Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

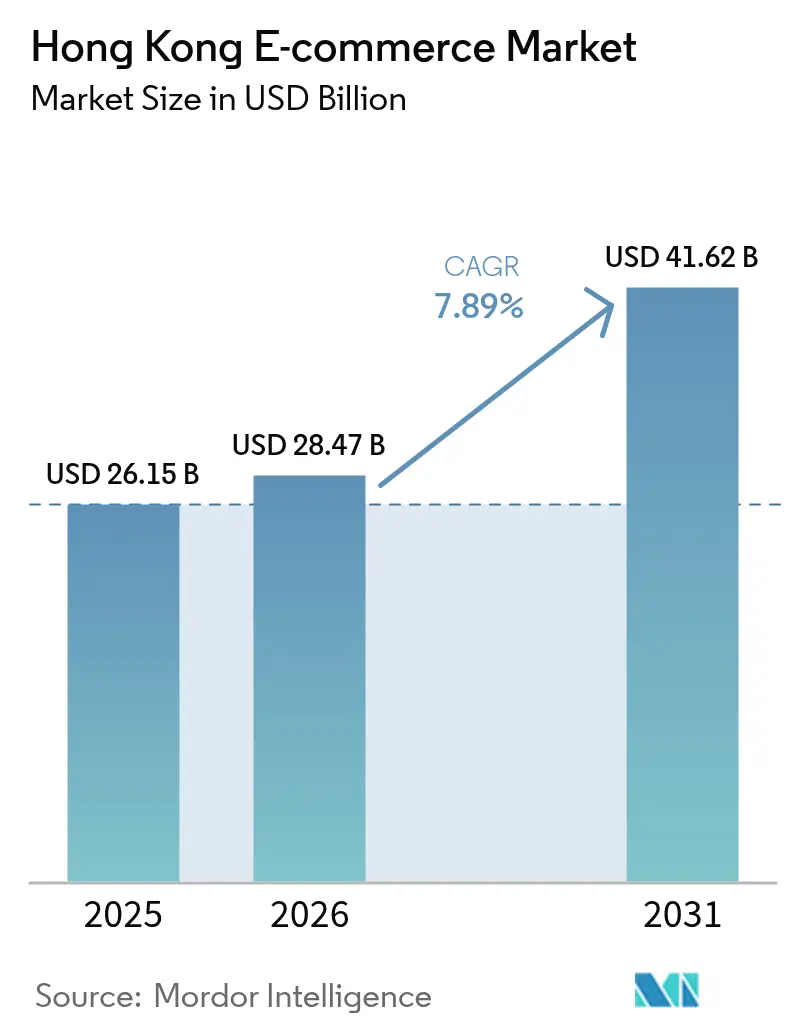

| Base Year Market Size (2025) | USD 26.15 Billion |

| Market Size (2026) | USD 28.47 Billion |

| Market Size (2031) | USD 41.62 Billion |

| Growth Rate (2026 - 2031) | 7.89% CAGR |

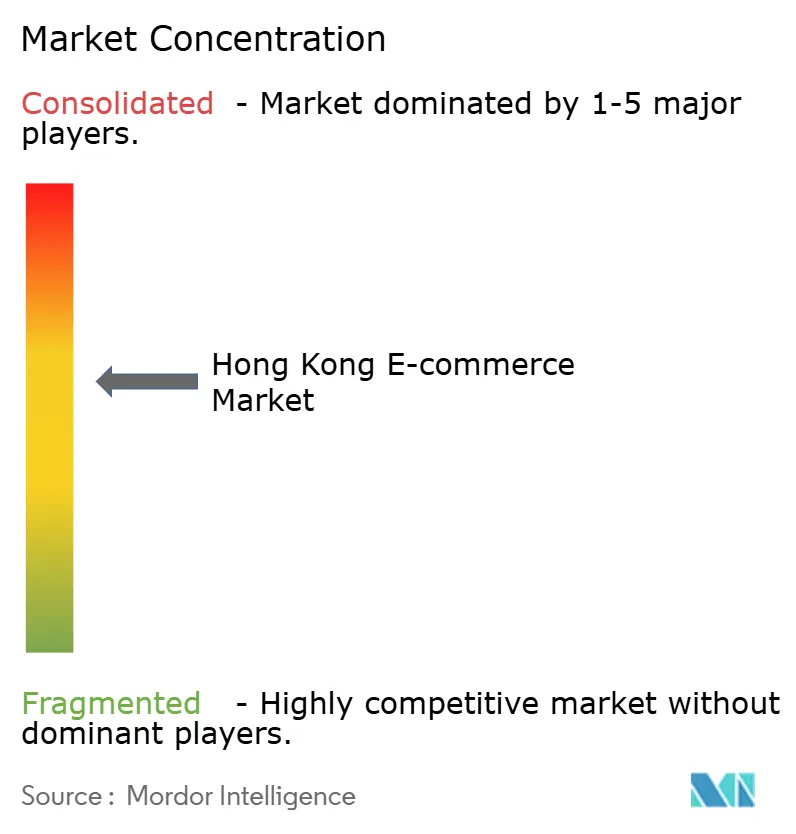

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hong Kong E-commerce Market Analysis by Mordor Intelligence

The Hong Kong e-commerce market size expanded from USD 26.15 billion in 2025 to USD 28.47 billion in 2026 and is projected to reach USD 41.62 billion by 2031, advancing at a 7.89% CAGR between 2026 and 2031. The territory’s one-click payments, 99% smartphone penetration, and positioning inside the Greater Bay Area logistics corridor keep demand for frictionless cross-border shopping elevated. Platforms differentiate through same-day delivery, live-stream checkouts and loyalty cashback instead of price alone, because customer acquisition costs climbed 22% year on year in 2025. Rapid digital-wallet adoption and government subsidies that reimbursed up to 75% of SME digitalization spend until mid-2026 further widened the online sales funnel. Competitive intensity remains high as mainland giants, homegrown champions and global entrants all chase Hong Kong’s affluent shoppers, while sky-high warehouse rents in Kwai Chung and Tsuen Wan compress fulfillment margins.

Key Report Takeaways

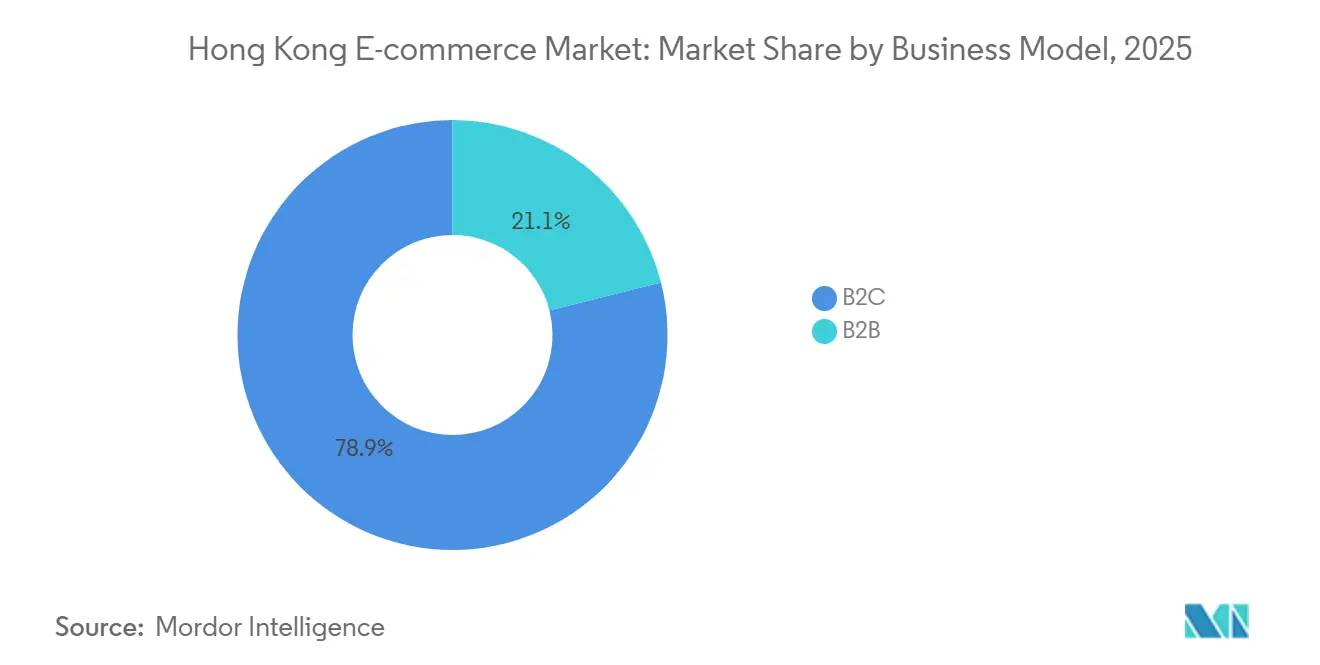

- By business model, business-to-consumer transactions held 78.92% of the Hong Kong e-commerce market share in 2025, whereas B2B procurement is growing fastest at an 8.03% CAGR through 2031.

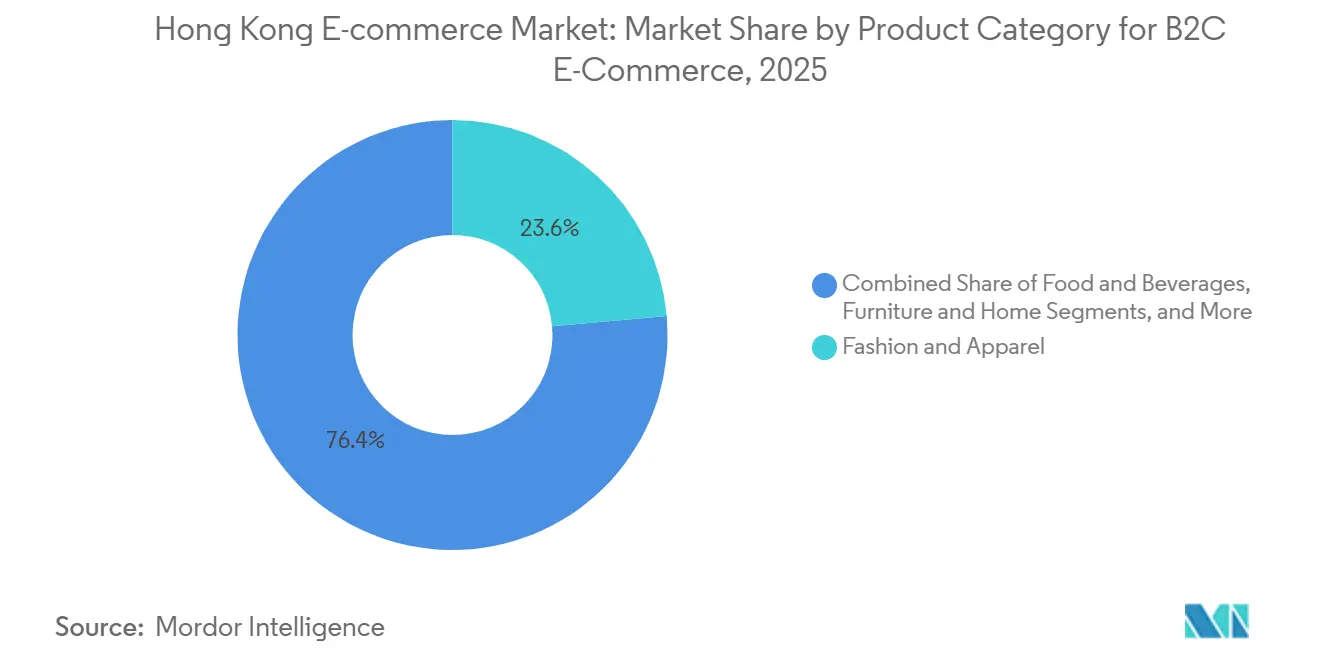

- By product category, fashion and apparel led with 23.59% revenue share in 2025; food and beverages is forecast to expand at an 8.31% CAGR to 2031.

- By device type, smartphones commanded 69.67% of Hong Kong e-commerce market size in 2025 and are advancing at a 7.97% CAGR through 2031.

- By payment method, credit and debit cards retained 43.92% share of Hong Kong e-commerce market size in 2025, while digital wallets record the fastest projected CAGR at 8.28% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Hong Kong E-commerce Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth of Mobile-First Shoppers Fueled by 5G Rollout and 99% Smartphone Penetration | +2.1% | Hong Kong SAR, Spillover to Greater Bay Area | Short Term (≤ 2 Years) |

| Accelerated Cross-Border Fulfillment via Greater Bay Area Logistics Corridors | +1.8% | Hong Kong SAR, Guangdong Province, Macao SAR | Medium Term (2-4 Years) |

| Government Digital Funding Schemes (D-Biz, E-Commerce Easy) Boosting SME Online Migration | +1.5% | Hong Kong SAR, Kowloon and New Territories SME Clusters | Short Term (≤ 2 Years) |

| High Credit Card and E-Wallet Usage Enabling Frictionless Checkout | +1.3% | Hong Kong SAR | Medium Term (2-4 Years) |

| Rising Affluence of Gen Z and Mainland Tourist Spend on Hong Kong Platforms | +1.0% | Hong Kong SAR, Mainland China Visitor Segments | Long Term (≥ 4 Years) |

| Live-Streaming and Social-Commerce Monetization Partnerships with KOLs | +0.9% | Hong Kong SAR, Cross-Border to Guangdong | Medium Term (2-4 Years) |

| Source: Mordor Intelligence | |||

Growth of Mobile-First Shoppers Fueled by 5G Rollout and 99% Smartphone Penetration

By late 2025 the territory’s four network operators had deployed more than 20,000 5G base stations, achieving greater than 90% coverage and sub-50 millisecond latency that supports augmented-reality try-ons and instant stock checks during checkout. Platforms embedded live-streaming inside their apps, and an academic survey found that 83.6% of consumers aged 18-30 completed fashion purchases exclusively on smartphones while desktop conversions fell below 12%. Brands optimizing vertical video, one-tap payments and biometric login capture disproportionate Gen Z wallet share. As data harvesting intensifies, compliance with the Personal Data (Privacy) Ordinance shapes UI design and consent flows.

Accelerated Cross-Border Fulfillment via Greater Bay Area Logistics Corridors

Customs streamlining in 2024-2025 cut parcel clearance between Hong Kong and Shenzhen from 48 hours to under six, enabling same-day delivery for bonded goods stored across the border.[1]Hong Kong Trade Development Council, “Greater Bay Area Logistics Report 2025,” HKTDC.com JD.com’s 2024 purchase of Kai Bo illustrates how mainland platforms position Hong Kong warehouses as export gateways for Southeast Asia. Local sellers still face asymmetric barriers entering mainland marketplaces, making logistics integration a one-way competitive accelerant. The Trade Single Window, which digitized 95% of declarations by 2025, sustains speed advantages though dual certification for cosmetics and infant formula remains a friction point TSW.HK.

Government Digital Funding Schemes Boosting SME Online Migration

Between 2020 and 2025 the Innovation and Technology Bureau disbursed over HKD 5 billion (USD 641 million) to cover up to 75% of storefront, gateway and digital-ads spend for qualifying SMEs.[2]Innovation and Technology Bureau, “SME Funding Schemes,” ITB.gov.hk A Hong Kong Productivity Council review found funded merchants logged 34% higher online revenue growth than non-participants, but 28% later abandoned e-commerce once subsidies lapsed.[3]Hong Kong Productivity Council, “Digital Transformation Impact Study 2025,” HKPC.org The programs sunset in mid-2026, placing sustained performance pressure on retailers now confronting higher paid-ads pricing and complex last-mile orchestration.

High Credit Card and E-Wallet Usage Enabling Frictionless Checkout

The Faster Payment System processed 4.2 billion transactions in 2025, allowing instant settlement across cards and wallets and eliminating multi-day clearing delays.[4]Hong Kong Monetary Authority, “Payment Systems Oversight Report 2025,” HKMA.gov.hk While cards maintained a 43.92% share, wallet transactions are climbing fastest as QR codes, BNPL installments and biometric authentication lower checkout friction for everyday purchases. Platforms that support multi-rail payments minimize abandonment during promotion spikes, yet must also meet two-factor mandates on orders above HKD 500 (USD 64).

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sky-High Warehouse Rents and Last-Mile Labor Costs Compressing Margins | -1.4% | Hong Kong SAR, Kwai Chung and Tsuen Wan | Medium Term (2-4 Years) |

| Saturation of Marketplace Advertising Driving Customer Acquisition Costs | -1.1% | Hong Kong SAR | Short Term (≤ 2 Years) |

| Persistent Consumer Concerns over Product Authenticity on C2C Channels | -0.7% | Hong Kong SAR, Cross-Border C2C Platforms | Medium Term (2-4 Years) |

| Talent Shortage in Data and Growth-Hacking Roles for E-Commerce Operations | -0.5% | Hong Kong SAR | Long Term (≥ 4 Years) |

| Source: Mordor Intelligence | |||

Sky-High Warehouse Rents and Last-Mile Labor Costs Compressing Margins

Average warehouse rents in Kwai Chung and Tsuen Wan reached HKD 18 per square foot (USD 2.30) in 2025 after a 14% annual jump, ranking among the world’s steepest logistics overheads.[5]JLL Hong Kong, “Industrial Property Report Q4 2025,” JLL.com.hk Platforms choosing local storage secure same-day delivery but sacrifice margin; shifting stock to Shenzhen cuts rent in half yet extends delivery windows to 24-48 hours, eroding competitiveness against HKTVmall’s local inventory. Rising minimum wages, coupled with courier shortages during Singles’ Day and Lunar New Year, pushed spot pay to HKD 80-100 an hour (USD 10.26-12.82), forcing experimentation with lockers and pickup points that only 25% of shoppers currently accept.

Saturation of Marketplace Advertising Driving Customer Acquisition Costs

Cost-per-click on Meta, Google and local sponsored listings climbed 22% in 2025 because nearly every Hong Kong e-commerce platform targets the same smartphone-savvy, urban demographic. KPMG benchmarking shows marketing expense swelling to 18-24% of revenue, roughly double the Southeast Asian median. As paid reach plateaus, platforms increasingly adopt marketing technology through owned content, live shows, KOL tie-ins, and gamified loyalty programs, while mainland players exploit WeChat Mini-Programs to sidestep bidding wars altogether.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Business Model: B2B Procurement Digitization Outpaces Retail Growth

Business-to-consumer transactions captured 78.92% of Hong Kong e-commerce market share in 2025, underscoring the territory’s consumer-led DNA. Still, B2B platforms are forecast to expand at an 8.03% CAGR through 2031, nearly matching overall Hong Kong e-commerce market size growth and reflecting procurement digitalization across logistics, food-service and construction verticals. Lower customer-acquisition spend, larger basket sizes and early-payment discounts make B2B economics attractive, particularly for suppliers feeding Kowloon’s restaurant clusters where next-day replenishment beats traditional wet-market visits.

B2C momentum is slowing as urban penetration nears saturation, prompting retention tactics such as subscription clubs and AI-based personalization instead of raw user acquisition. A 2025 behavioral study recorded 37% higher price sensitivity online versus in-store, hinting that future B2C wins hinge on perceived value rather than speed alone. Platforms unable to bundle content, payments and logistics into sticky ecosystems risk wallet share erosion as shoppers chase promotions across multiple apps.

By Device Type: Smartphones Cement Transaction Dominance

Smartphones generated 69.67% of 2025 transaction value and are projected to rise at a 7.97% CAGR, preserving the largest slice of Hong Kong e-commerce market size this decade. AR try-ons, live-stream flash sales and thumb-friendly checkout make the handset the primary storefront for fashion, cosmetics and impulse categories. Desktop shopping lingers for research-heavy electronics or furniture orders, yet its share keeps sliding as mobile pages adopt vertical scrolling and expanded specs tabs.

Platforms that overlook mobile load-time, vertical video and one-tap biometric pay face immediate user churn. Other screens, smart TVs, voice assistants, remain niche because Cantonese voice commerce and local-language skills lag consumer expectations. Surveys show only 28% trust unmanned AI recommendations, so firms mix chatbots with live-agent escalation while gradually improving conversational accuracy.

By Payment Method: Digital Wallets Narrow The Card Lead

Credit and debit cards continued to hold 43.92% of transaction value in 2025, buoyed by reward points and longstanding merchant acceptance, yet digital wallets are scaling at an 8.28% CAGR through 2031. The Faster Payment System’s real-time rails, QR adoption and wallet-linked BNPL plans entice younger shoppers for purchases above HKD 1,000 (USD 128). Cards remain dominant for larger-ticket buys because airline-mile programs retain aspirational pull, but wallet share continues to rise in everyday categories where speed trumps perks.

BNPL adoption shows sharp generation gaps: 34% of 18-29-year-olds used installments in 2025 versus 11% of shoppers aged 40-plus. Bank transfers and cash on delivery are fading to single-digit relevance as two-factor mandates and fraud controls tighten. Merchants offering three or more payment types register higher conversion, and Buy-Now-Pay-Later schemes gain traction for mid-priced electronics. These options broaden the Hong Kong e-commerce market and mitigate single-provider risk. The Hong Kong e-commerce industry is therefore set to showcase one of Asia’s most plural payment portfolios by 2031.

By Product Category: Online Groceries Race Ahead of Fashion

Fashion and apparel delivered a 23.59% revenue slice in 2025, making it the single biggest Hong Kong e-commerce market segment because cross-border Taobao listings dwarf local shop assortments. Yet food and beverages will post the fastest 8.31% CAGR into 2031, powered by on-demand grocery apps, restaurant aggregators and expatriate appetite for imported snacks. The city’s high-density living supports 30-minute delivery zones, and aging households prefer online grocery baskets over wet markets.

Beauty, consumer electronics and home furnishings contribute mid-single-digit shares. Beauty gains from live-stream tutorials and KOL product drops, with case studies showing eight-minute average view times. Electronics growth is softer because instant in-store pickup still satisfies tactile inspection needs, while heavy furniture lags under logistics costs and narrow high-rise corridors. AR room planners gradually erode this barrier, but conversion remains lower than light-weight categories.

Geography Analysis

Hong Kong operates simultaneously as a self-contained 7.5-million-resident market and as the southern anchor of the 86-million-person Greater Bay Area. Customs simplification cut parcel clearance below six hours, letting Shenzhen warehouses fulfill Hong Kong orders same day while using the city’s free-port status to re-export to Southeast Asia. The flow is asymmetric; mainland sellers enter Hong Kong with ease, yet local platforms struggle behind mainland firewalls.

Rule of law, IP safeguards, a freely convertible currency and bilingual skills let global brands pilot Asia-Pacific e-commerce strategies in Hong Kong before scaling regionally. The Trade Single Window, handling 95% of declarations electronically, accelerates cross-border shipping for Amazon and niche DTC labels. However, the city’s small population caps absolute Hong Kong e-commerce market size, prompting focus on high-margin verticals such as luxury beauty and premium electronics that offset warehouse rents.

Mainland tourist spending bounced back to pre-pandemic levels in 2025, accounting for 18% of total retail sales, with an increasing share transacted online via pre-order for hotel or cross-border delivery. Hence platforms must offer both Cantonese service and simplified-Chinese content plus Alipay and WeChat Pay integration. This hybrid B2C-cum-export profile distinguishes Hong Kong from Singapore, whose platforms serve domestic shoppers almost exclusively.

Competitive Landscape

No single operator dominates the Hong Kong e-commerce market; HKTVmall leads local platforms with an estimated 12-15% of B2C revenue in 2025 while Taobao, Tmall and JD.com collectively control roughly 35-40% through cross-border sales. Amazon, Zalora, Ztore, Shopline-powered independents and niche C2C markets divide the remainder. Shoppers demonstrate fluid platform loyalty, chasing coupons and delivery promises rather than committing to one ecosystem.

Three strategic levers matter. First, inventory breadth: Taobao scales through long-tail listings and low prices, whereas HKTVmall curates trusted local brands to combat counterfeit fears. Second, fulfillment speed: HKTVmall’s Hong Kong warehouses enable same-day dispatch, but JD.com’s 2025 Kai Bo acquisition shaved its Shenzhen-to-Hong Kong transit to one day. Third, payment flexibility: all major sites accept cards, Alipay HK, WeChat Pay HK and Tap and Go, yet only some integrate BNPL.

White-space still exists. B2B procurement portals face minimal competition from entrenched wholesale channels, live-stream monetization remains nascent versus mainland standards, and bonded-warehouse logistics can further cut cost per parcel. New entrants such as Shopline and Boutir attract SMEs by charging lower commissions and granting storefront control, powering roughly 8-10% of merchant onboarding in 2025. Technology arms races continue, with Alibaba’s Cainiao filing blockchain provenance patents to verify product authenticity and HKTVmall rolling out AI sortation robots to trim last-mile cost.

Hong Kong E-commerce Industry Leaders

JD.com, Inc.

Alibaba Group Holding Limited

Hong Kong Technology Venture Company Limited (HKTVmall)

WeChat Pay Hong Kong Limited

Amazon.com, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Alibaba opened a 150,000-square-foot AI-enabled Cainiao sorting hub in Tuen Mun, boosting cross-border parcel capacity to 200,000 units daily and cutting Shenzhen-to-Hong Kong Island delivery to under 12 hours.

- December 2025: HKTVmall partnered with HSBC to issue a 5% cashback co-branded credit card linked to its Club Shopping subscription base of 380,000 members, reinforcing user retention.

- November 2025: JD.com acquired Kai Bo for more than USD 50 million, unlocking same-day delivery for beauty and electronics categories previously constrained by customs delays.

- October 2025: Amazon launched a HKD 388 (USD 50) Prime membership with free two-day delivery and localized Cantonese streaming, marking its first recurring-revenue push in the territory.

Hong Kong E-commerce Market Report Scope

Conducting an e-commerce business means fostering relationships and selling information, services, and goods over computer communication networks. E-commerce usually refers to trading goods and services over the internet, which means broader economic activity. E-commerce consists of B2B and B2C and internal organizational transactions that support these activities.

The Hong Kong E-commerce Market Report is Segmented by Business Model (B2B, B2C), Device Type for B2C (Smartphone and Mobile, Desktop and Laptop, Other Device Types), Payment Method for B2C (Credit and Debit Cards, Digital Wallets, Buy Now Pay Later, Other Payment Methods), Product Category for B2C (Beauty and Personal Care, Consumer Electronics, Fashion and Apparel, Food and Beverages, Furniture and Home, Other Product Categories), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

By Business Model

| B2B |

| B2C |

By Device Type for B2C E-commerce

| Smartphone and Mobile |

| Desktop and Laptop |

| Other Device Types |

By Payment Method for B2C E-commerce

| Credit and Debit Cards |

| Digital Wallets |

| Buy Now Pay Later |

| Other Payment Methods |

By Product Category for B2C E-commerce

| Beauty and Personal Care | Hair Care |

| Skin Care | |

| Cosmetics and Beauty | |

| Other Beauty and Personal Care Product Categories | |

| Consumer Electronics | Mobile |

| PC and Laptops | |

| Audio Devices | |

| Gaming Devices | |

| Other Consumer Electronics Product Categories | |

| Fashion and Apparel | Clothing |

| Footwear | |

| Fashion Accessories | |

| Other Fashion and Apparel Product Categories | |

| Food and Beverages | Packaged Food |

| Bakery and Confectionery | |

| Meat, Poultry, and Seafood | |

| Other Food and Beverages Product Categories | |

| Furniture and Home | Home Furniture |

| Office Furniture | |

| Outdoor Furniture | |

| Other Furniture and Home Product Categories | |

| Other Product Categories |

| By Business Model | B2B | |

| B2C | ||

| By Device Type for B2C E-commerce | Smartphone and Mobile | |

| Desktop and Laptop | ||

| Other Device Types | ||

| By Payment Method for B2C E-commerce | Credit and Debit Cards | |

| Digital Wallets | ||

| Buy Now Pay Later | ||

| Other Payment Methods | ||

| By Product Category for B2C E-commerce | Beauty and Personal Care | Hair Care |

| Skin Care | ||

| Cosmetics and Beauty | ||

| Other Beauty and Personal Care Product Categories | ||

| Consumer Electronics | Mobile | |

| PC and Laptops | ||

| Audio Devices | ||

| Gaming Devices | ||

| Other Consumer Electronics Product Categories | ||

| Fashion and Apparel | Clothing | |

| Footwear | ||

| Fashion Accessories | ||

| Other Fashion and Apparel Product Categories | ||

| Food and Beverages | Packaged Food | |

| Bakery and Confectionery | ||

| Meat, Poultry, and Seafood | ||

| Other Food and Beverages Product Categories | ||

| Furniture and Home | Home Furniture | |

| Office Furniture | ||

| Outdoor Furniture | ||

| Other Furniture and Home Product Categories | ||

| Other Product Categories | ||

Key Questions Answered in the Report

How large is online retail spending in Hong Kong today?

Online retail reached USD 28.47 billion in 2026 and is on track to climb to USD 41.62 billion by 2031.

Which sales channel is expanding fastest in Hong Kong's digital commerce?

B2B procurement platforms are projected to grow at an 8.03% CAGR between 2026 and 2031, outpacing consumer channels.

Why do smartphones dominate transactions in the territory?

99% smartphone penetration coupled with 90% 5G coverage enables live-stream shopping and one-tap biometric payments that desktop sites cannot match.

What is the biggest cost pressure facing Hong Kong e-commerce operators?

Warehouse rents that averaged HKD 18 per square foot and courier wages that doubled during peak seasons squeezed fulfillment margins in 2025.

Which product category is set to grow fastest through 2031?

Online food and beverage sales are forecast to expand at an 8.31% CAGR, driven by on-demand grocery apps and dense delivery networks.

How concentrated is platform competition in Hong Kong?

The top five players control roughly half of total online sales, reflecting a moderate concentration that still leaves meaningful room for niche entrants.

Page last updated on: