Consumer Drones Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Market Size (2026) | USD 7.08 Billion |

| Market Size (2031) | USD 13.10 Billion |

| Growth Rate (2026 - 2031) | 13.11% CAGR |

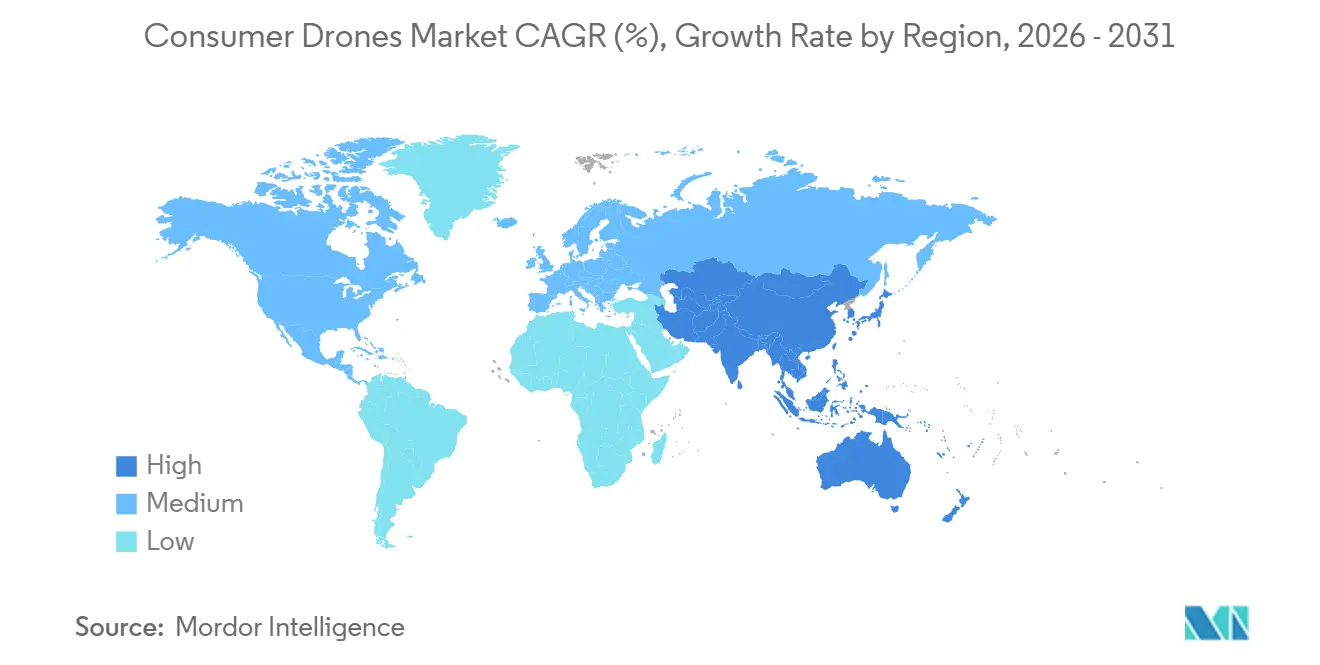

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Consumer Drones Market Analysis by Mordor Intelligence

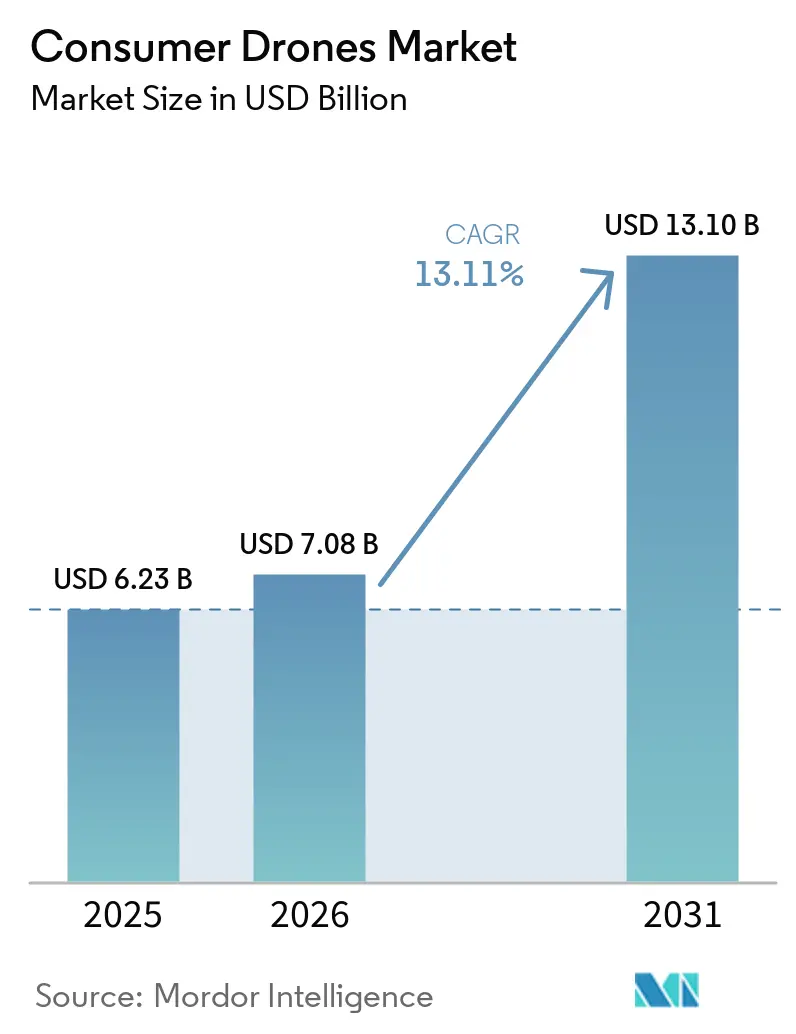

The consumer drones market size was valued at USD 6.23 billion in 2025, and is projected to grow from USD 7.08 billion in 2026 to USD 13.10 billion by 2031, growing at a CAGR of 13.11% from 2026 to 2031. Growth is being supported by lower battery costs and cheaper camera modules, which let brands add better flight time, imaging quality, and safety features without raising retail prices. Aerial content creation across short-form, travel, and lifestyle media is keeping demand broad, especially among first-time buyers who want simple, lightweight products. Rules that ease recreational use of drones below 250 g are steering product design toward lighter foldable models and widening the addressable buyer base. The consumer drones market is also becoming more software-led as brands compete on subject tracking, obstacle sensing, and transmission stability rather than on camera hardware alone. Shipping limits for lithium batteries and crowded radio bands will keep the growth path uneven, even as replacement demand becomes more regular.

Key Report Takeaways

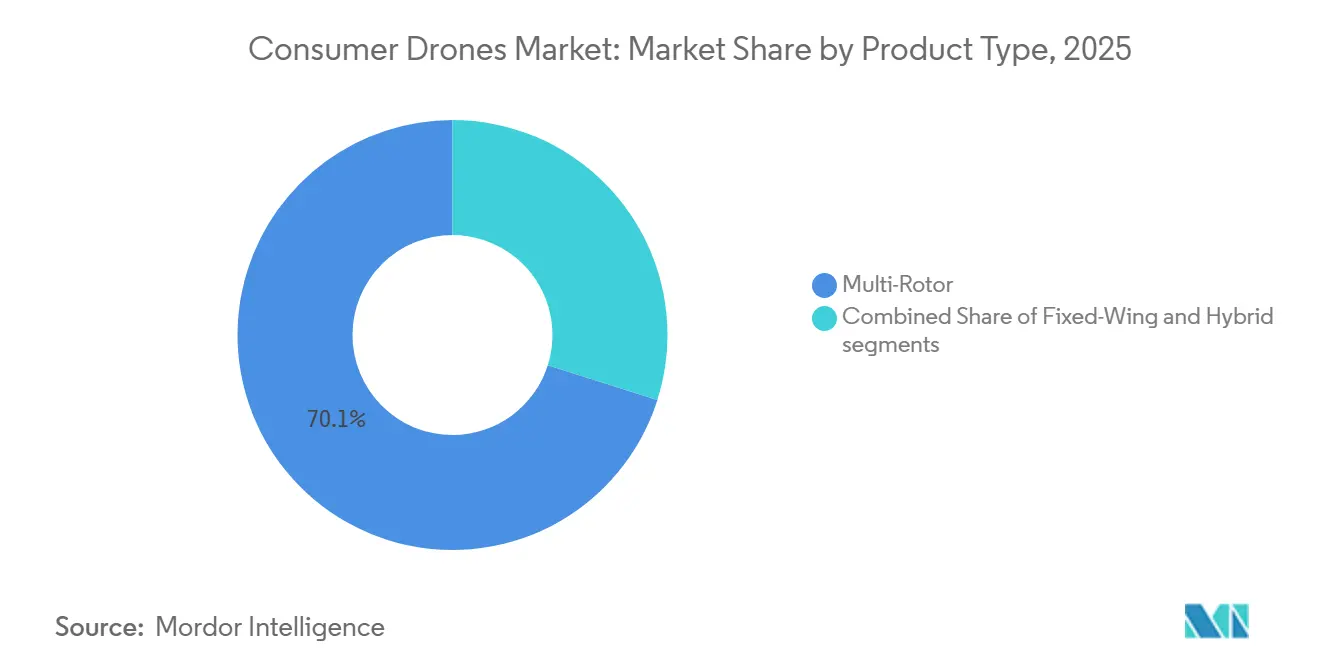

- By product type, multi-rotor drones led with 70.11% revenue share in 2025, while fixed-wing drones are forecast to expand at 15.22% CAGR through 2031.

- By flight range, drones below 4 km accounted for 57.62% of the consumer drones market in 2025, while drones above 8 km are forecast to grow at a 14.11% CAGR through 2031.

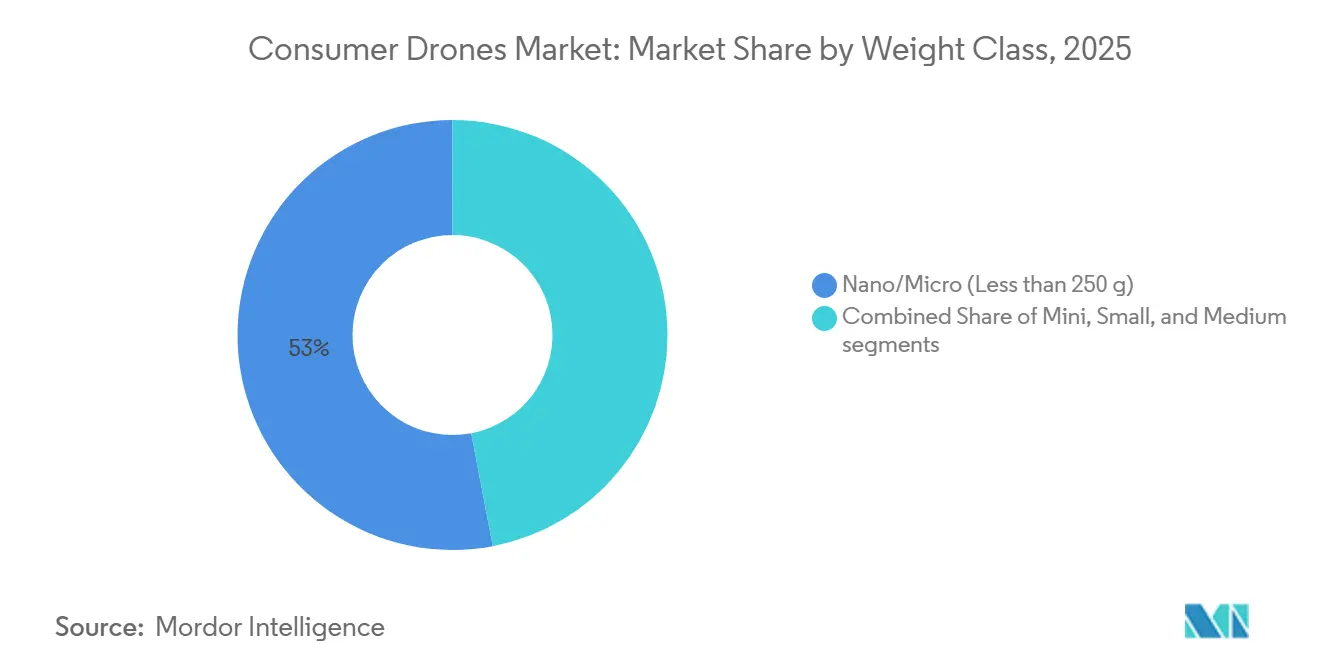

- By weight class, nano and micro drones held 53.00% of the consumer drones market share in 2025, while small drones are projected to grow at a 13.98% CAGR through 2031.

- By application, photography and videography accounted for 61.78% of the consumer drones market in 2025, while racing and sports are projected to grow at a 14.56% CAGR through 2031.

- By geography, North America accounted for 37.65% of global revenue in 2025, while Asia-Pacific is forecast to expand at a 15.01% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Consumer Drones Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid fall in Li-ion battery cost and energy density gains | +3.5% | Global, especially China and North America | Medium term (2-4 years) |

| High quality camera modules becoming commodity components | +2.5% | Global, strongest in Asia-Pacific and Europe | Short term (≤ 2 years) |

| Growing popularity of FPV drone racing leagues | +1.8% | North America, Europe, Asia-Pacific core | Medium term (2-4 years) |

| Smartphone-like replacement cycles emerging | +1.5% | North America, Europe, urban Asia-Pacific | Long term (≥ 4 years) |

| Youth-driven influencer culture on social-media platforms | +2.0% | Global, strongest in North America and Southeast Asia | Short term (≤ 2 years) |

| Increased availability of affordable, user-friendly drones | +2.2% | Global, spill-over to South America and MEA | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid Fall in Li-ion Battery Cost Redefines Drone Economics

Battery cost deflation is making the consumer drones market easier to enter for both brands and buyers. Lower battery costs reduce the bill of materials and create room for longer flight times, better cooling, and safer power management without forcing higher shelf prices, which matters most in entry and mid-range devices, where a small hardware cost change can decide whether a product reaches a first-time buyer. It also changes how brands think about accessories, because upgraded battery packs can become repeat purchases rather than bundled one-time items. DJI demonstrated that battery design can shape the value proposition by promoting an Intelligent Flight Battery Plus option for its new Lito series and tying it to extended flight time. As that pattern spreads, the market will continue to expand across a wider range of price points without sacrificing feature depth.

Camera Modules as Commodity Components Widen the Mass Market

Camera hardware has moved much faster into the mass market than it did a few years ago, changing how the consumer drones market is priced and packaged. DJI introduced the Mini 5 Pro in September 2025 with a 1-inch CMOS sensor in a near-249 g body, demonstrating how advanced imaging could be packed into a lightweight consumer form factor.[1]DJI, “DJI Brings World First to the Sky With Mini 5 Pro,” PR Newswire, prnewswire.com That shift reduces the old gap between premium and mainstream products and makes image quality feel like a starting requirement rather than a premium add-on. Once buyers expect strong video quality at lower prices, brands have less room to defend margins with camera hardware alone. SkyRover reinforced this direction in March 2026 by introducing a sub-249 g model priced below USD 300 with forward obstacle avoidance, 4K/60fps video, and 12 km HD transmission. The result is that the consumer drones market now rewards software ease, automated shooting, and reliable transmission more than raw sensor bragging rights.

FPV Drone Racing Leagues Institutionalize a New Consumer Demand Category

Organized FPV racing is giving the consumer drones market a more durable participation base than a casual hobby cycle usually provides. MultiGP said its International Open 2025 network included more than 30,000 registered pilots and 500 active chapters worldwide, which shows that the activity now has scale, repeat events, and a clear community structure.[2]MultiGP Drone Racing League, “International Open 2025,” MultiGP Drone Racing League, multigp.com That matters because structured competition keeps pilots buying replacement parts, upgrading goggles, and moving into more advanced aircraft over time. It also brings younger users into the category through events, clubs, and local chapters rather than through one-off gadget purchases. MultiGP expanded that footprint further when it hosted its first European Championship in Aichtal, Germany, in September 2025 with pilots from 18 countries. As this organized layer deepens, the consumer drones market gains a stronger funnel, from entry-level FPV products to higher-value enthusiast and imaging products.

Social-Media Influencer Culture Accelerates Aspirational Drone Consumption

Short-form video culture has made aerial footage more familiar to mainstream consumers, and that shift is pulling the consumer drones market beyond early adopters. Buyers are not only looking for image quality, but also for products that are easy to carry, easy to learn, and easy to post from, which has helped lightweight camera drones move from specialist devices into lifestyle electronics. DJI leaned into that demand in April 2026, launching the Lito 1 and Lito X1 as beginner-friendly sub-249 g products aimed at first-time aerial creators. The social layer also shortens the time between product cycles because new modes, new sensors, and new design changes quickly become visible through reviews and creator content. That pattern makes the market behave more like adjacent personal electronics categories, where aspiration and visibility matter almost as much as base utility.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Spectrum congestion in 2.4 GHz and 5 GHz ISM bands | -1.2% | North America and EU, spill-over to dense Asia-Pacific urban markets | Medium term (2-4 years) |

| Lithium-battery shipping restrictions tighten | -0.8% | Global, strongest on cross-border e-commerce routes from Asia-Pacific to North America and EU | Short term (≤ 2 years) |

| Consumer-privacy litigation risk | -0.9% | North America, Western Europe | Medium term (2-4 years) |

| Shortage of drone-qualified repair technicians | -0.7% | Global, most acute in China, India, Southeast Asia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Spectrum Congestion Constrains Reliability in Dense Deployments

The consumer drones market still relies heavily on crowded spectrum bands shared with Wi-Fi, Bluetooth, and an ever-growing set of connected devices. That creates a practical problem for users in cities, parks, and event settings, where signal noise can affect control confidence and video stability. The FCC adopted initial rules in July 2024 for drone operations in the 5030 to 5091 MHz band, but that framework is aimed at licensed advanced operations rather than everyday recreational flying.[3]Federal Communications Commission, “FCC Adopts Initial Rules for Drone Operations in the 5 GHz Band,” Federal Communications Commission, fcc.gov As a result, the core consumer segment remains exposed to the limits of the open ISM environment, even as the policy discussion moves forward, which matters because buyers do not judge a drone solely by its listed range; they judge it by how stable the connection feels in ordinary use. Until spectrum access improves for a broader user base, the consumer drones market will continue to face a reliability ceiling in dense environments.

IATA Battery Shipping Rules Add Cross-Border Logistics Complexity

The consumer drones market also faces a quieter supply chain constraint due to tighter rules on the transport of batteries. IATA made it mandatory from January 1, 2026, that lithium-ion cells and batteries packed with equipment above 2.7 Wh must not exceed a 30% state of charge when offered for air transport, unless specific approval applies. That creates extra discharge, documentation, and handling steps for brands shipping finished products across borders. The impact is heavier for companies that rely on direct e-commerce fulfillment from Asian production hubs into North America and Europe. Larger players can absorb this more easily through destination warehouses and tighter compliance systems. At the same time, smaller entrants face a higher per-unit burden, making logistics discipline an important competitive factor in the consumer drones market, not just a back-end operational issue.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Multi-Rotor Dominance Masks Fixed-Wing Disruption

Multi-rotor drones accounted for 70.11% of revenue in 2025, keeping them firmly at the center of the consumer drones market. Their strength comes from vertical takeoff, easy hovering, compact folding designs, and a flight style that matches photography and everyday recreational use. They also fit well with the lightweight product direction that now defines much of the mainstream category. For most buyers, a multi-rotor platform remains the simplest path to stable video and low learning friction.

Fixed-wing drones are forecast to grow at a 15.22% CAGR through 2031, indicating that a smaller share of the consumer drones market is seeking greater range and endurance. These products appeal more to prosumer users who care about area coverage and longer flight paths than to those who care about stationary hovering. Hybrid designs sit between the two camps and are slowly building relevance because they combine transit efficiency with hover capability. The main challenge is that the fixed-wing and hybrid side still has a thinner product pipeline than the multi-rotor base. Even so, the consumer drones market is likely to see greater differentiation as autonomous navigation improves and higher-skilled users seek aircraft that do more than capture short, local footage.

By Flight Range: Short-Range Utility Anchors the Market, Long-Range Eyes the Next Tier

Drones with flight ranges below 4 km accounted for 57.62% of revenue in 2025, underscoring how strongly the consumer drones market still depends on neighborhood- and travel-scale use. This part of the category fits the needs of casual users who want portability, easy setup, and less regulatory friction. It also fits the weight profile of the lightest and most widely sold consumer aircraft. For mainstream buyers, practical use matters more than extreme distance, so short-range products keep the broadest volume base.

The segment above 8 km is forecast to expand at a 14.11% CAGR through 2031, providing the consumer drones market with a clear premium growth lane. What buyers are really paying for here is stable live video and stronger link confidence, not only the maximum distance shown on a box. DJI highlighted that premium direction in March 2026 when it launched the Avata 360 with O4+ transmission capable of 1080p/60fps video at up to 20 km. That kind of feature set pulls long-range performance closer to the enthusiast mainstream. As the consumer drone industry moves forward, transmission reliability is likely to matter more than raw range escalation alone.

By Weight Class: The Sub-250 g Gravity Well Reshapes Industry Architecture

Nano and micro drones weighing under 250 g captured 53.00% of 2025 revenue, underscoring how decisively regulation is shaping the market. In the US, the FAA says recreational flyers do not need to register drones weighing less than 0.55 lb (about 250 g), a practical threshold that has pushed brands toward lighter designs.[4] That rule removes friction at the point of purchase and makes low-weight products easier to market to first-time users. It also explains why foldable quadcopters remain the preferred architecture in the mainstream category.

The small drones segment, weighing 2 kg to less than 5 kg, is forecast to grow at a 13.98% CAGR through 2031, indicating that the consumer drones market is not moving in only one direction. A higher-capability user group is willing to accept additional registration and compliance steps in exchange for stronger wind resistance, greater payload flexibility, and improved imaging performance. DJI reinforced pressure on the light end when it launched the Mini 5 Pro in September 2025, aligned with sub-250 g design priorities. The split is becoming clearer: the mass market chooses portability and ease, while a smaller prosumer base pays for capability. That divergence is reshaping how the consumer drones market allocates product development across entry-, travel-, and enthusiast-level models.

By Application: Photography Dominance Yields as Racing Accelerates

Photography and videography accounted for 61.78% of application revenue in 2025, keeping content creation at the heart of the consumer drones market. Travel footage, lifestyle videos, real estate visuals, and personal media stills account for most of the category's demand. This segment remains large because aerial imaging has become familiar to ordinary buyers rather than staying limited to specialists. At the same time, its lead is no longer expanding as easily because strong imaging has spread into lower price tiers.

Racing and sports are forecast to grow at a 14.56% CAGR through 2031, making the consumer drones market its fastest-moving use case. Organized FPV leagues add repeat participation, replacement buying, and skill progression, all of which support sustained equipment demand. The photography side will remain the core volume, but the consumer drone industry is expanding into a more participatory hardware category that includes competition, simulation, and learning. That matters because users who start with FPV often move into other aircraft types as their confidence grows. The result is that the consumer drones market is broadening from a camera tool into a more varied personal flight platform.

Geography Analysis

North America accounted for 37.65% of global revenue in 2025, making it the largest regional market for consumer drones. The region benefits from a large installed base of recreational users and a culture that readily blends travel, outdoor activities, and digital content creation. The FAA said there were more than 860,000 registered UAS as of August 2024 in its Drone Integration Concept of Operations, which shows the scale of the underlying user base.[5] That same document also points toward a future operating framework that could widen drone use cases over time. In the near term, the consumer drones market in North America remains shaped by compliance requirements, upgrade cycles, and strong demand from creator households.

Asia-Pacific is forecast to grow at a 15.01% CAGR through 2031, making it the fastest-growing regional market for consumer drones. China remains the central manufacturing and product development base for consumer drones, providing the region with strong supply depth and rapid product refresh cycles. India is also becoming more relevant as policy attention increases, and the user base expands, with the Ministry of Civil Aviation releasing the Draft Civil Drone Bill 2025 in September 2025. Japan and Australia add support through enthusiastic demand, outdoor recreation, and higher acceptance of premium electronics.

Europe remains a mature yet steadily growing part of the consumer drones market because buyers benefit from clearer cross-border operating rules and a larger pool of compliant products. France, Germany, and the UK anchor demand, while Eastern Europe is more uneven because trade conditions and purchasing power differ by country. South America is still smaller in revenue terms, but falling import prices and wider access to affordable models are improving entry conditions. The Middle East and Africa remain the earliest-stage region, with Gulf markets and South Africa as the clearest demand pockets in the broader consumer drones market.

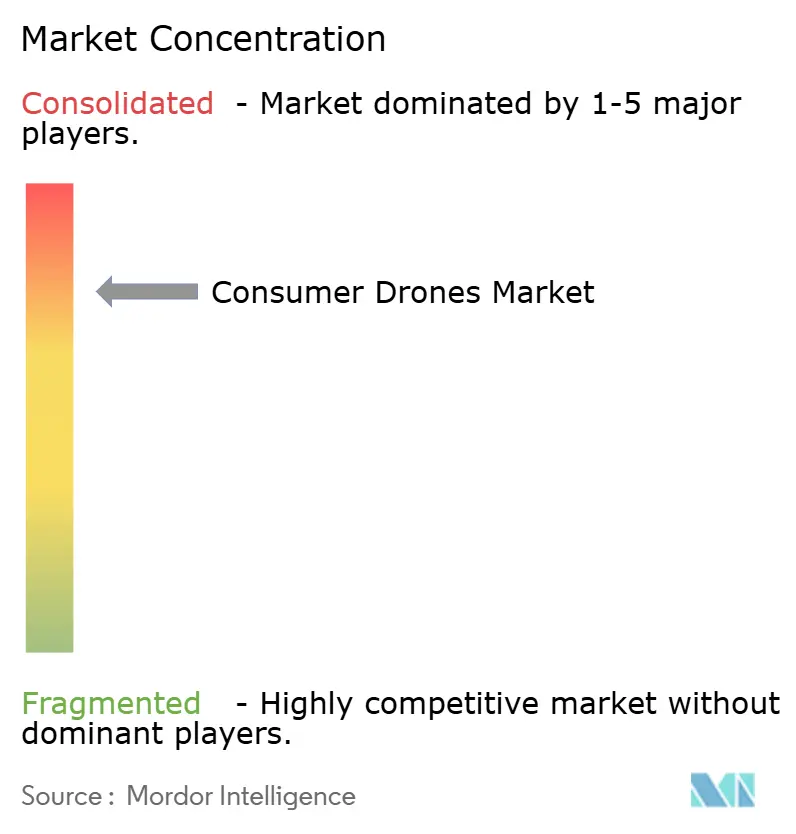

Competitive Landscape

The consumer drones market remains concentrated at the top of the category because one ecosystem player still sets the pace on product breadth, software integration, and launch frequency. DJI continues to cover entry, travel, and FPV needs with a product stack that is difficult for most rivals to match at the same speed. In April 2026, DJI launched the Lito 1 and Lito X1 as beginner-focused sub-250 g drones, expanding its reach to first-time creators and casual users. In September 2025, DJI also raised imaging quality in lightweight devices with the Mini 5 Pro, featuring a 1-inch CMOS sensor. Those moves show why the consumer drones market is still being shaped by a leader that competes across several price bands.

Below the leading tier, the rest of the consumer drones market is split across brands that usually specialize rather than dominate. Some companies compete on lower prices and e-commerce reach, while others focus on FPV, privacy-sensitive buyers, or compliance-oriented niches. That structure makes feature density important, but it also means software ease and after-sales support can decide whether a brand keeps a user beyond the first purchase.

Competition is therefore moving beyond hardware lists and toward ecosystem control. A brand that offers intuitive flight apps, dependable firmware support, and a broad accessory range can keep buyers on its platform longer than one that competes solely on camera specifications. Rivals still have openings in entry pricing, FPV specialization, education-focused products, and markets where compliance or local sourcing matters more than full ecosystem depth. The consumer drones market is also likely to remain uneven by region, because regulatory treatment and distribution models differ sharply across North America, Europe, and Asia-Pacific. That leaves room for smaller brands, but the top layer of competition still favors companies with scale, software depth, and a consistent release cycle.

Consumer Drones Industry Leaders

SZ DJI Technology Co., Ltd.

Skydio, Inc.

Autel Robotics Co., Ltd.

Yuneec (ATL Drone)

Parrot Drones SAS

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: DJI launched the Lito 1 and Lito X1 consumer drones, a new beginner-friendly sub-250 g series, targeted at first-time aerial creators, expanding DJI's consumer addressable market to include social media content novices seeking a regulatory-exempt, obstacle-aware entry platform.

- March 2026: DJI launched the Avata 360, a flagship FPV drone featuring dual 1-inch-equivalent CMOS sensors, 8K/60fps 360° video, and O4+ 20 km transmission, with global availability beginning April 2026. This release marks DJI's entry into the 360° immersive FPV category, directly competing with Antigravity's A1, launched in late 2025.

- January 2026: IATA's mandatory 30% state-of-charge restriction for Li-ion battery shipments entered into force under the 67th Dangerous Goods Regulations edition, materially increasing logistics complexity for cross-border consumer drone e-commerce and requiring supply chain process redesign from manufacturers shipping battery-installed units.

Global Consumer Drones Market Report Scope

Consumer drones cater to personal, non-commercial needs, focusing mainly on aerial photography, videography, and recreational flying. Ranging from entry-level "toy" drones priced under USD 100 to advanced platforms with 4K/8K cameras that can cost over USD 500, these user-friendly, often multi-rotor devices are popular among hobbyists and creators.

The consumer drones market is segmented by product type, light range, weight class, application, and geography. By product range, the market is segmented into multi-rotor, fixed-wing, and hybrid. By flight range, the market is segmented into less than 4 km, 4 to 8 km, and more than 8 km. By weight class, the market is segmented into nano/micro, mini, small, and medium. By application, the market is segmented into photography and videography, racing and sports, recreational, environmental and wildlife observation, and education and training. The report also covers the market sizes and forecasts for the consumer drones market in major countries across different regions. For each segment, the market size is provided in terms of value (USD).

| Multi-Rotor |

| Fixed-Wing |

| Hybrid |

| Less than 4 km |

| 4 to 8 km |

| More than 8 km |

| Nano/Micro (Less than 250 g) |

| Mini (250 g to Less than 2 kg) |

| Small (2 to Less than 5 kg) |

| Medium (More than 5 kg) |

| Photography and Videography |

| Racing and Sports |

| Recreational |

| Environmental and Wildlife Observation |

| Education and Training |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Product Type | Multi-Rotor | ||

| Fixed-Wing | |||

| Hybrid | |||

| By Flight Range | Less than 4 km | ||

| 4 to 8 km | |||

| More than 8 km | |||

| By Weight Class | Nano/Micro (Less than 250 g) | ||

| Mini (250 g to Less than 2 kg) | |||

| Small (2 to Less than 5 kg) | |||

| Medium (More than 5 kg) | |||

| By Application | Photography and Videography | ||

| Racing and Sports | |||

| Recreational | |||

| Environmental and Wildlife Observation | |||

| Education and Training | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the 2031 revenue outlook for consumer drones?

The consumer drones market is forecast to reach USD 13.10 billion by 2031, rising from USD 7.08 billion in 2026 at a 13.11% CAGR.

Which product type leads sales today?

Multi-rotor drones lead the category with 70.11% revenue share in 2025 because they fit photography, travel, and casual flying needs well.

Which application is growing the fastest?

Racing and sports is the fastest-growing application, with a projected 14.56% CAGR through 2031, helped by organized FPV leagues and repeat enthusiast demand.

Why are drones under 250 g so important?

They simplify ownership and use for recreational buyers in key markets, and that has pushed nano and micro drones to 53% of 2025 revenue.

Which region offers the strongest growth outlook?

Asia-Pacific is projected to expand at 15.01% CAGR through 2031, supported by manufacturing depth, product refresh cycles, and rising adoption in major countries.

What are the main risks affecting future demand?

The main constraints are tighter lithium battery shipping rules, crowded spectrum in dense environments, privacy concerns, and uneven service support capacity.

Page last updated on: