Drone Software Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

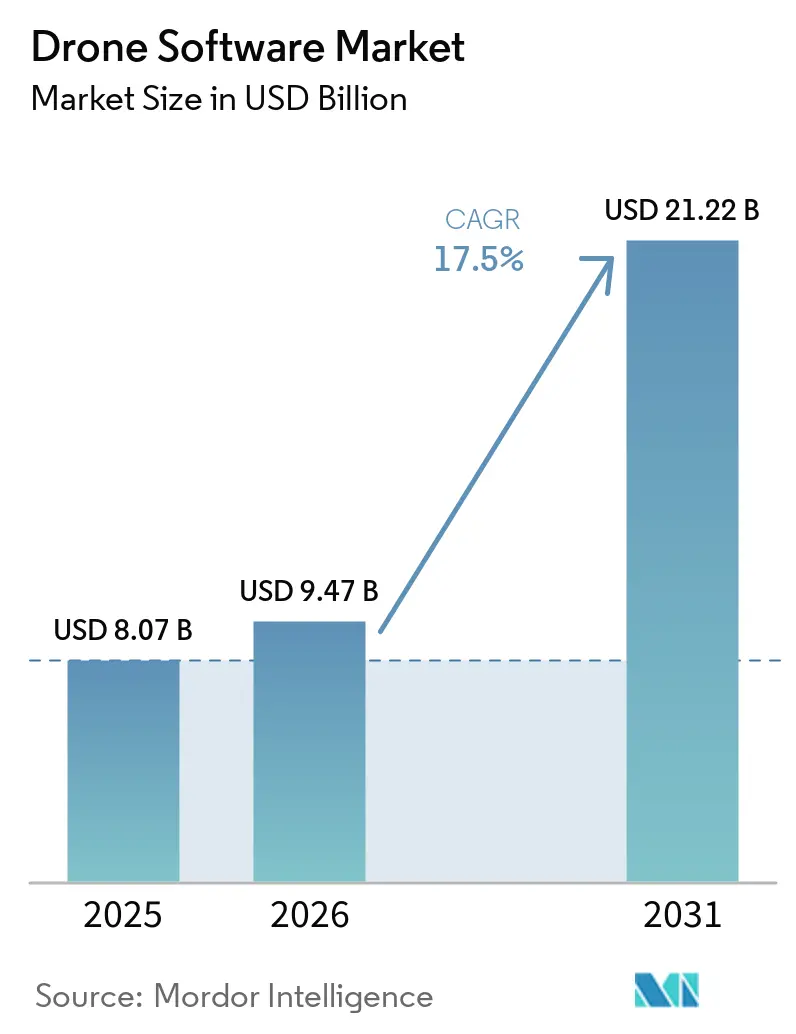

| Market Size (2026) | USD 9.47 Billion |

| Market Size (2031) | USD 21.22 Billion |

| Growth Rate (2026 - 2031) | 17.50% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Drone Software Market Analysis by Mordor Intelligence

The drone software market was valued at USD 8.07 billion in 2025, USD 9.47 billion in 2026, and is projected to reach USD 21.22 billion by 2031, growing at a CAGR of 17.50% over 2026-2031. Growth in the drone software market is being shaped by clearer operating rules, better onboard intelligence, and stronger demand from commercial users that now want routine autonomous flights rather than pilot-led missions. The economic center of the drone software market has also shifted away from airframe sales, as hardware margins have narrowed. At the same time, mission planning, fleet orchestration, onboard inference, and analytics offer stronger recurring economics per deployed system, pushing enterprise budgets in the drone software market toward multi-year subscriptions, especially in construction, utilities, and precision agriculture, where software value continues after the aircraft is purchased. Regulatory delays, procurement restrictions tied to sovereignty, and local data compliance rules are still slowing parts of the drone software market. Yet, automated imagery use in insurance claims is creating a steady demand stream less tied to construction or agricultural cycles.

Key Report Takeaways

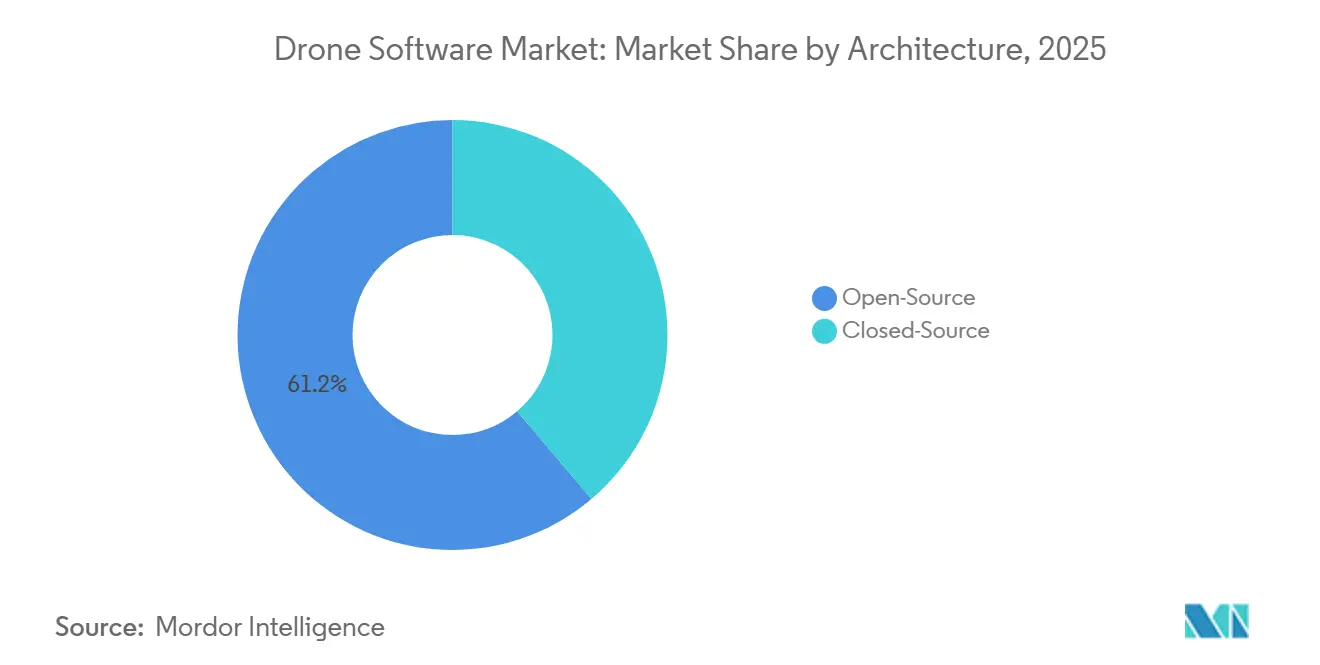

- By architecture, open-source held 61.18% of the drone software market in 2025, while closed-source is projected to grow at a 19.94% CAGR through 2031.

- By application, data processing and analytics accounted for 43.35% of the drone software market in 2025, while delivery and logistics are forecast to expand at a 17.85% CAGR through 2031.

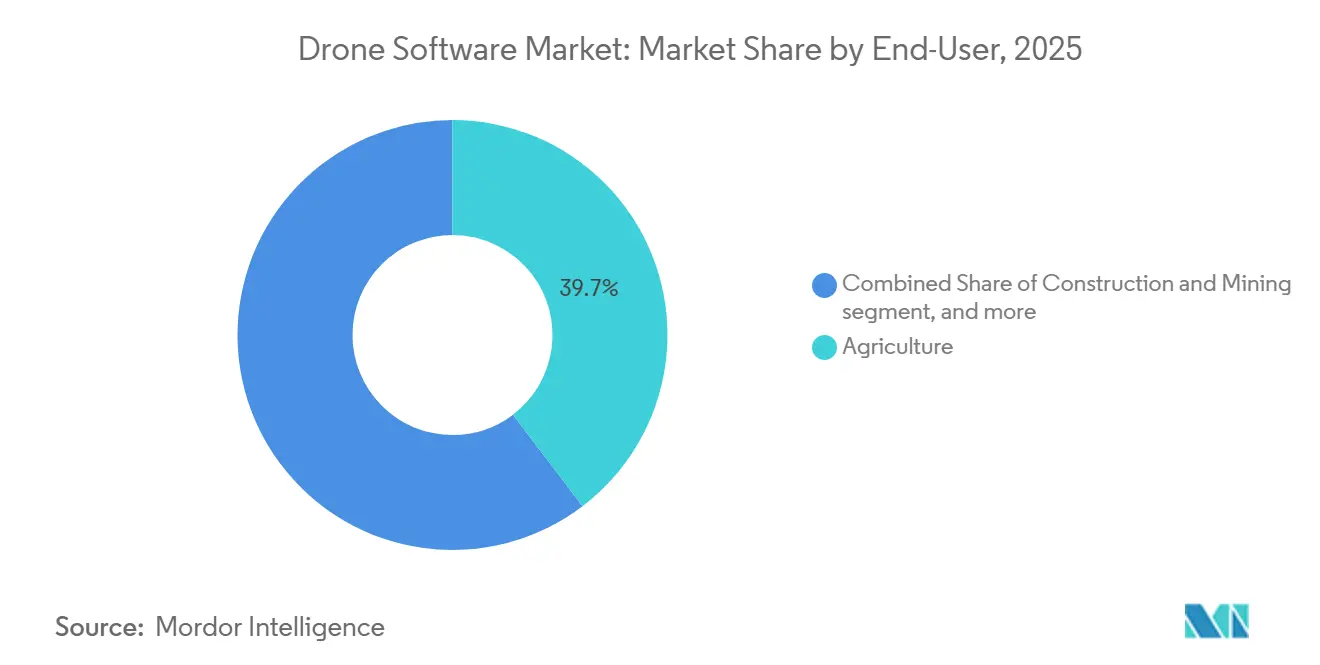

- By end-user, agriculture accounted for 39.66% of the drone software market in 2025, while logistics and transportation are projected to grow at a 18.47% CAGR through 2031.

- By deployment mode, onboard held a 64.48% share of the drone software market in 2025, while ground-based is projected to grow at an 18.72% CAGR through 2031.

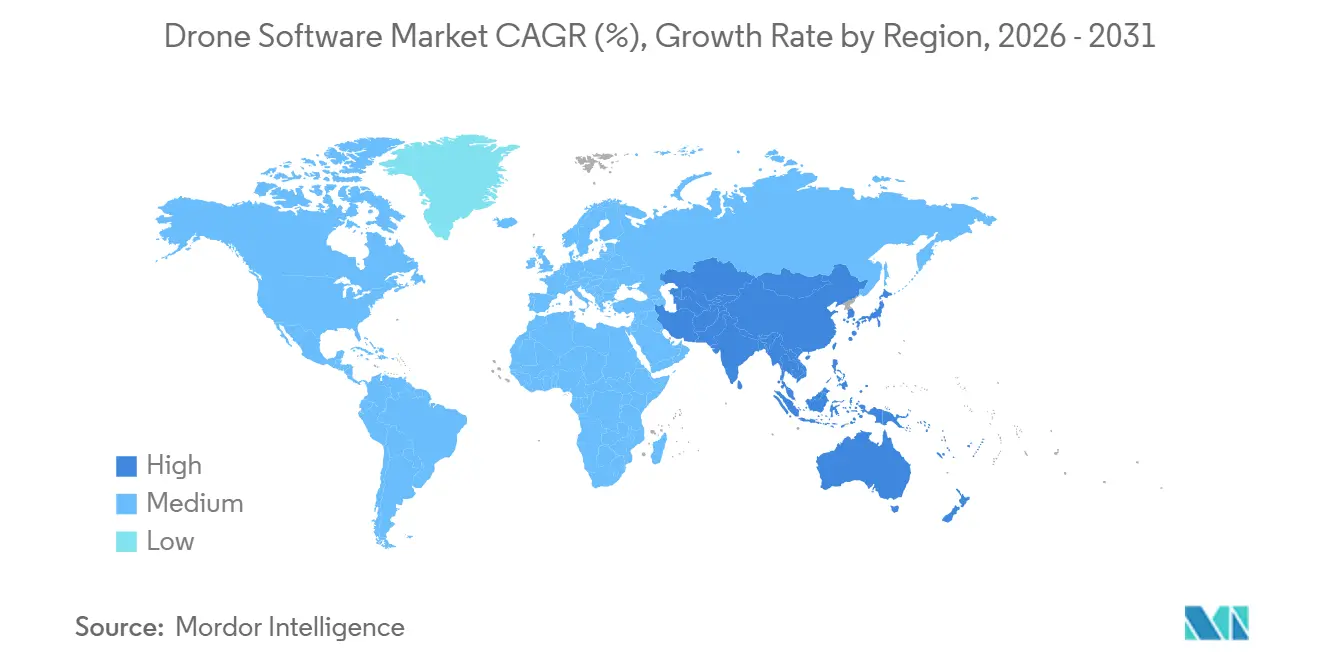

- By geography, North America held 39.93% of the drone software market in 2025, while Asia-Pacific is projected to expand at a 20.26% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Drone Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| FAA BVLOS rulemaking slated for 2026 | +2.5% | North America primarily, with signaling effects for EASA and CAAC | Long term (≥ 4 years) |

| On-drone edge-AI chips priced under USD 30 in the bill of materials | +2.2% | Global, with production concentrated in APAC and deployment gains highest in North America and the EU | Short term (≤ 2 years) |

| Rapid fall in Li-ion battery cost per kWh enabling longer missions | +2.0% | Global, concentrated gains in North America, EU, and APAC delivery corridors | Medium term (2-4 years) |

| Wave of agri-tech subsidies in emerging APAC economies | +1.8% | APAC core, including India, China, Japan, and the Philippines, with secondary spill-over to South America | Short term (≤ 2 years) |

| Mandatory digital twins for infrastructure projects in EU starting in 2026 | +1.5% | EU core, with spill-over to the UK, Norway, and Gulf-state infrastructure programs | Medium term (2-4 years) |

| Insurance-premium discounts tied to automated claims imagery | +1.0% | North America and the EU | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

FAA Part 108 BVLOS Framework Is Creating a Defined Software Addressable Market

The drone software market is gaining a clearer commercial path as the FAA moves BVLOS operations into a more formal rule structure. The FAA published its Part 108 NPRM in August 2025, outlining performance-based pathways for lower- and higher-risk operations, along with software requirements for strategic deconfliction, conformance monitoring, and third-party data services.[1]Federal Aviation Administration and Transportation Security Administration, “Normalizing Unmanned Aircraft Systems Beyond Visual Line of Sight Operations,” Federal Register, federalregister.gov This matters because compliance in the drone software market is no longer limited to flight control and now extends to reporting, event logging, and operator oversight. Skydio’s multi-drone operating approvals with public-sector users demonstrate that one operator can supervise multiple aircraft, underscoring the need for fleet management and situational awareness software.[2]Skydio, “The BVLOS Revolution Continues, Introducing Multi-Drone Operations,” Skydio, skydio.com

The rule also creates recurring software demand, as monthly reporting and incident disclosure requirements align better with subscription models than with one-time license sales. The final rule missed its February 2026 statutory deadline, so near-term buying decisions remain cautious, but the regulatory direction still supports scalable autonomy in the drone software market.

Edge AI Integration at Low Bill-of-Materials Cost Is Reshaping Onboard Capability

The drone software market is also moving toward a more edge-native architecture as onboard inference becomes affordable for commercial fleets. Lower compute costs are making obstacle avoidance, object classification, and autonomous navigation viable without constant reliance on the cloud, which changes how vendors design both aircraft software and enterprise workflows. It also shifts where value is captured in the drone software market, as software teams can push more functionality into the aircraft rather than into remote processing layers. At the same time, keeping more data on the aircraft reduces exposure to cross-border data transfer rules. Still, it also weakens some of the centralized data moats that software vendors built around cloud analytics. The result is a market that increasingly rewards hybrid architecture, with onboard intelligence handling immediate decisions and external systems managing aggregation, orchestration, and long-cycle analysis.

APAC Agri-Tech Subsidies Are Building a Software Demand Foundation

Public support programs across the Asia-Pacific region are strengthening demand for drone software in agriculture. Subsidy programs in India, China, and Japan are encouraging wider drone adoption, expanding the installed fleet that later needs planning tools, agronomic analytics, and usage records as the first software layer in agriculture is often bundled with the aircraft. At the same time, higher-value analytics often require a separate sales effort, local-language support, and clear productivity proof. The drone software market therefore benefits in stages, with flight planning and operations tools moving first, and yield, prescription, and soil analysis modules scaling later. Agriculture was already the largest end-user in 2025, so subsidy-led deployment creates a pipeline that supports future subscription revenue as operators move beyond basic spray operations. The pattern is especially important in the Asia-Pacific, where volume adoption is driven by public policy rather than purely private enterprise demand.

Insurance-Linked Imagery Workflows Are Expanding Commercial Use Cases

Insurance is creating a steadier use case for the drone software market than many infrastructure projects that move with capital spending cycles. Automated imagery and claims workflows give insurers a reason to invest in repeatable flight operations, standardized data capture, and faster review tools. That supports demand for mission-planning, image-processing, and integration software that can move drone outputs into claims systems without manual handoffs. It also broadens the drone software market's customer base, as revenue is no longer tied solely to surveyors, utilities, or large construction firms. As more insurers link imagery collection to cost control and service speed, software vendors gain a durable demand signal that persists even when spending slows in other commercial sectors. Claims processing is one of the more stable avenues for software expansion in the drone software market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of certified UAS software talent | -2.1% | Global, acute in North America and the EU where BVLOS certification raises the skill bar | Medium term (2-4 years) |

| Tighter cyber-sovereignty laws restricting data export | -1.8% | Global, with US-China data flows most affected and EU data residency rules adding friction | Long term (≥ 4 years) |

| Persistent public-privacy litigation in the EU and US | -1.3% | EU and North America | Long term (≥ 4 years) |

| Rising spectrum-management fees for commercial drone links | -0.9% | North America and the EU | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Cyber-Sovereignty Mandates Are Fragmenting Global Software Architecture

Cyber-sovereignty rules are making the drone software market less uniform across borders. US policy actions in 2025 moved federal procurement and export controls toward domestically aligned UAS systems, pushing software vendors to think in terms of separate compliance stacks rather than a single global platform, creating extra work in the drone software market because cloud integration, firmware support, logging functions, and update pipelines may all need review when regulated components are involved. The burden is highest for operators that work across government, infrastructure, and logistics contracts in more than one jurisdiction. These customers increasingly need one stack for US public contracts, another for European data residency, and another for Chinese identification rules. That raises costs for smaller vendors and pushes the drone software market toward middleware and compliance tools that can bridge local regulatory demands.

Certified UAS Software Talent Gaps Are Constraining Scale-Up

The drone software market also faces a practical labor constraint because certified UAS software work requires embedded systems skills, cybersecurity awareness, and knowledge of airspace processes simultaneously. The FAA’s Part 108 proposal formalized supervisory and coordination roles, underscoring the need for trained personnel on both the operator and vendor sides, slowing enterprise onboarding because client teams often need vendor support for integration, configuration, and reporting, rather than handling those tasks internally. It also puts pressure on margins in the drone software market because professional services headcount can grow faster than product revenue during large rollouts. Open-source familiarity does not fully solve this problem because engineers who know community stacks are not always prepared for documented, certifiable, and regulated commercial deployments. The issue is most visible in North America and Europe, where compliance thresholds are higher, and enterprise users expect faster scale-up.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Architecture: Open-Source Ecosystem Leads, Closed-Source Gaining Enterprise Ground

Open-source architecture held 61.18% of the drone software market share in 2025, making it the largest architecture type. This lead reflects the wide adoption of PX4 and ArduPilot as base layers for custom commercial systems across agriculture, inspection, and public safety. The strength of open-source options extends beyond lower licensing costs, as mixed-fleet operators also value hardware-agnostic interoperability and developer flexibility. That advantage matters in the drone software industry because enterprise fleets often combine aircraft from multiple manufacturers and still need a common mission logic and control approach. The segment also benefits from a deep developer ecosystem that supports rapid testing, customization, and module extension without forcing buyers to rely on a single hardware supplier.

Closed-source platforms are projected to grow at a 19.94% CAGR through 2031, making them the fastest-growing architecture segment in the drone software market. Enterprise clients are driving that shift because they want stronger vendor accountability, contractual support, and auditable security layers that sit above flight control functions. Auterion’s commercial positioning reflects this pattern, with a proprietary management layer built on top of an open-source core and backed by a USD 130 million Series B announced in September 2025.[3]Auterion, “Auterion Raises USD 130 Million Series B as Their AI-Enabled Software, Powering Low-Cost Commercial Hardware at Scale, Transforms Warfare,” Auterion, auterion.com The FAA’s proposed Airworthiness Acceptance process is likely to further support this movement, as documented compliance and traceability favor vendors that can deliver controlled releases and clear responsibility chains. Over time, the drone software market is likely to keep both models, with open-source remaining the development substrate and closed-source layers capturing a larger share of regulated enterprise spending.

By Application: Analytics Anchors Revenue, Logistics Emerges as the Next Scale Opportunity

Data processing and analytics accounted for 43.35% of the drone software market in 2025, making it the largest application segment. Its lead reflects the maturity of photogrammetry, remote sensing, and inspection workflows that are already embedded in construction, utilities, and agricultural operations. The segment spans volumetric measurement, crop analysis, thermal inspection, and claims documentation, making it suitable for a broader range of use cases than other applications. DroneDeploy expanded this value layer in October 2025 by launching Progress AI, Safety AI, and Inspection AI, including progress tracking across more than 50 concurrent construction projects, faster report generation, and the identification of more than 90,000 safety risks.[4]DroneDeploy, “DroneDeploy Unveils Agentic AI and Robotics Products at Horizons 2025,” DroneDeploy, dronedeploy.com The application also supports higher contract values because analytics outputs increasingly move directly into ERP, asset, and reporting systems rather than stopping at image capture.

Delivery and logistics are projected to grow at a 17.85% CAGR through 2031, making it the fastest-growing application in the drone software market. That growth depends on BVLOS progress because route optimization, traffic deconfliction, and multi-drone dispatch only scale when operators can move beyond pilot-visible missions. Mapping and surveying remain a stable revenue stream because infrastructure and project documentation workflows keep demand consistent across regulated environments. Flight control and fleet operations software is also gaining ground as multi-drone operating approvals expand, which raises the need for orchestration tools and real-time oversight layers. Training and simulation should also gain weight as the drone software industry adapts to formal operating, reporting, and training expectations under Part 108.

By End-User: Agriculture Holds Scale Advantage, Logistics Accelerates Fastest

Agriculture accounted for 39.66% of the drone software market in 2025, making it the largest end-user segment. Software demand in this segment comes from prescription spray mapping, stand counts, field monitoring, and variable-rate application logic. Public support programs in Asia-Pacific are funding aircraft purchases, creating a broader base of users who later need analytics, planning, and record-keeping tools. Logistics and transportation are projected to grow at a 18.47% CAGR through 2031, driven by warehouse automation, last-mile routing, and drone-in-a-box models that rely on always-on software control. A key challenge remains pricing, because smaller subsidy-supported operators in emerging markets cannot afford the same analytics fees as large commercial farms in North America or Australia can, so vendors need tiered pricing rather than a single global model.

Construction and mining remain major software buyers because reality capture and earthworks measurement are now embedded in project workflows across large sites. DroneDeploy deepened that position in May 2026 by expanding its partnership with PCL Construction to standardize reality capture across more than 1,000 active projects, while also reporting more than 20 trillion square feet of cumulative visual site data captured. Energy and utilities continue to offer attractive recurring software demand because inspection cycles are frequent and asset owners prefer long-term subscriptions over one-off assessments. Environmental monitoring and insurance is also becoming more structured, which supports demand for repeatable capture, analysis, and integration tools, while media and entertainment remains the smallest end-user segment by revenue. Across the drone software market, agriculture provides present scale, while logistics offers the clearest runway for faster expansion.

By Deployment Mode: Onboard Leads, Ground-Based Unlocks Network Scale

Onboard deployment accounted for 64.48% of the drone software market in 2025, making it the dominant deployment mode. This lead reflects enterprise demand for real-time obstacle avoidance, autonomous navigation, and command execution that cannot depend on cloud latency. It also aligns with sovereignty and privacy concerns because local inference reduces the need to move mission data across borders or through third-party servers. The architecture works especially well in regulated or sensitive operating environments where mission reliability and local processing matter more than broad cloud access. As onboard compute improves, more software value is likely to remain on the aircraft, strengthening the role of embedded operating layers in the drone software market.

Ground-based deployment is projected to grow at a 18.72% CAGR through 2031, making it the fastest-growing deployment mode. That growth comes from cloud-based fleet orchestration, remote mission management, and drone-in-a-box systems that need docking control, firmware updates, and centralized planning. Ground-based systems are also better suited to aggregate telemetry from larger fleets where data volumes exceed what can be processed entirely on the aircraft. The longer-term direction of the drone software market points to a hybrid model, with onboard systems handling immediate decisions and ground-based layers managing fleet analytics, mission scheduling, and enterprise integration. This balance is likely to define how large commercial drone programs scale over the next phase of adoption.

Geography Analysis

North America held 39.93% of the drone software market share in 2025, making it the largest regional market. The region benefits from the most advanced commercial UAS operating environment among major economies and from strong enterprise demand across construction, utilities, insurance, and public safety. The FAA's Part 108 proposal is especially important because it defines BVLOS software needs as distinct product categories, including strategic deconfliction, conformance monitoring, and third-party data services. US policy support for domestically aligned drone systems is also influencing vendor selection and procurement behavior, which favors software suppliers that can document compliance and traceability. This combination of regulatory structure, enterprise budgets, and defense-related alignment keeps North America at the center of the drone software market.

Europe held a meaningful position in the drone software market in 2025 and continues to evolve quickly through regulation and procurement standards. EASA rules remain the operating backbone, but digital twin adoption in infrastructure management is becoming the more direct software demand trigger. A2D Cloud clearly shows this regional preference by combining AI-driven defect detection with domestically hosted digital twin workflows for infrastructure users. GDPR and the emerging EU AI Act are also pushing vendors toward privacy-by-design features, which raise compliance costs but strengthen demand for secure, sovereign analytics architectures.

Asia-Pacific is the fastest-growing region in the drone software market, with a projected CAGR of 20.26% through 2031. The region's growth pattern differs from North America's because adoption is driven more by policy-led volume creation than by private enterprise pull alone. China's national standards on operational identification and real-name registration, issued in late 2025 and effective from May 1, 2026, are creating a direct compliance upgrade cycle for manufacturers and software providers. India's agricultural support programs are also building a broader hardware base that should translate into future demand for analytics and planning tools. At the same time, South America, the Middle East, and Africa remain smaller in total but still offer room for expansion, especially where large-scale farming creates a strong fit for precision agriculture software.

Competitive Landscape

The drone software market shows moderate concentration at the platform level, but it remains fragmented across specific applications and vertical workflows. DJI, DroneDeploy, Pix4D, and Esri have strong installed bases because they pair software with developer ecosystems, integrations, and, in some cases, hardware alignment. The clearest strategy split is between broad platforms that are deepening feature depth and specialized vendors that focus on one operational problem. DroneDeploy’s April 2026 quarterly release is a good example because it added support for processed map uploads from Pix4D and other third-party providers, broadening analytics capabilities without forcing customers into a closed capture workflow. That kind of integration strategy strengthens retention in the drone software market by allowing customers to keep existing workflows while expanding their software use.

Auterion represents another major competitive pattern in the drone software market, where defense-grade interoperability is being carried into a commercial opportunity. Its September 2025 Series B highlighted investor confidence in a model that combines open-source flight control foundations with a commercial management and autonomy layer. The company’s position also reflects a broader shift toward auditable, support-backed platforms that meet the needs of enterprise and government procurement. As FAA compliance expectations become more formal, larger vendors with certification teams and documentation capability should gain a structural advantage over smaller niche players.

Skydio’s multi-drone operating approvals with public sector users show how a competitive advantage in the drone software market can also come from providing scalable operations in live environments. That type of operating proof matters because buyers increasingly want software that can manage several aircraft, not just one mission at a time. At the same time, application niches such as inspection analytics, agriculture intelligence, and urban fleet orchestration remain open enough for specialists to win dedicated budgets. The competitive outcome in the drone software market is therefore being shaped less by single-product leadership and more by compliance depth, integration range, vertical fit, and the ability to support recurring enterprise operations.

Drone Software Industry Leaders

SZ DJI Technology Co., Ltd.

Pix4D SA

Esri Global, Inc.

DroneDeploy, Inc.

Parrot SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: DroneDeploy expanded its partnership with PCL Construction to standardize reality capture workflows across more than 1,000 active projects. This move reinforced its role as a leading construction intelligence platform at scale. Additionally, the company announced that it had surpassed 20 trillion square feet of cumulative visual site data captured, creating the largest construction visual dataset globally.

- March 2026: The New York Power Authority received FAA approval for multi-drone BVLOS operations, allowing a single remote Pilot in Command to oversee multiple Skydio X10 drones simultaneously, expanding Skydio's public safety and utility fleet management use case beyond its September 2025 precedent with LVMPD.

- November 2025: Rheinmetall completed a minority investment in Auterion, strengthening its strategic collaboration with AuterionOS for scalable defense-grade autonomous systems. This investment followed Auterion's USD 130 million Series B funding round, led by Bessemer Venture Partners in September 2025, which valued the company at over USD 600 million.

Global Drone Software Market Report Scope

The drone software market is an industry focused on developing, deploying, and using software solutions to enhance drones' functionality, efficiency, and capabilities across a range of applications and industries.

The drone software market is segmented by architecture, application, end-user, deployment mode, and geography. By architecture, the market is segmented into open-source and closed-source. By application, the market is categorized into mapping and surveying, inspection and maintenance, data processing and analytics, delivery and logistics, flight control and fleet operations, and training and simulation. By end-user, the market is divided into agriculture, construction and mining, energy and utilities, logistics and transportation, media and entertainment, and environmental monitoring and insurance. By deployment mode, the market is segmented into onboard and ground-based. The report also covers the market sizes and forecasts for the drone software market in major countries across different regions. For each segment, the market size is provided in terms of value (USD).

| Open-Source |

| Closed-Source |

| Mapping and Surveying |

| Inspection and Maintenance |

| Data Processing and Analytics |

| Delivery and Logistics |

| Flight Control and Fleet Ops |

| Training and Simulation |

| Agriculture |

| Construction and Mining |

| Energy and Utilities |

| Logistics and Transportation |

| Media and Entertainment |

| Environmental Monitoring and Insurance |

| Onboard |

| Ground-Based |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Architecture | Open-Source | ||

| Closed-Source | |||

| By Application | Mapping and Surveying | ||

| Inspection and Maintenance | |||

| Data Processing and Analytics | |||

| Delivery and Logistics | |||

| Flight Control and Fleet Ops | |||

| Training and Simulation | |||

| By End-User | Agriculture | ||

| Construction and Mining | |||

| Energy and Utilities | |||

| Logistics and Transportation | |||

| Media and Entertainment | |||

| Environmental Monitoring and Insurance | |||

| By Deployment Mode | Onboard | ||

| Ground-Based | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected value of the drone software market by 2031?

The drone software market is projected to reach USD 21.22 billion by 2031, up from USD 8.07 billion in 2025, with a CAGR of 17.50% over 2026-2031.

Which region leads drone software demand today?

North America led with a 39.93% share in 2025 because of its mature commercial UAS ecosystem, stronger enterprise spending, and active rulemaking around BVLOS operations.

Which region is expected to grow the fastest through 2031?

Asia-Pacific is forecast to grow the fastest at a 20.26% CAGR through 2031, supported by subsidy-led adoption, policy support, and compliance-driven software upgrades.

Which application generates the most revenue in drone software?

Data processing and analytics was the largest application segment in 2025 with a 43.35% share, supported by construction, utilities, agriculture, and inspection workflows.

What is driving faster adoption in delivery and logistics software?

Delivery and logistics is projected to grow at a 17.85% CAGR through 2031 as BVLOS progress supports route optimization, traffic deconfliction, and multi-drone dispatch.

Why is open-source still dominant in drone platforms?

Open-source held 61.18% of the market in 2025 because enterprises value hardware-agnostic interoperability, broad developer support, and flexible deployment across mixed fleets.

Page last updated on: