Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

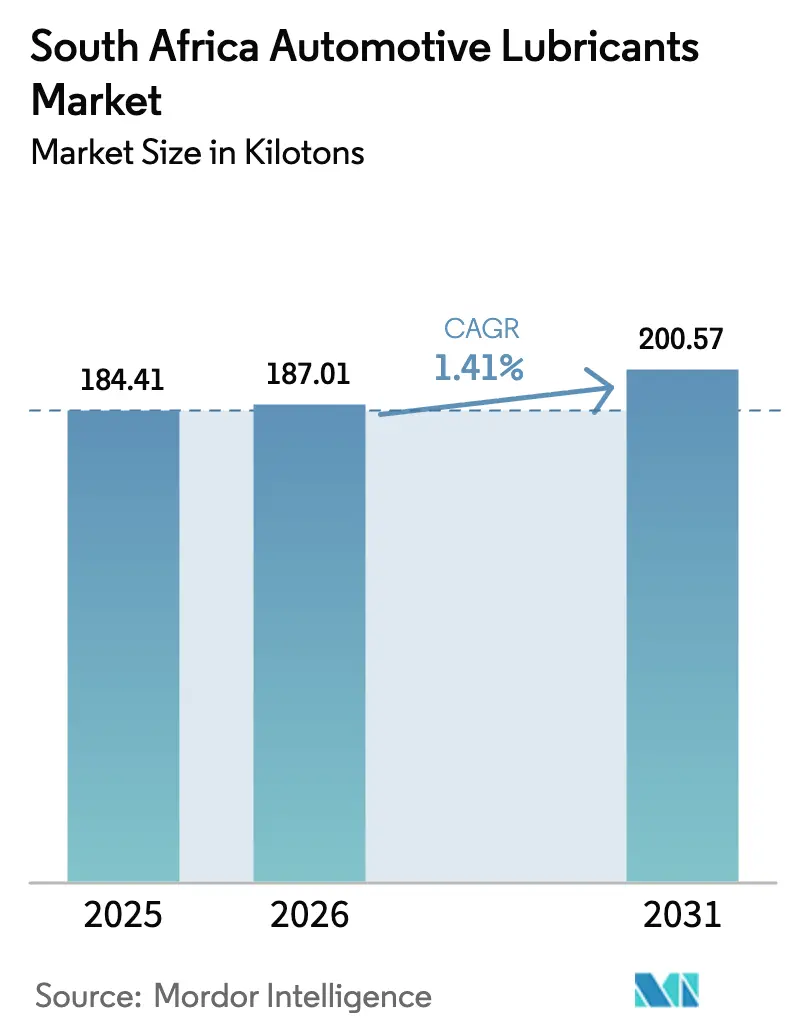

| Base Year Market Size (2025) | 184.41 kilotons |

| Market Volume (2026) | 187.01 kilotons |

| Market Volume (2031) | 200.57 kilotons |

| Growth Rate (2026 - 2031) | 1.41% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Africa Automotive Lubricants Market Analysis by Mordor Intelligence

The South Africa Automotive Lubricants Market size was valued at 184.41 kilotons in 2025 and is estimated to grow from 187.01 kilotons in 2026 to reach 200.57 kilotons by 2031, at a CAGR of 1.41% during the forecast period (2026-2031). Electric vehicles are gaining traction, but the market faces challenges from counterfeit products and power supply interruptions. However, several positive trends are emerging: a shift toward OEM-approved synthetics, resilience in the aftermarket, and government incentives for local blending. The used-car market's growing preference for automatic transmissions is driving up demand for Automatic Transmission Fluids. Additionally, as the passenger vehicle fleet ages, engine oil consumption remains steady. Global consolidation is reshaping the landscape, with Vivo Energy's acquisition of Engen enhancing supply security and downstream leverage. This shift occurs as industry giants Shell and BP reassess their local operations. Furthermore, base-oil re-refiners such as FFS Refiners and Oil Separation Solutions are closing feedstock loops and leading circular-economy initiatives.

Key Report Takeaways

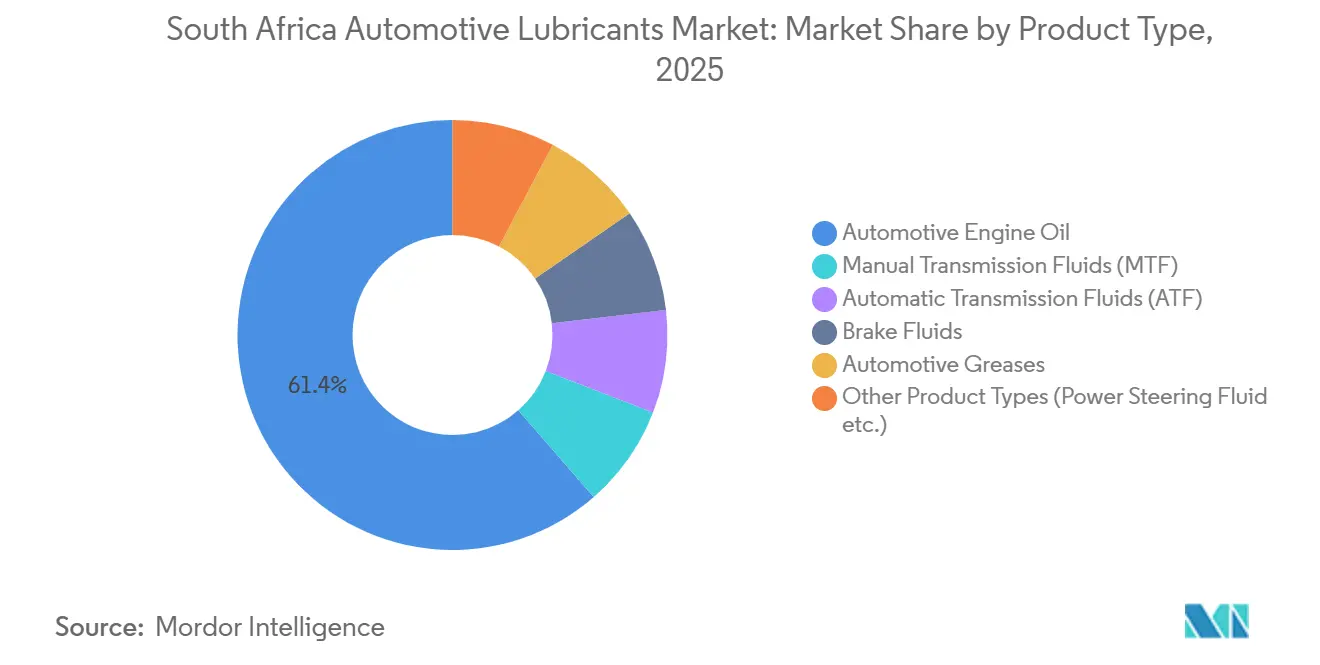

- By product type, automotive engine oil held 61.42% of the South Africa automotive lubricants market share in 2025. Automatic transmission fluids are projected to expand at a 1.79% CAGR to 2031.

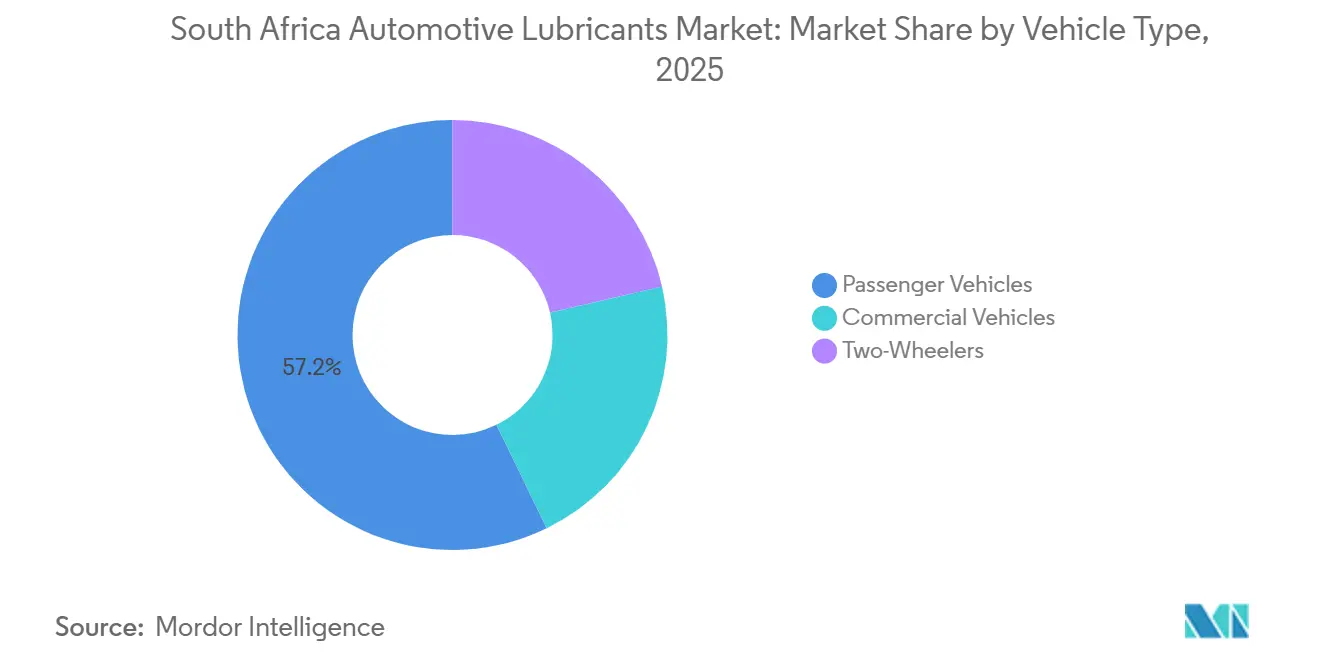

- By vehicle type, passenger vehicles led with 57.23% of the South Africa automotive lubricants market share in 2025. Commercial vehicles are forecast to advance at a 1.58% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South Africa Automotive Lubricants Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift toward OEM-approved synthetic and semi-synthetic grades | +0.50% | Gauteng, Western Cape, KwaZulu-Natal | Medium term (2-4 years) |

| After-market resilience amid prolonged new-vehicle affordability squeeze | +0.40% | National, peri-urban, and township areas | Long term (≥ 4 years) |

| Government incentives for local blending and base-oil re-refining | +0.20% | Gauteng, KwaZulu-Natal | Long term (≥ 4 years) |

| Township-focused distribution programmes (mobile “power shops”) | +0.20% | Gauteng, Western Cape, Eastern Cape | Medium term (2-4 years) |

| Telematics-linked OEM warranties enforcing compliant lubricant use | +0.10% | Metro dealerships nationwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shift Toward OEM-Approved Synthetic and Semi-Synthetic Grades

Tighter OEM specifications are not only shortening drain intervals but also widening viscosity windows. This shift is accelerating the transition from mineral to synthetic and semi-synthetic formulations. Shell’s global Helix refresh to API SQ, which was showcased in Egypt in 2026, is set to make its debut in South Africa. This rollout is anticipated to command premium pricing and intensify authenticity checks. Liqui Moly’s global sales surge in 2025, coupled with its planned capacity expansion, underscores a robust demand for higher-specification products[1]Liqui Moly, “LIQUI MOLY continues to grow in 2025,” liqui-moly.com . On the local front, AG Lubricants has begun blending Mobil Delvac Modern MX 15W-40, significantly reducing lead times for fleets.

After-Market Resilience Amid Prolonged New-Vehicle Affordability Squeeze

High interest rates and import duties are dampening new-car sales, inadvertently extending the service life of the existing fleet. The after-market is reaping benefits from the Right-to-Repair legislation, which mandates OEMs to share data with independent entities. Brand penetration among informal mechanics is being bolstered by initiatives such as Castrol’s kiosk in Soweto and Liqui Moly’s Advantage App.

Government Incentives for Local Blending and Base-Oil Re-Refining

Regulatory stipulations tied to the Vivo Energy - Engen deal ensure a long-term offtake from Astron’s Milnerton refinery and Sasol’s Secunda assets, solidifying the domestic base-oil supply. FFS Refiners operates a five-site network that upgrades millions of liters of waste oil annually, playing a pivotal role in reducing significant CO₂ emissions. Meanwhile, FUCHS is expanding its Isando facility to enhance capacity and respond swiftly to OEM demands.

Township-Focused Distribution Programmes (Mobile “Power Shops”)

Informal mechanics in townships, often reliant on middlemen, find themselves susceptible to counterfeit products. To address this, Castrol’s kiosk in Soweto and SA Lube’s mobile vans are delivering branded lubricants in smaller packs, helping to reduce inventory costs. Additionally, the Liqui Moly Advantage App not only tracks sales but also rewards training, further elevating the professionalism of township channels.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Gradual EV/NEV penetration reducing ICE-lubricant volumes | -0.30% | Gauteng, Western Cape metros | Long term (≥ 4 years) |

| Proliferation of counterfeit/sub-standard lubricants eroding premium sales | -0.20% | Informal retail channels nationwide | Medium term (2-4 years) |

| Load-shedding-induced fleet downtime reducing engine hours | -0.10% | Gauteng, KwaZulu-Natal logistics hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Gradual EV/NEV Penetration Reducing ICE-Lubricant Volumes

In 2025, passenger registrations saw a rise in new-energy vehicles (NEVs), though battery electric vehicles (BEVs) experienced a year-on-year dip. A tax deduction for EV manufacturing, which is set to take effect this month, has the potential to boost local assembly. However, with hybrids and BEVs requiring little to no engine oil, lubricant volumes are expected to decline.

Load-Shedding-Induced Fleet Downtime Reducing Engine Hours

Despite Eskom's report of several load-shedding-free days by February 2026, past outages prompted fleets to lengthen their drain intervals. Over recent years, a significant increase in rooftop-solar capacity has shifted lubricant consumption trends.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Automatic-Transmission Shift Drives ATF Outperformance

In 2025, automotive engine oil dominated South Africa's automotive lubricants market, claiming a substantial 61.42% share. The 10W-40 multigrade oil emerged as the most widely used, while the 5W-30 variant found its niche in the cooler coastal regions. Meanwhile, the 20W-50 oil became the preferred choice for older engines in the hotter inland areas. AG Lubricants highlighted the industry's pivot towards semi-synthetic and synthetic grades by locally blending Mobil Delvac Modern MX 15W-40. Sasol, not to be outdone, rolled out fully synthetic 0W-20 formulations tailored for turbocharged engines[2]Sasol, “Lubricants,” sasol.com .

Automatic transmission fluids are set to expand at the fastest rate, with a projected CAGR of 1.79% through 2026-2031, underscoring the growing consumer shift towards automatic vehicles. In 2025, the trend was evident in the used-car market: the Ford Ranger topped sales, followed by the Toyota Fortuner and Volkswagen Polo. This momentum is further strengthened by the shorter service intervals for automatic transmission fluids. Conversely, manual transmission fluids, brake fluids, and automotive greases are experiencing a downturn. This decline is linked to the waning popularity of manual gearboxes and the prolonged drain intervals for greases, a benefit of synthetic advancements. Moreover, there is heightened regulatory scrutiny, especially concerning SANS 1905 standards for brake fluids, amplifying quality control measures, particularly in humid coastal areas.

By Vehicle Type: Passenger Base Dominates, Commercial Uptick Anchored in Mining

Passenger vehicles accounted for 57.23% of the 2025 volume, buoyed by an aging vehicle parc, regular oil changes, and a surge in workshops spurred by the Right-to-Repair movement. Independent garages are gravitating towards multigrade semi-synthetics, striking a balance between performance and cost. Liqui Moly’s Advantage App is further cementing brand loyalty among township technicians.

Commercial vehicles are on a growth trajectory, projected at a 1.58% CAGR, primarily driven by the haulage demands of the mining sector. ExxonMobil's field trials underscored the benefits of heavy-duty synthetics, validating extended drain intervals - quadrupling oil-change frequencies on Komatsu HD465 dump trucks and yielding notable annual savings. This not only reduces costs but also curtails downtime, solidifying their status as the preferred choice for fleets. While two-wheelers occupy a smaller market segment, there is a steady demand for ashless two-stroke oils, particularly in recreational and utility contexts.

Geography Analysis

In South Africa, Gauteng, Western Cape, and KwaZulu-Natal lead the automotive lubricants market, fueled by high vehicle ownership, port logistics, and blending capacities. FUCHS’ expanded Isando plant in Gauteng, with its substantial base-oil storage and blending capacity, guarantees prompt supplies to original equipment manufacturer (OEM) dealerships and fleets.

Western Cape benefits from its proximity to Astron’s Milnerton refinery, secured by a long-term offtake agreement post Vivo Energy’s acquisition, facilitating both inland and export flows. In KwaZulu-Natal, the revamped blending site of TotalEnergies at the Durban port streamlines imports.

While the Eastern Cape and Free State play smaller roles, they are gaining traction, spurred by automotive assembly in Gqeberha and rising demand for agricultural lubricants. Township-distribution efforts flourish in Soweto, Khayelitsha, and Alexandra, where mobile kiosks cater to informal service bays. Gauteng and Western Cape face heightened regulatory scrutiny, with National Regulator for Compulsory Specifications (NRCS) audits and Viscous Lubricants South Africa (VLS-SA) checks aiming to curb counterfeit products.

Competitive Landscape

The South Africa automotive lubricants market is moderately consolidated. Vivo Energy’s takeover of Engen not only created a vast African station network but also emphasized significant storage and a multi-year turnover commitment. Strategic priorities spotlight capacity investments and digital outreach. FUCHS’ Isando expansion bolsters local blending, while Liqui Moly’s Advantage App gamifies sales and training for township garages. With carbon-pricing policies on the rise, re-refining specialists like FFS Refiners and Oil Separation Solutions are carving out notable market positions. Shell’s retail station divestment and BP’s Castrol reassessment present divergent perspectives on market growth. Concurrently, ExxonMobil's marine-lube distributorship expansion via Habot Marine signals its focus on niche markets.

South Africa Automotive Lubricants Industry Leaders

BP p.l.c.

Shell plc

TotalEnergies

Astron Energy (Pty) Ltd.

Engen Petroleum Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: AG Lubricants, the authorised distributor and manufacturer of Mobil lubricants in South Africa, secured the green light to locally blend a curated range of lubricants for a leading automotive manufacturer.

- February 2025: Germany's FUCHS Group opened the expansion of its production facility in Isando, South Africa, reinforcing its position in the automotive specialty lubricants market. The USD 27 million investment aims to enhance efficiency, production capacity, and customer service.

South Africa Automotive Lubricants Market Report Scope

Automotive lubricants reduce friction between contacting surfaces, thereby minimizing energy loss. These lubricants are vital for ensuring vehicles operate smoothly and have a prolonged lifespan. Engine oil, the most prevalent lubricant, not only reduces friction among engine components but also prevents corrosion, combats rust, and aids in cleaning the engine.

The South Africa automotive lubricants market is segmented by product type and vehicle type. By product type, the market is segmented into automotive engine oil, manual transmission fluids, automatic transmission fluids, brake fluids, automotive greases, and other product types. By vehicle type, the market is segmented into passenger vehicles, commercial vehicles, and two-wheelers. For each segment, the market sizing and forecasts have been done on the basis of volume (tons).

By Product Type

| Automotive Engine Oil | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades | |

| Manual Transmission Fluids (MTF) | |

| Automatic Transmission Fluids (ATF) | |

| Brake Fluids | |

| Automotive Greases | |

| Other Product Types (Power Steering Fluid etc.) |

By Vehicle Type

| Passenger Vehicles |

| Commercial Vehicles |

| Two-Wheelers |

| By Product Type | Automotive Engine Oil | 0W-XX |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| Manual Transmission Fluids (MTF) | ||

| Automatic Transmission Fluids (ATF) | ||

| Brake Fluids | ||

| Automotive Greases | ||

| Other Product Types (Power Steering Fluid etc.) | ||

| By Vehicle Type | Passenger Vehicles | |

| Commercial Vehicles | ||

| Two-Wheelers |

Key Questions Answered in the Report

What is the projected demand for lubricants in South Africa by 2031?

The South Africa automotive lubricants market size stands at 187.01 kilotons in 2026, and it is projected to reach 200.57 kilotons by 2031 at a 1.41% CAGR.

How quickly are Automatic Transmission Fluids expanding?

ATF volumes are forecast to rise at 1.79% CAGR through 2031, outpacing all other product categories due to widespread adoption of automatic gearboxes.

Which vehicle class will see faster lubricant-volume growth?

Commercial-vehicle demand is expected to climb at a 1.58% CAGR, propelled by mining haulage and extended drain intervals for heavy-duty synthetics.

Which provinces are the focal points for blending capacity?

Gauteng hosts FUCHS’ expanded Isando hub, Western Cape benefits from Astron’s Milnerton refinery, and KwaZulu-Natal leverages Durban’s port-linked blending and storage infrastructure.

Page last updated on: