Dental Surgical Instruments Market Size and Share

Market Overview

| Study Period | 2022 - 2031 |

|---|---|

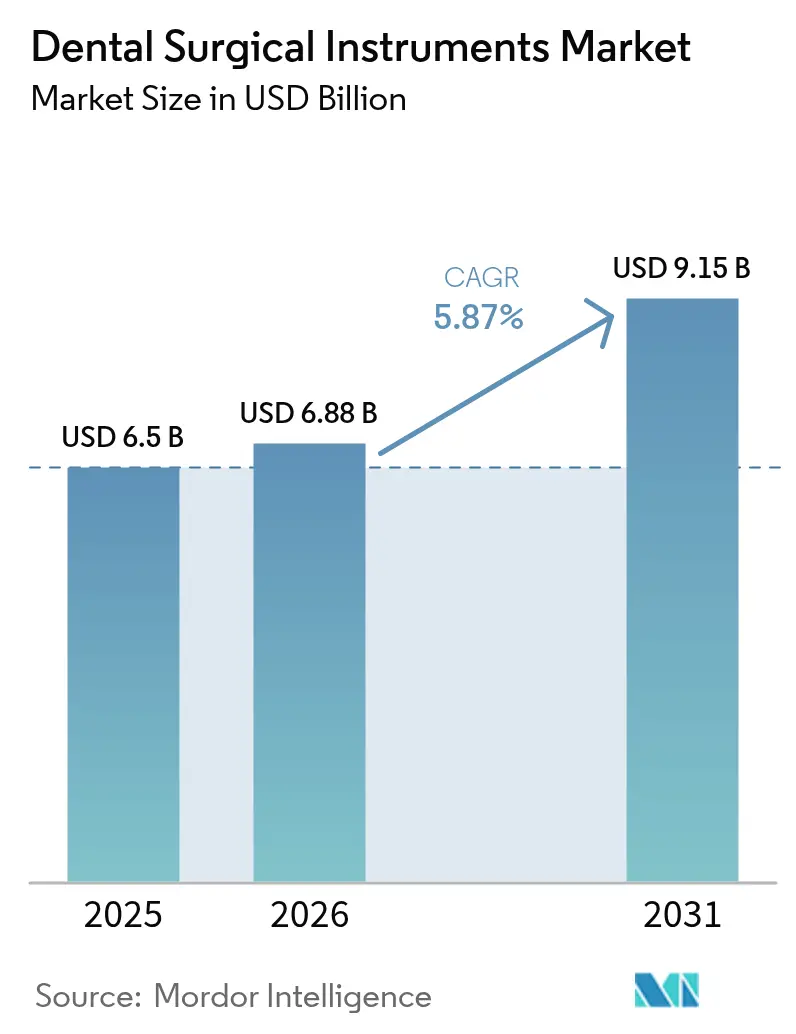

| Market Size (2026) | USD 6.88 Billion |

| Market Size (2031) | USD 9.15 Billion |

| Growth Rate (2026 - 2031) | 5.87% CAGR |

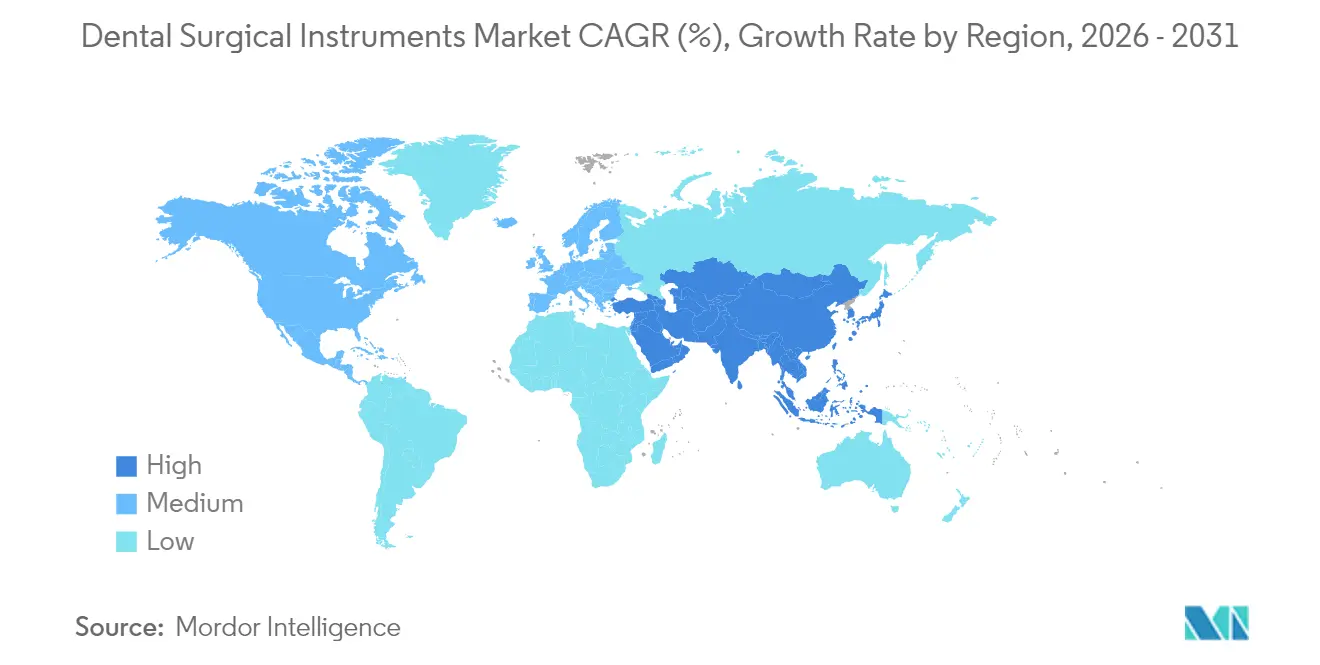

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

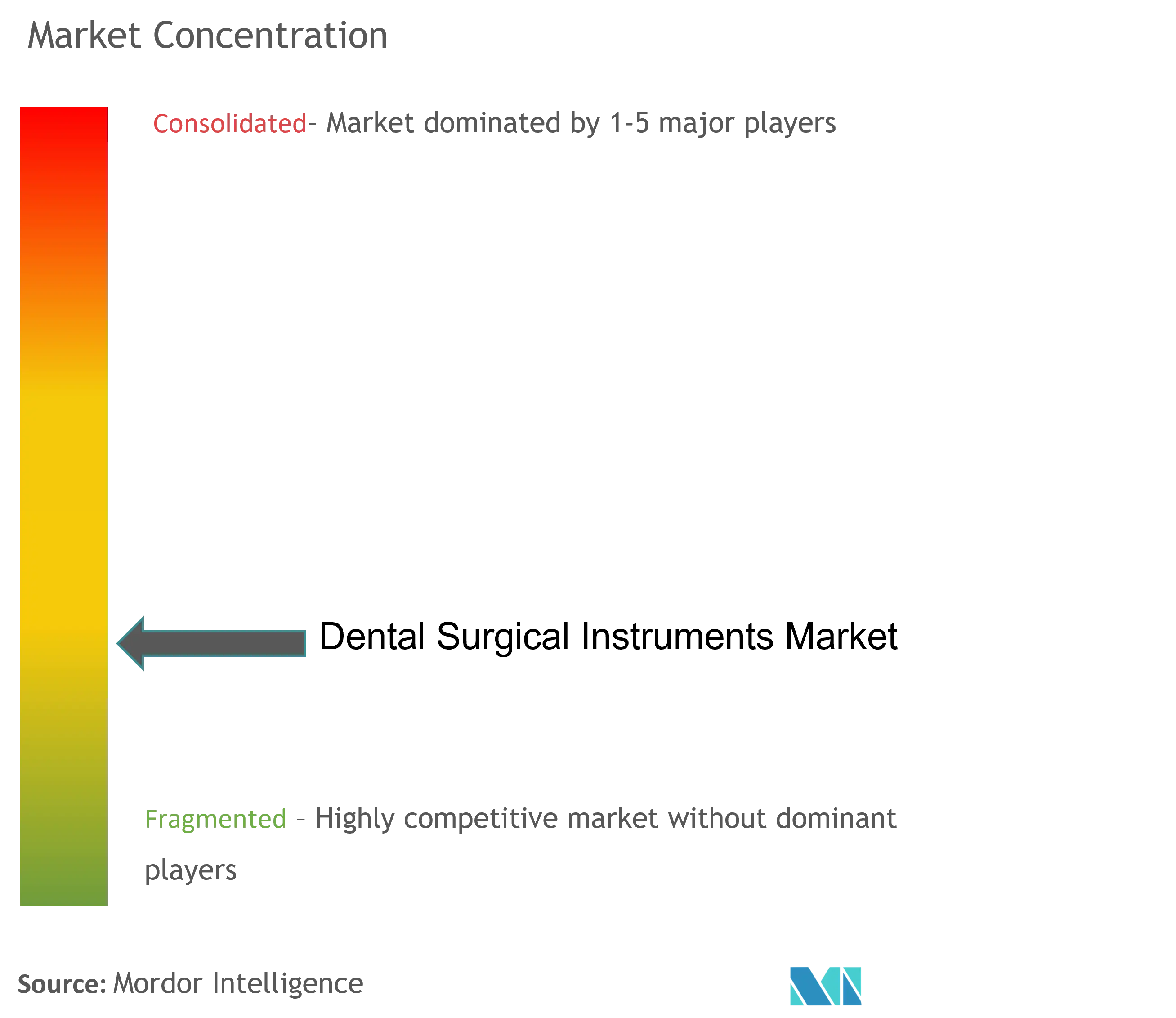

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Dental Surgical Instruments Market Analysis by Mordor Intelligence

Dental surgical instruments market size in 2026 is estimated at USD 6.88 billion, growing from 2025 value of USD 6.5 billion with 2031 projections showing USD 9.15 billion, growing at 5.87% CAGR over 2026-2031. Growing volumes of implantology, rapid uptake of AI-guided robotics, and rising cross-border demand for complex oral surgeries are the primary forces expanding the dental surgical instruments market. Handheld tools retain a central role, yet laser-based and piezoelectric systems are accelerating because they shorten healing time, preserve tissue, and improve patient comfort. North America continues to lead the dental surgical instruments market thanks to early adoption of digital workflows and supportive reimbursement, while Asia-Pacific is the fastest-growing region as tourism clusters and private investments enhance capacity. Intensifying consolidation among dental support organizations is reshaping procurement, and purpose-built geriatric programs are steering product design toward minimally invasive kits.

Key Report Takeaways

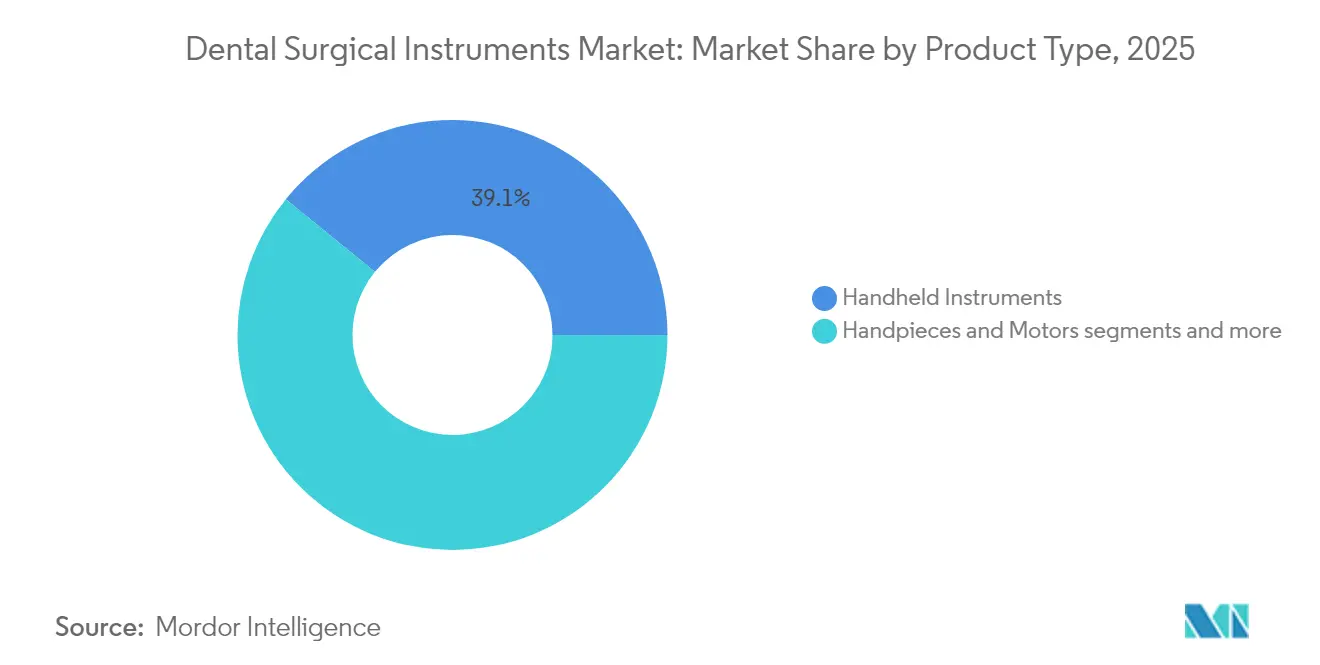

- By product type, handheld instruments led with 39.12% of dental surgical instruments market share in 2025, while dental lasers are projected to expand at a 6.86% CAGR through 2031.

- By application, implantology accounted for 40.05% share of the dental surgical instruments market size in 2025; orthodontic and cosmetic surgery is forecast to grow at 6.99% CAGR between 2026 and 2031.

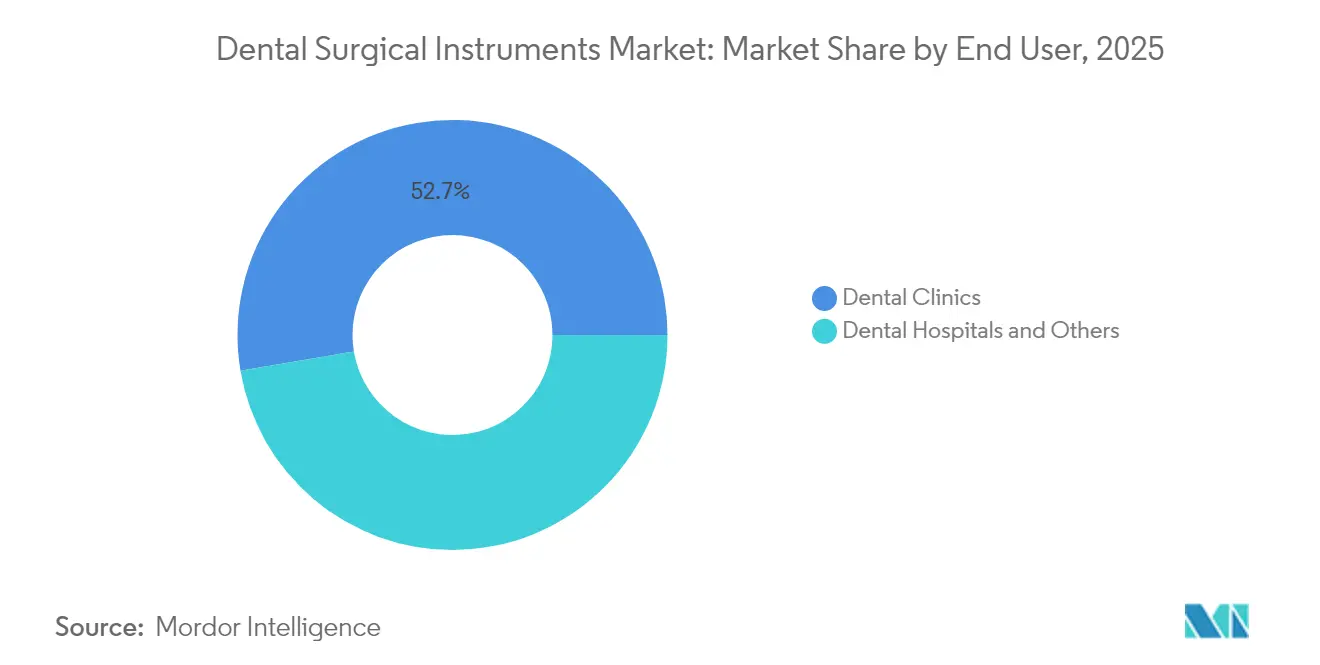

- By end user, dental clinics commanded 52.65% of the dental surgical instruments market size in 2025, while hospitals are advancing at a 6.69% CAGR through 2031.

- By region, North America held 40.85% share of the dental surgical instruments market in 2025; Asia-Pacific is expanding at a 7.18% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Dental Surgical Instruments Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Adoption of piezo-electric osteotomy instrumentation in Europe & Asia-Pacific | +1.4 | Europe & Asia-Pacific, with spillover to North America | Medium term (≈3-4 yrs) |

| AI-guided robotic micro-surgery uptake in North America implant centres | +0.9 | North America, limited penetration in other regions | Long term (≥5 yrs) |

| Tourism-led demand for complex implant surgeries in Turkey & GCC drives kit sales | +1.3 | Turkey, GCC countries, with global patient sourcing | Short term (≤2 yrs) |

| Driver – Geriatric oral‐health programs boosting minimally-invasive kits in Japan & Nordics | +0.8 | Japan & Nordic countries, with adoption in aging societies globally | Medium term (≈3-4 yrs) |

| Bulk procurement by fast-growing DSO chains in U.S. & Canada | +1.1 | U.S. & Canada, with expansion to other consolidated markets | Short term (≤2 yrs) |

| Clear-aligner IPR boom driving precision burs demand in South America | +0.6 | South America, with growth in emerging orthodontic markets | Medium term (≈3-4 yrs) |

| Source: Mordor Intelligence | |||

Adoption of Piezoelectric-Assisted Osteotomy

Selective micro-vibrations allow piezoelectric devices to cut mineralized tissue while sparing adjacent nerves and vessels, reducing postoperative pain and swelling for third-molar extractions and implant site preparation. Growing clinical evidence of a lower nerve-injury rate is prompting specialty practices to replace conventional rotary drills. Training centers in the United States and Germany now include piezosurgery modules in residency curricula, accelerating competency among young clinicians. Suppliers are refining tip designs for hard-to-access mandibular regions, and distributors report double-digit unit growth in 2024. As reimbursement parity with rotary systems improves, the driver sustains a positive medium-term lift on the dental surgical instruments market.

AI-Guided Robotic Dental Surgery Uptake

Robotics platforms integrate pre-operative cone-beam CT data with real-time navigation, enabling sub-millimeter implant placement accuracy and eliminating disposable surgical guides. Clinical trials in 2025 demonstrated mean trueness deviations of 1.2 mm compared with 2.0 mm for manual techniques, translating to fewer intra-operative adjustments. Early adopters report reduced chair time and predictable flapless protocols that appeal to patients. Capital cost remains high, yet leasing models and service contracts are lowering entry barriers. Regulatory approvals in Canada and Japan broaden the addressable base, feeding long-term momentum across the dental surgical instruments market.

Tourism-Led Demand for Complex Implant Surgeries

Price differentials of 60–75% for full-arch rehabilitation encourage patients from Western Europe and North America to seek care in Turkey, Mexico, or Thailand. Dedicated “all-on-four” packages bundle implants, prosthetics, hotel, and local transport, pushing case volumes that require high-precision drills, torque drivers, and grafting kits. Governments in destination countries grant tax incentives to clinics that meet international accreditation, spurring upgrades to premium instrumentation. This inflow delivers an immediate lift in revenue for the dental surgical instruments market, particularly for implant kits and regenerative biomaterial delivery tools.

Geriatric Oral-Health Programs Boosting Minimally-Invasive Kits

By 2030, persons aged ≥ 60 will exceed 1.4 billion globally, and mucosal fragility plus poly-pharmacy necessitate gentle approaches. National insurance schemes in Japan and Sweden subsidize air-abrasion units, diode lasers, and ergonomic ultrasonic scalers tailored for older adults. University clinics report increased use of fluoride varnish applicators and short-shank scalers to manage root caries in nursing-home residents. Instrument makers respond with lightweight, autoclavable handles that reduce operator fatigue. The convergence of demographic need and public funding keeps demand firm across the dental surgical instruments market.

Restraints Impact Analysis*

| Restarint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Reimbursement gap for advanced electrosurgical devices i | -0.7 | Caribbean & African markets, with limited global impact | Medium term (≈3-4 yrs) |

| Limited stainless-steel metallurgy capacity in Nordics inflates costs | -0.4 | Nordic countries, with supply chain effects in Europe | Long term (≥5 yrs) |

| EU MDR certification delays for new laser handpieces | -1.2 | European Union, with regulatory spillover to other regions | Short term (≤2 yrs) |

| Counterfeit handhelds influx from Asia impacting Oceania | -0.5 | Oceania region, with potential expansion to other markets | Short term (≤2 yrs) |

| Source: Mordor Intelligence | |||

High Cost of Dental Surgical Instruments

Premium diode lasers sell for USD 50,000–70,000 and piezoelectric surgery units for USD 5,000–15,000, exceeding the capital budgets of rural clinics. Service contracts and mandatory calibration add 15–20% to annual ownership costs. Community colleges in North Carolina secured USD 3.57 million to train assistants on advanced devices, underscoring the sizable investment required before revenue materializes. Smaller practices defer purchases, directly suppressing uptake in price-sensitive segments of the dental surgical instruments market.

Poor Reimbursement Policies

Only 49% of adult Medicaid beneficiaries visited a dentist in the past year, with low fees cited as the main barrier[1]Source: American Dental Association Health Policy Institute, “Medicaid Dental Visits 2024,” ada.org . Although the Centers for Medicare & Medicaid Services added 229 dental codes to clinical APCs for 2024, advanced implant or laser procedures often remain uncovered[2]Source: Centers for Medicare & Medicaid Services, “CY 2024 Outpatient Prospective Payment Final Rule,” cms.gov. This uncertainty discourages capital spending on innovative instrumentation. Pending state-level reforms could improve cost recovery, but in the interim reimbursement shortfalls temper the growth trajectory of the dental surgical instruments market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Shift Toward Minimally Invasive Precision

Handheld instruments retained 39.12% of dental surgical instruments market share in 2025, reflecting their central role in routine scaling, extraction, and restorative work. Stainless-steel explorers, needle holders, and bone files continue to set purchasing baselines, and incremental refinements in handle knurling and balance sustain loyalty among clinicians. Despite dominance, the product mix is nudging toward micro-surgical variants that allow finer gestures in confined operative fields. Dental lasers, although representing a smaller installed base, are the fastest-growing line with a 6.86% CAGR forecast through 2031. Orthodontic offices and periodontists favor erbium and diode systems that ablate soft tissue with minimal collateral damage, shortening chair time and driving positive word-of-mouth. The dental surgical instruments market size for laser systems is projected to expand steadily as unit prices decline and manufacturers bundle training with purchase agreements.

Powered handpieces and surgical motors are in steady demand for implant bed preparation and endodontic shaping. Brushless micro-motors and integrated LED illumination improve torque stability and visualization, further differentiating premium models. Electrosurgical units cater to coagulation in oro-facial oncology, whereas ultrasonic scalers remain cornerstones of periodontal maintenance. Although elective cosmetic cases fell during pandemic lockdowns, powered instrumentation rebounded swiftly as patient flow normalized. Vendors leveraging modular battery packs and autoclavable casings are expected to capture share, keeping the dental surgical instruments market on a technology-driven upgrade path.

By Application: Implantology Holds Ground as Aesthetics Accelerate

Implantology held 40.05% of the dental surgical instruments market in 2025 because edentulous cohorts demand fixed solutions over removable dentures. Precision torque wrenches, depth gauges, and sinus-lift kits are indispensable, and OEMs align their portfolios to popular internal-hex and conical connection systems. The dental surgical instruments market size tied to implantology is poised to expand as chairside CBCT imaging becomes standard of care, ensuring high confidence in immediate-load protocols. All-zirconia and titanium-zirconium implant fixtures that integrate with guided-surgery tooling further lock in instrument sales cycles.

Orthodontic and cosmetic surgery is the fastest-growing application with a 6.99% CAGR outlook. Clear aligner acceptance, fueled by aggressive direct-to-consumer marketing, increases demand for inter-proximal reduction burs, precision cutters, and finishing strips. Digitally planned veneers, gingival re-contouring, and enamel micro-abrasion also rely on high-speed, low-vibration handpieces fashioned from aerospace-grade alloys. Growth is most apparent in urban Asian markets where young adults pursue aesthetic upgrades concurrent with lifestyle spending. Endodontic microsurgery and periodontal regeneration enjoy niche but consistent adoption as microscope-assisted workflows spread from academic centers to private suites, sustaining diversification within the dental surgical instruments industry.

By End User: Clinics Dominate While Hospitals Scale Complex Care

Dental clinics captured 52.65% of the dental surgical instruments market in 2025 by virtue of accessibility, practitioner autonomy, and the rise of multi-chair group practices. DSOs exercise bulk-purchase leverage, negotiating multi-year supply contracts that standardize tool inventory across networks. Integration of intraoral scanners and CAD/CAM milling drives cross-selling of compatible surgical kits. Meanwhile, hospitals register the quickest advance at 6.69% CAGR, reflecting their ability to address medically complex cases such as oncology resections and trauma reconstructions. Operating-theater settings demand sterile-pack blades, powered saws, and resorbable plating systems, broadening procurement.

Academic institutions and research laboratories fall under the “others” category and function as technology incubators. Funding from National Institutes of Health grants and private philanthropy equips these centers with prototype navigation systems and augmented-reality microscopes. Field feedback cycles between innovators and clinical users shape successive product generations, reinforcing the value pipeline for the broader dental surgical instruments market

Geography Analysis

North America retained 40.85% of the dental surgical instruments market in 2025. Early reimbursement for robotic implant placement and widespread incorporation of cone-beam CT underwrite sustained equipment refresh cycles. The American Dental Association notes that 67% of U.S. practices now offer in-house 3-D imaging, a rate that pushes demand for compatible surgical guides and precision burs. Federal payment parity across service sites, finalized by the Centers for Medicare & Medicaid Services in 2024, strengthens hospital purchasing confidence for advanced oral-surgery sets.

Asia-Pacific shows the strongest momentum with a 7.18% CAGR to 2031. Thailand and Turkey attract inbound patients seeking full-arch implant rehabilitation at prices 60% lower than in Western Europe, necessitating robust inventories of implant drills, torque drivers, and graft syringes. China increases local manufacturing output through tax breaks on Class III medical devices, enhancing supply chain resilience. India’s Production-Linked Incentive scheme earmarks subsidies for mid-size med-tech firms, lifting domestic output of ultrasonic scalers and obturation systems. Japan advances robotics integration by pairing indigenous haptic controllers with imported navigation software, further diversifying regional product demand.

Europe continues to exhibit steady uptake driven by national prevention programs targeting periodontal disease. Germany champions laser adoption via reimbursement codes for minimally invasive frenectomies, while the United Kingdom’s NHS deploys mobile dental vans equipped with portable surgical sets to reach underserved communities. Central and Eastern Europe benefit from EU structural funds that modernize university clinics and foster cross-border training exchanges. In the Middle East and Africa, Gulf Cooperation Council states allocate oil revenues to build specialized implant centers, whereas South American markets such as Brazil witness a surge in esthetic demand linked to rising disposable income. Collectively, these dynamics anchor long-run expansion opportunities across the dental surgical instruments market.

Regulatory Landscape

Dental surgical instruments are regulated as medical devices, and market access depends on quality systems, technical documentation, and post-market surveillance. In the United States, FDA oversight under 21 CFR Part 820 is being operationalized through the Quality Management System Regulation (QMSR) alignment to ISO 13485, and FDA implemented an updated inspection approach in February 2026 as it moved away from QSIT-style inspections. This increases the focus on supplier controls and traceability across reusable instruments, powered systems, and laser platforms where calibrated performance and validated reprocessing are central to compliance.

In Europe, compliance is governed by Regulation (EU) 2017/745 (EU MDR). Notified-body capacity and evidence requirements have constrained access for new and modified devices, including laser handpieces highlighted in the report restraints. Guidance and clarifications continue to shape submissions, including CEN/TR 12401:2025 (CEN/TC 55) on classification guidance for dental materials and instruments under EU MDR. In June 2026, the European Commission published Delegated Regulations (EU) 2026/1451 and (EU) 2026/1359, which expand the list of well-established technologies (WET) for implantable and Class III devices. That can reduce certain clinical investigation and documentation burdens for established technologies, and it affects how implant-related surgical systems are justified in EU technical files.

Value Chain Analysis

The value chain begins with surgical-grade raw materials and subcomponents, and it moves through precision machining, surface finishing, assembly, packaging and sterilization validation, and then distribution to clinics, hospitals, and DSOs. Upstream inputs include stainless steels and titanium alloys, with traceability supported by Mill Test Reports and Certificates of Analysis. Specialized component makers supply parts for handpieces, motors, and laser delivery accessories, while OEMs and branded instrument companies integrate performance testing, cleaning and sterilization instructions, and final release under controlled quality systems.

Regulatory and standards alignment is also influencing how manufacturers handle supplier qualification and technical documentation across markets. The FDA QMSR effective February 2, 2026 harmonizes US quality requirements more closely with ISO 13485:2016, supporting global manufacturers that run a single QMS across sites, while raising expectations for supplier controls and complaint handling. In China, material and preclinical assessment standards for dental instrument metals (including YY/T 1952.1-2024 and YY/T 0294.1-2024) reinforce documentation discipline for instruments exported or produced locally. Downstream, large distributors and DSO procurement models amplify volume-based contracting and SKU standardization, which favors vendors that can sustain consistent metallurgy supply, validated reprocessing compatibility, and predictable lead times for high-turn handheld sets as well as higher-value powered and laser systems.

Competitive Landscape

The dental surgical instruments market is moderately consolidated. Dentsply Sirona emphasizes end-to-end digital workflow ecosystems that bundle scanners, planning software, and surgical kits, creating stickiness among clinician users. Henry Schein deepens vertical integration by embedding its BioHorizons implant line into distribution channels, leveraging scale to negotiate favorable supplier terms. Straumann deploys comprehensive education suites that train practitioners on tissue-level implant protocols, reinforcing product loyalty.

Acquisition activity targets high-margin niches. Acteon’s purchase of a French optics startup adds 4-K visualization to its surgical camera range, while Young Innovations invests in U.S. manufacturing capacity for stainless-steel scalers to hedge geopolitical risk. Start-ups hold disruptive potential: Perceptive Technologies prototypes AI-driven robotic arms capable of autonomous osteotomies, attracting venture interest from dental DSOs. Component suppliers such as NSK and W&H maintain stronghold positions in contra-angle handpieces by blending ceramic bearings with Bluetooth monitoring for preventive maintenance.

Competition now centers on data connectivity. Cloud dashboards that track handpiece RPMs, laser pulse counts, and sterilization cycles enable predictive servicing, lowering downtime for clinics. Firms offering open-architecture platforms gain advantage because they integrate seamlessly with third-party imaging and practice-management systems. Intellectual-property disputes over guided-surgery sleeve geometries underline the stakes of proprietary innovation within the dental surgical instruments market.

Dental Surgical Instruments Industry Leaders

COLTENE Holding AG

Integra LifeSciences Holdings Corporati

BIOLASE, Inc

The Yoshida Dental Mfg. Co., Ltd

3M

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

System-based purchasing and workflow standardization are creating white space beyond standalone manual kits, particularly as implantology and orthodontic and cosmetic procedures expand instrument pull-through. A concrete 2026 signal is Nobel Biocare completing the acquisition of Versah (February 2026), adding Densah burs and osseodensification techniques into its regenerative and implant portfolio, which supports bundling of implant planning and bone-preparation tooling. Henry Schein Orthodontics also signed an exclusive US distribution agreement for the Eversmile smartIPR system (July 2026), supporting demand for precision IPR instrumentation aligned to clear-aligner case flow referenced in the report trends.

Manufacturing capacity and infection-prevention readiness remain practical opportunity areas as clinics and DSOs prioritize reliable availability, consistent quality, and reprocessing-compatible designs. HuFriedyGroup opened a new Northbrook campus in Illinois in July 2026 to expand manufacturing capacity for dental instruments and infection prevention solutions, reinforcing a shift toward suppliers that can scale production and support standardized procurement across multi-site groups. On care delivery, the report points to increased implant procedure complexity tied to medical tourism corridors (e.g., Turkey and GCC) and public programs for older populations (e.g., Japan and Nordics). These channels increase the need for minimally invasive, high-precision kits (piezoelectric, laser, and ergonomic sets), paired with training and service models that reduce adoption friction for higher-cost equipment.

Recent Industry Developments

- July 2026: HuFriedyGroup opened a new campus in Northbrook, Illinois to expand manufacturing capacity for dental instruments and infection prevention solutions. The additional footprint supports higher output and operational scaling for a core category of reusable instruments, aligning with DSO-driven standardization and bulk purchasing dynamics. It also reinforces the shift toward suppliers that can pair instrumentation with validated infection-prevention processes.

- September 2025: MegaGen Implant acquired BIOLASE, transitioning ownership of a major dental laser provider. The deal strengthened BIOLASE access to an implant-focused ecosystem and broadened cross-selling potential between implant workflows and minimally invasive soft-tissue laser procedures. It also positioned BIOLASE for follow-on operational changes in manufacturing and commercial support.

- June 2024: BioHorizons launched the tapered pro conical implant, expanding options for immediate-load cases. The product addition increased demand for compatible surgical instrumentation such as drill sequences, torque drivers, and placement tools that match connection geometry and surgical protocols. For distributors, it widened bundling opportunities across implants and associated surgical kits.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market is defined as the revenues generated from instruments and related items used by dental professionals to perform surgical and interventional dental procedures, across clinics and hospital dental departments, and measured in current US dollars.

Scope exclusions: Services, dental implants as standalone devices, and non-surgical dental capital equipment that is not used as a surgical instrument are kept out where they are not sold as part of the defined instrument categories.

Segmentation Overview

- By Product Type (Value)

- Handheld Instruments

- Handpieces & Motors

- Electrosurgical & Cautery Systems

- Ultrasonic Instruments & Scalers

- Powered Surgical Instruments

- Dental Lasers

- Sutures & Hemostats

- By Application (Value)

- Implantology

- Endodontic Surgery

- Periodontal Surgery

- Orthodontic & Cosmetic Surgery

- Oral & Maxillofacial Surgery

- Restorative / Prosthodontic Surgery

- By End User (Value)

- Hospitals

- Dental Clinics

- Others

- By Geography (Value)

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started with building a clear demand and supply picture for dental procedures that commonly require surgical instruments, and then aligning it with the product scope used in this study. We used public sources such as the World Health Organization for oral health burden, the US Centers for Disease Control and Prevention for dental health indicators, and OECD health statistics for dentist density and care access patterns.

To add context on procedure flow and clinical adoption, we also referred to sources such as the American Dental Association, peer reviewed dental journals, and national health ministry portals that publish hospital activity or health system updates. Trade data and customs releases were used selectively to understand import reliance in markets where local manufacturing is limited, and patent databases helped spot innovation intensity in areas like laser and minimally invasive tools. For company level grounding, we reviewed annual reports, investor presentations, and press releases, and we also used paid subscriptions for company financials and intelligence plus a patent database to cross check revenues and product positioning. The desk source list is illustrative, and many other public references were used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary inputs were gathered through structured conversations and surveys with instrument manufacturers, distributors, dental clinic procurement teams, and clinicians who regularly perform restorative, endodontic, orthodontic, and oral surgery procedures. Because demand patterns vary by reimbursement, private clinic penetration, and dental tourism, coverage was balanced across APAC, EMEA, and the Americas, and follow ups were done when desk signals did not line up with field feedback.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 33% | CXOs: 19% | APAC: 50% |

| Mid tier: 45% | Functional/Unit leaders: 31% | EMEA: 32% |

| Smaller Players: 22% | Managers: 50% | Americas: 18% |

Market-Sizing & Forecasting

The sizing logic starts from a top-down rebuild of the dental surgery instrument demand pool using procedure volumes and care access indicators, which are then translated into spend using typical instrument and consumable usage patterns. Once the demand base was set, totals were corroborated using selective bottom-up checks, like sampled supplier revenue bands, distributor channel checks, and price per unit assumptions for commonly purchased kits.

Several market fingerprints were used as model inputs, such as dental procedure mix (restorative dentistry, orthodontics, endodontics, and other applications), dentist and clinic density, adoption of laser enabled dentistry, replacement cycles for handheld instruments, and import dependence in equipment-light manufacturing markets. Where product boundaries could blur, especially between consumables and broader dental equipment, allocation keys were applied and then rechecked through interviews so the model stayed consistent.

For forecasting, we used multivariate regression with scenario analysis around the variables that field respondents most often linked to spending shifts, including elective procedure recovery, private clinic investment, and the pace of technology upgrades. When bottom-up data gaps appeared in smaller countries, per clinic spend proxies were used, and then adjusted based on local procedure intensity and pricing differences before being rolled into the regional totals.

Data Validation & Update Cycle

Outputs are validated through multiple checks so large jumps do not pass without explanation. We compare modeled values against independent signals like procedure trends, import and production direction, and disclosed business performance cues from public company materials, and then outliers are reviewed and corrected where assumptions do not hold.

Before final sign-off, the model goes through a multi-step analyst review that tests sensitivity to key inputs, checks currency conversion timing, and confirms that scope boundaries are applied the same way across regions. Reports are refreshed annually, and interim updates are triggered when material events occur, such as major regulatory changes or sudden shifts in elective dental visits. Right before delivery, a fresh data pass is completed so clients receive the most current view available.

Mordor Intelligence's Dental Surgical Instruments Market Size Versus Other Published Estimates

Published market sizes for dental surgical instruments do not always match, even when they sound like the same topic, because the counted product basket and the timing of the base year can shift the total quickly. Differences also come from how authors translate procedure growth into instrument spend, and whether they validate price and mix assumptions with real buyer and channel feedback.

Procedure mix signals and adoption cues, including how fast laser based tools and consumables are being pulled into routine dentistry, are the evidence checks that keep Mordor Intelligence's estimate tied to the defined product scope and the 2026 base year, rather than blending in broader dental equipment lines. The largest gaps we saw in other published figures came from earlier base years, faster implied price growth, and wider category bundling that can pull in adjacent equipment or implant related revenue.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 6.88 B (2026) | |

| Industry Research Publisher A | USD 4.94 B (2024) | Uses a 2024 base year and a different growth path to 2031, which can compress the current size if later procedure recovery and mix shifts are not fully captured in the starting point. |

| Industry Research Publisher B | USD 5.30 B (2025) | Defines the category as dental surgery instruments across a broader product and channel segmentation, and the included items can vary by publisher, which changes what is counted as an instrument versus broader dental equipment. |

Looking across the table, the spread is mainly explained by base-year timing and what gets counted inside the instrument basket, especially when consumables and laser related tools are treated differently. Our approach stays traceable because the demand pool is linked to procedure activity and then checked with channel feedback, and that keeps the final number practical to interpret and repeat.

Key Questions Answered in the Report

What is the current value of the dental surgical instruments market?

The market stands at USD 6.88 billion in 2026 and is forecast to reach USD 9.15 billion by 2031.

Which product segment is growing fastest?

Dental lasers record the fastest growth, posting a 6.86% CAGR for 2026-2031 as clinicians adopt minimally invasive soft-tissue procedures.

Why is Asia-Pacific considered the most attractive growth region?

Asia-Pacific combines a 7.18% regional CAGR with rising dental tourism and government incentives that expand private-sector capacity.

How are robotics influencing clinical workflows?

AI-guided robots such as Yomi enable sub-millimeter implant placement, reduce reliance on surgical guides, and shorten procedure times, improving predictability.

Page last updated on: