Inspection Drones Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

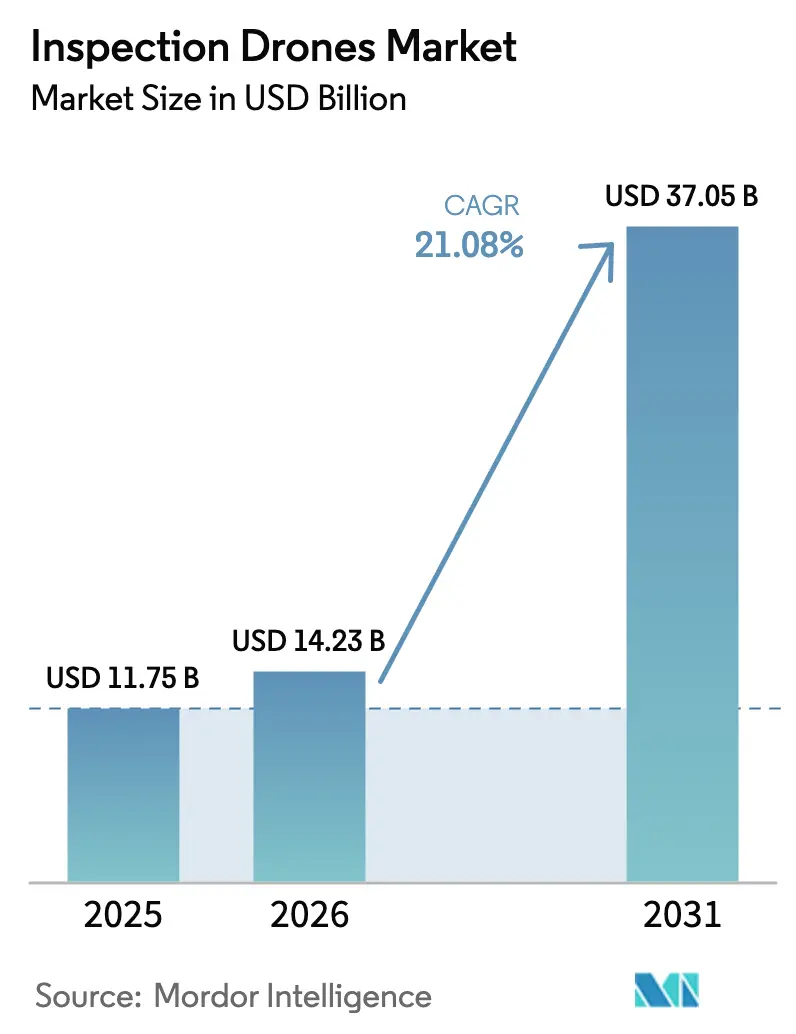

| Market Size (2026) | USD 14.23 Billion |

| Market Size (2031) | USD 37.05 Billion |

| Growth Rate (2026 - 2031) | 21.08% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Inspection Drones Market Analysis by Mordor Intelligence

The inspection drones market size was valued at USD 11.75 billion in 2025 and estimated to grow from USD 14.23 billion in 2026 to reach USD 37.05 billion by 2031, at a CAGR of 21.08% during the forecast period (2026-2031). Regulatory momentum behind beyond-visual-line-of-sight (BVLOS) rules, falling sensor and battery prices, and the need to modernize aging infrastructure are accelerating procurement decisions and reshaping competitive dynamics across the inspection drone market. Hybrid airframes that marry vertical-take-off functionality with fixed-wing cruise efficiency redefine mission economics, while software-centric offerings turn raw imagery into predictive maintenance insights. Utilities, oil and gas operators, and public-safety agencies are prioritizing long-range autonomous patrols, and satellite links now extend operational envelopes well beyond cellular coverage. Although cyber risks and patchwork global regulations temper near-term adoption, the inspection drone industry continues attracting capital and partnerships focusing on AI, cloud analytics, and fleet orchestration.

Key Report Takeaways

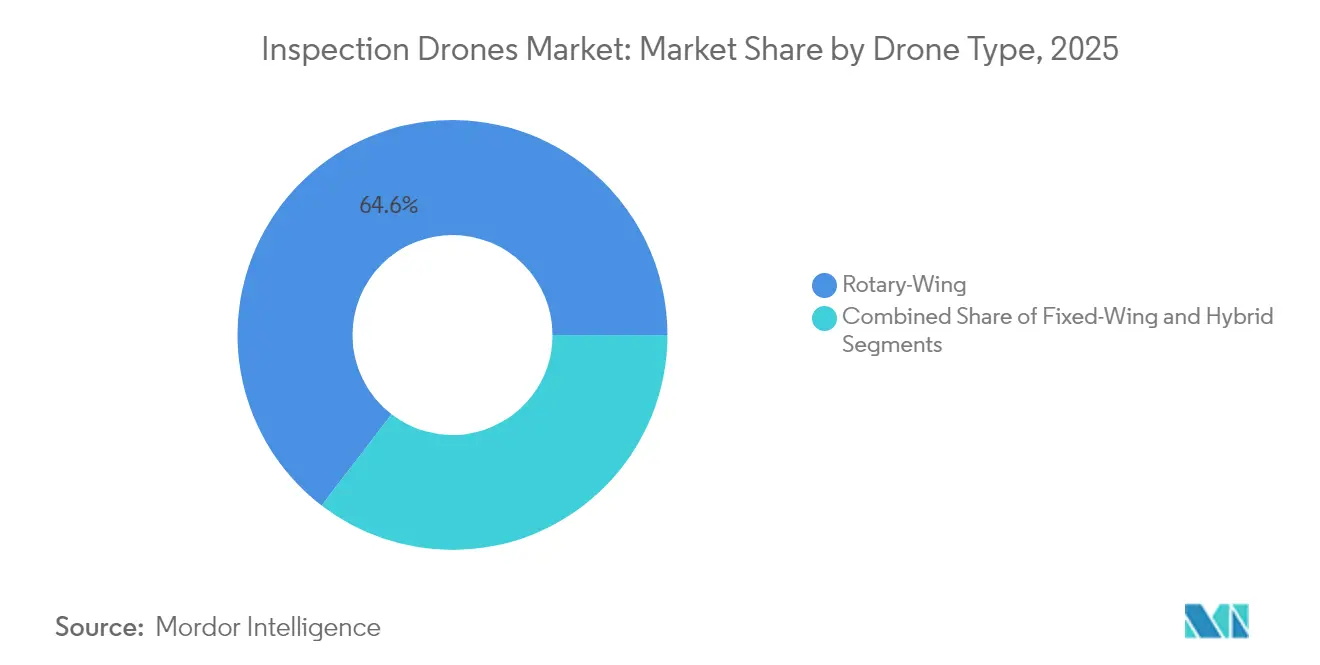

- By drone type, rotary-wing platforms led with 64.58% inspection drone market share in 2025; hybrid drones are projected to expand at a 22.94% CAGR through 2031.

- By end-use industry, agriculture held 26.94% of the inspection drone market size in 2025, whereas law enforcement is advancing at a 23.35% CAGR to 2031.

- By solution, services accounted for 42.45% of revenue in 2025; software platforms recorded the fastest growth at 21.74% CAGR through 2031.

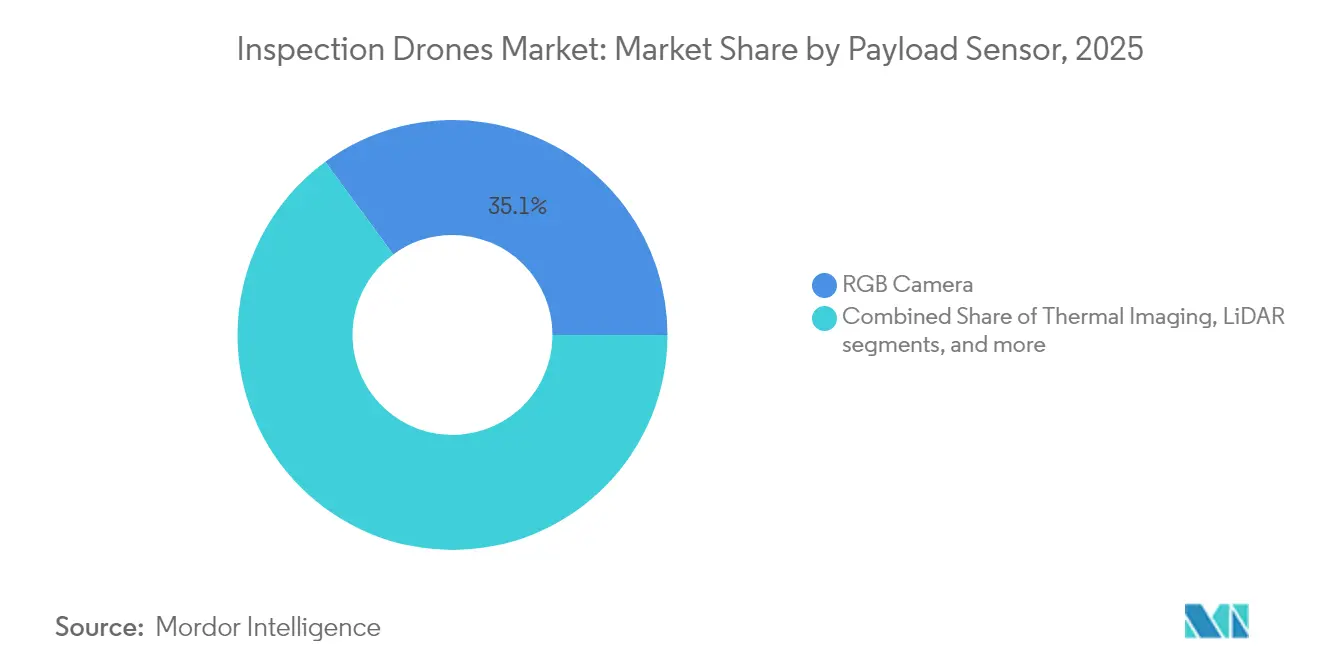

- By payload, RGB cameras captured 35.08% of the inspection drone market size in 2025, while LiDAR is forecasted to grow at a 22.48% CAGR.

- By range capability, short-range flights (less than 5 km) commanded 52.04% of demand in 2025, but the medium range (5–20 km) band is rising at a 22.12% CAGR.

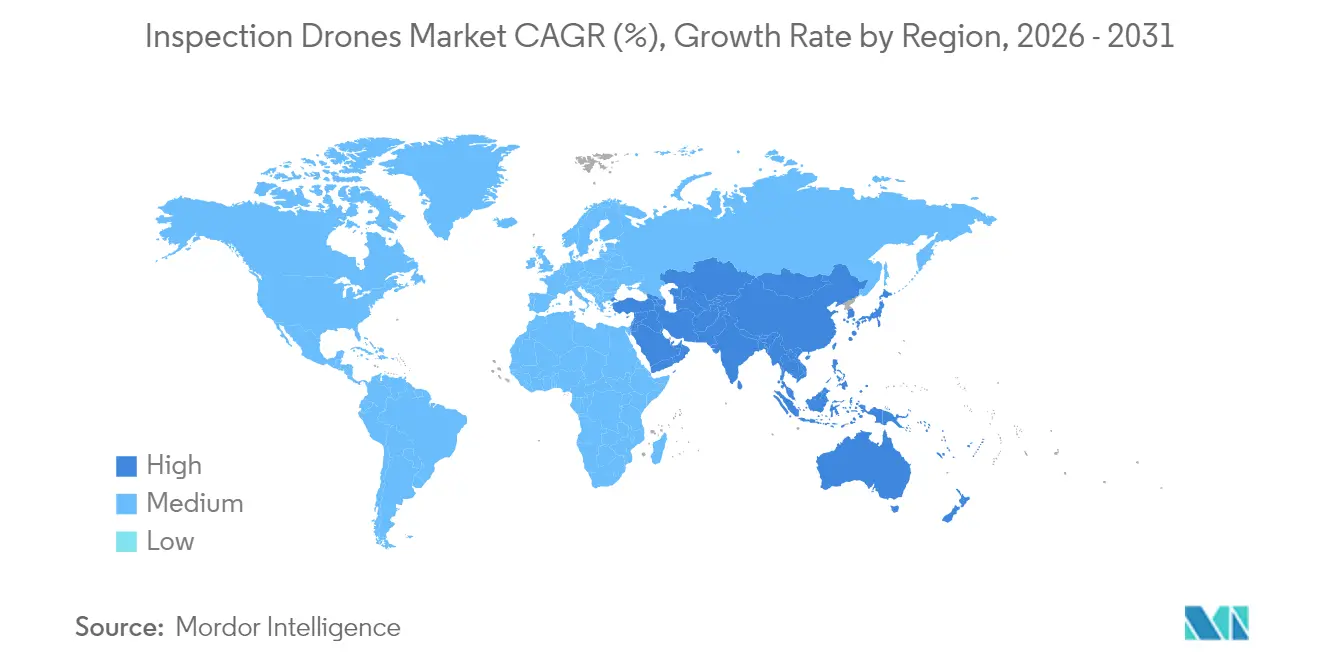

- By geography, North America contributed 37.32% of global revenue in 2025; Asia-Pacific is poised for a 20.96% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Inspection Drones Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory easing of BVLOS approvals | +4.2% | North America, European Union | Medium term (2-4 years) |

| Falling sensor and battery costs improving ROI | +3.8% | Global, Asia-Pacific cost leadership | Short term (≤2 years) |

| Aging energy infrastructure requiring frequent inspections | +3.1% | North America, European Union | Long term (≥4 years) |

| Integration of AI-enabled defect analytics platforms | +2.9% | Global developed markets | Medium term (2-4 years) |

| Insurance industry adoption of drone derived risk data | +2.4% | North America, European Union, Asia-Pacific | Medium term (2-4 years) |

| Satellite-to-drone comms enabling beyond-grid operations | +1.8% | Remote and offshore sites worldwide | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Regulatory easing of BVLOS approvals

The easing of Beyond Visual Line of Sight (BVLOS) regulations is driving the expansion of the inspection drone market. The Federal Aviation Administration (FAA) increased BVLOS waivers from 1,229 in 2020 to 26,870 in 2023 through waivers, air carrier certificates, and exemptions, indicating increased trust in drone safety and autonomous capabilities within the Inspection Drones Market. In February 2025, DroneDeploy received approval to perform automated BVLOS inspections of critical infrastructure, including data centers, across the United State, further accelerating the Inspection Drones Market. FAA draft rules and Canada’s 2025 amendments eliminate the cost and staffing burden of visual observers, allowing continuous corridor inspections for pipelines and transmission lines, strengthening the Inspection Drones Market outlook.The Elk Grove Police Department has already flown more than 1,000 city-wide BVLOS missions with an average response time of 3.5 minutes.[1]Fritz Reber & Nate Lange, “The Dawn of DFR 2.0: Elk Grove PD Flies into the Future,” Police1, police1.com Cyberhawk’s nationwide US waiver doubled its daily asset-survey capacity, underscoring the commercial leverage created by BVLOS flexibility.[2]Abi Wylie, “BVLOS Waiver Granted for Expanded Remote Drone Operations,” Unmanned Systems Technology, unmannedsystemstechnology.com Similar liberalization is underway across the European Union, setting the stage for truly continental service networks. Reducing reliance on visual observers and case-by-case waivers decreases operational bottlenecks and deployment costs, enabling wider adoption of drones for long-distance asset inspection. This regulatory easing of Beyond Visual Line of Sight (BVLOS) operations drives market growth.

Falling sensor and battery costs improving ROI

The decreasing costs of sensors and batteries drive the increased adoption of inspection drones across industries. Mass production and technological progress have reduced the prices of high-resolution cameras, thermal imaging sensors, LiDAR modules, and advanced navigation systems. Additionally, improvements in lithium-ion and solid-state battery technologies have enhanced energy density while lowering cost per watt-hour, resulting in extended flight times and improved mission productivity. Lithium-sulfur (Li-S)cells exceeding 285 Wh/kg extend endurance by up to 100%, enabling full-day patrols of isolated infrastructure without field swaps. Hyperspectral payload miniaturization now brings farm-level nutrient profiling within reach of mid-tier growers, and integrated gas sensors remove calibration stops that once discouraged confined-space inspections. The cost curve strengthens the inspection drone market value proposition against manned helicopters. Cost efficiency improves end-users' return on investment (ROI) by reducing capital expenditures and minimizing equipment replacements and downtime. Small and mid-sized enterprises that previously could not afford drone inspections are now adopting this technology. The combination of reduced hardware costs and enhanced performance makes drone-based inspections more accessible, contributing to market growth.

Aging energy infrastructure requiring frequent inspections

The global inspection drone market is expanding due to aging energy infrastructure, including oil pipelines, transmission towers, wind turbines, and offshore platforms. These assets, installed decades ago, are experiencing structural fatigue, corrosion, and wear. Increased regulatory requirements and safety standards compel energy operators to perform more frequent and thorough inspections. More than 70% of North American transmission assets pre-date 1985, prompting utilities to shift from manual climbs to autonomous drone sweeps that compress inspection cycles from weeks to days.[3]Amy Fischbach, “Harnessing the Power of AI for Inspections,” T&D World, tdworld.com European grid operators replicate these strategies as renewable integration raises reliability thresholds. Manual inspection methods are costly, time-consuming, and hazardous. Inspection drones enable faster, safer, and more cost-effective assessments of hard-to-reach infrastructure. These drones provide high-resolution imagery, thermal data, and real-time diagnostics that improve maintenance planning and failure prevention. The increasing use of drones to monitor aging infrastructure drives demand across the inspection drone market.

Integration of AI-enabled defect analytics platforms

AI-enabled defect analytics platforms drive growth in the inspection drone market by converting inspection data into actionable insights, significantly enhancing the Inspection Drones Market landscape. These platforms use machine learning algorithms to analyze visual, thermal, and LiDAR data collected during infrastructure inspections, creating new value streams in the Inspection Drones Market.The technology detects micro-cracks, corrosion, deformation, and other defects faster and more consistently than manual analysis methods, improving efficiency across the Inspection Drones Market. Integrating AI analytics reduces manual analysis time, minimizes errors, and enables predictive maintenance strategies. These platforms transform inspections into digital processes by integrating drone workflows, providing real-time alerts and trend analysis for asset managers across the Inspection Drones Market. Computer-vision models now detect cracks, corrosion, and thermal anomalies with up to 85% accuracy, converting imagery into actionable maintenance tickets within minutes.[4]Skydio, “Elevate Inspections with AI-Powered Drones: Skydio & Levatas Partnership,” Skydio, skydio.com Generative AI augments limited training datasets to automate tunnel and substation assessments, paving the way for fully unmanned workflows within the Inspection Drones Market.The increasing demand for analytics capabilities drives drone adoption and AI-powered software development, contributing to expansion in the Inspection Drones Market.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented global regulatory frameworks | -2.1% | Global, with varying regional compliance costs | Medium term (2-4 years) |

| Cyber-security vulnerabilities in drone cloud pipelines | -1.8% | Global, with heightened concerns in critical infrastructure | Short term (≤ 2 years) |

| Limited endurance for heavy-payload inspection missions | -1.5% | Global, particularly affecting long-range applications | Short term (≤ 2 years) |

| Public opposition near critical infrastructure | -1.2% | North America and Europe, with privacy and security concerns | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fragmented Global Regulatory Frameworks

The fragmented nature of global drone regulations constrains the growth of the inspection drone market and poses structural challenges for the Inspection Drones Market. Despite increasing demand for drone inspections across industries, varying regulations between and within countries create operational challenges for drone service providers and manufacturers in the Inspection Drones Market. Different requirements for flight permissions, beyond visual line of sight operations, data privacy, and pilot certification result in delays, higher compliance costs, and limited operational areas. These regulatory variations particularly affect highly regulated industries such as energy, utilities, and transportation, impacting cross-border projects and the ability to scale drone inspection operations. While the FAA and Transport Canada push ahead, European Union member states maintain divergent licensing and airworthiness rules, and China’s restrictive airspace policies contrast with Japan’s pro-inspection stance. Multinational operators must therefore sustain multiple compliance teams, driving up overhead and complicating logistics for long-range missions that cross borders. The lack of harmonized BVLOS standards curbs expansion plans and discourages smaller entrants. The absence of globally standardized regulations hinders the development of autonomous inspection systems and long-range drone operations. Companies must implement different strategies across various markets, reducing operational efficiency and limiting international expansion.

Cyber-security Vulnerabilities in Drone Cloud Pipelines

Cybersecurity vulnerabilities in drone cloud systems constrain the inspection drone market, particularly as drones integrate with IoT systems and cloud analytics platforms. Inspection drones gather sensitive visual and structural data transmitted through cloud environments for analysis, storage, and reporting. This data transmission creates potential entry points for cyber threats, including unauthorized access, data interception, spoofing, and flight path manipulation. Industries such as energy, defense, and infrastructure face significant risks due to their data confidentiality and operational integrity requirements. De-authentication hacks, GPS spoofing, and man-in-the-middle attacks expose inspection fleets to data theft and mission compromise, especially when imagery is streamed to cloud-based analytics engines. Critical-infrastructure owners remain wary because a single breach can jeopardize national-security assets. As a result, operators must invest in hardened C2 links, end-to-end encryption, and zero-trust architectures, adding costs that can delay or downsize deployment decisions. The lack of standardized encryption protocols and secure data transmission frameworks increases security risks. These vulnerabilities can disrupt operations, result in regulatory penalties, and damage client trust, making cybersecurity a significant challenge for inspection drone adoption in high-risk industries.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drone Type: Hybrid airframes redefine mission envelopes

Rotary-wing aircraft generated 64.58% of 2025 revenue, but hybrid configurations are on track for a 22.94% CAGR through 2031 as operators demand hover stability and 50 km-plus cruise legs. The hybrid surge will lift the inspection drone market size associated with corridor assets such as pipelines and rail lines. At the same time, fixed-wing designs remain essential for very-long-range surveys. Sikorsky’s rotor-blown-wing prototype reaching 86 kn cruise speed evidences the performance upside.

Operational flexibility underpins hybrid adoption. One airframe now handles confined substation scans at dawn and 80-km pipeline overflights in the afternoon, cutting fleet complexity. APAC regional operators have already deployed gas-turbine hybrid eVTOLs to overcome battery limits and humidity derating.

By End-Use Industry: Public-safety momentum complements agriculture scale

Agriculture retained 26.94% of 2025 spending thanks to crop-health and spraying missions, yet law-enforcement budgets are rising fastest at 23.35% CAGR as municipalities formalize drone-as-first-responder (DFR) doctrine. Chula Vista PD’s 20,000-call milestone validates faster arrival and reduced risk for officers. Energy utilities remain perennial clients, while entertainment sectors diversify revenue streams. Convergence accelerates technology diffusion. Thermal imaging perfected for fugitive searches improves livestock welfare monitoring, and multispectral crop indices assist police forensic sweeps. The inspection drone market share led by agriculture will narrow as public-safety projects scale nationally.

By Solution: Software turns data into preventive value

Service contracts captured 42.45% of revenue in 2025, yet software revenue is climbing at 21.74% CAGR as clients favor subscription dashboards that auto-flag defects and create compliance reports. When AI workflows cut image-review labor by 70%, the inspection drone market size generated by SaaS grows even faster than flight-hour totals. Blockchain add-ons now seal inspection evidence for regulators, while quantum-inspired optimizers trim flight-path energy budgets. Hardware commoditization rerates margins. Clients increasingly purchase drones off-the-shelf and license analytics from specialized vendors, prompting service providers to bundle cloud access with field operations to protect their share.

By Payload/Sensor Type: LiDAR adoption accelerates 3D digital twins

RGB cameras held a 35.08% share in 2025, but LiDAR units are expanding at a 22.48% CAGR as asset owners demand sub-centimeter meshing for digital twins. Inspection drone market size linked to LiDAR stems from blade-tip 3D scans that spot millimeter cracks before they propagate. Thermal arrays remain the standard for high-voltage hot-spot detection, whereas hyperspectral rigs move beyond research farms into mineral mapping. Cost decline is decisive. Solid-state LiDAR modules are now priced under USD 8,000, opening adoption to mid-tier service fleets. Integrated gas and chemical sensors unlock confined-space work where RGB imagery alone cannot quantify risk.

By Range Capability: BVLOS unlocks medium-range growth

Flights under 5 km still dominate with 52.04% share, but BVLOS waivers enable 5 to 20 km sorties that soar at 22.12% CAGR and swell the associated inspection drone market revenue. Operators can now finish 320-mile (around 515 km) pipeline patrols in a single day using a relay of medium-range sorties. Long-range missions above 20 km remain niche until harmonized cross-border rules mature. Economics favor medium-range profiles. One drone plus two batteries now replaces a truck-and-staff convoy over remote deserts, trimming logistics costs by up to 40%. Satellite command links guarantee coverage where cellular fades, further widening the attainable customer base.

Geography Analysis

North America delivered 37.32% of 2025 global revenue, driven by progressive FAA policies, grid-modernization investments, and strong venture funding, positioning it as a leader in the Inspection Drones Market.The region’s inspection drone market size also benefits from dense oil-and-gas pipeline networks that demand frequent mapping. Canada’s updated rules let 25 kg drones fly BVLOS without flight certificates, lowering entry barriers.

Asia-Pacific is the fastest climber at 20.96% CAGR through 2031 as China’s manufacturing ecosystem underpins hardware affordability and Japan pilots tunnel-inspection AI. India’s smart-manufacturing incentives stimulate factory-roof, flare-stack, and railway inspections. Partnerships like Terra Drone’s Saudi Aramco expansion illustrate demand spill-over into the Middle East.

Europe maintains steady growth, though national-level pilot licensing and data hosting variances complicate scale. Offshore wind farm deployments in the North Sea and Mediterranean continue to require routine blade and substation checks that favor BVLOS hybrids. Meanwhile, Africa and Latin America have adopted drones for power-line audits, where ground access is difficult.

Competitive Landscape

Market fragmentation persists because client needs vary widely by industry, geography, and data-security requirements. DJI anchors hardware but lacks sector-specific platforms, allowing Cyberhawk Innovations Ltd., Terra Drone Corporation, Aerodyne Group, and Skydio, Inc. to capture value via vertically integrated analytics. Partnerships define strategy: Skydio, Inc. couples its X10 airframe with the Levatas anomaly-detection AI, while Terra Drone teams with Mitsui on offshore tank metrology. New entrants chase AI-first niches. UK-based Hammer Missions raised GBP 1.4 million (USD 1.89 million) to automate façade inspections for US property clients, showing software can open regional doors without in-house drone manufacturing. Satellite-link specialists and battery innovators round out the ecosystem.

Inspection Drones Industry Leaders

SZ DJI Technology Co., Ltd.

Terra Drone Corporation

Aerodyne Group

Cyberhawk Innovations Ltd.

Yuneec (ATL Drone)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: DroneDeploy released new product features including Snapshot, enhanced inspection automation capabilities, and an improved Safety AI system. The update supports local and company-specific safety standards and improves workflows for thermal, visual, and 360-degree site monitoring.

- June 2025: Lamarr.AI partnered with Michigan Central and Newlab to launch a drone monitoring program for municipal buildings in Detroit. The program uses AI-powered aerial inspections to identify energy efficiency improvements in local government facilities.

- May 2025: MFE Inspection Solutions partnered with Skydio and obtained a comprehensive FAA Beyond Visual Line of Sight (BVLOS) waiver. This authorization allows them to conduct remote drone inspections across the United States using Skydio X10 drones and docking stations, enabling remote monitoring demonstrations through automated drone systems.

- May 2025: Terra Drone entered into a memorandum of understanding with Saudi Aramco to conduct drone inspection trials at oil and gas facilities. The agreement outlines plans to implement comprehensive operational monitoring by 2027, potentially establishing one of Terra Drone's most significant inspection contracts.

- March 2025: Sikorsky validated rotor-blown-wing UAS, achieving 40 VTOL transitions and 86 kn cruise for future pipeline patrols

Global Inspection Drones Market Report Scope

| Rotary-Wing Drones |

| Fixed-Wing Drones |

| Hybrid |

| Construction |

| Agriculture |

| Energy and Power |

| Entertainment |

| Law Enforcement |

| Other Applications |

| Hardware |

| Software |

| Services |

| RGB Camera |

| Thermal Imaging |

| LiDAR |

| Multispectral/Hyperspectral |

| Gas and Chemical Sensors |

| Short Range (Less than 5 km) |

| Medium Range (5 to 20 km) |

| Long Range (Greater than 20 km) |

| North America | United States | |

| Canada | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Drone Type | Rotary-Wing Drones | ||

| Fixed-Wing Drones | |||

| Hybrid | |||

| By End-Use Industry | Construction | ||

| Agriculture | |||

| Energy and Power | |||

| Entertainment | |||

| Law Enforcement | |||

| Other Applications | |||

| By Solution | Hardware | ||

| Software | |||

| Services | |||

| By Payload | RGB Camera | ||

| Thermal Imaging | |||

| LiDAR | |||

| Multispectral/Hyperspectral | |||

| Gas and Chemical Sensors | |||

| By Range Capability | Short Range (Less than 5 km) | ||

| Medium Range (5 to 20 km) | |||

| Long Range (Greater than 20 km) | |||

| By Geography | North America | United States | |

| Canada | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the inspection drone market and its growth outlook?

The inspection drones market was valued at USD 14.23 billion in 2026 and is projected to reach USD 37.05 billion by 2031, advancing at a 21.08% CAGR.

Which factors are driving the fastest adoption of inspection drones?

The strongest growth catalysts are regulatory easing of BVLOS flights, falling battery and sensor costs, mandatory inspections for aging energy infrastructure, and the rollout of AI-powered defect-analytics platforms.

Why are hybrid drones gaining traction over traditional rotary-wing models?

Hybrid airframes offer VTOL agility plus fixed-wing cruise efficiency, enabling longer-range corridor inspections without sacrificing hover capability, and are forecasted to grow at a 22.94% CAGR through 2031.

Which end-use industries currently spend the most on inspection drones?

Agriculture leads with 26.94% market share, but law-enforcement programs are expanding fastest at 23.35% CAGR as cities adopt drone-as-first-responder models.

How are software platforms reshaping the inspection drone value chain?

AI-driven analytics convert imagery into actionable maintenance tasks, reduce manual review hours by up to 70%, and drive the software segment’s 21.74% CAGR—outpacing both hardware and services growth.

What are the main restraints slowing wider drone inspection deployment?

Fragmented global regulations, cybersecurity risks in drone-cloud pipelines, limited endurance for heavy-payload missions, and local privacy opposition near critical infrastructure are key barriers.

Which regions offer the greatest near-term expansion opportunities?

North America maintains the largest revenue share at 37.32% thanks to favorable FAA policies, while Asia-Pacific is the fastest-growing region, projected at a 20.96% CAGR through 2031 as industrialization and supportive regulations accelerate demand.

Page last updated on: