Micro-Drones Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

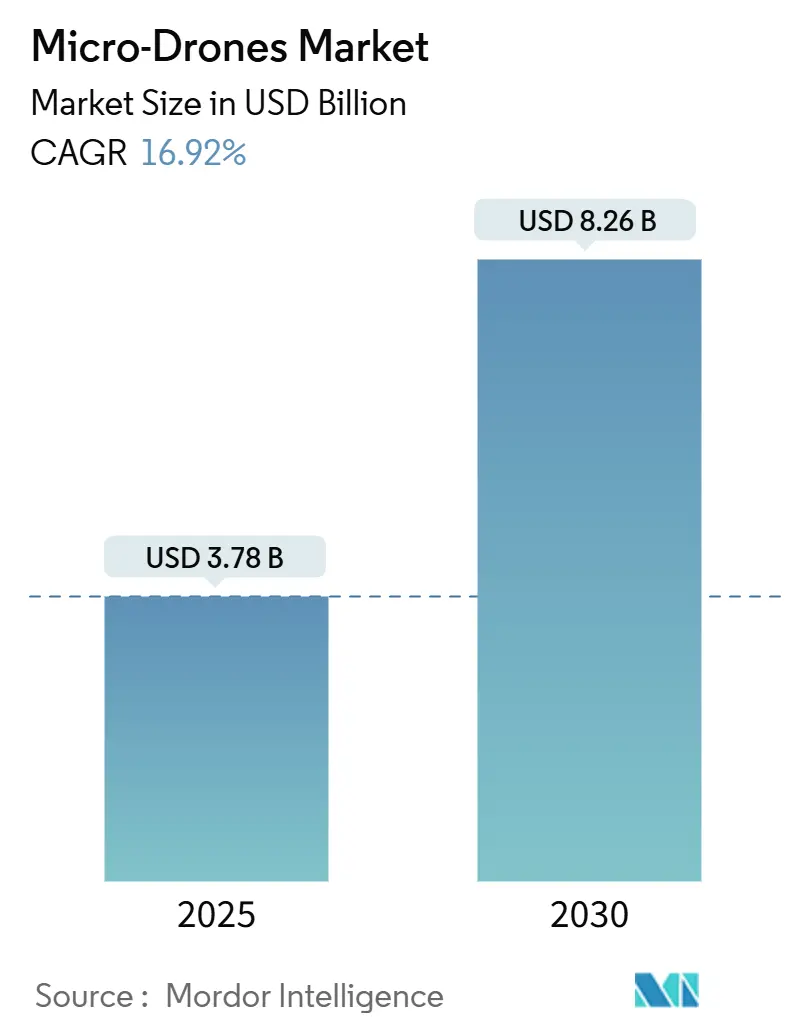

| Market Size (2025) | USD 3.78 Billion |

| Market Size (2030) | USD 8.26 Billion |

| Growth Rate (2025 - 2030) | 16.92% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Micro-Drones Market Analysis by Mordor Intelligence

The micro-drones market size is valued at USD 3.78 billion in 2025 and is projected to reach USD 8.26 billion by 2030, advancing at a 16.92% CAGR. The surge stems from miniaturization breakthroughs that have lowered component costs by 18% while improving performance, enabling new commercial use cases. Rotary-wing platforms dominate current deployments because their vertical-lift agility unlocks indoor operations, while energy-dense batteries and on-board AI continue to broaden mission profiles. Early adoption in precision agriculture, warehouse automation, and infrastructure inspection underscores the technology’s tangible return on investment as enterprises shift toward data-driven asset management. Supply-chain shocks during 2024 catalyzed vertical integration strategies among leading manufacturers, reinforcing the importance of secure semiconductor access.

Key Report Takeaways

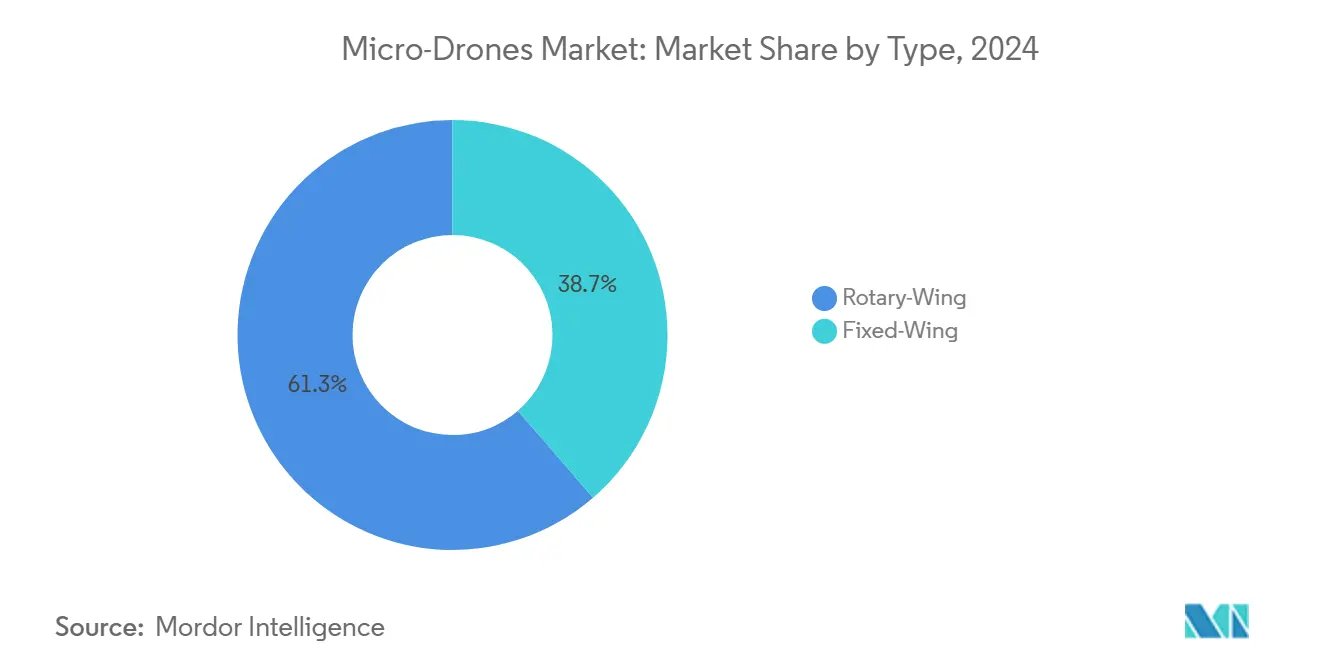

- By type, rotary-wing systems captured 61.34% of the micro-drones market share in 2024 and are expected to expand at a 17.24% CAGR through 2030.

- By weight class, platforms under 1 kg are forecast to grow at 17.89% CAGR, while the 1-2 kg category retained 53.43% share of the micro-drones market size in 2024.

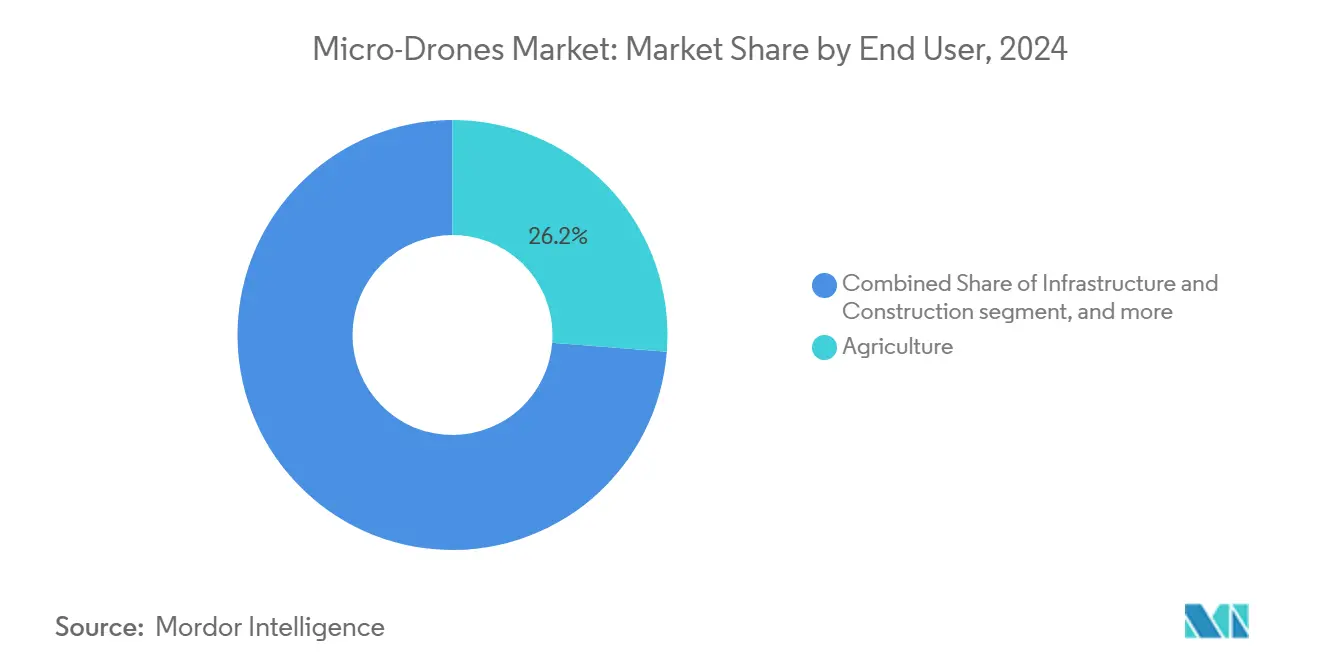

- By end user, agriculture held 26.24% revenue share in 2024; logistics and delivery represent the fastest-growing application with a 19.75% CAGR to 2030.

- By geography, North America led with a 36.43% share in 2024, whereas Asia-Pacific is set to record a 19.56% CAGR through 2030.

Global Micro-Drones Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Advancements in miniaturization technologies and reduction in component costs | +2.5% | Global; manufacturing hub in Asia-Pacific | Medium term (2-4 years) |

| Rising commercial adoption of micro-drones across industries | +3.1% | North America and Europe leading, APAC accelerating | Short term (≤ 2 years) |

| Rising adoption of micro-drones in precision agriculture applications | +2.8% | Global with strong uptake in North America, Europe, India | Medium term (2-4 years) |

| Expanding global use in infrastructure inspection and maintenance activities | +2.2% | North America and Europe core, APAC utilities growing | Medium term (2-4 years) |

| Increasing deployment for indoor inventory management and warehouse operations | +1.9% | North America and Europe; APAC logistics hubs | Short term (≤ 2 years) |

| Emergence of swarm intelligence applications for disaster response and recovery | +1.8% | Global; early use in disaster-prone regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Advancements in Miniaturization Technologies and Reduction in Component Costs

Breakthrough work on micro-actuators and high-density batteries now supports flight-ready platforms weighing less than 100 g and powered solely by light-driven nanomotors. Combined with 3D-printed airframes and consolidated supply chains, manufacturers have trimmed parts expenditures by 18%. These savings make precision-agriculture flights economically viable even for smallholder farms, where per-hectare monitoring costs have fallen steeply. Lower capital barriers entice service providers to scale fleets rapidly, accelerating the virtuous cycle of adoption that underpins the micro-drones market.

Rising Commercial Adoption of Micro-Drones Across Industries

Enterprises deploy micro-drones to streamline labor-intensive processes and gain real-time data visibility. In warehouses, autonomous stock-taking flights cut inventory audit time by 85%.[1]Corvus Robotics, “Warehouse Automation Through Micro-Drone Technology,” Corvus Robotics, corvus-robotics.com Energy utilities employ high-resolution imaging payloads to inspect power lines, bridges, and solar farms, reducing manual inspection costs by 40% while improving worker safety.[2]IEEE Power & Energy Society, “Infrastructure Inspection with Micro-Drones,” ieee-pes.org The diversity of sector-specific value propositions fuels demand for tailored payloads and AI-driven analytics, propelling micro-drones market penetration.

Rising Adoption in Precision Agriculture Applications

Agricultural operators embraced micro-drones at scale during 2024 as DJI platforms treated more than 100 million hectares worldwide. Precision spraying lowered pesticide volumes 30%, aligning with environmental mandates without compromising yield. Multispectral sensors detect nutrient deficiencies earlier than the naked eye, allowing corrective measures before stress symptoms appear. These gains resonate across developed and emerging farming regions, underpinning sustained growth in the micro-drones market.

Expanding Use in Infrastructure Inspection and Maintenance Activities

Grid operators leverage thermal cameras aboard micro-drones to identify failing insulators, slashing unplanned outages by 60%. Confined-space flights inside bridges, ducts, and industrial tanks replace hazardous rope-access tasks, enhancing worker safety while capturing granular imagery for digital twin records. Predictive maintenance algorithms ingest drone data to schedule interventions only when needed, extending asset life and lowering OPEX.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented and stringent international drone regulatory frameworks | –1.2% | Global; severity varies by region | Medium term (2-4 years) |

| Limitations in battery endurance and payload carrying capacity | –1.5% | Global across all weight classes | Short term (≤ 2 years) |

| Heightened global concerns around data privacy and security risks | –0.8% | Primarily North America and Europe | Medium term (2-4 years) |

| Congestion of RF spectrum affecting swarm communication and control | –0.7% | Dense urban and industrial areas worldwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fragmented and Stringent International Drone Regulatory Frameworks

Disparate rules complicate multinational fleet operations. In the European Union, comprehensive EASA regulations mandate pilot licensing and aircraft registration, driving up compliance costs.[3]European Union Aviation Safety Agency, “Comprehensive Drone Regulations,” easa.europa.eu Operators must navigate varying beyond visual line-of-sight (BVLOS) permissions and altitude limits in each jurisdiction, delaying deployment schedules. Harmonization efforts continue, yet the regulatory patchwork tempers near-term expansion of the micro-drones market.

Limitations in Battery Endurance and Payload Carrying Capacity

Lithium-ion (Li-ion) cells plateau near 300 Wh/kg, capping average flight endurance at 25 minutes under commercial payloads. Semi-solid-state prototypes reach 350 Wh/kg but remain too costly for fleet deployment. Operators still juggle trade-offs between sensor suites and mission longevity, restricting some inspection and delivery profiles. Continuous R&D investment aims to bridge the endurance gap that restrains widespread adoption.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Rotary-Wing Dominance Drives Versatile Applications

Rotary-wing platforms commanded 61.34% revenue in 2024, validating their suitability for precision hovering, vertical takeoff, and space-constrained flights. This configuration is projected to log a 17.24% CAGR, underpinning more than half of the forecast micro-drones market size for aerial services that demand maneuverability. Fixed-wing models persist in roles requiring long endurance and wide-area coverage, yet technological hybrids such as tilt-rotors blur category lines.

Continued R&D on ducted-fan shrouds and composite rotors enhances safety for indoor missions such as inventory cycles and plant inspections. Flight-control firmware upgrades enable nuanced thrust vectoring, broadening rotary-wing applicability to emerging tasks like precision seed planting. As software capabilities outpace pure airframe innovations, platform differentiation will hinge on autonomous navigation stacks that exploit the rotary-wing’s agility to deliver data-rich insights.

By Weight Class: Sub-1 kg Segment Accelerates Through Regulatory Advantages

Systems under 1 kg enjoy relaxed rules in many countries, catalyzing a 17.89% CAGR outlook. While the 1 to 2 kg band still comprised 53.43% of the 2024 micro-drones market size, lighter craft increasingly offer parity in sensor quality and onboard processing. Manufacturers integrate machine-learning chips that once required heavier airframes, compressing capabilities into palm-sized designs.

Enterprise buyers gravitate toward the sub-1 kg tier to minimize paperwork and insurance costs. Educational institutions adopt these units for STEM curricula, widening the talent pool for future drone operations. The performance gap with heavier categories narrows as component miniaturization continues, encouraging organizations to standardize fleets around ultra-light classes.

By End User: Agriculture Leads While Logistics Accelerates

Agriculture generated 26.24% of the 2024 micro-drones market revenue, anchored by quantifiable gains in yield and chemical savings. Higher fertilizer prices and labor shortages sustain investment momentum in computerized crop management. Drone analytics merge with agronomic software to produce variable-rate treatment maps, embedding unmanned systems firmly within modern farm workflows.

Logistics and delivery, however, promise the steepest ascent with a 19.75% CAGR as pilots scale last-mile drop networks. Warehouses deploy in-house drones to ferry SKU samples to pickers, capture real-time inventory snapshots, and trim cycle counts from days to hours. Regulatory sandboxes across the United States, Japan, and the United Arab Emirates facilitate BVLOS delivery corridors, priming wider commercial rollouts.

Geography Analysis

North America accounted for 36.43% of global revenue in 2024, benefitting from clarity under FAA Part 107 and an ecosystem of venture-backed service providers.[4]Federal Aviation Administration, “Part 107 Commercial Drone Operations,” faa.gov Large agriculture operations across the Midwest supplemented demand, while infrastructure and energy firms accelerated inspection contracts. Investment in AI-based autonomy from Silicon Valley startups continues to reinforce regional leadership.

Asia-Pacific is expected to post a 19.56% CAGR through 2030, driven by manufacturing clusters in Shenzhen and Taipei that compress production costs. Government programs in China, Japan, and India fund smart-city aerial services and agricultural modernization, creating high-volume procurement channels. Commercial missions constitute 92% of regional flights, indicating a mature focus on enterprise value rather than recreation.

Europe follows a measured growth path under EASA’s harmonized ruleset that balances innovation and safety compliance. Stringent data-privacy mandates impose added diligence, but cross-border drone corridors planned under the EU’s U-space initiative aim to streamline operations. Emerging markets in South America, the Middle East, and Africa witness progressive policy shifts—Brazil’s ANAC and the UAE’s GCAA have expedited licensing frameworks—paving the way for regional pilots to scale once infrastructure funding aligns.

Competitive Landscape

Industry concentration remains moderate, with SZ DJI Technology Co., Ltd. sustaining volume leadership due to vertically integrated manufacturing and proprietary flight-control ecosystems. North American innovators such as Skydio specialize in obstacle-avoidance AI, carving niches in defense and utility inspections. Semiconductor shortages in 2024 prompted strategic stockpiling and in-house chipset design among top vendors.

Competition pivots increasingly toward software orchestration, swarm intelligence, and data analytics platforms rather than pure airframe speeds or endurance. Patent activity shows accelerated filings in vision-based navigation, real-time SLAM, and cloud robotics, underscoring a transition from manual piloting to fully autonomous micro-drone fleets.

Global suppliers diversify revenue through managed-service models, bundling hardware leases with analytics subscriptions that convert capital expenditure into predictable operating costs. This recurring-revenue shift pressures traditional resellers yet fosters deeper client integration, raising switching barriers and redefining customer-vendor relationships within the micro-drones market.

Micro-Drones Industry Leaders

SZ DJI Technology Co., Ltd.

Parrot Drones SAS

Skydio, Inc.

Yuneec International Co. Ltd. (ATL Global Holding AG)

Autel Robotics Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: DJI unveiled the Mini 5 Pro, featuring a 1-inch sensor in a mini camera drone, an Intelligent Flight Battery with up to 36 minutes of flight time, and upgraded ActiveTrack 360° capabilities. The palm-sized drone weighs less than 249 grams.

- September 2023: DJI unveiled its Mini 4 Pro drone. The drone features enhanced obstacle detection capabilities, a 360° omnidirectional vision sensor, and APAS systems that provide comprehensive collision avoidance and flight safety.

Global Micro-Drones Market Report Scope

| Fixed-Wing |

| Rotary-Wing |

| Less than 1 kg |

| 1 to 2 kg |

| Agriculture |

| Infrastructure and Construction |

| Media and Entertainment |

| Logistics and Delivery |

| Energy and Utilities |

| Environmental and Wildlife |

| Others |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Type | Fixed-Wing | ||

| Rotary-Wing | |||

| By Weight Class | Less than 1 kg | ||

| 1 to 2 kg | |||

| By End User | Agriculture | ||

| Infrastructure and Construction | |||

| Media and Entertainment | |||

| Logistics and Delivery | |||

| Energy and Utilities | |||

| Environmental and Wildlife | |||

| Others | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the micro-drones market?

The micro-drones market size stands at USD 3.78 billion in 2025.

How fast is the market expected to grow over the next five years?

It is forecasted to expand at a 16.92% CAGR, reaching USD 8.26 billion by 2030.

Which drone type leads commercial adoption?

Rotary-wing platforms hold 61.34% revenue share due to their vertical-lift agility and hovering precision.

Why are sub-1 kg drones gaining popularity?

They benefit from lighter regulatory requirements and now deliver sensor performance once limited to heavier models.

What sector is projected to grow the fastest in drone usage?

Logistics and last-mile delivery show the highest CAGR at 19.75% through 2030 as trials transition into scaled operations.

Which region is growing most rapidly?

Asia-Pacific is set to record a 19.56% CAGR, driven by manufacturing cost advantages and proactive government programs.

Page last updated on: