Botswana Lubricants Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

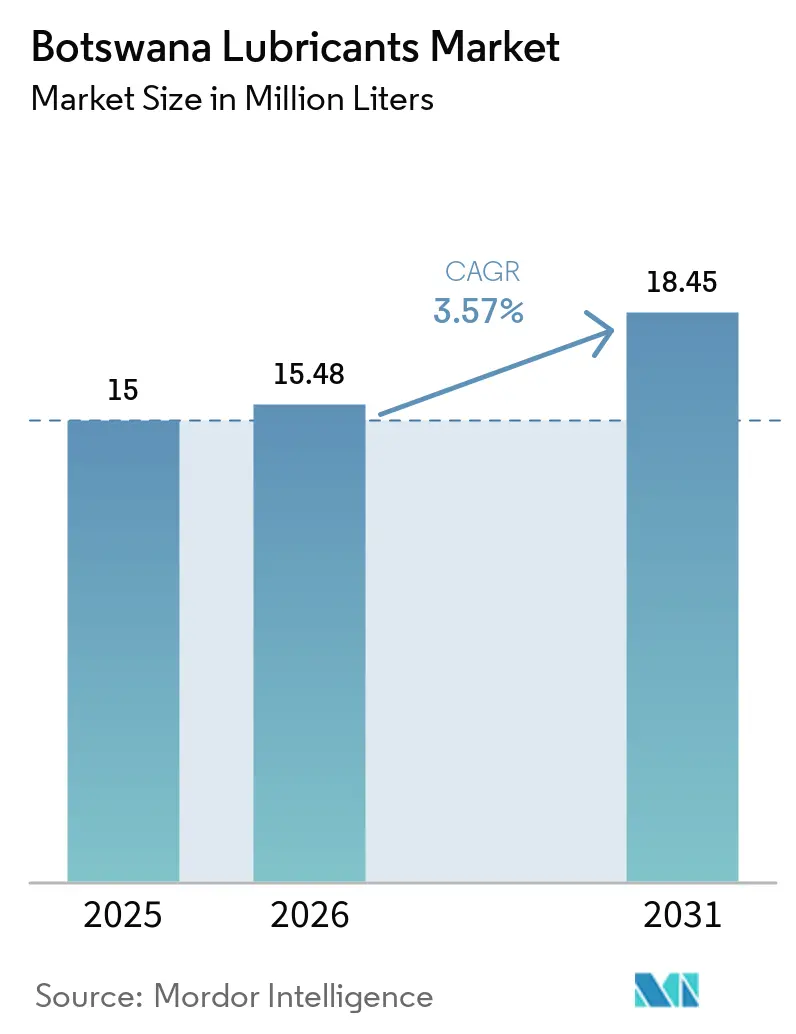

| Base Year Market Size (2025) | 15 Million liters |

| Market Volume (2026) | 15.48 Million liters |

| Market Volume (2031) | 18.45 Million liters |

| Growth Rate (2026 - 2031) | 3.57% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Botswana Lubricants Market Analysis by Mordor Intelligence

The Botswana Lubricants Market size is projected to be 15 million liters in 2025, 15.48 million liters in 2026, and reach 18.45 million liters by 2031, growing at a CAGR of 3.57% from 2026 to 2031. The increasing maintenance requirements of an aging vehicle fleet, recurring lubricant tenders from diamond-mining operations, and a BWP 11.54 billion (USD 0.85 billion) infrastructure pipeline are driving consistent demand in the market. However, pricing pressure remains as commercial buyers opt for lower-cost imports from South Africa. Product differentiation, particularly in synthetic lubricants that reduce downtime, continues to enhance gross-margin spreads. Channel uncertainty, stemming from Botswana Oil Limited’s 90% import mandate, is prompting global brands to reassess citizen-ownership partnerships. Additionally, the risk of counterfeit products is encouraging suppliers to adopt tamper-evident packaging. The expansion of cold-chain infrastructure and grid projects is creating niche demand for low-temperature greases and transformer oils, indicating gradual diversification within the Botswana lubricants market.

Key Report Takeaways

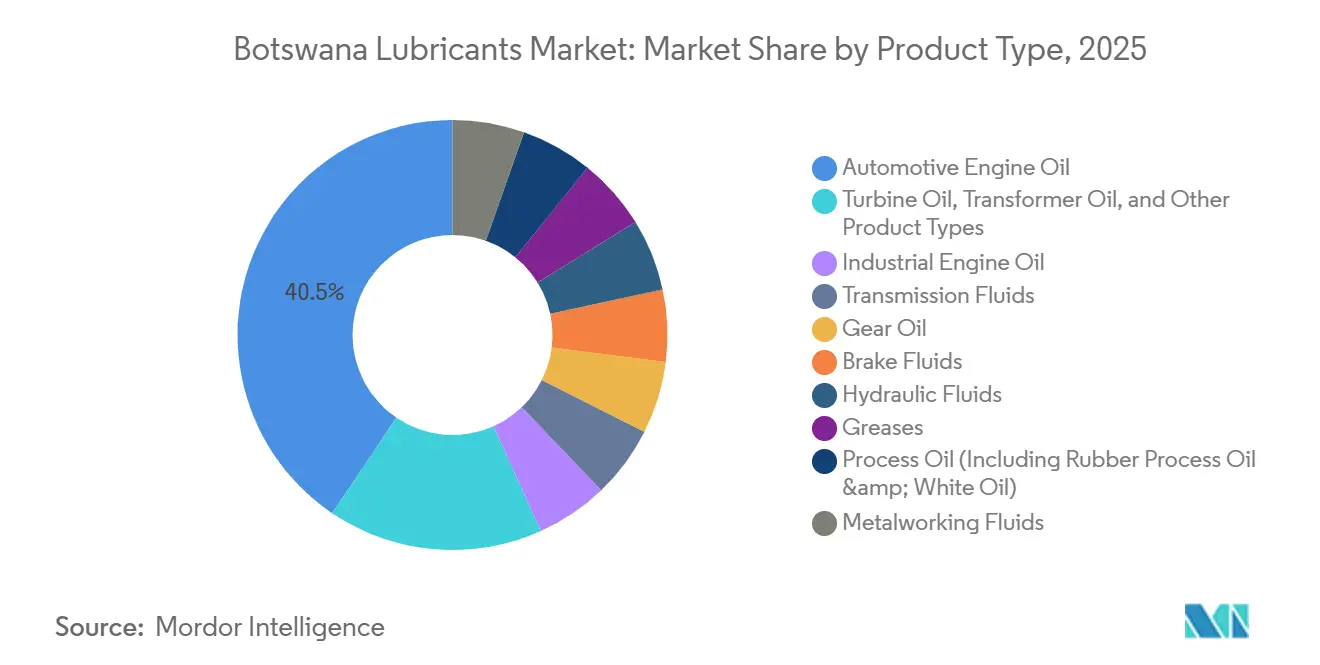

- By product type, automotive engine oil led with 40.54% of the Botswana lubricants market share in 2025, while process oil is projected to expand at a 4.21% CAGR through 2031.

- By end-user industry, automotive commanded 61.93% of 2025 volume, whereas industrial applications are expected to advance at a 4.41% CAGR to 2031.

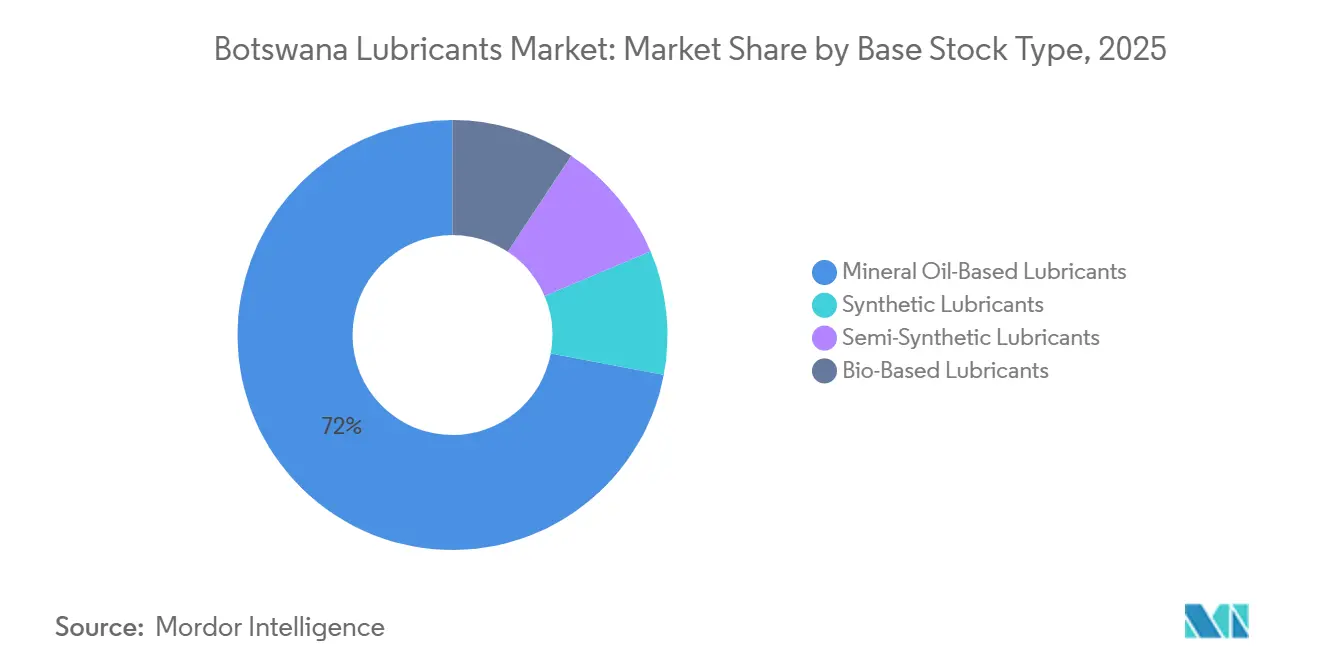

- By base-stock type, mineral oil-based lubricants held 72.04% of demand in 2025, but synthetic lubricants are expected to post the fastest 4.54% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Botswana Lubricants Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing average vehicle age | +0.9% | National, concentrated in Gaborone, Francistown, and Molepolole | Medium term (2-4 years) |

| Growth in used-vehicle imports and parc expansion | +0.8% | National, with the highest intensity in Gaborone (63.6% of first registrations) | Short term (≤ 2 years) |

| Increasing demand from mining and construction sectors | +0.7% | National, focused on Orapa, Jwaneng, Letlhakane mining belts and infrastructure corridors | Medium term (2-4 years) |

| Rising adoption of high-performance & synthetic lubricants | +0.5% | National, early uptake in mining fleets and long-haul commercial transport | Long term (≥ 4 years) |

| Cold-chain logistics expansion needing low-temperature greases | +0.2% | National, emerging in urban cold-storage hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Average Vehicle Age

Older engines consume more oil and require shorter drain intervals, leading to higher per-vehicle lubricant consumption. In Q2 2025, license renewals reached 149,709, with passenger cars accounting for 65.5% and trucks for 6.0%, reflecting the composition of the active fleet[1]Statistics Botswana, “Transport and Infrastructure Stats Brief, Quarter 1 2025,” statsbots.org.bw. Used imports, which constituted 77.3% of first-time registrations, typically arrive with high mileage, driving demand for both mineral oils and high-mileage synthetic lubricants. Toyota, Honda, and Mazda represented 59.4% of these registrations, standardizing viscosity grades such as 5W-30 and 10W-40. As vehicle aging progresses, formulations with seal conditioners and detergents are gaining traction.

Growth in Used-Vehicle Imports and Parc Expansion

First-time registrations in Q1 2025 totaled 11,583 units, with 77.4% being used vehicles, 85.0% of which were sourced from Japan. This influx expands the addressable vehicle parc and increases service frequency, particularly in Gaborone, which accounted for 63.6% of Q1 registrations. Cost-conscious vehicle owners prefer frequent, low-cost oil changes, while workshops promote semi-synthetic oils to reduce wear. These trends are expected to drive market growth, with the impact being more pronounced during 2026-2027 as recently imported 2015-2020 models reach their maintenance peak.

Increasing Demand from Mining and Construction Sectors

Debswana’s August 2025 three-year tender for four mines highlights the institutional demand for hydraulic fluids, greases, and OEM-approved engine oils. Additionally, the 2025 budget allocated BWP 11.54 billion (USD 0.85 billion) for infrastructure projects, including roads, rail, and water systems, which require heavy equipment consuming significant lubricant volumes[2]Republic of Botswana Ministry of Finance, “2025 Budget Speech,” cabri-sbo.org. Rail freight reached 214,854 net tons in Q2 2025, further driving demand for gear and compressor oils. The continuous operation of equipment in dusty and high-load environments increases the demand for premium formulations.

Rising Adoption of High-Performance & Synthetic Lubricants

Synthetic lubricants extend drain intervals and resist oxidation, reducing lifecycle costs for mining trucks and long-haul vehicles. Castrol’s June 2025 launch of GTX 5W-30 and 10W-40 with “3X Clean” technology demonstrates brand investment in performance oils. As price differentials narrow and OEMs increasingly recommend synthetics for turbocharged engines, this segment is projected to support market growth, particularly after 2028, when fleet payback analyses are expected to mature.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Counterfeit and low-quality lubricant proliferation | -0.4% | National, acute in informal retail channels and border towns | Short term (≤ 2 years) |

| Price sensitivity amplified by import tariffs and foreign exchange volatility | -0.5% | National, most severe for commercial and fleet buyers | Medium term (2-4 years) |

| Slow rollout of national used-oil take-back scheme curbing volumes | -0.2% | National, regulatory influence is limited | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Counterfeit and Low-Quality Lubricant Proliferation

Non-compliant lubricant products affect legitimate brands and may cause engine issues. While the Botswana Energy Regulatory Authority (BERA) enforces BOS 628:2015 and BOS 629:2015 standards, it has limited capacity for sampling and inspections. Engen Botswana reported a 7% decline in lubricant volumes in 2023, attributed to customers opting for lower-cost, unverified imports. This trend impacts market growth, particularly in the short term, as informal retailers expand faster than inspection capabilities.

Price Sensitivity Amplified by Import Tariffs and Foreign Exchange Volatility

Retail lubricant prices are shaped by landed cost components such as freight, import duties, and exchange rate fluctuations. In December 2023, BERA issued a tender to redesign the wholesale margin model, addressing gaps between current pricing structures and actual logistics costs. Additionally, corporate tax increases and VAT modernization measures outlined in the 2025 budget are expected to raise distributor operating costs. In response, buyers are extending drain intervals or switching to unbranded oils, affecting the Botswana lubricants market growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Engine Oils Anchor, Process Oils Accelerate

Automotive engine oil accounted for 40.54% of the Botswana lubricants market share in 2025, driven by the 3,000-5,000 km service intervals common to high-mileage Japanese imports. While the volume remains significant, its growth is projected to lag behind the overall Botswana lubricants market size due to the adoption of extended-drain synthetic oils and the gradual shift toward electrification, which reduces per-vehicle oil consumption. Process oil (including rubber process oil and white oil), the fastest-growing sub-segment, is expected to grow at a rate of 4.21% by 2031, supported by applications in tire manufacturing, rubber compounding, and cosmetic formulations.

Demand patterns reflect Botswana’s industrial landscape. Industrial engine oils are essential for lubricating diesel generators that address grid instability, while metalworking fluids are critical for mining equipment fabrication. Turbine and transformer oils benefit from the BWP 2.66 billion (USD 0.19 billion) allocated to the Ministry of Minerals and Energy for grid expansion projects. Greases see increased demand due to the rehabilitation of Botswana Railways and the use of earthmoving fleets in road construction projects. These segments collectively sustain consistent demand and create opportunities for upselling as suppliers introduce advanced formulations.

By End-User Industry: Automotive Leads, Industrial Gains

The automotive sector accounted for 61.93% of the projected 2025 lubricant volume, driven by Botswana's passenger vehicle usage, with 8,256 new car registrations recorded in Q2 2025. Commercial vehicles, despite lower unit numbers, consume larger lubricant volumes due to higher mileage and larger sump capacities. Industrial applications such as mining, power generation, and metallurgy are expected to grow at a CAGR of 4.41%, surpassing the automotive segment. This growth is attributed to the continuous operation of equipment under demanding conditions. Mining fleets and construction machinery rely on hydraulic fluids and greases, with operational intensity directly influencing lubricant demand.

Aerospace and marine lubricant usage remains limited, primarily serving airport ground support equipment and inland watercraft. The agricultural sector is expected to benefit from BWP 2.88 billion (USD 0.21 billion) allocated for mechanization, driving demand for lubricants used in tractors and irrigation pumps. These trends collectively diversify lubricant consumption beyond automotive applications, supporting the long-term stability of the Botswana lubricants market.

By Base-Stock Type: Mineral Dominance, Synthetic Ascent

Mineral formulations accounted for 72.04% of the projected 2025 demand, driven by their cost-effectiveness and compatibility with older engines. Consumers impacted by foreign exchange fluctuations continue to opt for conventional oils despite performance limitations. Semi-synthetic oils provide a gradual upgrade option, while bio-based lubricants remain limited due to the absence of fiscal incentives.

Synthetic lubricants are projected to grow at a CAGR of 4.54% through 2031, nearly one percentage point higher than the overall market growth rate. Debswana’s tender requirements and Castrol's American Petroleum Institute (API) SP-compliant GTX launch indicate increasing institutional and retail demand for synthetic oils. As original equipment manufacturer (OEM) warranty requirements increasingly specify higher-specification oils, the synthetic segment in Botswana's lubricants market is expected to achieve incremental market share by 2031.

Geography Analysis

In Q2 2024, Gaborone led vehicle registrations and had the most extensive workshop and retail network in Botswana. Distributors achieve economies of scale and faster inventory turnover due to high traffic volumes and concentrated commercial fleets. Francistown, supported by Botswana Oil's 38-million-liter depot, ranks second, addressing supply bottlenecks along the northern corridor. Molepolole contributes to retail sales, driven by demand from Gaborone.

Mining hubs like Orapa, Jwaneng, and Letlhakane consume significant volumes of bulk hydraulic oils and greases through institutional contracts. During peak overhaul cycles, their monthly consumption can exceed urban retail sales. Tlokweng, a border town, faces challenges from price arbitrage as informal traders import lower-cost lubricants from South Africa, complicating compliance enforcement. Rural centers like Serowe and Palapye benefit from agricultural mechanization funding, though low population density limits overall lubricant consumption.

Future growth in the Botswana lubricants market is expected to align with infrastructure investments. The BWP11.54 billion (USD 0.85 billion) 2025 pipeline focuses on road construction in central and northern districts, driving demand for lubricants used in earthmoving equipment. Additionally, the Botswana Energy Regulatory Authority (BERA) is working to establish alternative import routes through Namibia and Mozambique, reducing reliance on the Durban corridor and potentially narrowing regional price disparities. These developments are likely to support balanced geographic growth, while urban centers continue to dominate the market.

Competitive Landscape

The Botswana lubricants market remains consolidated. Global companies such as Shell plc, BP p.l.c., TotalEnergies, Exxon Mobil Corporation, and Chevron Corporation compete with regional suppliers like Engen and PETRONAS, as well as citizen-owned distributors. The consolidation of 90% import mandates by Botswana Oil Limited in April 2024 requires international brands to either negotiate through indirect channels or establish joint ventures with local partners, significantly altering contract structures. Engen Botswana recorded a 7% decline in lubricant volumes in 2023, attributed to competition from parallel South African imports and reduced retail margins.

Castrol’s planned GTX launch demonstrates a multi-tiered approach, offering 500 ml packs for individual motorists, 5-liter cans for workshops, and 210-liter drums for fleet operators. This strategy is supported by lubricant education programs aimed at maintaining its premium market position. Debswana’s strict Safety, Health, and Environmental (SHE) standards and Original Equipment Manufacturer (OEM) compliance requirements favor suppliers with advanced technical capabilities, providing an advantage to established players with laboratory facilities. Measures to address counterfeiting, such as QR-code authentication and tamper-proof seals, are becoming key differentiators, while smaller distributors rely on competitive pricing and personal relationships to sustain their market presence.

Growth opportunities exist in synthetic and bio-based lubricant formulations, predictive oil analysis, and used-oil collection services, which align with evolving environmental regulations. However, technology adoption remains inconsistent, creating opportunities for early adopters to secure fleet-service contracts. The market remains moderately concentrated, with the top five suppliers accounting for approximately 60% of the market share, while a diverse group of regional importers and workshop-level resellers make up the remainder.

Botswana Lubricants Industry Leaders

Puma Energy

TotalEnergies

Engen Petroleum (PTY) LTD

Shell plc

BP p.l.c.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Debswana issued a three-year tender for bulk and packaged lubricants, applicable to the Jwaneng, Orapa, Letlhakane, and Damtshaa mines in Botswana. The tender requires registration on SAP (Systems, Applications and Products in Data Processing), Ariba, and compliance with Original Equipment Manufacturer (OEM) standards.

- June 2025: Castrol launched its next-generation GTX 5W-30 and 10W-40 engine oils in Gaborone, Botswana. These products are distributed through Lubricants Supplies Botswana, a key supplier in the region, ensuring availability across major urban centers. The launch aims to cater to the growing demand for high-performance engine oils in Botswana's automotive market.

Botswana Lubricants Market Report Scope

Lubricants, such as oil, grease, and water, are substances applied between surfaces to reduce friction, heat, and wear during movement. These barriers facilitate smooth sliding of parts, protecting them from damage and optimizing operational efficiency.

The botswana lubricants market is segmented by product type, end-user industry, and base stock type. By product type, the market is segmented into automotive engine oil, industrial engine oil, transmission fluids, gear oil, brake fluids, hydraulic fluids, greases, process oil (including rubber process oil & white oil), metalworking fluids, turbine oil, transformer oil, and other product types. By end-user industry, the market is segmented into automotive, marine, aerospace, heavy equipment, and industrial. By base stock type, the market is segmented into mineral oil-based lubricants, synthetic lubricants, semi-synthetic lubricants, and bio-based lubricants. The market sizes and forecasts are provided in terms of volume (Liters).

| Automotive Engine Oil |

| Industrial Engine Oil |

| Transmission Fluids |

| Gear Oil |

| Brake Fluids |

| Hydraulic Fluids |

| Greases |

| Process Oils (Rubber & White Oils) |

| Metalworking Fluids |

| Turbine Oil |

| Transformer Oil |

| Other Product Types |

| Automotive | Passenger Vehicles |

| Commercial Vehicles | |

| Two-Wheelers | |

| Marine | |

| Aerospace | |

| Heavy Equipment | Construction |

| Mining | |

| Agriculture | |

| Industrial Manufacturing | Power Generation |

| Metallurgy & Metalworking | |

| Textiles | |

| Oil & Gas | |

| Other End-Use Industries |

| Mineral Oil-based |

| Semi-Synthetic |

| Fully Synthetic |

| Bio-based / Re-refined |

| By Product Type | Automotive Engine Oil | |

| Industrial Engine Oil | ||

| Transmission Fluids | ||

| Gear Oil | ||

| Brake Fluids | ||

| Hydraulic Fluids | ||

| Greases | ||

| Process Oils (Rubber & White Oils) | ||

| Metalworking Fluids | ||

| Turbine Oil | ||

| Transformer Oil | ||

| Other Product Types | ||

| By End-User Industry | Automotive | Passenger Vehicles |

| Commercial Vehicles | ||

| Two-Wheelers | ||

| Marine | ||

| Aerospace | ||

| Heavy Equipment | Construction | |

| Mining | ||

| Agriculture | ||

| Industrial Manufacturing | Power Generation | |

| Metallurgy & Metalworking | ||

| Textiles | ||

| Oil & Gas | ||

| Other End-Use Industries | ||

| By Base Stock Type | Mineral Oil-based | |

| Semi-Synthetic | ||

| Fully Synthetic | ||

| Bio-based / Re-refined | ||

Key Questions Answered in the Report

What is current market size of Botswana Lubricants Market?

The Botswana Lubricants Market size is projected to be 15 million liters in 2025, 15.48 million liters in 2026, and reach 18.45 million liters by 2031, growing at a CAGR of 3.57% from 2026 to 2031.

Which product category currently dominates consumption?

Automotive engine oil leads with a 40.54% share of 2025 volumes.

Where does the strongest growth opportunity lie?

Process oils are expected to post a 4.21% CAGR through 2031, outpacing all other product types.

Why are synthetic lubricants gaining traction?

Mining fleets and long-haul trucks value extended drain intervals and lower downtime, driving a 4.54% CAGR for synthetics.

Page last updated on: