Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

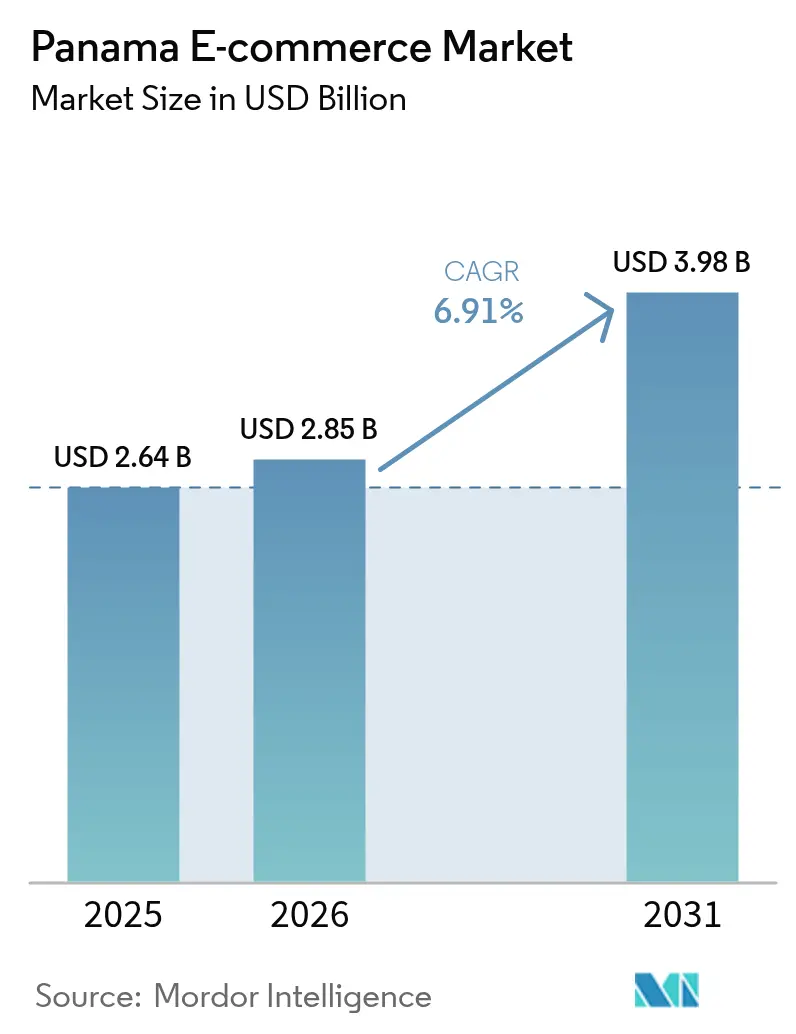

| Base Year Market Size (2025) | USD 2.64 Billion |

| Market Size (2026) | USD 2.85 Billion |

| Market Size (2031) | USD 3.98 Billion |

| Growth Rate (2026 - 2031) | 6.91% CAGR |

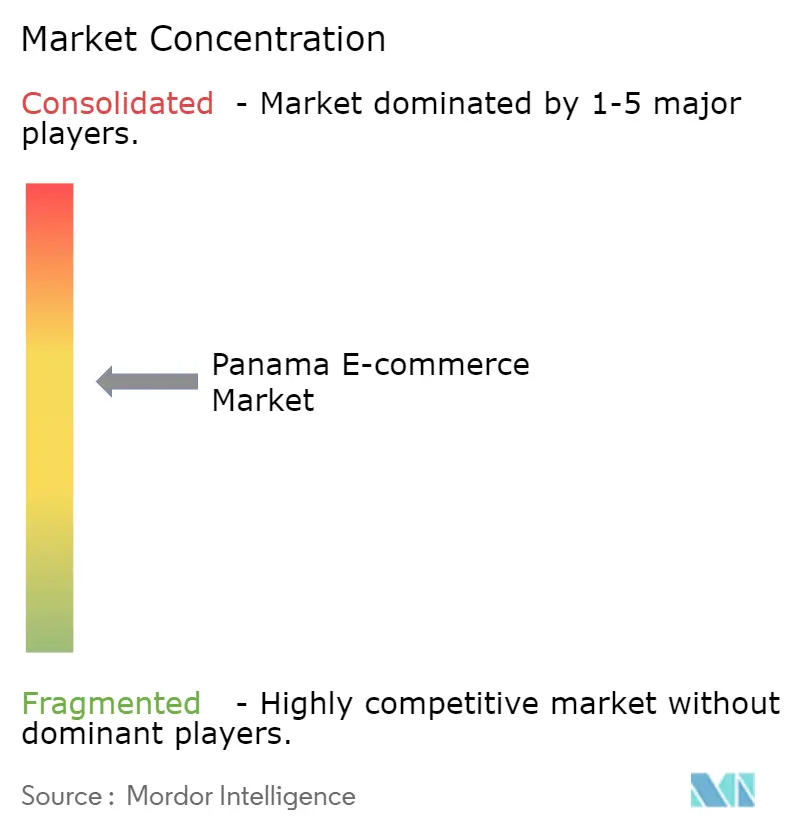

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Panama E-commerce Market Analysis by Mordor Intelligence

The Panama e-commerce market size is projected to expand from USD 2.64 billion in 2025 and USD 2.85 billion in 2026 to USD 3.98 billion by 2031, registering a CAGR of 6.91% between 2026 to 2031. Panama’s position as a hemispheric logistics crossroads, combined with government-backed digitalization programs, supports steady online retail uplift even though the country’s population is just 4.4 million. Cross-border sellers exploit duty-free access to 87% of United States consumer goods, allowing them to price aggressively without eroding margins. Smartphone-first shopping behavior is entrenched because mobile connections exceed the number of inhabitants, enabling social-commerce discovery and single-session purchases. International platforms lean on free-zone infrastructure to promise two-day regional delivery, while local retailers counter with same-day fulfillment inside Panama City to preserve share.

Key Report Takeaways

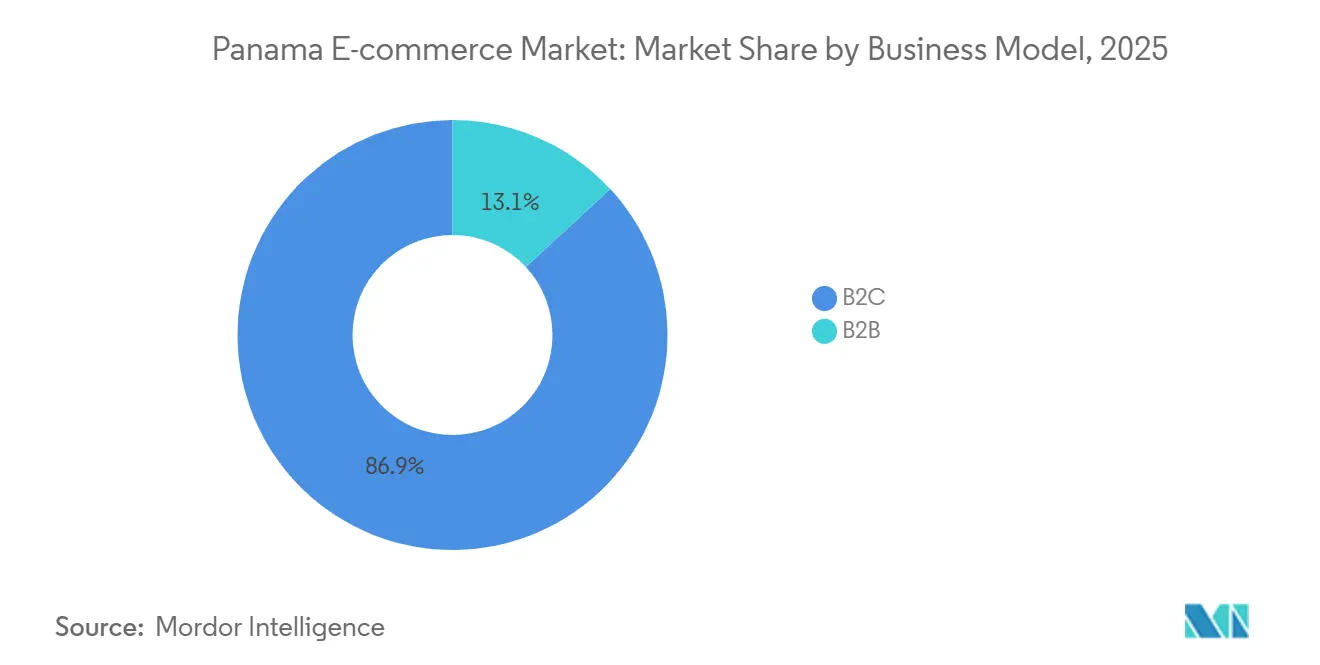

- By business model, the B2C segment held 86.89% of the Panama e-commerce market share in 2025, while the B2B channel is projected to grow at a 9.23% CAGR to 2031.

- By device type, smartphone and mobile devices accounted for 72.67% of B2C transaction volume in 2025; desktop usage is forecast to decline as mobile orders expand at a 7.02% CAGR through 2031.

- By payment method, digital wallets captured 44.92% share of the Panama e-commerce market size in 2025, but credit and debit cards are expected to record the fastest growth at an 8.17% CAGR to 2031.

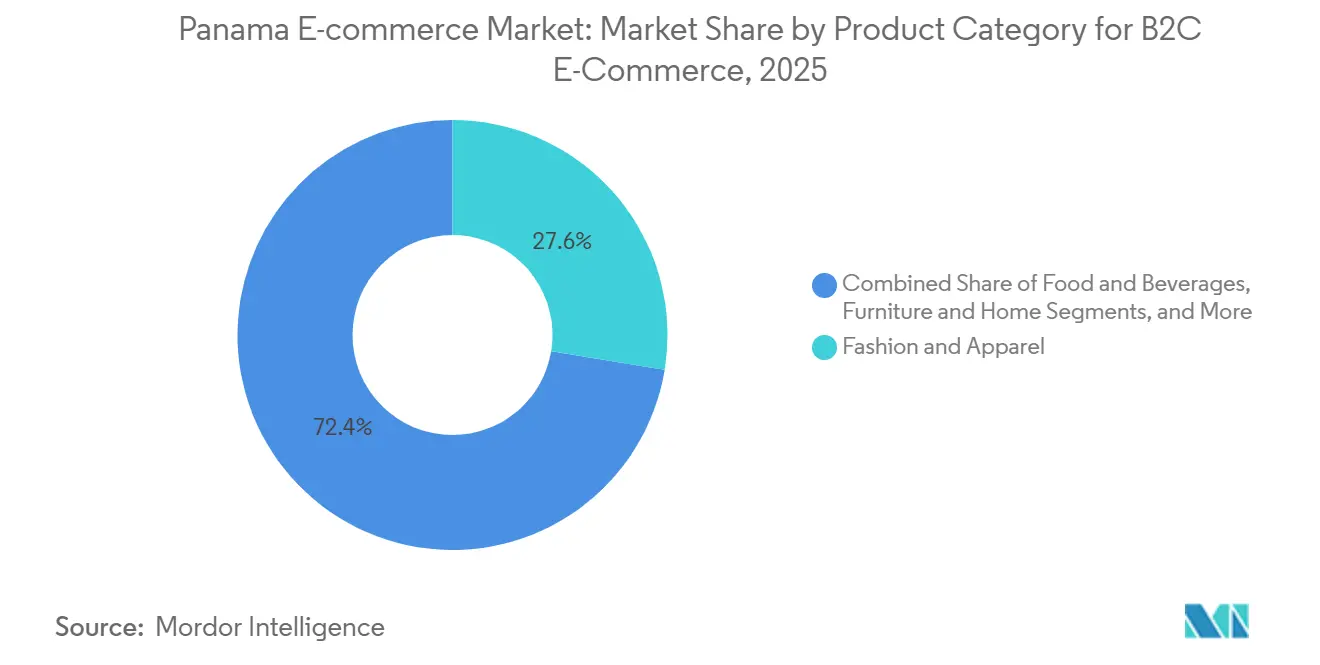

- By product category, fashion and apparel led with 27.59% revenue share in 2025, whereas food and beverages is set to advance at an 8.02% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Panama E-commerce Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government-backed Agenda Digital Panamá 2025 accelerating SME digitalization | +1.8% | National, early gains in Panama City, Colón, David | Medium term (2-4 years) |

| Fintech payment rails widening addressable unbanked shopper base | +1.5% | National, concentrated in urban centers | Short term (≤ 2 years) |

| Logistics free-zone expansion cutting delivery lead-times | +1.2% | Colón Free Zone, Panama Pacifico, regional spillover | Medium term (2-4 years) |

| Cross-border purchase appetite powered by U.S.-Panama trade preference | +1.0% | National, higher in Panama City and border provinces | Long term (≥ 4 years) |

| Diaspora-remittance-linked gifting boosting international GMV | +0.7% | Provinces with high emigration rates | Short term (≤ 2 years) |

| AI-driven last-mile routing lowering fulfillment cost per parcel | +0.6% | Urban corridors, gradual expansion to secondary cities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government-Backed Agenda Digital Panamá 2025 Accelerating SME Digitalization

The USD 60 million loan disbursed by the Inter-American Development Bank in 2022 funds network upgrades and skills training that push micro and small firms online. Yappy, Banco General’s mobile wallet, surpassed 1.6 million users and 28,000 merchants by 2025, and the Municipality of Panama processed 1,300 tax payments through Yappy in only two weeks.[1]“Panama: IDB Approves USD 60 Million Loan for Digital Transformation,” Inter-American Development Bank, iadb.org Public-sector acceptance of digital wallets reassures hesitant shopkeepers that electronic payments are safe, driving onboarding without costly field sales. Mandatory e-invoicing for state contracts forces suppliers to digitize back-office workflows, shortening payment cycles and freeing working capital for online advertising. The cumulative effect is a wider commercial catalog available to domestic shoppers and an easier path for regional buyers sourcing from Panama-based SMEs.

Fintech Payment Rails Widening Addressable Unbanked Shopper Base

Digital wallets already hold 44.92% payment share, reflecting a market where 119% mobile-connection penetration coexists with just 45% formal bank-account ownership.[2]“Global Findex Database 2021,” World Bank, globalfindex.worldbank.org Nequi and Kuara deploy alternative credit scoring that relies on mobile transaction histories, opening installment plans to first-time online buyers. Wallets integrate quick-response codes at corner stores so cash-preferring consumers can top up balances without visiting branches, closing the last-mile gap between informal income and formal commerce. Merchants gain from lower fraud exposure because tokenized wallet credentials reduce card-not-present chargebacks. Together, these features enlarge the effective customer pool and underpin mid-single-digit growth in the Panama e-commerce market.

Logistics Free-Zone Expansion Cutting Delivery Lead-Times

Maersk’s 20,394 square-meter facility launched in July 2025 inside Panama Pacifico exemplifies the shift from bulk re-export to pick-and-pack e-commerce fulfillment.[3]“Maersk Opens New Logistics Center at Panama Pacifico,” Maersk, maersk.com Sellers pre-position high-value, low-weight goods such as smartphones and cosmetics, confident they can clear customs duty-free when re-shipping into neighboring countries. Two-day delivery to Costa Rica, Colombia, or the Caribbean becomes feasible, giving Panama-based inventories a speed advantage over shipments that route through Miami. Third-party logistics firms bundle parcels across multiple marketplaces to raise vehicle fill rates and dilute last-mile cost premiums that plague Latin America. Over time, lower shipping fees translate into narrower delivered-price gaps versus local brick-and-mortar stores, sustaining transaction growth.

Cross-Border Purchase Appetite Powered by U.S.-Panama Trade Preference

The bilateral Trade Promotion Agreement wiped tariffs from 87% of United States consumer products, letting Panamanian shoppers secure branded electronics and apparel at prices up to 30% below domestic tags. United States exports to Panama totaled USD 5.9 billion in 2023, dwarfing Panama’s USD 377 million shipments northbound Transparent landed-cost calculators built into large marketplaces encourage price comparison across borders, boosting mobile browsing sessions that close with offshore checkouts. Retailers operating inside Panama counter by bundling same-day delivery or local warranty repair, but the enthusiasm for direct-from-United States buying persists, adding impetus to mid-single-digit annual expansion in the Panama e-commerce market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented rural address system inflating delivery failure rates | -1.2% | Rural provinces, indigenous territories, informal settlements | Long term (≥ 4 years) |

| Elevated import duties and customs clearance delays causing checkout abandonment | -0.9% | National, affects cross-border purchases | Medium term (2-4 years) |

| Cyber-fraud perception limiting card-not-present transactions | -0.7% | National, higher in lower-income segments | Short term (≤ 2 years) |

| Low digital maturity of Tier-2 and Tier-3 merchants | -0.5% | Secondary cities and rural commercial centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fragmented Rural Address System Inflating Delivery Failure Rates

Many rural districts still rely on landmark-based directions because formal street names and house numbers are absent. Couriers spend extra minutes per drop, and failed handoffs climb, increasing cost per parcel by up to 20%.[4]“Logistics Performance Index 2023,” World Bank, lpi.worldbank.org Geolocation apps exist, yet smartphone ownership lags in areas where internet penetration falls below 50%. Pickup-point pilots show promise but require consumer education and consistent operating hours. Until public agencies fund address standardization or universal parcel lockers, rural penetration of the Panama e-commerce market will trail urban adoption by at least half a decade.

Elevated Import Duties and Customs Clearance Delays Causing Checkout Abandonment

Although the average tariff is 6.3%, non-preferential goods face duties up to 15%, and manual documentation persists for apparel and home goods. When marketplaces cannot surface definitive landed costs at checkout, abandonment rates jump 30% versus domestic carts. The VUCE single-window initiative promises relief, yet uneven product-category roll-out means shoppers lack confidence in delivery timelines. Smaller cross-border merchants, unable to pre-pay duties or fast-track clearance, shoulder the highest churn, muting potential volume in the Panama e-commerce market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Business Model: Enterprise Procurement Fuels Next-Leg Growth

The B2C segment contributed 86.89% of the Panama e-commerce market share in 2025, but B2B orders are expected to expand at a 9.23% CAGR to 2031. Manufacturers and wholesalers now embed digital catalogs inside messaging apps, letting restaurant and hotel buyers repeat orders without field-sales visits. As more suppliers integrate net-30 payment terms and bulk-shipping discounts, the Panama e-commerce market size for B2B transactions will rise steadily.

SME sellers gain leverage by aggregating purchase histories to negotiate better financing, narrowing the working-capital gap against large importers. Marketplaces piloting B2B storefronts in neighboring Mexico and Brazil provide a template for Panamanian roll-outs once critical mass emerges. Over time, enterprise procurement is likely to outpace consumer demand, diversifying gross merchandise value away from fashion and electronics.

By Device Type: Mobile Screens Dominate Discovery and Checkout

Smartphone and tablet transactions represented 72.67% of B2C sales in 2025, and their share is climbing as mobile orders rise at a 7.02% CAGR through 2031. High-speed 4G coverage blankets urban corridors, and handset upgrades put multi-lens cameras in almost every pocket, spurring social-commerce referrals. Because mobile users complete purchases inside the same session in which they discover a product, merchants that shorten form fields and enable biometric login see conversion lifts.

Desktop traffic is plateauing, limited largely to office workers placing weekday orders during lunch breaks. Voice assistants and smart-TV commerce remain novelty channels because Spanish-language skills and local-content libraries are thin. Consequently, the Panama e-commerce market increasingly orbits around app notifications, influencer live streams, and wallet push messages that trigger impulse buys.

By Payment Method: Card Networks Reclaim Share on Security Features

Digital wallets held 44.92% of payments in 2025, yet card transactions are forecast to grow the fastest at 8.17% CAGR on the back of expanded 3D Secure 2.0 coverage. Merchants value automatic liability shifts and real-time fraud scoring that reduce chargebacks. Wallet providers respond by bundling installment plans funded by short-tenor working-capital lines, but high-ticket electronics buyers still prefer the dispute-resolution guarantee offered by card issuers.

Cash on delivery and bank transfers are fading as wallet top-ups become frictionless at supermarket cashiers and corner kiosks. Over the forecast window, payment choice will fragment by basket value, with low-value fashion orders staying wallet-centric and higher-value technology items skewing toward cards. This mix supports healthy revenue diversification within the Panama e-commerce market.

By Product Category: Quick-Commerce Pushes Food and Beverages to the Fore

Fashion and apparel commanded 27.59% of sales in 2025 thanks to tariff-free direct-from-United States sourcing, but food and beverages should post the fastest 8.02% CAGR through 2031. Urban consumers adopt 15-minute grocery delivery for convenience meals, while the diaspora channels part of USD 846 million in annual remittances into premium food gifts. Quick-commerce operators optimize micro-fulfillment centers that pick seven orders per rider per hour, allowing them to hit sub-USD 2 delivery costs on average.

Electronics relies on free-zone inventory that ships across Central America within 48 hours, supporting cross-border revenue streams. Beauty and personal care categories flourish under influencer-led promotions that convert social engagement into cart adds in a single swipe. Furniture sees momentum in B2B refurbishments of hospitality venues, underscoring the widening scope of the Panama e-commerce market beyond consumer discretionary goods.

Geography Analysis

Panama City, Colón, and David together generate roughly three-quarters of online transaction value thanks to dense logistics assets such as Tocumen International Airport and dual-ocean container ports. Maersk’s 2025 warehouse launch inside Panama Pacifico further concentrates fulfillment inside the capital region, enabling two-day cross-border delivery into Central America. Colón Free Zone, responsible for USD 19.8 billion in throughput during 2023, is pivoting from wholesale re-export to e-commerce hub status, giving the Panama e-commerce market a staging ground for rapid regional scale.

Rural provinces lag because fixed-line broadband is scarce and mobile-data plans remain expensive relative to income. Agenda Digital Panamá funds rural towers and community Wi-Fi, yet gaps in addressing and low smartphone ownership will delay significant order penetration for at least five years. Couriers test pickup-point models inside pharmacies and agro-supply stores, but consumer uptake is slow without widespread digital literacy campaigns.

Border regions such as Chiriquí and Bocas del Toro mix physical cross-border shopping with online orders routed via United States platforms that ship duty-free under the trade agreement. Transparent landed-cost calculators encourage shoppers to split baskets, bulky household goods bought in Costa Rica on day trips, high-value electronics ordered online for home delivery. Domestic retailers facing this arbitrage pressure accelerate same-day delivery promises in an effort to keep pesos onshore, reinforcing competitive dynamism inside the Panama e-commerce market.

Competitive Landscape

International marketplaces dominate selection and cross-border logistics, yet local incumbents retain trust advantages by offering cash pickups, call-center support, and immediate returns. MercadoLibre serves Panama through regional fulfillment corridors but has not introduced its Mercado Pago wallet locally, a gap that limits end-to-end control over checkout flows. Rappi expands quick-commerce reach across Latin America and integrates Fountain9 algorithms to fine-tune inventory per micro-zone, pressuring rivals to match 15-minute delivery promises.

Farmacias Arrocha employs ADR Technologies automation to replenish 49 stores twice daily, folding pharmacy orders into same-day e-commerce dispatches. Multimax leverages its electronics stores for click-and-collect, capturing consumers wary of doorstep theft. Neobanks such as Kuara jockey with Yappy to sign unbanked micro-merchants, tempting them with zero interchange fees for wallet-to-wallet transfers.

Fragmentation persists because 70% of SMEs still lack a digital storefront. Gig-economy fleets numbering more than 15,000 riders shuttle parcels for multiple apps, giving newcomers rapid geographic coverage without capital-heavy van purchases. The absence of a comprehensive payment-systems law permits experimentation but also heightens consumer-protection ambiguity, especially in chargeback disputes. Against this backdrop, the Panama e-commerce market rewards nimble operators that bundle fulfillment, payments, and marketing into turnkey packages for offline merchants ready to leapfrog legacy retail.

Panama E-commerce Industry Leaders

Amazon.com Inc.

MercadoLibre Inc.

Rappi Inc.

Panafoto S.A.

Félix B. Maduro S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Alcaldía de Panamá enabled Yappy digital wallet for municipal tax payments, processing 1,300 transactions worth USD 58,000 within two weeks.

- July 2025: Maersk opened a 20,394 square-meter logistics center at Panama Pacifico geared toward regional e-commerce distribution.

- April 2025: Uber Panama reported 6,900 driver-partners and 280,000 active users, boosting last-mile density.

- March 2025: PedidosYa survey showed 88.3% of merchants lifted sales after joining the platform.

Panama E-commerce Market Report Scope

E-commerce is the purchasing and selling of products and services over the Internet. It is conducted over computers, mobiles, tablets, and other smart devices. There are primarily two types of e-commerce, including Business-to-Consumer (B2C) and Business-to-Business (B2B).

The Panama E-commerce Market Report is Segmented by Business Model (B2B, B2C), Device Type for B2C E-commerce (Smartphone and Mobile, Desktop and Laptop, Other Device Types), Payment Method for B2C E-commerce (Credit and Debit Cards, Digital Wallets, Buy Now Pay Later, Other Payment Methods), Product Category for B2C E-commerce (Beauty and Personal Care, Consumer Electronics, Fashion and Apparel, Food and Beverages, Furniture and Home, Other Product Categories), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

By Business Model

| B2B |

| B2C |

By Device Type for B2C E-commerce

| Smartphone and Mobile |

| Desktop and Laptop |

| Other Device Types |

By Payment Method for B2C E-commerce

| Credit and Debit Cards |

| Digital Wallets |

| Buy Now Pay Later |

| Other Payment Methods |

By Product Category for B2C E-commerce

| Beauty and Personal Care | Hair Care |

| Skin Care | |

| Cosmetics and Beauty | |

| Other Beauty and Personal Care Product Categories | |

| Consumer Electronics | Mobile |

| PC and Laptops | |

| Audio Devices | |

| Gaming Devices | |

| Other Consumer Electronics Product Categories | |

| Fashion and Apparel | Clothing |

| Footwear | |

| Fashion Accessories | |

| Other Fashion and Apparel Product Categories | |

| Food and Beverages | Packaged Food |

| Bakery and Confectionery | |

| Meat, Poultry, and Seafood | |

| Other Food and Beverages Product Categories | |

| Furniture and Home | Home Furniture |

| Office Furniture | |

| Outdoor Furniture | |

| Other Furniture and Home Product Categories | |

| Other Product Categories |

| By Business Model | B2B | |

| B2C | ||

| By Device Type for B2C E-commerce | Smartphone and Mobile | |

| Desktop and Laptop | ||

| Other Device Types | ||

| By Payment Method for B2C E-commerce | Credit and Debit Cards | |

| Digital Wallets | ||

| Buy Now Pay Later | ||

| Other Payment Methods | ||

| By Product Category for B2C E-commerce | Beauty and Personal Care | Hair Care |

| Skin Care | ||

| Cosmetics and Beauty | ||

| Other Beauty and Personal Care Product Categories | ||

| Consumer Electronics | Mobile | |

| PC and Laptops | ||

| Audio Devices | ||

| Gaming Devices | ||

| Other Consumer Electronics Product Categories | ||

| Fashion and Apparel | Clothing | |

| Footwear | ||

| Fashion Accessories | ||

| Other Fashion and Apparel Product Categories | ||

| Food and Beverages | Packaged Food | |

| Bakery and Confectionery | ||

| Meat, Poultry, and Seafood | ||

| Other Food and Beverages Product Categories | ||

| Furniture and Home | Home Furniture | |

| Office Furniture | ||

| Outdoor Furniture | ||

| Other Furniture and Home Product Categories | ||

| Other Product Categories | ||

Key Questions Answered in the Report

How large will online retail spending in Panama be by 2031?

Forecasts indicate the Panama e-commerce market size should reach USD 3.98 billion by 2031, growing at a 6.91% CAGR from 2026.

Which business model is growing fastest?

The B2B channel is projected to expand at a 9.23% CAGR through 2031 as enterprises shift procurement to digital platforms.

Why are payment cards regaining momentum against wallets?

Merchants value 3D Secure 2.0 fraud controls and chargeback protection, leading card transactions to post an expected 8.17% CAGR from 2026.

What product category shows the highest forward growth?

Food and beverages should advance at an 8.02% CAGR as quick-commerce services widen assortment and shorten delivery windows.

How does Panama's logistics infrastructure support cross-border sales?

Free-zone warehouses and dual-ocean ports enable two-day delivery into Central America, making Panama a regional fulfillment hub for online merchants.

What limits rural e-commerce adoption?

Fragmented addressing and sub-50% internet penetration raise delivery failure rates and deter courier expansion in outlying provinces.

Page last updated on: