E-Commerce Fulfillment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

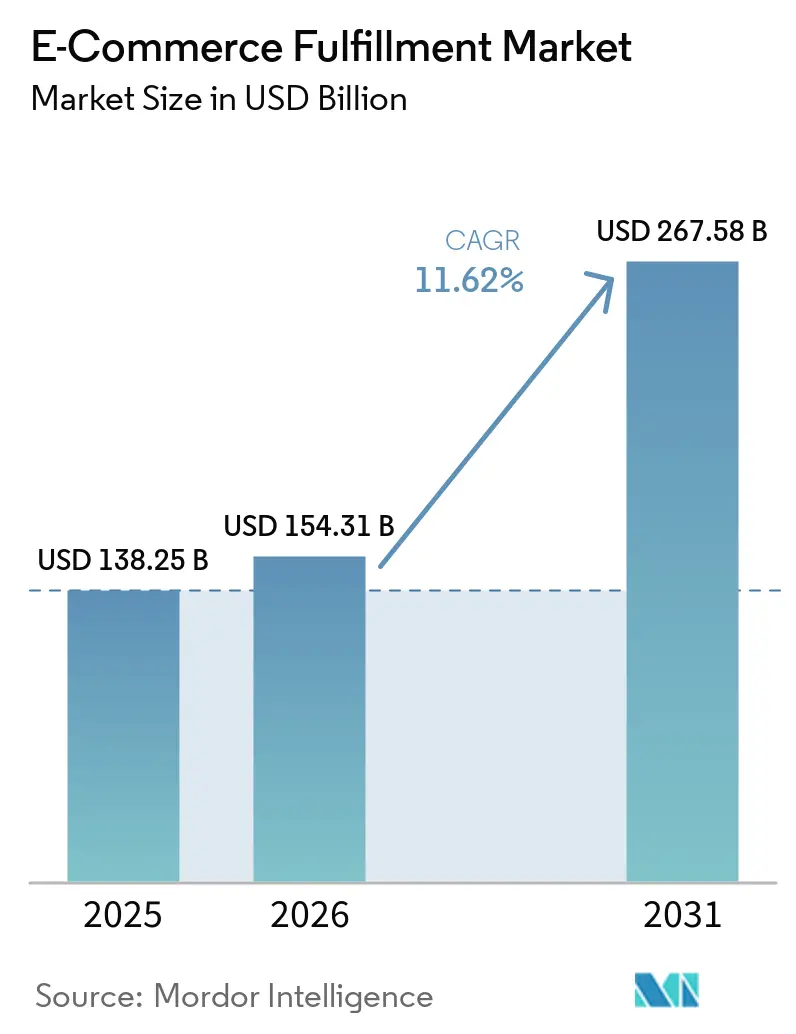

| Market Size (2026) | USD 154.31 Billion |

| Market Size (2031) | USD 267.58 Billion |

| Growth Rate (2026 - 2031) | 11.62% CAGR |

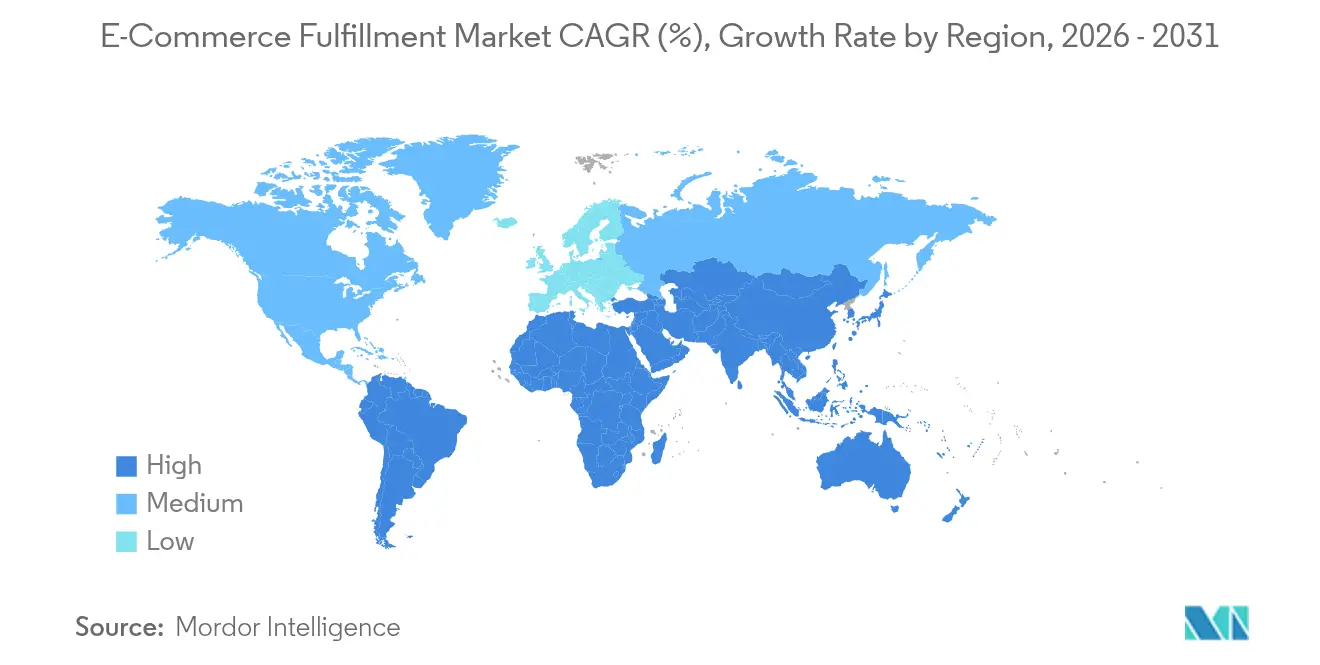

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

E-Commerce Fulfillment Market Analysis by Mordor Intelligence

The e-commerce fulfillment market size is expected to grow from USD 138.25 billion in 2025 to USD 154.31 billion in 2026 and is forecast to reach USD 267.58 billion by 2031 at 11.62% CAGR over 2026-2031. Rapid migration to online retail, accelerated consumer expectations for same-day delivery, and sustained logistics technology investment underpin this trajectory. Automated warehouse systems, bonded hub strategies for cross-border trade, and advanced data analytics are lowering cost-to-serve while lifting service levels. Intensifying labor shortages in key logistics corridors are catalyzing robotics adoption, and sustainability mandates are reshaping packaging design and transport mode mix. Scale players and specialized providers are pursuing strategic alliances and targeted acquisitions to secure network density and differentiate on speed, precision, and end-to-end visibility across the e-commerce fulfillment market.[1]International Transport Forum, “The Final Frontier of Urban Logistics: Tackling the Last Metres,” itf-oecd.org

Key Report Takeaways

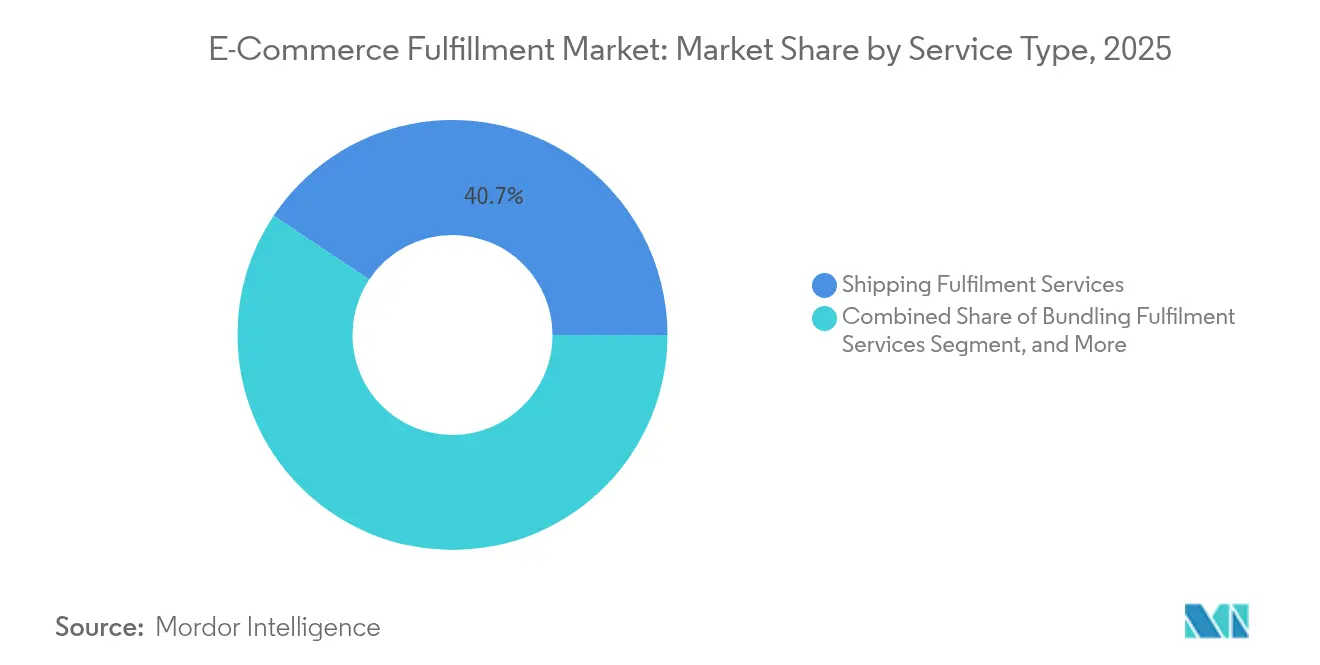

- By service type, shipping fulfillment services led with a 40.65% revenue share in 2025; bundling fulfillment services is forecast to expand at a 14.61% CAGR through 2031.

- By fulfillment model, third-party logistics held 59.25% of the e-commerce fulfillment market share in 2025, while dropshipping is advancing at a 22.46% CAGR to 2031.

- By sales channel, B2B commanded 61.20% share of the e-commerce fulfillment market size in 2025; direct-to-consumer is growing at a 15.74% CAGR to 2031.

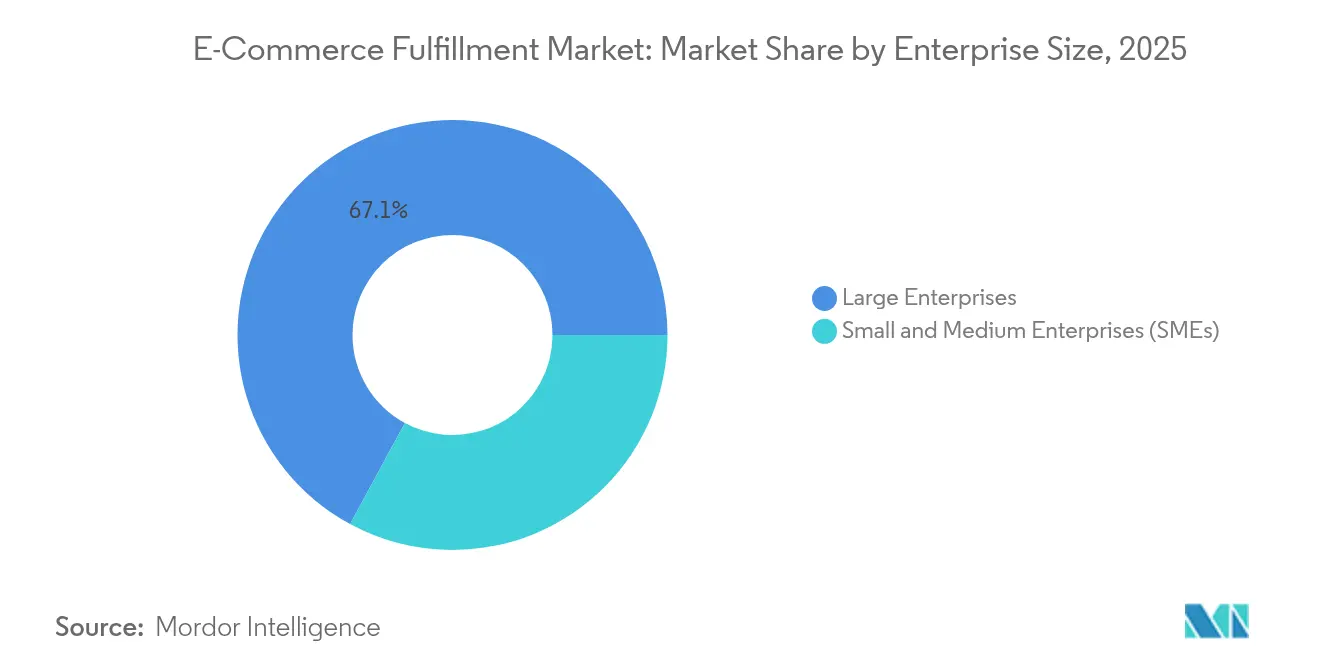

- By enterprise size, large enterprises contributed 67.10% of revenues in 2025; SMEs are progressing at a 15.08% CAGR through 2031.

- By application, clothing and footwear captured 17.65% of the e-commerce fulfillment market size in 2025, and consumer electronics is expanding at a 16.08% CAGR to 2031.

- By geography, North America held 31.70% revenue share in 2025, whereas Asia-Pacific is poised to rise at a 14.76% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global E-Commerce Fulfillment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Consumer SMEs' Outsourcing to 3PLs in North America | +2.3% | North America, with spillover effects in Europe | Medium term (2-4 years) |

| Cross-border Chinese Sellers Driving EU Bonded Hubs | +2.1% | Europe, with emerging impact in UK, Germany, France | Medium term (2-4 years) |

| Fast-Fashion Social Commerce Fuelling Micro-fulfilment in SE-Asia | +1.9% | Southeast Asia, China, India | Short term (≤ 2 years) |

| Same-day Delivery Mandates Triggering Urban Automation in US and EU | +1.5% | North America, Europe | Medium term (2-4 years) |

| Indian Grade-A Warehouse Parks Enabled by Government Incentives | +1.2% | India, with regional impact across Asia-Pacific | Long term (≥ 4 years) |

| Retail-media Data Monetisation Creating Fulfilment Analytics Revenue | +1.0% | Global, with early adoption in North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

SMEs outsourcing fulfillment to 3PLs in North America

Small and medium enterprises across the United States and Canada are reallocating capital away from in-house logistics toward external specialists to gain scalability and technology access. Robotics-enabled 3PL campuses provide 24-hour pick-and-pack operations, driving error rates below 1% and compressing order-to-ship windows from minutes to seconds. Freight consolidation services shorten transit lanes and enable zone-skipping strategies, which lower parcel costs and improve delivery predictability. The trend allows SMEs to match the service benchmarks of national retailers without heavy fixed investments, enhancing competitiveness within the e-commerce fulfillment market.[3]University of California Riverside, “Warehouse and Trucking Industries in the Inland Empire Have Provided More Jobs,” ucr.edu

Cross-border Chinese sellers using EU bonded hubs

Chinese merchants are placing inventory inside European Union bonded warehouses to bypass customs delays and shorten delivery times to under three days for priority customers. The approach is reshaping European network design, triggering carrier diversification and real-time inventory allocation across regional micro-fulfillment sites. Established European retailers are accelerating integration of dynamic clearance tools and localized returns processing to defend share. Bonded hubs are also spurring demand for specialized last-mile partners capable of customs-compliant, low-touch hand-offs, reinforcing competitive intensity in the e-commerce fulfillment market.[2]European Parliament, “The Impact of EU Legislation in the Area of Digital and Green Transition,” europarl.europa.eu

Social-commerce micro-fulfillment in Southeast Asia

Viral product demand on social platforms is driving retailers to locate stock inside dense urban spokes within Southeast Asian megacities. Micro-sites under 10,000 sq ft equipped with shuttle robots replenish storefronts and courier networks hourly, supporting one-or-two-hour delivery promises. High order variability is balanced through predictive demand algorithms that reposition inventory across city clusters overnight, improving sell-through and reducing split shipments. The model demonstrates how social-commerce adoption can compress fulfillment cycles in the e-commerce fulfillment market.

Same-day delivery automation in urban markets

Metropolitan fulfillment centers in North America and Europe now integrate goods-to-person robotics, automated sortation, and electric cargo fleets to meet same-day mandates. Retailers deploy AI-assisted workforce scheduling to offset labor scarcity and maintain peak throughput during holiday surges. Municipal freight policies encouraging low-emission zones accelerate transition to micro-mobility assets such as e-bikes and delivery pods, which improve sustainability metrics without sacrificing velocity. These investments raise the technology threshold for new entrants within the e-commerce fulfillment market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Labour Shortage and Wage Inflation in Inland Empire, US | -1.8% | North America, particularly Western US | Short term (≤ 2 years) |

| EU CSRD and Packaging-waste Rules Inflating Compliance Costs | -1.5% | European Union, with spillover effects globally | Medium term (2-4 years) |

| Port Congestion and Red-Sea Disruption Volatility | -1.3% | Global, with acute impact on Europe-Asia trade routes | Short term (≤ 2 years) |

| Air-Freight Carbon-reduction Pledges Limiting Express Options | -1.1% | Global, with early impact in Europe and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Labor shortage and wage inflation in Inland Empire, US

Industrial vacancy increases and trucking deficits in southern California elevate wage expectations, lift cost-per-unit, and limit peak-season capacity. Operators accelerate deployment of autonomous forklifts and AMRs to sustain throughput with fewer staff and to hedge against churn. Asset-light network designs with multi-tenant hubs spread labor risk geographically, though real-estate costs rise as firms seek alternative nodes. These adjustments temporarily compress margins within the e-commerce fulfillment market.

EU sustainability and packaging-waste regulations

The Packaging and Packaging Waste Regulation, effective mid-2026, requires 50% void reduction and enforceable recyclability criteria by 2030. Fulfillment centers re-engineer packing lines with right-sizing equipment and shift to mono-material formats, incurring capital expenditure and process redesign costs. Multi-level audit trails and extended producer responsibility fees add administrative overhead. Non-compliance risk steers brands toward specialized sustainable packaging vendors, altering cost structures in the e-commerce fulfillment market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Technology lifts value-added bundles

Shipping fulfillment services led with a 40.65% share in 2025, underlining their indispensable role in the e-commerce fulfillment market. Network densification, zone-skipping lanes, and dynamic carrier selection are optimizing delivery cost and reliability. The segment increasingly deploys predictive routing powered by real-time traffic and weather data to sustain on-time performance. Bundling fulfillment services, forecast to grow at 14.61% CAGR, package returns management, personalization, and customer care into a single invoice, enabling merchants to convert logistics from a cost center to a loyalty lever. Improved forecast accuracy and SKU rationalization within bundled contracts streamline inventory turns and boost gross margins.

Warehousing and storage fulfillment continues to modernize through robot-to-goods systems that expand cubic storage and compress travel paths, delivering a 20% productivity uplift. Other niche services, such as custom kitting and subscription box assembly, act as brand signature touchpoints, reinforcing customer engagement and extending lifetime value. Collectively, these services expand addressable revenue pools inside the e-commerce fulfillment market.

By Fulfillment Model: Outsourcing scales, dropshipping diversifies

Third-party logistics providers captured 59.25% of 2025 revenues, validating outsourcing as the dominant configuration in the e-commerce fulfillment market. 3PLs leverage occupancy-based pricing and shared automation to drive down per-unit cost and provide capacity elasticity during promotional spikes. Dropshipping, set to rise at 22.46% CAGR, allows merchants to test assortments without inventory exposure and to penetrate micro-niches through supplier direct-ship models. Cloud-based storefront connectors automate order routing to manufacturers, shortening time-to-market for new SKUs. In-house fulfillment remains meaningful for brands requiring strict product stewardship or regulated handling, yet rising automation capital burdens constrain wider adoption. Hybrid models integrate store back-rooms, 3PLs, and manufacturer ship-from-source to balance speed, cost, and control across the e-commerce fulfillment market.

By Sales Channel: B2B anchors volume, D2C accelerates

B2B transactions represented 61.20% of the e-commerce fulfillment market share in 2025, reflecting large-lot shipments, contractual replenishment cycles, and compliance-heavy labeling that favor high-capacity facilities. Integrated EDI flows and scheduled dock appointments minimize dwell time and enable continuous flow through cross-dock nodes. The D2C channel is growing at a 15.74% CAGR as brands deploy native storefronts and social-commerce integrations to access first-party data and margin lift. Dynamic pick-pack personalization and value-added insertions contribute to elevated customer experience. B2C marketplace volumes continue to scale, prompting fulfillment providers to integrate seller-fulfilled prime programs and empower same-day cut-offs in the e-commerce fulfillment market.

By Enterprise Size: Scale leverages automation, SMEs democratize tech

Large enterprises accounted for 67.10% of 2025 revenue, capitalizing on multi-node distribution footprints and robotics to handle millions of daily order lines. AI-driven inventory placement engines position stock nearest to demand clusters, reducing zone miles and carbon emissions. SMEs, advancing at 15.08% CAGR, access shared user facilities and plug-and-play WMS modules that remove integration friction. Volume-based pricing tiers and pay-as-you-go automation add flexibility, allowing SMEs to match the service benchmarks of tier-one retailers without prohibitive fixed costs. The convergence narrows service disparities and enlarges the customer base for the e-commerce fulfillment market.

By Application: Apparel leads, electronics surges

Clothing and footwear held an 17.65% revenue share in 2025, characterized by frequent purchase cadence and complex returns workflows that require scalable reverse logistics. Multilevel sortation and apparel-folding robotics minimize touchpoints and maintain garment integrity. Consumer electronics, tracking a 16.08% CAGR, demands secure, ESD-compliant environments and value-add services such as configuration and functional testing. Automated vertical lift modules improve density for small parts and accelerate kitting for bundled accessories. Beauty, healthcare, home, and leisure categories each introduce unique compliance and temperature-controlled demands, broadening solution portfolios across the e-commerce fulfillment market.

Geography Analysis

North America, accounting for 31.70% of global revenue in 2025, benefits from mature interstate transport corridors and high consumer spending power. Automation adoption mitigates wage inflation and worker scarcity in logistics clusters, while electric vehicle deployments reduce urban emissions. Canada’s strategic positioning supports trans-Pacific and trans-Atlantic consolidation, creating cross-border synergies within the e-commerce fulfillment market.

Asia-Pacific is the fastest-growing region at a 14.76% CAGR, propelled by rising disposable incomes and mobile-commerce penetration. China’s RMB 21.4 trillion cross-border e-commerce sector anchors regional outbound flows, while India’s Grade-A warehousing incentives improve capacity quality and supply chain visibility. Southeast Asian nations leverage fast-fashion social commerce to deploy micro-fulfillment spokes, compressing lead times in dense urban settings. These dynamics expand service uptake across the e-commerce fulfillment market.

Europe demonstrates robust network modernization as bonded hubs and sustainability regulations reshape fulfillment strategies. The EU’s regulatory push toward recyclable packaging and Scope 3 emissions reporting accelerates investment in right-sized packing automation and carbon-accounting platforms. United Kingdom, Germany, and France lead in omnichannel integration and zero-emission last-mile pilots, elevating operational standards. Meanwhile, Latin America and the Middle East and Africa register rapid e-commerce adoption, creating greenfield opportunities for providers skilled in navigating infrastructure constraints and customs complexity within the e-commerce fulfillment market.

Competitive Landscape

The e-commerce fulfillment market is structurally fragmented, with global integrators such as Amazon Logistics, FedEx, and DHL Supply Chain operating alongside regional specialists and technology-first disruptors. Scale players invest heavily in robotics, predictive analytics, and renewable energy fleets to lock in service-level advantages and cost leadership. Midsize contenders differentiate by focusing on vertical niches, offering specialized handling for heavyweight, high-value, or regulated SKUs.

Automation vendors like AutoStore and Hai Robotics enable fulfillment operators to raise storage density above 3.5 units per cubic foot and raise pick accuracy toward 99.9%. Fulfillment providers integrate these systems with AI-driven labor planning to mitigate seasonal volatility. Near-shoring trends drive network redesigns, promoting smaller, client-dedicated nodes that leverage shared management systems, thus expanding competitive options within the e-commerce fulfillment market.

Strategic alliances and minority investments characterize recent deal activity as carriers seek market access and technology capabilities in one move. Integrated supply chain offerings that span inbound freight, order management, and retail-media analytics are emerging as differentiators. The interplay of scale, specialization, and technology adoption sustains competitive dynamism across all tiers of the e-commerce fulfillment market.

E-Commerce Fulfillment Industry Leaders

Amazon.com Inc.

ShipBob, Inc.

DHL

FedEx Corporation

Rakuten Group, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: THG implemented AutoStore's warehouse automation system, achieving a 40% reduction in labor costs and the fastest delivery times in the UK with a 24-month ROI.

- March 2025: JD Logistics unveiled an international business development roadmap to enable 2-3 day delivery in dozens of overseas markets by 2025, significantly enhancing its global e-commerce fulfillment capabilities.

- March 2025: THG Ingenuity announced a three-year partnership with Criteo to enhance e-commerce solutions and retail media opportunities for its partners in the UK, leveraging Criteo's Commerce Media Platform to monetize first-party data.

- February 2025: Escaro Royale, a premium footwear brand, announced plans to adopt a dark store model in Mumbai to reduce delivery times and carbon footprint, as part of its strategy to achieve USD 5 million in revenue through global expansion.

Global E-Commerce Fulfillment Market Report Scope

E-commerce fulfillment involves receiving, processing, and delivering online retail orders to customers. This process includes various activities, such as inventory management, order processing, shipping and delivery, and returns management, all of which take place after an e-commerce business receives an order.

The study tracks the revenue accrued through the sale of E-commerce fulfillment solutions by various players across the globe. It also tracks the key market parameters, underlying growth influencers, and major vendors operating in the industry, which supports the market estimations and growth rates over the forecast period. The study further analyses the overall impact of COVID-19 aftereffects and other macroeconomic factors on the market. The report’s scope encompasses market sizing and forecasts for the various market segments.

The E-commerce fulfillment market is segmented by service type (warehousing and storage fulfillment services, bundling fulfillment services, shipping fulfillment services, and others), sales channel (direct to customer, business to customer, and business to business), enterprise size (small & medium enterprises (SMEs), and large enterprises), application (automotive, beauty & personal care, books & stationery, consumer electronics, healthcare, clothing & footwear, home & kitchen application, sports & leisure, and others), and geography (North America, Europe, Asia Pacific, Middle East and Africa, and Latin America). The market sizes and forecasts regarding value (USD) for all the above segments are provided.

| Warehousing and Storage Fulfilment Services |

| Bundling Fulfilment Services |

| Shipping Fulfilment Services |

| Other Niche / Value-added Services |

| In-house Fulfilment |

| Third-Party Fulfilment (3PL) |

| Dropshipping |

| Hybrid Fulfilment |

| Direct-to-Consumer (D2C) |

| Business-to-Consumer (B2C Marketplace) |

| Business-to-Business (B2B) |

| Small and Medium Enterprises (SMEs) |

| Large Enterprises |

| Automotive |

| Beauty and Personal Care |

| Books and Stationery |

| Consumer Electronics |

| Healthcare |

| Clothing and Footwear |

| Home and Kitchen |

| Sports and Leisure |

| Other Applications |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East | United Arab Emirates |

| Saudi Arabia | |

| Rest of Middle East | |

| Africa | South Africa |

| Rest of Africa |

| By Service Type | Warehousing and Storage Fulfilment Services | |

| Bundling Fulfilment Services | ||

| Shipping Fulfilment Services | ||

| Other Niche / Value-added Services | ||

| By Fulfilment Model | In-house Fulfilment | |

| Third-Party Fulfilment (3PL) | ||

| Dropshipping | ||

| Hybrid Fulfilment | ||

| By Sales Channel | Direct-to-Consumer (D2C) | |

| Business-to-Consumer (B2C Marketplace) | ||

| Business-to-Business (B2B) | ||

| By Enterprise Size | Small and Medium Enterprises (SMEs) | |

| Large Enterprises | ||

| By Application | Automotive | |

| Beauty and Personal Care | ||

| Books and Stationery | ||

| Consumer Electronics | ||

| Healthcare | ||

| Clothing and Footwear | ||

| Home and Kitchen | ||

| Sports and Leisure | ||

| Other Applications | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East | United Arab Emirates | |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current value of the e-commerce fulfillment market?

The e-commerce fulfillment market size stands at USD 154.31 billion in 2026 and is forecast to reach USD 267.58 billion by 2031.

Which region is expanding the fastest?

Asia-Pacific is the fastest-growing region, advancing at a 14.76% CAGR between 2026 and 2031.

What segment holds the largest revenue share by fulfillment model?

Third-party logistics providers account for 59.25% of 2025 revenues, making outsourcing the dominant model.

Why are bonded hubs important in Europe?

Bonded hubs allow cross-border sellers to pre-position inventory inside the EU, cutting delivery times and simplifying customs, which boosts competitiveness.

How are sustainability regulations affecting fulfillment operations?

EU packaging rules are prompting investments in right-sizing equipment and recyclable materials, increasing short-term costs but aligning operations with long-term environmental goals.

What technologies are most influential in modern warehouses?

Robotics, AI-driven inventory placement, and automated storage and retrieval systems raise pick accuracy to near-perfect levels and compress processing times, enhancing productivity across the e-commerce fulfillment market.

Page last updated on: