Market Overview

| Study Period | 2021 - 2031 |

|---|---|

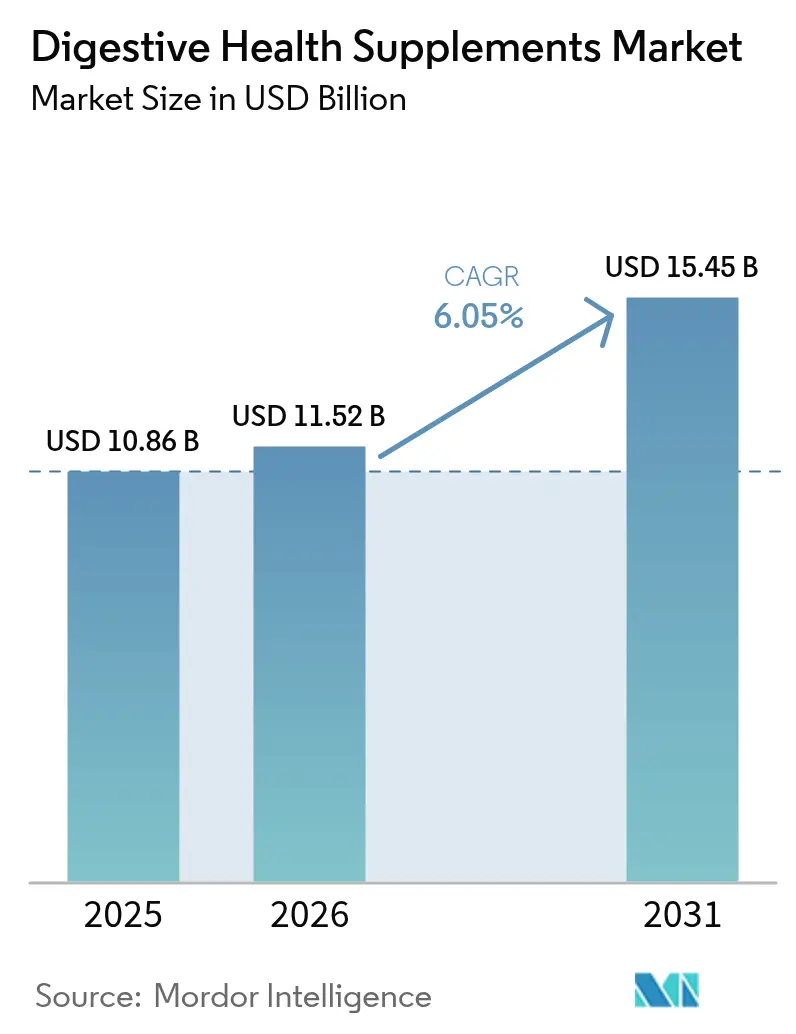

| Market Size (2026) | USD 11.52 Billion |

| Market Size (2031) | USD 15.45 Billion |

| Growth Rate (2026 - 2031) | 6.05% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Digestive Health Supplements Market Analysis by Mordor Intelligence

The Digestive Health Supplements market size is expected to grow from USD 10.86 billion in 2025 to USD 11.52 billion in 2026 and is forecast to reach USD 15.45 billion by 2031 at 6.05% CAGR over 2026-2031.

Preventive health attitudes, clinical validation of microbiome interventions, and heightened global oversight are driving momentum in the market. These factors are shaping consumer preferences and pushing the industry toward higher standards. Demand is bolstered by an aging population seeking metabolic support to manage age-related health concerns, younger consumers influenced by social media, uncovering the gut-immune connection and its impact on overall well-being, and companies rolling out data-driven personalization services to cater to individual health needs. Regulatory convergence, especially with the U.S. Food and Drug Administration's surprise inspections abroad, is bridging the historical quality divide between domestic and international facilities, fostering trust in the category by ensuring consistent product standards. Concurrently, attributes like clean-label positioning and transparent sourcing have transitioned from premium perks to essential standards, compelling brands to invest in traceable supply chains and third-party verifications to meet consumer expectations and regulatory requirements.

Key Report Takeaways

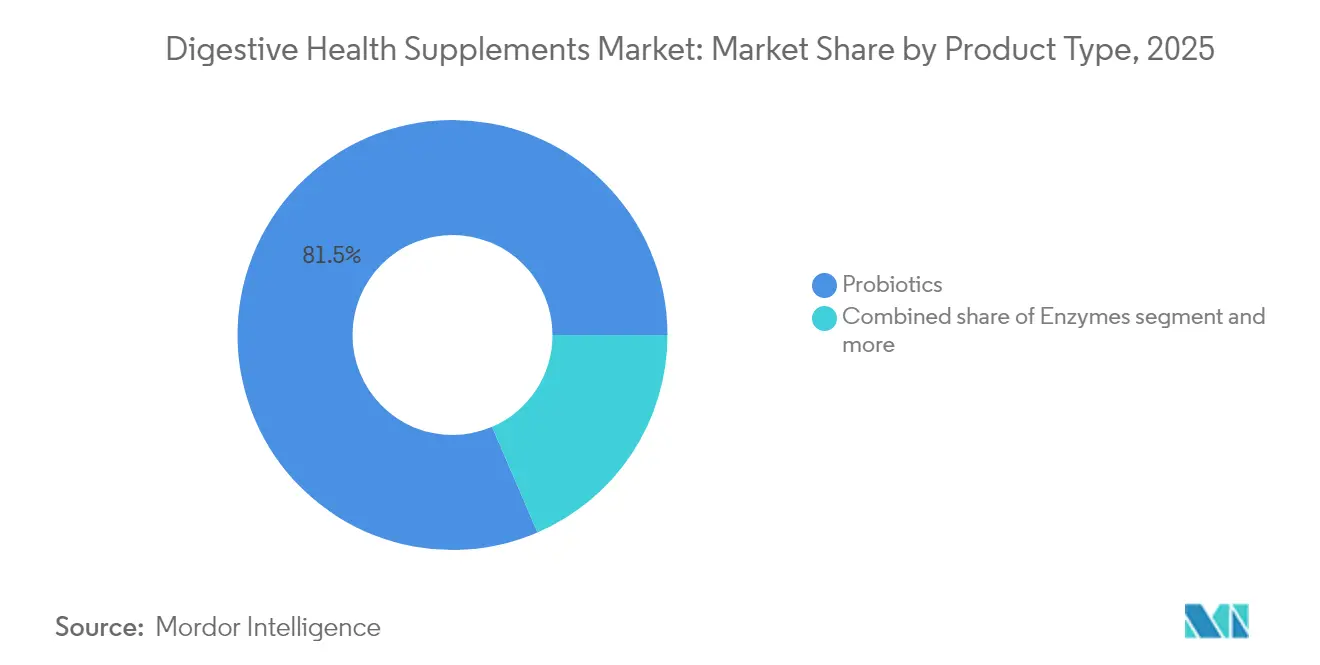

- By type, probiotics led with 81.47% of the digestive health supplements market share in 2025, while enzymes are projected to expand at a 7.34% CAGR through 2031.

- By form, capsules and soft gels accounted for 46.88% share of the digestive health supplements market size in 2025; gummies and chewables register the fastest growth at 7.08% CAGR to 2031.

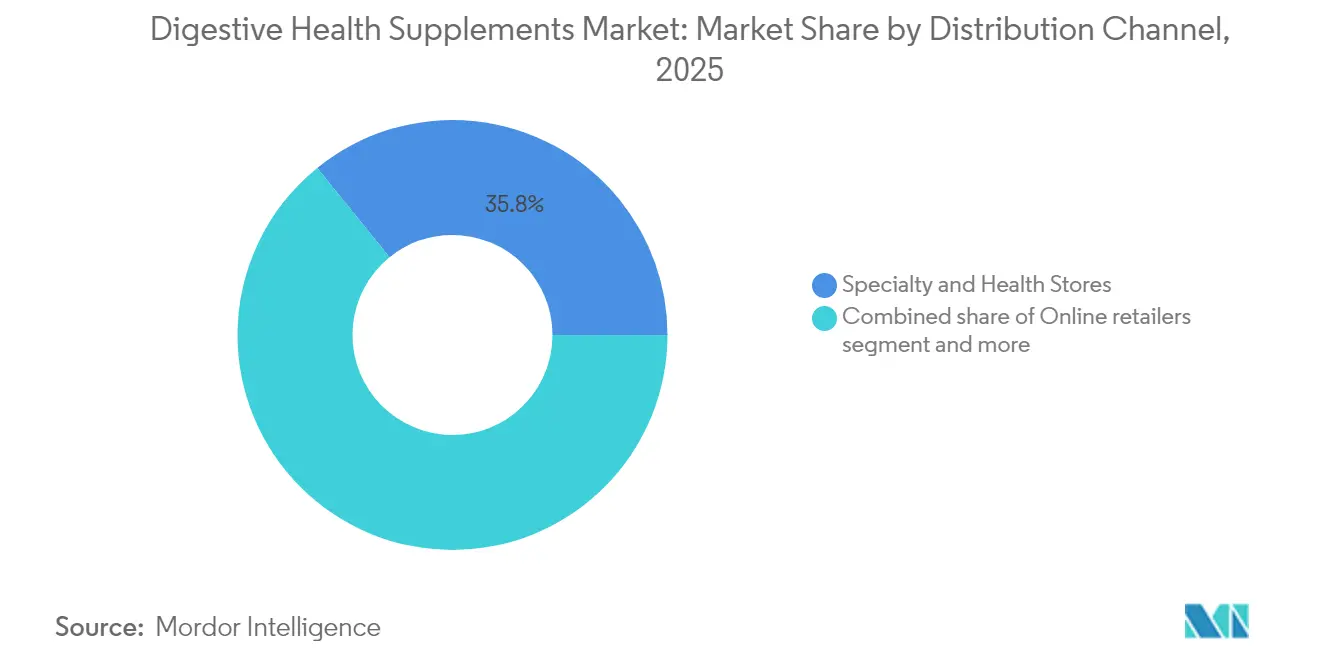

- By distribution channel, specialty, and health stores held a 35.83% share in 2025, whereas online retailers posted the strongest CAGR at 8.36% through 2031.

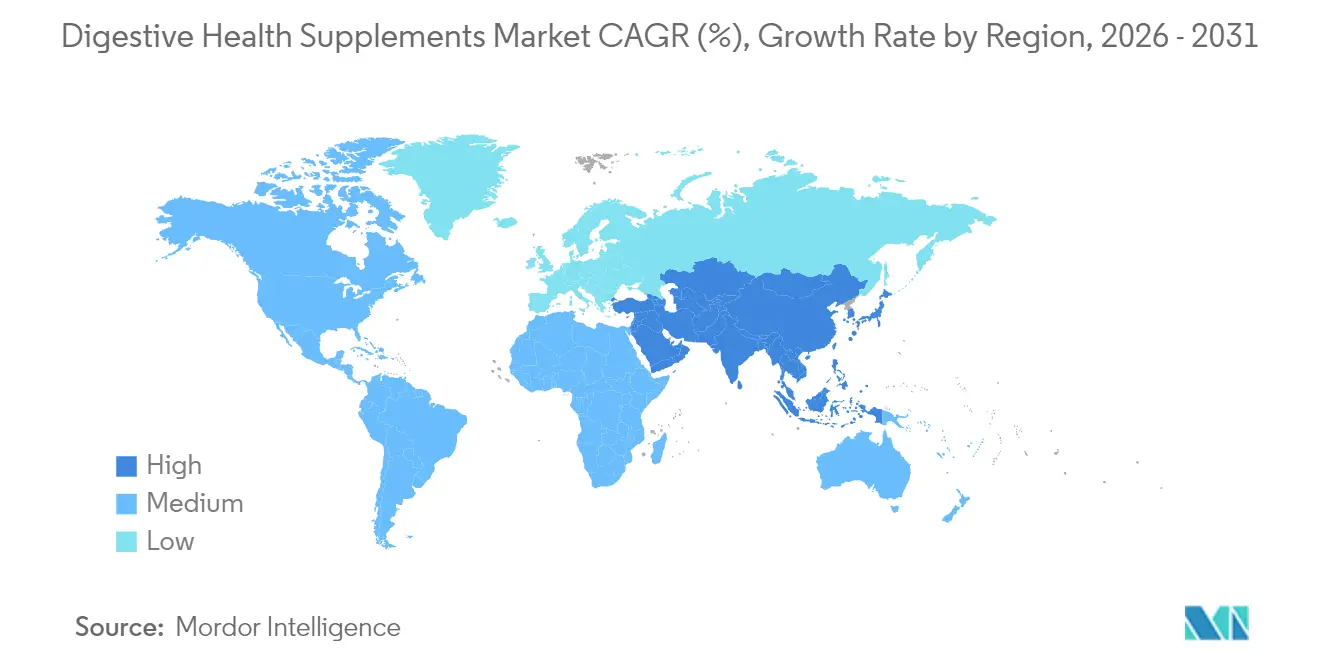

- By geography, North America captured a 41.84% share in 2025, and the Middle East and Africa region is poised for the quickest advance at 8.47% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Digestive Health Supplements Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising incidence of gastrointestinal disorders boosts growth | +1.8% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Increasing consumer awareness of the microbiome–immune axis drives demand | +1.2% | North America and EU, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Integration of digestive supplements into daily nutritional regimens drives growth | +0.9% | Global, led by developed markets | Short term (≤ 2 years) |

| Enhanced digestive health awareness through digital media platforms adds to its growth | +0.7% | Global, with Gen Z concentration in urban centers | Short term (≤ 2 years) |

| Increasing trend for clean-label and plant-based supplement formulations | +0.6% | North America and EU, spill-over to Asia-Pacific | Medium term (2-4 years) |

| Growing use of digestive aids among aging adults with slower metabolism | +0.5% | North America, Europe, Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Incidence of Gastrointestinal Disorders Boosts Growth

As functional gastrointestinal disorders rise in prevalence, supplements are transitioning from occasional remedies to staples in long-term health regimens. The World Health Organization reports over 1.7 billion annual cases of enteric diseases, with wealthier regions seeing a marked increase in inflammatory conditions [1]Source: World Health Organisation, "Diarrhoeal disease", www.who.int. With a growing number of individuals facing Irritable Bowel Syndrome, Gastroesophageal Reflux Disease, and lactose intolerance, the consumption of digestive supplements is on the rise. The National Institute of Diabetes and Digestive and Kidney Diseases notes that around 60 to 70 million Americans grapple with digestive diseases each year [2]Source: National Institute of Diabetes and Digestive and Kidney Diseases, "Digestive Statistics for the United States", niddk.nih.gov. Pharmaceutical giants, like Nestlé Health Science, are lending credibility to this sector, evidenced by their recent acquisition of Vowst. This is a pivotal move, as Vowst boasts the distinction of being the first FDA-approved oral microbiota therapy for recurrent C. difficile infections. With clinical evidence backing them, certain strains are swaying consumer preferences, moving them from casual trials to targeted treatments. This evolution not only ensures a steady demand—resilient even during economic slumps—but also opens avenues for premium pricing on scientifically validated products, elevating the market's value beyond mere volume growth.

Increasing consumer awareness of the microbiome–immune axis drives demand

Research underscores the gut's crucial role in immune health, prompting consumers to gravitate towards specific probiotic strains. Studies highlight how Akkermansia muciniphila strengthens gut barriers, curbs inflammation, and boosts metabolic health, driving the surge in demand for these specialized probiotics. This growing awareness of the gut microbiome's impact on overall health has led to increased interest in targeted interventions that address specific health concerns. In a shift post-pandemic, consumers are now placing a premium on preventive health measures rather than reactive treatments, as they aim to maintain long-term wellness and resilience against potential health challenges. Digital innovations, like Dieta Health's stool-imaging app, are adeptly converting biomarker data into personalized product suggestions, empowering consumers to make informed choices. These advancements in technology are bridging the gap between scientific insights and consumer accessibility, enabling individuals to better understand their unique health needs. As a result, there's a marked tilt towards supplements targeting specific health issues, with consumers favoring tailored solutions over one-size-fits-all alternatives.

Integration of digestive supplements into daily nutritional regimens drives growth

Consumers in developed markets are increasingly integrating digestive aids into their daily routines, blurring the lines between traditional supplements and functional foods. This trend is further fueled by innovative formats: sugar-free gummies and flavored powders enhance user adherence through their convenience and palatable taste, while prebiotic sodas elevate digestive ingredients to the forefront of mainstream beverages, appealing to health-conscious individuals seeking both health benefits and enjoyable consumption experiences. Additionally, the growing awareness of gut health's impact on overall well-being has driven demand for these products, encouraging manufacturers to invest in research and development for more effective and appealing solutions. As the digestive health supplements market merges with packaged foods, it broadens its distribution channels, spanning grocery stores to online platforms, and fortifies itself against seasonal demand shifts, ensuring steady market performance year-round.

Enhanced digestive health awareness through digital media platforms adds to its growth

Social media algorithms are increasingly favoring gut-health content, leading to viral loops that enhance understanding of the category through peer stories and expert insights. These algorithms amplify the visibility of gut-health discussions, making it easier for consumers to access and engage with relevant information. Discussions on TikTok have notably heightened searches for gummy formulations, particularly among Gen Z, who are drawn to convenient and palatable supplement options. This demographic's preference for innovative and easy-to-consume products has driven brands to focus on gummy supplements as a key growth area. Capitalizing on this trend, virtual-first providers such as Oshi Health are merging tele-consultations with tailored product bundles. This approach not only addresses consumer demand for personalized solutions but also broadens the reach of digestive health supplements beyond traditional brick-and-mortar stores, tapping into the growing preference for online health services and subscription-based models.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent labelling and novel-food approval delays for synbiotic blends hinder growth | -0.8% | EU primary, with regulatory spillover to other markets | Medium term (2-4 years) |

| Adulteration and potency degradation during supply chain affecting brand trust | -0.6% | Global, with concentration in cost-sensitive segments | Short term (≤ 2 years) |

| Price sensitivity limiting premium supplement uptake | -0.4% | Emerging markets, with selective impact in developed economies | Medium term (2-4 years) |

| Competition from alternative natural remedies affects growth | -0.3% | Global, With traditional medicine strongholds in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent labelling and novel-food approval delays for synbiotic blends hinders growth

Europe's Novel Foods Regulation requires detailed dossiers for botanical ingredients, but interpretations vary across member states. Gaining approval for multi-strain, multi-fiber synbiotics can take over 18 months, inflating development costs and postponing product launches. The complexity of the approval process, which involves rigorous safety assessments and compliance with varying national standards, further exacerbates these delays. Smaller companies find it challenging to finance these lengthy compliance processes, giving larger firms with seasoned regulatory teams a competitive edge. National actions, like Denmark's restrictions on ashwagandha, highlight how local decisions can override EU-wide approvals, necessitating region-specific reformulations that compromise economies of scale. These reformulations often require additional investment in research and development, further straining resources for smaller players.

Adulteration and potency degradation during supply chain affecting brand trust

Laboratory audits revealing underdosed products have shaken consumer confidence in the supply chain. Testing by NOW Foods found several berberine brands delivering less than 40% of their claimed active ingredients, raising concerns about product efficacy and transparency. Parallel audits of bromelain products noted even lower active levels, further highlighting inconsistencies in product quality. In response to these lapses, the FDA has ramped up inspections of foreign facilities, making unannounced visits to manufacturers in China and India. These inspections aim to bolster supply chain integrity by identifying and addressing non-compliance issues. However, they also lead to short-term disruptions, particularly for facilities that fail to meet regulatory standards and face subsequent actions. Such revelations have intensified calls for more stringent third-party verifications in the digestive health supplements market. These measures are seen as essential to restoring consumer trust and ensuring product quality. Additionally, compliant brands are being urged to prominently showcase their quality seals as a way to differentiate themselves in a competitive market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Probiotics Dominate Despite Enzyme Acceleration

In 2025, probiotics dominated the market, capturing 81.47% of the revenue. This highlights years of strain-specific research and growing consumer trust. Strong evidence supporting probiotics' efficacy has driven their widespread adoption for digestive health. Enzymes, projected to grow at a 7.34% CAGR through 2031, are gaining traction due to rising demand for solutions addressing lactose intolerance and pancreatic insufficiency. These enzymes cater to specific health needs, appealing to health-conscious consumers. The "Others" category now includes postbiotics and synbiotics, with Akkermansia muciniphila products receiving European Food Safety Authority approval in 2024. Such advancements are reshaping the digestive health supplements market, focusing on clinically validated solutions to meet emerging consumer demands.

With clinical backing, enzymes command premium prices and have established a presence in practitioner channels, where healthcare professionals recommend them. Probiotics are diversifying into age-specific and mood-enhancing formats, addressing mental well-being alongside digestive health. Manufacturers are investing in heat-stable strains, expanding their use into gummies and baked goods, thus entering the functional foods market. New entrants in the postbiotic sector emphasize shelf stability and immune benefits, reflecting the evolving competitive landscape. These innovations are expected to drive differentiation and growth as companies meet the rising demand for advanced, science-backed solutions.

By Form: Gummies Transform Compliance, Capsules Keep Scale

In 2025, capsules and soft gels held a 46.88% market share, remaining the top choice for high-dose actives due to precise dosage delivery and protection of sensitive ingredients. Gummies and chewables are growing at a 7.08% CAGR through 2031, driven by better taste, vegan pectin systems, and starch-free production lines that lower costs and increase accessibility. Tablets are declining as consumers prefer convenient formats, while powders are gaining traction among sports nutrition enthusiasts and clinics for their customizable, high-performance formulations. New entrants like liquid-filled gummies and sublingual films are enhancing bioavailability and carving unique positions in the digestive health supplements market.

Consumers increasingly view gummies as snacks rather than medicinal products, boosting daily adherence and appealing to a wider age demographic, including children and older adults. Brands are tapping into this trend, using natural colors, sugar-free sweeteners, and recyclable jars to meet clean-label demands and align with sustainability goals. On the other hand, capsules continue to be favored by those who prioritize science, valuing controlled dosages and advanced technologies, such as delayed-release mechanisms, that ensure strain survival against stomach acid and improve efficacy.

By Distribution Channel: E-commerce Redefines Access

In 2025, specialty and health stores captured 35.83% of global revenue by leveraging expert staff and curated product assortments. These stores attract health-conscious shoppers seeking tailored advice and premium offerings. Online retailers, benefiting from search convenience, peer reviews, and swift shipping, are projected to grow at an 8.36% CAGR through 2031. The rise of e-commerce, mobile commerce, and digital payment advancements is reshaping purchasing habits and driving online sales. Direct-to-consumer subscription models enhance lifetime value and data capture by ensuring consistent product access, fostering brand loyalty, and enabling brands to gather insights for product innovation in the digestive health supplement market.

Mass supermarkets and pharmacies cater to impulse buys and immediate needs, but omnichannel strategies are gaining prominence. Brands are adopting click-and-collect options, influencer partnerships, and educational webinars to ensure visibility across the shopper's journey. These strategies create a unified shopping experience across physical and digital channels, meeting evolving consumer expectations. Loyalty programs and personalized marketing campaigns further strengthen customer engagement. With cold-chain probiotics gaining popularity, efficient last-mile logistics are crucial to ensure product integrity and timely delivery. Investments in temperature-controlled supply chains and advanced tracking systems are becoming essential to meet growing demand.

Geography Analysis

North America commands a dominant 41.84% share of the global revenue, bolstered by clear FDA guidelines that empower assertive health-claim messaging. Consumers in the region increasingly view supplements as essential preventive care. According to the Council for Responsible Nutrition Survey 2023, nearly 74% of adults in the United States reported using dietary supplements, including digestive supplements . Furthermore, insurance pilots reimbursing microbiome therapeutics could solidify this trend, strengthening the digestive health supplements market in this already mature territory.

The Middle East and Africa are on a rapid ascent, boasting the fastest CAGR of 8.47% through 2031. This growth is fueled by increasing disposable incomes, the expansion of pharmacy chains, and proactive government health initiatives like Saudi Arabia's Vision 2030. With a youthful demographic and a deep-rooted cultural affinity for herbal tonics, the region is primed for the adoption of modern probiotics and enzymes. To navigate the diverse regulatory landscape and seamlessly blend Western formulations with indigenous botanicals, multinationals are forging partnerships with local distributors, setting the stage for a robust penetration of the digestive health supplements market.

Europe's regulatory environment offers both opportunities and challenges. EU-wide harmonization eases market access, but varying national interpretations create compliance hurdles. Sustainability mandates are driving a shift to organic ingredients and recyclable packaging. While consumers cautiously evaluate scientific evidence, they are willing to invest in proven products. In Asia-Pacific, traditional remedies merge with modern science, driving rapid adoption. China's regulatory framework accelerates imports via cross-border e-commerce while supporting domestic innovation. Urbanization and dietary shifts toward high-protein, low-fiber diets are boosting demand for tailored digestive solutions. Personalized nutrition services, integrating genetic and microbiome insights, further enhance the market's growth.

Competitive Landscape

The digestive health supplements market exhibits moderate fragmentation. Leadership is spread out, enabling specialized entrants to carve out niches using novel strains, advanced delivery technologies, and personalized programs. Acquisitions in the sector tend to focus on enhancing complementary capabilities rather than seeking direct overlaps. Major players in the market include Neste SA, Bayer AG, Amway Corp., Haleon plc, and Herbalife Nutrition Ltd.

Technology is carving out a significant niche in this market. While larger players leverage their e-commerce platforms to amplify these digital services, start-ups are finding success with subscription models, offering microbiome sequencing kits and app-based coaching. Another competitive front is supply-chain transparency; companies are increasingly using blockchain tracking to validate strain viability and origin, addressing consumer concerns stemming from periodic potency scandals.

Agility is key in navigating the swift currents of innovation cycles and evolving regulations, particularly in Europe. To adeptly guide synbiotic blends through the stringent Novel Foods pathway, companies are establishing dedicated regulatory affairs teams. Early approvals not only command a pricing premium but also ensure shelf exclusivity, creating a self-reinforcing loop that fuels further investment in clinical trials. In a sign of the market's evolution, traditional pharmaceutical giants are beginning to bundle microbiome therapeutics with standard over-the-counter digestive solutions, hinting at a deeper integration within the digestive health supplements arena.

Digestive Health Supplements Industry Leaders

-

Neste SA

-

Bayer AG

-

Amway Corp.

-

Herbalife Nutrition Ltd.

-

Haleon plc

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Quality and compliance are creating a clear whitespace for brands and CDMOs that can verify strain identity, potency, and label accuracy at scale, particularly as oversight tightens and consumer trust hinges on reproducibility. The rollout of faster, in-house QC tools such as bioMérieuxs GENE-UP PROBIOTIC SPECIES ID (launched July 2026) supports a shift from periodic third-party testing to routine batch-level verification, which favors manufacturers with stronger analytics, documentation, and traceability. Parallel investments in specialized production footprints, including Vidyas 28,750-square-foot probiotic facility in Bunnell, Florida (opened April 2026) and Vitaquests probiotics suite expansion in Parsippany, New Jersey (February 2026), reinforce opportunities in differentiated manufacturing models that protect viability (for example, separate lines for spore-forming versus non-spore-forming probiotics).

Portfolio expansion is increasingly centered on prebiotic fibers, synbiotics, and precision formulation capabilities that connect supplements with functional-food and beverage adjacencies. Ingredions June 2026 acquisition of NutriLeads Benicaros prebiotic fiber asset package (IP, clinical work, and know-how) and Samyangs debut of Fibernova (a crystalline prebiotic fiber positioned as 99% fructooligosaccharides) at IFT First 2026 highlight active ingredient innovation and ownership of clinically supported fiber platforms. Alongside this, AI-enabled formulation approaches, such as Enbiosis Biotechnologys digital-twin positioning for designing precision microbiome formulations (June 2026), create room for more targeted products and personalization services, especially in online and subscription channels where brands can pair biomarker-led coaching with repeat purchasing.

Recent Industry Developments

- July 2026: Amway announced the launch of a new probiotic product tailored for the South Korean market, featuring exclusive strains positioned for local gut health needs. The move reinforces competitive intensity in Asia-Pacific, where large direct-selling players use localized microbiome narratives and established member networks to accelerate adoption.

- May 2026: Nestle Health Science entered a licensing agreement with IdB Holding S.p.A. to develop and commercialize VOWST in Europe, subject to European Medicines Agency approval. This links the supplements ecosystem more tightly with regulated microbiome therapeutics and raises the bar for evidence, quality systems, and market access capabilities in Europe.

- August 2024: Organic India introduced certified organic Fiber Gummies and Ashwagandha Gummies in glass jars, emphasizing prebiotic fiber delivery with low sugar and clean-label positioning. The launch underscores how format innovation and transparent packaging cues are being used to broaden everyday compliance, particularly in gummy and chewable segments.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers dietary supplements positioned for digestive comfort and gut health, sold in consumer-packaged formats across retail and online channels. Revenues are counted at the point of sale in value terms (USD) for the defined products.

Scope exclusions: Prescription gastrointestinal drugs are excluded, along with general foods and beverages that are not marketed and sold as supplements.

Segmentation Overview

-

By Type

- Prebiotics

- Probiotics

- Enzymes

- Botanicals

- Other Types

-

By Form

- Capsules and Softgels

- Tablets

- Gummies and Chewables

- Powders

- Other Forms

-

By Distribution Channel

- Supermarkets/Hypermarkets

- Specialty and Health Stores

- Online Retailers

- Other Distribution Channels

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

Europe

- Germany

- United Kingdom

- Italy

- France

- Spain

- Netherlands

- Poland

- Belgium

- Sweden

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- Australia

- Indonesia

- South Korea

- Thailand

- Singapore

- Rest of Asia-Pacific

-

South America

- Brazil

- Argentina

- Colombia

- Chile

- Peru

- Rest of South America

-

Middle East and Africa

- South Africa

- Saudi Arabia

- United Arab Emirates

- Nigeria

- Egypt

- Morocco

- Turkey

- Rest of Middle East and Africa

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research is used to set market boundaries and build the first pass of the demand and supply picture. Public sources include the US FDA (dietary supplement labeling and enforcement actions), NIH Office of Dietary Supplements fact sheets, the US CDC (digestive health indicators that inform demand context), and the World Health Organization for broader health and nutrition signals.

To map products to real-world selling conditions, we also rely on company annual reports, investor presentations, press releases, and reputable retail and trade articles to track product launches and pricing direction by form (capsules, tablets, gummies, powders). A paid subscription for company financials and intelligence, plus a paid patent database, are also used in a limited way to confirm corporate exposure to digestive health supplements and to spot active innovation themes. These are illustrative sources only, and other public references are used as needed for data collection, cross-checking, and clarification.

Primary Interviews and Surveys

Primary input is used to pressure-test what desk research cannot reliably show, especially how products are classified, where pricing is moving, and how channel mix is shifting between pharmacies, specialty stores, and online retail. We speak with manufacturers, ingredient-focused participants, distributors, and channel-side experts across APAC, EMEA, and the Americas, and then incorporate that feedback to adjust assumptions and close data gaps that show up in the model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 37% | CXOs: 15% | APAC: 51% |

| Mid tier: 42% | Functional/Unit leaders: 39% | EMEA: 29% |

| Smaller Players: 21% | Managers: 46% | Americas: 20% |

Market-Sizing & Forecasting

The core market build starts with a top-down approach, where we reconstruct demand using the supplement consumer base and usage rates, then convert that into value using typical pack prices by form and channel. After this structure is in place, selective bottom-up approximations are used to keep it realistic, such as rolling up a sample of supplier revenues, checking channel mix shifts, and validating a few price points across key countries.

For digestive health supplements, the inputs that matter most include supplement penetration for gut health claims, the share of probiotics, prebiotics, enzymes, and botanicals within digestive use, average selling prices by form (capsules, tablets, gummies, powders), the online retail share versus store-based channels, and country-level currency movements that can change reported USD value. When local splits are hard to obtain, the gap is handled by applying conservative proxy ratios from similar markets, followed by expert checks before those ratios are allowed into the final totals.

Forecasts are produced using scenario analysis. A base case is built from expected shifts in channel mix, pricing direction, and category preference, and mild upside and downside cases are used to test sensitivity to those inputs. The final path is selected only after it matches what interviewees see for consumer demand and what desk research indicates from product and channel activity.

Data Validation & Update Cycle

Validation is done in several passes, so the numbers do not rely on a single assumption. We compare the model outputs with independent signals such as regional supplement spending patterns, direction of price changes by form, and whether channel shares are moving in line with public disclosures and expert feedback.

If a variance looks unusual, such as a sudden regional jump that is not supported by pricing or distribution expansion, the assumption is re-checked and respondents may be re-contacted for clarification. Before sign-off, the work is reviewed by another analyst to catch logic breaks and unit conversion errors, and the report is refreshed annually with interim updates if a material event changes the outlook. Right before delivery, a final pass is completed to ensure the latest information is reflected in the model and narrative.

Mordor Intelligence's Digestive Health Supplements Market Sizing Compared With Other Published Estimates

Published market values for digestive health supplements can differ widely because studies do not always count the same product set, sales channels, or time periods. Differences also appear when one publisher reports retail sales value, while another uses a broader health and wellness spending view.

The spread typically comes from scope choices, for example whether botanicals positioned for digestion are included, how synbiotics are treated within probiotics or as a separate bucket, and whether online retail is modeled with the same price and promotion logic as store channels. It also depends on USD conversion, including whether a single-year exchange rate is used, and whether the base year is refreshed when form mix shifts toward gummies and powders, which can raise average prices without a similar volume jump.

By separating digestive health supplements by type and form, and then re-checking channel mix and USD conversion in the base year update, the estimate stays tied to what is actually sold in the market, which is the approach used by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 11.52 B (2026) | |

| Industry Publisher A | USD 19.30 B (2025) | Uses an earlier base year and a broader interpretation of digestive health positioning across demographics and benefits, and the higher value can also reflect different treatment of adjacent wellness claims within supplement listings. |

| Market Tracker B | USD 9.24 B (2023) | Anchors the series on an older base year and provides limited visibility on how product forms and newer channel mix changes are priced into the estimate, which can compress the reported value in fast-shifting categories. |

The table indicates that timing, scope, and pricing logic are the practical drivers behind the differences in reported values. The estimate is maintained by aligning the scope and then re-checking channel mix and USD conversion during the base year update, so the totals reflect what is actually sold in the market.

Key Questions Answered in the Report

What is the current value of the digestive health supplements market?

The digestive health supplements market size is valued at USD 11.52 billion in 2026.

Which segment holds the largest share of the digestive health supplements market?

Probiotics dominate with 81.47% of global revenue in 2025, supported by extensive clinical research.

Which region is growing fastest in the digestive health supplements market?

The Middle East and Africa is projected to grow at an 8.47% CAGR between 2026 and 2031.

Why are gummies gaining popularity in digestive health products?

Gummies offer palatable flavors, vegan pectin options and convenience, driving a 7.08% CAGR through 2031.

Page last updated on: