Drone Services Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 29.90 Billion |

| Market Size (2030) | USD 109.25 Billion |

| Growth Rate (2025 - 2030) | 29.58% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Drone Services Market Analysis by Mordor Intelligence

The drone services market size reached USD 29.9 billion in 2025 and is projected to climb to USD 109.246 billion by 2030, reflecting a 29.58% CAGR over the forecast horizon. Regulatory fast-tracking, AI-driven data analytics, and cost-efficient Beyond Visual Line of Sight (BVLOS) approvals are converging to propel enterprise adoption across the energy, construction, agriculture, and public safety sectors. North America remains the revenue leader, driven by the momentum of FAA waivers. At the same time, the Asia-Pacific region is expected to deliver the steepest growth as China and other economies open low-altitude corridors for commercial operations. Energy utilities keep drone fleets busy with condition-based maintenance that cuts grid inspection costs by more than half and raises anomaly-detection accuracy by 78%. Hybrid Vertical-Take-Off-and-Landing (VTOL) designs, which offer an 800 km range and satellite command links, extend the commercial radius into offshore, mountainous, and desert regions.

Key Report Takeaways

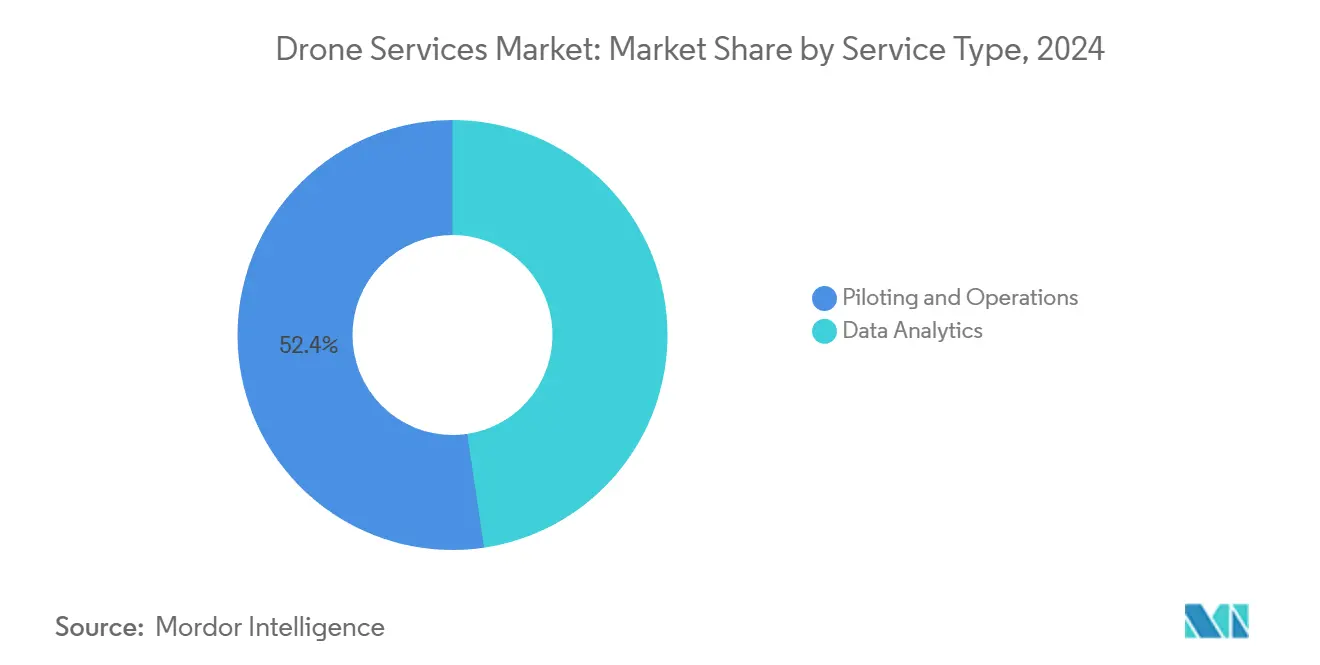

- Piloting and operations held 52.35% of the drone services market share in 2024, while data analytics is forecasted to accelerate at a 31.34% CAGR to 2030.

- Energy and utilities captured 32.18% of revenue in 2024, whereas infrastructure and construction are poised to expand at a 30.14% CAGR through 2030.

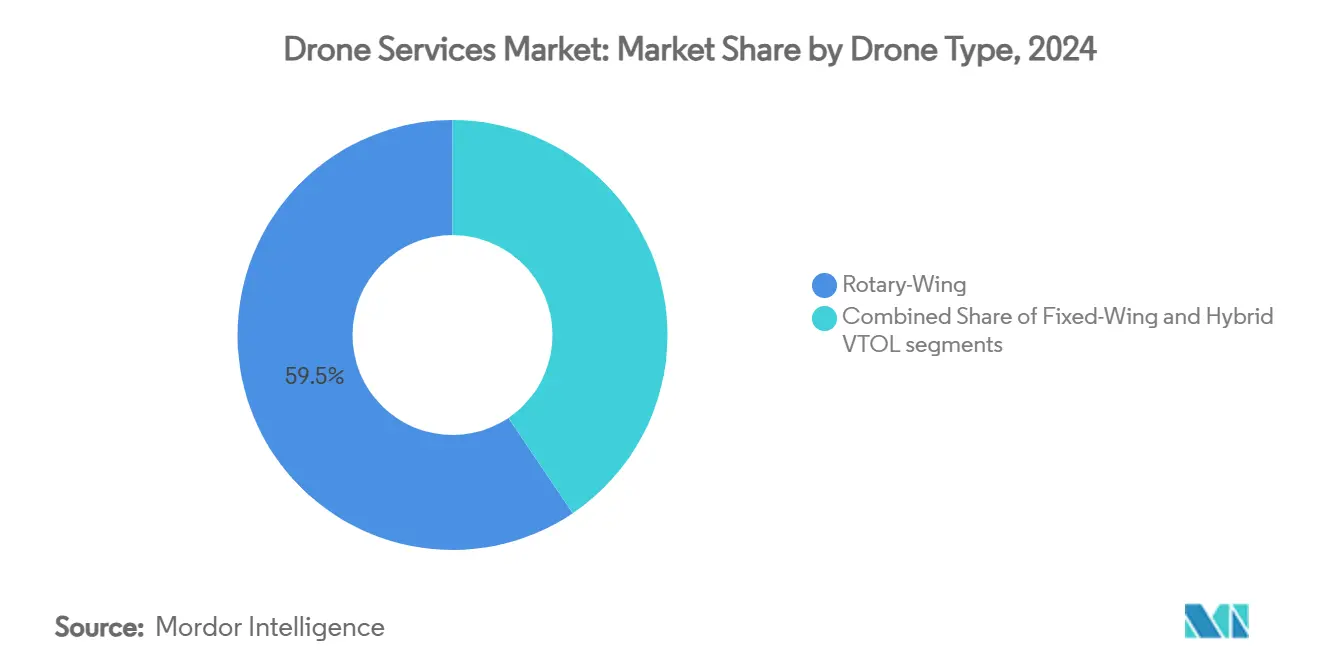

- Rotary-wing platforms controlled 59.45% of 2024 sales, but hybrid VTOL systems are projected to advance at a 34.54% CAGR by 2030.

- Visual Line of Sight flights accounted for 53.37% of current activity; BVLOS operations are expected to post a 28.76% CAGR over the outlook period.

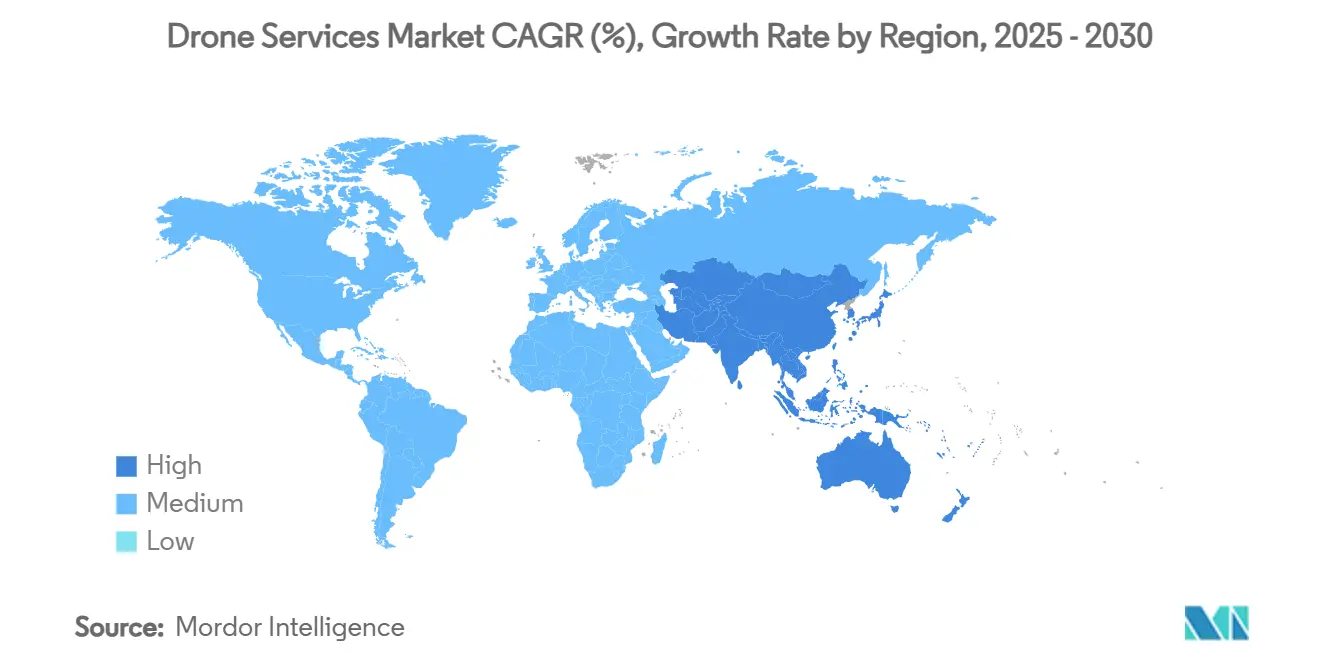

- North America generated 41.97% of 2024 turnover, and Asia-Pacific is on track for a 30.25% CAGR to 2030.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Drone Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for high-frequency asset inspection in energy and utilities | +8.5% | North America and Europe | Medium term (2-4 years) |

| Rapidly declining cost per flight hour for BVLOS operations | +7.2% | North America and EU | Short term (≤ 2 years) |

| Integration of AI-powered analytics unlocking end-to-end solutions | +6.8% | Global | Medium term (2-4 years) |

| Regulatory fast-tracking of urban air mobility corridors | +5.4% | North America and EU | Long term (≥ 4 years) |

| Satellite-to-drone communication enabling offshore coverage | +4.1% | Global offshore energy | Medium term (2-4 years) |

| Carbon-offset programs favouring drone logistics over ground miles | +3.2% | EU, North America, APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for High-Frequency Asset Inspection in Energy and Utilities

Power-line, pipeline, and renewable-asset operators re-engineered maintenance around automated aerial scans. Dominion Energy’s multi-role program inspects solar farms, storm-hit grids, and nuclear power plants around the clock. At the same time, Georgia Power’s fleet flagged 5,174 anomalies across 7,000 structures, triple the count achieved by ground crews, and carved 60% from annual O&M budgets.[1] T&D World Staff, “How Drones Are Revolutionizing Power Line Inspections: Georgia Power’s Success Story,” tdworld.com Methane-sniffing payloads extend coverage to leak-prone pipelines, meeting tightening environmental rules and protecting shareholder value. The outcome is a shift from reactive fixes to predictive lifecycle management, which lengthens asset service life and reduces outage penalties.

Rapidly Declining Cost per Flight Hour for BVLOS Operations

Transport Canada removed special-flight certificates for Level 1 complex BVLOS sorties in November 2025, collapsing lead times and compliance spending. The FAA’s forthcoming Part 108 framework mirrors that flexibility. At the same time, Iridium’s L-band link underpinned the first waiver for remote pipeline patrols in the United States, cementing reliable command-and-control pathways.[2]Iridium Communications Inc., “Iridium Connected Drones Granted First FAA Waiver for BVLOS Commercial Operations,” iridium.com Combined with 24/7 drone-in-a-box launchers, end-to-end mission costs land well below crewed helicopter benchmarks, opening previously marginal business cases across sparsely populated corridors and offshore rigs.

Integration of AI-Powered Analytics Unlocking End-to-End Solutions

Computer-vision models embedded on edge processors now classify structural faults, crop stress, or emergency-scene hazards in real time, shifting drones from data collectors to decision-makers. Warehouse operators such as Anyline compress full-bay barcode audits into single-operator shifts, while ag-spray systems curb pesticide volumes by 30% without yield penalties.[3]MDPI Editors, “A Review of Drone Technology and Operation Processes in Agricultural Crop Spraying,” mdpi.com Construction teams overlay LiDAR meshes on BIM files to surface millimeter-scale deviations, avoiding costly rework and keeping schedules intact. These AI workflows raise switching costs and solidify platform stickiness.

Regulatory Fast-Tracking of Urban Air Mobility Corridor

EASA’s May 2024 AAM rule set, the FAA’s powered-lift SFAR, and Florida’s vertiport-friendly Senate Bill 1662 jointly craft a predictable pathway for eVTOL passenger and cargo lanes.[4]European Union Aviation Safety Agency, “Air Taxis as Urban Transport,” easa.europa.eu Public sentiment already skews positive, with 83% of Europeans supporting urban air taxis. States such as Oklahoma forecast USD 5.6 billion in AAM-linked activity and 4,600 new jobs by 2045, underscoring the economic magnetism of corridor authorization surrounding major metros.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented regulatory standards across countries | −4.8% | Global | Long term (≥ 4 years) |

| Limited battery endurance for heavy-lift drones | −3.6% | Global logistics | Medium term (2-4 years) |

| Public privacy and data-protection concerns | −2.4% | EU and North America | Short term (≤ 2 years) |

| Persistent GPS jamming in conflict zones | −1.9% | Eastern Europe and Middle East | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Fragmented Regulatory Standards Across Countries

Operators juggling FAA, EASA, and emerging-market rule books must secure multiple pilot certifications, hardware labels, and insurance endorsements, inhibiting cross-border scale. Canada’s 2025 overhaul diverges from EU class-marking schemes, forcing fleets to carry redundant documentation and inflating compliance overhead. The asynchronous rollout delays enterprise RFPs for continental delivery corridors and keeps smaller fleets domestic.

Limited Battery Endurance for Heavy-Lift Drones

Lithium-ion packs hit energy-density ceilings that cap realistic payload-to-flight-time ratios. Experimental lithium-sulfur chemistries promise 2x storage per kilogram, yet remain at the prototype stage. A 20 kg multirotor today averages 45 minutes aloft, making two-way trips above 15 km commercially marginal. Until cells improve or hybrid powertrains mature, frequent swap-outs and cold-weather derating restrain logistics scaling.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Platform Dominance, MRO Upswing

Piloting and operations captured 52.35% of the drone services market share in 2024, underscoring the labor-intensive oversight still required under most aviation rules. Data Analytics is projected to advance at a 31.34% CAGR through 2030, the quickest pace among all service categories, signaling a shift toward monetizing insight rather than flight hours. The accelerating uptake of autonomous docking stations from suppliers such as Percepto and Skydio is expected to reduce pilot demand and compress the cost base of traditional operations. Programs like Elk Grove, California’s Drone as First Responder 2.0 already allow one operator to supervise several autonomous aircraft simultaneously, demonstrating how centralized Real-Time Information Centers can scale coverage without proportional labor growth. As regulations evolve toward corporate-oversight models, the drone services market size for piloting and operations is expected to grow more slowly than analytics-centric offerings, even as it remains vital for safety management.

Edge computing and 5G links now enable drones to process LiDAR, thermal, and multispectral feeds during flight, converting raw pixels into actionable work orders before landing. Airborne Ultralight Spectrometer technology exemplifies this evolution by detecting methane and CO2 in real-time, enabling firms such as TotalEnergies to align with ambitious emissions goals. Computer-vision models routinely deliver 78% higher fault-detection accuracy than manual reviews while trimming electrical downtime by 35%. These gains reduce data-handling costs and speed decision cycles, strengthening the competitive position of providers offering end-to-end analytics platforms. Enterprises consequently view insight delivery as the core value driver, relegating flight execution to an enabling function rather than the primary revenue source.

By Industry Vertical: Energy Leadership Versus Construction Acceleration

Energy and utilities delivered 32.18% of 2024 turnover, underlining the segment’s central role in grid-modernisation and methane-leak compliance mandates. The drone services market share for this vertical benefits from steady inspection cycles that convert CAPEX into predictable OPEX budgets. Drones equipped with optical zoom and thermal sensors review conductors, insulators, and right-of-way vegetation, trimming helicopter charter fees, and reducing crew hazard exposure.

Infrastructure and construction commands the fastest growth at 30.14% CAGR. BIM-friendly photogrammetry and LiDAR models compared against as-planned drawings identify millimetre discrepancies early, preventing costly rework. Megaprojects in APAC and the Middle East now embed weekly aerial scans as contractual deliverables, embedding drones into digital-twin workflows that cut schedule drift.

By Drone Type: Rotary Dominance Challenged by Hybrid Innovation

Rotary-wing craft retained 59.45% of 2024 sales thanks to superior hovering and vertical lift, suiting close-range inspections and precision drops. Their modularity allows payload swaps, such as cameras, gas detectors, and sprayers, within minutes, keeping utilisation high. However, a limited range keeps the mission scope local.

Hybrid VTOL airframes are expanding at a 34.54% CAGR, marrying fixed-wing cruise efficiency with rotary lift. Horizon Aircraft’s Cavorite X7 achieved transition flight at 450 km/h and 800 km range, marking a turning point for inter-city cargo corridors. The drone services market size for hybrid platforms could exceed USD 20 billion by 2030 if certification timelines are met.

By Operating Range: VLOS Now, BVLOS Next

VLOS holds 53.37% of 2024 activity, buoyed by easily obtainable licenses and immediate commercial use cases, such as real estate shoots and small farm spraying. The segment remains relevant for dense urban airspace where regulators limit autonomous manoeuvres.

BVLOS is advancing at a 28.76% CAGR and will likely overtake VLOS once Part 108 and similar rules codify corporate agency oversight. The drone services market size for BVLOS deliveries of medical supplies alone is forecasted to pass USD 6 billion by 2030, spurred by hospitals like the Cleveland Clinic planning routine prescription drops.

Geography Analysis

North America retained 41.97% of 2024 revenue thanks to coherent federal guidance, insurance acceptance, and a deep base of enterprise early adopters. The FAA logged 300 Drone-as-First-Responder (DFR) program submissions by mid-2025, illustrating municipal appetite for autonomous incident assessment.[5]Police1, “Drone as First Responder Programs Expand in 2025,” police1.com Utilities such as Georgia Power and Dominion Energy provide textbook ROI cases, while Oklahoma forecasts a USD 5.6 billion boost from advanced-air-mobility corridors.

The Asia-Pacific region is projected to grow at a 30.25% CAGR through 2030. Manufacturing scale keeps hardware prices low, and governments in China, Japan, South Korea, and India fund pilot corridors covering logistics, healthcare, and agriculture. Land-survey bookings and precision-spray packages anchor sizable order books, with survey operators expecting the regional drone services market size to exceed USD 2.5 billion by 2033.

Europe combines EASA’s harmonized rules with a strong sustainability mandate. More than 1.6 million operators are registered under the common framework, and 83% of surveyed citizens view air taxis positively. Carbon-pricing mechanisms and dense urban topography give drones a clear advantage for short-haul deliveries. Pioneering offshore projects in the North Sea and Baltic expand the use cases for heavy-lift beyond inspection to include spare-parts logistics.

Competitive Landscape

The drone services market remains moderately fragmented, with the top five firms controlling a significant share of global revenue; however, consolidation is underway. Axon's USD 300 million acquisition of Dedrone boosts public-safety offerings by fusing gunshot detection with counter-UAS analytics. Volatus Aerospace's merging with Drone Delivery Canada illustrates supply-chain rationalisation aimed at nationwide parcel corridors.

Traditional aerospace entrants, such as Robinson Helicopter's acquisition of Ascent AeroSystems, indicate that legacy OEMs are diversifying their rotorcraft markets with unmanned portfolios. Start-ups differentiate themselves through AI, edge processing, and specialized payloads, such as hyperspectral imagers for mining or ultralight gas-analysis spectrometers for environmental audits.

Providers able to showcase multi-year incident-free flight logs, robust BVLOS authorisations, and turnkey data platforms occupy the premium tier of the drone services market. Customers are increasingly awarding bundled contracts that combine flight operations, cloud analytics, and maintenance, thereby reducing the number of vendors and increasing switching costs.

Drone Services Industry Leaders

Aerodyne Group Limited

Terra Drone Corporation

Cyberhawk Innovations Limited

Wing Aviation LLC

DroneDeploy, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Arrive AI, specializing in autonomous delivery networks, partnered with Skye Air Mobility, India's primary hyperlocal drone delivery platform. The collaboration focuses on implementing automated delivery solutions across India's expanding drone technology market.

- April 2025: Kansas drone sprayers treated 10.3 million acres, generating USD 215 million in farm revenue.

- April 2025: Draganfly Inc., a developer of drone solutions and systems, was selected by SafeLane Global Ltd. as its primary unmanned aerial systems (UAS) and aerial survey provider.

- November 2024: Salam Kisan, an agri-tech platform, has secured the tender from the Government of Maharashtra, India, and the Maharashtra Agro-Industries Development Corporation (MAIDC) for drone spraying services. Through its drone-as-a-service model, the company aims to expand precision farming across the state.

Global Drone Services Market Report Scope

| Piloting and Operations |

| Data Analytics |

| Construction and Infrastructure |

| Agriculture and Forestry |

| Energy and Utilities |

| Law Enforcement and Public Safety |

| Medical and Parcel Delivery |

| Others (Mining, Real-estate, Media) |

| Rotary-wing |

| Fixed-wing |

| Hybrid VTOL |

| Visual Line-of-Sight (VLOS) |

| Beyond Visual Line-of-Sight (BVLOS) |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Service Type | Piloting and Operations | ||

| Data Analytics | |||

| By End User Industry | Construction and Infrastructure | ||

| Agriculture and Forestry | |||

| Energy and Utilities | |||

| Law Enforcement and Public Safety | |||

| Medical and Parcel Delivery | |||

| Others (Mining, Real-estate, Media) | |||

| By Drone Type | Rotary-wing | ||

| Fixed-wing | |||

| Hybrid VTOL | |||

| By Operating Range | Visual Line-of-Sight (VLOS) | ||

| Beyond Visual Line-of-Sight (BVLOS) | |||

| By Geography (Value) | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the drone services market today?

The drone services market size reached USD 29.9 billion in 2025 and is projected to hit USD 109.246 billion by 2030.

Which segment dominates the drone services market?

Piloting and operations currently lead with 52.35% of revenue as labor-intensive oversight is still required under most aviation rules.

What is the fastest-growing application area?

Infrastructure and construction services are forecast to grow at a 30.14% CAGR through 2030 as AI-enabled site audits become standard.

When will BVLOS operations become mainstream?

The FAA’s Part 108, expected by March 2026, should standardise BVLOS rules; waiver volumes already indicate rapid scaling across North America.

What limits heavy-lift drone deployments?

Battery energy-density ceilings restrict payload-range combinations, though hybrid-electric and hydrogen propulsion systems are in development.

Which region will see the highest growth?

Asia-Pacific is set to expand at a 30.25% CAGR, propelled by dedicated airspace corridors, manufacturing scale, and vast rural delivery needs.

Page last updated on: