Cargo Drones Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

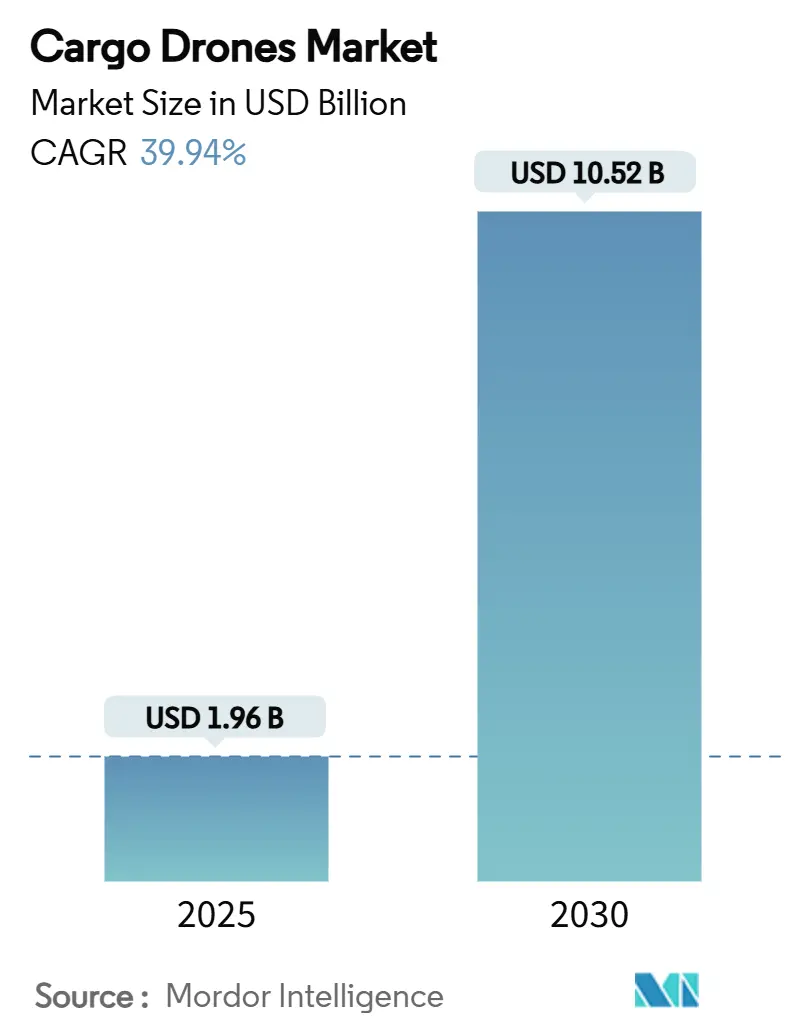

| Market Size (2025) | USD 1.96 Billion |

| Market Size (2030) | USD 10.52 Billion |

| Growth Rate (2025 - 2030) | 39.94% CAGR |

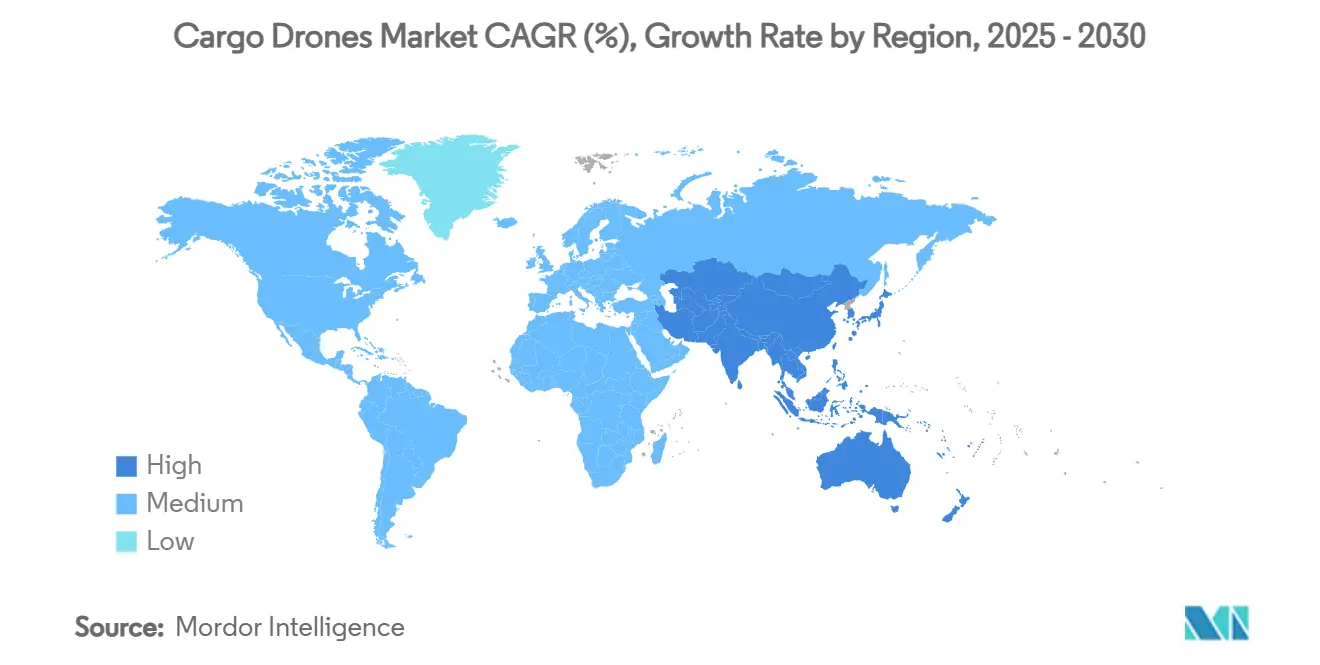

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cargo Drones Market Analysis by Mordor Intelligence

The cargo drones market size stands at USD 1.96 billion in 2025 and is on track to reach USD 10.52 billion by 2030, advancing at a 39.94% CAGR during the forecast period. Rapid regulatory progress, proven delivery scale, and intensifying pressure for same-day fulfillment steer the cargo drones market toward mainstream logistics adoption. Amazon’s 1.5 million completed Prime Air deliveries signal that aerial autonomy can already out-serve traditional vans on short routes. Multi-rotor platforms dominate early deployments because they launch vertically from cramped city sites, yet hybrid VTOL concepts are accelerating as operators chase longer legs without sacrificing rooftop access. E-commerce volumes climbing from 63.5 billion Chinese parcels in 2019 to an expected 175.1 billion in 2024 show why retailers view drones as the only cost-viable path to 30-minute delivery windows.[1]Source: MDPI, “Integrating Autonomous Vehicles and Drones for Last-Mile Delivery: A Routing Problem with Two Types of Drones and Multiple Visits,” mdpi.com Urgent medical logistics add another growth layer as Zipline’s programs cut maternal deaths by 51% in Rwanda, proving commercial viability beyond retail. Persistent lithium-price volatility and gaps in aviation insurance temper near-term profitability, but unit economics continue to improve as battery USD/kWh drops and BVLOS rules remove the need for line-of-sight pilots.

Key Report Takeaways

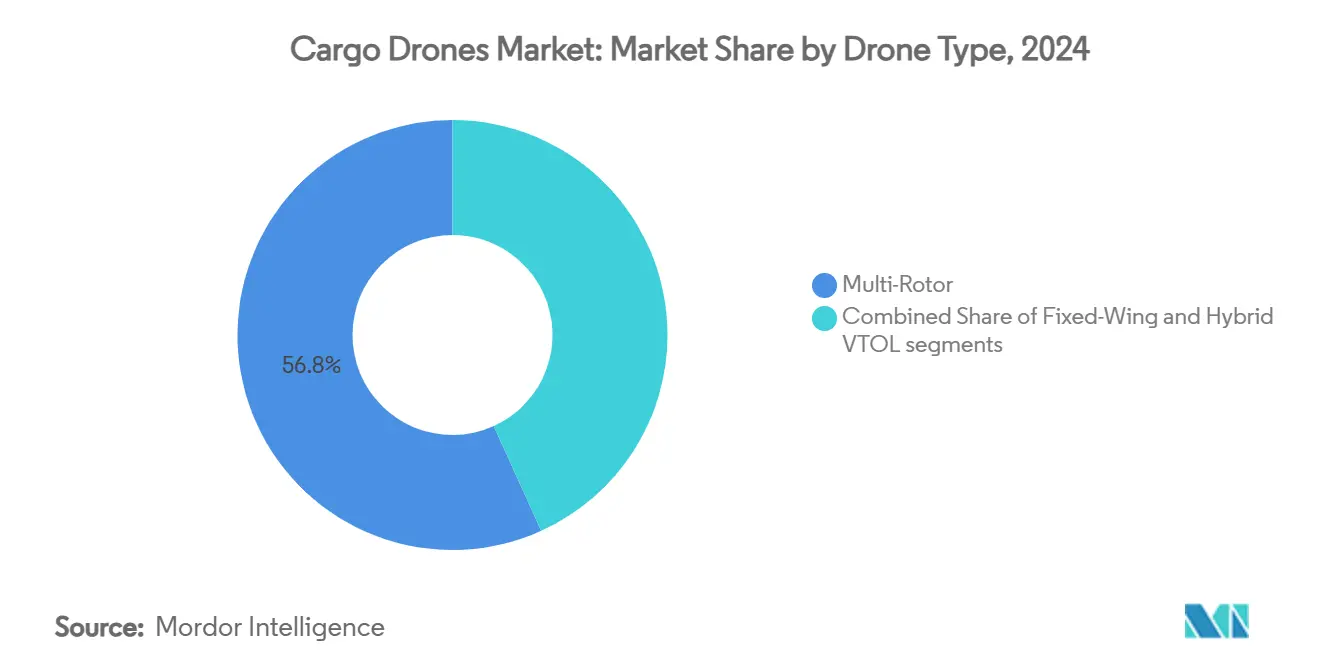

- By drone type, multi-rotor configurations led with 56.78% of the cargo drones market share in 2024; hybrid VTOL systems are projected to expand at a 45.51% CAGR through 2030.

- By payload capacity, the sub-100 kg segment commanded 61.20% share of the cargo drones market size in 2024; aircraft exceeding 1,000 kg are forecasted to grow at a 49.60% CAGR to 2030.

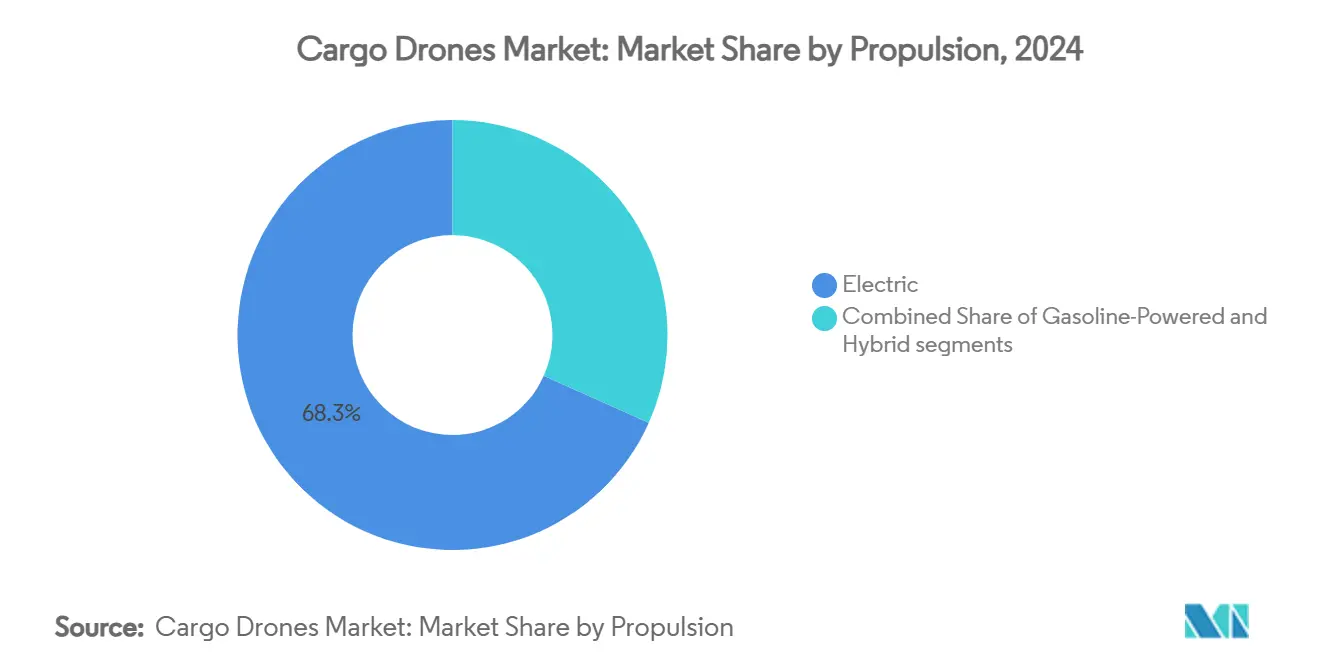

- By propulsion, electric systems captured 68.30% share of the cargo drones market size in 2024, while hybrid platforms are set to climb at a 46.07% CAGR through 2030.

- By operating range, VLOS operations held 64.45% of the cargo drones market share in 2024; BVLOS missions recorded the fastest trajectory, with a 48.70% CAGR to 2030.

- By end-use industry, retail and e-commerce accounted for 41.25% of the cargo drones market size in 2024, whereas healthcare and emergency services will surge at a 43.80% CAGR through 2030.

- By geography, North America dominated the cargo drones market with a 38.74% share in 2024, but Asia-Pacific is expected to sprint ahead at a 47.78% CAGR to 2030.

Global Cargo Drones Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce boom and next-day delivery race | +6.8% | Global; especially North America, Asia-Pacific | Medium term (2-4 years) |

| BVLOS approvals accelerating commercial roll-outs | +5.2% | North America and Europe leading | Short term (≤2 years) |

| Falling battery USD/kWh improving mission economics | +4.3% | Global manufacturing hubs | Long term (≥4 years) |

| Middle-mile hub-to-hub gap in autonomous trucking corridors | +3.1% | North America and Europe | Medium term (2-4 years) |

| Disaster-relief stock-piling contracts in cyclone-prone islands | +2.4% | Asia-Pacific and Caribbean | Short term (≤2 years) |

| Remote mining camps shifting from helicopter to heavy-lift drones | +1.8% | Australia, Canada, Africa, South America | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

E-commerce boom and next-day delivery race

Global parcel counts are multiplying, with China’s express deliveries leaping 175% in five years to 175.1 billion pieces, outstripping labor-intensive van fleets. Urban gridlock inflates van drop-offs by 30-40%, whereas rooftop launches let drones bypass traffic and triple coverage radii. Walmart’s Dallas service now promises 30-minute fulfillment through Zipline’s P2 drones, creating new service benchmarks. Eliminating drivers and trucks can slash per-delivery costs and free retail cash flow for inventory expansion. Amazon’s ambition to ship 500 million packages annually by 2030 underlines how volume scale will cement aerial delivery economics and strengthen the cargo drones market outlook.

BVLOS approvals accelerating commercial roll-outs

Congress mandated final FAA Part 108 rules by March 2026, shifting BVLOS from case-by-case waivers to blanket authorization and clearing backlogs that throttle commercial expansion. Amazon already operates a 10-mile radius in Texas and Arizona after newly granted exemptions, showcasing the transformative effect of BVLOS on service footprints. Europe’s STS-02 framework under EASA lets operators replace direct pilot oversight with corridor observers, further trimming labor overhead. [2]Source: European Union Aviation Safety Agency, “Standard Scenario (STS),” easa.europa.eu Regulatory harmony across major aviation markets allows manufacturers to pursue unified airframes and avionics, unlocking mass-production cost curves. NASA’s search for cargo drone partners signals federal urgency to integrate uncrewed systems alongside commercial jets.

Falling battery USD/kWh improving mission economics

Argonne analysts project pack prices sliding from USD 140/kWh in 2023 to USD 86/kWh by 2035, with IRA tax incentives cutting effective costs even faster. Lower energy costs extend operational range or raise payload without sacrificing profit margins. Structural battery composites promise weight-neutral airframes that double endurance once they mature beyond current TRL-4 test rigs. A switch to lithium iron phosphate cells enhances thermal safety and reduces dependency on constrained cobalt supply chains. Intelligent battery management balances rotor draw dynamically, adding 15-20% flight time on the same charge, supporting stronger adoption in the cargo drones market.

Middle-mile hub-to-hub gap in autonomous trucking corridors

Japan’s Shin-Tomei Expressway will pilot a 25 km autonomous freight lane that shifts 26% of Tokyo-Osaka cargo out of crewed trucks. Cargo drones can extend those ground corridors skyward, bridging DC-to-DC gaps without driver rest cycles. Natilus has secured USD 6.8 billion in orders for blended-wing freighters that leapfrog road congestion and bad weather delays. Hub-aligned flight plans cut waypoint complexity, enabling tighter fleet utilization. Operators report 60-70% faster transfers than night-time trucking while trimming per-ton emissions, reinforcing opportunities for the cargo drones market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Patchwork national air-traffic integration rules | -4.1% | Global; complex cross-border ops | Medium term (2-4 years) |

| Payload/flight-time trade-off limits profit margins | -3.7% | Worldwide constraint | Long term (≥4 years) |

| Lithium-supply volatility for high-density battery chemistries | -2.8% | Global supply chain | Short term (≤2 years) |

| Insurance underwriting gaps for autonomous aerial cargo | -2.2% | Developed aviation markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Patchwork national air-traffic integration rules

Divergent detect-and-avoid specifications oblige drone OEMs to redesign avionics for every jurisdiction, inflating certification budgets and delaying rollouts. The lack of mutual recognition means a system cleared in the United States still faces fresh test flights in the EU or Australia. Cross-border freight lanes remain bureaucratically complex, curbing economies of scale for transnational carriers. Operators frequently maintain parallel operating manuals and pilot credential paths, undermining training efficiency. Market entrants, therefore, prioritize single-region dominance over global footprints, which tempers worldwide growth for the cargo drones market.

Payload/flight-time trade-off limits profit margins

Physics dictates that every extra kilogram shortens airborne endurance, squeezing revenue potential per sortie. Lithium-ion (Li-ion) energy density caps force operators to accept heavier loads for short hops or lighter parcels for profitable range. Rotor Technologies’ 1,000-pound-plus Airtruck retails at USD 850,000, placing high fixed costs against still-nascent revenue streams.[3]Source: Rotor Technologies, “Rotor Technologies Launches World’s Largest Civilian Drone,” rotor.ai Trucks, by contrast, carry 40,000 pounds without range penalties, challenging middle-mile drone economics. Unpowered cargo-glider experiments like Aerolane’s promise 65% fuel cuts yet demand new regulatory acceptance of engine-off flight segments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drone Type: Multi-rotor dominance faces hybrid disruption

Multi-rotor aircraft captured 56.78% of the cargo drones market size in 2024 as their vertical takeoff and hovering precision align with rooftop delivery pads. Simple airframes, lower pilot-training demands, and straightforward maintenance keep capital expenditure modest, encouraging rapid fleet proliferation across early adopter cities. Amazon’s MK30 illustrates iterative gains, quieter rotors, and weatherized housings that lower community resistance and shrink downtime. Fixed-wing drones hold a niche for rural lanes where cruise efficiency trumps spot-landing agility, yet volume remains small relative to urban demand.

Hybrid VTOL systems are scaling at 45.51% CAGR, reshaping the cargo drones market by melding rotor lift for tight urban departure with fixed-wing cruise for intercity hops. Recent flight-control software allows seamless transition between hover and forward flight, eliminating complex pilot inputs. Operators exploiting hybrid platforms cover 150–250 km corridors without recharging, handling time-sensitive goods previously stuck on overnight trucks. The influx of aerospace incumbents such as Boeing via Wisk brings aerospace-grade reliability and certification muscle, accelerating mainstream acceptance.

By Payload Capacity: Sub-100 kg leadership challenged by heavy-lift emergence

The sub-100 kg bracket held 61.20% of the cargo drones market share in 2024 because parcel-weight sweet spots of 1–10 lb fit comfortably within lightweight quadcopters. As Zipline has demonstrated, fewer regulatory hurdles and lower airframe stresses support high sortie cadence, letting fleets rack up millions of flights. Profitability benefits from battery packs small enough to swap in under two minutes, maximizing aircraft utilization.

Heavy-lift drones topping 1,000 kg are projected to climb at 49.60% CAGR, opening a fresh tier of the cargo drones market size for mining, construction, and offshore energy logistics. The Airtruck’s 2,500-lb MTOW enables sling-in of drill parts or wind-turbine blades where road or vessel options add days to schedules. As BVLOS corridors for larger aircraft mature, insurance models improve, and capital budgeting becomes easier, pushing projects from piloting to production.

By Propulsion: Electric dominance with hybrid acceleration

Electric powertrains owned 68.30% of the cargo drones market in 2024 as urban noise rules and zero-tailpipe mandates favor batteries over combustion. Fewer moving parts cut maintenance and allow plug-in charging at retail micro-fulfillment hubs. Recent funding rounds, including Pyka’s USD 40 million Series B, show investor confidence in battery-dependent economics.

Yet hybrid engines are scaling at 46.07% CAGR as payload mass collides with battery weight over longer legs. Dual-source thrust splits tasks: electric lift for silent takeoffs and efficient combustion cruise above noise-sensitive districts. Operators report 40–60% range gains with only marginal fuel burn, balancing sustainability pledges against delivery-time guarantees. The added flexibility widens the cargo drones market appeal for mid-mile hubs lacking rapid-charge infrastructure.

By Operating Range: VLOS constraints drive BVLOS transformation

Piloted, line-of-sight flights dominated 64.45% of the cargo drones market share in 2024 because they sidestep lengthy waiver red tape. Spotter-based safety assurance reassures regulators but forces operators to position crews along routes, inflating labor.

BVLOS missions are rocketing at 48.70% CAGR as draft FAA Part 108 rules promise standardized corridors that free companies from site-specific paperwork. Amazon’s 10-mile circles in College Station triple its previous radius without adding pilots, proving the economic uplift. European operators already exploit STS-02 to orchestrate multi-aircraft fleets from single control rooms, foreshadowing labor-light business models.

By End-use Industry: Retail leadership with healthcare acceleration

Retail and e-commerce retained 41.25% of the cargo drones market size in 2024 as consumer tolerance for multi-day shipping evaporated. Predictable parcel dimensions streamline loading bays and AI routing, cutting per-drop costs. Big-box chains convert portions of parking lots into launch grids, bolstering last-mile efficiency without buying new real estate.

Healthcare and emergency services are poised to expand at a 43.80% CAGR, propelled by evidence that drones halve maternal mortality via blood delivery in Rwanda. Lab sample flights maintain biochemical integrity over 36 km routes in eight minutes, vastly faster than van transit. Emergency agencies embrace drones for line-of-sight hazard scans, slashing responder exposure in fires and floods. Multi-mission flexibility encourages fleet sharing between hospitals and disaster-response units, diversifying revenue.

Geography Analysis

North America held 38.74% of the cargo drones market in 2024, powered by FAA-backed test corridors and tech-giant capital outlays. Texas alone mapped 10 dedicated drone zones along SH 130, letting more than 100 use cases from public safety to freight trial routes. Amazon's 1.5 million cumulative deliveries, plus Zipline's multi-state rollouts, prove consumer acceptance of doorstep drops. Canada's remote mining sites add heavy-lift demand, and regulators prioritize autonomous alternatives to expensive helicopter charters.

Europe showcases regulatory cohesion as EASA harmonizes VTOL rules across 27 nations, enabling manufacturers to certify once and sell continent-wide. Ørsted's Borssele wind farm deliveries now finish in four minutes per turbine compared with six-hour vessel hauls, exemplifying industrial cost savings. Dense urban cores such as Paris and Barcelona explore zero-emission zones that explicitly favor electric drones over diesel vans, cementing future demand.

Asia-Pacific, projected to clock a 47.78% CAGR, benefits from ballooning e-commerce checks on Alibaba and JD storefronts that press for same-day shipping nationally. Under construction, Japan's autonomous Expressway network provides a template for multi-modal freight nodes integrating ground robots and aerial drones. Island chains across Indonesia and the Philippines unlock essential-goods corridors unreachable by trucks. Australia's sprawling mines create high-margin lanes for heavy-lift VTOLs that displace costly helicopter lifts, reinforcing the cargo drones market's geographic expansion.

Competitive Landscape

The cargo drone market remains moderately fragmented, with niche specialists coexisting alongside big-tech entrants. Zipline has surpassed 1 million deliveries and leverages proprietary winch systems for safe medical parcel drops, creating a defensible moat in healthcare logistics. Amazon enjoys unmatched data analytics and fulfillment network synergies, allowing rapid route optimization once BVLOS permissions are explicit.

Hardware innovators such as Rotor Technologies push payload frontiers, fielding more than 1,000 lb Airtrucks to capture construction and agriculture spending. Nautilus secured blended-wing freighter orders worth USD 6.8 billion, signaling airlines' willingness to integrate uncrewed assets for mid-haul routes.

Strategic investments from legacy aviation giants shore up certification expertise. Boeing's stake in Wisk suggests incumbents view uncrewed cargo as complementary rather than cannibalistic. Market consolidation is likely once BVLOS rules stabilize, rewarding operators with manufacturing scale, insurance leverage, and diversified route networks that can amortize R&D across large flight hours.

Cargo Drones Industry Leaders

Zipline International Inc.

Dronamics Global Limited

Wing Aviation LLC

Natilus

Matternet, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: After a two-month pause to address altitude sensor issues, Amazon resumed drone deliveries in Texas and Arizona, introducing the updated MK30 drone designed for quieter operation and light-rain capability.

- June 2024: FlyingBasket, Europe's top producer of heavy-lift cargo drones, forged a strategic alliance with Molicel, a prominent name in lithium-ion (Li-ion) battery innovation. Together, they aim to revolutionize the cargo drone sector by crafting cutting-edge battery systems for FlyingBasket's upcoming FB3 cargo drones.

Global Cargo Drones Market Report Scope

| Fixed-Wing |

| Multi-Rotor |

| Hybrid VTOL |

| Less than 100 kg |

| 100 to 1,000 kg |

| More than 1,000 kg |

| Electric |

| Gasoline-Powered |

| Hybrid |

| Visual Line-of-Sight (VLOS) |

| Beyond Visual Line-of-Sight (BVLOS) |

| Retail and E-commerce |

| Healthcare and Emergency |

| Agriculture |

| Industrial and Manufacturing |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By DroneType | Fixed-Wing | ||

| Multi-Rotor | |||

| Hybrid VTOL | |||

| By Payload Capacity | Less than 100 kg | ||

| 100 to 1,000 kg | |||

| More than 1,000 kg | |||

| By Propulsion | Electric | ||

| Gasoline-Powered | |||

| Hybrid | |||

| By Operating Range | Visual Line-of-Sight (VLOS) | ||

| Beyond Visual Line-of-Sight (BVLOS) | |||

| By End-Use Industry | Retail and E-commerce | ||

| Healthcare and Emergency | |||

| Agriculture | |||

| Industrial and Manufacturing | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Italy | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the cargo drone market size in 2025?

The cargo drone market is valued at USD 1.96 billion in 2025.

What compound annual growth rate (CAGR) is expected for the cargo drone market during 2025-2030?

The market is set to expand at a 39.94% CAGR over the 2025-2030 period.

What proportion of the market did multi-rotor drones capture in 2024?

Multi-rotor platforms accounted for 56.78% of the cargo drone market in 2024.

How will the final FAA Part 108 BVLOS rule, expected in 2026, reshape cost structures and route-planning decisions for U.S. operators?

Standardized BVLOS permissions will remove the need for route-specific waivers, letting a single pilot supervise multiple aircraft and expanding delivery radii from roughly 3 mi to 10 mi per facility, as Amazon’s recent exemption already shows.

Which operational metric best predicts profitability for heavy-lift (greater than 1,000 kg) drone services?

Flight hours per airframe is the critical lever: every 100 additional hours of aerial uptime spreads the USD 850,000 Airtruck capital cost across another 50–60 tons moved, significantly lowering dollar-per-ton-kilometer economics relative to helicopters.

Page last updated on: