Medical Drones Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

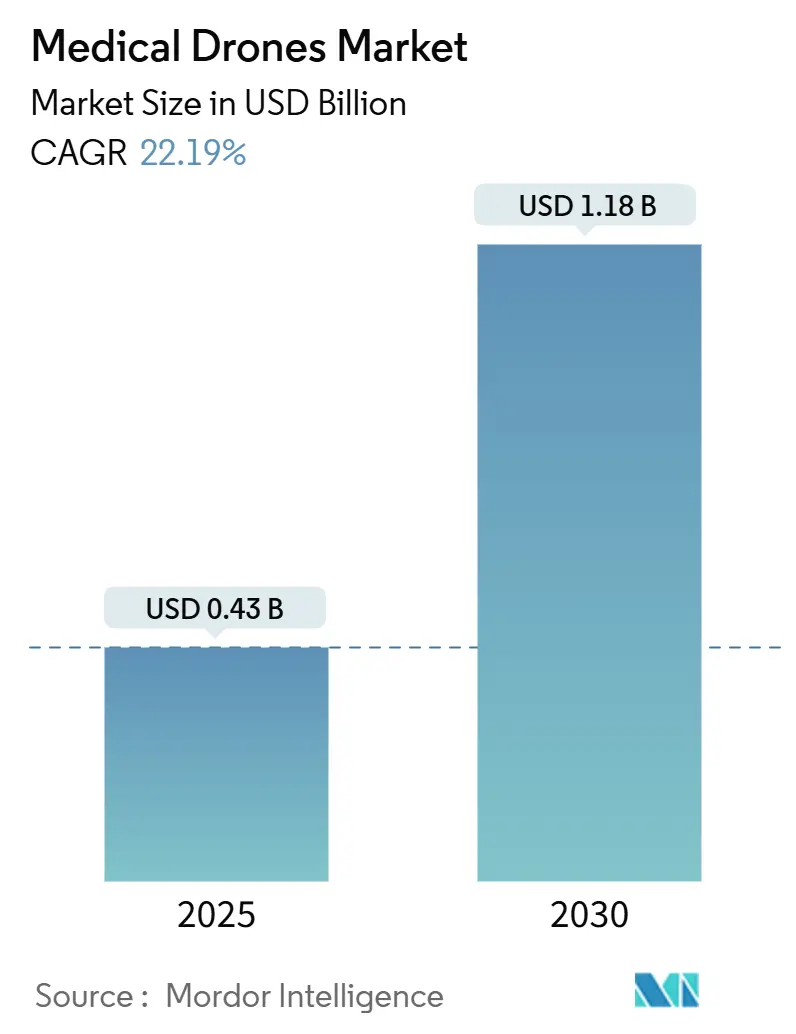

| Market Size (2025) | USD 0.43 Billion |

| Market Size (2030) | USD 1.18 Billion |

| Growth Rate (2025 - 2030) | 22.19% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Medical Drones Market Analysis by Mordor Intelligence

The Medical Drones Market size is estimated at USD 0.43 billion in 2025, and is expected to reach USD 1.18 billion by 2030, at a CAGR of 22.19% during the forecast period (2025-2030).

Rapid progress in beyond-visual-line-of-sight (BVLOS) approvals, lower lithium-ion battery costs, and the spread of drone-supported blood and vaccine networks across Sub-Saharan Africa provide the strongest lift. Wider adoption of Unmanned Aircraft System Traffic Management (UTM) technology is beginning to create assured air corridors around major hospital clusters, while hybrid vertical-take-off-and-landing (VTOL) designs lengthen practical range for heavier, time-sensitive payloads. Health-system initiatives that penalize avoidable readmissions are encouraging hospitals to invest in autonomous logistics, and ongoing hydrogen-propulsion trials suggest a shift toward zero-emission long-haul organ transport. Competitive intensity remains healthy as established platform providers face new entrants that specialize in region-specific services and infrastructure.

Key Report Takeaways

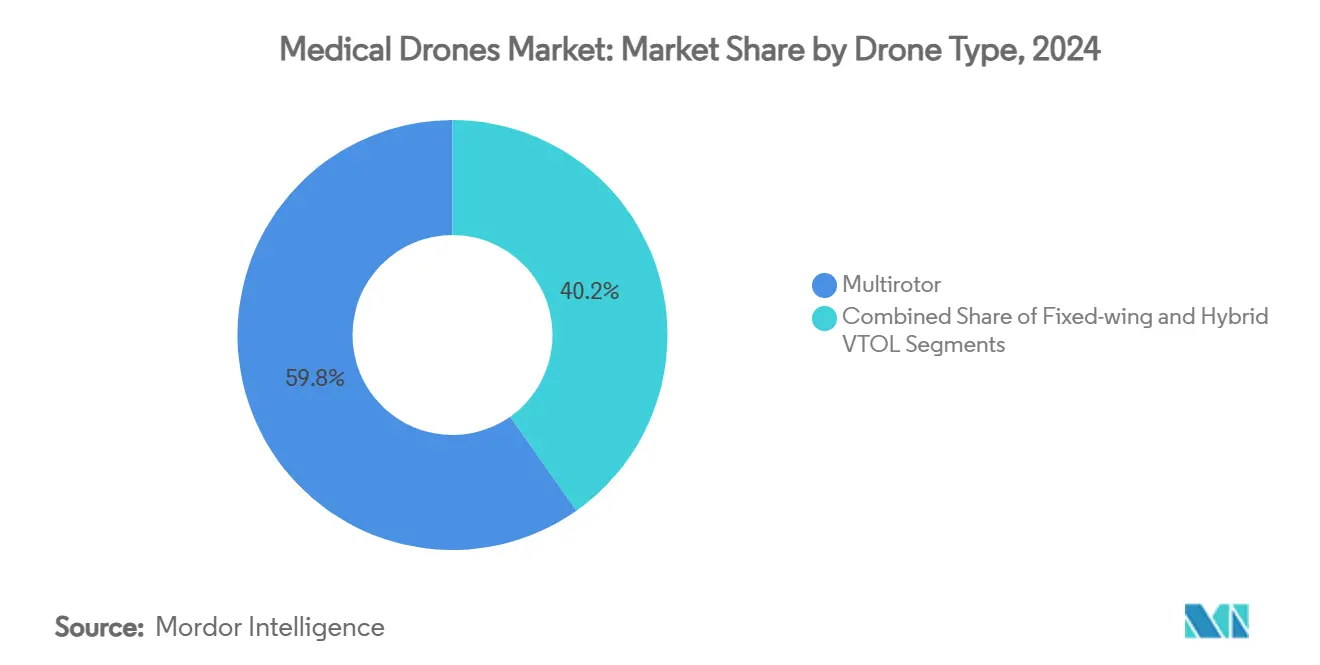

- By drone type, multirotor models led with 59.78% market share in 2024, while hybrid VTOL posted the fastest 26.48% CAGR through 2030.

- By application, blood and vaccine delivery accounted for 46.23% of the medical drones market size in 2024; organ and tissue transport is advancing at a 25.62% CAGR through 2030.

- By end user, hospitals and health systems held 52.34% share of the medical drones market size in 2024 and are growing at 25.79% CAGR to 2030.

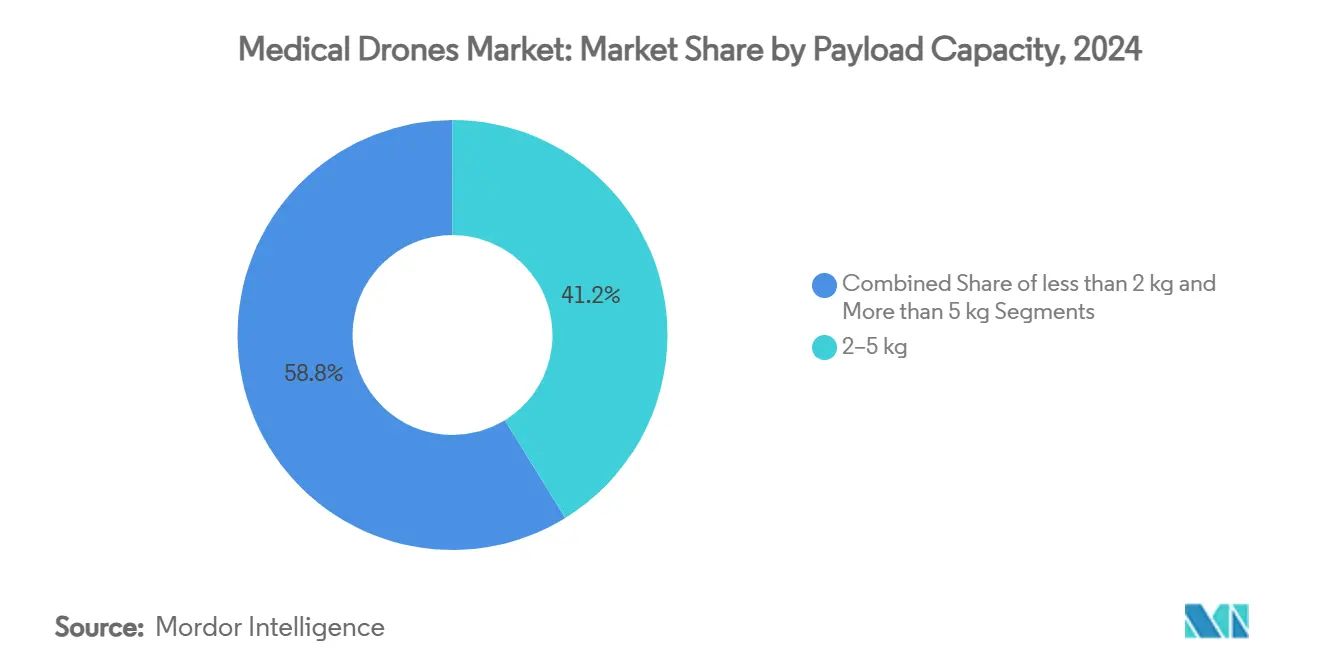

- By payload, the 2–5 kg band captured 41.22% of the medical drones market share in 2024, while the >5 kg segment is expanding at 24.01% CAGR.

- By range, the 20–80 km segment secured 44.36% revenue share in 2024, while the >80 km band is projected to grow at 24.64% CAGR through 2030.

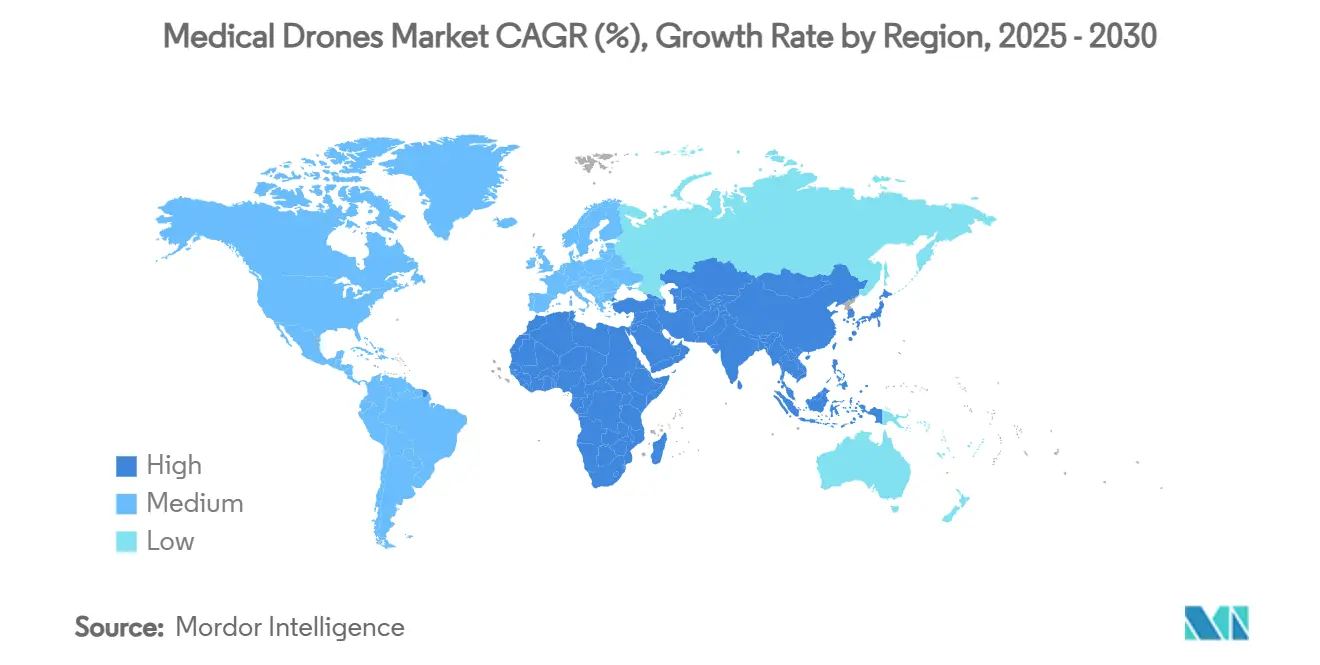

- By region, North America retained 33.41% market share in 2024; Asia-Pacific is recording the highest 25.64% CAGR through 2030.

Global Medical Drones Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Expansion Of Drone-Based Blood & Vaccine Logistics In Sub-Saharan Africa | +4.2% | Sub-Saharan Africa, spill-over to APAC | Medium term (2-4 years) |

| Regulatory "Sandbox" Programs Accelerating BVLOS Approvals | +3.8% | Global, with early gains in North America & EU | Short term (≤ 2 years) |

| Commercialisation Of Autonomous Delivery Corridors Around Super-Hubs | +3.5% | North America & EU core, expanding to APAC | Medium term (2-4 years) |

| Falling Li-Ion Battery $/Kwh Pushing Range-Per-Kg Up By >30% Since 2022 | +2.9% | Global | Long term (≥ 4 years) |

| Hospital Value-Based-Care Incentives To Cut Emergency Re-Admission Costs | +2.1% | North America, expanding to EU | Medium term (2-4 years) |

| Emergence Of Hybrid VTOL Designs Enabling Longer-Range Organ Transport Missions | +1.8% | Global, concentrated in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid expansion of drone-based blood & vaccine logistics in Sub-Saharan Africa

Zipline’s hub in Ghana, now the world’s largest medical drone center, shows why the medical drone market is scaling first in regions where ground networks are sparse. Rwanda recorded a 51% fall in maternal mortality after drone services began, and Ghana posted a 56% drop in maternal deaths, giving regulators concrete public-health evidence. New rollouts in Eswatini and other states confirm the model’s transferability and inspire Asia-Pacific trials. Metrics from these operations provide the proof needed for faster certification in developed countries, shortening commercial lead times.[1]Erin Fichter, “A Mixed Method Impact Assessment of Aerial Logistics in Ghana,” Springer, link.springer.com

Regulatory “sandbox” programs accelerating BVLOS approvals

The FAA’s BEYOND program, Hong Kong’s Regulatory Sandbox, and similar pilots in the United Kingdom and Canada let operators prove safety in controlled settings. By condensing the approval cycle from seven years to under two, sandboxes remove a key barrier for the medical drones market. The FAA’s draft Part 108 rules propose company-level oversight in place of single-mission waivers, signalling a move toward routine BVLOS flights across large fleets.[2]North Carolina DOT UAS Division, “BEYOND,” ncdot.gov

Commercialisation of autonomous delivery corridors around super-hubs

Dallas became the first U.S. city with a designated autonomous delivery hub in 2024, allowing multiple providers to share a single low-altitude corridor and cut per-delivery costs by up to 60%. Zipline’s partnerships with Mayo Clinic and other systems show how corridor models scale services across hospital networks. Vertiport infrastructure, together with 24/7 UTM oversight, positions medical drones to outperform ground transport during peak traffic and adverse weather.[3]Jason Reagan, “Zipline Drones Transform Dallas Into First Autonomous Delivery Hub,” DroneXL, dronexl.co

Falling lithium-ion battery cost improving range-per-kilogram

Silicon-anode cells now exceed 500 Wh/kg, enabling 60-minute missions with ample payload. Mass-manufactured 21700 cells and next-generation lithium-sulfur chemistries widen the operating envelope for the medical drone market. Longer endurance cuts fleet size requirements for continuous service, improving unit economics. National R&D programs in Russia, China, and the United States are pushing the chemistry further, promising heavier organ loads over triple-digit kilometers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Air-Traffic-Management (UTM) Interoperability Bottlenecks | -2.8% | Global, acute in dense urban areas | Short term (≤ 2 years) |

| Payload Vibration & Temperature-Control Limitations For Fragile Biologics | -2.1% | Global, critical for organ transport | Medium term (2-4 years) |

| Community Noise & Privacy Pushback In Dense Urban Zones | -1.9% | North America & EU urban centers | Medium term (2-4 years) |

| Supply-Chain Exposure To Rare-Earth Magnets & High-Grade Carbon Fibre | -1.4% | Global, concentrated in APAC supply chains | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Air-traffic-management interoperability bottlenecks

Early UTM architectures cannot yet deconflict hundreds of simultaneous flights, forcing regulators to limit traffic density and constraining immediate scale. European simulations show capacity drops of up to 40% during peak periods, while U.S. performance-based standards are still two years from finalization. Until commercial and military systems share real-time intent data, the medical drones market must rely on reserved corridors and capped sortie volumes.

Payload vibration & temperature-control limits for fragile biologics

Organs and certain vaccines demand tight thermal bands and minimal shock. Although active cooling using Peltier elements now permits -10°C transport, the added mass and power draw shorten range and reduce payload flexibility. Improving insulation materials and dynamic damping systems is costly and slows mainstream adoption of heavy-value missions within the medical drones market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drone Type: Hybrid VTOL platforms extend reach

Multirotor aircraft commanded 59.78% of the medical drones market in 2024 thanks to fine-grained maneuverability and minimal launch infrastructure. Hybrid VTOL, however, is accelerating at 26.48% CAGR, making it the fastest-moving slice of the medical drones market. These airframes switch to efficient forward flight after take-off, allowing ranges well past 100 km while still landing on compact hospital pads. The segment benefits from field trials such as United Therapeutics’ hydrogen-powered R44 and Wingcopter’s fuel-cell demonstrator. Growing interest from air-ambulance operators underscores broader use cases beyond logistics.

Tilt-rotor innovations aim to hit cruise speeds above 200 km/h without compromising hover precision, which is vital for rooftop helipads. Compound helicopter designs from Dufour Aerospace show how load factors once exclusive to crewed platforms can be met at a fraction of operating cost. Fixed-wing drones remain essential for rural supply chains, but runway demands constrain urban adoption, making multirotor and hybrid VTOL the technology pair that will define the mainstream medical drones market.

By Application: Organ transport sparks high-value growth

Blood and vaccine delivery represented 46.23% of the medical drones market size during 2024 and retains dominance because of proven cold-chain protocols and immediate humanitarian impact. Organ and tissue transport, though smaller, is growing at 25.62% CAGR as transplant surgeons push for wider donor-recipient matches. Record-setting 2024 flights demonstrated viable liver delivery over 160 km, showcasing how drones can bypass traffic delays that erode transplant windows.

Emergency medicines and personal protective equipment (PPE) surged during the pandemic and have settled into routine critical-care support. Lab-sample distribution is another bright spot as hospitals seek faster diagnostics. Cooling systems leveraging Peltier modules help maintain organ viability while AI route planning adjusts for weather deviations, lifting reliability. These combined advances establish a diversified demand base that protects the medical drones market from single-application risk.

By End User: Hospitals anchor adoption curves

Hospitals and health systems generated 52.34% of the medical drone market revenue in 2024, and purchase orders are accelerating with a 25.79% CAGR outlook. Hospital decision makers see drones as a direct lever to cut readmission penalties and boost patient satisfaction scores. Emergency medical services follow closely, particularly in regions adopting drone-delivered automated external defibrillators that reach cardiac-arrest victims 67% faster than ambulances.

Humanitarian NGOs and government agencies rely on donor funding to pilot medical drone corridors in underserved areas. Demonstrations across the Dominican Republic and rural Canada illustrate how autonomous flights give isolated communities access to pharmacy essentials. As hospital-at-home models proliferate, subscription-based drone logistics platforms are lining up long-term contracts, cementing healthcare providers as the strategic nucleus of the medical drones market.

By Payload Capacity: Heavy-lift requirement intensifies

The 2–5 kg bracket held 41.22% of the medical drone market share in 2024, sufficient for blood packs and vaccines. Yet demand for payloads above 5 kg is expanding at 24.01% CAGR as organ transport and multi-patient care kits become routine. Engineers have shown that placing the payload above the center frame improves airflow and stability, allowing carriage volumes to cover half of propeller disk area without trimming efficiency. Heavy-lift drones now ferry up to 100 kg over 100 km, foreshadowing full trauma kits and dialysis fluids in rural emergencies.

Modular pods integrating vibration damping and cold chain controls let operators match cargo profile with mission needs. The flexibility lowers fleet diversity and simplifies maintenance, saving operators costs while broadening service offerings in the medical drones market.

By Range: Long-haul capability diversifies networks

Routes stretching 20–80 km captured 44.36% of the medical drone market revenue in 2024, bridging typical city-to-suburb transit gaps. The >80 km band is outpacing all others with a 24.64% CAGR on the back of VTOL hybrids and hydrogen fuel cells. Malawi’s drone corridor cutting an 8-hour road trip to 35 minutes highlights the life-saving potential. Within urban cores, ≤ 20 km missions dominate for urgent doses and lab samples, where speed outweighs distance.

Battery swapping stations and solar-assisted charging arrays now dot long corridors, enabling near-continuous sorties. Hydrogen platforms promise ranges past 400 km, opening inter-city transplant possibilities that will enlarge the medical drones market.

Geography Analysis

North America led with 33.41% medical drones market share in 2024, supported by the FAA’s proactive BVLOS programs and deep hospital-system partnerships. Health-care reimbursement models reward reduced readmissions, and major providers—Cleveland Clinic, Mayo Clinic, Memorial Hermann—have operationalized drone lanes spanning multiple campuses. Warm investor sentiment is evident in repeated venture rounds for U.S. and Canadian service start-ups, cementing the region’s early-mover status.

Europe follows closely, buoyed by the European Union Aviation Safety Agency’s harmonized standards on noise, sustainability, and U-space. Trials across the United Kingdom, Germany, and the Nordics benefit from dense hospital networks and public acceptance among patients accustomed to telemedicine. Nevertheless, local opposition in select urban centers has prompted altitude caps and flight-time windows that temper immediate scale.

Asia-Pacific shows the steepest growth path at 25.64% CAGR. China’s low-altitude economy policy envisions a multibillion-dollar commercial drone sector by 2030, and Shenzhen already operates a city-wide blood-delivery network. Japan’s refreshed radio regulations unlocking 5 GHz spectrum and Australia’s advanced-air-mobility blueprint point to broader regional alignment. Emerging economies such as Indonesia and Vietnam are piloting humanitarian corridors that emulate Africa’s successes, foreshadowing considerable future volume for the medical drones market.

The Middle East & Africa leverages drones as a leapfrog solution where roads are sparse. Ghana hosts the largest single medical drone hub worldwide, while Eswatini and Rwanda continue to scale national coverage. Policymakers are packaging drone logistics within universal-health-coverage plans, ensuring long-term funding. South America is earlier in the cycle, but Brazil and Chile have initiated sandbox programs, suggesting rising contribution after 2027.

Competitive Landscape

The medical drones market remains moderately fragmented. Zipline maintains the largest operational footprint with over 1 million commercial deliveries across four continents, supported by proprietary autonomous flight software and capsule-drop technology. Wingcopter differentiates through tilt-rotor hybrids and hydrogen research partnerships that target longer-haul medical missions. Matternet focuses on dense-city networks, holding type certification for its M2 platform in the United States.

New entrants such as Swoop Aero scale rapidly by offering turnkey services in 14 countries, leveraging standardized aircraft and cloud-based fleet management. Skyports emphasizes infrastructure, raising USD 110 million in 2024 to build vertiports and provide end-to-end drone services. Manna Aero exports its Dublin playbook to the United Kingdom, underscoring a shift toward execution excellence over proprietary airframes.

Technology moats are deepening. Companies patent temperature-controlled payload bays, autonomous docking stations, and AI route optimization engines. Hydrogen fuel-cell and high-density battery breakthroughs serve as new battlegrounds for range and payload supremacy. Service-centric models are drawing hospital contracts with availability guarantees and per-delivery billing, reducing customer capital outlay and accelerating adoption across the medical drones market.

Medical Drones Industry Leaders

-

Zipline

-

Wingcopter

-

Matternet

-

Swoop Aero

-

Volansi

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: FAA signals progress on BVLOS rulemaking, projecting a 12–18-month acceleration toward routine commercial operations.

- June 2025: NHS London adds ground robots to its drone network, creating a hybrid autonomous supply chain.

- April 2025: Alfresa Holdings and Aeronext launch guideline-compliant pharmaceutical drone delivery in Kawanehon Town, Japan.

- April 2025: Massachusetts begins large-scale healthcare drone trials across urban environments.

Global Medical Drones Market Report Scope

| Fixed-wing |

| Multirotor (Quad/Hex/Octa) |

| Hybrid VTOL |

| Blood & Vaccine Delivery |

| Emergency Medicines & PPE |

| Lab Sample Transport |

| Organ & Tissue Transport |

| Hospitals & Health Systems |

| Emergency Medical Services (EMS) Providers |

| Humanitarian NGOs & Governments |

| <2 kg |

| 2–5 kg |

| >5 kg |

| ≤20 km |

| 20–80 km |

| >80 km |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Drone Type | Fixed-wing | |

| Multirotor (Quad/Hex/Octa) | ||

| Hybrid VTOL | ||

| By Application | Blood & Vaccine Delivery | |

| Emergency Medicines & PPE | ||

| Lab Sample Transport | ||

| Organ & Tissue Transport | ||

| By End User | Hospitals & Health Systems | |

| Emergency Medical Services (EMS) Providers | ||

| Humanitarian NGOs & Governments | ||

| By Payload Capacity | <2 kg | |

| 2–5 kg | ||

| >5 kg | ||

| By Range | ≤20 km | |

| 20–80 km | ||

| >80 km | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

1. How large is the medical drones market in 2025 and what is its growth outlook?

The medical drones market size reached USD 435 million in 2025 and is forecast to grow at a 22.19% CAGR to USD 1.18 billion by 2030.

2. Which application segment is expanding at the fastest pace?

Organ and tissue transport is the fastest‐growing application, advancing at a 25.62% CAGR as transplant programs seek quicker, more reliable logistics.

3. What technology breakthrough is enabling longer‐range medical drone missions?

Hybrid VTOL platforms paired with high‐energy‐density batteries and emerging hydrogen fuel cells are extending practical flight ranges well beyond 100 km.

4. Why are hospitals the leading adopters of medical drones?

Hospitals benefit directly from lower emergency readmission penalties and faster patient‐care cycles, giving them both economic and clinical incentives to deploy autonomous delivery services.

Page last updated on: