Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

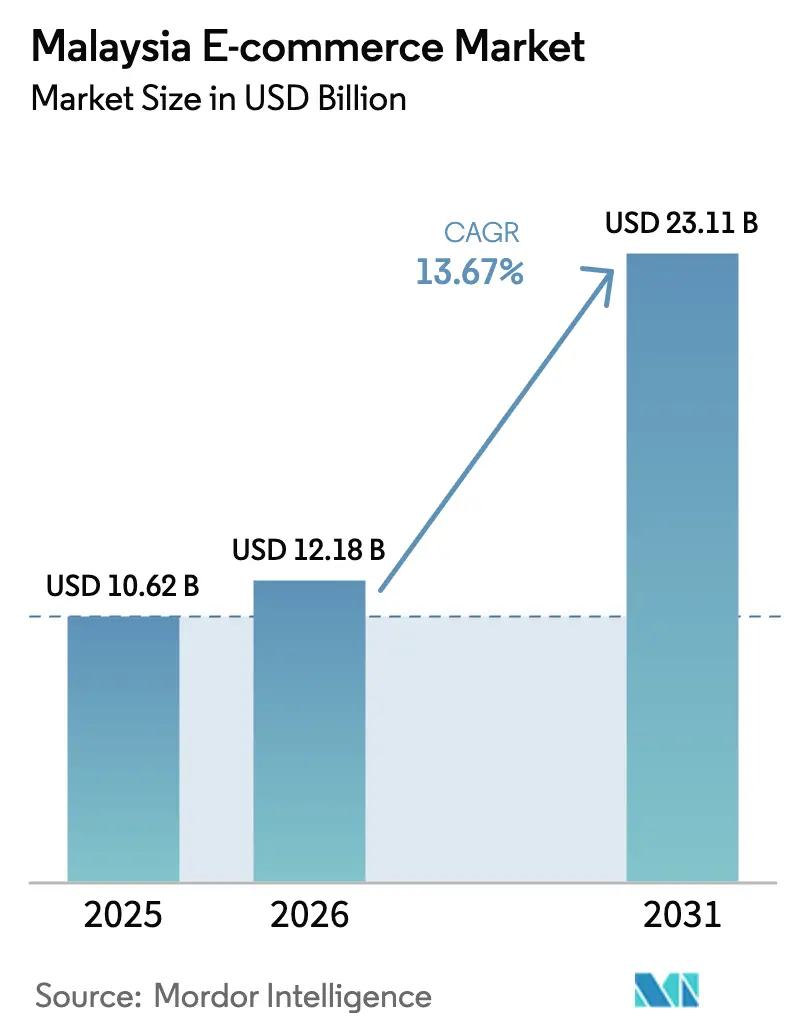

| Base Year Market Size (2025) | USD 10.62 Billion |

| Market Size (2026) | USD 12.18 Billion |

| Market Size (2031) | USD 23.11 Billion |

| Growth Rate (2026 - 2031) | 13.67% CAGR |

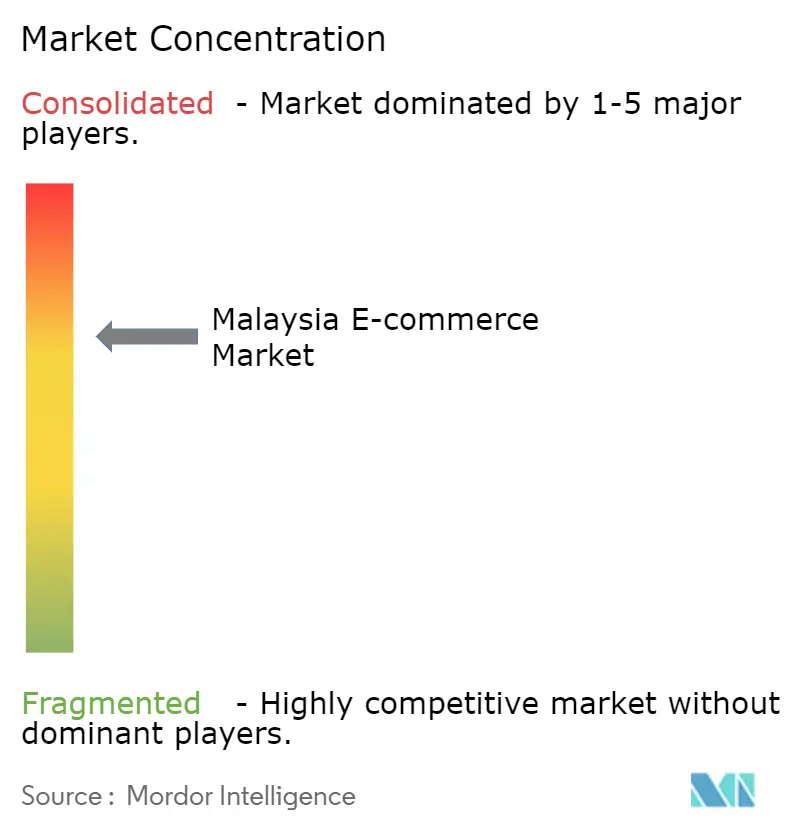

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Malaysia E-commerce Market Analysis by Mordor Intelligence

The Malaysia e-commerce market size is expected to increase from USD 10.62 billion in 2025 to USD 12.18 billion in 2026 and reach USD 23.11 billion by 2031, growing at a CAGR of 13.67% over 2026-2031. Strong policy support, ubiquitous mobile connectivity, and instant digital payments continue to propel the Malaysia e-commerce market, especially among millennials and first-time rural buyers. Government mandates such as the National E-Commerce Strategic Roadmap 2.0 and MyDIGITAL lower entry barriers for 1.1 million small businesses, while 82.4% 5G coverage underpins app-first shopping journeys. Interoperable DuitNow QR has removed payment friction at 2.6 million merchant points, enabling live-stream shopping to flourish as social video converts on-the-spot interest into sales. Competitive intensity is rising as TikTok Shop, Shopee, and Lazada pour subsidies into user acquisition even though urban penetration already exceeds 85% and customer acquisition costs keep climbing. The Malaysia e-commerce market retains considerable upside in halal-certified assortments and value-added reverse logistics that can unlock demand from East Malaysia’s underserved consumers.

Key Report Takeaways

- By product category, fashion and apparel led with 26.67% revenue share in 2025, while food and beverages are forecast to expand at a 16.46% CAGR through 2031.

- By business model, the B2C segment held 80.89% of the Malaysia e-commerce market share in 2025, whereas B2B is projected to record the fastest 15.63% CAGR to 2031.

- By device, smartphones captured 72.67% of the Malaysia e-commerce market size in 2025 and are projected to advance at a 15.87% CAGR over the forecast horizon.

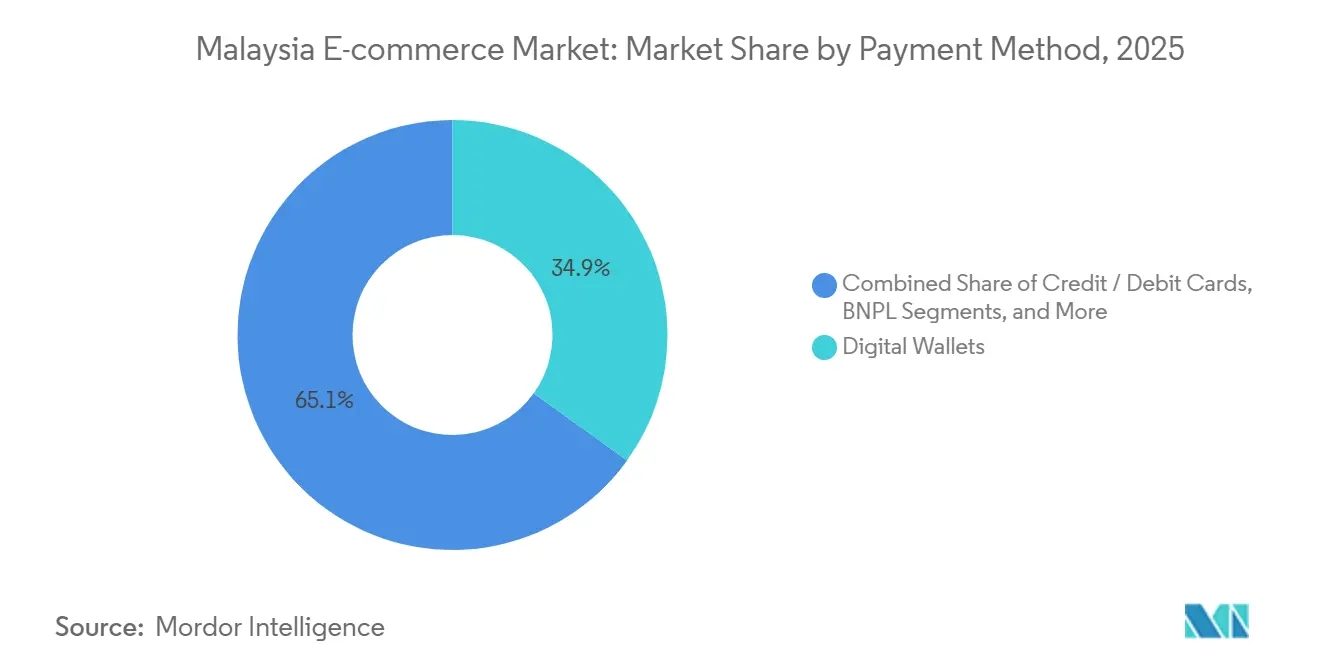

- By payment method, digital wallets accounted for 34.92% of transaction value in 2025, while buy-now-pay-later solutions are set to grow at a 17.18% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Malaysia E-commerce Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government Digitalisation Agendas (NESR 2.0, MyDIGITAL) | +2.2% | National, early gains in Klang Valley, Penang, Johor Bahru | Medium term (2-4 years) |

| 90%+ Smartphone Penetration and Expanding 5G Coverage Boosting M-Commerce | +1.8% | National, faster in urban centers | Short term (≤ 2 years) |

| Rapid E-Wallet Adoption and Interoperable DuitNow QR | +1.5% | Peninsular core, expanding to East Malaysia | Short term (≤ 2 years) |

| Dense Third-Party Logistics and On-Demand Delivery Build-Out | +1.3% | Peninsular Malaysia core | Medium term (2-4 years) |

| Live-Stream and Social-Commerce GMV Surge | +1.4% | National, urban youth leading | Short term (≤ 2 years) |

| Halal-Certified Online Shelves Unlocking Rural Demand | +0.9% | National, spillover to Indonesia, Brunei, Middle East | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government Digitalisation Agendas (NESR 2.0, MyDIGITAL)

Policy blueprints act as scaffolding that de-risk private investment in fulfilment, payments, and digital skills. Grants lowered onboarding costs for 1.148 million businesses by 2025, while mandatory e-invoicing in July 2025 nudged legacy retailers online.[1]Malaysia Digital Economy Corporation, “MyDIGITAL Blueprint Progress Report 2025,” MDEC.MY Customs pre-clearance slashed parcel transit times from China and Singapore by 30% in 2024, yet the MYR 1.65 trillion GMV target for 2025 still outpaces current infrastructure. Continued public spending until 2031 remains pivotal for rural inclusion.

90%+ Smartphone and 5G Coverage Boosting M-Commerce

5G covered 82.4% of populated areas by Q3 2025, though median speeds fell to 243 Mbps as user density surged.[2]Opensignal, “Malaysia 5G Experience Report Q3 2025,” OPENSIGNAL.COM Smartphones already drive nearly three-quarters of Malaysia e-commerce market transactions, and progressive web apps that load under three seconds shield conversion rates even on congested towers. Planned mid-band spectrum in 2026 will triple capacity in Kuala Lumpur, Penang, and Johor Bahru, while rural Sabah and Sarawak still depend on 4G backhaul that struggles with high-definition product videos.

Rapid E-Wallet Adoption and Interoperable DuitNow QR

Digital wallets processed MYR 31.1 billion (USD 7.2 billion) in 2024 and held 34.92% share of online payments in 2025.[3]PayNet, “DuitNow QR Annual Report 2024,” PAYNET.MY Cross-border QR linkages with Singapore, Thailand, and Indonesia handled 4.1 million transactions, supporting frictionless tourist shopping and seller liquidity via same-day payouts. A 2025 directive will force all licensed wallets onto DuitNow by mid-2026, yet wallet proliferation, 3.2 active accounts per user, creates brand-loyalty challenges.

Live-Stream and Social-Commerce (TikTok Shop) GMV Surge

The two-month suspension of TikTok Shop in 2024 erased around USD 200 million in monthly GMV, proving both its scale and regulatory vulnerability. After local registration, TikTok Shop recaptured Gen Z buyers, and live-stream formats now generate up to 22% of platform GMV. Brands are reallocating budgets from static ads to interactive sessions that convert three-to-five times faster, but stricter content moderation raises compliance costs that favor incumbents with deep resources.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Cyber-Fraud and Data-Breach Incidents Eroding Trust | -1.6% | National, higher in urban centers | Short term (≤ 2 years) |

| High Last-Mile Cost to East Malaysia and Remote Islands | -0.8% | Sabah, Sarawak, Labuan, islands | Long term (≥ 4 years) |

| Escalating CAC From Urban Market Saturation | -1.1% | Klang Valley, Penang, Johor Bahru | Medium term (2-4 years) |

| Emerging Data-Localisation and Cross-Border Compliance Risk | -0.7% | National, ASEAN trade | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Cyber-Fraud and Data-Breach Incidents Eroding Trust

The communications regulator logged over 70,000 online-scam cases in 2024, costing consumers more than MYR 1.8 billion (USD 420 million).[4]Malaysian Communications and Multimedia Commission, “Cyber Security Incident Report 2024,” MCMC.GOV.MY High-profile telco breaches heightened fears around credential theft, pushing cart-abandonment to 68% in 2025. Two-factor authentication and biometrics reduce fraud but add 18 seconds to mobile checkout, straining user patience.

Escalating CAC From Urban Market Saturation

Urban penetration already exceeds 85% in the Klang Valley, Penang, and Johor Bahru, forcing platforms to spend more on cash-backs, free shipping, and influencer fees to capture incremental users. Customer acquisition cost (CAC) for first-time buyers climbed 23% year on year in 2025, eroding contribution margins even as average order values plateaued. Promotional intensity peaked during peak-sale events when Shopee, Lazada, and TikTok Shop collectively offered more than MYR 150 million (USD 35 million) in vouchers in a single week, yet traffic gains proved short-lived. Rising digital-ad prices on Meta and Google further inflate CAC because social-commerce entrants compete for the same urban eyeballs. Platforms are responding by shifting budgets toward loyalty programs and in-app games that raise repeat-purchase frequency, but payback periods still stretch beyond 18 months for new city users. Unless rural onboarding accelerates, elevated CAC will keep pressuring profitability through at least 2028.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Business Model: B2B Digitization Accelerates as Procurement Shifts Online

Business-to-consumer transactions retained 80.89% of the Malaysia e-commerce market in 2025 on the back of subsidies and influencer-led discovery. The Malaysia e-commerce market size for B2B platforms is projected to grow at 15.63% CAGR to 2031 as mandatory e-invoicing drives enterprises toward API-ready procurement portals. Wholesale marketplaces such as Dropee and Ralali automate invoices, unlock bulk discounts, and shrink working-capital cycles by up to 18 days. Despite the momentum, B2B GMV remains clustered in Peninsular Malaysia because East Malaysian manufacturers still face prohibitive air-freight costs.

Consumer-facing platforms spent an estimated MYR 3.5 billion (USD 814 million) on shipping rebates and cashback in 2025, a tactic expected to moderate as investors demand profit. Fashion, electronics, and beauty comprised roughly 60% of B2C GMV, aided by live-stream tags that convert impulse interest at triple the rate of keyword search. B2B growth provides a new revenue pool, yet capturing it requires deeper logistics integrations and embedded financing tools.

By Device Type: Mobile Dominance Reinforced by 5G Rollout and App-First Strategies

Smartphones generated 72.67% of 2025 transactions, and this slice of the Malaysia e-commerce market size is forecast to climb with a 15.87% CAGR to 2031. Progressive web apps that load rapidly on 4G and in-app wallets that remember credentials keep friction low.

Desktop usage lingers among enterprise buyers and older shoppers but is declining 8% each year. Tablets and smart TVs remain niche; however, voice-assisted grocery purchasing is gaining popularity in family households. New privacy rules around device fingerprinting shift attribution toward persistent app logins, a clear advantage for mobile-centric ecosystems.

By Payment Method: BNPL Fastest Growth as Credit Access Widens

Digital wallets led with 34.92% share in 2025 as interoperable DuitNow QR wiped out checkout barriers. Buy-now-pay-later, the fastest rising slice of the Malaysia e-commerce market, is set to post 17.18% CAGR to 2031, fuelled by Gen Z’s appetite for installment plans on electronics and fashion.

Bank Negara Malaysia’s 2024 rules mandated affordability checks and delinquency reporting, raising compliance costs yet legitimizing the sector. Card payments still dominate cross-border orders but face merchant resistance due to 2% interchange fees. Cash on delivery continues to fade as e-invoicing demands traceable digital trails.

By B2C Product Category: Food and Beverages Fastest Growth on Quick-Commerce Momentum

Fashion and apparel captured 26.67% of 2025 revenue, benefiting from social try-ons and AI sizing that trim return rates. Food and beverages are poised to grow at 16.46% CAGR to 2031, the quickest in the Malaysia e-commerce market, thanks to GrabMart’s 30-minute delivery promise in major cities.

Consumer electronics enjoy strong brand partnerships and trade-in offers, while beauty gains from subscription replenishment models. Furniture, automotive parts, and pet supplies carve out smaller yet double-digit growth corridors as augmented-reality visualization and auto-reorder features mitigate past frictions.

Geography Analysis

Peninsular Malaysia accounted for roughly 75% of 2025 transactions as dense logistics hubs support same-day delivery and higher discretionary spend. The Malaysia e-commerce market continues to benefit from cross-border QR payments with Singapore, Thailand, and Indonesia that handled MYR 348.3 million (USD 81 million) in 2024.

East Malaysia, home to 5.8 million residents, generated close to 15% of volume but lags because last-mile costs inflate basket prices by up to 60%. The Malaysia e-commerce market share in rural Sabah and Sarawak will rise once the Pan Borneo Highway and Salam subsea cable narrow connectivity gaps, yet projects extend beyond 2028.

Digital-literacy drives and subsidies have already onboarded over a million small businesses, reducing the urban-rural divide from 5.2 million to 3.8 million unconnected adults between 2024 and 2026. Nevertheless, average order value outside the Klang Valley remains 30% lower, reflecting lower disposable incomes and a heavier focus on essentials.

Competitive Landscape

Shopee controlled about 60% of the Malaysia e-commerce market in 2025, powered by Sea Limited’s USD 2.7 billion Q3 2024 e-commerce revenue, up 27% year on year.[5]Sea Limited, “Third Quarter 2024 Financial Results,” INVESTORS.SEA.COM Lazada retained near-30% share after Alibaba’s divestment to Central Group, pivoting toward profitability with selective fulfillment-center closures.

TikTok Shop’s December 2024 re-entry re-ignited live-stream commerce and pushed incumbents to raise marketing outlays despite flattening urban penetration. Regulatory compliance around content moderation and data privacy is becoming a moat: platforms with established legal and cyber-security teams can absorb rising overheads more easily than start-ups.

Vertical specialists, Zalora for fashion, Senheng for electronics, PG Mall for general merchandise, address product niches and halal-certified demand. White-space remains in reverse logistics, especially affordable returns from East Malaysia, and in B2B procurement where 1.15 million SMEs still rely on manual ordering. AI-driven personalization and dynamic pricing are table stakes as leading platforms process billions of data points daily to refine rankings and inventory forecasting.

Malaysia E-commerce Industry Leaders

Shopee (Sea Ltd)

Lazada Group (Alibaba)

Lelong.my

Zalora (Global Fashion Group)

GoShop (Astro GS Shop Sdn Bhd)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Malaysia’s mandatory e-invoicing system went live for large companies, accelerating enterprise adoption of platforms with built-in invoicing APIs.

- April 2025: Sandakan air-cargo terminal opened with 15,000 metric-ton capacity, cutting East Malaysia air-freight times by 12 hours.

- March 2025: Pos Malaysia’s Pos Fulfill launched a 50,000-sq-ft center in Kota Kinabalu, expanding East Malaysian warehousing.

- February 2025: Bank Negara Malaysia finalized licensing rules for BNPL, capping interest rates and mandating affordability checks.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

According to Mordor Intelligence, the Malaysia e-commerce market refers to the total value of goods and fee-based services bought through internet-enabled websites or mobile apps from Malaysia-registered sellers, covering domestic and outward cross-border flows for both B2C and B2B transactions. Internal corporate purchases made on digital procurement platforms are counted to reflect true commercial activity.

Pure peer-to-peer resale, online travel bookings, and streaming subscriptions sit outside this sizing.

Segmentation Overview

- By Business Model

- B2C

- B2B

- By Device Type (B2C)

- Smartphone / Mobile

- Desktop and Laptop

- Other Device Types

- By Payment Method (B2C)

- Credit / Debit Cards

- Digital Wallets

- Buy Now Pay Later (BNPL)

- Other Payment Methods

- By Product Category (B2C)

- Beauty and Personal Care

- Consumer Electronics

- Fashion and Apparel

- Food and Beverages

- Furniture and Home

- Toys, DIY and Media

- Other Product Categories

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed marketplace operators, payment gateways, third-party logistics firms, and mid-sized merchants across Klang Valley, Johor, and Sabah. The discussions clarified active seller numbers, average basket size, cash-on-delivery share, and regulatory moves, letting us close data gaps and stress-test model assumptions.

Desk Research

Our analysts began by mining quarterly e-commerce revenue tables from the Department of Statistics Malaysia, Bank Negara electronic payment dashboards, and International Telecommunication Union connectivity metrics, which frame users, spend, and access. Insights from MDEC's National E-commerce Strategic Roadmap updates, Logistics and Supply Chain Association briefs, and open customs shipment tallies helped us map cross-border intensity and channel mix. Company filings gathered through D&B Hoovers and news feeds on Dow Jones Factiva supplied merchant GMV hints, capacity additions, and pricing cues. The sources named illustrate the breadth; many further references were reviewed to screen and verify every datapoint.

Market-Sizing & Forecasting

We start with a top-down reconstruction of Department of Statistics totals, adjust for intra-company trade, cross-border leakage, and currency movements, and then use bottom-up roll-ups of leading platform GMV, sampled ASP × order volumes, and parcel manifests as cross-checks. Key variables powering the model include internet user growth, smartphone penetration, disposable income index, digital wallet transaction volume, and BNPL uptake. A multivariate regression links these drivers to historical value, while scenario analysis brackets impacts from tax or logistics shifts. When bottom-up indicators diverge, figures are rebased toward the weighted mean agreed during expert calls.

Data Validation & Update Cycle

Each estimate passes variance checks against government releases, platform disclosures, and payment proxies before sign-off. Two analysts review the workbook independently, followed by a senior review. The study refreshes annually, with interim updates if policy or competitive shocks materially move the baseline.

Why Mordor's Malaysia E-Commerce Baseline Stands Solid

Published estimates often diverge because firms select different scopes, projection horizons, and refresh rhythms. We acknowledge this spread, then focus on the levers that widen the gap.

Differences typically stem from whether B2B demand is counted, how cross-border sales are treated, the way average selling prices trend, and the cadence at which macro variables are rolled forward. By including verified B2B flows, applying annual refreshes, and blending top-down with selective bottom-up checks, Mordor's 2025 baseline remains balanced and dependable.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 10.69 B (2025) | Mordor Intelligence | - |

| USD 10.75 B (2024) | Regional Consultancy A | Omits B2B and digital service revenue |

| USD 15.7 B (2028) | Trade Journal B | Projects from one channel and older base year |

| USD 80.40 B (2024) | Industry Association C | Bundles broader digital economy and payment flows |

These comparisons show that definition creep or infrequent updates can swing totals sharply. Our disciplined scope and annually refreshed model give decision-makers a transparent baseline traceable to clear variables and repeatable steps.

Key Questions Answered in the Report

How large is the Malaysia e-commerce market in 2026?

It reached USD 12.18 billion in 2026 and is on track for USD 23.11 billion by 2031, reflecting a 13.67% CAGR.

Which segment is growing fastest within Malaysia's online retail space?

Food and beverages are poised for the quickest 16.46% CAGR through 2031, fueled by quick-commerce models that promise 30-minute delivery.

What drives the dominance of smartphones in online shopping?

82.4% 5G coverage and app-first designs pushed smartphones to 72.67% of 2025 transactions, and this share keeps rising with faster spectrum rollouts.

Why is buy-now-pay-later expanding so quickly?

BNPL solutions combine instant credit decisions with capped interest rates under new regulations, enabling 17.18% CAGR as Gen Z shoppers finance higher-ticket items.

What challenges curb growth in East Malaysia?

Air-freight premiums and sparse infrastructure inflate delivery costs by up to 60%, delaying parity with Peninsular shopping experiences until highway and subsea-cable projects finish after 2028.

Page last updated on: