Drone Package Delivery Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

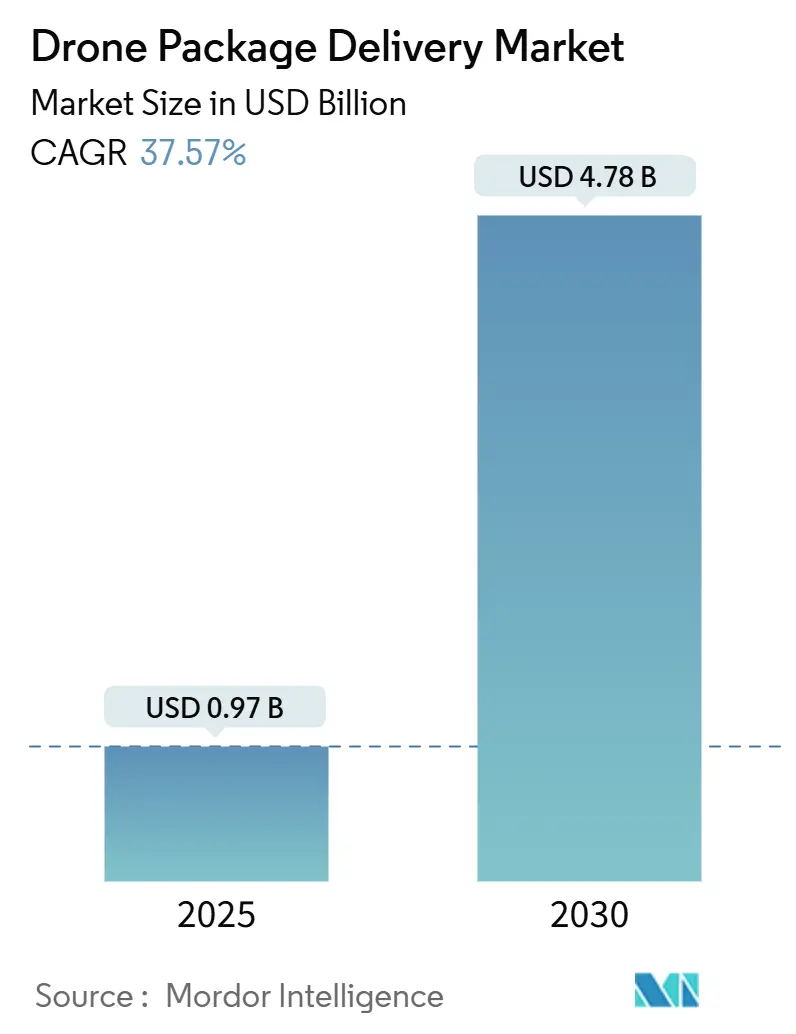

| Market Size (2025) | USD 0.97 Billion |

| Market Size (2030) | USD 4.78 Billion |

| Growth Rate (2025 - 2030) | 37.57% CAGR |

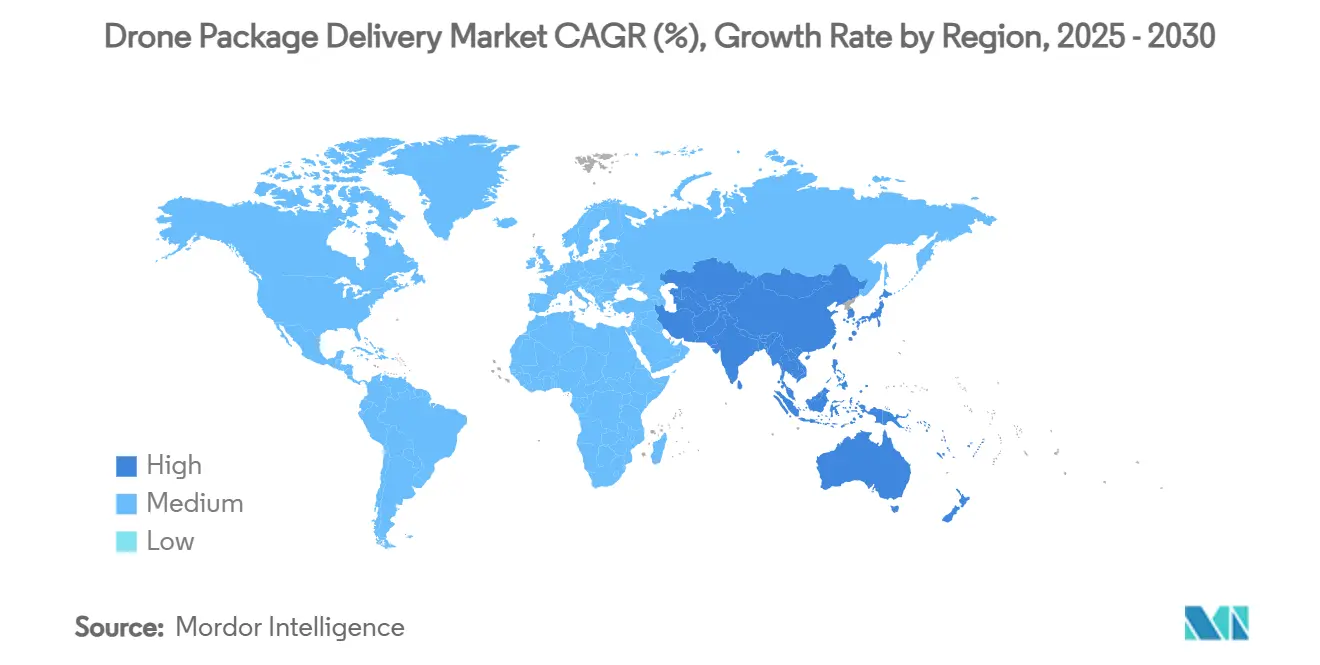

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Drone Package Delivery Market Analysis by Mordor Intelligence

The Drone Package Delivery Market size is estimated at USD 0.97 billion in 2025, and is expected to reach USD 4.78 billion by 2030, at a CAGR of 37.57% during the forecast period (2025-2030).

Regulatory liberalization, especially approvals for beyond-visual-line-of-sight (BVLOS) flights, converges with battery advances and rising e-commerce expectations to transform pilot programs into revenue-generating networks. Operators securing early BVLOS certificates rapidly convert test corridors into commercial lanes, while partnerships with retailers and healthcare systems shorten time-to-scale and reduce customer acquisition costs. Asia-Pacific’s low-altitude economy policies, North America’s retail alliances, and Europe’s sustainability mandates combine to enlarge the addressable customer base, encouraging investors to shift from hardware bets toward service-led platforms. Competitive intensity remains moderate because certification hurdles and ground infrastructure needs slow copy-cat entry, allowing first movers to lock in exclusive airspace slots and neighborhood goodwill.

Key Report Takeaways

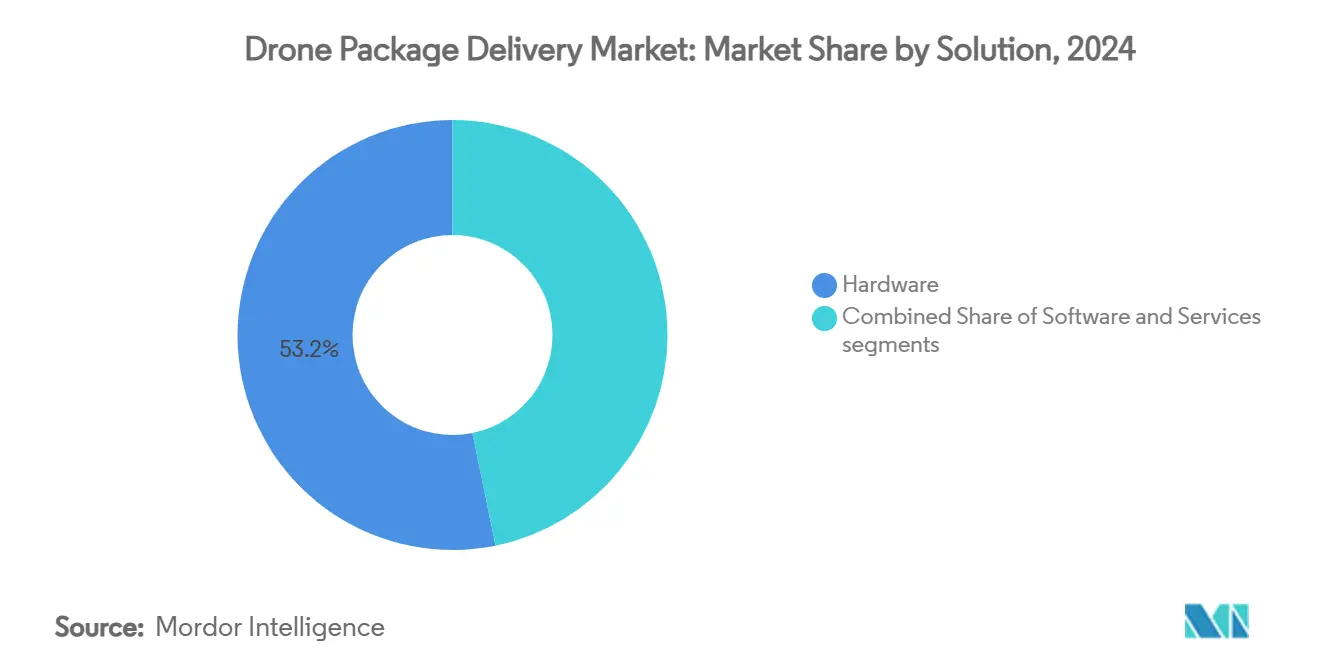

- By solution, services advanced at a 42.10% CAGR to 2030, while hardware captured 53.21% of the 2024 drone package delivery market size.

- By drone type, hybrid VTOL platforms expanded at 45.22% CAGR, yet multi-rotor systems retained 66.76% 2024 revenue share within the drone package delivery market.

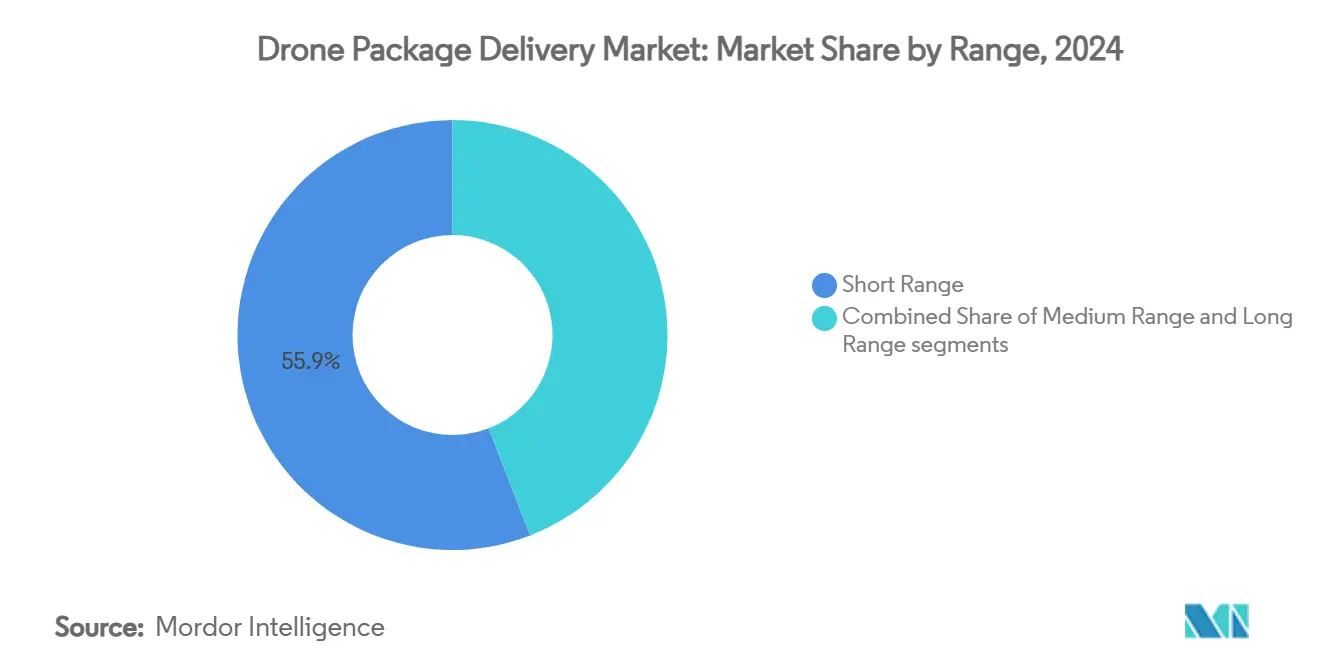

- By range, long-range missions increased at 40.01% CAGR; short-range flights still accounted for 55.89% of the 2024 drone package delivery market size.

- By package size, less than 2 kg held 46.22% of the market share, whereas more than 5 kg registered the highest 38.85% CAGR during the forecast period.

- By end use, medical aid delivery registered the highest 43.56% CAGR during the forecast period, whereas food delivery held 36.87% of the 2024 drone package delivery market share.

- By geography, Asia-Pacific led growth with a 41.20% CAGR, but North America commanded 33.15% revenue share in 2024.

Global Drone Package Delivery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Improving regulatory frameworks supporting commercial long-range drone operations | +8.2% | US, EU, China | Medium term (2-4 years) |

| Surging demand for rapid fulfillment driven by e-commerce and quick commerce growth | +9.1% | Global urban centers | Short term (≤ 2 years) |

| Expanding use of drones for cold-chain logistics in remote and underserved areas | +6.7% | Asia-Pacific core; Africa, rural Americas spill-over | Medium term (2-4 years) |

| Increased investment in scalable drone logistics platforms and service networks | +7.3% | North America, EU moving to Asia-Pacific | Long term (≥ 4 years) |

| Sustainability goals driving adoption of low-emission last-mile delivery solutions | +4.8% | EU leadership; North America follower | Long term (≥ 4 years) |

| Advancements in AI-driven fleet management enhancing operational efficiency | +5.5% | Technology-forward regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Improving Regulatory Frameworks Supporting Commercial Long-Range Drone Operations

Historic BVLOS approvals in the Dallas-Fort Worth airspace marked the Federal Aviation Administration’s move from waiver-based pilots to standardized permits that let operators fly autonomously without visual observers.[1]Federal Aviation Administration, “FAA Makes Drone History in Dallas Area,” FAA.GOV Parallel progress in Europe, where EASA’s April 2024 VTOL package created uniform certification tracks, lowers compliance friction for cross-border fleets. China’s low-altitude economy initiative accelerates the same trend by treating UAS corridors as public infrastructure, enabling large-scale experiments. These policy shifts create time-boxed windows for incumbents to lock in routes, erect docks, and build community trust before the rules open to broad competition. Integration of Unmanned Aircraft System Traffic Management (UTM) software allows many service providers to share lanes, removing the single-operator bottleneck that had capped growth. The emerging Part 108 corporate-oversight model signals a shift from aircraft-specific paperwork toward performance-based oversight that scales far faster than legacy aviation rules.

Surging Demand for Rapid Fulfillment Driven by E-Commerce and Quick Commerce Growth

Same-day parcel volumes have risen near 30% annually as retailers compete on speed instead of price, making ultra-fast delivery a loyalty tool rather than a paid premium. Amazon’s public goal of 500 million drone drops by 2030 demonstrates the scale of latent demand, especially for sub-5-lb goods that dominate online baskets. Alphabet’s Wing routinely averages sub-19-minute fulfillment windows, confirming drones can beat road couriers in dense suburbs. DoorDash’s 15-minute Dallas deliveries show consumers pay extra for immediacy, giving retailers margin headroom to offset drone opex. Weather resilience and traffic-free routing further boost reliability, strengthening the customer experience flywheel that funnels future traffic toward operators offering the fastest guaranteed dispatch.

Expanding Use of Drones for Cold-Chain Logistics in Remote and Underserved Areas

When road access or refrigeration is unreliable, healthcare systems turn to drones for blood, vaccines, and temperature-sensitive drugs. Active Peltier-based cooling keeps payloads at –10 °C without bulky ice packs, extending range and cutting waste. In Rwanda, Zipline now services 84% of hospitals, cutting postpartum hemorrhage fatalities by 51% through on-demand blood drops. Volansi’s cold-chain program in rural North Carolina shows the model can scale commercially under US regulations. With medical drone deliveries p rojected to rise from USD 1.47 billion in 2024 to USD 4.68 billion by 2032, healthcare is emerging as the use case most insulated from price wars because it addresses life-or-death logistics.

Increased Investment in Scalable Drone Logistics Platforms and Service Networks

Investors now back network builders instead of airframe tinkerers. Zipline’s USD 4.2 billion valuation and USD 500 million capital raise highlight the premium on route density and recurring revenue. Walmart’s 100-store drone rollout with Wing and Zipline demonstrates how asset-light Delivery-as-a-Service (DaaS) models can extend a retailer’s customer promise without owning fleets. Autonomous docks such as A2Z’s AirDock enable 24/7 charging and parcel hand-off without staff, dropping per-delivery labor to cents and unlocking overnight utilization. Beta Technologies’ 46-station charging grid proves the complementary ground network is forming in parallel, making range-limited drones viable at a continental scale.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Payload capacity and battery efficiency limitations for heavy or bulk deliveries | -6.8% | Global; sharper in sparsely populated regions | Medium term (2-4 years) |

| Public concerns over noise pollution, privacy, and airspace safety | -4.2% | Dense urban neighborhoods worldwide | Short term (≤ 2 years) |

| Insufficient ground infrastructure for takeoff, landing, and charging in urban areas | -5.5% | Developing-market metros | Long term (≥ 4 years) |

| Limited availability of high-energy-density batteries suitable for aviation applications | -7.1% | Technology-dependent markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Payload Capacity and Battery Efficiency Limitations for Heavy or Bulk Deliveries

Energy density of mainstream lithium-ion (Li-ion) packs hovers near 200 Wh/kg, capping economically viable payloads at under 5 lb and constraining the drone package delivery market to high-value, low-weight products. Lithium-sulfur (Li-S) chemistries could double storage but remain in pilot lines producing under 20,000 units annually. Hybrid-electric craft like Elroy Air’s Chaparral stretch range to 300 mi with 300 lb cargo, yet added mechanical complexity lifts maintenance overheads. Operators thus face a trade-off: chase heavier freight with pricier airframes or stick to profitable light parcels until batteries leap forward.

Public Concerns Over Noise Pollution, Privacy, and Airspace Safety

Amazon’s College Station trials paused after neighbors likened drone swarms to a “giant hive of bees,” even though measured sound pressure sat within suburban norms. MK30 redesigns promise a 50% noise cut, but perception, not decibels, drives complaints. Privacy worries around airborne cameras compound resistance, pushing regulators toward transparency mandates that may curb autonomous route changes. Australia logged only three formal objections to thousands of deliveries, yet researchers warn complex red tape discourages feedback, masking latent dissent. Without proactive community outreach, noise and privacy issues could slow permits in new zip codes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Solution: Services Drive Market Evolution

The services slice captured 42.10% CAGR to 2030, signaling a pivot from asset sales toward recurring logistics revenue within the drone package delivery market. Operators bundling aircraft, software, and insurance into pay-per-drop contracts achieve higher asset turns and lock-in, contrasting hardware vendors facing commoditization.

Growth persists because enterprise clients prefer operating expense models that avoid fleet ownership, while software subscriptions for routing, UTM integration, and predictive maintenance layer incremental margin. Hardware retains the 53.21% 2024 revenue lead, yet its share slips each quarter as contract logistics overtakes box sales. The services boom also accelerates financing innovations—usage-based leases and per-flight insurance—that de-risk adoption for hospitals and retailers.

By Drone Type: Hybrid VTOL Leads Innovation

Hybrid VTOL units posted a 45.22% CAGR, reflecting demand for fixed-wing range plus vertical agility in the drone package delivery market. Multi-rotors continue to dominate volume with a 66.76% 2024 share because they are inexpensive, easy to service, and ideal for 5-mile (8.04 km) milk runs.

Sikorsky's rotor-blown-wing flight, hitting 86 knots, validated that hybrids can handle 10-mile (16 km) suburb-to-city hops without runways. Fixed-wing platforms remain popular for medical air-bridge routes over sparsely populated terrain, yet lack VTOL capabilities for curbside drops. Investor capital now flows to modular airframes capable of swapping lift-plus-cruise components, hinting the category gap will narrow by decade's end.

By Range: Long-Range Operations Unlock Scalability

Long-range missions outpaced all with a 40.01% CAGR as BVLOS approvals multiplied, though short-range flights still held 55.89% of 2024 revenue in the drone package delivery market. Short hops dominate early deployments because pads cluster at store rooftops, but economics favor expanding radius: a 10-mile (16 km) service zone covers thirty-six times more households than a 2-mile (3.2 km) ring.

Hybrid-propulsion and mid-air recharging concepts aim to push effective radii beyond 50 miles (80.46 km), enabling city-to-exurb coverage without extra vans. Long-range corridors underpin medical drone bridges, allowing cold-chain vaccines to leapfrog broken roads. As operators layer mid-range spokes onto these hubs, network effects reinforce regional dominance.

By Package Size: Lightweight Dominance Persists

Parcels under 2 kg formed 46.22% of 2024 revenue, matching e-commerce item weight distributions, yet packages above 5 kg posted the fastest 38.85% CAGR in the drone package delivery market. Battery upgrades and lightweight composites let aircraft handle bulkier boxes without halving range.

The 2 to 5 kg band is where aerial and ground couriers duel on cost, prompting algorithmic consolidation of multi-stop routes to lift aerial load factors. Heavy-parcel adoption accelerates in business-to-business (B2B) supply chains—ship-to-shore spares, mining samples—where immediacy trumps cost. Operators bet that once heavier categories normalize, cross-subsidies from high-margin medical or industrial drops will defend blended profitability.

By End Use: Medical Delivery Leads Growth

Medical aid deliveries clocked 43.56% CAGR, the fastest of any application, while food held 36.87% of 2024 revenue inside the drone package delivery market. Life-critical use cases enjoy looser cost constraints, and cold-chain performance extends to biologics needing –10°C shipping profiles.

Food remains the volume anchor because quick-service restaurants exploit drones for lunch-hour peaks. Retail parcels add density outside mealtimes, lifting aircraft utilization. Industrial requisitions—tools and spare parts—rise as payload ceilings climb, offering high ASP but sporadic volume. Collectively, the mix diversification cushions operators from seasonality.

Geography Analysis

North America commanded 33.15% of 2024 revenue, leveraging clear FAA pathways and wallet-share from Amazon, Walmart, and healthcare networks. BVLOS corridors in Texas and Arizona furnish commercial proof points, though community pushback over noise in College Station shows social license remains fragile. Canada’s Transport Canada is refining RPAS Category 4 rules, while Mexico’s civil aviation agency has begun limited waivers around Monterrey, hinting at continent-wide convergence. Venture capital, 5G coverage, and warehouse robotics ecosystems reinforce the region’s technology edge, sustaining double-digit growth despite its maturity.

Asia-Pacific delivered the highest 41.20% CAGR and is forecast to become the most significant regional contributor to the drone package delivery market by 2030. China’s low-altitude economy aims for a CNY 1.5 trillion (USD 207 billion) value by 2025, with commercial drone revenue exceeding CNY 117 billion (USD 16.34 billion) in 2023 and projected to top CNY 400 billion (USD 55.87 billion) by 2025. Deliveries rose 80% between 2021 and 2022 to 875,000 drops as regulators opened city-level air lanes. India green-lit BVLOS trials for ShopX, while Japan approved 10 last-mile pilots, illustrating a regional policy thaw.[2] Urban Air Mobility, “Japan Approves 10 Pilot Projects,” URBANAIRMOBILITYNEWS.COM Dense megacities lacking curb space provide ideal vertiport demand, and electronics supply chains cut airframe BOM costs, further spurring uptake.

Europe balances innovation with stringent safety and privacy norms. EASA’s unified framework lets a certified operator fly in 27 member states without additional filings, encouraging cross-border routes. Germany, France, and the UK test sustainable delivery corridors to meet net-zero freight targets. Nordic health authorities already rely on drones to bridge archipelagos, highlighting how diverse geography fits. Sustainability subsidies, such as Germany’s Urban-Air-Mobility (UAM) fund, offset high labor expenses that would otherwise tilt economics toward road couriers.

The Middle East and Africa leverage drones to leapfrog weak road grids. Rwanda’s national blood network remains the marquee case; Ghana and Kenya replicate the template, while Gulf Cooperation Council states pilot rooftop pads on new smart-city builds. South America’s mountainous terrain similarly motivates drone corridors; regulators in Brazil and Chile consult FAA and EASA rulebooks to avoid reinvention, implying smoother market entry for Western certificate holders.

Competitive Landscape

The drone package delivery market remains fragmented because regulatory fragmentation and ground infrastructure costs deter rapid international scaling. Wing Aviation LLC and Zipline International Inc. form a top tier yet together hold well under 25% combined global revenue, leaving niches for regional specialists. Wing Aviation LLC monetizes through white-label delivery for retailers; Zipline International Inc. doubles down on healthcare and is expanding into restaurant chains.

Start-ups such as A2Z Drone Delivery and Elroy Air innovate around infrastructure and payload capacity, aiming to license technology or run dedicated cargo lanes. Hardware OEMs, including DJI and Skydio, increasingly supply off-the-shelf platforms to service integrators, commoditizing the lower end of the stack. Competitive advantage now concentrates in regulatory affairs teams, community-relations playbooks, and AI route optimizers that raise sortie yield.

Strategic tie-ups accelerate share capture: Walmart is committed to covering up to 75% of Dallas-Fort Worth households via Wing Aviation LLC and Zipline International Inc., while healthcare systems integrate Zipline International Inc. APIs into hospital inventory software, locking in volumes.[3]Wing Communications, “Wing and Walmart Announce World’s Largest Drone Delivery Expansion,” WING.COM Continuous fundraising arms leaders with capital to pre-build vertiports and charging pads, creating physical network effects that late entrants struggle to match.

Drone Package Delivery Industry Leaders

Wing Aviation LLC

Zipline International Inc.

Matternet, Inc.

Manna Drone Delivery

United Parcel Service, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Wing and Walmart unveiled a 100-store drone delivery expansion across five US metro areas, aiming for sub-19-minute average drops.

- June 2025: DoorDash and Flytrex initiated drone delivery services in the Dallas-Fort Worth metropolitan area, providing deliveries from multiple local and national restaurant chains.

- April 2025: Zipline introduced its Platform 2 (P2) drones for retail and healthcare product deliveries. The drones carry up to 8 pounds within a 10-mile radius and utilize a tethered "Zip" carrier to complete deliveries in 30 minutes. The drone can operate in the rain and winds up to 45 mph.

Global Drone Package Delivery Market Report Scope

| Hardware |

| Software |

| Services |

| Multi-Rotor |

| Fixed-Wing |

| Hybrid VTOL |

| Short Range |

| Medium Range |

| Long Range |

| Less than 2 kg |

| 2 to 5 kg |

| More than 5 kg |

| Food Delivery |

| Retail Goods Delivery |

| Postal Delivery |

| Medical Aid Delivery |

| Precision Agriculture Delivery |

| Industrial Delivery |

| Maritime Delivery |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Solution | Hardware | ||

| Software | |||

| Services | |||

| By Drone Type | Multi-Rotor | ||

| Fixed-Wing | |||

| Hybrid VTOL | |||

| By Range | Short Range | ||

| Medium Range | |||

| Long Range | |||

| By Package Size | Less than 2 kg | ||

| 2 to 5 kg | |||

| More than 5 kg | |||

| By End Use | Food Delivery | ||

| Retail Goods Delivery | |||

| Postal Delivery | |||

| Medical Aid Delivery | |||

| Precision Agriculture Delivery | |||

| Industrial Delivery | |||

| Maritime Delivery | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current market size of the drone package delivery market?

The drone package delivery market size stands at USD 0.97 billion in 2025 and is projected to reach USD 4.78 billion by 2030, advancing at a 37.57% CAGR.

Which region is growing fastest in commercial drone delivery?

Asia-Pacific is expanding at a 41.20% CAGR, propelled by China’s low-altitude economy policies and dense megacities that favor aerial logistics.

Why are medical deliveries leading growth in drone applications?

Medical drops grow fastest because drones cut delivery times from nearly an hour to minutes, maintain cold-chain temperatures, and reach remote clinics without roads.

What technical hurdle limits heavier drone payloads?

Energy density of lithium-ion (Li-ion) batteries caps economical payloads under 5 lb; next-gen lithium-sulfur (Li-S) cells must mature before bulk freight becomes widespread.

How do regulatory trends influence market expansion?

BVLOS approvals in the US, EU, and China standardize long-range operations, letting operators scale from test flights to citywide networks without visual observers.

Which companies currently lead the competitive landscape?

Wing Aviation LLC, and Zipline International Inc. form the leading duo, each with distinct strategies: retail integration, white-label partnerships, and healthcare specialization respectively.

Page last updated on: