Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

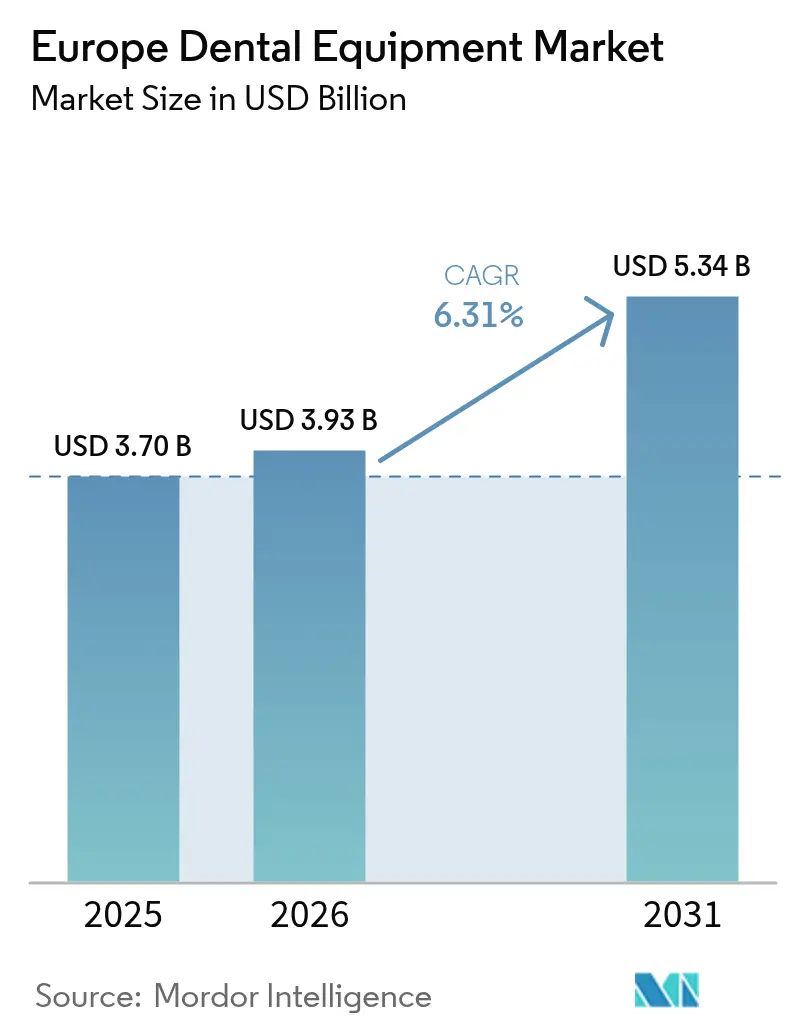

| Base Year Market Size (2025) | USD 3.70 Billion |

| Market Size (2026) | USD 3.93 Billion |

| Market Size (2031) | USD 5.34 Billion |

| Growth Rate (2026 - 2031) | 6.31% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Dental Equipment Market Analysis by Mordor Intelligence

The Europe Dental Equipment Market size is expected to grow from USD 3.70 billion in 2025 to USD 3.93 billion in 2026 and is forecast to reach USD 5.34 billion by 2031 at 6.31% CAGR over 2026-2031.

Demand is propelled by the convergence of chairside digital workflows with AI-powered diagnostics, which shortens treatment cycles and improves clinical accuracy. Strong uptake of3D printing for customized prosthetics, coupled with growing preference for biomimetic and zirconia materials, is reshaping restorative procedures. Country-level dynamics also matter: Germany’s engineering base anchors equipment manufacturing, while the UnitedKingdom’s private-practice boom is accelerating premium device investment. Meanwhile, the new Medical Devices Regulation (MDR) is tightening quality standards and lengthening approval timelines, nudging clinics toward trusted multinational suppliers and well-documented devices health[1]Source: European Commission, “Getting Ready for the New Regulations,” health.ec.europa.eu .

Key Report Takeaways

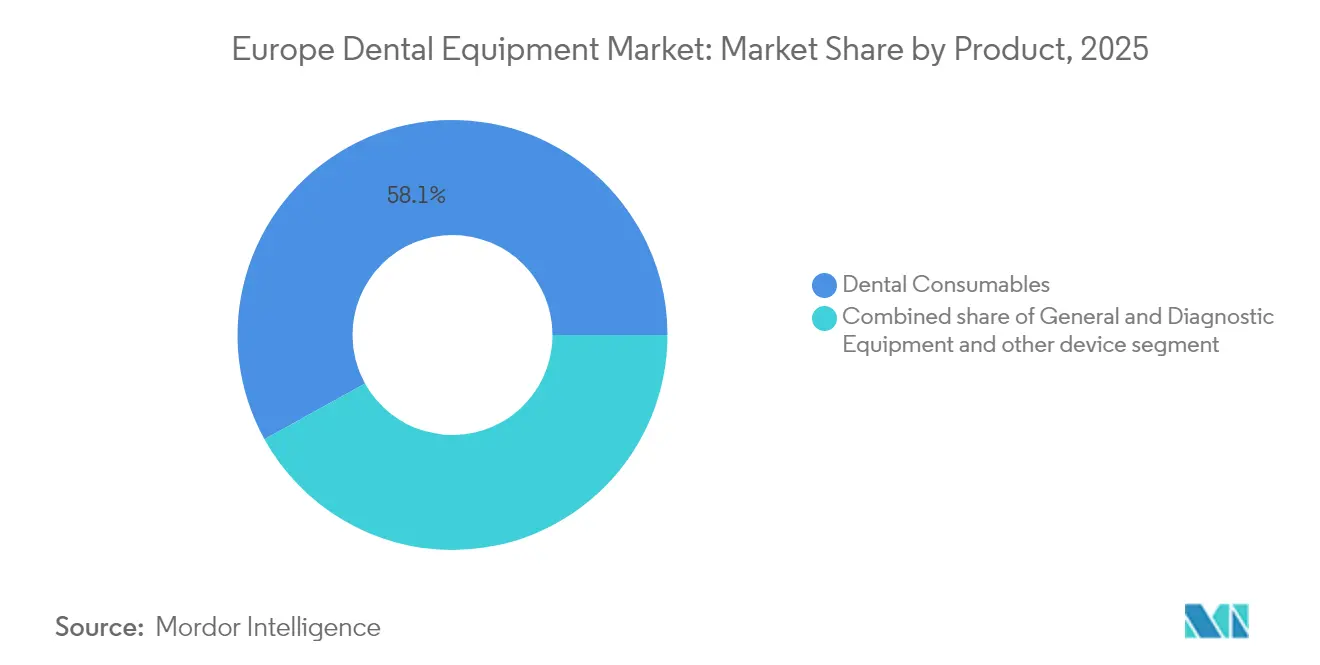

- By product, dental consumables accounted for 58.05% of market share in 2025, while general and diagnostics equipment is forecast to grow at the fastest CAGR of 7.93% through 2031.

- By treatment type, orthodontics held a 64.62% share in 2025, with prosthodontics projected to be the fastest-growing segment at 8.34% CAGR through 2031.

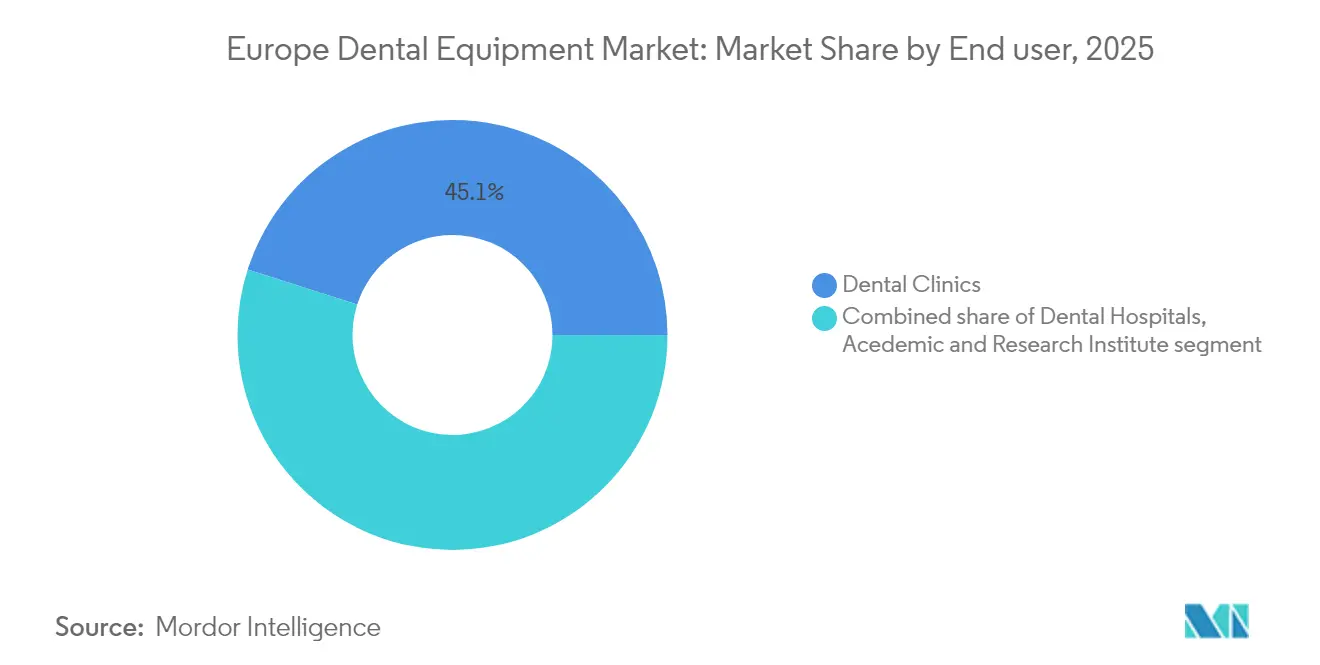

- By end user, dental clinics led with a 45.08% market share in 2025 and are also set to post the fastest CAGR at 7.29% between 2026 and 2031.

- By country, Germany represented the largest share at 24.32% in 2025, while the United Kingdom is expected to see the highest growth rate at 7.55% CAGR through 2031

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Dental Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing incidence of dental diseases | +1.2% | Pan-Europe | Long term (≥ 4 years) |

| Innovation in dental products | +1.0% | Western Europe | Medium term (2-4 years) |

| Increasing demand for cosmetic dentistry | +0.9% | United Kingdom, Spain, Italy | Short term (≤ 2 years) |

| Technological advancements in dental solutions | +1.1% | Germany, Nordics | Long term (≥ 4 years) |

| Government-sponsored oral-health screening programs expanding imaging fleet in Nordics | +0.6% | Nordics | Short term (≤ 2 years) |

| Orthodontic tourism inflow to Spain & Hungary boosting demand for digital intra-oral scanners | +0.5% | Spain, Hungary | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Increasing Incidence of Dental Diseases

The Europe dental equipment market is heavily influenced by a rising disease burden that now affects more than half of the region’s adults who.int. Dental caries alone afflict 33.6% of residents, while 25.2% experience significant tooth loss, generating steady demand for restorative devices and imaging systems. Severe periodontitis cases are projected to escalate through 2050, prompting practices to adopt advanced periodontal probes and portable diagnostic units. Refugee cohorts amplify unmet need: 84% of Ukrainian children examined in Italy showed caries, underscoring the requirement for mobile X-ray and preventive technologies [2]Source: Cianetti S. et al., “Real-World Dental Health of Ukrainian War Refugee Children,” bmcoralhealth.biomedcentral.com. Collectively, these epidemiological pressures are set to lift unit shipments across consumables, scalers, and CAD/CAM-enabled prosthetics.

Innovation in Dental Products

Biomimetic glass ionomer cements and nanofilled composite resins are improving longevity of restorations, lowering retreatment rates, and reducing chair time materials-journal.com. Natural polymers such as chitosan and collagen now underpin guided tissue regeneration membranes, boosting clinical adoption of compatible delivery equipment materials-journal.com. Equipment vendors are integrating dedicated dispensers and curing lights optimized for these new chemistries. Zirconium dioxide implants act as optical waveguides that allow photodynamic biofilm inactivation, cutting bacterial counts by as much as 85% and opening opportunities for laser-ready implant handpieces microorganisms-journal.com. As R&D pipelines widen, suppliers that bundle consumables with application devices stand to capture recurring revenue streams across the Europe dental equipment market.

Increasing Demand for Cosmetic Dentistry

Aesthetic procedures are rewriting capital-planning priorities for clinics across the Europe dental equipment market. Heightened social-media exposure drives demand for whitening, veneer placement, and clear aligner therapies. Clinics now routinely purchase diode lasers, high-resolution intraoral scanners, and chairside milling units to support minimally invasive treatments. Digital workflows, particularly CAD/CAM and photogrammetry-based smile design, cut turnaround times and enable same-day veneers. Zirconia multilayer materials deliver both strength and translucency, allowing laboratories to drop veneering stages and reduce remakes. Consequently, vendors with integrated aesthetic portfolios enjoy faster equipment pull-through in high-growth urban centers.

Technological Advancements in Dental Solutions

Artificial intelligence strengthens diagnostics by automating radiograph annotation and caries detection, and leading platforms such as MolarMate and 3Shape Automate report acceptance rates above 90% for AI-generated crown designs. Er:YAG lasers facilitate flapless extraction, minimizing postoperative discomfort and accelerating healing . Adjunctive diode-laser therapy reduces periodontal bleeding on probing by 75%, encouraging multispecialty practices to upgrade ultrasonic scalers with laser modules. CAD/CAM interoperability with AI boosts cementation accuracy and cuts adjustment appointments, reinforcing digital equipment replacement cycles across the Europe dental equipment market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lack of Proper Reimbursement of Dental Care | ~1.3% | Southern Europe, UK, France | Long term (≥ 5 yrs) |

| High Cost of Surgeries | ~1.0% | Southern & Eastern Europe, UK | Long term (≥ 5 yrs) |

| Shortage of trained CAD/CAM technicians in CEE slows lab automation uptake | ~0.7% | Central & Eastern Europe | Medium term (~ 2-4 yrs) |

| Price compression in entry-level handpieces due to Asian OEM influx | ~0.5% | All Europe, especially CEE & South | Short term (≤ 2 yrs) |

| Source: Mordor Intelligence | |||

Lack of Proper Reimbursement of Dental Care

Fragmented national coverage models hinder uniform technology rollouts. France reimburses only 60% of basic consultations, dampening appetite for premium imaging upgrades among smaller practices. Denmark requires adults to pay 60% of fees, while Sweden’s tiered subsidy introduces copay uncertainty, blunting early adoption of high-cost lasers nhwstat.org. UK clinics, grappling with constrained NHS budgets, face reduced capital reserves, as evidenced by practices in Sheffield struggling to service recent expansion loans. As a result, leasing and pay-per-use models are gaining ground within the Europe dental equipment market.

High Cost of Surgeries

Out-of-pocket payments for implants and complex prosthodontics remain steep, prompting budget-sensitive patients to defer procedures. DSOs such as Colosseum Dental Group leverage group purchasing to negotiate lower equipment prices, yet independent clinics often delay procurement of CBCT scanners and surgical lasers . MDR compliance adds incremental testing and documentation expenses, raising final device prices and tightening margins for manufacturers and buyers alike. These pressures steer clinics toward multifunctional workstations that maximize utilization across specialties, shaping the purchasing mix within the Europe dental equipment market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Consumables Retain Dominance as Diagnostics Accelerate

Europe dental equipment market size data show dental consumables captured 58.05% revenue share in 2025 on the back of recurring purchase cycles and procedural indispensability. Natural biomaterials such as alginate, cellulose, and hydroxyapatite are winning clinician favor for their biocompatibility, pushing suppliers to introduce pre-dosed cartridges that simplify chairside handling materials. The Europe dental equipment industry is simultaneously witnessing a leap in smart dispensers that track usage and automate reordering, reducing stockouts.

General and diagnostics equipment, although smaller by revenue, is posting the fastest 7.93% CAGR through 2031 as AI-ready intraoral scanners and CBCT units become routine for treatment planning. Lasers represent the most dynamic subcategory because Er:YAG systems now enable flapless extractions, while diode-laser periodontal adjuncts deliver measurable reductions in probing depth. Suppliers focused on bundling consumables with diagnostics—such as infection-control kits packaged with imaging sensors—stand to deepen wallet share in the Europe dental equipment market.

By Treatment: Orthodontic Leadership Meets Prosthodontic Momentum

Orthodontics held 64.62% of Europe dental equipment market share in 2025, reflecting strong penetration of clear aligners and associated digital scanners towardshealthcare.com. Multilayer polymer aligners preserve force delivery after thermomechanical aging, fostering repeat purchases by high-volume providers. Europe dental equipment industry vendors now bundle cloud-based monitoring apps with aligner printers, shortening refinement cycles and lifting aligner throughput.

Prosthodontics is expanding at an 8.34% CAGR, underpinned by population aging and tooth-loss prevalence pubmed.ncbi.nlm.nih.gov. Chairside milling of zirconia multilayer crowns eliminates veneering, cutting laboratory turnaround by 40% and improving esthetics dentsplysirona.com. Growth in implant surgery drives demand for motorized torque devices and guided surgery kits, further enlarging the Europe dental equipment market size for this treatment category.

By End User: Clinics Consolidate and Digitalize

Dental clinics commanded 45.08% of the Europe dental equipment market size in 2025, and their 7.29% CAGR highlights ongoing consolidation waves. DSOs aggregate purchasing power to equip chains with uniform CBCT, scanning, and milling ecosystems, ensuring treatment consistency across sites. The Europe dental equipment industry is therefore witnessing multi-year master-supply agreements that stabilize order books for manufacturers.

Hospitals concentrate high-complexity surgeries, necessitating advanced anesthesia and surgical-grade laser platforms, but remain a smaller revenue contributor. Academic institutes like ACTA, treating roughly 330 patients daily, act as reference centers for prototype validation and early-stage clinical . Their feedback loops guide product refinements that later ripple through mainstream segments of the Europe dental equipment market.

Geography Analysis

Germany generated 24.32% of Europe dental equipment market revenue in 2025, anchored by a dense supplier cluster and favorable insurance reimbursements that cover a broad spectrum of restorative procedures. Local manufacturers export CAD/CAM mills and precision handpieces across the region, keeping domestic clinics at the forefront of adoption. Robust collaboration between universities and engineering firms accelerates iterative device upgrades, ensuring that German practices test and implement innovations early.The United Kingdom is advancing at a brisk 7.55% CAGR as NHS capacity constraints shift patient flow into self-pay channels, where providers differentiate through premium imaging and cosmetic. Private-equity investment is spurring practice roll-ups, with groups installing standardized scanner-printer workflows that elevate capital intensity per operatory samera.co.uk. Alignment with MDR requirements is straightforward for multinationals, but UK clinics still face cost headwinds from post-Brexit import checks, nudging them toward local distributors of Europe dental equipment market products.

France, Italy, and Spain display mixed dynamics shaped by reimbursement policy divergence. In France, 60% coverage of basic consultations restricts discretionary equipment spending, yet high urban concentration of aesthetic clinics supports diode-laser sales. Italy’s focus on advanced implantology drives CBCT uptake, while Spain’s growing orthodontic franchise sector boosts aligner printer demand. The Nordics report varied copay schemes: Denmark requires adult fees yet grants children free care, whereas Sweden’s subsidy for high-cost cases supports adoption of digital prosthodontic. Eastern European markets reveal disparate oral-health outcomes; Romania films strong preventive indices, contrasting with lower scores in Lithuania, resulting in heterogeneous equipment needs. These nuances collectively diversify revenue streams within the Europe dental equipment market.

Competitive Landscape

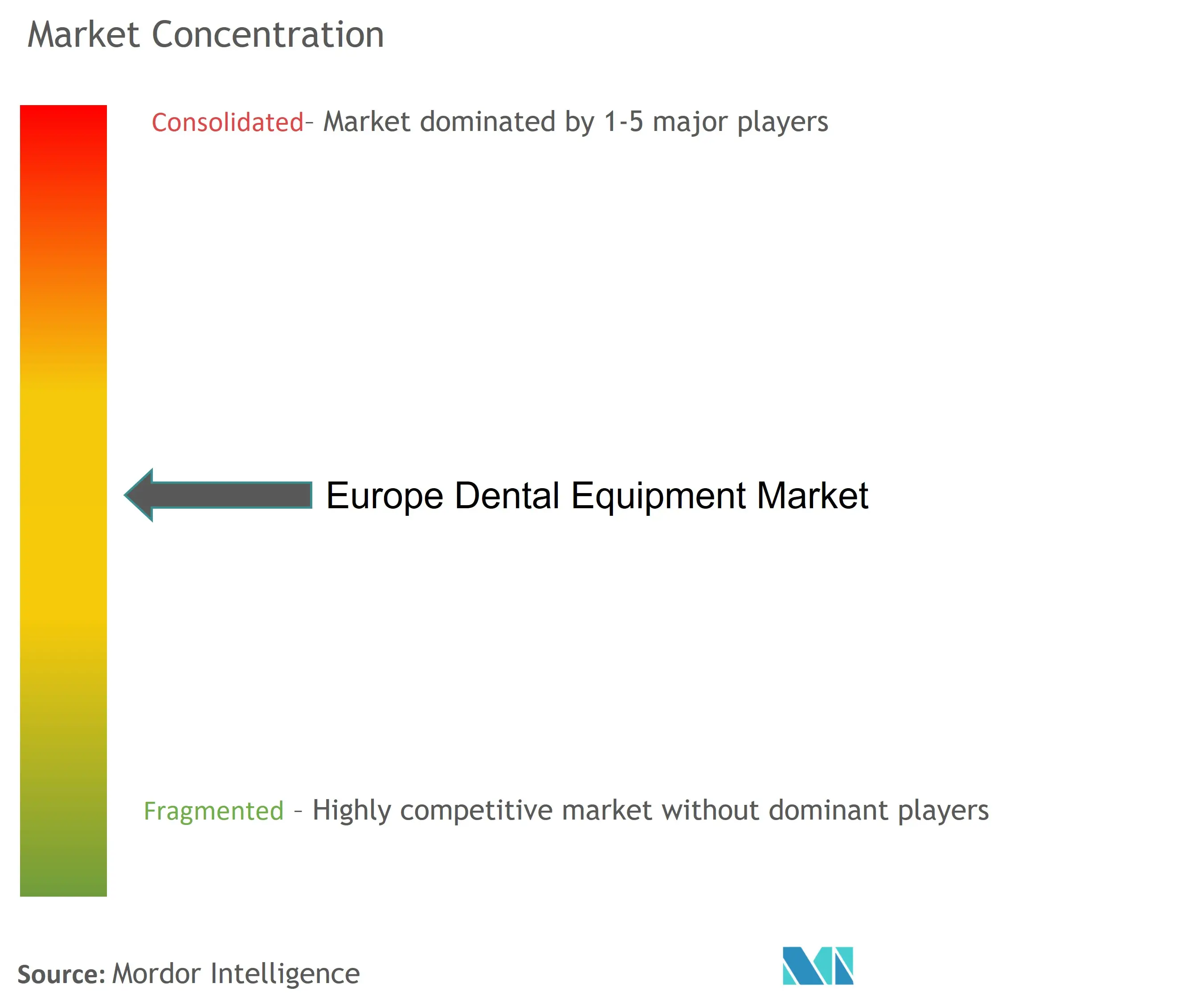

The Europe dental equipment market shows moderate concentration, with global leaders Dentsply Sirona, Straumann, and Align Technology collectively holding sizeable share through diversified portfolios spanning scanners, mills, and implant systems. Continuous R&D emphasizes digital connectivity: Straumann’s 2025 patent filing for textured laser abutments safeguards bonding integrity and underpins its implant dominance. Dentsply Sirona’s zirconia multilayer discs streamline lab workflows, reinforcing material-hardware cross-selling.

Specialist innovators, including 3Shape, fuel ecosystem collaboration by integrating AI design engines with open-architecture labs and chairside units, achieving 94% clinician acceptance for automated crowns. Such partnerships boost vendor lock-in and raise switching costs for clinics wedded to proprietary file formats. Private equity continues to roll up fragmented practice bases, with Nordic Capital’s backing of European Dental Group expanding procurement leverage that can tilt negotiations toward bundled multi-year supply contracts.

White-space opportunities emerge in geriatric-friendly ergonomic handpieces and pediatric-sized scanners, where smaller manufacturers can outmaneuver conglomerates. Price-sensitive geographies also invite subscription-as-a-service models that spread outlay over multi-year patient volumes, aligning device costs with cash flow realities of independent practices. As MDR post-market surveillance rules tighten, companies capable of funding longitudinal data collection will solidify reputations, narrowing the field of certified suppliers and shaping future structure of the Europe dental equipment market.

Europe Dental Equipment Industry Leaders

3M

Straumann

Carestream Health

Dentsply Sirona

GC Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Align Technology rolled out AI-powered X-ray Insights across the EU and UK, automating radiographic analyses for clinicians.

- March 2025: Orthocell entered the DACH region via new distributors, widening availability of its regenerative membranes

- March 2025: Solventum launched 3M Clarity Aligners in the UK, expanding clear-aligner choice and fueling scanner demand

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the Europe dental equipment market as all professionally installed, new-build capital devices, ranging from diagnostic imaging units and treatment chairs to CAD/CAM mills and dental lasers, that are sold to hospitals, private clinics, and teaching institutes across 32 European nations. Consumables such as implants, composites, burs, or aligners are not counted, and neither are refurbished or rental units.

Scope exclusion: accessories sold as part of routine maintenance kits are outside the market size.

Segmentation Overview

- By Product

- General and Diagnostics Equipment

- Dental Laser

- Soft Tissue Lasers

- Hard Tissue Lasers

- Radiology Equipment

- Extra Oral Radiology Equipment

- Intra-oral Radiology Equipment

- Dental Chair and Equipment

- Other General and Diagnostic equipment

- Dental Laser

- Dental Consumables

- Dental Biomaterial

- Dental Implants

- Crowns and Bridges

- Other Dental Consumables

- Other Dental Devices

- General and Diagnostics Equipment

- By Treatment

- Orthodontic

- Endodontic

- Peridontic

- Prosthodontic

- By End User

- Dental Hospitals

- Dental Clinics

- Academic & Research Institutes

- By Country

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed oral-care professors, procurement managers at mid-sized clinics, and product managers at European distributors to validate unit throughput, installation lead times, and likely ASP progression. Targeted surveys with orthodontists in Germany, Spain, and Poland filled data gaps on intraoral scanner penetration and expected replacement horizons.

Desk Research

We first pulled foundational demand signals from public sources such as Eurostat procedure volumes, OECD Health Statistics on dental practitioner density, and national customs codes for HS-coded dental apparatus. Regulatory filings from bodies such as the MHRA and BfArM revealed recent device approvals that influence replacement cycles. Company 10-Ks and investor decks clarified average selling prices, while scholarly articles in journals like the International Journal of Computerized Dentistry helped us size the digital workflow sub-segment. Paid datasets, Dow Jones Factiva for deal news and D&B Hoovers for firm-level revenues, rounded out competitive intelligence. This list illustrates key inputs; numerous other sources supported data gathering and cross-checks.

Market-Sizing & Forecasting

A top-down reconstruction combines Eurostat chair deliveries and trade import values, which are then aligned with practitioner counts and penetration-rate based demand pools. Select bottom-up roll-ups, sampled distributor volumes multiplied by invoice-verified ASPs, provide a reasonableness check before totals are adjusted. Key variables include annual chair installations, per-capita dental visits, private insurance coverage, imaging unit replacement cycles, and average implant surgery counts that correlate with auxiliary equipment sales. Forecasts rely on multivariate regression enriched with ARIMA smoothing; macroeconomic growth, aging population ratios, and digital workflow adoption rates serve as predictors.

Data Validation & Update Cycle

Outputs pass three-layer variance tests, anomaly flags trigger re-contact with experts, and senior reviewers sign off before publication. Reports refresh every twelve months, with interim tweaks if material regulatory or technology shifts occur.

Why Mordor's Europe Dental Equipment Baseline Commands Reliability

Published estimates often diverge because firms apply different product scopes, base years, and currency conversions.

Key gap drivers include (a) whether consumables revenues are bundled with capital gear, (b) the use of manufacturer shipment data versus end-user demand signals, and (c) refresh cadence that affects price deflators.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 3.46 B (2024) | Mordor Intelligence | - |

| USD 13.41 B (2024) | Global Consultancy A | Combines consumables and equipment, relies mainly on supplier revenue disclosures. |

| USD 11.24 B (2024) | Trade Journal B | Broad oral-care scope, limited cross-checks with practitioner population data. |

| USD 2.81 B (2023) | Regional Consultancy C | Counts capital devices only, older base year, excludes intraoral scanners and CAD/CAM mills. |

Taken together, the comparison shows how Mordor's disciplined scoping, mixed-method modeling, and annual refresh yield a balanced, transparent baseline that decision-makers can trace back to clear variables and repeatable steps.

Key Questions Answered in the Report

What is the size of the Europe dental equipment market in 2026?

The market is valued at USD 3.93 billion in 2026 and is forecast to expand at a 6.31% CAGR through 2031.

Which product category currently leads the market?

Dental consumables top the revenue chart with a 58.05% share in 2025 given their constant, high-volume use.

Why are European clinics investing in AI and chairside digital workflows?

AI-powered scanners and CAD/CAM systems reduce treatment time, boost diagnostic accuracy, and enable same-day restorations that patients increasingly expect.

What is the fastest-growing country market?

In between 2026 and 2031, the United Kingdom is anticipated to grow at the fastest pace in Europe.

Page last updated on: