East Africa Automotive Lubricants Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

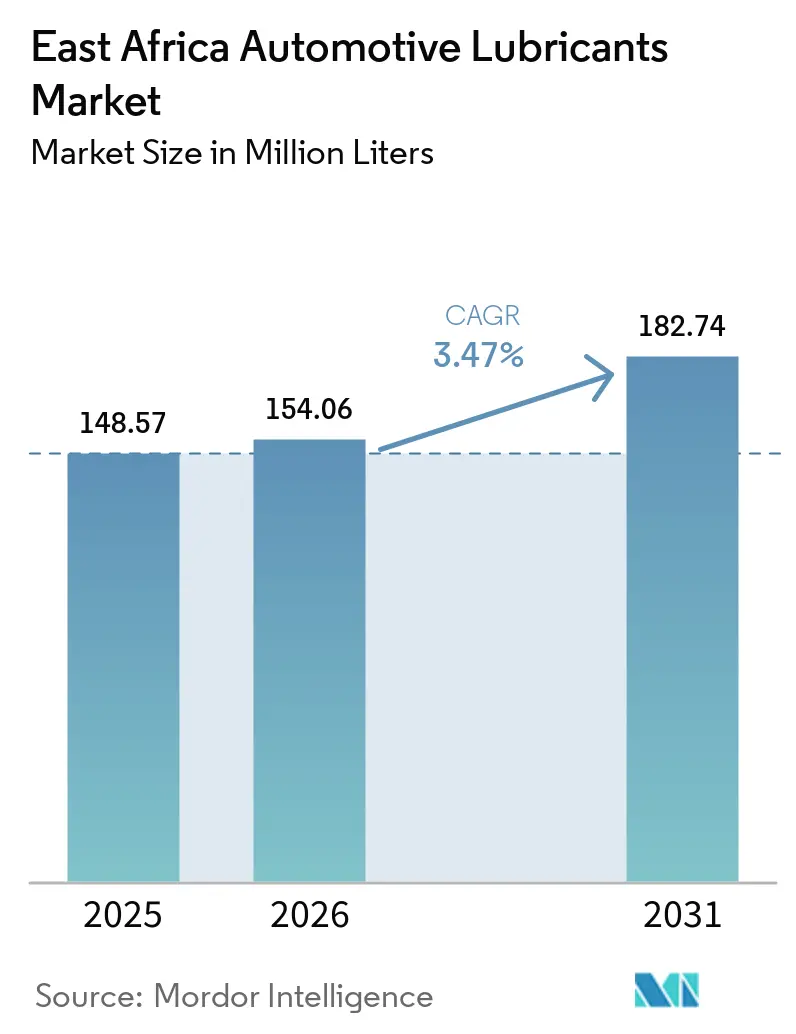

| Base Year Market Size (2025) | 148.57 Million liters |

| Market Volume (2026) | 154.06 Million liters |

| Market Volume (2031) | 182.74 Million liters |

| Growth Rate (2026 - 2031) | 3.47% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

East Africa Automotive Lubricants Market Analysis by Mordor Intelligence

The East Africa Automotive Lubricants Market size is expected to increase from 148.57 million liters in 2025 to 154.06 million liters in 2026 and reach 182.74 million liters by 2031, growing at a CAGR of 3.47% over 2026-2031. Structural demand is transitioning from basic drain-and-fill cycles to specification-driven purchasing, influenced by increasing telematics adoption, the introduction of harmonized East African Community (EAC) quality standards, and the growing use of motorcycles in Kenya, Uganda, and Tanzania. Domestic blending capacity is expanding, driven by seven Tanzanian plants and the enhanced Mombasa facility operated by TotalEnergies, which collectively form a key regional supply base. Counterfeit product penetration, particularly higher in Kenya than in Tanzania, affects brand equity and pricing potential. Additionally, the widening price gap between low-cost mineral grades and high-performance synthetics sustains a two-tier pricing structure. Global portfolio changes, such as BP p.l.c.'s sale of a controlling stake in Castrol, are creating opportunities for regional independents and Chinese companies. These entrants are focusing on the growing commercial-vehicle aftermarket with digitally traceable products.

Key Report Takeaways

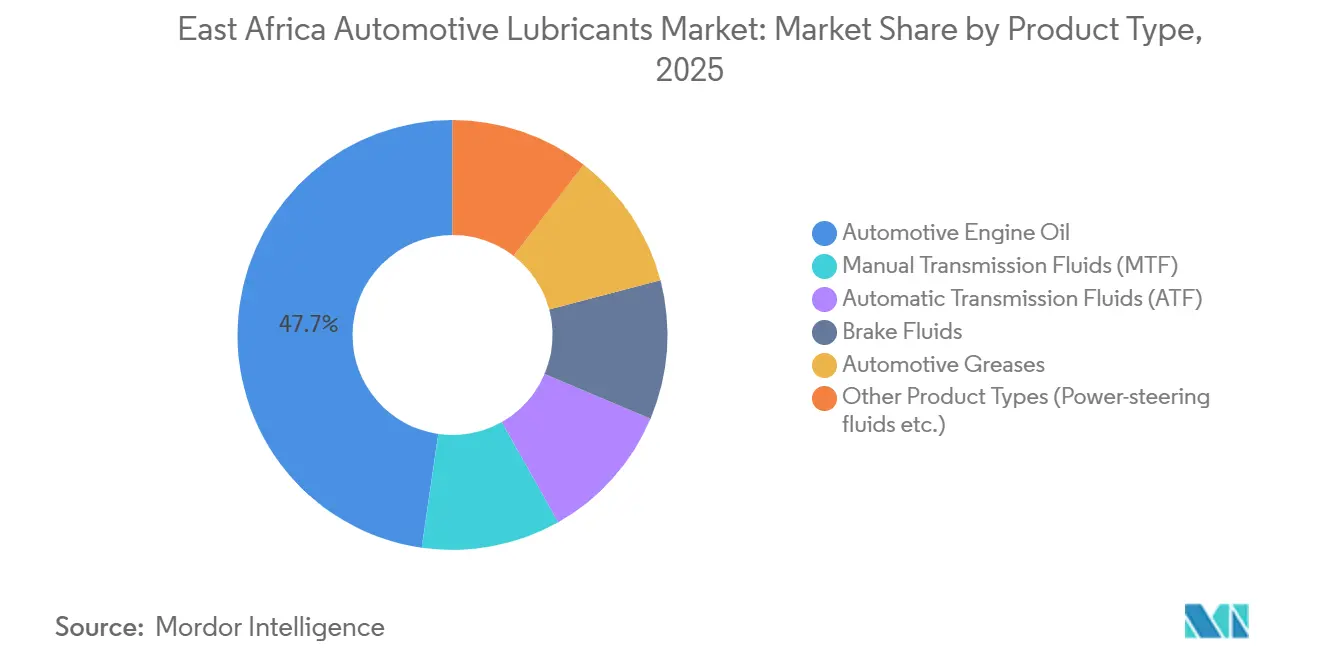

- By product type, automotive engine oil led with 47.72% of East Africa automotive lubricants market share in 2025, while automatic transmission fluids are forecast to rise at a 3.76% CAGR to 2031.

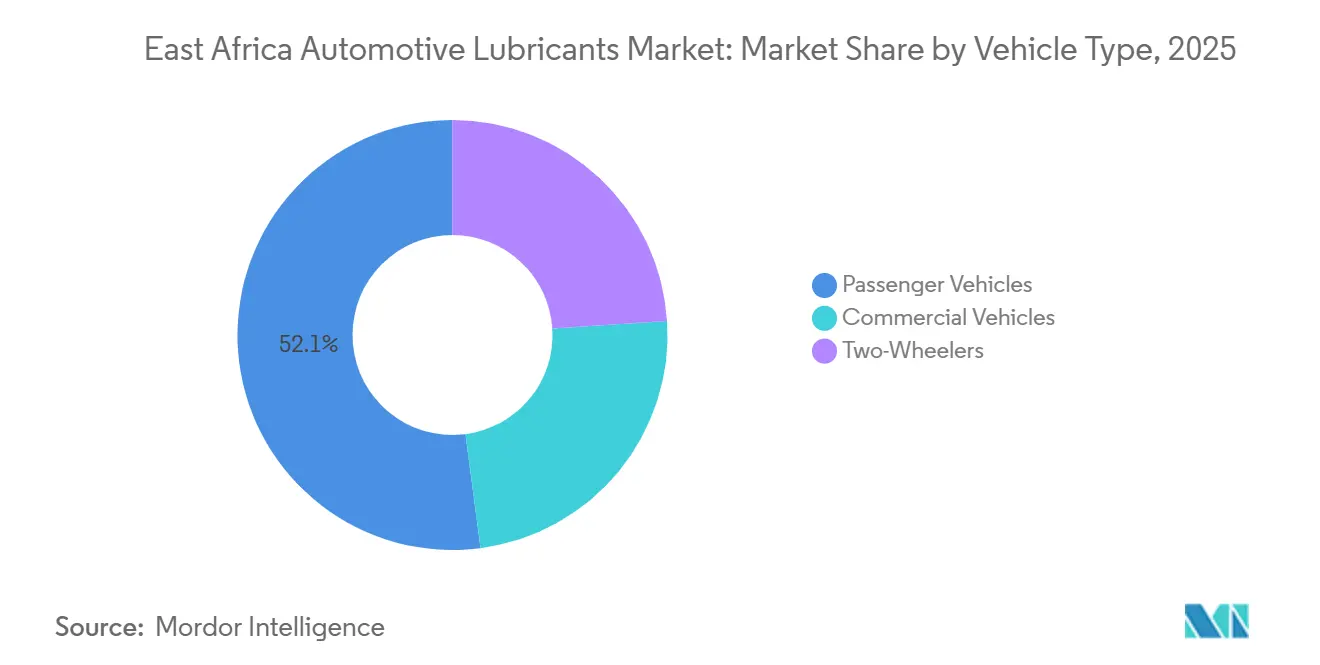

- By vehicle type, passenger cars accounted for 52.07% of the East Africa automotive lubricants market size in 2025, and commercial vehicles are projected to expand at a 3.64% CAGR through 2031.

- By geography, Kenya held 41.12% of the East Africa automotive lubricants market share in 2025; Tanzania is set to grow at a 3.68% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

East Africa Automotive Lubricants Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High average vehicle age and surge of used-vehicle imports | +0.6% | Kenya, Tanzania, Uganda; Kenya and Tanzania lead absolute import volumes | Medium term (2-4 years) |

| Rapid growth of motorcycle parc in Kenya, Uganda and Tanzania | +0.8% | Kenya (primary), Uganda and Tanzania (secondary); urban and peri-urban zones | Short term (≤ 2 years) |

| Expansion of road-infrastructure and cross-border trade corridors | +0.5% | Kenya (Lamu Port, Mombasa), Tanzania (Central Corridor), Uganda (Northern Corridor) | Long term (≥ 4 years) |

| Logistics, mining and agriculture boom boosting commercial vehicles demand | +0.7% | Tanzania (mining core), Kenya (logistics hub), Uganda (agriculture) | Medium term (2-4 years) |

| Telematics-driven fleet maintenance raising oil-change compliance | +0.4% | Kenya (regulatory mandate), Tanzania, and Uganda (voluntary adoption) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Average Vehicle Age and Surge of Used-Vehicle Imports

Approximately 90% of light vehicles in circulation across East Africa are pre-owned imports. Older powertrains contribute to increased oil consumption due to worn piston rings and higher operating temperatures. Between January and August 2024, Tanzania processed 46,944 Japanese vehicle imports, while Kenya handled 38,861 units during the same period, supporting a replacement market that prioritizes affordable mineral multigrades[1]The Citizen, “Tanzania Leads Africa in Importing Japanese Used Cars,” thecitizen.co.tz. Uganda’s decision in 2025 to reduce the import-age ceiling to 10 years slightly improves fleet quality but shortens turnover intervals, maintaining lubricant demand. The import mix is increasingly shifting toward automatic and hybrid vehicles, driving demand for automatic transmission fluids (ATF) and low-viscosity synthetic oils. Suppliers offering competitively priced, original equipment manufacturer (OEM)-approved formulations are positioned to secure consistent repeat business as the influx of used vehicles continues.

Rapid Growth of Motorcycle Parc in Kenya, Uganda, and Tanzania

Motorcycle registrations in Kenya more than doubled year-on-year, reaching 145,714 units in the first 11 months of 2025. Formal asset-finance models are improving maintenance compliance among boda-boda operators[2]Business Daily, “Telematics Devices Cut Fuel Theft by 85pc,” businessdailyafrica.com. The two-wheeler segment drives demand for small-pack sales of 2-stroke and 4-stroke oils. However, the segment faces challenges from electrification, with electric motorcycles already accounting for over 15% of Kenyan registrations and requiring minimal lubrication beyond chain grease. While internal-combustion motorcycles provide a short-term boost in lubricant volumes, marketers must diversify into greases and specialty fluids to mitigate long-term declines in engine oil demand. Key success factors include appropriate package sizing, rural distribution networks, and retailer education.

Expansion of Road Infrastructure and Cross-Border Trade Corridors

The commissioning of Lamu Port Phase I in February 2026 establishes a northern shipping hub projected to handle 1.2 million twenty-foot equivalent units (TEUs) by 2027. Alongside upgrades to Tanzania’s Central Corridor, these developments extend heavy-truck duty cycles and increase consumption of high-temperature diesel engine oils, hydraulic fluids, and greases used in port operations. While freight migration to the Standard Gauge Railway moderates some of this growth, road transport remains the dominant mode for last-mile delivery to landlocked regions such as the Democratic Republic of the Congo (DRC), South Sudan, and Rwanda. Integrated supply contracts bundling lubricants with fuel and telematics services are gaining popularity among fleet operators seeking predictable operating costs.

Logistics, Mining, and Agriculture Boom Boosting Commercial Vehicles

Tanzania has recorded growth in its mining sector and allocated USD 20 billion for gas infrastructure development, increasing the demand for specialty lubricants capable of withstanding heat, heavy loads, and abrasive ore dust. Kenya and Uganda are investing over USD 50 billion in roads, pipelines, and rail projects, leading to higher utilization of heavy equipment and extended lubricant drain intervals. In agriculture, mechanization is introducing tractors and tillers that require gear oils and greases, though these needs remain underserved by formal distribution channels. Suppliers with established rural reseller networks and on-site technical support are well-positioned to benefit as agricultural mechanization expands.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of counterfeit and sub-standard lubricants | -0.3% | Kenya (~20% market share), Tanzania (grater than 50% of consumed goods), Uganda (border zones) | Medium term (2-4 years) |

| Extreme price sensitivity favouring low-cost mineral oils | -0.4% | Kenya, Uganda, Tanzania; boda-boda, taxi, and informal transport sectors | Long term (≥ 4 years) |

| Weak regulatory enforcement and fragmented quality standards | -0.2% | Regional: KEBS, TBS, UNBS enforcement gaps across Kenya, Tanzania, Uganda | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Proliferation of Counterfeit and Sub-Standard Lubricants

Kenya’s Anti-Counterfeit Authority seized products worth significant amounts at the Busia border in February 2026. Despite such efforts, counterfeit oils still account for approximately 20% of national consumption and over half of Tanzania’s volume. Counterfeiters often refill used bottles or dilute genuine stocks, leading to engine failures that affect consumer trust. In response, TotalEnergies introduced tamper-proof seals with Unstructured Supplementary Service Data (USSD) validation codes, while several Chinese brands implemented blockchain-based track-and-trace packaging. Although enforcement gaps remain, increasing consumer awareness and the adoption of digital verification tools are gradually reducing the prevalence of counterfeit products.

Extreme Price Sensitivity Favoring Low-Cost Mineral Oils

Mineral multigrades are priced at a 3:1 premium per liter, which most taxi and boda-boda operators are unwilling to absorb, despite the longer drain intervals they offer. With per-capita Gross Domestic Product (GDP) ranging from USD 2,000-4,000, lubricant spending remains highly elastic. Recycled base oils are priced approximately 50% lower than virgin stocks, further influencing consumer choices. While corporate fleets with Original Equipment Manufacturer (OEM) warranties tend to adopt synthetic oils, the majority of the used-vehicle market continues to rely on mineral oils, limiting the potential for upgrades. Suppliers strategically segment their offerings, balancing cost considerations with performance claims supported by OEM approvals.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Engine-Oil Leadership Masks ATF Momentum

Automotive engine oil accounted for 47.72% of the 2025 volume in the East Africa automotive lubricants market, driven by the high drain frequency required for cars, trucks, and motorcycles. The market size for automatic transmission fluids (ATF) in East Africa is projected to grow at a compound annual growth rate (CAGR) of 3.76% through 2031, as automatic gearboxes gain popularity in cities like Nairobi and Dar es Salaam, where stop-and-go traffic is common. Legacy grades such as 15W-40 and 20W-50 continue to dominate due to consistently high ambient temperatures. However, premium 5W-30 synthetic oils are gradually gaining traction, particularly in newer Japanese and European vehicle imports that require low-viscosity oils for tighter engine tolerances.

Manual transmission fluids are experiencing modest growth as manual gearboxes remain prevalent in passenger vehicles, although their market share is gradually declining. Brake fluids and automotive greases follow standard maintenance schedules, while power steering fluids and coolants are increasingly included in bundled service kits offered at original equipment manufacturer (OEM) workshops. A diverse product portfolio has become essential for market players. For instance, National Oil Ethiopia offers a range of products, including Havoline mineral and synthetic grades, GL-4 and GL-5 gear oils, DOT 4 brake fluids, and lithium or molybdenum disulfide greases, distributed across eight regional depots. Suppliers that expand their offerings beyond basic engine oils are better positioned to maintain margins as demand for automatic transmission fluid (ATF) and synthetic lubricants continues to grow.

By Vehicle Type: Passenger Cars Hold Volume, Commercial Fleets Propel Growth

Passenger vehicles accounted for 52.07% of the 2025 East Africa automotive lubricants market share, supported by a significant aging fleet of imported sedans and hatchbacks that typically require mineral multigrades every 3,000-5,000 kilometers. Commercial vehicles are projected to grow at a compound annual growth rate (CAGR) of 3.64% through 2031, driven by higher per-unit lubricant consumption and extended operating hours along expanding logistics corridors. Long-haul trucks consume between 15-25 liters per oil change, significantly exceeding the fill rates of passenger cars, while construction equipment contributes additional demand for hydraulic fluids and grease, linked to ongoing mining and infrastructure projects.

Motorcycles represent the fastest-growing segment in terms of units; however, each engine requires only 1 liter of lubricant per service, limiting the overall volume contribution. Electrification is already reducing engine oil demand for approximately one in seven two-wheelers in Kenya, a trend that may further constrain segment volumes over the forecast period. Additionally, the adoption of fleet telematics in public-service vehicles in Kenya is standardizing maintenance intervals, encouraging the use of premium synthetic lubricants with OEM approvals. The overall market outlook favors suppliers capable of offering tailored product solutions to meet the diverse operational requirements of passenger cars, commercial vehicles, and motorcycles.

Geography Analysis

Kenya holds a 41.12% market share in the East Africa automotive lubricants market as of 2025. This position is supported by mandatory telematics in trucking, a diverse supplier landscape, and the February 2026 activation of Lamu Port Phase I, which is expected to increase northbound truck mileage. While the government is intensifying enforcement against counterfeit products, these still account for approximately 20% of the national volume. The steady inflow of used Japanese cars sustains passenger-vehicle oil demand, although incentives for electric motorcycles could impact future volumes.

Tanzania, with a forecasted Compound Annual Growth Rate (CAGR) of 3.68% from 2026 to 2031, is the fastest-growing market in the region. Growth is driven by mining expansion, gas infrastructure development, and a network of seven domestic blenders meeting national demand. The Central Corridor competes with Kenya’s northern routes, enhancing truck utilization and increasing diesel-engine oil throughput. Despite stricter licensing rules introduced in 2022, counterfeit lubricants still account for more than 50% of the market, prompting legitimate blenders to adopt tamper-proof packaging and establish consumer hotlines.

Uganda’s market dynamics are influenced by cross-border trade with South Sudan and the eastern Democratic Republic of the Congo (DRC). A 2025 policy tightening used-vehicle age limits to 10 years is expected to slightly improve fleet quality. However, the reversal of a zero-rated electric vehicle (EV) duty is slowing electrification, thereby extending demand for internal-combustion engine lubricants. Limited national blending capacity leaves importers exposed to foreign-exchange risks and occasional supply disruptions due to border delays.

Ethiopia and Rwanda are emerging markets in the region. Ethiopia’s aviation sector entered into a five-year lubricants agreement with Exxon Mobil Corporation in January 2026, indicating a growing technical demand that may extend to the automotive segment. In Rwanda, the rapidly expanding motorcycle population and improving road infrastructure are attracting branded small-pack lubricant suppliers. However, the market scale remains modest compared to Kenya or Tanzania.

Competitive Landscape

The East Africa automotive lubricants market is moderately fragmented. Strategic partnerships are shaping channel access in the market. Rubis Energy Kenya received working capital and Enterprise Resource Planning (ERP) support from the National Oil Corporation in March 2025, enabling expanded operations across more than 300 fuel stations. Castrol products remain available at Rubis forecourts, benefiting from brand recognition despite BP p.l.c.’s global divestment of majority ownership. Chinese company TERZO has announced a three-phase regional expansion plan targeting 15% penetration in the commercial vehicle segment by 2027. This initiative is supported by artificial intelligence (AI)-developed lubricants designed for high ambient temperatures and blockchain-secured anti-counterfeit labeling.

Domestic blending capacity is now a key factor in cost leadership. TotalEnergies has doubled the capacity of its Mombasa plant to 47,000 tons and holds International Organization for Standardization (ISO) 9001 and ISO 14001 certifications. Oryx Energies operates a 100,000-ton twin-plant network located in Dar es Salaam and Lomé. Anti-counterfeit technologies are becoming increasingly essential, with Unstructured Supplementary Service Data (USSD) and Quick Response (QR) code validation systems being adopted by premium brands.

East Africa Automotive Lubricants Industry Leaders

Shell plc

TotalEnergies

BP p.l.c. (Castrol)

Rubis Energy Kenya

Puma Energy

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: TERZO announced a strategic supply partnership involving artificial intelligence (AI)-based high-temperature engine oils and blockchain-enabled traceability solutions. This initiative is aimed at enhancing the efficiency and reliability of East Africa's automotive lubricants market. The company is targeting a 15% share of the aftermarket by 2027, with a focus on addressing the growing demand for advanced lubricants in the region.

- March 2025: Rubis Energy Kenya and the National Oil Corporation of Kenya entered into a working capital and Enterprise Resource Planning (ERP) partnership, facilitating the expansion of Rubis's lubricant distribution to over 300 retail sites. This collaboration is expected to strengthen the supply chain and enhance the availability of automotive lubricants in the East African market, addressing the growing demand in the region.

East Africa Automotive Lubricants Market Report Scope

Automotive lubricants, including fluids and greases, are designed to reduce friction, wear, and heat among moving engine components. These lubricants form a protective film to shield surfaces from corrosion, clean internal contaminants, and enhance vehicle efficiency. They are composed of base oils, either mineral or synthetic, combined with additives essential for engine longevity.

The East Africa automotive lubricants market is segmented by product type, vehicle type, and geography. By product type, the market is segmented into automotive engine oil, manual transmission fluids (mtf), automatic transmission fluids (ATF), brake fluids, automotive greases, and other product types (power-steering fluids, etc.). By vehicle type, the market is segmented into passenger vehicles, commercial vehicles, and two-wheelers. The report also covers the market size and forecasts for automotive lubricants in 7 countries across the region. The market sizes and forecasts are provided in terms of volume (Liters).

| Automotive Engine Oil | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades | |

| Manual Transmission Fluids (MTF) | |

| Automatic Transmission Fluids (ATF) | |

| Brake Fluids | |

| Automotive Greases | |

| Other Product Types (Power-steering fluids etc.) |

| Passenger Vehicles |

| Commercial Vehicles |

| Two-Wheelers |

| Kenya |

| Tanzania |

| Uganda |

| Ethiopia |

| Rwanda |

| Burundi |

| Democratic Republic of Congo |

| By Product Type | Automotive Engine Oil | 0W-XX |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| Manual Transmission Fluids (MTF) | ||

| Automatic Transmission Fluids (ATF) | ||

| Brake Fluids | ||

| Automotive Greases | ||

| Other Product Types (Power-steering fluids etc.) | ||

| By Vehicle Type | Passenger Vehicles | |

| Commercial Vehicles | ||

| Two-Wheelers | ||

| By Geography | Kenya | |

| Tanzania | ||

| Uganda | ||

| Ethiopia | ||

| Rwanda | ||

| Burundi | ||

| Democratic Republic of Congo |

Key Questions Answered in the Report

What is current market size of East Africa Automotive Lubricants Market?

The East Africa Automotive Lubricants Market size is expected to increase from 148.57 million liters in 2025 to 154.06 million liters in 2026 and reach 182.74 million liters by 2031, growing at a CAGR of 3.47% over 2026-2031.

Which product category is expanding the quickest?

Automatic transmission fluids lead with a projected 3.76% CAGR as automatic gearboxes gain share in city traffic.

Why are commercial-vehicle lubricants a strategic priority?

Trucks and off-road equipment use far larger oil volumes per service interval and benefit from booming logistics and mining activity.

How are suppliers responding to regulatory and quality challenges?

Leading brands deploy International Organization for Standardization (ISO)-certified blending plants, tamper-proof packaging, and digital traceability to reassure fleet and retail buyers.

Page last updated on: