Passenger Drones Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

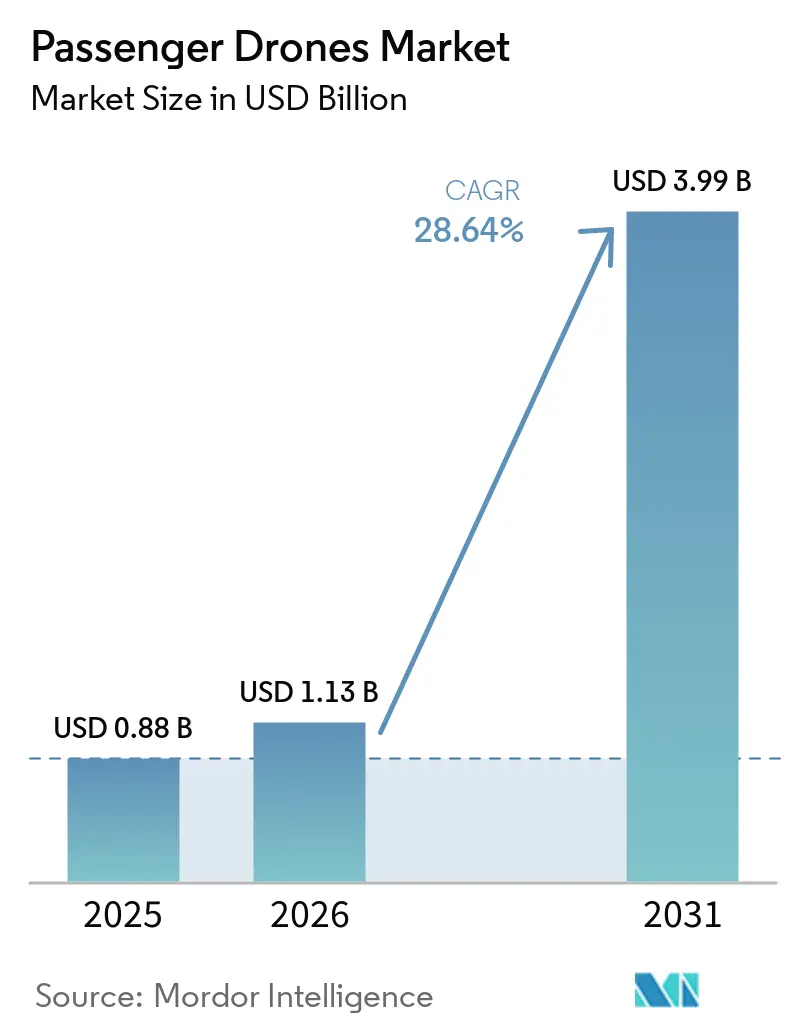

| Market Size (2026) | USD 1.13 Billion |

| Market Size (2031) | USD 3.99 Billion |

| Growth Rate (2026 - 2031) | 28.64% CAGR |

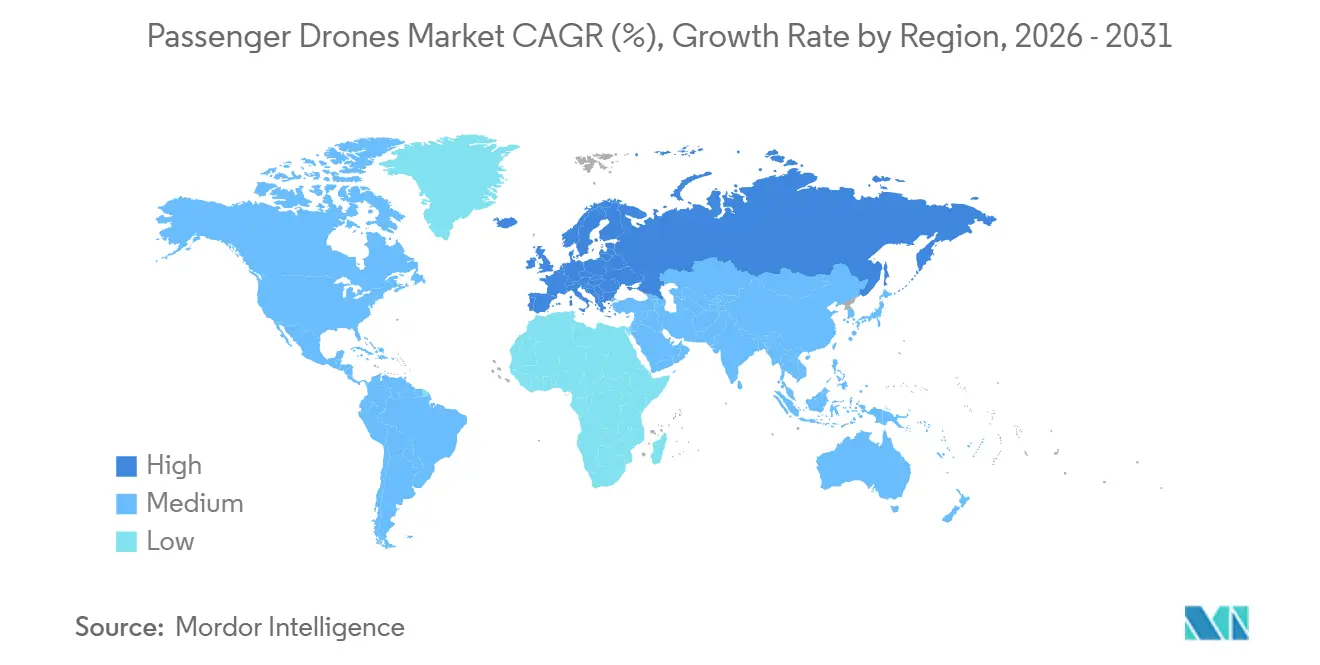

| Fastest Growing Market | Europe |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Passenger Drones Market Analysis by Mordor Intelligence

The passenger drones market size is projected to expand from USD 0.88 billion in 2025 and USD 1.13 billion in 2026 to USD 3.99 billion by 2031, registering a CAGR of 28.64% during the forecast period. Commercial activity has entered a new stage in 2026, as ticketed passenger drone services are now operating in more than 1 city simultaneously, marking a clear break from the earlier phase of test flights and demonstration programs. The market is being lifted by faster commercialization of full-electric aircraft for short urban routes, clearer certification pathways from major aviation authorities, and vertiport projects that are turning planned corridors into physical transport assets. Competition is still broad, but the field is narrowing as only a smaller group of manufacturers can carry the cost, certification work, and infrastructure coordination needed for commercial scale. Battery mass and uneven certification timelines across the FAA, EASA, CAAC, and JCAB still limit route range, payload flexibility, and cross-border rollout. Even with those constraints, the passenger drones market has moved beyond concept validation and entered a period defined by operating services, certification races, and infrastructure buildout.

Key Report Takeaways

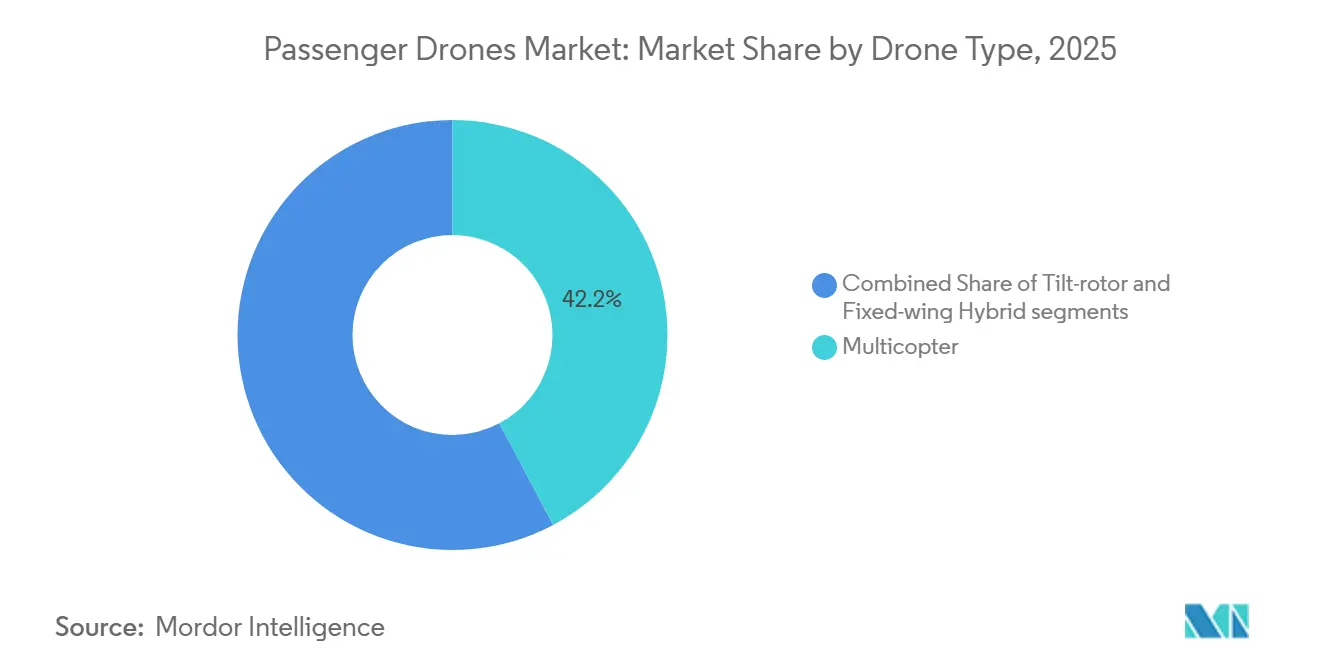

- By drone type, multicopters held 42.24% share in 2025, while tilt-rotors are projected to expand at a 30.12% CAGR through 2031.

- By seating capacity, more than 4-seater platforms accounted for 49.23% of the passenger drones market size in 2025, while the 2 to 4-seater segment is forecast to grow at a 31.16% CAGR through 2031.

- By mode of operation, piloted aircraft held 66.47% share of the market in 2025 and is also forecast to witness the highest CAGR at 29.71% through 2031.

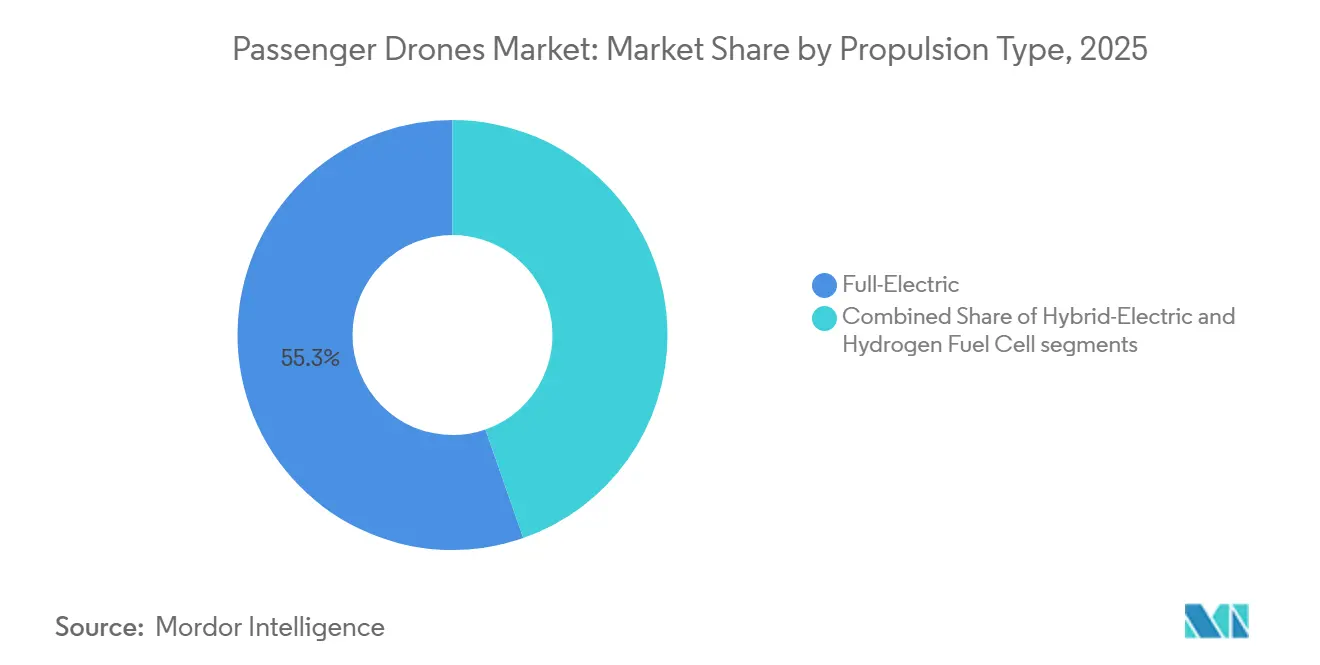

- By propulsion type, full-electric platforms led with a 55.34% share in 2025, while hydrogen fuel-cell propulsion is foto advance at a 31.47% CAGR through 2031.

- By application, urban air taxis accounted for 53.33% of the passenger drones market in 2025 and are projected to expand at a 30.06% CAGR through 2031.

- By geography, North America held 38.77% share in 2025, while Europe is forecast to grow at the fastest CAGR of 29.91% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Passenger Drones Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Advances in battery energy density and cost reductions | +5.7% | Global, with early gains in China, US, and Germany | Short term (≤ 2 years) |

| Urban traffic congestion catalyzing demand for UAM | +4.1% | Global, concentrated in North America, Europe, and APAC megacities | Medium term (2-4 years) |

| Supportive regulatory sandboxes and pilot programs | +3.4% | North America and EU primary, spillover to UAE, Japan, South Korea | Medium term (2-4 years) |

| Defense-derived autonomous flight-control breakthroughs | +2.9% | North America and Europe, with technology transfer to APAC | Long term (≥ 4 years) |

| Real-estate-backed vertiport ecosystems | +2.8% | UAE, US, South Korea, Japan | Medium term (2-4 years) |

| Corporate environmental, social, and governance -driven demand for zero-emission executive mobility | +2.2% | Global corporate hubs, North America, Europe, Gulf States | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Urban Traffic Congestion Catalyzing Demand for Urban Air Mobility

Urban congestion is creating a stronger economic case for short-range air mobility in large cities, helping the passenger drones market move closer to regular commercial use. Route planning is no longer shaped solely by aircraft developers, as airport authorities, transit agencies, and property developers are now influencing where passenger pickup, landing, and charging assets will be located. The strongest near-term signal is that infrastructure is being built before fleets reach broad scale, which reduces the gap between certification and service launch in the passenger drones market. Dubai's Roads and Transport Authority and Skyports Infrastructure announced the technical completion of the world's first commercial vertiport at Dubai International Airport in April 2026, which is tied to a 4-node network that includes Dubai Marina, Dubai Mall, and Palm Jumeirah.[1]Skyports Infrastructure, “Air Taxi Ready, World's First Commercial Vertiport by Dubai International Airport Reaches Technical Completion,” Skyports Infrastructure Press Release, skyports.net Cities that move first on these networks are building operating advantages that will be difficult for slower markets to match once traffic rights, real estate access, and partner ecosystems are already in place.

Advances in Battery Energy Density and Cost Reductions

Battery improvement remains the most important technical lever for the passenger drones market because route economics, payload, turnaround time, and aircraft configuration all depend on it. Better energy density also makes full-electric platforms more practical for urban service because it extends useful range without requiring a shift away from zero-emission drivetrains. EHang stated that it completed the world's first eVTOL solid-state battery flight test in November 2024, using an EH216-S aircraft with an energy density of 480 Wh/kg. That result matters because higher-density battery systems can widen the commercial window for short urban routes and can also strengthen the position of manufacturers already close to certification. The passenger drones market is likely to feel this driver first in geographies where battery supply chains, aircraft manufacturing, and certification activity are already moving in parallel.

Supportive Regulatory Sandboxes and Pilot Programs

The passenger drones market is benefiting from a shift in regulatory posture, as authorities are moving from high-level guidance to operating frameworks that support early service deployment. EASA issued ED Decision 2025/010/R and related guidance in 2025, providing the European market with a more comprehensive rulebook for manned VTOL-capable aircraft.[2]European Union Aviation Safety Agency, “ED Decision 2025/010/R, Introduction of a Regulatory Framework for the Operation of Drones, Enabling Innovative Air Mobility With Manned VTOL-Capable Aircraft,” EASA Document Library, easa.europa.eu In March 2026, Joby announced it had been selected to begin operations under the White House eVTOL Integration Pilot Program, which supports pre-certification activities across multiple states, enabling operators to build operating experience, gather safety data, and prepare for demand in parallel with the final certification steps. The market gains momentum as regulatory programs shorten the time between aircraft readiness and first commercial revenue.

Real-Estate-Backed Vertiport Ecosystems

Vertiport development has become one of the most important non-aircraft variables in the passenger drones market because service cannot scale without reliable access to takeoff, landing, charging, and passenger processing sites. The funding base for these assets is expanding beyond aviation, as airports, urban transport agencies, and property developers are now treating vertiports as part of broader mobility and land-use plans. Korea Airports Corporation and the Korea Aerospace Research Institute broke ground in March 2026 on Seoul metropolitan area's first urban UAM vertiport at KINTEX in Goyang under the K-UAM Phase 2 Demonstration program.[3]Korea Airports Corporation via Seoul Economic Daily, “Seoul Metro Area's First UAM Vertiport Breaks Ground This Month,” Seoul Economic Daily, en.sedaily.com Skyports also confirmed in April 2026 that Dubai International Airport's commercial vertiport had reached technical completion, indicating that infrastructure is progressing across more than 1 early-adopter geography simultaneously. As these projects move forward, the passenger drones market becomes easier for operators and investors to evaluate because route plans are tied to visible assets rather than future concepts.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Certification and safety-standard uncertainties | -3.6% | Global, most acute in North America and Europe where CAA standards are most stringent | Long term (≥ 4 years) |

| Payload-range trade-offs driven by battery mass | -2.0% | Global, most constraining for Inter-City Shuttle and More than 4 Seater segments | Medium term (2-4 years) |

| Cold-weather battery performance degradation | -1.3% | North America, Russia, Northern Europe | Medium term (2-4 years) |

| Social-media driven reputational risk on incidents | -1.1% | Global, amplified in high-connectivity North American and European markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Certification and Safety-Standard Uncertainties

Certification remains the heaviest structural brake on the passenger drones market because aircraft developers still face different technical pathways across major jurisdictions. A manufacturer that advances in 1 regulatory system cannot assume a smooth or rapid transfer into another, which raises costs and delays market entry. EASA's 2025 operating framework was an important step for Europe, but the coexistence of separate FAA, EASA, CAAC, and JCAB approaches still keeps compliance burdens high for global programs. The result is that manufacturers often move through sequential approval queues rather than launching across multiple major markets simultaneously. That slows fleet deployment, strains capital needs, and keeps the passenger drones market dependent on a smaller group of companies that can carry long certification cycles.

Cold-Weather Battery Performance Degradation

Cold weather reduces battery performance, limiting year-round route reliability in parts of North America and Northern Europe, creating an issue for the passenger drones market because aircraft performance depends heavily on battery output, thermal management, and charging behavior. Cold-climate operations also require extra infrastructure at vertiports for battery conditioning, which adds cost and operational complexity. That means early commercial networks are more likely to cluster in warm or moderate climates, even when congestion is severe in colder cities. The practical effect is that the passenger drone market may expand first in areas with easier battery conditions, not always in areas with the strongest urban demand.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drone Type: Multicopters Lead but Tilt-Rotors Are Accelerating

Multicopters held 42.24% of the passenger drones market share in 2025, and that lead reflected a simpler mechanical layout, shorter validation cycles, and lower training complexity for early commercial operations. Their configuration is better aligned with short urban routes, where stable takeoff and landing behavior matter more than long cruise efficiency. That has given multicopters a practical certification advantage in the near term because regulators are closely examining powered-lift failure points and operational safety. EHang's EH216-S supports this pattern because it is a multicopter design and became the first eVTOL platform to secure commercial type certification and production certification from the CAAC.

Tilt-rotors are the fastest-growing drone type in the passenger drones market, with a projected CAGR of 30.12% over 2026 to 2031. Their advantage lies in better cruise efficiency at higher speeds, making them more suitable for corridor routes that extend beyond short urban hops. Joby advanced into FAA-conforming TIA flight testing in 2026, which keeps tilt-rotor architectures central to the Western certification race. Archer is also pushing the same configuration through commercial launch preparation, which shows that large parts of the passenger drone industry still see tilt-rotors as the design best suited to longer, denser route networks. Fixed-wing hybrid aircraft remain the smallest sub-segment because their use case is narrower and better fits inter-city and specialized transport missions than early urban deployment.

By Seating Capacity: Large Configurations Dominate, Mid-Range Growing Fastest

More than 4-seater aircraft accounted for 49.23% of the passenger drone market in 2025, indicating that operators and manufacturers are still targeting formats where seat economics improve with higher occupancy. This segment fits urban air taxi, inter-city shuttle, VIP movement, and emergency support use cases better than smaller personal mobility concepts. Larger cabin layouts also appeal to corporate users because they can move delegations rather than single travelers. EHang's VT35, unveiled in October 2025 with a target range of 200 km and compatibility with existing EH216-S vertiport infrastructure, reinforces the push toward higher-capacity mobility programs.

The 2- to 4-seater segment is the fastest-growing part of the passenger drones market, with a 31.16% CAGR through 2031. This format sits in a practical middle ground because it can serve constrained urban vertiports while still generating enough revenue per flight to support commercial operations. Archer's Midnight is built around this logic, with a pilot-plus-four-passenger layout and a route profile designed for dense airport-to-city links. Smaller personal aircraft remain the least developed commercial segment, even though new regulatory pathways in the US may make light two-occupant powered-lift formats easier to enter over time. Across seating classes, the passenger drone industry is balancing per-flight economics with infrastructure constraints, route length, and certification timing rather than simply chasing maximum passenger count.

By Mode of Operation: Piloted Operations Define Near-Term Commercialization

Piloted aircraft accounted for 66.47% of the passenger drones market in 2025 and also carry the highest projected CAGR of 29.71% through 2031. That unusual combination reflects a basic regulatory reality because commercial passenger service still depends on a pilot in command in most major approval pathways. Joby's participation in the White House eIPP program in 2026 also shows that early US operations are being structured around piloted service rather than fully autonomous deployment. In practical terms, the passenger drones market is moving first through the operating model that regulators, insurers, and public authorities are most willing to accept.

Semi-autonomous systems sit between today's operating norms and the longer-term autonomy target, with remote oversight and onboard automation sharing flight tasks. This architecture offers a realistic transition path by allowing manufacturers to build automation capability without requiring regulators to accept a full jump to pilotless passenger service. China is the clear exception in the passenger drones market because EHang has already launched paid, autonomous passenger operations in Guangzhou and Hefei without an onboard pilot. Fully autonomous service in North America and Europe is likely to take longer, as regulators still require more safety data and equivalence testing before broad commercial approval. The mode-of-operation split shows that commercial timing is determined more by certification readiness than by aircraft developers' technical ambition.

By Propulsion Type: Full-Electric Leads, Hydrogen Fuel Cell Accelerating

Full-electric propulsion held a 55.34% share in 2025, and that leadership stems from a simpler drivetrain architecture, better supply chain readiness, and a closer fit with short urban route profiles. The aircraft furthest along in certification or commercialization, including EHang's EH216-S, Joby's S4, and Archer's Midnight, are all tied to full-electric systems. That means every regulatory step reached by those leading programs also strengthens the near-term position of electric propulsion in the passenger drones market. Full-electric aircraft also align well with the zero-emission policy direction and with the infrastructure now being planned around urban charging and vertiport turnaround.

Hydrogen fuel cell propulsion is the fastest-growing propulsion segment at a 31.47% CAGR from 2026 to 2031. Its appeal comes from the promise of longer range with zero direct emissions, which is especially relevant as the passenger drones market moves farther into corridor and inter-city missions. ZeroAvia announced a manufacturing hub in Scotland in May 2025 to scale hydrogen-electric propulsion systems, and the FAA had already published special conditions for its 600 kW electric engine.[4]ZeroAvia, “ZeroAvia to Build Manufacturing Hub in Scotland,” ZeroAvia, zeroavia.com That combination suggests that hydrogen development is shifting from lab-stage ambition toward industrial preparation, even if route deployment will still depend on infrastructure buildout. Hybrid-electric systems remain an important bridge option because they can support longer missions before hydrogen support networks become widely available.

By Application: Urban Air Taxi Anchors the Market, Consolidating Its Dominance

Urban air taxis accounted for 53.33% of the market in 2025 and are also projected to post the fastest application CAGR of 30.06% through 2031. This lead comes from a strong fit between current battery limits and route lengths of 15 km to 50 km, where air travel can save meaningful time against road alternatives. Urban corridors also offer clearer pricing potential because high-income, congestion-heavy routes can support premium fares more easily than longer or less dense networks. Joby's 2026 activity shows how one platform can be positioned across several city markets at once through Dubai, the White House eIPP states, and New York-linked operations supported by acquired infrastructure.

Inter-city shuttle remains the application with the highest revenue potential per trip. Still, it also faces the longest path to broad commercialization because it needs a wider range and a fuller network at both ends of the route. Air tourism has emerged as a useful early revenue path in some markets because route risk is lower and consumer demand can be concentrated in controlled locations. EHang's sightseeing operations in China and expansion activities in Japan, Qatar, and Thailand show how this path can support commercial learning before broader city mobility is fully mature. Emergency medical services are also gaining attention because adapted regulatory pathways and dedicated use cases may open before mass urban networks reach full scale. Across applications, the market is focusing on use cases that best align with today's technology and regulatory readiness, rather than trying to commercialize every mission profile at once.

Geography Analysis

North America held 38.77% of the market share in 2025, reflecting the region's deep private capital base, active certification work, and broad infrastructure foundation. The US remains the center of that position because the FAA's commercial framework and the country's capital ecosystem continue to attract the leading Western programs. Joby's selection under the White House eIPP in March 2026 turned early US commercialization from a future objective into an active operating pathway across as many as 10 states. That shift matters because the passenger drones market in North America now has clearer links between federal support, aircraft readiness, and route-level deployment planning.

Europe is the fastest-growing regional segment, with a projected CAGR of 29.91% over 2026 to 2031. EASA's 2025 decisions under the new VTOL regulatory framework provided Europe with a more comprehensive operating framework and helped reduce uncertainty for developers and operators. The UK is also relevant because Vertical Aerospace is progressing on a track that can support later cross-border fleet movement once approvals are in place.

Asia-Pacific hosts the most commercially advanced operations in the passenger drones market, as China is already operating ticketed autonomous passenger services in 2026. EHang launched EH216-S commercial services in Guangzhou and Hefei in March 2026, making China the first market to have revenue-generating autonomous passenger drone operations at this scale. Japan is also moving forward, and SkyDrive became the country's first eVTOL developer to receive Approved Design Organization certification from JCAB in April 2026. South Korea added another infrastructure signal when the first Seoul metro UAM vertiport, KINTEX, broke ground in March 2026 under the national demonstration program. The Middle East is developing rapidly, with Dubai's completed vertiport and the UAE's pathway for Archer's Midnight under a Restricted Type Certificate approach. South America remains small, but Brazil's dense urban structure and familiarity with helicopter mobility keep it relevant as a future adoption market once bilateral recognition and the availability of certified aircraft improve.

Competitive Landscape

The passenger drones market remains fragmented because more than a dozen OEM programs are still active across multicopter, tilt-rotor, and hybrid designs, and no single company controls more than a low-teens share of global active aircraft sales. Even so, the certification process is steadily separating companies with real commercial paths from those still operating at the concept or limited test stage. EHang is the clearest example of that shift because it delivered 221 eVTOL units in FY2025 and posted its first GAAP-profitable quarter in Q4 2025. The company also launched ticketed services in Guangzhou and Hefei in March 2026, which gave it a commercial position that no Western peer has yet matched.

In Western markets, Joby and Archer remain among the most visible contenders because both are combining certification work with route-level commercial planning. Joby completed FAA Stage 4 and entered TIA flight testing with its first FAA-conforming aircraft, which keeps it at the front of the US certification race. Archer achieved full FAA Means of Compliance acceptance and is also using the UAE as an earlier commercial entry path through its Restricted Type Certificate strategy with Abu Dhabi Aviation. These moves show that companies are no longer waiting for a single all-or-nothing certification event and are instead building revenue options in jurisdictions that can move faster.

Strategic differentiation in the passenger drones market is now centered on access to battery supply, vertiport partnerships, and control over autonomy software. EHang's model is notable because it ties aircraft development, battery development with partners, and operator relationships into a more tightly integrated structure. Joby is taking a different route by linking aircraft progress with airspace integration capability and strong liquidity, supported by a USD 2.5 billion cash position in Q1 2026. Another opening remains in emergency medical services and intercity shuttle operations, where no manufacturer has yet secured a commercial-scale contract. Companies that engage earlier with these narrower but practical use cases may find a clearer path to differentiated deployment than those focused only on the most crowded urban taxi corridors. The competitive picture is still open, but the advantage is shifting toward firms that can manage certification, infrastructure, and financing as one coordinated program rather than as separate workstreams.

Passenger Drones Industry Leaders

Joby Aero, Inc.

Volocopter GmbH

Guangzhou EHang Intelligent Technology Co. Ltd.

Archer Aviation Inc.

Airbus SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: UAE General Civil Aviation Authority (GCAA) and Archer Aviation agreed to transition Midnight into a Restricted Type Certificate (RTC) program, providing an established pathway for early commercial air taxi operations in Abu Dhabi with Abu Dhabi Aviation as the launch operator, advancing Archer's revenue-generating service ahead of full FAA type certification.

- April 2026: Dubai's Roads and Transport Authority and Skyports Infrastructure announced the technical completion of the world's first commercial vertiport at Dubai International Airport, a 3,100-square-meter facility featuring two take-off and landing pads that form the central hub of a four-node network extending to Dubai Marina, Dubai Mall, and Palm Jumeirah.

- April 2026: SkyDrive became Japan's first dedicated eVTOL developer to receive Approved Design Organization (ADO) certification from JCAB, enabling the company to perform in-house design and post-design inspections and materially accelerating its type certification process toward a 2028 commercial service target.

- March 2026: Joby Aviation completed its SR3 audit with the FAA. It commenced TIA flight testing using its first FAA-conforming aircraft, a key milestone on the path to type certification, while simultaneously being selected as a partner in the White House eIPP program, enabling pre-certification operations in up to 10 states.

Global Passenger Drones Market Report Scope

Passenger drones are unmanned aerial vehicles designed to transport people. These drones are equipped with advanced technologies to ensure safety, efficiency, and convenience in urban and inter-city transportation.

The passenger drones market is segmented by drone type, seating capacity, mode of operation, propulsion type, application, and geography. By drone type, the market is segmented into multicopter, tilt-rotor, and fixed-wing hybrid. By seating capacity, the market is categorized into single-seater, 2 to 4-seater, and more than 4-seater. By mode of operation, the market is divided into piloted, semi-autonomous, and fully autonomous. By propulsion type, the market is segmented into full-electric, hybrid-electric, and hydrogen fuel cell. By application, the market is classified into urban air taxi, intercity shuttle, air tourism, emergency medical services, and VIP transport. The report also covers the market sizes and forecasts for the passenger drones market in major countries across different regions. For each segment, the market size is provided in terms of value (USD).

| Multicopter |

| Tilt-rotor |

| Fixed-wing Hybrid |

| Single Seater |

| 2 to 4 Seater |

| More than 4 Seater |

| Piloted |

| Semi-Autonomous |

| Fully Autonomous |

| Full-Electric |

| Hybrid-Electric |

| Hydrogen Fuel Cell |

| Urban Air Taxi |

| Inter-City Shuttle |

| Air Tourism |

| Emergency Medical Services |

| VIP Transport |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Drone Type | Multicopter | ||

| Tilt-rotor | |||

| Fixed-wing Hybrid | |||

| By Seating Capacity | Single Seater | ||

| 2 to 4 Seater | |||

| More than 4 Seater | |||

| By Mode of Operation | Piloted | ||

| Semi-Autonomous | |||

| Fully Autonomous | |||

| By Propulsion Type | Full-Electric | ||

| Hybrid-Electric | |||

| Hydrogen Fuel Cell | |||

| By Application | Urban Air Taxi | ||

| Inter-City Shuttle | |||

| Air Tourism | |||

| Emergency Medical Services | |||

| VIP Transport | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is driving growth in passenger drone adoption through 2031?

Growth is being supported by commercial service launches in 2026, clearer certification pathways, better battery performance, and real vertiport construction that is turning route plans into operating assets.

How large could the passenger drones space become by 2031?

The passenger drones market size is projected to reach USD 3.99 billion by 2031 from USD 1.13 billion in 2026, with a CAGR of 28.64% over 2026 to 2031.

Which aircraft type is leading current demand?

Multicopters led with 42.24% share in 2025 because they are mechanically simpler and better suited to early urban deployment and certification needs.

Which use case is most important for commercial rollout?

Urban air taxi is the main use case, with 53.33% share in 2025 and the fastest projected application CAGR of 30.06% through 2031.

Which region is ahead in commercial readiness?

North America led with 38.77% share in 2025, but China in Asia-Pacific has the most advanced live commercial operations because EHang launched ticketed autonomous services in 2026.

Why is certification still the main challenge for manufacturers?

Different approval systems across the FAA, EASA, CAAC, and JCAB force companies to manage separate pathways, which raises cost, slows entry, and narrows the field of viable contenders.

Page last updated on: