Construction Drones Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

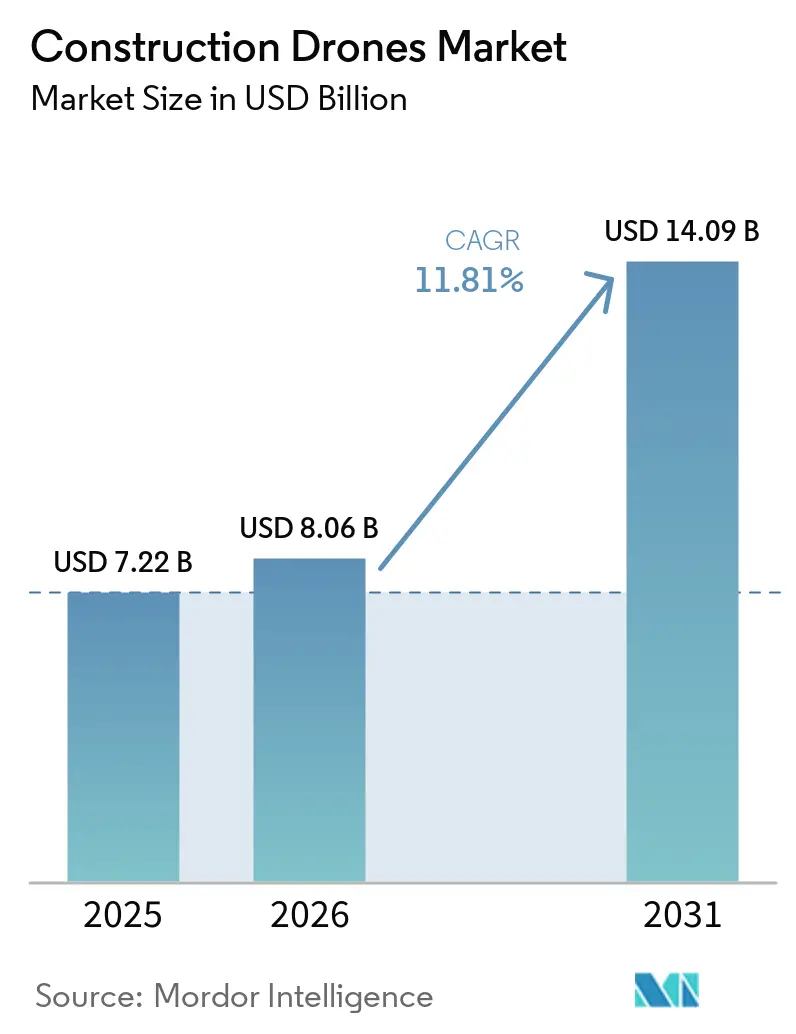

| Market Size (2026) | USD 8.06 Billion |

| Market Size (2031) | USD 14.09 Billion |

| Growth Rate (2026 - 2031) | 11.81% CAGR |

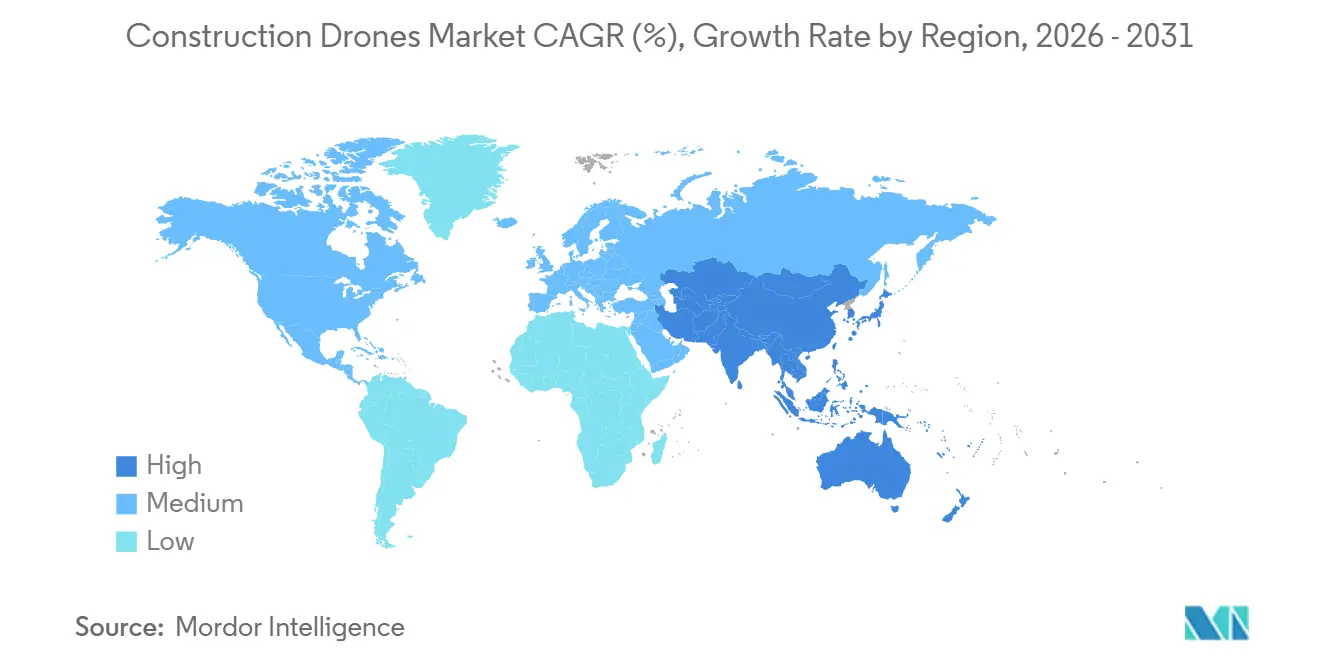

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Construction Drones Market Analysis by Mordor Intelligence

The construction drones market size was valued at USD 7.22 billion in 2025, and is projected to grow from USD 8.06 billion in 2026 to USD 14.09 billion by 2031, growing at a CAGR of 11.81% from 2026 to 2031. The need is pushing the construction drones market for faster site visibility, tighter schedule control, and steady digital adoption across project delivery workflows. Contractors are using drone fleets less as stand-alone hardware and more as a recurring field-data layer that supports project monitoring, documentation, and coordination with digital design systems. The construction drones market is also benefiting from labor shortages, which are making autonomous and semi-autonomous monitoring tools more attractive for routine inspection and progress capture. At the same time, the construction drones market is becoming more segmented by security and compliance requirements, especially in the US, where procurement choices are increasingly shaped by cybersecurity and supply chain rules. Competitive positioning is shifting toward software, autonomy, and managed operations, creating space for both platform leaders and specialized vendors as the construction drones market matures.

Key Report Takeaways

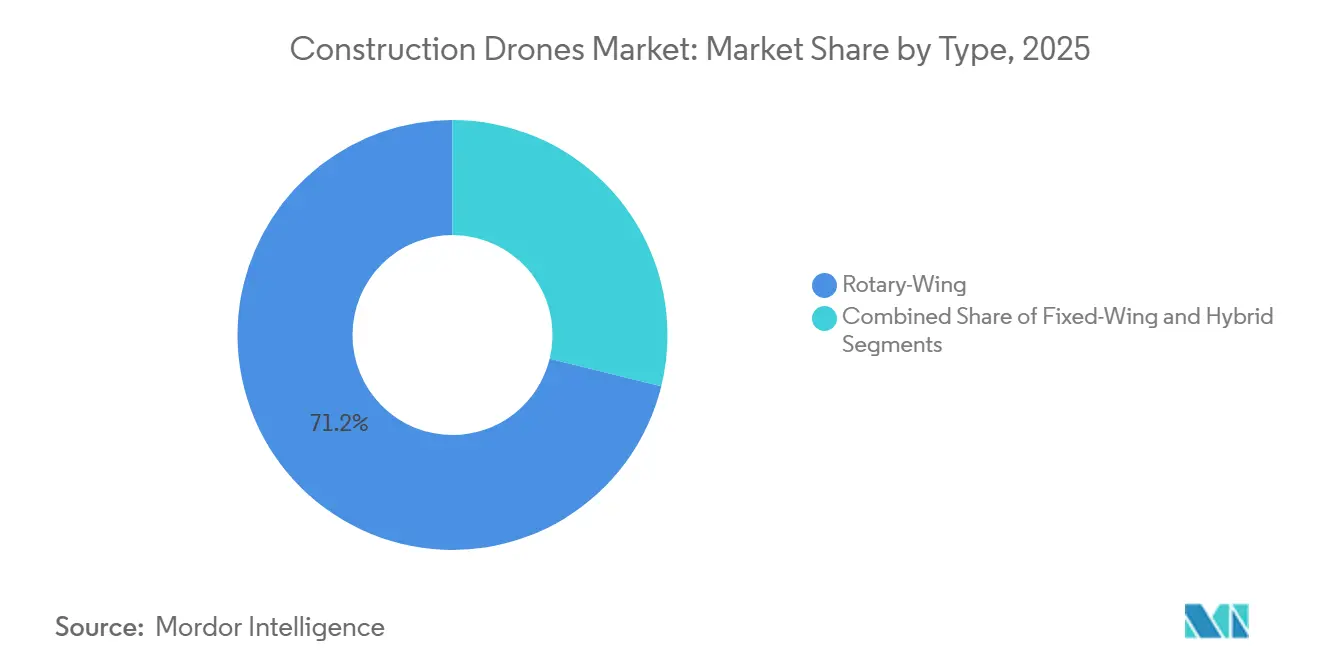

- By type, rotary-wing platforms led with 71.17% revenue share in 2025, while hybrid VTOL platforms are projected to expand at a 13.43% CAGR through 2031.

- By component, hardware accounted for 57.64% of revenue in 2025, while software is forecast to grow at a 12.77% CAGR through 2031.

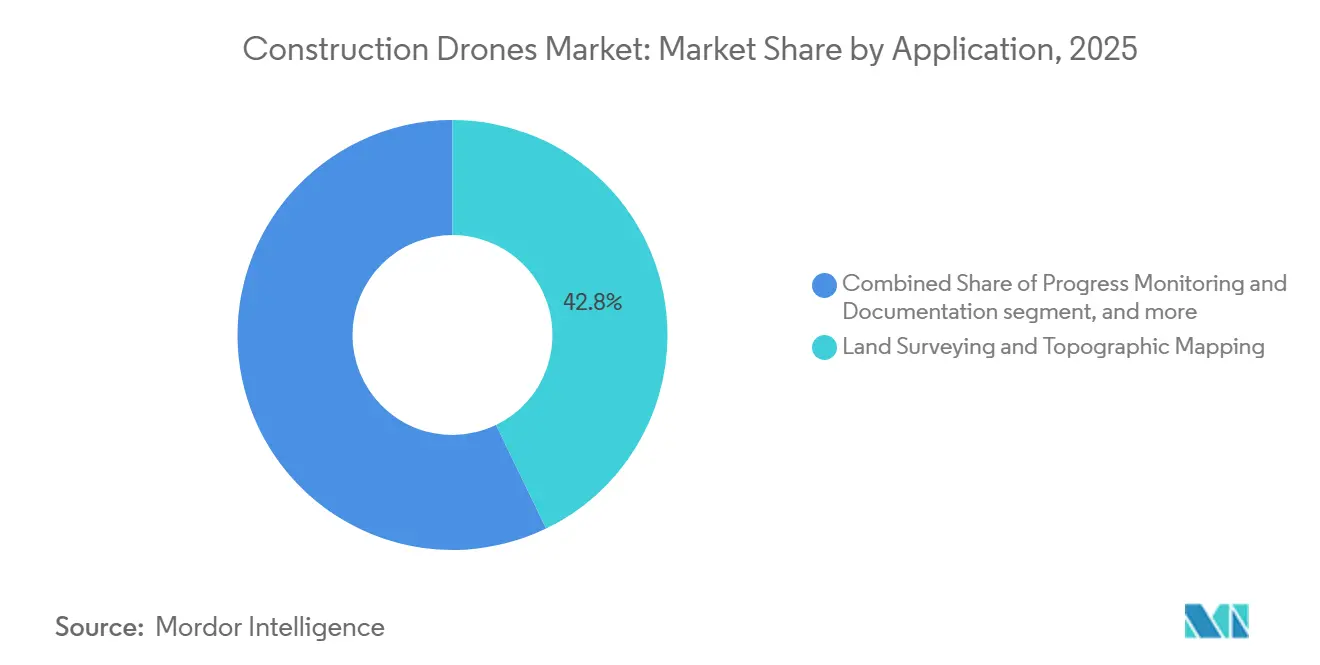

- By application, land surveying and topographic mapping accounted for 42.83% share of the construction drones market size in 2025, while security and surveillance are forecast to grow at a 14.89% CAGR through 2031.

- By end user, industrial users accounted for 41.67% of revenue in 2025, and are forecast to grow with the highest CAGR of 13.57% through 2031.

- By geography, North America held 37.56% of the construction drones market share in 2025, while Asia-Pacific is projected to grow at a 13.32% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Construction Drones Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid adoption for site surveying and mapping | +3.2% | Global, with concentration in North America and APAC | Short term (≤ 2 years) |

| Building Information Modeling digital-twin integration pull-through | +2.2% | North America and EU, spill-over to APAC | Medium term (2-4 years) |

| Declining sensor and battery costs | +1.8% | Global | Medium term (2-4 years) |

| Autonomous monitoring to offset labor shortages | +1.4% | North America and EU core, spill-over to APAC | Medium term (2-4 years) |

| Post-pandemic infrastructure stimulus | +1.0% | North America, EU, APAC core | Short term (≤ 2 years) |

| Insurer-led risk-monitoring mandates | +0.7% | North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid Adoption for Site Surveying and Mapping

Drone-based surveying has moved from a specialist task to a regular operating workflow across many project types in the construction drones market. Project teams are using aerial capture to generate point clouds and 3D survey outputs with less field effort than traditional manual approaches. Research on BIM-drone integration shows that drone-based reality capture improves monitoring and progress management by enabling direct comparison between site-generated 3D survey images and design models, making more frequent survey cycles practical and strengthening demand for recurring software subscriptions and managed data services across the construction drones market. It also raises owner expectations for as-built documentation, because weekly or even daily capture is easier to justify in terms of both cost and time. As those expectations spread through contract terms, the construction drones market gains a steadier stream of repeat usage rather than one-time aircraft purchases.

BIM Digital-Twin Integration Pull-Through

The construction drones market is seeing structural demand from BIM and digital twin workflows rather than solely from direct drone adoption campaigns. When drone-generated point clouds flow into digital project environments, teams can compare planned work with actual site conditions faster and with less manual checking. Peer-reviewed research confirms that digital-twin systems supported by drone reality capture improve real-time synchronization between virtual plans and physical construction progress. That means each new BIM requirement from a public client, lender, or standards-based supply chain also widens the addressable market for construction drones. Software providers benefit strongly from this pattern because the value shifts toward analytics, model comparison, and workflow integration rather than only toward aircraft capability. Hence, software growth is outpacing hardware growth in the construction drones market.

Autonomous Monitoring to Offset Labor Shortages

Labor shortages are now a practical operating issue for contractors, and that is supporting broader adoption across the construction drones market. In the US, Associated Builders and Contractors estimated that 439,000 net new construction workers were needed in 2025 to meet demand, while AGC reported that nearly 80% of construction firms had difficulty hiring qualified hourly craft workers and 88% expected those conditions to stay difficult or worsen.[1]Associated General Contractors of America, “2025 Construction Hiring and Business Outlook Report,” Associated General Contractors of America, agc.org In this setting, dock-based drone systems and scheduled aerial patrols help firms monitor progress, safety conditions, and site changes without relying on more field supervisors. The construction drones market is therefore gaining relevance not only as a mapping tool but also as a workforce support system for repetitive monitoring tasks. Autonomous deployment also fits contractor efforts to standardize reporting across multiple sites with smaller on-site teams. As labor pressure stays elevated, the construction drones market should continue to benefit from demand for routine, repeatable site intelligence.

Declining Sensor and Battery Costs

Steady improvements in payload economics and mission efficiency also support the construction drones market. Lower sensor costs and better battery performance are reducing the cost per survey mission and making more advanced capture tools available to contractors beyond the largest, which matters most in construction because adoption decisions are often made at the project level, where lower mission costs improve the case for recurring use. Better endurance also helps fleets cover larger areas with fewer interruptions, improving scheduling and reducing field coordination effort. These changes are expanding the practical use of the construction drones market to mid-tier contractors that previously viewed high-precision drone programs as too expensive. As operating economics continue to improve, adoption is likely to spread across a wider range of project sizes and contractor profiles.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent airspace and privacy rules | -1.5% | Global, most acute in EU and North America | Long term (≥ 4 years) |

| Shortage of licensed drone pilots | -0.8% | Global, especially emerging markets | Short term (≤ 2 years) |

| Cyber-security vulnerabilities in commercial-off-the-shelf (COTS) drones | -0.6% | Global | Medium term (2-4 years) |

| High lifecycle maintenance costs of fleets | -0.5% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Airspace and Privacy Rules

Regulatory fragmentation remains one of the clearest limits on expansion in the construction drones market. Dense urban project areas often sit under controlled airspace, which makes approvals, waivers, and operating conditions more complex than the technology itself. In the US, the FAA published its BVLOS Notice of Proposed Rulemaking in August 2025, with a performance-based framework across multiple population-risk categories, and the comment process remained active into 2026.[2]Federal Register, “Normalizing Unmanned Aircraft Systems Beyond Visual Line of Sight Operations, Reopening of Comment Period,” Federal Register, federalregister.gov In Europe, EASA Amendment 5 to Regulation (EU) 2019/947 took effect in May 2025, and France ended its legacy national-standard scenarios from January 2026, requiring migration toward EU-specific-category authorization under DGAC oversight. These differences increase compliance effort for firms operating across borders or near sensitive sites, and they favor larger operators with stronger legal and aviation support resources. Until operating rules become more predictable, the construction drones market will continue to face slower scaling in more regulated environments.

Cyber-Security Vulnerabilities in COTS Drones

Cybersecurity is becoming a more visible risk in the construction drones market as fleets handle survey files, site imagery, and infrastructure data. An FAA-sponsored penetration study identified recurring weaknesses across commercial drone fleets, including default SSID identifiers, default login credentials, and default root credentials, all of which created verified openings for spoofing, data theft, and flight interference. The construction drones market is therefore splitting between buyers focused mainly on price and buyers focused on compliance, secure architecture, and procurement traceability. That shift strengthens the case for NDAA-aligned hardware and better fleet controls, but it also adds transition cost and slows purchasing decisions for some firms.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Rotary-Wing Incumbency Coexists with Rapid Hybrid Scaling

Rotary-wing platforms held 71.17% of the 2025 construction drones market share, reflecting their strong fit for urban job sites, confined takeoff areas, and hovering tasks. These systems remain the default choice for many contractors because they are easier to deploy around buildings, temporary structures, and active work zones. The construction drones market still relies on multi-rotor flexibility for façade inspection, progress capture, and localized surveying. Within the construction drones industry, this format also aligns with training and operational practices that many field teams already understand. That installed familiarity helps explain why rotary-wing systems continue to set the baseline for new fleet adoption.

Fixed-wing platforms serve a different role in the construction drones market, especially on large corridor and land-scale assignments where endurance matters more than hover performance. Highway alignments, pipeline routes, and coastal assets remain better matched to longer-range flight profiles. Even so, the gap between rotary-wing and fixed-wing use is narrowing as mission efficiency improves across several aircraft classes. Hybrid VTOL platforms are expected to grow at a 13.43% CAGR through 2031 because they combine practical field deployment with broader area coverage. In the construction drones market, that mix is attractive for bridge, dam, renewable, and remote civil projects that need both transit efficiency and close inspection capability.

By Component: Software Monetization Gap Reshapes Long-Term Economics

Hardware accounted for 57.64% of the construction drones market in 2025, indicating that fleet build-out still starts with aircraft, payloads, and supporting equipment. Many firms are still in the early stages of program development, so capital spending on equipment accounts for a significant share of total revenue. Services fill the gap for contractors that prefer outsourced flying, data capture, or compliance support on a project basis. The construction drones market, therefore, still has a strong front-end hardware profile even though long-term value is shifting elsewhere. This pattern is common where installed bases are still growing, and operating models vary widely by contractor size.

Software is forecast to grow at a 12.77% CAGR through 2031, making it the fastest-growing component in the construction drones market. The main reason is that value is moving toward data processing, AI-assisted analytics, mission planning, and integration with project systems. Research on drone and digital twin workflows supports this shift because real-time synchronization depends on data handling and model comparison, not just on aircraft deployment. As programs mature, customer retention is increasingly tied to platform usability and workflow integration rather than only to the aircraft brand. Within the construction drones industry, software is the clearest long-term source of differentiation and recurring revenue.

By Application: Surveying Leadership Remains Firm While Surveillance Gains Speed

Land surveying and topographic mapping accounted for 42.83% of the construction drones market in 2025, confirming that surveying remains the main entry point for adoption. Many contractors first deploy drones to replace slower or more labor-intensive site measurement methods before expanding into other uses. The construction drones market has therefore built much of its installed base around topographic capture, volume measurement, and progress documentation. These uses fit directly into planning, billing support, and site coordination. They also create a practical foundation for later expansion into inspection and automated monitoring.

Peer-reviewed work shows that drone-generated point clouds can be compared against BIM models to support progress tracking and verify physical work against design intent. That supports the broader role of the construction drones market across the project lifecycle, from early surveying to ongoing site checks. Security and surveillance are expected to grow at a 14.89% CAGR through 2031 as safety requirements, insurer attention, and remote monitoring needs become more important. Dock-based operations strengthen this case by making recurring patrols more practical without requiring an operator to be on site at all times. In the construction drones market, surveillance is becoming less of a reactive documentation tool and more of a routine layer for site risk management.

By End-User: Industrial Programs Set the Utilization Benchmark

Industrial end users accounted for 41.67% of 2025 revenue in the construction drones market and are expected to grow at the highest CAGR of 13.57% through 2031. Energy infrastructure, mining, utilities, and heavy civil programs tend to run across longer timelines and larger footprints than other project categories. That makes drone fleets easier to justify because aircraft utilization, repeat-mission demand, and software use remain high over several years. The construction drones market benefits from this steady demand pattern because industrial operators often build dedicated internal workflows rather than relying on one-time project spending. In practice, these programs set the operating benchmark for how drone data is used at scale.

Commercial construction remains an important expansion path in the construction drones market as project owners push for stronger documentation, BIM use, and schedule transparency. Data centers, hospitals, transit projects, and other institutional projects are better positioned than smaller private developments to absorb the costs of continuous monitoring. Residential construction remains the smallest end-user segment because individual project budgets and shorter cycles often make dedicated fleets harder to justify. Many residential firms are more likely to use drone services on demand rather than maintain their own program, leaving the construction drones market with a clear utilization split: industrial work supports the heaviest use, while commercial demand broadens the customer base over time.

Geography Analysis

North America held 37.56% of the construction drones market share in 2025, making it the largest regional segment. The region benefits from a large construction spending base, active technology adoption among major contractors, and broad use of digital project workflows. AGC reported that 26% of US construction firms planned to increase drone investment in 2025, suggesting a shift from pilot programs to recurring budgets. The construction drones market in North America also reflects strong demand for secure and compliant platforms as federal and regulated project work becomes more selective on procurement standards.

Europe remains a mature secondary region in the construction drones market, supported by a more harmonized regulatory base than many other multi-country markets. EASA Amendment 5 to Regulation (EU) 2019/947 took effect in May 2025, which helped shape operating expectations across member states. France imposed a near-term compliance burden when legacy national-standard scenarios ended in January 2026, and operators had to move toward EU-specific category authorization under DGAC oversight. Even with that transition cost, the construction drones market in Europe remains supported by cross-border service potential and continued use in inspection and progress monitoring. The UK, Germany, and France remain the leading adoption centers within the region.

Asia-Pacific is the fastest-growing regional segment in the construction drones market, with a projected CAGR of 13.32% through 2031. China and India are the main scale drivers, though demand patterns differ between rapid smart-site deployment and infrastructure-led adoption. Japan is an important indicator of operational maturity. In March 2025, KDDI Smart Drone and Obayashi Corporation completed a fully remote, automated drone inspection demonstration at an active dam construction site using Skydio Dock for X10.[3]KDDI Smart Drone, “国内建設業界初、自動充電ポート付きドローン『Skydio Dock for X10』を活用した遠隔自動ダム巡回の実証に成功,” KDDI Smart Drone, kddi.smartdrone.co.jp South Korea also demonstrated the shift toward autonomous operations when DJI Enterprise published a March 2026 case study on SK Construction's use of DJI Dock 3 for remote construction site management during winter conditions. South America, the Middle East, and Africa remain smaller markets for construction drones. Still, large infrastructure corridors, energy projects, and selective smart-city investments continue to open demand for surveying, earthwork monitoring, and inspection services.

Competitive Landscape

The construction drones market remains moderately concentrated, with SZ DJI Technology holding broad hardware leadership while several focused rivals compete in specific use cases. The strongest competitive pressure is coming from firms that pair compliant hardware with autonomy and workflow software. In April 2026, Skydio raised USD 110 million in a Series F round and announced the SkyForge initiative, a five-year commitment to invest USD 3.5 billion in US manufacturing and support more than 2,000 direct jobs.[4]Skydio Editorial Team, “Skydio Commits USD 3.5 Billion to Expand U.S. Drone Manufacturing and Secure American Drone Leadership,” Skydio Official Blog, skydio.com That move matters in the construction drones market because procurement rules are increasingly tied to supply chain security and domestic manufacturing depth.

Competition is also shifting toward managed operations, automated docks, and software that can turn site data into usable daily outputs. DJI strengthened that position with Dock 3 in February 2025, a vehicle-mountable drone-in-a-box system built for 24/7 remote operations and mobile deployment. The March 2026 SK Construction case then showed how dock-based workflows are being used for scheduled patrols and remote progress visibility in live construction environments. The construction drones market is therefore moving away from simple aircraft comparison and toward a broader contest over uptime, autonomy, data delivery, and compliance. Vendors that can combine those features are better placed to defend pricing and retain customers.

Specialists continue to challenge larger vendors at the application level in the construction drones market, especially in mapping, confined inspection, and industrial structures. These companies do not always need to displace a platform leader across the whole project workflow to win contracts. A focused capability can still secure a strong position where the work is technically difficult or regulation makes compliance more valuable. At the same time, the construction drones market is becoming harder for smaller entrants because certification, cybersecurity expectations, and customer switching costs are rising. This keeps the field competitive, but it also favors vendors that can support long sales cycles, regulated procurement, and recurring service delivery.

Construction Drones Industry Leaders

SZ DJI Technology Co., Ltd.

Parrot Drones SAS

Yuneec (ATL Drone)

3DR, Inc.

Autel Robotics Co. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Skydio secured USD 110 million in a Series F funding round, achieving a post-money valuation of USD 4.4 billion. Concurrently, the company announced the SkyForge initiative, a five-year, USD 3.5 billion commitment to expand US drone manufacturing, including the development of a new facility that will be five times larger than its current space, thereby strengthening Skydio's position as the leading NDAA-compliant option for US federal construction programs.

- August 2025: The FAA and TSA published the BVLOS NPRM (Part 108) in the Federal Register. This proposal outlines performance-based, risk-tiered regulations for UAS operations beyond visual line of sight (BVLOS) across five population-density categories. The rule specifically applies to commercial construction, aerial surveying, and inspection operations and serves as a prerequisite for scalable autonomous drone deployment at construction sites in the United States.

- May 2025: Skydio unveiled Remote Flight Deck, a browser-based control system for 5G networks, streamlining multi-site construction assessments.

- January 2025: DJI introduced Dock 3, a weather-sealed drone-in-a-box enabling 24/7 autonomous sorties and dual-drone rotation for continuous site coverage.

Global Construction Drones Market Report Scope

Construction drones are unmanned aerial vehicles (UAVs) specifically designed for construction applications. These drones assist with tasks such as land surveying, progress monitoring, infrastructure inspection, and security, enhancing efficiency and accuracy in construction operations.

The construction drones market is segmented by type, component, application, end-user, and geography. By type, the market is segmented into rotary-wing, fixed-wing, and hybrid. By component, it is divided into hardware, software, and services. By application, the market covers land surveying and topographic mapping, progress monitoring and documentation, infrastructure inspection, security and surveillance, and earthwork and volume measurement. By end-user, the market is segmented into residential construction firms, commercial construction contractors, and industrial. The report also covers the market sizes and forecasts for the construction drones market in major countries across different regions. For each segment, the market size is provided in terms of value (USD).

| Rotary-Wing |

| Fixed-Wing |

| Hybrid |

| Hardware |

| Software |

| Services |

| Land Surveying and Topographic Mapping |

| Progress Monitoring and Documentation |

| Infrastructure Inspection |

| Security and Surveillance |

| Earth work and Volume Measurement |

| Residential Construction Firms |

| Commercial Construction Contractors |

| Industrial |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Type | Rotary-Wing | ||

| Fixed-Wing | |||

| Hybrid | |||

| By Component | Hardware | ||

| Software | |||

| Services | |||

| By Application | Land Surveying and Topographic Mapping | ||

| Progress Monitoring and Documentation | |||

| Infrastructure Inspection | |||

| Security and Surveillance | |||

| Earth work and Volume Measurement | |||

| By End-User | Residential Construction Firms | ||

| Commercial Construction Contractors | |||

| Industrial | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is driving growth in construction drones through 2031?

Growth is being supported by faster surveying needs, stronger BIM and digital-twin workflows, labor shortages, and rising demand for autonomous monitoring. The market is projected to reach USD 14.09 billion by 2031 at an 11.81% CAGR.

Which drone type leads adoption on construction sites?

Rotary-wing platforms lead adoption because they work well in confined urban sites and hovering tasks. They held 71.17% revenue share in 2025.

Why is software growing faster than hardware in this space?

Software is growing faster because the value is shifting toward analytics, mission planning, AI processing, and integration with project systems. Software is projected to expand at a 12.77% CAGR through 2031.

What is the largest use case for construction drone deployments?

Land surveying and topographic mapping remain the largest use case. This application accounted for 42.83% of revenue in 2025 because it is often the first workflow contractors digitize.

Which region is expanding the fastest for construction drone adoption?

Asia-Pacific is the fastest-growing region, with a projected CAGR of 13.32% through 2031. Growth is supported by infrastructure build-out and wider adoption of remote and automated site monitoring.

What are the main risks that could slow wider deployment?

The main risks are regulatory fragmentation, privacy and airspace restrictions, cybersecurity weaknesses in commercial fleets, and the operational challenge of scaling compliant autonomous flights across different jurisdictions.

Page last updated on: