Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

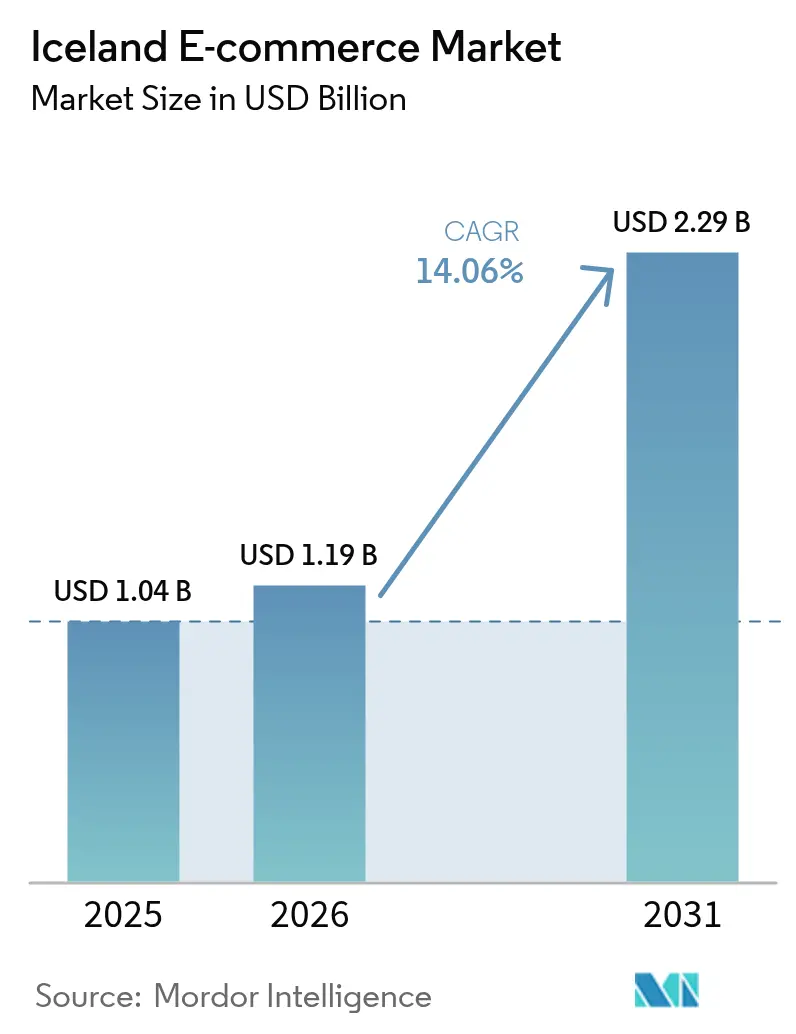

| Base Year Market Size (2025) | USD 1.04 Billion |

| Market Size (2026) | USD 1.19 Billion |

| Market Size (2031) | USD 2.29 Billion |

| Growth Rate (2026 - 2031) | 14.06% CAGR |

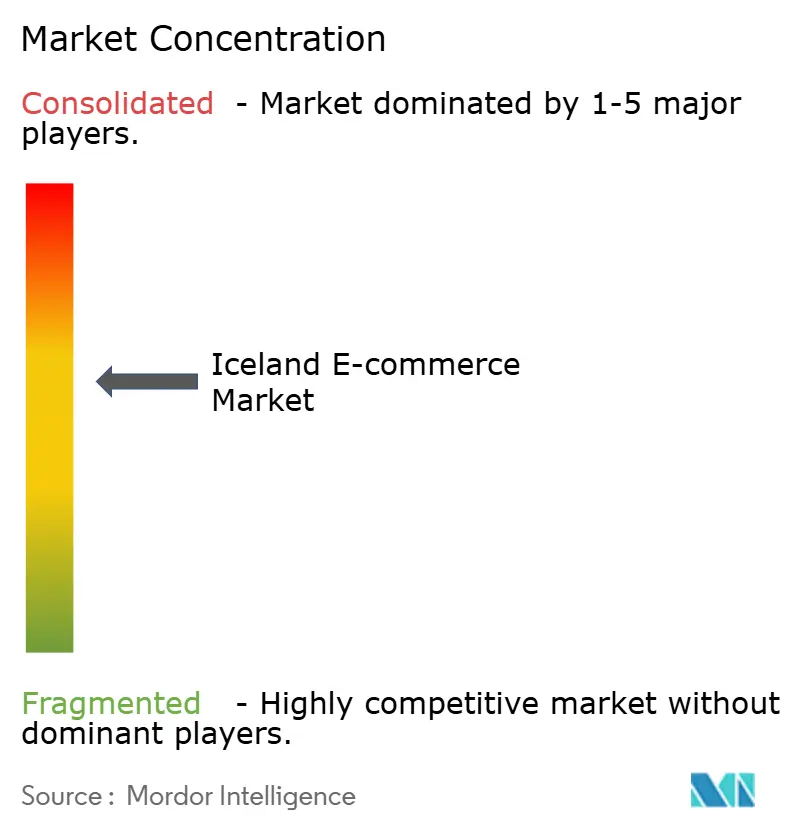

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Iceland E-commerce Market Analysis by Mordor Intelligence

The Iceland e-commerce market size in 2026 is estimated at USD 1.19 billion, growing from 2025 value of USD 1.04 billion with 2031 projections showing USD2.29 billion, growing at 14.06% CAGR over 2026-2031. Consistent 99.8% internet penetration, the country’s cash-lite payment culture, and a mobile-first shopping mindset underpin this expansion. Robust domestic card turnover, which topped ISK128.5 billion (USD 1.06 billion) in April 2025, confirms the strong consumer appetite for online transactions.[1]Central Bank of Iceland, “Payment Intermediation in April 2025,” cb.is International retailers benefit from a government VAT rebate on low-value imports, yet local merchants counter with Iceland Post’s same-day Reykjavik service and tailored loyalty programs. B2B digital procurement is accelerating as firms pursue efficiency gains, while tourism-fuelled demand for niche Icelandic goods opens cross-border revenue streams. Despite its momentum, the Iceland e-commerce market continues to battle scale constraints, volatile logistics costs, and import duties on non-EEA parcels.

Key Report Takeaways

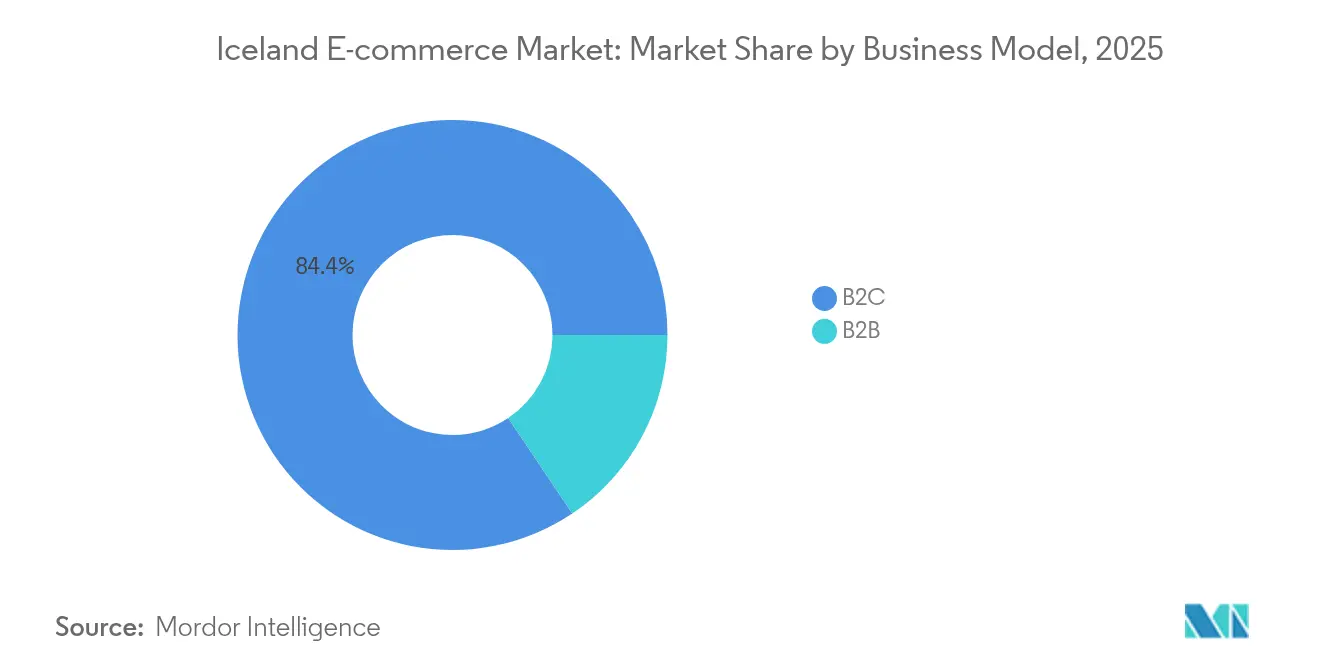

- By business model, the B2C segment led with an 84.40% Iceland e-commerce market share in 2025; B2B is forecast to grow at a 14.34% CAGR through 2031.

- By device type, mobile commerce captured 71.35% of 2025 sales and is pacing an annual 13.55% rise to 2031.

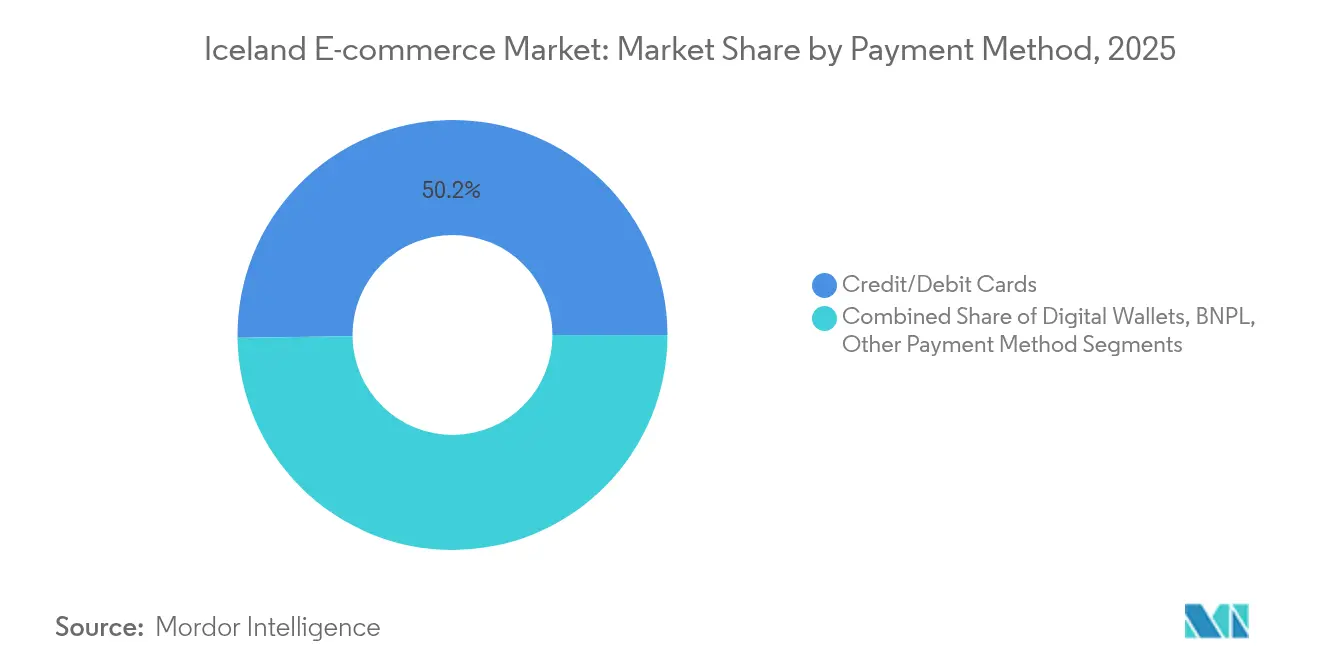

- By payment method, cards secured 50.20% share of transactions in 2025, while digital wallets are advancing at an 17.95% CAGR.

- By product category, Fashion & Apparel dominated with 27.45% revenue in 2025; Food & Beverages is expanding at a 14.31% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Iceland E-commerce Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hyper-digitised Population with 99% Internet Penetration | +3.6% | National | Long term (≥ 4 years) |

| Universal Bank-ID Adoption Enabling Frictionless Checkout | +3.1% | National | Medium term (2-4 years) |

| Government VAT-rebate on Cross-border Purchases Below ISK 2,000 | +2.6% | National, with early gains in Reykjavik | Medium term (2-4 years) |

| Iceland Post's Same-Day Reykjavik Network | +2.1% | Reykjavik metropolitan area | Short term (≤ 2 years) |

| Tourism-Driven Demand for Icelandic Niche Goods Online | +1.7% | National, with concentration in tourist destinations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Hyper-digitised Population with 99.8% Internet Penetration

Universal high-speed connectivity has produced digitally fluent shoppers who comfortably execute end-to-end purchases on smartphones, driving 72% of 2024 online sales. The state-backed Digital Iceland program deepened this readiness, with 38% of citizens adopting the government service app and 60% of driving licences now digital.[2]AWS Institute, “Iceland's Digital Modernizers Collaborate to Innovate,” d1.awsstatic.com Such infrastructure enables merchants to scale traffic without heavy customer-education costs and supports rapid diffusion of emerging formats like live shopping.

Universal Bank-ID Adoption Enabling Frictionless Checkout

Bank-ID, embedded across public and private services, streamlines log-ins and reduces payment friction, shrinking cart abandonment. The central Fast Payment System clears ISK payments in under 40 milliseconds and operates round-the-clock with zero downtime since launch.[3]World Bank, “Case Study: Iceland Fast Payment System,” fastpayments.worldbank.org Plans to pilot a rafkróna digital currency promise to embed instant settlement directly into the checkout flow, potentially lifting conversion and merchants’ working-capital efficiency.

Government VAT-Rebate on Cross-Border Purchases Below ISK2,000

The 24% standard VAT ordinarily lifts import prices, yet the rebate for low-value consignments removes that hurdle and spurs frequency of small-ticket overseas orders. International sellers of accessories and specialty foods have gained share, compelling domestic retailers to refine loyalty perks and private-label strategies to offset price gaps.

Iceland Post’s Same-Day Reykjavik Network

Posturinn’s dense urban routes enable same-day drops that overseas rivals struggle to match. For perishables and meal kits, this reliability directly shields repeat-purchase rates. Pending postal reforms that shift deliveries to community locker hubs could further cut last-mile cost and emissions, prompting merchants to recalibrate fulfilment options.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Small Domestic Customer Base Limits Economies of Scale | -2.1% | National | Long term (≥ 4 years) |

| Volatile Air-freight Costs Owing to Weather & Volcanic Disruptions | -1.7% | National, with greater impact on remote regions | Medium term (2-4 years) |

| High Import Duties on Non-EEA Parcels ≥ ISK 10,000 | -1.1% | National | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Small Domestic Customer Base Limits Economies of Scale

With fewer than 400,000 residents, local order volume can seldom amortize platform, marketing, and fulfilment investments. Operators therefore pivot to cross-border sales and membership schemes to lift average revenue per user. Fiscal tightening measures such as kilometre-based taxation may also temper discretionary spending, heightening the urgency of geographic diversification.

Volatile Air-Freight Costs Owing to Weather & Volcanic Disruptions

Unpredictable storms and ash clouds inflate shipping premiums and lengthen delivery windows beyond the usual 5-7 days to Europe, impacting SKUs with low margins or freshness requirements. Firms mitigate by holding buffer stock in key EU hubs and shifting slow-moving items to sea freight, though that strategy ties up capital.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Business Model: B2B Segment Accelerates Beyond Consumer Market

Iceland e-commerce market for B2C stood at 84.40% Iceland e-commerce market share in 2025, yet B2B digital trade is predicted to grow 14.34% annually to 2031, surpassing the mainstream channel. Public and private tenders increasingly specify e-procurement, shifting overall purchase cycles online.

Large hospitality chains now source perishables via integrated portals that reconcile invoices directly with accounting software, compressing payables lead time. Cloud-based marketplaces facilitate cross-dock consolidation, cutting inbound freight charges for small wholesalers. Alignment of VAT rules with EU place-of-supply standards from 2026 is anticipated to streamline compliance and encourage more SMEs to adopt e-procurement.

By Device Type: Mobile-First Strategy Reshapes User Experience

Mobile commerce processed 71.35% of transactions in 2025 and is rising at 13.55% CAGR, underscoring a decisive shift in shopper behavior. Responsive sites with biometric log-ins are now baseline, while in-app push campaigns drive higher order frequency.

Desktop maintains relevance for complex purchases such as multi-item B2B carts, but conversion lags mobile on fashion and grocery baskets. Wearables and in-car interfaces remain nascent; however, 5G rollout across major routes positions them for future growth. A potential rafkróna CBDC native to mobile wallets could further accelerate mobile checkout penetration.

By Payment Method: Digital Wallets Disrupt Card Dominance

Cards retained 50.20% share of 2025 online payments, yet wallet transactions are growing 17.95% each year. Tokenized wallet rails enhance security and support one-tap mobile orders, crucial for impulse purchases.

Bank transfers serve B2B invoices, while BNPL providers capture millennials seeking budgeting flexibility. The CBDC exploration aims to reduce cross-border fees and settlement delay, potentially lowering merchant service charges and inviting greater small-ticket volume.

By B2C Product Category: Food & Beverages Outpace Traditional Leaders**

Fashion & Apparel generated 27.45% of 2025 turnover, but Food & Beverages is on track for the fastest 14.31% CAGR. Grocery chains deploy dark-store picking and chilled lockers, raising delivery reliability and basket value.

Consumer Electronics holds solid rank supported by franchise operator Elko, while Beauty and DIY categories cultivate subscription programs to stabilize demand. Tourists sustain overseas reorder flows for wool and skincare, extending category life-cycle revenue.

Geography Analysis

Reykjavik accounted for more than 60.20% of the Iceland e-commerce market in 2025 thanks to population density, 1-day delivery, and the prevalence of digital wallets at checkout. Same-day coverage allows grocers to capture evening meal orders and electronics retailers to promise next-day repairs, cementing loyalty.

Beyond the capital, the West and North regions show mid-teen growth as logistics routes improve; rural households increasingly rely on online channels for specialty items unavailable locally. Delivery windows of 2-3 days remain acceptable for apparel and books but hinder perishable categories, sparking trials of community freezer hubs.

Internationally, outbound cross-border sales help local merchants magnify scale. Orders to the EU enjoy duty-free treatment under EEA terms, while shipments to North America rely on air-freight capacity tied to tourism passenger volumes. Conversely, inbound higher-value non-EEA parcels face the ISK10,000 (USD 82.5) duty barrier, moderating average-ticket size yet encouraging frequency of micro-orders.

Regulatory Landscape

E-commerce in Iceland is governed by Act No. 30/2002 on Electronic Commerce and Other Electronic Services, which is aligned with EU Directive 2000/31/EC through Iceland's EEA framework. The national tax and reporting environment tightened for platforms with Digital Platform Reporting Rules aligned with OECD and EU DAC7, effective January 1, 2025, requiring platform operators to collect and report seller information for relevant transactions.

Market conduct and connectivity regulation also shape digital commerce outcomes. The Icelandic Competition Authority (Samkeppni) applies competition law in line with EEA principles, while the Electronic Communications Office of Iceland (Fjarskiptastofa/ECOI) oversees telecom market entry and related obligations that underpin e-commerce reach and service quality, including network security focus areas under the current electronic communications regime.

Value Chain Analysis

The Iceland e-commerce value chain starts with merchants and brands selling through owned webshops and international marketplaces, supported by enabling layers such as digital identity (Bank-ID usage for authentication), payment acceptance (cards, wallets, transfers), and commerce technology stacks (platform hosting, checkout, fraud screening, and analytics). Increasing formalization is visible in the transaction layer as public-sector digital standards diffuse into the broader ecosystem, including B2G e-invoicing capability aligned with EU e-invoicing requirements.

Fulfilment and logistics remain the key operational differentiator and constraint due to cross-border dependence and last-mile economics outside Reykjavik. Domestic capability spans postal and courier networks and third-party logistics providers offering pick-pack-ship and distribution. Examples include Gorilla Warehouse for integrated warehousing and fast order processing for platform-based sellers, and Parlogis for warehousing, customs-related handling, and distribution for consumer and specialized goods. Retailers are also investing in planning and replenishment to reduce inventory and spoilage costs; for example, Krónan selected RELEX Solutions (July 2024) to automate forecasting and replenishment across multiple distribution centers, strengthening availability for online and omnichannel demand.

Competitive Landscape

The Iceland e-commerce market features a blend of global marketplaces and agile domestic specialists. Amazon and eBay serve cross-border segments, leveraging price breadth; however, local players such as Heimkaup differentiate through curated Icelandic SKUs and next-day delivery promises. Elko’s 2024 revenue rose 2.5% to NOK 47.15 billion (USD 4.5 billion) and the chain scales click-and-collect to keep freight costs predictable.

Samkaup pioneers online grocery since 2017 and now layers recipe-based baskets to raise unit economics. Fintech startups simplify multi-currency settlement, critical for exporters of niche goods. Meanwhile, the government’s crackdown on unsafe imports from ultralow-cost apps like Temu elevates compliance overhead, benefiting established retailers with documented supply chains.

Private-equity capital is entering: the EIF’s EUR 30 million (USD 33 million) allocation to Alfa Framtak’s new fund seeks to scale logistics tech and sustainability-oriented SMEs, signaling confidence in the addressable upside. Overall, competition centres on order-to-door speed, payment optionality, and depth of Iceland-branded assortments.

Iceland E-commerce Industry Leaders

Amazon.com, Inc.

Inter IKEA Systems B.V

Elko ehf

eBay Inc.

ASOS plc

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Compliance-driven tooling and services form a near-term whitespace as Iceland aligns platform and transaction reporting with EU and OECD mechanisms. The Digital Platform Reporting Rules effective January 1, 2025 increase demand for seller onboarding, data capture, and reconciliation workflows across marketplaces and merchant-of-record models, creating opportunities for payment providers, SaaS commerce platforms, and accountants to package DAC7-ready reporting, identity verification, and audit trails for Icelandic merchants and cross-border platforms.

Infrastructure and public-sector digitization programs are also translating into commercial opportunity for merchants and enablers. Digital Iceland published new guidance on applying AI within software development projects and implemented a new interdisciplinary framework agreement in April 2026, supporting broader adoption of AI-enabled customer service, personalization, and process automation across suppliers that serve the public sector and adjacent private markets. On the connectivity side, ECOI initiated a targeted risk assessment in April 2026 focused on security and supply-chain integrity of mobile networks and core infrastructure, while continuing significant market power (SMP) obligations on Mila in 2026. This keeps wholesale access governance in focus for broadband competition and the quality of last-mile connectivity that mobile-first commerce depends on.

Recent Industry Developments

- July 2026: Wolt launched quick delivery for around 300 over-the-counter pharmacy products through a partnership with Urdarapotek in the greater Reykjavik area. The service expands the range of regulated everyday essentials available via on-demand delivery and raises expectations for last-mile fulfillment through local e-commerce platforms.

- June 2026: Elko ehf opened a new electronics and accessories store in Smaralind shopping center (Kopavogur). The expansion supports an omnichannel footprint in a high-traffic retail hub and reinforces click-and-collect and service-led retail alongside online sales.

- April 2025: The European Investment Fund committed EUR 30 million to Alfa Framtak's AF3 private-equity vehicle, targeting digital transformation themes such as fulfillment automation and cross-border warehousing. This adds growth capital capacity for Iceland-focused logistics and commerce technology upgrades that address scale and cost constraints.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the Iceland e-commerce market is defined as the value of goods and services ordered through online channels by buyers in Iceland, covering business and consumer purchases, and counted at transaction value.

Scope exclusions: We exclude purely offline sales, informal peer-to-peer cash trades that are not tracked through online ordering, and non-transaction digital activity such as browsing and advertising.

Segmentation Overview

- By Business Model

- B2C

- B2B

- By Device Type

- Smartphone / Mobile

- Desktop and Laptop

- Other Device Types

- By Payment Method

- Credit / Debit Cards

- Digital Wallets

- BNPL

- Other Payment Method

- By B2C Product Category

- Beauty and Personal Care

- Consumer Electronics

- Fashion and Apparel

- Food and Beverages

- Furniture and Home

- Toys, DIY and Media

- Other Product Categories

Data Sources, Market Sizing, and Validation

Desk Research

Desk research started with public reference points that describe Iceland digital behavior and the retail and payments environment, so our assumptions stay realistic. Sources used included, where relevant, Statistics Iceland for household and retail series, the Central Bank of Iceland for payments trends, and the Icelandic tax authority guidance for VAT related rules that affect cross-border parcels.

We also reviewed non-paywalled sources such as OECD and Eurostat indicators for digital adoption comparisons, and we used logistics and customs publications that clarify delivery constraints for an island market. Company annual reports, investor presentations, and reputable press were used to sanity-check category momentum and channel strategies, and a paid subscription focused on company financials and news helped fill gaps where private disclosures were limited. The sources listed here are illustrative only, and many other public documents and databases were also used for data collection, validation, and clarification during the research.

Primary Interviews and Surveys

Primary work was used to test what the secondary data could not fully explain, especially the split between domestic online sales and cross-border purchases, and how payment methods and delivery costs are influencing conversion. We spoke with a mix of online retailers, marketplace operators, logistics providers, payment ecosystem participants, and category specialists, then cross-checked responses to align on practical assumptions for order value, returns, and promotional intensity.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 29% | CXOs: 15% | APAC: 48% |

| Mid tier: 56% | Functional/Unit leaders: 42% | EMEA: 34% |

| Smaller Players: 15% | Managers: 43% | Americas: 18% |

Market-Sizing & Forecasting

Sizing was built using a top-down and bottom-up approach, where national-level digital commerce demand was reconstructed from the buying population, online shopping participation, and typical spending levels, and then adjusted for cross-border ordering patterns that are common in Iceland. To keep the model grounded, we corroborated totals with selective bottom-up checks, such as sampled category sales ranges, ASP by basket type, and channel-level direction from retailer and logistics interviews.

Key inputs used in the model included online shopper penetration, category mix shifts (for example electronics versus grocery and essentials), average order value and discount depth, payment method adoption (cards versus wallets and BNPL where present), and delivery and returns economics that can suppress or accelerate conversion. Because these variables do not move at the same speed, forecasting leaned on scenario analysis with short, practical ranges for the main drivers, and then a central case was agreed through expert feedback. Where direct volume signals were missing, gaps were handled by using conservative participation rates and by anchoring ASP progression to observed inflation and promotion patterns rather than assuming smooth growth.

Data Validation & Update Cycle

Outputs were validated through multiple checks, including comparing implied per shopper spending against independent indicators, and reviewing category splits against what industry participants report as fast-moving or slowing. When the model produced sharp year-to-year jumps, the assumptions were rechecked, and follow-up calls were triggered to confirm whether the change was real or driven by one-off factors like currency movement or promotional spikes.

Before sign-off, a separate analyst review is completed so calculation logic, unit conversions, and scope boundaries remain consistent across sections. The report is refreshed annually, and interim updates are made when material events occur, such as rule changes affecting cross-border VAT treatment or meaningful shifts in payment behavior. Right before delivery, we run a final update pass so clients receive the most current view available.

Mordor Intelligence's Iceland Ecommerce Market Size Measured Against Other Published Estimates

Published market sizes for Iceland e-commerce often do not match because the scope line is drawn differently, and the timing of currency conversion and the way average order value is trended can move the result noticeably. Some figures also mix a platform view with a buyer spending view, which can create double counting when cross-border activity is involved.

The biggest gap drivers we saw were whether cross-border purchases by Iceland residents are included, whether B2B transactions are counted alongside consumer sales, and whether totals are kept in local currency until the final conversion step. By refreshing exchange-rate timing and re-checking implied spending per online shopper during each annual update cycle, the model stays closer to observed demand signals, a choice applied by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.04 B (2025) | |

| Industry Data Platform A | USD 0.69 B (2024) | Often reflects reported online retail revenue tracking and may exclude B2B buying and parts of cross-border spend, with a different base year that reduces comparability to a 2025 transaction-value estimate. |

| Global Consultancy A | USD 1.40 B (2026) | Uses a later base year and a broader definition that can fold in adjacent digital commerce elements (such as services and wider platform activity), and the currency timing and ASP progression assumptions are not always transparent. |

Looking across the three values, the spread is largely explained by year alignment and by whether the estimate is anchored to buyer transaction value versus narrower retailer revenue reporting. When scope boundaries are kept explicit and assumptions are rechecked against simple spend and participation signals, the resulting market size becomes easier to trace and replicate for decision use.

Key Questions Answered in the Report

What is the current size of the Iceland e-commerce market?

It is valued at USD1.19 billion in 2026 and is projected to double to USD2.29 billion by 2031.

Which segment is growing fastest in the Iceland e-commerce market?

B2B digital commerce is expanding at a 14.34% CAGR, outpacing the consumer channel.

How important is mobile shopping in Iceland?

Mobile accounts for 71.35% of transactions and is still rising at 13.55% annually, making a mobile-first strategy essential.

What payment methods are gaining ground?

Digital wallets are the quickest-growing method, posting an 17.95% CAGR, although cards remain the single largest medium.

How do government policies influence cross-border shopping?

A VAT rebate on imports under ISK 2,000 (USD 16.47) encourages small-value overseas orders, while duties on parcels above ISK 10,000 (USD 82.37) temper larger purchases.

Which product categories present the best growth prospects?

Food & Beverages leads growth at 14.31% CAGR due to improved cold-chain logistics and changing consumer preferences.

Page last updated on: