Health Drinks Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

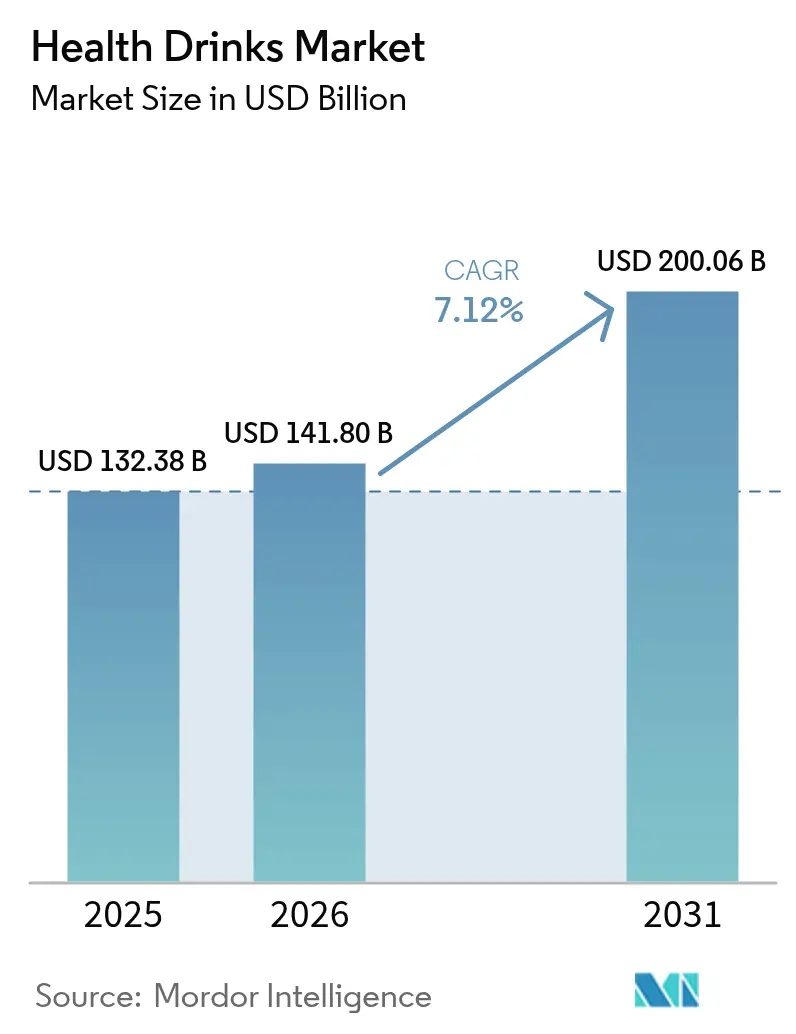

| Market Size (2026) | USD 141.8 Billion |

| Market Size (2031) | USD 200.06 Billion |

| Growth Rate (2026 - 2031) | 7.12% CAGR |

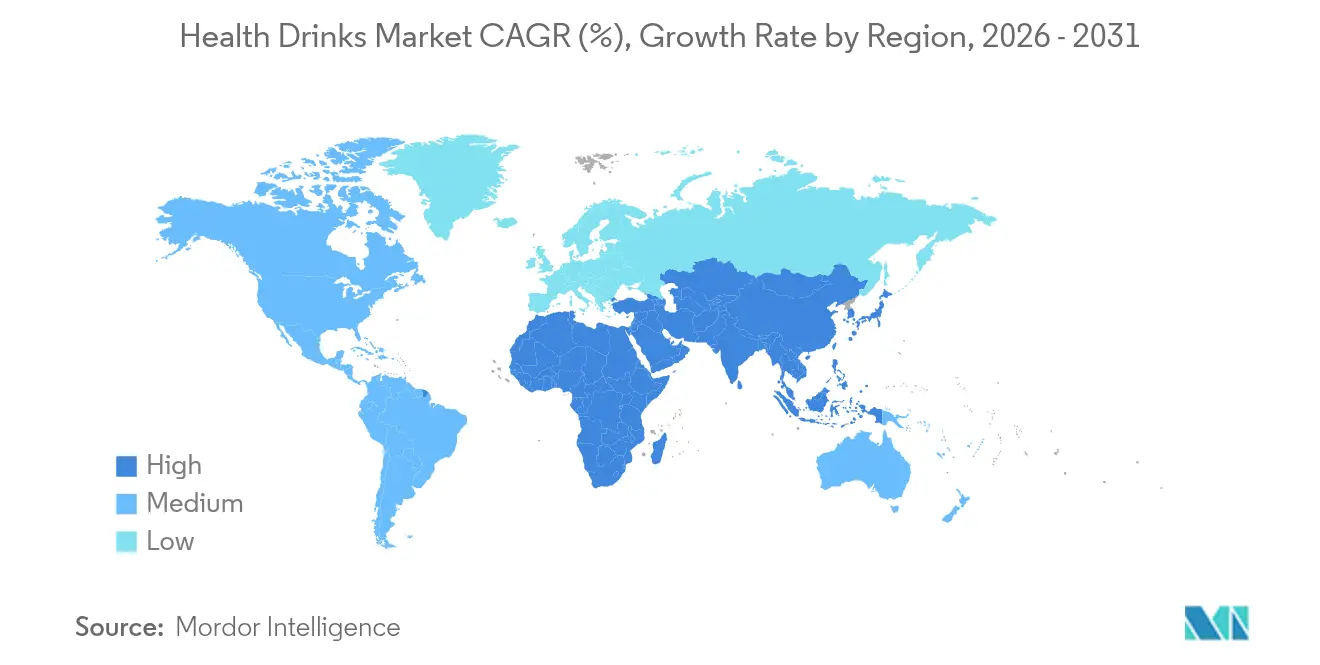

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Health Drinks Market Analysis by Mordor Intelligence

The health drinks market size was valued at USD 132.38 billion in 2025 and estimated to grow from USD 141.8 billion in 2026 to reach USD 200.06 billion by 2031, at a CAGR of 7.12% during the forecast period (2026-2031). This growth is driven by changing demographics, rising healthcare spending, and clearer regulations, which are encouraging consumers to choose preventive nutrition and functional beverages. Increased digital access, advancements in ingredients, and eco-friendly packaging are also boosting demand. Regionally, North America holds the largest market share in 2024, while Asia-Pacific is the fastest-growing region through 2030. Among products, fruit and vegetable juices lead the market, while dairy and plant-based drinks are growing the fastest due to rising interest in plant-based options, concerns about lactose intolerance, and sustainability. Online retail stores are becoming the preferred distribution channel, surpassing traditional hypermarkets/supermarkets. Sustainable packaging innovations are driving the growth of Tetra Pack. The health drinks market is moderately fragmented, providing opportunities for smaller or new companies to enter and compete. This setup promotes innovation as brands can stand out with unique formulations, functional benefits, eco-friendly packaging, or focused marketing strategies. Companies often use collaborations, acquisitions, and regional expansions to strengthen their market presence.

Key Report Takeaways

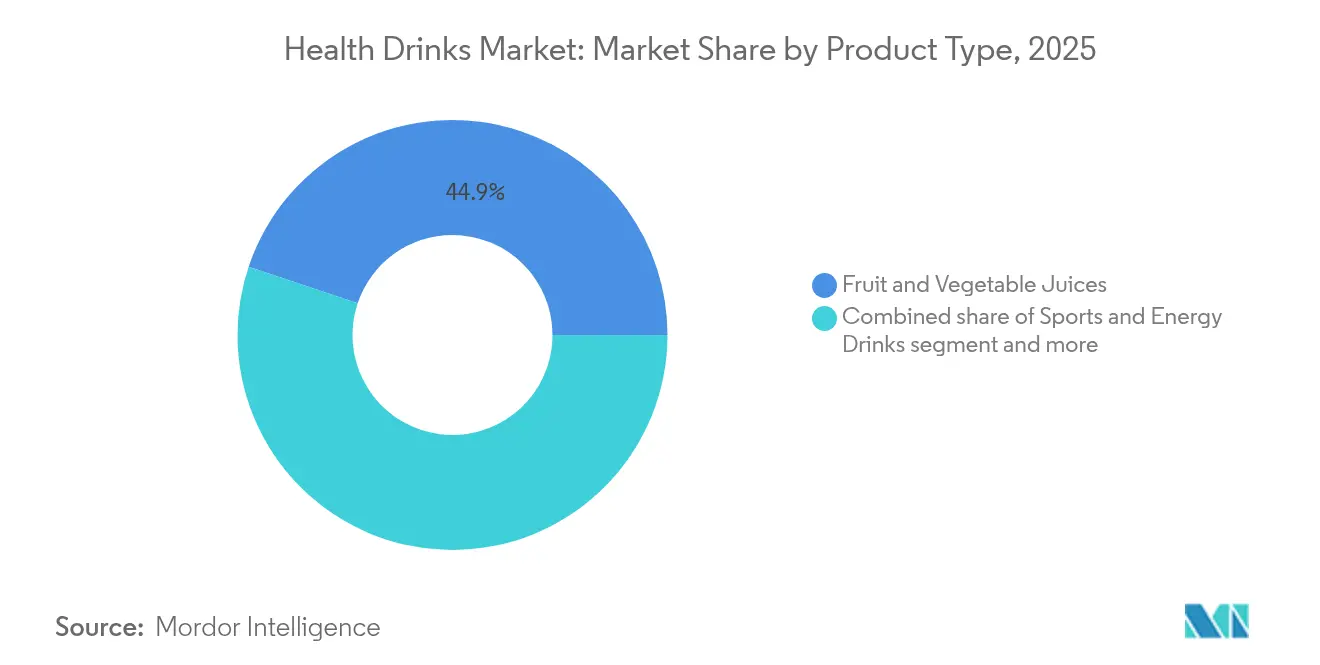

- By product category, fruit and vegetable juices led with 44.85% of the health drinks market share in 2025; dairy and plant-based drinks are forecast to expand at a 7.32% CAGR through 2031.

- By packaging type, bottles accounted for a 65.10% share of the health drinks market size in 2025, while tetra packs are advancing at a 7.34% CAGR to 2031.

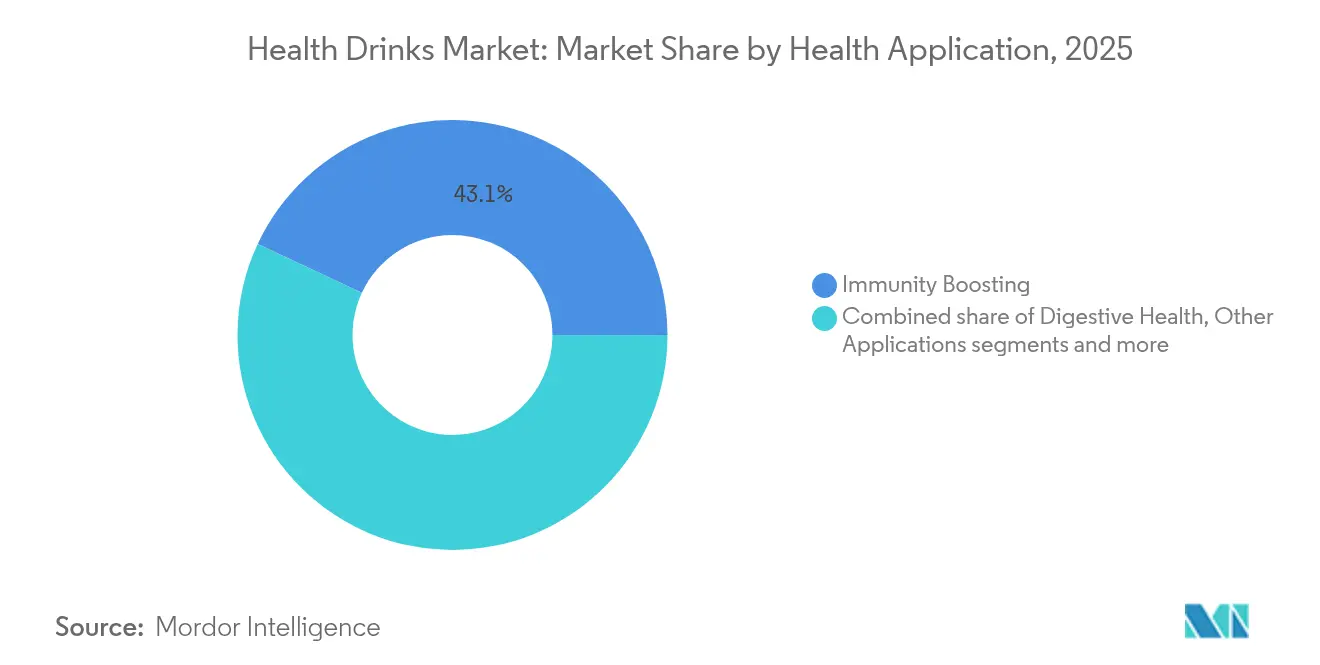

- By health application, immunity-boosting applications captured 43.05% share of the health drinks market size in 2025, and digestive health applications are growing at an 8.28% CAGR to 2031.

- By distribution channel, hypermarkets/supermarkets retained a 35.10% share in 2025; online retail is expanding at a 7.75% CAGR to 2031.

- By geography, North America held a 36.10% share in 2025, whereas the Asia-Pacific is registering the fastest regional CAGR at 7.92% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Health Drinks Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising health and wellness awareness | +1.5% | Global, with strongest impact in North America and Europe | Medium term (2-4 years) |

| Growing penetration of low-/no-sugar formulations | +1.2% | North America and Europe leading, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Increasing prevalence of lifestyle diseases | +0.8% | Global, particularly acute in developed markets | Long term (≥ 4 years) |

| Demand for natural and clean-label products | +0.9% | North America and Europe core, emerging in Asia-Pacific | Medium term (2-4 years) |

| Rise of fitness and sports culture | +0.6% | Global, with youth demographics driving adoption | Short term (≤ 2 years) |

| Influence of social media and trends | +0.3% | Global, strongest in digitally connected markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising health and wellness awareness

The health drinks market is expanding rapidly as more people prioritize wellness and healthier lifestyles. Shifts in consumer habits during the pandemic, rising obesity rates, and a decline in physical activity have fueled demand for metabolic health drinks, which are viewed as a convenient way to support overall health. According to the World Health Organization, by 2025, an additional 1.5 billion people, ranging from 1.2 to 1.8 billion, are expected to experience improved health and well-being, underscoring the vast growth potential for health-focused beverages [1]Source: World Health Organization, "WHO Data", data.who.int. This anticipated improvement in global health underscores a growing demand for products that promote preventive care and an active lifestyle. Younger consumers, in particular, are driving this shift, seeking clean-label products with transparent ingredient lists and scientifically validated benefits. Many rely on digital platforms and social media for real-time proof of these claims. In response, manufacturers are developing innovative, clinically tested formulations and strengthening credibility through evidence-based marketing positioning health drinks not just as nutritional supplements, but as aspirational lifestyle and premium wellness products.

Growing penetration of low-/no-sugar formulations

The shift toward healthier consumption habits is driving the growth of low- and no-sugar health drinks. This trend is driven by growing evidence that links sugary beverages to severe health conditions, including diabetes, which, as of 2024, impacts 589 million adults aged 20-79 globally, according to the International Diabetes Federation[2]Source: International Diabetes Federation, "The Diabetes Atlas", diabetesatlas.org. Governments are encouraging this shift by introducing sugar taxes and restricting sugary drinks in schools, while organizations like the World Health Organization are promoting these measures to fight childhood obesity. Consumers are also changing their behavior, with the International Food Information Council (IFIC) 2024 survey showing that 66% of Americans are trying to reduce their sugar intake this year[3]Source: International Food Information Council (IFIC), "2024 IFIC Food and Health Survey", ific.org. To meet this demand, brands are launching more low-sugar options. For instance, in November 2024, Red Bull introduced Red Bull Zero, a sugar-free, zero-calorie version of its original energy drink, offering the same taste without the sugar.

Rise of fitness and sports culture

The growing popularity of fitness and sports is changing the health drinks market, as young people frequently share their gym sessions, sports events, and active lifestyles online. This has turned hydration and recovery drinks into symbols of a healthy lifestyle. Data highlights this trend, as of December 2024, nearly half (48%) of the people in the United Kingdom exercise 3 or more times a week, according to the Agriculture and Horticulture Development Board (AHDB), and most aim for a balanced diet, showing a strong focus on health[4]Source: Agriculture and Horticulture Development Board (AHDB), "Consumer Attitudes Show Health Is All About Balance", ahdb.org.uk. Similarly, the Sports and Fitness Industry Association's (SFIA's) Topline Participation Report shows 247.1 million Americans were active in at least 1 activity in 2024[5]Source: Sports and Fitness Industry Association's (SFIA's), "SFIA’s Topline Participation Report Shows 247.1 Million Americans Were Active in 2024", sfia.org. This combination of physical activity and healthy eating is increasing demand for drinks that not only hydrate but also provide added benefits like electrolytes, protein, and ingredients for energy, endurance, and recovery.

Demand for natural and clean-label products

Consumers are increasingly avoiding synthetic additives, making "natural" products a basic expectation in the health drinks market. People are paying closer attention to ingredients, favoring products with transparent sourcing, sustainable farming, and minimal processing, even if they cost more. According to Ingredion’s 2024 ATLAS study, 78% of global consumers were willing to spend extra on foods and drinks labeled "natural" or "all natural." In December 2024, the United States Food and Drug Administration (FDA) introduced a new rule for the "healthy" label. This rule replaces outdated nutrient thresholds with food-group-based criteria, limits added sugars, sodium, and saturated fat, and excludes naturally occurring saturated fat in nuts, seafood, and seeds, aligning with modern dietary guidelines. In this changing market, having a clean label is essential for survival, significantly influencing strategies in the functional beverage sector.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory hurdles and safety concerns | -1.1% | Global, with varying intensity by jurisdiction | Medium term (2-4 years) |

| Intense competition and product substitution | -0.7% | Global, particularly acute in mature markets | Short term (≤ 2 years) |

| Regulatory scrutiny on caffeine and novel ingredients | -0.6% | North America and Europe leading, expanding globally | Long term (≥ 4 years) |

| Concerns over sugar and artificial additives | -0.4% | Global, with consumer-driven regional variations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory hurdles and safety concerns

Regulatory challenges and safety concerns are significant barriers to the health drinks market, as stricter rules increase compliance risks and legal issues. For example, in January 2025, Abbott faced lawsuits claiming misleading marketing of toddler milk due to its sugar content. Globally, regulations are becoming stricter, with a 2024 BioMed Central Public Health report showing that 73 countries limit caffeine levels or restrict energy drink sales to minors, making international launches more difficult. Companies now need to invest more in clinical research, detailed product documentation, and advanced monitoring systems while meeting various labeling and advertising rules. These challenges lead to higher compliance costs, longer product development times, and increased scrutiny, which can slow innovation and make it harder for new players to enter the market.

Regulatory scrutiny on caffeine and novel ingredients

Regulations around caffeine and new ingredients are becoming stricter worldwide, creating challenges for health drink manufacturers. In 2024, the European Union made it mandatory to display caffeine content on the front of packaging, addressing concerns about young people consuming too much caffeine. In the U.S., lawmakers introduced the Sarah Katz Caffeine Safety Act in 2025, which aims to improve transparency about caffeine in products and set age restrictions for energy drink sales. For new ingredients like botanicals and functional additives, companies now face stricter approval processes. They must provide detailed safety data, allergen studies to meet GRAS (Generally Recognized As Safe) requirements. These processes are expensive, often costing millions, and can take years to complete. This stricter regulation slows down product launches and discourages investment, making it harder to innovate in the market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Plant-Based Drives Category Evolution

Fruit and vegetable juices remained the top segment in the health drinks market in 2025, holding 44.85% of the market share. Their popularity is driven by consumer familiarity, easy availability in stores, and the belief that juices are naturally healthy. Ready-to-drink beverage options, combined with their association with vitamins, minerals, and antioxidants that support immunity, make them a preferred choice. New products like cold-pressed juices, fortified blends, and low-sugar options are keeping them relevant as consumers look for both taste and health benefits.

On the other hand, dairy-based and plant-based health drinks are the fastest-growing segment, expected to grow at a CAGR of 7.32% through 2031. This growth is fueled by increasing awareness of lactose intolerance and the rising demand for sustainable, protein-rich alternatives. Plant-based drinks, in particular, are gaining popularity as consumers prioritize clean labels, ethical sourcing, and environmental sustainability. Innovations like almond-protein shakes and probiotic dairy alternatives are attracting both traditional dairy consumers and health-conscious buyers, making this segment a key driver of future growth in the health drinks market.

By Packaging Type: Sustainability Reshapes Container Preferences

Bottled formats accounted for 65.10% of the health drinks packaging share in 2025, primarily because they are widely available, affordable, and convenient for consumers. Bottles are easy to use for both retail purchases and on-the-go consumption, making them a popular choice. Well-established production systems and strong distribution networks support their dominance. Features like lightweight materials and resealable caps make them practical for single-serve use, especially for outdoor activities or quick purchases. These factors have solidified bottles as the preferred packaging option for health drinks.

Tetra packs are the fastest-growing packaging type, with an expected CAGR of 7.34% through 2031. This growth is driven by increasing consumer and regulatory focus on sustainability, as cartons are often made with renewable materials and recycled content. They are also gaining popularity among health drink brands that want to emphasize freshness, longer shelf life, and an eco-friendly image. Cartons appeal to environmentally conscious consumers and align with the market's shift toward sustainable practices. This trend highlights how packaging is becoming a key tool for brands to communicate health, innovation, and sustainability to their customers.

By Health Application: Digestive Wellness Accelerates Growth

In 2025, immunity-focused applications made up 43.05% of health drink sales, showing how consumers continue to prioritize wellness habits developed during the pandemic. These beverages are enriched with key nutrients like vitamins C and D, which have become essential for daily health maintenance rather than being used occasionally. Companies are marketing these drinks as convenient and effective ways to support immune health, making them a regular part of consumers' routines. The growing focus on preventive care and overall well-being has further boosted the demand for these products, positioning them as a vital segment in the health drinks market.

On the other hand, digestive-health applications are expected to grow at the fastest rate, with a projected CAGR of 8.28% through 2031. This growth is fueled by increasing consumer awareness of the importance of gut health and its connection to overall wellness, including immunity and mental health. Products containing probiotics, prebiotics, and fermented ingredients are gaining traction due to their scientifically proven benefits for digestion and gut balance. As more consumers seek beverages that promote gut health, this segment is becoming a key area of innovation and growth in the health drinks market. The rising demand for gut-friendly options highlights the shift toward functional drinks that address specific health concerns.

By Distribution Channel: Digital Commerce Transforms Retail Landscape

In 2025, hypermarkets/supermarkets accounted for 35.10% of the revenue, making them a key distribution channel in the health drinks market. These stores are popular because they offer a wide variety of products and frequently run promotions and discounts, which attract price-conscious consumers. Shoppers also benefit from the convenience of comparing different brands and purchasing products immediately. The physical presence of these outlets allows customers to inspect products firsthand, which builds trust and confidence in their purchases. As a result, hypermarkets and supermarkets continue to play a significant role in driving sales within the market.

Online retail is projected to grow at a CAGR of 7.75% through 2031, making it the fastest-growing distribution channel in the health drinks market. Features like influencer recommendations and the convenience of same-day delivery drive the growth of e-commerce. These factors make it easier for consumers to explore and purchase health drinks without visiting physical stores. Online platforms also provide detailed product descriptions, customer reviews, and personalized suggestions, enhancing the overall shopping experience. As more consumers embrace digital shopping, online retail is expected to significantly influence the market's growth in the coming years.

Geography Analysis

North America accounted for 36.10% of the health drinks market share in 2025, driven by high disposable incomes, a strong focus on health and wellness, and supportive regulations like the United States Food and Drug Administration's Generally Recognized as Safe framework. Consumers in the region are increasingly willing to spend on premium health drinks that offer innovative and clinically proven benefits. The presence of advanced research collaborations and nutraceutical start-ups has further strengthened the market, enabling the development of high-quality products. The region's well-established distribution networks and marketing strategies have made health drinks easily accessible to a wide audience. These factors collectively position North America as a leading market for health drinks.

Europe closely follows North America, supported by strong regulatory measures promoting sustainability and healthier product formulations. Governments in the region are actively encouraging manufacturers to reduce sugar content and adopt eco-friendly packaging solutions. This has led to the increased use of natural sweeteners and recycled materials, aligning with consumer preferences for environmentally friendly products. Transparency in product labeling and a focus on clean ingredients have also helped build consumer trust, driving steady growth in the market. With a growing demand for sustainable and health-focused beverages, Europe remains a significant contributor to the global health drinks market.

Asia-Pacific is the fastest-growing region, with a projected CAGR of 7.92% through 2031. The region's growth is fueled by rising incomes, urbanization, and increasing health awareness, particularly in countries like China, India, and Indonesia. Social media has played a key role in shaping consumer preferences, driving demand for health drinks that promote wellness and nutrition. Government initiatives, such as Japan's Foods with Function Claim (FFC) program and India's fortification campaigns, have further supported market expansion. Companies are also introducing products tailored to local nutritional needs, such as Abbott's PediaSure Nutri-Pull, which has gained popularity in the region. These factors make Asia-Pacific a critical driver of growth in the health drinks market.

Regulatory Landscape

Health drinks operate across overlapping food, supplement, and functional-claims regimes, so compliant labeling and claim substantiation tend to gate global rollouts. In the United States, FDA actions around front-of-pack messaging and its ongoing work toward a formal definition for ultra-processed foods are shaping how brands frame health positioning, while caffeine and energy-drink scrutiny continues to influence labeling and age-related sales policies. In the European Union, the Nutrition and Health Claims Regulation keeps a high bar for functional claims, including stricter substantiation expectations for botanicals, which is pushing manufacturers toward human-study evidence and more conservative on-pack language.

Regulatory divergence is also tightening operational requirements in key Asia-Pacific markets. China issued GB 7718-2025 (General Standard for the Labeling of Prepackaged Foods) in March 2025, with implementation set for March 16, 2027, prompting companies to plan artwork, ingredient naming, and claim structures ahead of the effective date. Packaging rules are another cross-cutting compliance driver, as Extended Producer Responsibility statutes adopted in several US states (including California, Oregon, Maine, and Minnesota) shift packaging cost burdens and reporting obligations to manufacturers, reinforcing the market move toward more recyclable and lower-impact formats.

Value Chain Analysis

The health drinks value chain runs from ingredient origination (fruit and vegetable inputs, dairy and plant proteins, probiotic cultures, botanicals, sweeteners, and functional actives), through formulation and validation, and then into specialized manufacturing such as aseptic processing, HPP for premium juices, and powder blending for functional hydration mixes. Aseptic processing capabilities are concentrated in hubs including China, Germany, and the United States, while co-packers and technology providers play an outsized role in scaling new functional SKUs quickly. Brand owners increasingly mix in-house production with outsourced capacity to shorten development cycles, while managing quality, shelf-life performance, and sensory stability for fortified formulations.

On the downstream side, distribution covers traditional retail and rapidly expanding online channels, supported by digital content, influencer marketing, and subscription or DTC models for targeted wellness use cases. Supply risk is most visible upstream for probiotic cultures and botanical extracts, where tariffs and geopolitical tensions have encouraged localized fermentation and more domestic sourcing. That shift increases the importance of supplier qualification, specifications, and audit-ready documentation. Investment in bottling and packaging infrastructure remains material to the chain, including Danone's April 2026 commitment of EUR 20 million to upgrade its Evian bottling facility, alongside EUR 8 million to preserve other French bottling sites, reflecting capacity and packaging execution for hydration and functional-water portfolios.

Competitive Landscape

The health drinks market remains moderately fragmented, with multinational companies maintaining their dominance while increasingly relying on mergers and acquisitions to stay competitive. For instance, PepsiCo acquired Poppi for USD 1.95 billion, and Keurig Dr Pepper purchased stakes in Ghost Energy for USD 990 million. These acquisitions highlight a trend where established players prefer buying innovative brands rather than developing new products in-house, especially as functional drink trends evolve rapidly. Ingredient suppliers are also focusing on gaining GRAS (Generally Recognized as Safe) certifications to secure a competitive edge. For example, PurGinseng has become a valuable ingredient for brands aiming to position themselves as premium in the market.

Technology is playing a crucial role in shaping the health drinks market, with investments directed toward advancements like microencapsulation, flavor-masking techniques, and blockchain for supply chain transparency. Brands are differentiating themselves by offering innovative products such as cold-pressed high-pressure processing (HPP) beverages, adaptogen-infused sparkling waters, and AI-personalized nutrition packs delivered directly to consumers. There is growing interest in therapeutic beverages, such as Nestlé’s GLP-1 drink, which targets specific health needs. Companies are also focusing on sustainability by introducing fully compostable packaging solutions, which appeal to environmentally conscious consumers.

Start-ups are using direct-to-consumer (DTC) channels and social media platforms to drive growth. For example, Celsius achieved triple-digit growth by partnering with fitness influencers on TikTok, while Lifeway’s collagen kefir blend capitalized on the rising demand for products that combine beauty and gut health benefits. The product development cycle has significantly shortened, with new products now reaching the market in just six months compared to the previous two years. This rapid pace of innovation is pushing established companies to adapt by creating venture studios, collaborating with co-packers, or risk falling behind. As consumer preferences become more sophisticated, the health drinks market is expected to see continuous innovation and intense competition.

Health Drinks Industry Leaders

-

PepsiCo, Inc.

-

The Coca-Cola Company

-

Nestlé S.A.

-

Danone S.A.

-

Red Bull GmbH

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

White space is expanding where brands can translate consumer health intent into products that meet tightening claim, sugar, and ingredient scrutiny. Low- and no-sugar reformulation creates a platform opportunity across juices, functional sodas, and ready-to-drink tea, supported by consumers actively reducing sugar intake, including the 2024 IFIC survey in the United States reporting 66% of Americans trying to reduce sugar. At the same time, compliance-ready functional positioning is driving investment in science-backed claims and proprietary ingredients, aligning with demand for clean labels and clinically supported benefits.

Innovation is clustering around gut health, protein-forward nutrition, and everyday hydration that blurs the line between sports drinks, functional waters, and better-for-you carbonated offerings. Company actions in 2025-2026 show how scale is being applied, with PepsiCo using the Poppi acquisition to deepen its presence in gut-health soda and continuing to broaden functional platforms across its portfolio. The Coca-Cola Company has also emphasized Zero Sugar and protein and hydration platforms such as Fairlife and Topo Chico. In parallel, Asia-Pacific programs that formalize functional claims and fortification, including Japan's Foods with Function Claim program and India's fortification campaigns, support structured pathways for localized formulations, particularly for dairy and plant-based drinks and digestive-health beverages that require clear benefit communication and robust documentation.

Recent Industry Developments

- June 2026: The Coca-Cola Company unveiled BODYARMOR FIT, its first-ever sparkling sports drink, designed for everyday hydration beyond athletic activity. The launch expands Coca-Cola's portfolio into everyday hydration, diversifying beyond traditional sports drinks.

- May 2026: PepsiCo Inc. launches Propel Clear Protein, a 3-in-1 powder containing 20g of protein, fiber, and electrolytes. The move expands high-protein hydration options and leverages PepsiCo's functional beverage footprint after the Poppi acquisition to capture the protein and fitness segment.

- April 2026: PepsiCo Inc. launches Pure Leaf Mental Focus iced tea, the brand's first functional iced tea line, containing naturally occurring L-theanine. The entry broadens PepsiCo's functional beverage portfolio with cognition-focused tea.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the health drinks market covers non-alcoholic beverages positioned with a health or wellness benefit. Revenue is measured as consumer sales revenue across the supply chain to retail.

Scope exclusions: We exclude pharmaceuticals and medical nutrition sold strictly under clinical supervision, along with alcoholic beverages and plain bottled water without a health positioning.

Segmentation Overview

-

By Product Type

- Fruit and Vegetable Juices

- Sports and Energy Drinks

- Herbal and Adaptogenic Drinks

- Meal Replacement Drinks

- Dairy and Plant-based Drinks

- Other Product Types

-

By Packaging Type

- Bottles

- Cans

- Tetra Packs

- Others

-

By Health Application

- Immunity Boosting

- Digestive Health

- Hydration and Recovery

- Other Applications

-

By Distribution Channel

- Hypermarkets / Supermarkets

- Specialty Stores

- Online Retail Stores

- Convenience Stores

- Other Channels

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

South America

- Brazil

- Colombia

- Chile

- Peru

- Argentina

- Rest of South America

-

Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Poland

- Belgium

- Sweden

- Rest of Europe

-

Asia-Pacific

- China

- Japan

- India

- Australia

- Indonesia

- South Korea

- Thailand

- Singapore

- Rest of Asia-Pacific

-

Middle East and Africa

- South Africa

- Saudi Arabia

- United Arab Emirates

- Nigeria

- Egypt

- Morocco

- Turkey

- Rest of Middle East and Africa

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by building a clear map of what counts as a health drink and how it is sold across regions, then aligns those products to consistent revenue measurement in USD. We rely on public and official sources that can be checked by anyone, including U.S. FDA labeling guidance, the European Commission food information rules, Codex Alimentarius standards, and trade statistics such as UN Comtrade.

To keep assumptions realistic, we also review national statistics office material for consumer spending proxies, World Bank and IMF macro series for inflation and currency context, and peer reviewed nutrition and food science literature for claim and ingredient direction. Company annual reports, investor presentations, and reputable press coverage are used to understand portfolio mix shifts and route-to-market changes. Where available, we use a paid subscription for company financials and a paid patent database to cross-check innovation intensity and category momentum. The sources listed here are illustrative, and additional references are used to collect data, validate it, and clarify open questions.

Primary Interviews and Surveys

Primary work is used to pressure-test the desk assumptions that matter most, especially how buyers define a health drink in each region and how pricing changes by pack format and channel. We speak with a mix of brand owners, ingredient and packaging participants, distributors, and retail or foodservice operators, then balance insights across APAC, EMEA, and the Americas so no single demand pattern over-drives the model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 36% | CXOs: 15% | APAC: 44% |

| Mid tier: 48% | Functional/Unit leaders: 32% | EMEA: 29% |

| Smaller Players: 16% | Managers: 53% | Americas: 27% |

Market-Sizing & Forecasting

Sizing starts from the top down, reconstructing consumption and category demand using region-level beverage spending indicators, trade flows where relevant, and observed category participation in modern and traditional channels. After shaping regional totals, we corroborate them with selective bottom-up checks, such as sampling average selling price ranges by pack type and channel, then multiplying by plausible volume bands. We compare the outputs with supplier and distributor channel feedback to see if the implied unit economics look consistent.

We track several inputs because they shift the market in visible ways and can be validated without relying on internal company systems. These include price and pack architecture shifts (single serve versus multi-pack), distribution mix (on-trade versus off-trade), claim intensity (immunity, energy, hydration, gut health), and the direction of dairy alternatives and ready-to-drink tea and coffee within health-oriented positioning. For forecasting, scenario analysis is used to reflect different inflation and premiumization paths, followed by expert-led adjustments on how quickly newer formats like kombucha or fortified waters expand in each region. Where a bottom-up check is thin in a country, we fill gaps using regional peer benchmarks, then re-check the implied per-capita spend and price ladder with interview inputs.

Data Validation & Update Cycle

Numbers are validated through multiple passes, with model outputs compared against independent signals such as trade direction, category growth commentary from public filings, and observed pricing movement in key markets. If a region shows an unusual swing, we trace it back to the driver assumptions, then re-contact relevant respondents to confirm whether it reflects a real change or a modeling artifact.

Before sign-off, another analyst reviews the calculation steps, the year-to-year bridges, and currency handling so final totals remain internally consistent. Reports are refreshed annually, and interim updates are made when material events occur, such as regulatory shifts on claims, large pricing shocks, or major channel disruptions. Right before delivery, a fresh pass is done so clients receive the most current view available at that time.

Mordor Intelligence's Global Health Drinks Market Size Measured Against Other Published Estimates

Published market values for health drinks can vary widely because the term is used loosely, and because some estimates blend adjacent beverage categories that are not always purchased for a health purpose. Differences also come from how analysts treat channel coverage, currency timing, and how quickly premium pricing is assumed to rise.

The benchmark table shows a noticeable spread that is mostly explained by scope and pricing logic, and then by how often assumptions are refreshed in fast-moving subcategories. The table also reflects that some publishers anchor on a broader functional drinks bucket, while others keep the lens narrow to a smaller set of labeled health drink formats, which changes the total even when growth rates appear similar.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 141.80 B (2026) | |

| Trade Journal A | USD 149.00 B (2026) | Uses a wider functional-drinks style definition that can fold in more everyday RTD beverages with light wellness cues, which expands the counted demand pool beyond strictly health-positioned drinks. |

| Regional Consultancy B | USD 130.00 B (2026) | Applies more conservative price progression and premiumization assumptions across key channels, and often reports with slower adoption of newer health formats, which keeps revenue totals lower. |

The table shows that part of the gap comes from what gets counted as a health drink, and in the Mordor Intelligence model the total is tied to beverages with explicit health positioning rather than a broader functional refreshment bucket. Once that scope is fixed, the remaining differences typically come down to how average prices are moved forward by channel and pack mix, and whether category shifts are re-validated as new products and claims enter the market.

Key Questions Answered in the Report

How big is the health drinks market in 2026?

The health drinks market size is USD 141.8 billion in 2026, on track to reach USD 200.06 billion by 2031 at a 7.12% CAGR.

Which region is expanding fastest for health drinks?

Asia-Pacific leads growth with a 7.92% CAGR, fueled by rising incomes, urban lifestyles, and amplified fitness culture.

What product segment is growing quickest?

Dairy and plant-based beverages are set to advance 7.32% annually through 2031 as consumers favor lactose-free and sustainable protein options.

How important is online retail in health-drink sales?

Online retail is the fastest-growing channel at a 7.75% CAGR, supported by influencer marketing, and richer product education.

Page last updated on: