Cognac and Brandy Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

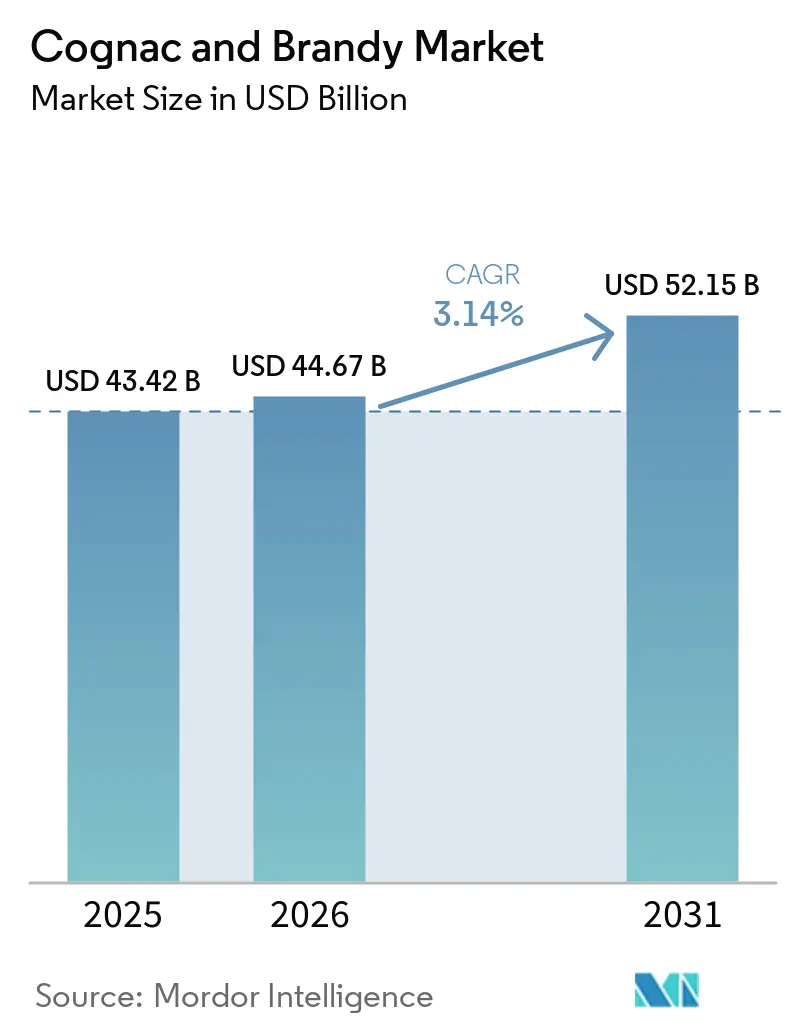

| Market Size (2026) | USD 44.67 Billion |

| Market Size (2031) | USD 52.15 Billion |

| Growth Rate (2026 - 2031) | 3.14% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cognac and Brandy Market Analysis by Mordor Intelligence

The cognac and brandy market size is expected to grow from USD 43.42 billion in 2025 to USD 44.67 billion in 2026 and is forecast to reach USD 52.15 billion by 2031 at 3.14% CAGR over 2026-2031. This growth trajectory is supported by the rising preference for premium and luxury alcoholic beverages, particularly among millennials and affluent consumers. Additionally, the expanding popularity of cognac and brandy in emerging markets, coupled with innovative product launches and strategic marketing initiatives by key players, is expected to further propel market growth. The increasing focus on product differentiation and the adoption of sustainable production practices are also likely to contribute to the market's positive outlook. Overall, the cognac and brandy market is set to maintain a stable growth pattern, driven by evolving consumer preferences and industry advancements.

Key Report Takeaways

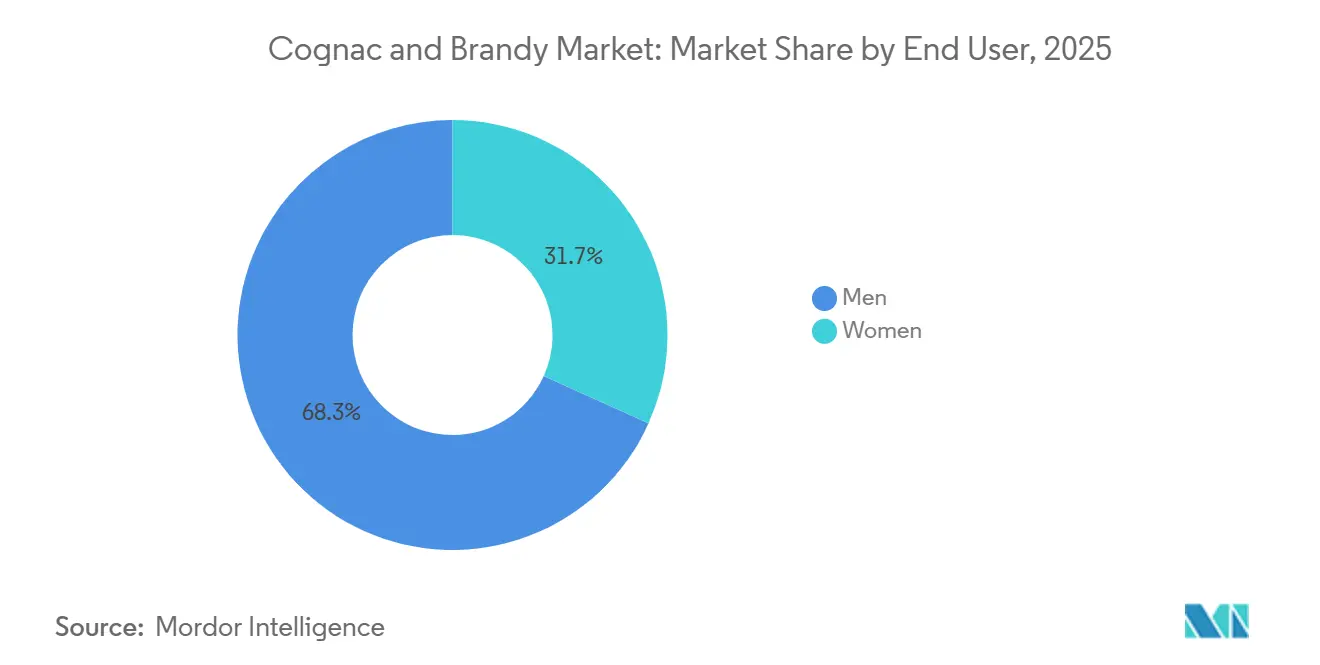

- By end user, men held 68.26% of the cognac and brandy market in 2025, while women are projected to expand at 4.56% CAGR through 2031.

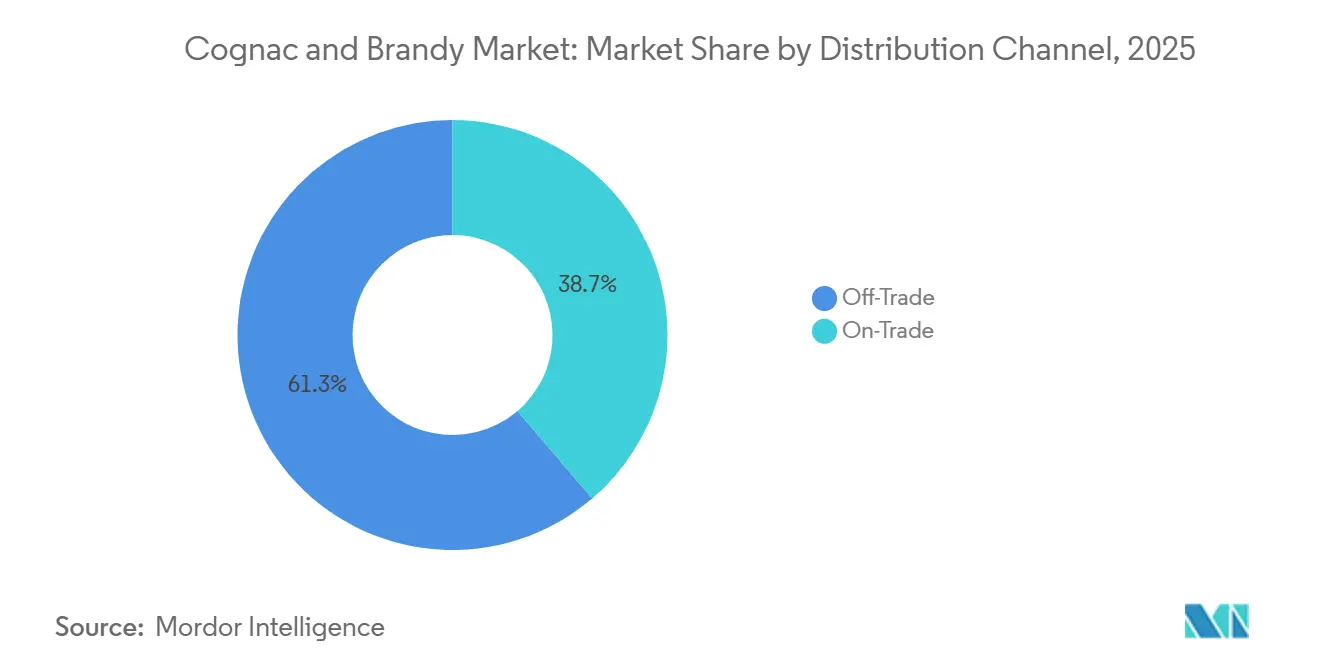

- By distribution channel, off-trade accounted for 61.26% of the cognac and brandy market in 2025, while on-trade is forecast to grow at 4.89% CAGR through 2031.

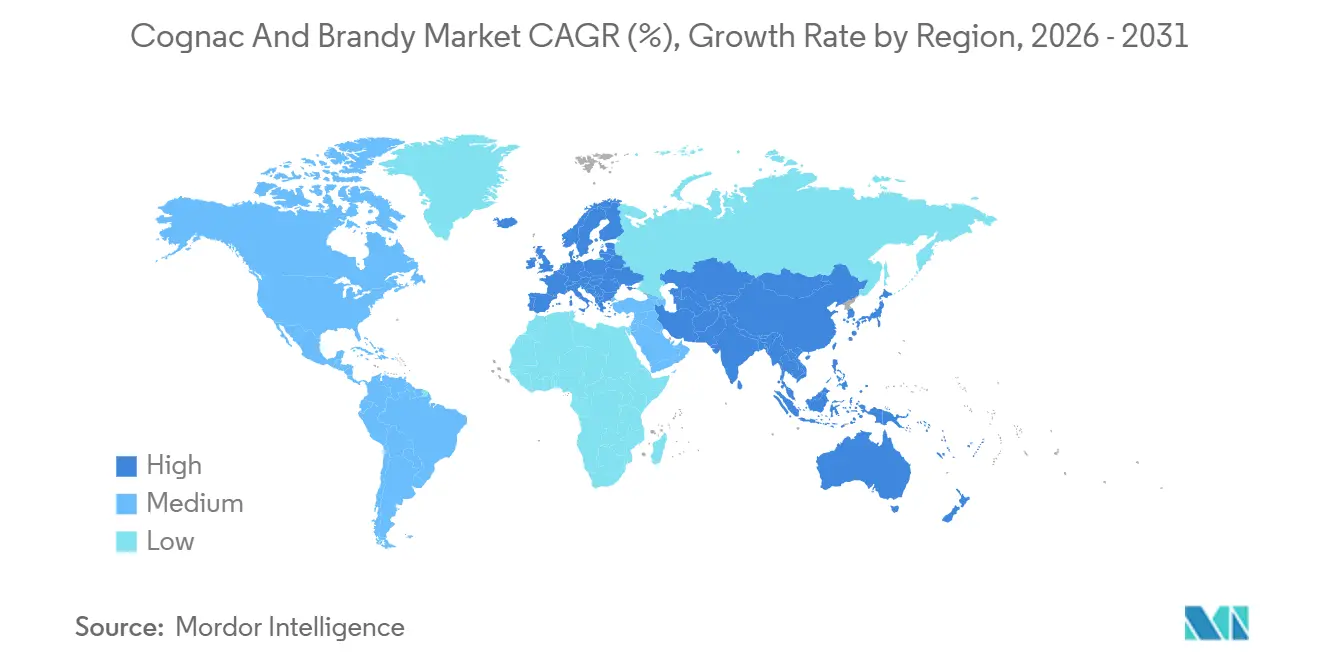

- By geography, Europe captured 34.12% of the cognac and brandy market in 2025, while Asia-Pacific is expected to record the fastest regional CAGR at 4.23% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Cognac and Brandy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing consumer preference for aged and craft spirits | +0.7% | Global, strongest in North America, Europe, and Asia-Pacific | Medium term (2-4 years) |

| Expansion of the tourism and hospitality sector contributing to strong market growth | +0.5% | Europe, Asia-Pacific, and South America | Medium term (2-4 years) |

| Rising demand for high-end and premium alcoholic beverages | +1.2% | Global, with strongest premium intensity in Asia-Pacific and North America | Long term (≥ 4 years) |

| Product innovation through flavored, limited-edition, and cask-finished variants | +0.3% | North America and Europe, with early traction in Asia-Pacific | Short term (≤ 2 years) |

| Expansion of cocktail culture and mixology trends globally | +0.4% | North America, Europe, and Southeast Asia | Medium term (2-4 years) |

| Rising popularity of luxury gifting and celebratory consumption | +0.3% | Asia-Pacific, North America, and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing consumer preference for aged and craft spirits

Growing consumer preference for aged and craft spirits is a significant driver of the cognac and brandy market, as consumers increasingly seek premium, authentic, and high-quality alcoholic beverages. Rising interest in artisanal production methods, unique flavor profiles, and heritage-driven brands has encouraged manufacturers to expand their portfolios with aged, small-batch, and limited-edition offerings. This trend is further supported by the broader growth of the craft alcohol industry. According to the Brewers Association, the number of U.S. craft breweries increased from 9,118 in 2021 to 9,796 in 2024, reflecting strong consumer demand for craft alcoholic beverages[1]Source: Brewers Association, “Brewers Association Reports 2024 U.S. Craft Brewing Industry Figures”, brewersassociation.org. The growing appreciation for craftsmanship and product differentiation is fostering innovation and premiumization across the spirits sector, prompting producers to introduce premium cognac and brandy variants that cater to evolving consumer tastes and higher spending on luxury alcoholic drinks.

Expansion of the tourism and hospitality sector contributing to strong market growth

The expansion of the tourism and hospitality sector is a key driver of growth in the cognac and brandy market, as increasing travel activity boosts consumption of premium alcoholic beverages across hotels, restaurants, bars, resorts, and duty-free retail channels. International tourists often seek authentic local drinking experiences and premium spirits, supporting higher demand for cognac and brandy in major tourism destinations. According to the United Nations Tourism Report, approximately 1.52 billion international tourists were recorded globally in 2025, nearly 60 million more than in 2024, highlighting the continued recovery and expansion of global travel[2]Source: United Nations Tourism, “International tourist arrivals up 4% in 2025 reflecting strong travel demand around the world”, untourism.int. This rise in tourist arrivals is increasing on-trade sales and encouraging hospitality operators to expand their premium spirits offerings. In addition, luxury tourism trends and growing spending on experiential dining are driving greater consumption of aged and high-end cognac and brandy products, thereby contributing to sustained market growth worldwide.

Rising demand for high-end and premium alcoholic beverages

The rising demand for high-end and premium alcoholic beverages is a major driver of the cognac and brandy market. Consumers are increasingly willing to spend more on premium spirits that offer superior quality, authenticity, aging credentials, and distinctive flavor profiles. Growing disposable incomes, urbanization, and the expansion of affluent consumer groups are supporting the shift toward luxury alcoholic drinks. In addition, changing consumer preferences toward premium drinking experiences and status-oriented consumption are boosting demand for aged cognac and premium brandy variants. The trend is particularly evident among younger adult consumers who value craftsmanship, heritage, and exclusivity in their beverage choices. Manufacturers are responding by introducing premium, ultra-premium, and limited-edition products to strengthen brand positioning and profitability.

Product innovation through flavored, limited-edition, and cask-finished variants

Product innovation through flavored, limited-edition, and cask-finished variants is a significant driver of growth in the cognac and brandy market. Consumers are increasingly seeking unique taste experiences and differentiated premium products, encouraging producers to expand beyond traditional offerings. Flavored expressions infused with fruit, spice, or botanical notes are attracting younger consumers and broadening the category’s appeal. At the same time, limited-edition releases create a sense of exclusivity and scarcity, driving consumer interest and premium pricing opportunities. Cask-finished variants, aged in barrels previously used for wine, whisky, sherry, or other spirits, offer distinctive flavor profiles that appeal to enthusiasts and collectors. These innovations help brands strengthen product portfolios, enhance customer engagement, and differentiate themselves in a competitive market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent alcohol regulations, advertising restrictions, and licensing requirements | -0.4% | Global, especially China, the European Union, and North America | Long term (≥ 4 years) |

| Increasing health concerns related to heavy alcohol intake | -0.2% | North America, Europe, and Asia-Pacific | Medium term (2-4 years) |

| Growing consumer shift toward low-alcohol and non-alcoholic alternatives | -0.4% | North America, Europe, and Australia | Short term (≤ 2 years) |

| High excise duties and taxation on alcoholic beverages | -0.3% | European Union, North America, India, and South Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent alcohol regulations, advertising restrictions, and licensing requirements

Stringent alcohol regulations, advertising restrictions, and licensing requirements act as significant restraints on the growth of the cognac and brandy market. Governments across many countries impose strict rules on the production, distribution, marketing, and sale of alcoholic beverages to address public health concerns and reduce alcohol misuse. Restrictions on alcohol advertising and promotional activities limit brand visibility and make it more challenging for companies to attract new consumers and expand market reach. In addition, complex licensing procedures and compliance requirements can increase operational costs and create barriers to market entry, particularly for smaller producers. Frequent regulatory changes and varying legal frameworks across regions further complicate business expansion strategies. High excise duties and regulatory oversight may also affect product pricing and consumer affordability.

Increasing health concerns related to heavy alcohol intake

Increasing health concerns related to heavy alcohol intake act as a major restraint on the cognac and brandy market, as rising awareness of alcohol-related diseases is influencing consumer behavior and reducing overall consumption in several regions. Public health campaigns and stricter dietary guidelines are encouraging moderation, particularly among younger and health-conscious consumers. Concerns over liver disease, cardiovascular risks, and addiction are prompting a gradual shift toward low-alcohol and alcohol-free alternatives. In some regions, alcohol consumption levels remain alarmingly high, further intensifying health concerns and regulatory scrutiny. For instance, Romania recorded an average alcohol consumption of 16.96 liters per capita, one of the highest rates globally, according to the World Health Organization[3]Source: World Health Organization, “Total alcohol per capita (>= 15 years of age) consumption (litres of pure alcohol)”, data.who.int. Such high consumption figures have led governments and health agencies to promote stricter awareness initiatives and control measures. As a result, growing health consciousness is expected to limit demand growth for high-alcohol spirits like cognac and brandy over the long term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End User: Women's Segment Outpaces Market Average as Occasion Diversity Expands

Men accounted for the largest share of the cognac and brandy market in 2025, representing 68.26% of total revenue. The segment's dominance is largely attributed to the long-established consumption culture of cognac and brandy among male consumers across both developed and emerging markets. Premium and super-premium cognac varieties continue to enjoy strong demand from men, particularly in social gatherings, celebrations, business events, and luxury consumption occasions. Higher spending capacity and greater brand awareness among male consumers have also contributed to the segment's leadership position. In addition, the popularity of aged spirits, craft distillations, and collector-grade cognac products remains significantly higher among men, supporting sustained market demand.

The women segment is expected to register the fastest growth in the cognac and brandy market, expanding at a CAGR of 4.56% through 2031. Rising participation of women in premium alcoholic beverage consumption is creating new growth opportunities for manufacturers and distributors. Changing social norms, increasing disposable incomes, and growing interest in luxury lifestyle products are encouraging greater adoption of cognac and brandy among female consumers. Brands are also introducing innovative flavors, lighter blends, and targeted marketing campaigns that resonate with women, further supporting segment expansion. The increasing popularity of cocktail culture and mixology has made cognac and brandy more accessible to female consumers who prefer versatile drinking experiences.

By Distribution Channel: Off-Trade Volume Leadership Masks On-Trade's Premiumisation Role

The off-trade channel dominated the cognac and brandy market in 2025, accounting for 61.26% of total revenue. The segment's leadership is primarily driven by the widespread availability of cognac and brandy through liquor stores, supermarkets, hypermarkets, specialty alcohol retailers, and e-commerce platforms. Consumers increasingly prefer purchasing alcoholic beverages through off-trade channels due to convenience, competitive pricing, and access to a broader range of brands and product variants. Bulk purchases for home consumption, private gatherings, and gifting occasions have further strengthened demand through retail outlets. The expansion of organized retail networks and online alcohol delivery services in several markets has also enhanced product accessibility and consumer reach.

The on-trade channel is projected to be the fastest-growing distribution segment, registering a CAGR of 4.89% through 2031. Growth is being supported by the recovery and expansion of bars, restaurants, hotels, lounges, and nightlife venues across major markets. Rising consumer interest in premium drinking experiences and craft cocktail culture is encouraging greater consumption of cognac and brandy in on-premise establishments. Hospitality operators are increasingly incorporating premium spirits into curated beverage menus, tasting events, and mixology programs, boosting product visibility and consumption. In addition, growing urbanization, tourism activity, and higher discretionary spending are contributing to increased foot traffic at entertainment and dining venues.

Geography Analysis

Europe dominated the global cognac and brandy market in 2025, accounting for 34.12% of total revenue. The region’s leadership is primarily supported by its long-standing heritage in spirit production and consumption, particularly in countries such as France, Spain, Germany, and Italy. France remains the global center of cognac production, benefiting from strong domestic demand and substantial export volumes to international markets. European consumers demonstrate a high preference for premium and aged spirits, supporting the growth of high-value cognac and brandy categories. The region also benefits from a well-established distribution network comprising specialty liquor stores, supermarkets, and hospitality venues. In addition, strong brand recognition, premiumization trends, and a mature alcoholic beverage culture continue to reinforce Europe’s leading position in the market.

Asia-Pacific is projected to be the fastest-growing regional market, registering a CAGR of 4.23% through 2031. Rising disposable incomes, rapid urbanization, and the expansion of middle-class populations across countries such as China, India, Japan, and South Korea are driving demand for premium alcoholic beverages. Consumers in the region are increasingly shifting toward imported and luxury spirits, including cognac and premium brandy products. The growing influence of Western drinking habits, cocktail culture, and luxury lifestyle trends is further accelerating market expansion. E-commerce penetration and the development of modern retail infrastructure are also improving product accessibility across key markets. As international brands continue to invest in marketing, distribution, and product innovation, Asia-Pacific is expected to remain the primary engine of future market growth.

North America represents a significant market for cognac and brandy, supported by strong consumer interest in premium spirits and a thriving cocktail culture, particularly in the United States and Canada. South America is witnessing gradual growth as rising urbanization and improving economic conditions encourage greater consumption of imported alcoholic beverages, especially in countries such as Brazil and Argentina. Meanwhile, the Middle East and Africa region is experiencing steady expansion, driven by growth in tourism, hospitality, and premium beverage consumption in select markets. Demand in these regions is further supported by increasing availability of international brands through organized retail and duty-free channels.

Competitive Landscape

The cognac and brandy market exhibits a moderately consolidated competitive landscape, with a mix of global spirits companies and established regional producers competing across premium, super-premium, and mass-market categories. Market leaders benefit from strong brand heritage, extensive distribution networks, and well-established relationships with retailers, hospitality operators, and distributors. The industry is characterized by significant brand loyalty, particularly within the cognac segment, where product authenticity, aging expertise, and geographic origin play critical roles in purchasing decisions. Large manufacturers continue to leverage their global presence to expand market reach while maintaining premium brand positioning. At the same time, regional producers compete by emphasizing craftsmanship, unique flavor profiles, and local heritage.

Competition within the market is increasingly driven by premiumization strategies, product innovation, and portfolio diversification. Leading companies are expanding their offerings through limited-edition releases, aged variants, and premium packaging designed to attract affluent consumers and collectors. Strategic investments in brand building, digital marketing, and experiential promotions are helping manufacturers strengthen consumer engagement and enhance brand value. Companies are also focusing on expanding their presence in emerging markets, where rising disposable incomes and growing interest in premium spirits are creating new growth opportunities. Collaborations with hospitality venues, mixologists, and luxury lifestyle brands have become important tools for increasing product visibility.

The market has also witnessed growing emphasis on mergers, acquisitions, and distribution partnerships aimed at strengthening geographic reach and operational capabilities. Major players are investing in supply chain efficiency, sustainable production practices, and vineyard management to secure long-term raw material availability and maintain product quality standards. Expansion of e-commerce channels and direct-to-consumer sales platforms is further reshaping competitive dynamics, enabling brands to engage with consumers more effectively. Meanwhile, increasing demand for authentic, high-quality spirits is encouraging producers to highlight provenance, craftsmanship, and heritage in their marketing strategies.

Cognac and Brandy Industry Leaders

Rémy Cointreau SA

Pernod Ricard SA

LVMH Moët Hennessy Louis Vuitton SE

Diageo plc

Sazerac Company, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Campari Group strengthened its premium spirits portfolio and expanded its global cognac footprint by completing the acquisition of Courvoisier Cognac from Beam Suntory.

- January 2026: Copper & Kings American Brandy Company introduced a flagship portfolio that featured Six-Year American Brandy V.S.O.P., Six-Year American Apple Brandy Bottled-in-Bond, and Brandy Barrel-Finished Straight Bourbon. This launch was designed to strengthen the company's position in the premium American brandy market, modernize its core offerings, and expand its presence in the growing craft spirits segment.

- January 2026: Hennessy launched its Limited Edition Carnival Bottle 2026, which celebrated Caribbean culture and further enriched its lineup of special-edition cognacs. This release was targeted at collectors and premium consumers, enhancing its appeal in the luxury spirits market.

- March 2025: Campari announced its strategic focus on integrating and growing the recently acquired Courvoisier Cognac business, aiming to solidify its position in the global premium cognac segment.

Global Cognac and Brandy Market Report Scope

Cognac and brandy are distilled alcoholic spirits produced from fermented fruit juice, with grapes being the most commonly used raw material. The cognac and brand market is segmented by end user, distribution channel and geography. Based on end user, the market is segmented into men and women. Based on distribution channel, the market is segmented into off-trade and on-trade channels. Based on distribution channel, the market is segmented into foodservice and retail. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and Middle-East and Africa. For each segment, the market sizing and forecasting have been done in value terms (USD million) and volume (litres).

| Men |

| Women |

| On-Trade | |

| Off-Trade | Specialty/Liquor Stores |

| Other Off Trade Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Sweden | |

| Belgium | |

| Poland | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Indonesia | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Colombia | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Saudi Arabia | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By End User | Men | |

| Women | ||

| By Distribution Channel | On-Trade | |

| Off-Trade | Specialty/Liquor Stores | |

| Other Off Trade Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Sweden | ||

| Belgium | ||

| Poland | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Indonesia | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Colombia | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Saudi Arabia | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the Cognac and Brandy Market by 2031?

The Cognac and Brandy Market is forecast to reach USD 52.15 billion by 2031, up from USD 44.67 billion in 2026, at a 3.14% CAGR over 2026-2031.

Which region leads global demand for cognac and brandy?

Europe led with 34.12% share in 2025, supported by France's production base and mature Western European consumption markets.

Which region is expected to grow the fastest through 2031?

Asia-Pacific is projected to post the fastest regional CAGR at 4.23% through 2031, with growth becoming more diversified beyond China.

Which consumer group is expanding the fastest?

Women are the fastest-growing end-user group, with a projected 4.56% CAGR from 2026 to 2031 as consumption occasions broaden beyond traditional male-led settings.

Why is on-trade becoming more important for producers?

Off-trade still led with 61.26% share in 2025, but on-trade is growing faster at 4.89% CAGR because it drives trial, cocktails, brand education, and premium trade-up.

Page last updated on: