Mortuary Equipment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.83 Billion |

| Market Size (2031) | USD 2.35 Billion |

| Growth Rate (2026 - 2031) | 5.13% CAGR |

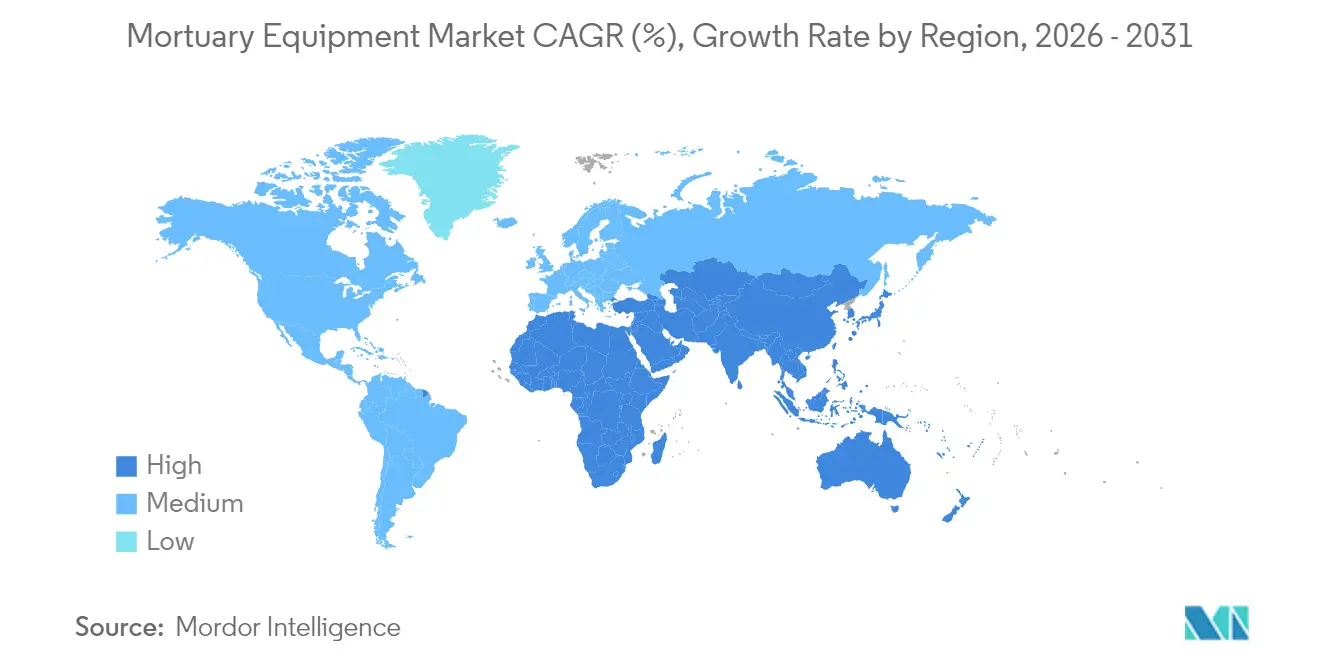

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

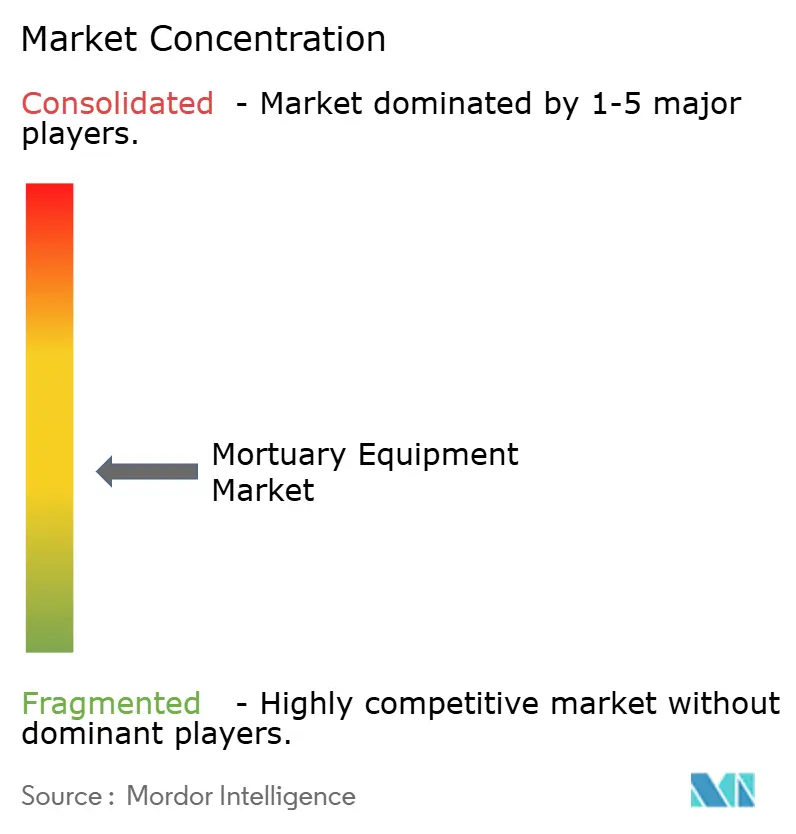

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mortuary Equipment Market Analysis by Mordor Intelligence

The Mortuary Equipment Market size was valued at USD 1.74 billion in 2025 and estimated to grow from USD 1.83 billion in 2026 to reach USD 2.35 billion by 2031, at a CAGR of 5.13% during the forecast period (2026-2031).

Demand is strongest for refrigeration units because every facility requires reliable cold storage that complies with updated refrigerant rules. Automation momentum is visible as hospitals, medical examiners, and pathology labs replace manual handling with IoT-linked lifts and conveyor systems that raise throughput and improve staff safety. Capital spending is also encouraged by government grants that modernize autopsy infrastructure and by private-equity investment targeting niche medical devices. Supply chain volatility in stainless steel and refrigerants is pushing manufacturers to redesign products for cost efficiency while meeting stricter environmental mandates. Collectively these forces keep the mortuary equipment market on a predictable upward path, albeit one punctuated by regional cultural sensitivities that shape adoption speed.

Key Report Takeaways

- By product type, refrigeration units led with 38.95% of mortuary equipment market share in 2025 and cadaver lifts and transport systems are projected to post the fastest 6.78% CAGR through 2031.

- By technology, semi-automatic systems held 33.77% share of the mortuary equipment market size in 2025, while fully automated and IoT-enabled equipment is set to advance at a 6.12% CAGR to 2031.

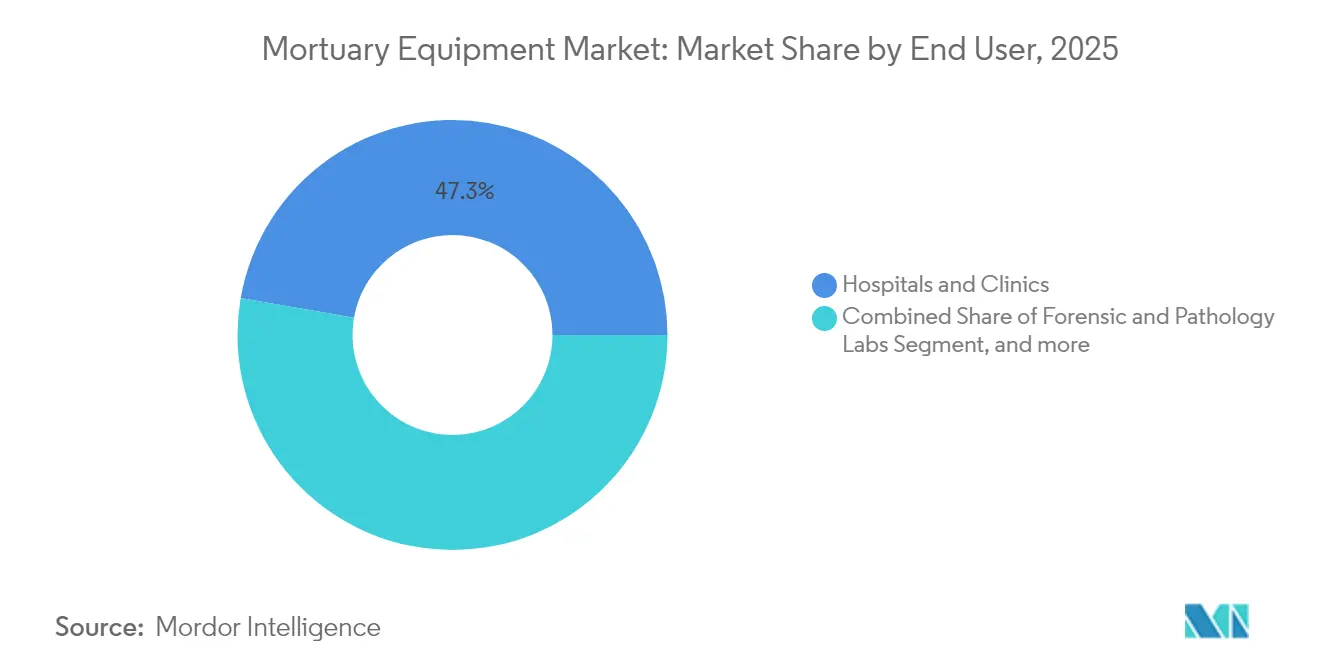

- By end user, hospitals and clinics accounted for 47.25% of the mortuary equipment market size in 2025; forensic and pathology laboratories are expanding at an 8.18% CAGR through 2031.

- By geography, North America commanded 36.88% revenue in 2025; Asia Pacific is on course for the highest 7.16% CAGR by 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Mortuary Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging Population & Rising Mortality Rates | +1.2% | Global, concentrated in North America & Europe | Long term (≥ 4 years) |

| Expansion of Morgue Facilities & Automation Needs | +0.9% | Global, strongest in Asia Pacific | Medium term (2-4 years) |

| Growth in Forensic & Pathology Research Funding | +0.7% | North America & Europe, emerging in Asia Pacific | Medium term (2-4 years) |

| Adoption of Digital Autopsy Workflows | +0.6% | North America & Europe, pilot programs in Asia Pacific | Long term (≥ 4 years) |

| Increase in Bariatric Cadavers Necessitating High-Capacity Lifts | +0.4% | North America, expanding to Europe & Asia Pacific | Short term (≤ 2 years) |

| Disaster-Response Demand for Portable Modular Coolers | +0.3% | Global, episodic regional spikes | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Aging Population and Rising Mortality Rates

Longer life expectancy coupled with larger cohorts of seniors, is straining existing morgue infrastructure. Facilities such as the Iowa Office of the State Medical Examiner—originally built for 800 cases but processing 2,000 have secured USD 36.3 million for new autopsy stations, illustrating how caseload pressure turns directly into equipment orders. Wider demographic data show a similar imbalance across U.S. and European countries, prompting administrators to seek high-capacity refrigeration, heavier-duty lifts, and compact racking that fits into retrofitted basements. The mortuary equipment market, therefore, benefits from predictable replacement and expansion cycles that track aging trends rather than discretionary capital budgets.

Expansion of Morgue Facilities and Need for Automation

Hospital upgrades and green-field forensic centers increasingly specify semi-automatic or fully automated workflows with IoT monitoring. Digital twin pilots in pathology labs cut labeling errors by 90% and improve slide quality by up to 30%, proving the operational value of sensors and analytics. New installations combine temperature probes, RFID-tagged cadaver trays, and cloud dashboards so supervisors can monitor conditions remotely. Automation also mitigates labor constraints as experienced mortuary technicians retire faster than replacements arrive, a mismatch that hospital administrators cite when approving cap-ex for innovative lifts and conveyors. Consequently, the mortuary equipment market is witnessing premium pricing for network-ready devices.

Forensic and Pathology Research Funding Growth

Federal programs such as the Bureau of Justice Assistance Strengthening the Medical Examiner-Coroner System grant provide portable X-ray units and fellowship salaries, directly boosting procurement volumes for imaging suites, cutting tables, and biosafety cabinets.[1]Bureau of Justice Assistance, “Strengthening the Medical Examiner-Coroner System Program,” bja.ojp.gov Separately, the National Institute of Justice has funded CT-scan–driven virtual autopsy pilots that save three full-time pathologist positions each year, creating a persuasive ROI case.[2]National Institute of Justice, “Reducing Turnaround Time in Toxicology Screening,” nij.ojp.gov Grants often stipulate modern data-capture equipment, nudging buyers toward IoT-enabled workstations and digital evidence storage hardware. These funding flows keep the mortuary equipment market resilient even when general hospital budgets tighten.

Adoption of Digital Autopsy Workflows

Post-mortem CT and MR imaging have migrated from research to routine, particularly for complex trauma and culturally sensitive cases where minimal invasion is preferred. Mixed-reality headsets now allow pathologists to inspect 3-D reconstructions while standing over the body, reducing repeat incisions and shortening report times. The shift forces facilities to add dedicated scanner bays, advanced workstations, and secure servers, widening the product basket purchased under the mortuary equipment market. Vendors that integrate imaging hardware with autopsy tables and case-management software gain an edge, fostering deeper hardware–software partnerships across the supply chain.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital & Maintenance Costs of Advanced Systems | -0.8% | Global, acute in emerging markets | Medium term (2-4 years) |

| Cultural and Religious Sensitivities Around Post-Mortem Practices | -0.5% | Global, concentrated in Asia Pacific & Middle East | Long term (≥ 4 years) |

| Volatile Supply Chain for Medical-Grade Stainless Steel | -0.4% | Global, severe in Europe & North America | Short term (≤ 2 years) |

| Regulatory Pressure from New Refrigerant Standards (F-Gas Phase-Down) | -0.3% | Europe primary, expanding to other regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital and Maintenance Costs of Advanced Systems

Medical-grade stainless steel prices spiked when molybdenum reached USD 90 per kg in 2023, lifting chassis and racking costs by double-digit percentages. Manufacturers also face the U.S. FDA Quality Management System Regulation deadline that harmonizes with ISO 13485:2016 from February 2026, adding audit and documentation expenses.[3]Food and Drug Administration, “Quality Management System Regulation Final Rule,” fda.gov These inputs push list prices upward, putting automated mortuary carts beyond the reach of many municipal coroners whose annual equipment budgets rarely exceed USD 200,000. Maintenance contracts for sensor-laden systems also cost more than manual tables, prolonging payback periods. As a result, some facilities stagger upgrades, tempering near-term growth in the mortuary equipment market.

Cultural and Religious Sensitivities Around Post-Mortem Practices

In regions where faith traditions emphasize rapid burial or restrict autopsy incisions, standard embalming pumps and dissection suites see limited uptake. Studies of Muslim, Jewish, and Indigenous families show higher refusal rates for full autopsy, prompting coroners to rely on imaging or external examination. East-Asian practices often involve family washing rituals and specialized coffin dimensions that clash with Western-sized racks, forcing local distributors to offer custom trays. Vendors incur extra design costs and longer certification timelines, which slow expansion into high-population markets. Consequently cultural factors remain a structural restraint on the mortuary equipment market despite rising mortality.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Refrigeration Leadership and Lift Innovation

Refrigeration systems retained 38.95% of mortuary equipment market share in 2025, a reflection of universal preservation needs and tighter F-Gas regulations that push buyers toward HFC-free models. Refrigerators and modular coolers anchor every capital project, making this segment the largest contributor to mortuary equipment market size. Growth continues as facilities retrofit to meet phase-down schedules and to add extra chambers for surge capacity during disasters. Vendors differentiate through tighter temperature uniformity, hydrocarbon refrigerants, and embedded data loggers that feed compliance dashboards.

Cadaver lifts and transport trolleys exhibit the fastest 6.78% CAGR because bariatric decedents are more common and worker-injury rules demand mechanical assistance. OEMs now market bariatric lifts rated to 1,000 lb, often with dual-column scissor designs that maintain stability in crowded corridors. Integration with ceiling-mounted track systems further reduces manual handling, a feature valued by unionized hospital staff. Although these lifts occupy a smaller slice of mortuary equipment market size today, their rapid adoption will trim refrigeration dominance over the forecast period. Shelving racks, autopsy tables, embalming pumps, and specialty consumables round out the product mix, each benefitting from incremental upgrades tied to broader facility overhauls.

By Technology: Semi-Automatic Prevalence and IoT Momentum

Semi-automatic equipment held 33.77% revenue in 2025 because it balances affordability with partial labor savings. Programmable height-adjust lifts and push-button tray loaders fall into this tier and remain popular in municipal morgues with budget ceilings. Yet the shift toward network-ready devices is unmistakable. Fully automated carts that move decedents from cooler to table without human push force are growing at 6.12% CAGR, making them one of the brightest niches within the mortuary equipment market.

IoT-enabled modules present the biggest upside. Digital sensors embedded in refrigeration doors transmit humidity and temperature data to dashboards, helping maintain chain-of-custody records acceptable in court proceedings. Predictive maintenance analytics flag compressor wear before failure, preventing evidence spoilage and reducing energy bills. Clinics adopting such systems report 15% lower downtime and 8% lower utility costs within a year, validating the business case for management teams. While manual equipment still sees uptake in low-income settings, procurement preference is clearly shifting toward cloud-connected portfolios, reinforcing the market’s long-run digitization narrative.

By End User: Hospital Dominance and Forensic Laboratory Upswing

Hospitals and clinics controlled 47.25% of mortuary equipment market size in 2025 because they bundle decedent care into broader acute-care services. Large academic centers also use mortuary suites for teaching, thereby justifying investments in ergonomic tables, multi-view camera systems, and RFID-tagged body pouches that integrate with electronic medical records. Regulations mandating temperature logging and infectious-disease controls further elevate hospital spending, locking in their leadership.

Forensic and pathology laboratories represent the fastest-expanding buyers at 8.18% CAGR. National grants earmarked for toxicology, DNA backlogs, and drug overdose investigations pay for CT scanners, robotic saws, and ventilated necropsy hoods—items that command premium margins in the mortuary equipment market. Research institutes additionally require 3-D visualization workstations for teaching and case reconstruction, enhancing demand for GPU-powered servers and specialized software. Funeral homes, disaster-response agencies, and medical schools contribute smaller but steady volumes, often purchasing modular coolers and portable embalming gear that travel with mass-fatality response teams.

Geography Analysis

North America generated 36.88% of 2025 sales, making it the clear leader in the mortuary equipment market. Stronger public funding, mature private autopsy service providers, and rigorous OSHA standards underpin high baseline demand for refrigeration suites, powered lifts, and stainless workstations. The recently approved USD 36.3 million Iowa expansion illustrates how state budgets fund significant capacity additions that immediately translate into equipment orders. Federal grants through the Bureau of Justice Assistance further accelerate procurement of imaging and handling systems. As a result the region expects continued 5%-plus growth even against a high installed base.

Asia Pacific is forecast to expand at 7.16% CAGR, the fastest worldwide. Healthcare modernization programs in China, India, and Southeast Asian economies include morgue upgrades within hospital masterplans. Japan’s concerted push to professionalize death-care services, emphasizing ethical practices and compliance, encourages digital autopsy and IoT-ready coolers, directly lifting segment revenues. Rapid urbanization drives cremation over burial, widening the addressable product scope to include ash-processing equipment. Although cultural resistance influences certain subsegments, the sheer scale of hospital construction and demographic aging allows the mortuary equipment market to flourish across Asia Pacific.

Europe shows mid-single-digit gains anchored by standardized regulations. The 2024/573 F-Gas rule forces the replacement of older HFC-based refrigeration by 2030, creating a regulatory pull for advanced coolers. National health services also invest in bariatric lifts as obesity prevalence rises. Supply chain challenges, especially stainless coil shortages, add cost pressures yet have not derailed expansion plans. Latin America, the Middle East, and Africa present early-stage opportunities where donor-funded hospital projects introduce modern mortuary suites; however, economic volatility and cultural factors limit the conversion of potential into immediate sales.

Competitive Landscape

The mortuary equipment market remains moderately fragmented even as consolidation accelerates. Waud Capital Partners’ 2025 takeover of Mopec Group, one of the largest U.S. autopsy-table makers, signals growing private-equity appetite for specialized medical devices. Regional brands still hold a considerable share, particularly in Europe, where family-owned workshops supply customized stainless units to local hospitals. Yet global healthcare suppliers such as Thermo Fisher Scientific leverage broad distribution networks to cross-sell pathology workstations alongside general lab equipment.

Technology capability is the new battleground. Manufacturers that embed IoT sensors, develop cloud dashboards, and partner with software firms to deliver digital twin solutions differentiate sharply from legacy metal-fabrication shops. Disaster-response modules, such as trailer-mounted coolers and inflatable mortuaries, constitute another white-space arena with heightened interest after recent pandemic and weather-related mass-fatality events. Meanwhile, compliance expertise covering F-Gas, ISO 13485, and local cremation regulations acts as a non-price lever that large vendors use to win multiyear service contracts. In sum, the mortuary equipment market rewards firms that combine material engineering, regulatory advisory, and data analytics skill sets.

Mortuary Equipment Industry Leaders

Roftek Ltd

SM Scientific Instruments Pvt. Ltd

KUGEL medical GmbH & Co. KG

LEEC Ltd

Thermo Fisher Scientific Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Chinese producer YSENMED launched ysenmedmortuary.com to showcase autopsy tables, body freezers, and embalming systems, improving global accessibility and supporting OEM/ODM partnerships.

- July 2024: France-based GPG Granit acquired Isofroid, a specialist in mortuary refrigeration and preservative fluids. This acquisition diversified GPG Granit's portfolio across conservation and memorialization lines and supported overseas expansion.

Global Mortuary Equipment Market Report Scope

As per the scope of the report, mortuaries are places where corpses are well-preserved under hygienic conditions for autopsies or educational, research, legal, and other purposes. Different types of equipment are used in mortuaries for preservation and for shifting and storing the cadavers for various purposes. The mortuary equipment market is segmented by product type and geography. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Refrigeration Units |

| Autopsy Tables & Workstations |

| Cadaver Lifts & Transport Systems |

| Embalming & Preservation Equipment |

| Shelving & Storage Racks |

| Body Bags & Consumables |

| Cremation & Tissue-Disposal Equipment |

| Other Accessories |

| Manual |

| Semi-automatic |

| Fully-Automated / IoT-enabled |

| Hospitals & Clinics |

| Forensic & Pathology Labs |

| Academic & Research Institutes |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Refrigeration Units | |

| Autopsy Tables & Workstations | ||

| Cadaver Lifts & Transport Systems | ||

| Embalming & Preservation Equipment | ||

| Shelving & Storage Racks | ||

| Body Bags & Consumables | ||

| Cremation & Tissue-Disposal Equipment | ||

| Other Accessories | ||

| By Technology | Manual | |

| Semi-automatic | ||

| Fully-Automated / IoT-enabled | ||

| By End User | Hospitals & Clinics | |

| Forensic & Pathology Labs | ||

| Academic & Research Institutes | ||

| Other End Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the size of the global mortuary equipment market in 2026?

The mortuary equipment market size is USD 1.83 billion in 2026.

How fast is demand for cadaver lifts growing?

Cadaver lifts and transport systems are projected to grow at 6.78% CAGR through 2031.

Which region leads in revenue for mortuary equipment?

North America accounts for 36.88% of global sales thanks to robust forensic funding and private infrastructure.

Why are IoT-enabled mortuary devices becoming popular?

Connected sensors cut equipment downtime, improve compliance, and align with hospital digitization strategies, driving accelerated adoption.

What regulatory change is influencing refrigeration purchases in Europe?

The EU F-Gas Regulation 2024/573 mandates phasedown of high-GWP refrigerants, prompting replacement of legacy mortuary coolers.

How does cultural sensitivity affect equipment sales?

Religious or cultural objections to invasive autopsies reduce demand for embalming pumps and dissection tools in certain regions, slowing market penetration.

Page last updated on: