Beverage Stabilizers Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

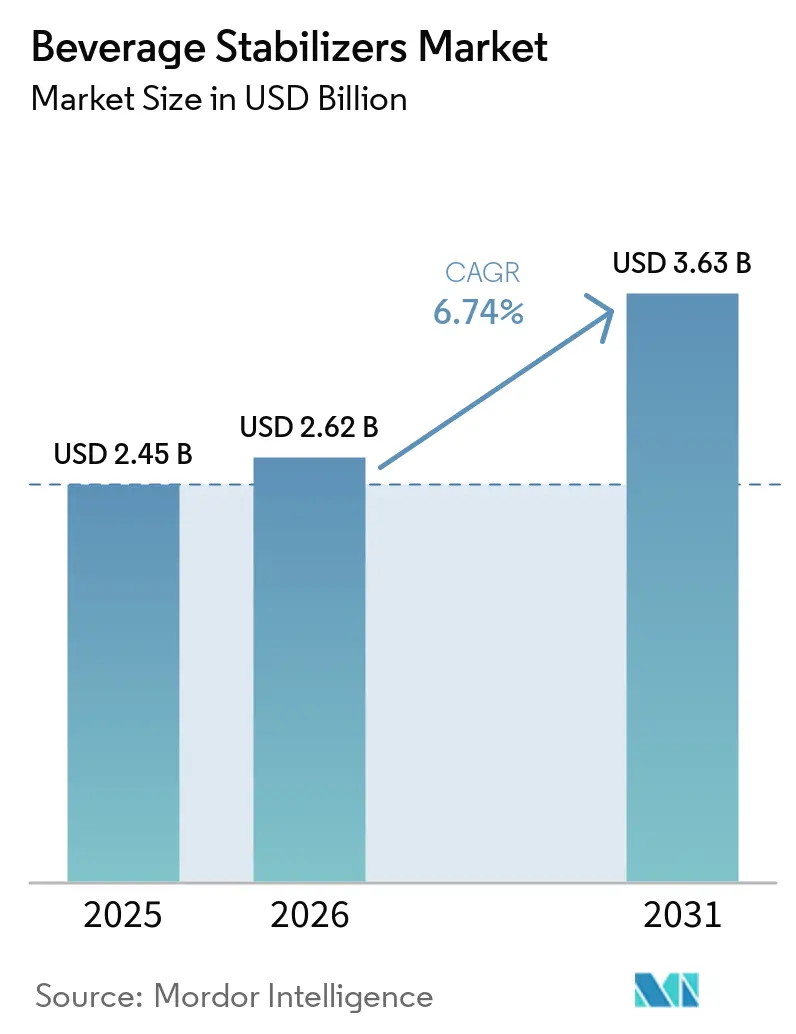

| Market Size (2026) | USD 2.62 Billion |

| Market Size (2031) | USD 3.63 Billion |

| Growth Rate (2026 - 2031) | 6.74% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Beverage Stabilizers Market Analysis by Mordor Intelligence

The beverage stabilizers market size is projected to grow from USD 2.45 billion in 2025 to USD 2.62 billion in 2026 and is anticipated to reach USD 3.63 billion by 2031, registering a CAGR of 6.74% during the forecast period of 2026-2031. This growth is primarily driven by the increasing demand for ready-to-drink beverages, plant-based dairy alternatives, and functional drinks. These products depend on stabilizers to ensure stable suspension, regulate viscosity, and provide a consistent mouthfeel, even under challenging conditions such as heat stress and aseptic processing. Moreover, the market is witnessing a significant shift as beverage manufacturers transition from synthetic and semi-synthetic inputs to botanical and fermentation-derived hydrocolloids. Suppliers offering multi-component stabilizer blends are emerging as key players, as beverage producers increasingly view stabilizer systems as essential formulation tools that enhance sensory quality and strengthen brand positioning. In these segments, attributes such as stable texture, visual consistency, and effective ingredient suspension are critical differentiators compared to standard beverage lines. The market remains moderately consolidated, with key players focusing on innovation and strategic partnerships to maintain competitiveness.

Key Report Takeaways

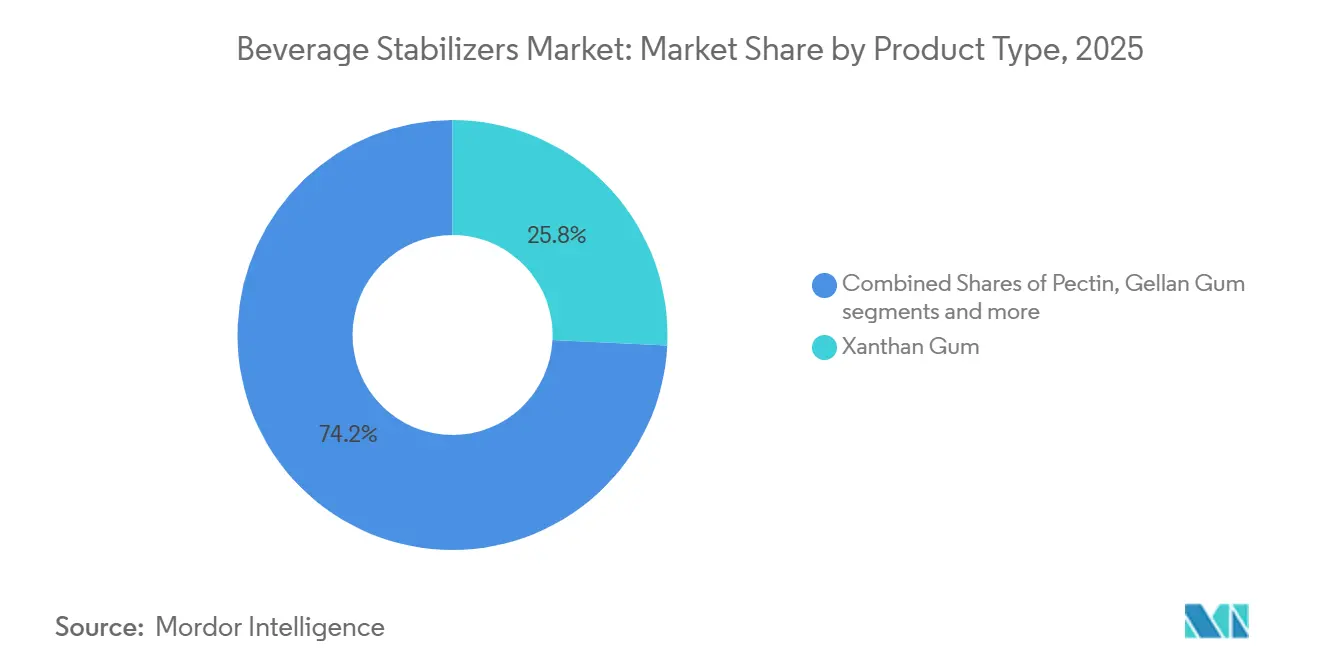

- By product type, xanthan gum led with 25.78% revenue share in 2025, while pectin is forecast to expand at a 7.42% CAGR through 2031.

- By form, powder held 73.67% share in 2025, while liquid stabilizer concentrates recorded the highest projected CAGR at 8.03% through 2031.

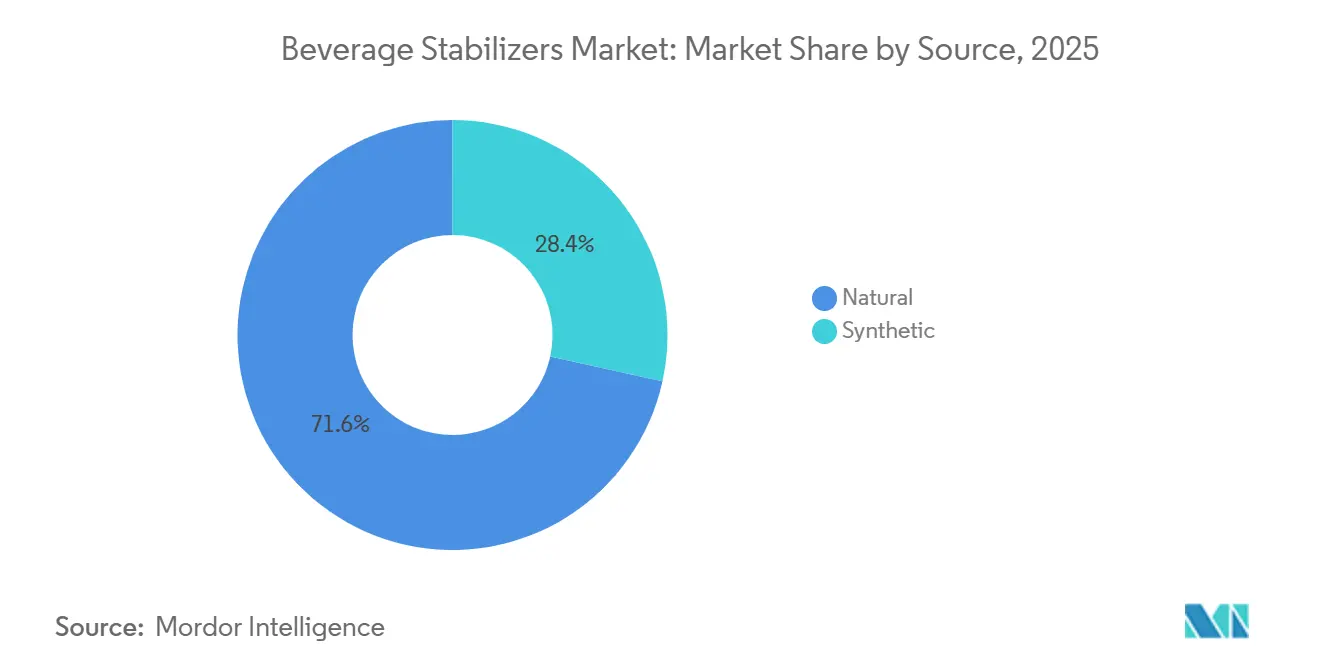

- By source, natural stabilizers accounted for 71.55% share in 2025, while synthetic stabilizers are projected to grow at a 7.54% CAGR through 2031.

- By functionality, stabilization captured 62.15% of the market in 2025, while viscosification is advancing at a 7.61% CAGR through 2031.

- By end use, fruit and vegetable drinks held 52.61% share in 2025, while sports and energy drinks are forecast to grow at an 8.27% CAGR through 2031.

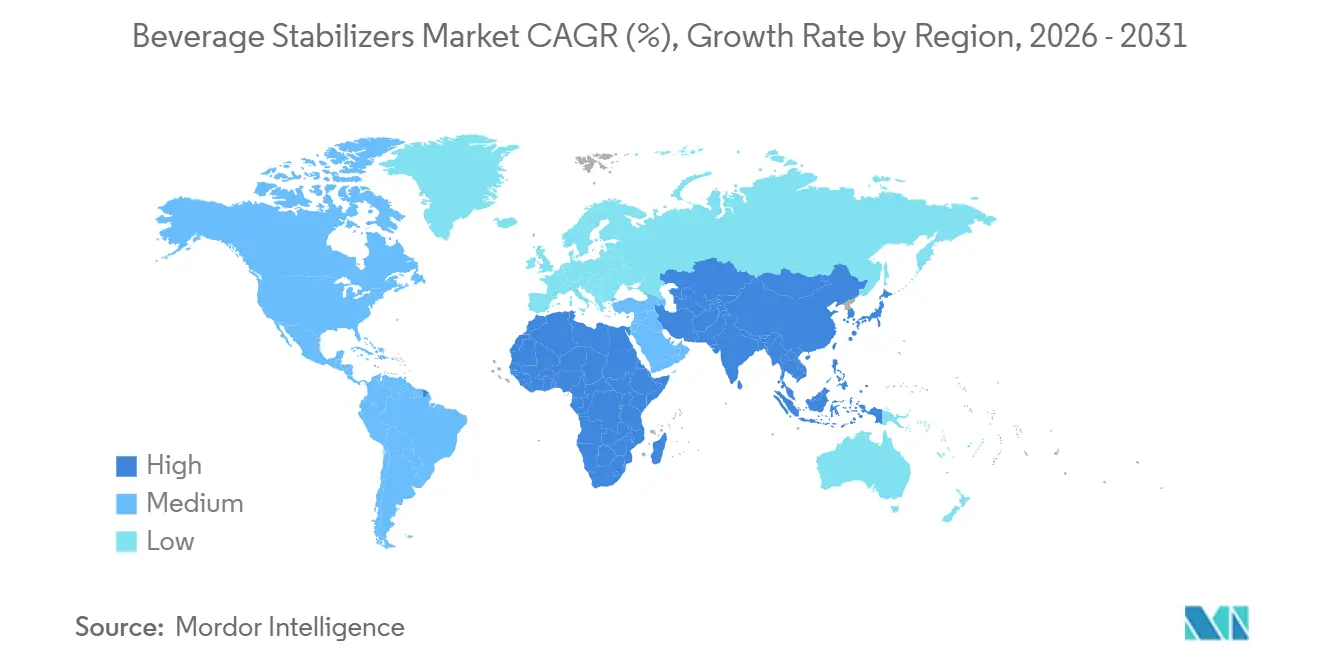

- By geography, North America held 32.46% share in 2025, while the Asia-Pacific is projected to grow at a 7.09% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Beverage Stabilizers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing consumer preference for ready-to-drink beverages | +1.8% | Global | Short term (≤ 2 years) |

| Growing focus on clean-label and natural ingredients encouraging use of plant-derived stabilizers | +1.5% | North America and Europe, spill-over to Asia-Pacific | Medium term (2–4 years) |

| Demand for functional and fortified beverages increasing the need for stabilizers | +1.2% | Global | Medium term (2–4 years) |

| Rising consumption of protein beverages and nutritional drinks | +0.9% | North America, Europe, Asia-Pacific | Medium term (2–4 years) |

| Continuous innovation in beverage formulations driving demand for multifunctional stabilizers | +0.8% | Global | Long term (≥ 4 years) |

| Demand for shelf-stable beverages with extended storage life | +0.6% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Increasing consumer preference for ready-to-drink beverages

The increasing demand for ready-to-drink (RTD) beverages is driving significant growth in the global beverage stabilizers market. Modern consumers prioritize convenience, seeking beverages that are easy to consume on the go, which has led to a surge in demand for RTD products such as tea, coffee, energy drinks, functional beverages, and flavored water. These products rely heavily on stabilizer systems to ensure consistent texture, visual appeal, ingredient suspension, and overall product quality throughout their shelf life and distribution processes. As beverage manufacturers continue to diversify their RTD offerings across various packaging formats, the need for advanced and efficient stabilizers has grown substantially. Additionally, the expansion of convenience retail channels, the proliferation of vending machine networks, and the rising popularity of health-oriented beverage options are prompting producers to adopt innovative stabilization solutions. These solutions not only extend shelf life but also enhance the sensory experience for consumers, thereby contributing to the sustained growth of the beverage stabilizers market.

Growing focus on clean-label and natural ingredients is encouraging the use of plant-derived stabilizers

The increasing demand for clean-label products is significantly driving the global beverage stabilizers market. Consumers are prioritizing transparency in ingredient sourcing, driving beverage manufacturers to adopt plant-based stabilizers such as pectin, gum arabic, and gellan gum. These naturally derived stabilizers align with the growing preference for minimally processed and easily recognizable ingredients. According to the International Food Information Council (IFIC) Food & Health Survey 2025, approximately 25% of Americans associate healthy food with limited or no artificial ingredients or preservatives[1]Source: International Food Information Council, "2025 IFIC Food & Health Survey", ific.org. This trend underscores the importance of clean-label formulations in shaping consumer purchasing behavior. In response, beverage producers are reformulating their offerings to incorporate natural stabilizers that not only enhance texture, suspension, and shelf life but also support clean-label claims. This shift is enabling brands to cater to health-conscious consumers while strengthening their market positioning in an increasingly competitive landscape.

Demand for functional and fortified beverages is increasing the need for stabilizers

The rising demand for functional and fortified beverages is driving significant growth in the global beverage stabilizers market. Consumers are increasingly gravitating toward beverages enriched with proteins, vitamins, minerals, probiotics, and botanical ingredients, which have introduced greater formulation challenges for manufacturers. These nutrient-rich ingredients often lead to sedimentation, phase separation, and texture inconsistencies, necessitating the use of advanced stabilization systems to maintain product quality, consistency, and an extended shelf life. A 2026 study published in Foods, an open-access journal by the Multidisciplinary Digital Publishing Institute (MDPI), demonstrated that microcrystalline cellulose (MCC) at a concentration of 0.35% (w/v) delivered optimal stabilization performance in vitamin-fortified protein beverages[2]Source: Multidisciplinary Digital Publishing Institute, "Enhancing Stability of Vitamin-Fortified Protein Beverages: Optimization of Stabilizer Type and Concentration and Screening of Natural Antioxidant Combinations", mdpi.com. This underscores the critical role of innovative stabilizer systems in addressing the complexities of nutrient-enriched formulations. As the market for sports nutrition drinks, functional waters, protein beverages, and wellness-oriented products continues to grow, demand for specialized, high-performance beverage stabilizers is expected to rise steadily, further shaping the market landscape.

Rising consumption of protein beverages and nutritional drinks

The increasing demand for protein beverages and nutritional drinks is a key driver of the global beverage stabilizers market. Consumers are becoming more health-conscious, focusing on protein intake to support fitness goals, weight management, and overall well-being. This trend has led to a surge in demand for ready-to-drink protein shakes and fortified nutritional beverages. According to the International Food Information Council (IFIC) Food & Health Survey 2025, approximately 70% of Americans actively seek to include protein in their diets, underscoring the growing consumer preference for protein-enriched products[3]Source: International Food Information Council, "2025 IFIC Food & Health Survey", ific.org. These beverages often face challenges such as protein sedimentation, phase separation, and texture inconsistencies, which necessitate the use of advanced stabilizer systems. These systems play a critical role in maintaining protein suspension, ensuring a smooth texture, and preserving product quality throughout its shelf life. As manufacturers continue to innovate and expand their offerings of dairy- and plant-based protein beverages, demand for specialized stabilizers that enhance stability, sensory attributes, and overall product performance is expected to grow significantly in the coming years.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fluctuating prices of raw materials such as hydrocolloids, gums, and starches | -1.2% | Global | Short term (≤ 2 years) |

| Stringent food safety and labeling regulations across different countries | -0.8% | Europe, North America, Asia-Pacific | Medium term (2–4 years) |

| Availability of alternative formulation technologies and ingredient systems | -0.6% | Global | Long term (≥ 4 years) |

| Demand for minimally processed beverages with fewer additives may limit stabilizer usage | -0.4% | North America and Europe | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Fluctuating prices of raw materials such as hydrocolloids, gums, and starches

Fluctuations in the prices of essential raw materials, including hydrocolloids, gums, starches, seaweed, and citrus-derived ingredients, pose a significant challenge to the global beverage stabilizers market. The production of these stabilizers relies heavily on agricultural and natural feedstocks, which are highly susceptible to external factors such as adverse weather conditions, geopolitical tensions, supply chain disruptions, and fluctuating energy costs. These factors can lead to inconsistent availability and unpredictable pricing of raw materials, thereby increasing manufacturers' production costs. Furthermore, the geographic concentration of production for certain stabilizers, such as seaweed-derived carrageenan, exacerbates supply risks and intensifies price volatility. This situation creates additional pressure on manufacturers to manage profit margins while maintaining competitive pricing. Such instability not only hampers beverage formulators' ability to secure a reliable supply of ingredients but also impacts the overall growth potential of the beverage stabilizers market.

Stringent food safety and labeling regulations across different countries

Strict food safety, labeling, and additive regulations across various countries significantly constrain the global beverage stabilizers market. Manufacturers and ingredient suppliers are required to comply with various regulatory frameworks governing the use, approval, labeling, and traceability of beverage stabilizers. This compliance process often leads to extended product development timelines and increased operational costs. Regulatory disparities among key regions, such as North America, Europe, and Asia-Pacific, compel companies to develop region-specific documentation, testing protocols, and formulation strategies for identical products. Furthermore, ongoing reviews and evolving standards for certain food additives, such as carrageenan, introduce uncertainty and may necessitate reformulation of existing products. These regulatory challenges not only delay market entry but also escalate costs for manufacturers aiming to launch products across multiple international markets. As a result, navigating these complexities has become a critical factor for companies operating in the beverage stabilizers market, affecting their ability to scale operations and maintain global competitiveness.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Xanthan Gum Dominance Coexists with Pectin's Clean-Label Rise

Xanthan gum has established itself as the largest product segment in the beverage stabilizers market, accounting for 25.78% of total market revenue in 2025. Its dominance is attributed to its superior ability to thicken, suspend, and control viscosity, ensuring consistent beverage texture and stability. This ingredient is widely used across a range of applications, including juices, dairy beverages, sports drinks, and ready-to-drink products, due to its efficiency at low concentrations and compatibility with diverse beverage formulations. The growing focus on maintaining product quality and extending shelf life continues to drive demand for xanthan gum.

Pectin is projected to be the fastest-growing product segment, with a 7.42% CAGR during the forecast period of 2026-2031. This growth is fueled by consumers' growing preference for natural, clean-label ingredients, as pectin is predominantly sourced from citrus and apple fruits. Beverage manufacturers are increasingly incorporating pectin into fruit-based drinks, plant-based beverages, and functional formulations to enhance stability and mouthfeel while aligning with consumer preferences for natural ingredient profiles. The growing demand for healthier, minimally processed beverages is expected to further boost the adoption of pectin in the coming years.

By Form: Powder Dominates, Liquid Concentrates Redefine Processing Economics

Powder stabilizers held the largest share of the global beverage stabilizers market in 2025, accounting for 73.67% of the form segment. Their dominance is primarily due to their extended shelf life, ease of storage, and cost-efficient handling during production processes. These stabilizers are widely used across beverage categories, including soft drinks, dairy-based beverages, juices, and functional drinks, owing to their ability to deliver consistent results and adapt to formulations. Additionally, their compatibility with large-scale manufacturing operations has solidified their position as the preferred choice among beverage producers.

Liquid stabilizer concentrates are anticipated to be the fastest-growing segment, with a projected CAGR of 8.03% from 2026 to 2031. This growth is fueled by the rising demand for ready-to-use ingredient solutions that streamline beverage production and reduce preparation time. Liquid stabilizers offer superior dispersion and ease of integration into formulations, making them particularly suitable for high-volume production environments. As manufacturers increasingly prioritize operational efficiency and simplified processes, the adoption of liquid stabilizer concentrates is expected to gain significant momentum during the forecast period.

By Source: Natural Leads by Volume, Synthetic Segment Grows from a Value-Add Niche

In 2025, natural stabilizers dominated the beverage stabilizers market, accounting for 71.55% of the market share. This dominance is attributed to the increasing consumer demand for clean-label products that prioritize plant-based, minimally processed, and sustainable ingredients. Commonly used natural stabilizers, such as pectin, guar gum, xanthan gum, and carrageenan, play a crucial role in enhancing texture, stability, and shelf life in beverage formulations. The growing focus on health and wellness trends continues to drive the adoption of natural stabilizers, solidifying their position as the leading segment in the market.

Synthetic stabilizers, while holding a smaller market share, are projected to grow the fastest, with a CAGR of 7.54% from 2026 to 2031. Their rising adoption is driven by consistent performance, cost-effectiveness, and the ability to meet specific formulation needs. These stabilizers are particularly favored in applications that require enhanced stability, tolerance to processing conditions, and reliable performance across diverse storage environments. As beverage manufacturers continue to innovate and develop increasingly complex formulations, demand for synthetic stabilizers is expected to grow significantly over the forecast period.

By Functionality: Stabilization Leads by Volume, Viscosification Leads by Growth

Stabilization has established itself as the leading functionality segment in the global beverage stabilizers market, accounting for 62.15% of total revenue in 2025. This segment's prominence stems from the essential role stabilizers play in ensuring product consistency, preventing ingredient separation, and prolonging shelf life. Manufacturers of beverages such as dairy drinks, juices, plant-based alternatives, and functional beverages increasingly depend on stabilization solutions to maintain uniform texture and visual appeal throughout the product's lifecycle. The rising consumer demand for premium, shelf-stable beverages continues to reinforce the segment's dominant position in the market.

Viscosification is projected to be the fastest-growing functionality segment, with a CAGR of 7.61% during the forecast period of 2026-2031. This growth is fueled by the increasing consumer preference for beverages with improved mouthfeel and a premium texture. Beverage producers are incorporating viscosity-enhancing ingredients into products like smoothies, dairy-based drinks, plant-based alternatives, and nutritional beverages to elevate sensory appeal and differentiate their offerings. As innovation in the beverage industry increasingly emphasizes texture enhancement and consumer experience, the viscosification segment is expected to witness significant expansion in the coming years.

By End Use: Fruit and Vegetable Drinks Lead, Sports and Energy Drinks Grow Fastest

Fruit and vegetable drinks emerged as the largest end use segment in the global beverage stabilizers market, accounting for 52.61% of total market revenue in 2025. This segment's leading position is attributed to the extensive use of stabilizers to maintain suspension stability, prevent phase separation, and enhance the texture of juice-based and fruit-infused beverages. The growing consumer preference for natural, nutritious, and functional drinks has further driven demand for stabilization solutions. As manufacturers continue to diversify their offerings in the fruit and vegetable beverage category, the reliance on beverage stabilizers is expected to remain significant, driving consistent growth in this segment.

Sports and energy drinks are expected to be the fastest-growing end use segment, with a projected CAGR of 8.27% over 2026-2031. The rising global focus on fitness, active lifestyles, and performance-enhancing beverages is a key driver of demand for these products. Stabilizers are essential in these formulations, as they ensure uniform dispersion of ingredients, enhance mouthfeel, and maintain product consistency, especially in beverages containing proteins, vitamins, and other functional components. Ongoing innovation in sports nutrition and energy drink formulations is likely to further boost the adoption of stabilizers, making this segment a significant driver of market growth during the forecast period.

Geography Analysis

North America maintained its leadership in the global beverage stabilizers market in 2025, accounting for 32.46% of the total revenue. This stronghold is driven by the region's advanced beverage industry, characterized by high consumption of ready-to-drink beverages and a growing preference for functional and premium products. Beverage manufacturers in North America rely heavily on stabilizers to enhance texture, ensure consistency, and improve shelf stability across a wide range of applications. Furthermore, the presence of key ingredient suppliers and cutting-edge food processing infrastructure reinforces the region's dominant position in the market.

The Asia-Pacific region is anticipated to witness the fastest growth in the beverage stabilizers market, with a projected CAGR of 7.09% through 2031. This growth is fueled by rapid urbanization, increasing disposable incomes, and a rising demand for packaged and convenience beverages. The region is also experiencing a surge in domestic beverage production, alongside significant investments from global beverage companies seeking to tap into the expanding market. Additionally, the growing popularity of functional and fortified beverages is driving the adoption of stabilizers, presenting substantial growth opportunities for market players in Asia-Pacific.

Europe emerged as the second-largest regional market, supported by a strong demand for clean-label, premium, and health-oriented beverage products. Manufacturers in the region are increasingly adopting natural stabilizing solutions to cater to consumer preferences for transparency and high-quality ingredients. The rising consumption of plant-based beverages, fruit drinks, and wellness-focused formulations continues to propel the demand for stabilizers. Meanwhile, South America and the Middle East & Africa are gaining traction as emerging markets, driven by increasing packaged beverage consumption, expanding retail networks, and growing beverage production activities in these regions.

Competitive Landscape

The beverage stabilizers market operates within a moderately consolidated competitive environment, where large multinational ingredient suppliers coexist with specialized manufacturers focusing on niche stabilizer technologies. Major players maintain their dominance by utilizing extensive product portfolios, robust global distribution networks, and established relationships with beverage producers. Meanwhile, smaller niche players carve out opportunities by offering customized solutions tailored to specific beverage formulations and applications. This dynamic fosters a competitive landscape that drives continuous innovation and product differentiation across the market.

One of the key trends shaping market competition is the growing focus on portfolio diversification and integrated ingredient solutions. Beverage manufacturers are progressively seeking suppliers capable of providing a comprehensive range of stabilizers and texture-enhancing ingredients from a single source, streamlining procurement and formulation processes. To address this demand, market participants are enhancing their capabilities through strategic collaborations, acquisitions, and expanded product offerings. As a result, the competitive focus is shifting from standalone ingredients to holistic beverage formulation platforms that deliver multiple functional benefits, catering to evolving consumer preferences.

In the beverage stabilizers market, technical expertise, regulatory compliance support, and application development capabilities have emerged as critical differentiators. Suppliers are prioritizing research and development to create advanced stabilization systems that align with the growing demand for clean-label, plant-based, and functional beverages. Companies that offer formulation expertise, ensure adherence to diverse regulatory standards, and maintain reliable supply chains are increasingly preferred by beverage manufacturers. Consequently, success in this market is becoming more reliant on innovation, superior service quality, and customer-centric solutions rather than solely on operational scale.

Beverage Stabilizers Industry Leaders

-

Cargill Inc.

-

Tate & Lyle PLC

-

Ingredion Inc.

-

Kerry Group PLC

-

International Flavors & Fragrances Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Cargill opened a new corn milling plant in Gwalior, Madhya Pradesh, operated by Indian manufacturer Saatvik Agro Processors, to meet increasing demand from India's confectionery, infant formula, and dairy industries.

- October 2024: Jungbunzlauer has initiated construction of a USD150 million facility in Canada to produce xanthan gum, a fermentation-derived ingredient used in food, cosmetic, and pharmaceutical products. The facility will utilize locally sourced corn as the primary raw material.

- June 2024: Tate & Lyle announced its acquisition of CP Kelco for USD 1.8 billion, creating a leading global specialty food and beverage solutions business with enhanced capabilities in hydrocolloids, including pectin and specialty gums. The merger aims for revenue growth of 4-6% per annum and cost synergies of at least USD 50 million by the second full financial year following completion.

- January 2024: IFF launched Grindsted Pectin FB 420 for baking applications. It is ideal for baking applications, has unique sensory qualities for bake-stable fruit fillings, and is label-friendly and process-efficient.

Global Beverage Stabilizers Market Report Scope

Beverage stabilizers are essential ingredients that help preserve the texture, consistency, appearance, and shelf life of beverages by preventing ingredient separation and enhancing mouthfeel. The global beverage stabilizers market includes product type, form, source, functionality, end use, and geography. Based on product type, the market is classified into xanthan gum, pectin, gum arabic, gellan gum, carrageenan, carboxymethyl cellulose, and others. Based on form, the market is classified into powder and liquid. Based on the source, the market is classified into natural and synthetic. Based on functionality, the market is classified into stabilization, viscosification, texturization, and others. Based on end use, the market is classified into carbonated soft drinks, fruit and vegetable drinks, dairy and dairy alternative drinks, sports and energy drinks, alcoholic drinks, and others. Based on geography, the market is classified into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. The market forecasts are provided in terms of value (USD).

| Xanthan Gum |

| Pectin |

| Carrageenan |

| Gum Arabic |

| Gellan Gum |

| Carboxymethyl Cellulose (CMC) |

| Others |

| Powder |

| Liquid |

| Natural |

| Synthetic |

| Stabilization |

| Viscosification |

| Texturization |

| Others |

| Carbonated Soft Drinks |

| Fruit and Vegetable Drinks |

| Dairy and Dairy Alternative Beverages |

| Sports and Energy Drinks |

| Alcoholic Drinks |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Xanthan Gum | |

| Pectin | ||

| Carrageenan | ||

| Gum Arabic | ||

| Gellan Gum | ||

| Carboxymethyl Cellulose (CMC) | ||

| Others | ||

| By Form | Powder | |

| Liquid | ||

| By Source | Natural | |

| Synthetic | ||

| By Functionality | Stabilization | |

| Viscosification | ||

| Texturization | ||

| Others | ||

| By End Use | Carbonated Soft Drinks | |

| Fruit and Vegetable Drinks | ||

| Dairy and Dairy Alternative Beverages | ||

| Sports and Energy Drinks | ||

| Alcoholic Drinks | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current outlook for beverage stabilizers?

The beverage stabilizers market stands at USD 2.62 billion in 2026 and is forecast to reach USD 3.63 billion by 2031, anticipated to grow at a 6.74% CAGR. Demand is being supported by RTD beverages, plant-based dairy alternatives, and functional drinks.

Which product type leads product demand?

Xanthan gum leads product demand with a 25.78% share in 2025 because it performs well across a broad pH range and supports both suspension and viscosity control in multiple beverage formats.

Which end use category is expanding the fastest?

Sports and energy drinks are the fastest-growing end use segment, forecasted to grow at an 8.27% CAGR through 2031, as brands work to stabilize amino acids, electrolytes, and other active ingredients in RTD formats.

Why are natural stabilizers ahead of synthetic options?

Natural stabilizers held 71.55% share in 2025 because beverage brands continue to move toward botanical, seaweed-derived, and fermentation-sourced ingredients that support cleaner labels and stronger consumer familiarity.

Page last updated on: