and long-term market sustainability.

Key Report Takeaways

- By product type, hot beverages led with 41.32% revenue share in 2024; functional beverages are projected to expand at a 7.23% CAGR through 2030.

- By category, plain led with 62.56% revenue share in 2024; flavored are projected to expand at a 7.89% CAGR through 2030.

- By format, powder accounted for 86.54% share of the instant beverage mixes market size in 2024, while liquid concentrates are forecast to rise at a 6.77% CAGR to 2030.

- By price positioning, the value tier commanded 36.11% share of the instant beverage mixes market in 2024; premium and gourmet products will advance at an 8.21% CAGR over the same horizon.

- By distribution channel, off-trade commanded 65.48% share of the instant beverage mixes market in 2024; on-trade will advance at an 6.78% CAGR over the same horizon.

- By geography, Asia-Pacific captured 41.22% of the instant beverage mixes market share in 2024, whereas North America exhibits the fastest regional CAGR of 6.72% to 2030.

Global Instant Beverage Premix Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Busy Lifestyles and Time Constraints | +1.2% | Global, with highest impact in North America and Asia-Pacific urban centers | Short term (≤ 2 years) |

| Premiumization | +0.9% | North America and Europe primary, expanding to Asia-Pacific affluent segments | Medium term (2-4 years) |

| On-the-Go Consumption | +1.1% | Global, particularly strong in urban metros and transit hubs | Short term (≤ 2 years) |

| Innovative Flavors and Product Customization | +0.8% | North America and Europe lead, Asia-Pacific following with regional adaptations | Medium term (2-4 years) |

| Advances in Packaging | +0.6% | Global, with sustainability focus in Europe and North America | Long term (≥ 4 years) |

| E-commerce Expansion | +0.7% | Global, with highest penetration in North America and China | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Busy Lifestyles and Time Constraints

The acceleration of urban work patterns and dual-income households is fundamentally reshaping beverage consumption toward instant formats. According to the Bureau of Labor Statistics, the number of full-time employees in the United States rose from 127.16 million in 2021 to 133.36 million in 2024 [2]Source: Bureau of Labor Statistics, "Number of full-time employees in the United States", bls.gov. USDA research demonstrates that households with all adults employed purchase significantly more convenience foods, with time constraints from work and childcare driving this behavioral shift. This trend extends beyond traditional demographics, as remote work arrangements have blurred the lines between home and office consumption occasions [3]Source: U.S. Department of Agriculture, "What Drives Consumers to Purchase Convenience Foods?", usda.gov. As consumers juggle demanding work schedules, social commitments, and family responsibilities, the time available for traditional meal and drink preparation is shrinking. This shift has led to a fundamental change in consumption habits, with many people seeking convenient, easy-to-prepare products that fit seamlessly into their fast-paced lives. Instant beverage mixes—offering quick preparation, portability, and consistent taste—directly cater to these needs, allowing consumers to enjoy a variety of drinks, from coffee to functional wellness beverages, in just moments with minimal effort. Single-serve packets, diverse flavors, and functional benefits like energy or cognitive support further enhance the attractiveness of instant beverage mixes to busy consumers.

On-the-Go Consumption

On-the-go consumption is a key driver fueling the instant beverage mixes market by catering to the evolving needs of today’s fast-paced and mobile lifestyles. Consumers increasingly seek beverages that can be prepared and enjoyed quickly—whether at work, while commuting, traveling, or during busy daily routines—making portability and ease of use essential product attributes. Instant beverage mixes, available in powder and liquid formats, come in single-serve, portable packaging and can be prepared in seconds, often without special equipment. This convenience resonates especially with working professionals, students, and travelers, enabling them to enjoy a variety of drinks anywhere, anytime. The trend toward on-the-go lifestyles has also spurred innovation in packaging and format further expanding product appeal and market penetration. As the demand for quick, customizable, and portable beverage solutions continues to rise, on-the-go consumption remains a central force driving sustained growth and innovation in the instant beverage mixes market.

Innovative Flavors and Product Customization

Innovative flavors and product customization are major forces accelerating the instant beverage mixes market, fueling both consumer excitement and brand differentiation. Evolving beyond traditional offerings, brands are introducing gourmet and artisanal flavors—such as saffron chai, hazelnut mocha, and globally inspired fruit blends—to deliver café-quality, at-home experiences without the complexity of preparation. These unique and sophisticated flavor mash-ups attract consumers seeking both novelty and sensory richness, while limited-time and seasonal releases drive trial and loyalty by keeping the category fresh and engaging. For instance, in May 2025,The Campbell's Company launched a powdered version of its popular V8 Energy Drink that could be mixed with water for convenient caffeination. The portable option was available in Peach Mango, Strawberry Lemonade and Pomegranate Blueberry flavors. Each packet contained 80 milligrams of caffeine from green and black tea, plus antioxidants and vitamins A, C and E. Together, innovative flavors and customization position instant beverage mixes as not just convenient, but also aspirational lifestyle choices. They satisfy consumers’ evolving desire for variety, creativity, and personal expression—making the category more dynamic and closely attuned to the preferences of diverse, global markets.

Advances in Packaging

Advances in packaging are significantly propelling the growth of the instant beverage mixes market by enhancing convenience, product freshness, and sustainability. Modern packaging innovations—such as single-serve sachets, resealable pouches, portion-controlled sticks, and biodegradable materials—cater to consumers’ demand for portability and ease of use, making on-the-go consumption seamless and mess-free. Improved barrier technologies help preserve the flavor, aroma, and nutritional quality of instant mixes, ensuring consistent taste and a longer shelf life. Additionally, eco-friendly and recyclable packaging options are resonating with environmentally conscious shoppers, allowing brands to align with global sustainability trends and regulatory requirements. These packaging advancements not only elevate the consumer experience but also expand distribution potential by making products more suitable for e-commerce and modern retail channels, ultimately driving broader adoption and growth within the instant beverage mixes market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competition from RTD (Ready-to-Drink) Beverages | -0.8% | Global, intense in North America and Europe | Short term (≤ 2 years) |

| Limited Sensory Experience | -0.4% | Global, greater impact in premium segments | Medium term (2-4 years) |

| Allergens and Dietary Restrictions | -0.3% | North America and Europe under stricter rules | Long term (≥ 4 years) |

| Regulatory Hurdles | -0.2% | Global, varying by jurisdiction | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Competition from RTD (Ready-to-Drink) Beverages

RTD products offer superior taste consistency and eliminate preparation steps, appealing to consumers seeking maximum convenience. However, instant beverage mixes maintain advantages in shelf stability, cost per serving, and customization flexibility that RTD beverage products cannot match. The competitive dynamic is driving instant beverage manufacturers to focus on premium positioning and functional benefits that justify the preparation requirement. Coca-Cola's SEC filing emphasizes its strategy as a "total beverage company" that spans multiple categories, indicating how major players are hedging across both instant and RTD formats. As a result, RTD options, from coffee and tea to functional and alcoholic beverages, are drawing market share and shelf space that might otherwise go to instant beverage mixes. In this competitive environment, instant beverage mix brands are compelled to continuously innovate in flavor, functionality, and packaging to retain consumer interest and relevance.

Limited Sensory Experience

The inherent limitation of instant beverages in replicating the full sensory experience of freshly prepared drinks remains a persistent market restraint. Consumer expectations for aroma, texture, and flavor complexity continue to evolve, particularly in premium segments where instant products compete directly with artisanal alternatives. The challenge is most pronounced in coffee categories where the ritual of brewing contributes significantly to the consumption experience. Manufacturers are investing in encapsulation technologies and flavor release mechanisms that enhance the sensory profile of instant products during preparation and consumption. The development of instant beverages that change color, temperature, or texture during mixing represents an attempt to add sensory engagement to the preparation process. Research into biodegradable packaging materials that can enhance aroma release during opening is addressing one aspect of the sensory limitation while supporting sustainability goals.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Functional Beverages Drive Innovation

Hot beverages maintain market leadership with 41.32% share in 2024, reflecting established consumer habits around instant coffee and tea consumption. However, functional beverages represent the fastest-growing segment at 7.23% CAGR through 2030, driven by consumer demand for products that deliver health benefits alongside convenience. The protein and meal replacement subsegment within functional beverages is experiencing particularly strong growth as consumers seek nutritional solutions that fit busy lifestyles. Cold beverages occupy a middle position, with iced tea mixes and fruit-flavored drinks benefiting from seasonal consumption patterns and innovation in natural flavoring. The sports nutrition market's global value growth demonstrates the expanding consumer base beyond professional athletes to lifestyle users.

Immunity boosters and energy drink mixes within the functional category are gaining traction as consumers prioritize health and performance benefits. The COVID-19 pandemic accelerated interest in immune-supporting ingredients, with manufacturers incorporating vitamins, minerals, and botanical extracts into instant formats. Malted drinks and milk tea mixes show regional strength, particularly in Asia-Pacific markets where these products align with traditional consumption patterns. The development of instant beverages that combine multiple functional benefits, such as energy and immunity support, represents an emerging trend that addresses consumer desire for comprehensive wellness solutions in convenient formats.

By Category: Flavored Variants Accelerate Growth

Plain instant beverages command 62.56% market share in 2024, dominated by traditional coffee and tea formats that prioritize authenticity and simplicity. However, flavored variants are experiencing faster growth at 7.89% CAGR, reflecting consumer appetite for variety and taste innovation. The flavored segment's expansion is driven by successful flavor extensions in coffee categories, including seasonal offerings and dessert-inspired profiles that appeal to younger demographics. Manufacturers are leveraging natural flavoring technologies to create authentic taste experiences that differentiate flavored products from artificial alternatives. The success of flavored instant beverages in premium segments demonstrates consumer willingness to pay for taste innovation and quality ingredients.

Regional flavor preferences are shaping product development strategies, with Asian markets favoring fruit and floral notes while Western markets gravitate toward spice and dessert flavors. The development of limited-edition flavored variants creates excitement and trial opportunities that drive category growth. Cross-category flavor inspiration, such as incorporating popular snack or dessert flavors into instant beverages, represents an emerging trend that expands the flavor palette beyond traditional beverage categories. The integration of functional ingredients into flavored variants allows manufacturers to combine taste appeal with health benefits, creating products that satisfy multiple consumer needs simultaneously.

By Form: Powder Dominance with Liquid Innovation

Powder format maintains overwhelming dominance with 86.54% market share in 2024, benefiting from superior shelf stability, cost efficiency, and packaging convenience. The powder format's advantages include reduced shipping costs, extended shelf life, and portion control flexibility that appeals to both manufacturers and consumers. However, liquid concentrates are growing at 6.77% CAGR, driven by premium positioning and enhanced taste delivery that more closely approximates freshly prepared beverages. Liquid formats excel in cold beverage applications where powder dissolution can be challenging, particularly in on-the-go consumption scenarios. The development of single-serve liquid concentrates in portable packaging addresses convenience needs while maintaining the taste advantages of liquid formats.

Innovation in powder technology is focusing on improved solubility, enhanced flavor release, and reduced settling to address traditional format limitations. Encapsulation technologies are enabling powder formats to deliver more complex flavor profiles and functional ingredient stability. The emergence of hybrid formats that combine powder convenience with liquid taste characteristics through advanced processing represents a strategic response to format limitations. Packaging innovations in powder formats include resealable pouches, portion-controlled sachets, and dispensing systems that enhance user experience while maintaining cost advantages.

By Price Range: Premium Segment Leads Growth

Value segments maintain the largest market share at 36.11% in 2024, reflecting price sensitivity among mass-market consumers and the importance of affordability in driving category penetration. Mid-range products occupy a significant portion of the market, balancing quality and price considerations that appeal to mainstream consumers. However, premium and gourmet segments are experiencing the highest growth at 8.21% CAGR, driven by consumer willingness to pay for superior ingredients, unique flavors, and brand prestige. The premium segment's growth reflects broader consumer trends toward quality over quantity and the perception of instant beverages as lifestyle products rather than commodity items.

Premium positioning strategies include organic certifications, single-origin sourcing, artisanal flavor profiles, and sustainable packaging that justify higher price points. The success of premium instant coffee collaborations, such as Nestlé's partnership with Starbucks, demonstrates consumer acceptance of premium pricing for quality and brand associatio. Gourmet segments are expanding beyond traditional coffee and tea to include exotic flavors, functional ingredients, and limited-edition offerings that create exclusivity and trial motivation. The development of premium instant beverages that rival specialty café experiences represents the next evolution in category premiumization.

By Distribution Channel: On-Trade Gains Momentum

Off-trade channels dominate with 65.48% market share in 2024, encompassing supermarkets, convenience stores, and online retailers that provide broad consumer access and competitive pricing. Supermarkets and hypermarkets remain the primary distribution channel for bulk purchases and family consumption, while convenience stores cater to impulse purchases and on-the-go consumption needs. Online retailers are experiencing rapid growth as e-commerce penetration increases and consumers embrace the convenience of home delivery and subscription services.

On-trade channels are growing at 6.78% CAGR, driven by workplace vending machines, food service applications, and hospitality sector adoption. The Indian vending machine market's projected 17.2% CAGR growth by 2028 reflects the expanding role of automated retail in instant beverage distribution. Food service applications include office coffee services, hotel amenities, and restaurant beverage programs that utilize instant formats for consistency and cost control. The development of commercial-grade instant beverage systems for food service applications represents an emerging opportunity that bridges retail and institutional markets.

Geography Analysis

Asia-Pacific dominates the global instant beverage mixes market with 41.22% share in 2024, driven by deeply ingrained tea and coffee consumption cultures across major economies including China, India, and Japan. The region's leadership stems from both supply-side advantages, including established manufacturing capabilities and agricultural raw material access, and demand-side factors such as large population bases and rising disposable incomes. Cultural preferences for traditional beverages like masala tea and green tea create natural demand for instant formats that preserve authentic flavors while offering modern convenience. Government initiatives supporting food processing and export capabilities in countries like India are creating favorable conditions for market expansion, while urbanization trends drive demand for convenient beverage solutions among time-pressed consumers.

North America emerges as the fastest-growing geography with 6.72% CAGR through 2030, propelled by health-conscious consumers seeking functional benefits and premium experiences in their daily routines. The region's growth trajectory reflects successful premiumization strategies, with consumers demonstrating willingness to pay higher prices for organic ingredients, sustainable packaging, and innovative flavor profiles. The region's regulatory environment supports functional ingredient innovation while maintaining strict safety standards that enhance consumer confidence.

Europe and other regions exhibit steady growth patterns influenced by sustainability mandates, premium positioning, and regulatory frameworks that favor natural ingredients and transparent labeling. European consumers prioritize environmental considerations in their purchasing decisions, driving demand for instant beverages with sustainable packaging and ethical sourcing credentials. The region's emphasis on organic and clean-label products aligns with instant beverage innovation in natural flavoring and functional ingredient integration. Middle East and Africa, along with South America, represent emerging opportunities where urbanization, rising incomes, and changing lifestyle patterns create demand for convenient beverage solutions. These regions benefit from growing retail infrastructure and increasing exposure to global beverage trends through digital channels and international brand expansion.

Competitive Landscape

The instant beverage mixes market exhibits moderate concentration, indicating balanced competition between established multinational corporations and emerging regional players. This fragmentation creates opportunities for innovation-driven companies to capture market share through differentiated product offerings, strategic partnerships, and targeted market entry strategies. Major players, including Nestlé S.A., Mondelēz International, Inc., Unilever PLC, Starbucks Corporation, and The Kraft Heinz Company, leverage global distribution networks and brand recognition to maintain market positions, while smaller companies compete through niche positioning, local market expertise, and agile product development capabilities.

The relentless focus on health and wellness trends—such as natural ingredients, low sugar, and added functional benefits—drives product differentiation and compels manufacturers to continuously adapt to evolving consumer needs. Premiumization, sustainability commitments, and the adoption of eco-friendly packaging are additional factors reshaping competition, as companies vie for health-conscious and environmentally aware consumers. Meanwhile, rapid adoption of digital technologies, from AI in manufacturing to direct-to-consumer e-commerce models, is enabling both multinational and regional brands to reach new markets and customers with greater personalization and efficiency.

Smaller regional and niche brands are also gaining ground by focusing on clean-label formulations, plant-based options, and tailored solutions for local tastes and dietary preferences, often responding more quickly to specific consumer demands. The market is further energized by frequent collaborations, partnerships, and strategic acquisitions aimed at expanding product portfolios and geographic reach. In December 2024, Ocean Spray Cranberries, Inc. announced a new way to enjoy their juice drink with the introduction of powdered drink mixes, in partnership with Dyla Brands. This collaboration marked a significant step in bringing familiar and delicious flavors to the powdered beverage drink mix space.

Instant Beverage Premix Industry Leaders

-

Nestlé S.A.

-

Mondelēz International, Inc

-

Unilever PLC

-

Starbucks Corporation

-

The Kraft Heinz Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Good Enough Brands launched its functional beverage: Good Enough Probiotics Reds Mix, Fruit Punch Flavored Drink Mix. Each serving of the mix contained probiotic strain Anaerostipes caccae CLB101 to support gut health. The drink mix focused on delivering a refreshing, low-calorie beverage that promotes healthy digestion.

- June 2025: The V8 Energy team brought a fresh twist to their iconic vegetable-based beverages with the launch of V8 Energy Drink Mix. The drink mix powder offered a steady energy boost in a new convenient on-the-go format. A convenient option for those on the go, V8 Energy Drink Mix provided a smooth, fruit-forward profile, packed with 80mg of natural caffeine from black and green tea. V8 Energy Drink Mix was available in three delicious flavors: Pomegranate Blueberry, Peach Mango, and Strawberry Lemonade.

- May 2025: RTD tea brand Kaytea introduced a new range of instant iced tea powder products, aiming to bring 'next generation hydration' to the United Kingdom market. The powders were available in three flavours – Peach and Mango, Lemon and Classic Milk Tea. Designed for easy preparation, the pre-blended powders could simply be stirred into hot water and topped with ice or mixed with cold water in a blender.

- May 2025: Continental Coffee, one of India's leading beverage brands and a subsidiary of CCL Products (India) Limited, launched a refreshing new addition to its growing portfolio – the Continental THIS Lemon Iced Tea Premix Available pan-India. The Lemon Iced Tea Premix was available in two convenient formats – a 400g pouch and a 140g stick pack (10g x 14 sticks) catering to both individual and family consumption.

Global Instant Beverage Premix Market Report Scope

| Hot Beverages | Instant Coffee |

| Instant Tea | |

| Hot Chocolate/Cocoa Mix | |

| Malted Drinks | |

| Milk Tea Mixes | |

| Cold Beverages | Iced Tea Mix |

| Lemonade Mix | |

| Fruit-flavored Drink Mixes | |

| Sports and Electrolyte Drink Mixes | |

| Others | |

| Functional Beverages | Protein/Meal Replacement Mixes |

| Immunity Boosters | |

| Energy Drink Mixes | |

| Sleep/Relaxation Mixes | |

| Others |

| Plain |

| Flavored |

| Powder |

| Liquid |

| Value |

| Mid-range |

| Premium/Gourmet |

| On-Trade | |

| Off-Trade | Supermarkets/Hypermarkets |

| Convenience/Grocery Stores | |

| Online Retailers | |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Thailand | |

| Rest of Asia-Pacific | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America |

| By Product Type | Hot Beverages | Instant Coffee |

| Instant Tea | ||

| Hot Chocolate/Cocoa Mix | ||

| Malted Drinks | ||

| Milk Tea Mixes | ||

| Cold Beverages | Iced Tea Mix | |

| Lemonade Mix | ||

| Fruit-flavored Drink Mixes | ||

| Sports and Electrolyte Drink Mixes | ||

| Others | ||

| Functional Beverages | Protein/Meal Replacement Mixes | |

| Immunity Boosters | ||

| Energy Drink Mixes | ||

| Sleep/Relaxation Mixes | ||

| Others | ||

| By Category | Plain | |

| Flavored | ||

| By Form | Powder | |

| Liquid | ||

| By Price Range | Value | |

| Mid-range | ||

| Premium/Gourmet | ||

| By Distribution Channel | On-Trade | |

| Off-Trade | Supermarkets/Hypermarkets | |

| Convenience/Grocery Stores | ||

| Online Retailers | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Thailand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the instant beverage mixes market?

The instant beverage mixes market size is USD 92.05 billion in 2025.

How fast will the instant beverage mixes market grow through 2030?

The market is forecast to grow at a 6.24% CAGR, reaching USD 124.56 billion by 2030.

Which region leads the instant beverage mixes market?

Asia-Pacific leads, holding 41.22% share in 2024.

Which product segment is expanding the quickest?

Functional instant beverages are advancing at a 7.23% CAGR to 2030.

Page last updated on: