Ghana Lubricants Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

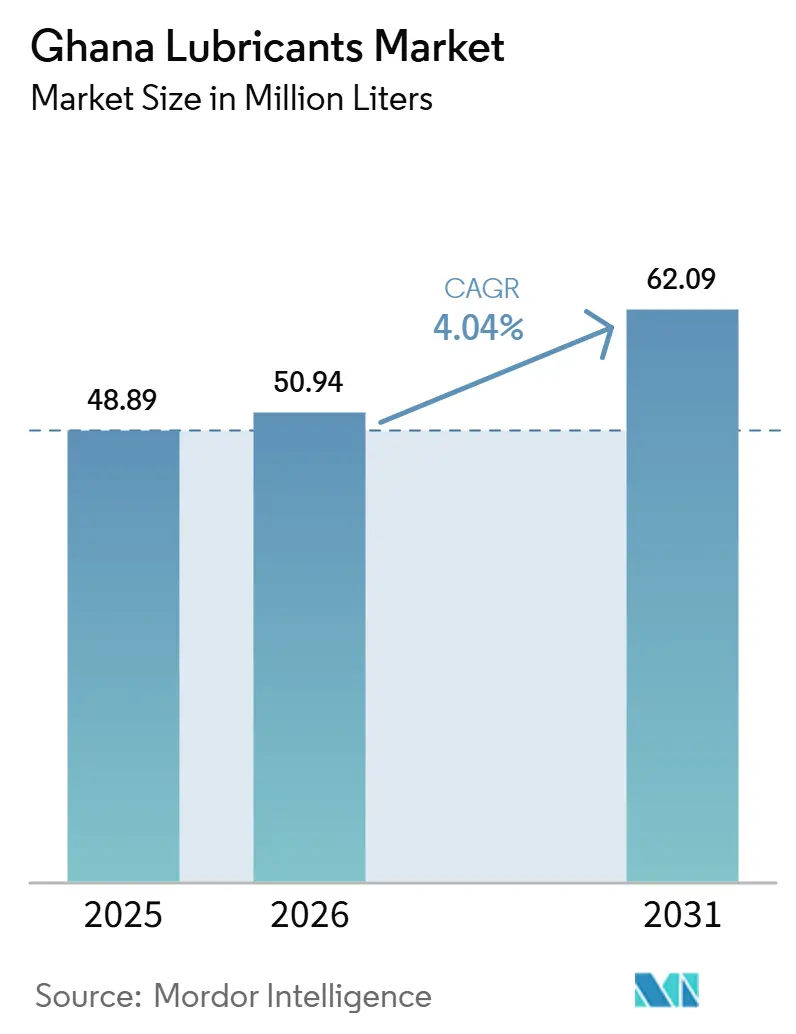

| Base Year Market Size (2025) | 48.89 Million liters |

| Market Volume (2026) | 50.94 Million liters |

| Market Volume (2031) | 62.09 Million liters |

| Growth Rate (2026 - 2031) | 4.04% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ghana Lubricants Market Analysis by Mordor Intelligence

The Ghana Lubricants Market size is expected to increase from 48.89 million liters in 2025 to 50.94 million liters in 2026 and reach 62.09 million liters by 2031, and is expected to grow at a CAGR of 4.04% over 2026-2031. The Ghana lubricants market is supported by a vehicle fleet of 3.5 million units in 2025. The average vehicle age of 14 to 16 years keeps oil drain intervals short and refill demand steady. This also makes the market less exposed to short-term fluctuations in new vehicle sales, as older engines require frequent servicing and higher fill volumes. Demand is expanding beyond passenger and commercial vehicles, with road construction, mining activity, and broader industrial use driving consumption of hydraulic fluids, gear oils, and greases, which typically carry better unit economics than standard engine oils. There is also a gradual shift toward higher-specification products, as vehicles assembled under the national automotive policy increasingly carry OEM service requirements that favor branded and compliant formulations. The competitive landscape remains shaped by a few established oil marketing companies, while growth opportunities are present in industrial applications, premium grades, and formal service networks that serve users moving away from informal supply channels.

Key Report Takeaways

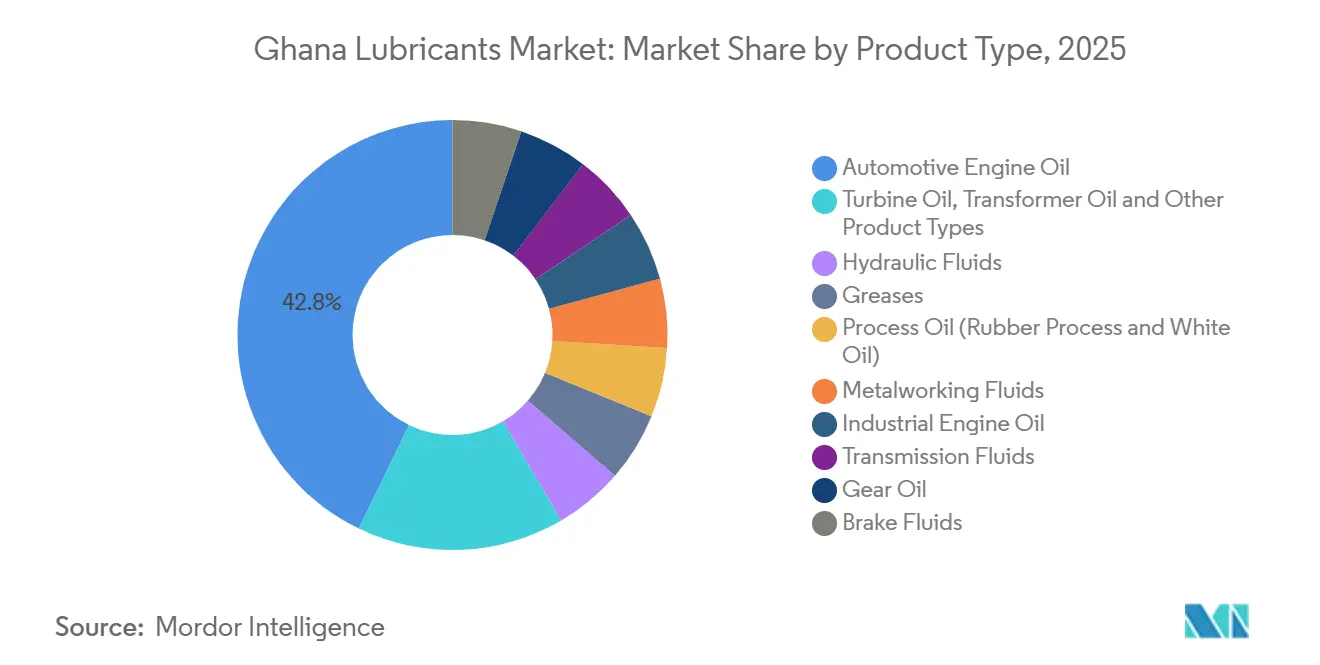

- By product type, Automotive Engine Oil held 42.84% of volumes in 2025, while Metalworking Fluids is set to record the fastest projected growth at 4.61% through 2031.

- By base-stock type, Mineral Oil-based lubricants accounted for 72.22% of volumes in 2025, while Fully Synthetic lubricants are expected to post the highest CAGR at 4.83% through 2031.

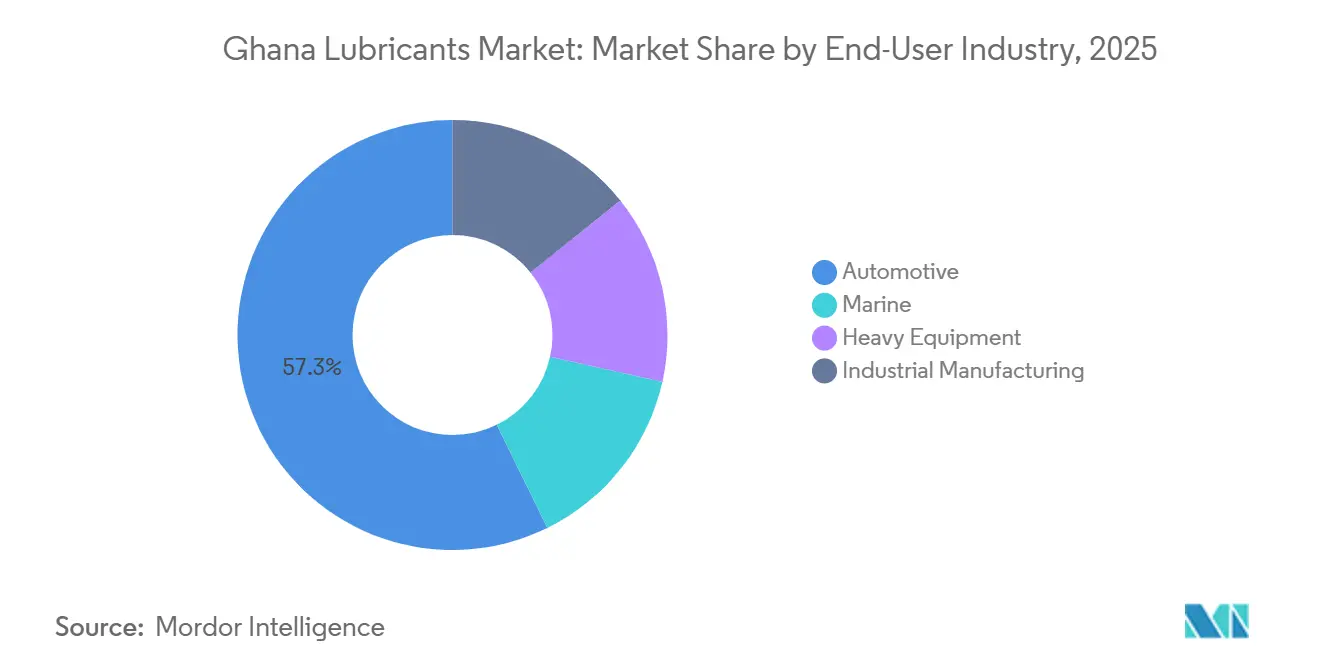

- By end-user industry, Automotive contributed 57.28% of volumes in 2025, while Industrial Manufacturing is projected to expand at the fastest rate of 4.75% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Ghana Lubricants Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strong demand from motor vehicles and transportation | +1.2% | National, with peak concentration in Greater Accra, Kumasi, and Takoradi | Short term (≤ 2 years) |

| Growing vehicle parc and urbanization | +0.8% | National | Short term (≤ 2 years) |

| Expansion of construction and transport infrastructure under the Big Push program | +0.7% | National, with priority corridors across Accra to Kumasi, the Eastern corridor, and cross-border routes | Medium term (2-4 years) |

| Rise of ride-hailing mobility platforms | +0.3% | Greater Accra, Kumasi, Cape Coast, and Takoradi | Short term (≤ 2 years) |

| Increasing maritime and port activity at Tema and Takoradi | +0.2% | Greater Accra Region and Western Region | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Strong Demand From Motor Vehicles Anchors Market Volumes

The Ghana lubricants market draws its most stable volume base from the transportation fleet, which reached 3.5 million units in 2025 and remained heavily weighted toward older vehicles. Engines in this age profile tend to experience more blow-by, seal wear, and contamination, which shorten practical oil change intervals and increase lubricant consumption per vehicle annually. This pattern gives the Ghana lubricants market a durable floor because service demand stays active even when vehicle replacement slows. The January 2024 move to enforce Euro IV and Euro V fuel standards on gasoline imports also supports demand for better detergent and oxidation control in lubricants, gradually shifting buyers toward compliant products. Newer assembled vehicles are adding a second layer of demand because they require specific grades and approved formulations rather than generic substitutes. As a result, volume remains anchored by the aging fleet, while product mix slowly improves through formal channels that carry branded and API-qualified offerings.

Growing Vehicle Parc Deepens The Lubricant Consumer Base

The Ghana lubricants market is also expanding through a broader vehicle fleet, supported by urbanization, stronger mobility needs, and higher freight movement within the country. Commercial vehicle activity remains especially important because trucks and other work vehicles accumulate mileage quickly on the Accra, Kumasi, and Takoradi corridor and consume heavy-duty engine oils at a steady pace. The national automotive development program has created a pool of locally assembled vehicles, and those units are adding original equipment manufacturer (OEM)-led service demand to the formal aftermarket. Financing and leasing programs are widening access to newer vehicles among urban buyers who would otherwise depend on older imports, which strengthens the branded service ecosystem over time. The Ghana lubricants market benefits from this split because older vehicles sustain commodity demand while newer units increase the need for grade-specific and manufacturer-approved lubricants. Freight activity linked to regional trade also supports this trend because higher vehicle utilization keeps lubricant replacement cycles active across commercial fleets.

Infrastructure Expansion Lifts Heavy Equipment Lubricant Demand

Public infrastructure spending is shifting part of the Ghana lubricants market toward industrial and equipment-led applications. The Big Push program committed GHS 50 billion to 50 road projects covering 1,144 kilometers, keeping excavators, graders, compactors, and batching equipment in long operating cycles across all 16 regions. These machines consume hydraulic fluids, gear oils, engine oils, and greases on hour-based maintenance schedules, which supports recurring replacement rather than one-time demand. Equipment deployment under district road improvement work in 2024 demonstrated how quickly lubricant demand can rise at local depots when machinery is rolled out across multiple job sites. Support pledged by the African Development Bank in June 2025 strengthens execution visibility over several years, helping sustain the industrial side of the Ghana lubricants market beyond short project cycles[1]African Development Bank, “Infrastructure Strategy Support for Ghana,” African Development Bank, afdb.org. Proposed rail development between Takoradi and Hamile would extend that effect further because construction and earthmoving activity would push lubricant demand into northern and northwestern corridors that have historically seen lower formal distribution coverage.

Ride-Hailing Platforms And Port Activity Raise Use Intensity

The Ghana lubricants market is being driven by use intensity as much as by vehicle count, and ride-hailing is one of the clearest examples of that shift. Uber had engaged more than 200,000 driver partners by June 2026 across Accra, Kumasi, Cape Coast, and Takoradi, while Bolt and Yango added a further layer of organized urban fleet activity. Drivers operating in stop-and-go traffic often compress oil change intervals well below standard private-use schedules because the number of trips and engine hours builds quickly. Leasing and financing arrangements tied to platform work also tend to steer drivers toward specified grades and branded service points, which benefits formal lubricant sellers. Port activity adds another use-intensity effect because higher vessel calls and increased container handling at Tema and Takoradi raise demand for marine lubricants and maintenance oils for handling equipment. The Ghana lubricants market is therefore growing not only through more assets in use, but also through higher utilization of vehicles and machinery already operating on roads and at port sites.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High prevalence of counterfeit lubricants | -0.7% | National, with stronger impact in peri-urban and rural markets beyond Accra and Kumasi | Short term (≤ 2 years) |

| Volatility in imported base oil and additive costs | -0.5% | National, across an import-dependent supply chain centered on Tema Lube Oil Company | Medium term (2-4 years) |

| Price sensitivity in informal transport and SME segments | -0.4% | National, with stronger effect outside the top 3 urban centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Counterfeit Lubricants Create A Systemic Market Integrity Challenge

Counterfeit products remain one of the clearest barriers to value capture in the Ghana lubricants market. They undercut prices, weaken trust, and damage engines, which users then associate with the broader category. The 2025 Petroleum Product Analysis Report recorded 199 million liters of unaccounted petroleum products in the downstream sector, and lost tax revenue exceeded GHS 600 million. These figures indicate the scale of informal movement that can also affect lubricants. Refilled containers and close-copy packaging make visual detection difficult for workshops and end users, particularly outside the largest cities. The National Petroleum Authority (NPA) and the Ghana Standards Authority maintain lubricant quality oversight, but enforcement coverage is thinner in rural and peri-urban locations where informal traders have a wider reach[2]National Petroleum Authority, “Petroleum Product Analysis Report 2025,” National Petroleum Authority, npa.gov.gh. The NPA Bill 2024 could improve this situation if it strengthens licensing and inspection authority across the downstream chain. Until enforcement improves, the Ghana lubricants market will continue to face pressure on branded volume, pricing discipline, and end-user confidence.

Base Oil Import Dependency And Price Sensitivity Limit Premium Adoption

The Ghana lubricants market faces a structural cost constraint because domestic blending depends on imported base oils and additives. Tema Lube Oil Company recorded USD 46.91 million in import activity in 2025, reflecting this reliance. The dependency creates a direct pass-through from global base oil and crude price movements into local lubricant pricing, making margin management difficult for blenders and marketers. Exchange-rate fluctuations add further pressure, as a weaker cedi raises local costs even when international input prices are stable. Foreign-currency liabilities remain significant for large participants such as TotalEnergies Marketing Ghana. These pressures are most acute in a market where informal transport operators and small enterprises often prioritize upfront price over longer drain intervals or better engine protection. As a result, fully synthetic and premium products grow more slowly than they might in a less price-sensitive environment, even when Original Equipment Manufacturer (OEM) requirements support their technical case. As long as domestic base oil production remains absent, the Ghana lubricants market will continue to balance growth in higher-value formulations against the constraints imposed by imported cost exposure and cautious end-user spending.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Industrial Grades Accelerate Alongside The Automotive Bedrock

Automotive Engine Oil held 42.84% of the Ghana lubricants market share in 2025, making it the largest product category by volume. This position reflects the size and age of the national vehicle fleet, where older engines require frequent servicing and commercial activity sustains lubricant demand year-round. The category remains central to the Ghana lubricants market because passenger vehicles, taxis, buses, and freight fleets all draw from the same broad maintenance base, even where the specification mix differs. Industrial products are growing faster than engine oil, indicating that demand composition is widening rather than scaling in place.

Metalworking Fluids are forecast to grow at 4.61% through 2031, the fastest rate among product types, reflecting increased activity in fabrication, light machinery, and agro-processing. Hydraulic Fluids are also benefiting from machinery use under the Big Push road program, while greases continue to see demand from mining operations that rely on heavy equipment and high-pressure applications. Transmission Fluids and Gear Oils are finding additional demand from commercial fleets and industrial gear systems in manufacturing and power facilities. Transformer Oils and Turbine Oils remain smaller and more specialized, but grid rehabilitation and utility maintenance provide a steady demand base that supports the broader Ghana lubricants market as industrial applications take a larger share.

By Base-Stock Type: Mineral Oil Dominates, Fully Synthetic Builds Durable Momentum

Mineral Oil-based lubricants accounted for 72.22% of the Ghana lubricants market size in 2025, reflecting the installed blending capacity at Tema Lube Oil Company and the price sensitivity of most end users. This segment remains dominant because it fits the operating economics of older vehicles, informal workshops, and users who prioritize cost over long drain intervals. The Ghana lubricants market continues to lean toward this base-stock because mainstream automotive and transport demand is broad, recurring, and largely volume-driven. The dominance of mineral oil does not prevent an upgrade trend in parts of the formal service channel.

Fully Synthetic lubricants are projected to grow at 4.83% through 2031, making them the fastest-growing base-stock segment. Their growth is driven by vehicles assembled under the automotive development policy, where authorized service centers are required to maintain manufacturer-specified grades and cannot substitute lower-cost products without affecting service compliance. Semi-Synthetic products occupy the middle ground, offering a balance between improved performance and manageable cost for fleets and high-mileage users. Bio-based lubricants remain limited due to the absence of a domestic feedstock-to-lubricant processing base, although research on castor and jatropha-derived oils supports a future niche in specialty industrial use, providing the Ghana lubricants industry a longer-term pathway for diversification without altering the current market structure.

By End-User Industry: Automotive Volumes Lead As Industrial Manufacturing Drives The Growth Rate

Automotive contributed 57.28% of lubricant volumes in 2025, placing it ahead of other end-user categories in the Ghana lubricants market. Passenger vehicles and commercial trucks remain the main volume drivers because they turn over lubricant stocks frequently and operate along the country's busiest road corridors. This position is reinforced by the aging vehicle base, which increases service frequency and keeps commodity engine oils moving through retail stations, workshops, and service centers. Where newer vehicles are entering the fleet, they add to the formal service channel rather than displacing the large installed base that drives most volume.

Industrial manufacturing is projected to expand at 4.75% through 2031, the fastest growth rate among end-user groups, reflecting stronger demand from power generation, oil and gas, textiles, metallurgy, and related operations. Within this category, oil and gas use requires high-specification products such as compressor oils, high-temperature greases, and sealing applications, making it commercially significant even where volumes are not the largest. Heavy Equipment remains another major outlet, as construction, mining, and agriculture all require consistent lubrication of mobile and fixed assets, and the mining sector's USD 3.5 billion in local procurement in 2024 supports that recurring need. Marine demand is narrower by geography, but rising throughput at Tema and the associated equipment cycles at port and vessel level ensure that this segment remains a meaningful part of the Ghana lubricants market as industrial and logistics activity continues to expand.

Geography Analysis

The Ghana lubricants market is geographically concentrated along the Accra, Tema, Kumasi, and Takoradi corridor, where transport activity, port infrastructure, blending capacity, and industrial use are most dense. Greater Accra remains the primary entry and distribution point, with Tema hosting the blending and import base. Tema Lube Oil Company recorded USD 46.91 million in base oil and additive imports in 2025. Tema Port processed 1.1 million TEUs in 2025, and this cargo volume supports demand for marine lubricants, container-handling equipment oils, and maintenance products across the port. Greater Accra also has the highest ride-hailing activity in the country, which drives high-frequency replacement demand for engine oils and related products. The overlap of formal retail stations, branded workshops, and commercial fleets makes the southern corridor the operational core of the Ghana lubricants market.

The Ashanti Region is the second major demand center. Gold output projected at 4.4 million to 5.1 million ounces for 2025 reflects the continuity of mining activity that supports lubricants demand in the region. Kumasi serves as both an urban vehicle service hub and a gateway to mining operations, giving the region a strong mix of automotive and heavy equipment consumption. Mining fleets require hydraulic fluids, greases, and specialty oils on a sustained basis. The Kumasi Inner Ring Road under the Big Push program is also increasing equipment concentration in the area. Formal coverage from GOIL, TotalEnergies, and Vivo Energy Holding B.V improves product availability, helping the Ghana lubricants market capture value through workshops and fleet accounts rather than informal supply routes.

Western and Northern Ghana are growing in importance, each with a distinct demand profile within the Ghana lubricants market. The Western Region supports offshore oil and gas activity around the Jubilee and TEN fields, and investment plans for up to 20 new wells announced in June 2025 strengthen demand for compressor oils, hydraulic fluids, and high-temperature greases used in support operations. Takoradi remains relevant through maritime traffic and planned logistics expansion, while the proposed Takoradi to Hamile railway would extend construction-related lubricant demand further inland. In Northern Ghana, road expansion and cross-border connectivity projects are increasing demand for agricultural machinery lubricants and construction fluids, creating opportunities for distributors operating beyond the established southern network.

Competitive Landscape

The Ghana lubricants market is moderately consolidated. A defining structural feature is the role of Tema Lube Oil Company, where several oil marketing companies rely on the same domestic blending base and therefore compete on formulation quality, regulatory compliance, service support, and channel execution rather than blending ownership. TotalEnergies Marketing Ghana held an estimated 33% share of the lubricants market in 2026, supported by OEM-linked product positioning, mining account management, and quality credentials. GOIL remained a major domestic participant, with its fuel network providing national reach. Its management has indicated plans to recover lubricants market share through stronger execution in mining, aviation, and auto-gas-linked channels. The Ghana lubricants market is characterized not by a monopolistic structure, but by a few recognized brands competing on specification trust, while informal distribution continues to shape access in many locations.

Vivo Energy Holding B.V has pursued a premium positioning strategy in the market. In March 2026, it launched the Shell Advance AX7 and Advance Ultra ranges in Ghana, targeting urban driving conditions where engine protection and stop-and-go performance are priorities. It also commissioned a Shell Lube Bay at Michel Camp in Tema, linking product sales directly to professional servicing rather than treating lubricants as a standalone retail item. In May 2026, a memorandum with the Applied Technology Institute to train certified mechanics under the Mechanic Advocacy Program added a longer-term route to influencing workshop preference and brand loyalty within the Ghana lubricants market.

Puma Energy divested its Tema and Takoradi storage terminals in September and December 2025, signaling a reduced downstream infrastructure commitment in Ghana. This shift may create additional room for oil marketing companies with stronger local networks to deepen their presence in commercial and industrial accounts. White space remains most visible in industrial specialties such as metalworking fluids, transformer oils, and process oils, where local stocking and technical services remain limited. If the NPA Bill 2024 raises licensing thresholds and increases regulatory scrutiny, the Ghana lubricants market could consolidate further around larger, better-capitalized marketers, while informal repackagers face reduced room to operate.

Ghana Lubricants Industry Leaders

TotalEnergies

Vivo Energy Holding B.V.

GOIL PLC

Puma Energy

BP p.l.c. (Castrol)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Ghana's Ministry of Trade, Agribusiness and Industry confirmed that the automotive assembly sector has outperformed expectations since 2019, with seven operational assembly facilities now active under the GADP. The growing domestic fleet produced by these plants is progressively increasing OEM-specified lubricant demand across formal service channels.

- March 2026: Vivo Energy Holding B.V. in Ghana launched the Shell Advance AX7 and Advance Ultra lubricant ranges at its Airport Shell service station in Accra. The new grades are formulated for reduced friction, extended engine life, and improved protection under Ghana's stop-and-go urban traffic conditions. These products are now distributed nationally through the company's 25 Shell service stations and accredited resellers, representing the brand's most significant lubricant product launch in the market in recent years.

Ghana Lubricants Market Report Scope

A lubricant is a substance introduced between moving surfaces to reduce friction, heat, and wear. Beyond minimizing mechanical wear, lubricants also serve as coolants, protect against corrosion, and act as seals.

The Ghana lubricants market is segmented by product type, base-stock type, and end-user industry. By product type, the market is segmented into gear oil, brake fluids, hydraulic fluids, greases, process oil (rubber process and white oil), metalworking fluids, turbine oil, transformer oil, and other product types. By base-stock type, the market is segmented into mineral oil-based, semi-synthetic, fully synthetic, and bio-based. By end-user industry, the market is segmented into automotive, marine, heavy equipment, and industrial manufacturing. The market sizes and forecasts are provided in terms of volume (Liters).

| Automotive Engine Oil |

| Industrial Engine Oil |

| Transmission Fluids |

| Gear Oil |

| Brake Fluids |

| Hydraulic Fluids |

| Greases |

| Process Oil (Rubber Process and White Oil) |

| Metalworking Fluids |

| Turbine Oil |

| Transformer Oil |

| Other Product Types |

| Mineral Oil-based |

| Semi-synthetic |

| Fully Synthetic |

| Bio-based |

| Automotive | Passenger Vehicles |

| Commercial Vehicles | |

| Two-Wheelers | |

| Marine | |

| Heavy Equipment | Construction |

| Mining | |

| Agriculture | |

| Industrial Manufacturing | Power Generation |

| Metallurgy and Metalworking | |

| Textiles | |

| Oil and Gas | |

| Other End-Use Industries |

| By Product Type | Automotive Engine Oil | |

| Industrial Engine Oil | ||

| Transmission Fluids | ||

| Gear Oil | ||

| Brake Fluids | ||

| Hydraulic Fluids | ||

| Greases | ||

| Process Oil (Rubber Process and White Oil) | ||

| Metalworking Fluids | ||

| Turbine Oil | ||

| Transformer Oil | ||

| Other Product Types | ||

| By Base-Stock Type | Mineral Oil-based | |

| Semi-synthetic | ||

| Fully Synthetic | ||

| Bio-based | ||

| By End-User Industry | Automotive | Passenger Vehicles |

| Commercial Vehicles | ||

| Two-Wheelers | ||

| Marine | ||

| Heavy Equipment | Construction | |

| Mining | ||

| Agriculture | ||

| Industrial Manufacturing | Power Generation | |

| Metallurgy and Metalworking | ||

| Textiles | ||

| Oil and Gas | ||

| Other End-Use Industries | ||

Key Questions Answered in the Report

What is current market size of Ghana Lubricants Market?

The Ghana Lubricants Market size is expected to increase from 48.89 million liters in 2025 to 50.94 million liters in 2026 and reach 62.09 million liters by 2031, and is expected to grow at a CAGR of 4.04% over 2026-2031.

What is driving lubricant consumption in Ghana the most?

The largest volume base comes from the country’s 3.5 million vehicle fleet in 2025, especially older vehicles that require frequent oil changes and higher refill volumes.

Which product category leads lubricant demand in Ghana?

Automotive Engine Oil led with 42.84% of volumes in 2025, reflecting the weight of passenger, taxi, bus, and freight use across the country.

Which lubricant segment is growing the fastest in Ghana?

Metalworking Fluids are projected to expand at 4.61% through 2031, showing the rising role of manufacturing, fabrication, and agro-processing demand.

Page last updated on: