Plastic Surgery Instruments Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.73 Billion |

| Market Size (2031) | USD 2.48 Billion |

| Growth Rate (2026 - 2031) | 7.50% CAGR |

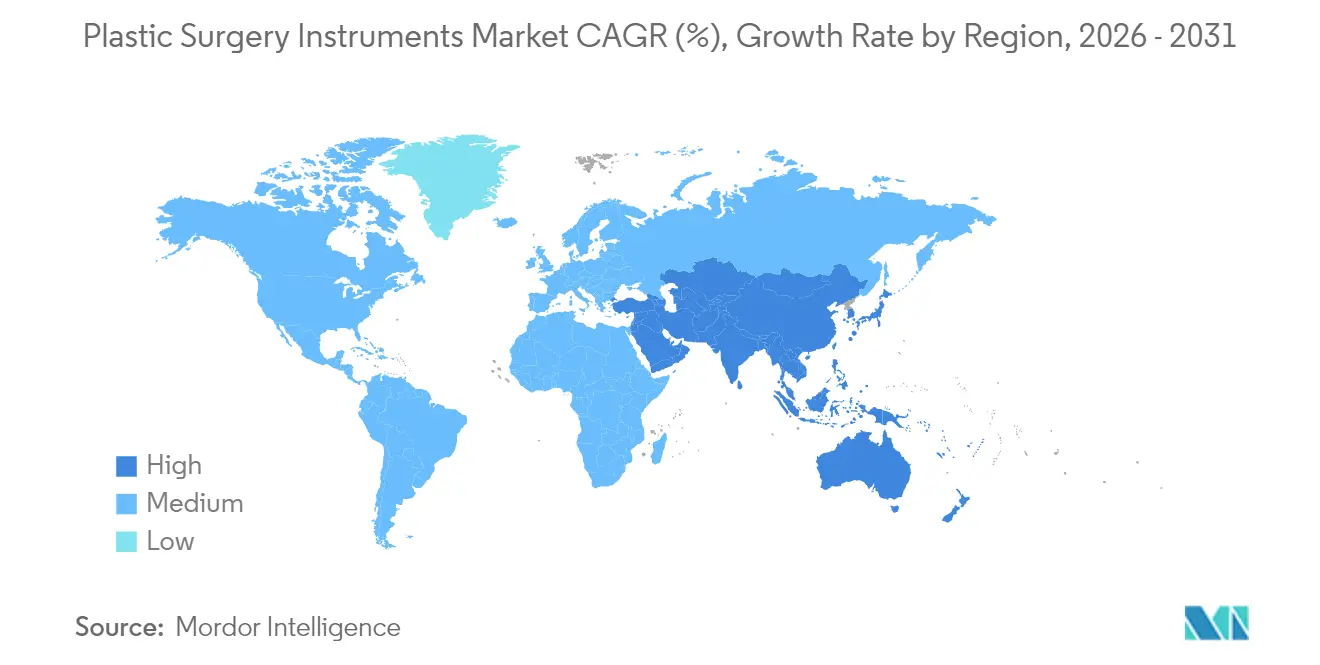

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

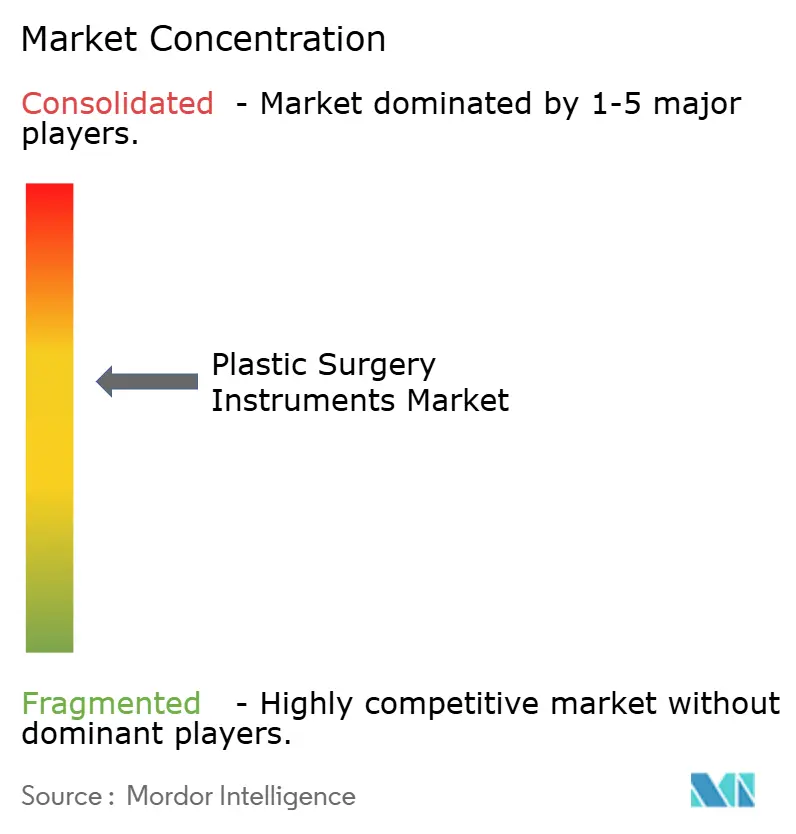

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Plastic Surgery Instruments Market Analysis by Mordor Intelligence

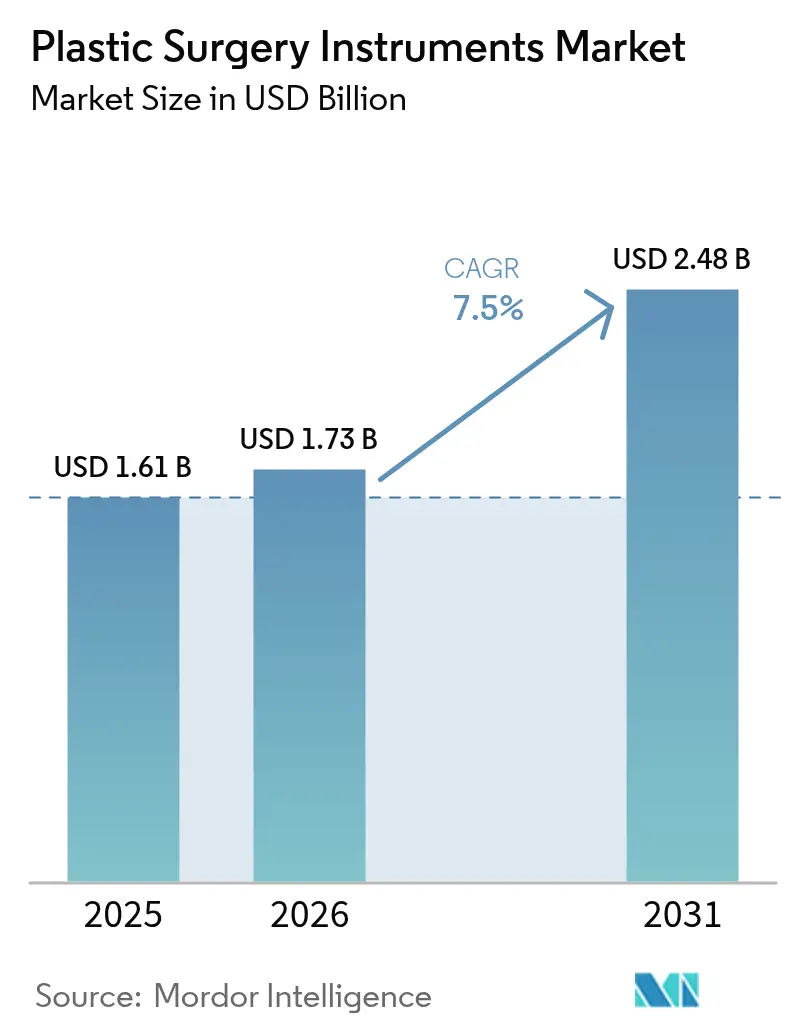

The Plastic Surgery Instruments market size is expected to grow from USD 1.61 billion in 2025 to USD 1.73 billion in 2026 and is forecast to reach USD 2.48 billion by 2031 at 7.50% CAGR over 2026-2031.

Strong growth reflects rising global procedure volumes, rapid uptake of electrosurgical systems, and sustained demand from both cosmetic and reconstructive surgery. Electrosurgical devices outpace traditional handheld tools with a 9.89% CAGR as surgeons adopt energy-based technologies that shorten operative times and minimize tissue trauma. Asia-Pacific leads regional momentum with a 13.23% CAGR, supported by medical tourism and expanding middle-class purchasing power, while North America retains leadership through a 42.34% revenue share anchored by early technology adoption and high discretionary income. Hospitals remain the dominant care setting, but specialty clinics and ambulatory centers are capturing share as minimally invasive techniques enable same-day discharge.

Key Report Takeaways

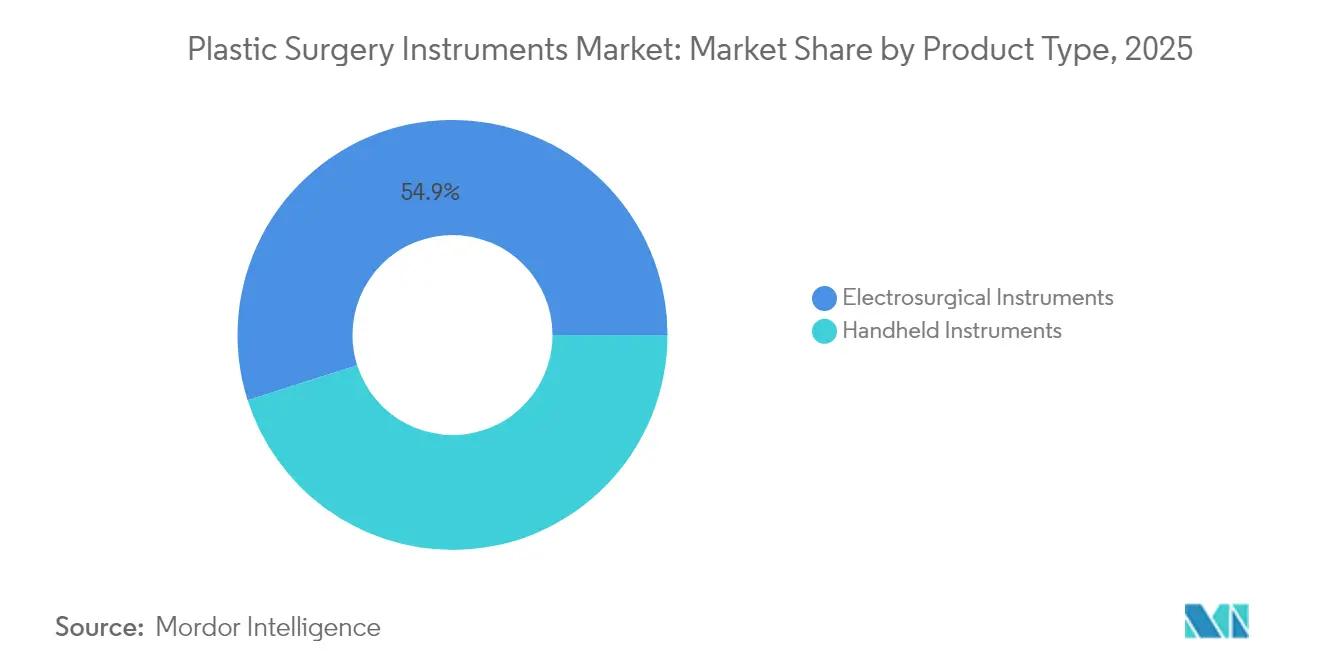

- By product type, handheld instruments commanded 45.10% of the plastic surgery instruments market share in 2025, while electrosurgical systems are projected to post the fastest 9.77% CAGR through 2031.

- By procedure, cosmetic surgery held 58.20% revenue share in 2025; breast reconstruction is forecast to expand at 10.37% CAGR to 2031.

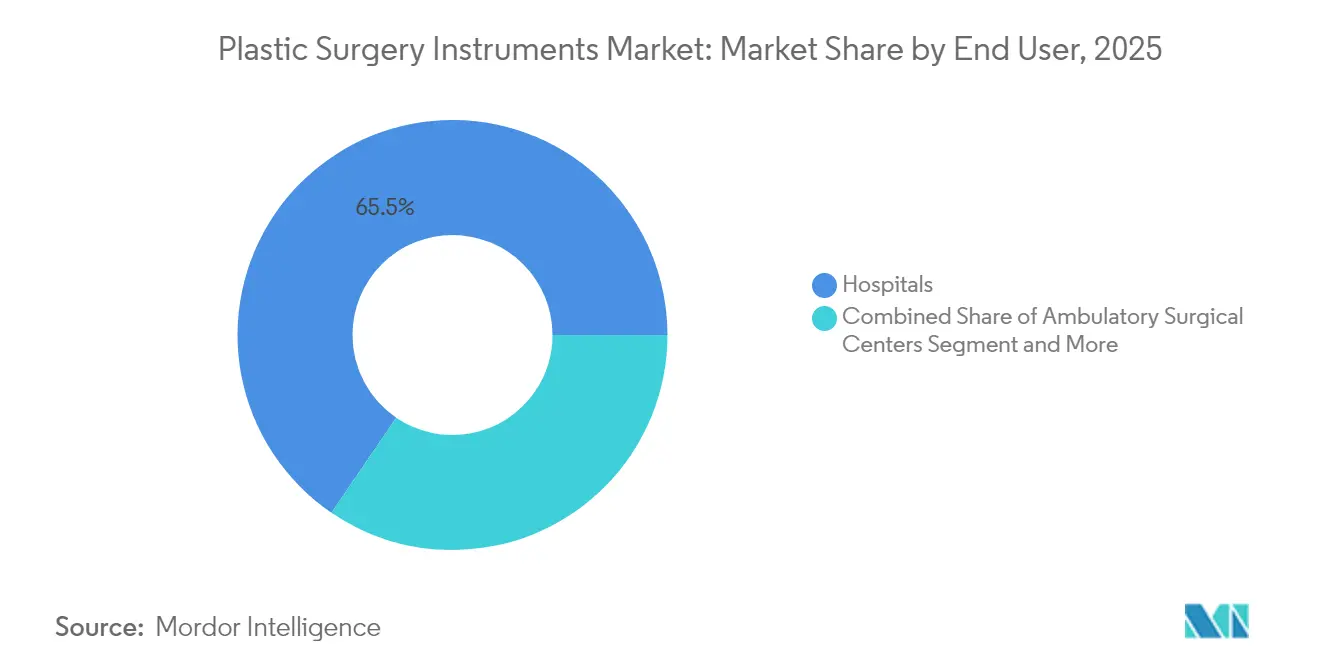

- By end user, hospitals captured 65.48% of the plastic surgery instruments market size in 2025, although specialty clinics are advancing at an 11.81% CAGR.

- By geography, North America led with 41.94% revenue in 2025, whereas Asia-Pacific is set to grow at a 13.05% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Plastic Surgery Instruments Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Global Procedural Volumes in Cosmetic Surgery | +1.8% | Global, with APAC leading growth | Medium term (2-4 years) |

| Shift Toward Minimally-Invasive & Electrosurgical Techniques | +1.5% | North America & EU, expanding to APAC | Short term (≤ 2 years) |

| Aging Population Seeking Age-Related Reconstructive Work | +1.2% | North America & Europe primarily | Long term (≥ 4 years) |

| Expanding Medical Tourism Hubs | +0.9% | APAC core, spill-over to MEA | Medium term (2-4 years) |

| OR Tray-Optimization Cuts Hospital Costs, Boosts Instrument Refresh Cycles | +0.7% | Global, led by cost-conscious markets | Short term (≤ 2 years) |

| 3-D Printed Patient-Specific Guides Shortening Re-Op Rates | +0.5% | North America & EU advanced centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Global Procedural Volumes in Cosmetic Surgery

Surging demand for rhinoplasty, liposuction, and male aesthetic procedures in India, Brazil, and the United States enlarges the plastic surgery instruments market by increasing equipment turnover requirements. High-volume practices now prioritize reusable forceps and precision cutters engineered for extended sterility cycles. Manufacturers are scaling production of anatomy-specific cannulas and micro-scissors to align with diverse patient characteristics. The emphasis on volume efficiency accelerates instrument refresh rates, benefiting suppliers able to guarantee durability under intensive reprocessing. Hospitals that optimize tray contents have realized annual savings of USD 159,600, which can be redirected toward next-generation devices.

Shift Toward Minimally-Invasive & Electrosurgical Techniques

Energy-based devices such as Harmonic ACE+7 scalpels cut breast reconstruction operative time to 179 minutes versus 286 minutes with legacy cautery and nearly halve intraoperative bleeding. Second-generation radio-frequency liposuction systems reduce complication rates to 0.7% from 8.3% for first-generation units, prompting rapid replacement of older platforms.[1]PubMed Database, “Comparative outcomes of electrocautery versus ultrasonic dissection in breast surgery,” National Library of Medicine, pubmed.ncbi.nlm.nih.gov Bio-Active Electrode technology yields 5–8 micron lateral tissue damage, vastly narrower than the 20–90 micron range of conventional electrodes, which improves cosmetic outcomes and pathology accuracy.[2]Global Journal Editors, “Bio-Active Electrode reduces thermal spread,” Global Journal of Otolaryngology, juniperpublishers.com As a result, hospital procurement teams are accelerating capital budgeting for precision energy systems.

Aging Population Seeking Age-Related Reconstructive Work

Mastectomy patients increasingly opt for immediate implant-based reconstruction that demands instruments capable of atraumatic tissue handling in older individuals with slower healing. Smooth-surface tissue expanders are gaining acceptance over textured variants to mitigate late adverse events. Novel biomaterials produced through 3D bioprinting aim to curb capsular contracture rates, a complication that disproportionately affects senior cohorts. Instrument makers are responding with ergonomically balanced retractors and adaptive electrosurgical tips that reduce surgeon fatigue during delicate dissections.

Expanding Medical Tourism Hubs

Thailand and India attract a growing influx of international patients by combining cost advantages with international accreditation, stimulating demand for premium electrosurgical platforms that satisfy multiple regulatory standards. Instrument standardization across tourist centers supports bulk procurement agreements, lowering per-unit costs and encouraging adoption of robotic and AI-enabled systems. Cultural preferences in Asia favor less invasive facial contouring, which fuels the development of micro-instruments and articulating endoscopes optimized for small incisions.

Restraints Impact Analysis of Plastic Surgery Instruments Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Post-Operative Complications & Infection Risk | -1.3% | Global, acute in developing markets | Short term (≤ 2 years) |

| High Capital Cost of Powered/Electrosurgical Systems | -0.9% | Cost-sensitive markets globally | Medium term (2-4 years) |

| Growing ESG Scrutiny on Single-Use Instruments' Waste Stream | -0.6% | EU & North America primarily | Long term (≥ 4 years) |

| Supply-Chain Exposure to Cluster Geopolitical Risks | -0.4% | Global, concentrated in Asia supply chains | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Post-Operative Complications & Infection Risk

Implant-based breast reconstruction shows 8.53% infection rates that trigger implant removal in 31.2% of cases and abandonment in 20.7% of infected patients. Microbiological audits reveal skin flora contamination on surgical packs due to inadequate sterilizer maintenance and improper handling. No-touch expander techniques reduced infections in controlled trials, indicating that redesigned clamps and insertion sleeves can mitigate risk. Persistent infection concerns elevate sterilization costs and may defer elective surgeries.

High Capital Cost of Powered/Electrosurgical Systems

Advanced platforms demand upfront investments that smaller clinics often defer. Escalating tariffs of up to 125% on Chinese components heighten acquisition costs for suppliers and may slow innovation. Medtronic has responded by consolidating distribution centers to offset rising logistics expenses. Facilities counterbalance cost pressures through instrument-tray optimization, with one study reporting USD 285,756 in yearly savings from reducing redundant tools. Nevertheless, high capital thresholds can restrict adoption rates in emerging markets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Plastic Surgery Instruments Market Segment Analysis

By Product Type:

Electrosurgical Innovation Accelerates Market EvolutionHandheld devices accounted for 45.10% of the plastic surgery instruments market share in 2025, serving as essential tools across various procedures. Electrosurgical systems, although smaller in base, are poised to surge at a 9.77% CAGR as surgeons seek precision and hemostatic efficiency. LigaSure technology enables 90.2% bloodless pocket creation, compared to 59.4% with traditional cautery, thereby markedly lowering postoperative drain volumes. This clear outcome differential fuels rapid capital allocation toward energy-based generators and innovative electrodes.

Bipolar platforms are increasingly replacing monopolar systems in the plastic surgery instruments market, reducing compressive forces and tissue trauma. AI-integrated consoles such as Stryker SurgiCount+ provide real-time blood-loss analytics that support surgical quality monitoring. As disposable-tip models proliferate, suppliers align with hospital sustainability goals by offering reprocessable handpieces that keep consumable costs in check.

By Procedure:

Reconstructive Surgery Drives Premium Instrument DemandCosmetic surgery retained 58.20% revenue in 2025, yet breast reconstruction is advancing at a 10.37% CAGR as implant technology improves survivorship quality. Second-generation radio-frequency liposuction now posts only 0.7% complication rates versus 8.3% for legacy systems, underscoring the procedural shift toward safer energy modalities.

Reconstructive techniques increasingly rely on patient-specific 3D-printed guides that shorten operating time and raise accuracy. Biomaterial breakthroughs such as Integra dermal templates deliver 90.2% success in facial defect repairs. These advances expand the plastic surgery instruments market size for niche tools like micro-saws and low-heat cutters engineered for delicate tissue interfaces.

By End User:

Specialty Clinics Transform Care Delivery ModelsHospitals maintained a 65.48% market share in the plastic surgery instruments market in 2025 by offering multidisciplinary support for complex cases. Specialty clinics are on track for an 11.81% CAGR, attracting patients with focused expertise and efficient scheduling. Instrument manufacturers respond with compact electrosurgical generators that fit space-constrained procedure rooms.

Ambulatory centers benefit from optimized tray designs that cut breast lumpectomy setup time to 4 minutes and reprocessing costs to USD 26.01, down from USD 49.98. Portable robotic arms support intricate dissections in outpatient settings. These innovations aim to improve workflow efficiency and surgical accuracy without relying on large-scale operating rooms. These trends diversify ordering patterns toward lightweight retractors and quick-connect endoscopes.

Geography Analysis

North America Plastic Surgery Instruments Market

North America has the highest adoption of AI-guided energy platforms and advanced robotic systems, safeguarding its 41.94% market share of plastic surgery instruments in 2025 despite rising competition. Continuous FDA engagement, such as February 2025 dermal-filler hearings, underpins a rigorous safety culture that shapes device rollout timelines. Canada and Mexico complement U.S. demand by serving cross-border patients and offering cost-conscious packages.

APAC Plastic Surgery Instruments Market

Asia-Pacific posts a 13.05% CAGR propelled by Thailand’s accreditation-led tourism, India’s skilled surgeon surplus, and robust domestic demand in China and Japan. Korean clinics set aesthetic trends that spread throughout the region, increasing uptake of micro-powered cannulas and precision endoscopic cutters. Market entrants partner with local distributors to navigate heterogeneous regulatory environments.

EMEA Plastic Surgery Instruments Market

Europe maintains consistent growth driven by Germany, France, and the United Kingdom where public reimbursement supports reconstructive cases. Circular-economy policies spur hospitals to convert from single-use to reprocessable devices, influencing supplier product lines. Eastern European states leverage cost advantages to court intra-EU medical travelers. The Middle East and Africa accelerate instrument purchases for new surgical hubs in the Gulf, while South Africa functions as a regional skills center.

Competitive Landscape

Competition within the plastic surgery instruments market remains moderate. Johnson & Johnson, Stryker, and Medtronic leverage extensive catalogs and global reach, whereas focused entities such as KLS Martin and Integra LifeSciences capture niche segments through customization. Medtronic’s November 2024 acquisition of Fortimedix Surgical enriches its articulating-instrument portfolio and signals a tightening race for precision mechanics.

Technology leadership rests on energy efficiency, ergonomic enhancements, and digital integration. Stryker’s AI-enabled SurgiCount+ system automates blood-loss estimation and sponge tracking, offering quantifiable workflow savings. Johnson & Johnson’s 2024 shift to a unified MedTech identity aims to streamline innovation pipelines and sharpen market messaging. Niche disruptors bring 3D-printing capabilities for patient-specific guides that shorten revision cycles, while eco-centric startups experiment with biodegradable polymer handles that address hospital sustainability targets.

Price competition intensifies as procurement teams deploy total-cost-of-ownership analyses that weigh consumable expenses and sterilization logistics. Companies respond with hybrid reprocessing models allowing single-use tips on reusable handles, balancing safety with environmental scrutiny. Strategic partnerships between device makers and outpatient chains are emerging to secure dedicated instrument volumes.

Plastic Surgery Instruments Industry Leaders

Tekno-Medical Optik-Chirurgie GmbH

Zimmer Biomet

KLS Martin Group

B. Braun Melsungen

Integra LifeSciences

- *Disclaimer: Major Players sorted in no particular order

Plastic Surgery Instruments Market Companies Covered in this Report

- KLS Martin Group

- Integra LifeSciences

- Zimmer Biomet

- B. Braun

- Sklar Surgical Instruments

- Tekno-Medical Optik-Chirurgie

- BMT Medizintechnik

- Anthony Products

- Bolton Surgical

- Surgicon Pvt.

- Blink Medical

- Medtronic

- Stryker

- Johnson & Johnson

- Conmed

- Olympus

- Ethicon

- Boston Scientific

- MicroAire

- Arthrex

Market Opportunities and Future Outlook

Energy-based and microsurgical workflows are opening whitespace for instrument makers that can pair precision electrosurgery with compatible, procedure-specific accessories. The U.S. commercial launch of Medical Microinstruments (MMI) Robotic Suture for the Symani Surgical System (April 2026) highlights rising demand for dedicated micro-instruments and sutures designed for motion scaling and tissue handling in reconstructive use cases, complementing the report trend toward minimally invasive and electrosurgical techniques.

In Europe, MDR compliance updates are pushing opportunities around validated reprocessing and biocompatibility documentation, areas that directly affect reusable handheld and electrosurgical accessories. Commission Implementing Regulation (EU) 2026/977 (4 May 2026) sets more uniform notified-body conformity assessment requirements, while June 2026 OJEU updates to harmonized standards added EN ISO 10993-1:2025 (biocompatibility) and EN ISO 15883-2:2025 (washer-disinfectors for surgical instruments). These changes favor suppliers that can provide complete evidence packages, sterilization-compatible designs, and service support for hospitals and specialty clinics seeking instrument refreshes without disrupting reprocessing workflows.

Recent Industry Developments in Plastic Surgery Instruments Market

- June 2026: Zimmer Biomet announced an agreement to acquire the iovera cryoneurolysis system from Pacira BioSciences. The deal expands non-opioid pain management options and supports elective procedural pathways, potentially increasing utilization of surgical instrument sets across orthopedic and adjacent reconstructive settings.

- February 2026: KLS Martin Group announced 2025 performance and outlined a 2026 capex program focused on infrastructure, digitalization, and production and development structures to drive automation and capacity upgrades, improving lead times and customization for specialty surgical instrumentation.

- November 2024: Medtronic completed the acquisition of Fortimedix Surgical, adding articulating instrumentation capabilities that complement energy-based procedure portfolios and reinforce competition around precision mechanics and minimally invasive access tools used in plastic and reconstructive surgery.

Plastic Surgery Instruments Market Report Scope and Research Methodology

Market Definition and Coverage

This market includes revenue earned from instruments used by surgeons and clinical teams to perform cosmetic and reconstructive plastic surgery, covering core handheld tools and procedure-support instruments used in operating rooms and outpatient settings.

Scope exclusions (for clarity): Consumables such as sutures, implants, and post-operative wound dressings are not counted in this market.

Segments Covered in This Report

- By Product Type

- Handheld Instruments

- Forceps

- Scissors

- Retractors

- Others

- Electrosurgical Instruments

- Bipolar Instruments

- Monopolar Instruments

- Handheld Instruments

- By Procedure

- Cosmetic Surgery

- Breast Procedures

- Face & Head Cosmetic Surgery

- Body & Extremities Procedures

- Reconstructive Surgery

- Breast Reconstruction

- Congenital Deformity Correction

- Tumor Removal

- Other Reconstructive Surgeries

- Cosmetic Surgery

- By End User

- Hospitals

- Ambulatory Surgical Centers

- Specialty & Cosmetic Clinics

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research starts with building a clean view of procedure volumes, care settings, and safety and sterilization requirements that shape instrument demand. We refer to public sources such as the American Society of Plastic Surgeons procedure statistics, WHO health system indicators, OECD health data, and US FDA device databases for approvals, recalls, and safety notices.

To translate activity into market value, we also review trade and customs releases (where available), peer-reviewed surgical journals that discuss technique shifts and instrument preferences, and hospital and ambulatory surgery center publications that indicate case mix changes. Company filings, product catalogs, and investor presentations are used to understand portfolio breadth, average pricing logic, and replacement patterns, with selective support from paid subscriptions for company financials and patent databases to confirm innovation direction. The sources listed here are illustrative only, and many other public and paid references were used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work is used to pressure-test instrument mix per procedure, typical replacement cycles, and how single-use versus reusable choices differ by facility type and sterilization capacity. We speak with clinical users, distributors, and manufacturing side experts across major regions so that gaps from public data, especially around pricing and adoption timing, can be closed with realistic assumptions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 39% | CXOs: 15% | APAC: 50% |

| Mid tier: 45% | Functional/Unit leaders: 41% | EMEA: 29% |

| Smaller Players: 16% | Managers: 44% | Americas: 21% |

Market-Sizing & Forecasting

Sizing begins with a top-down build where procedure volumes by key surgery types are mapped to typical instrument sets, and then adjusted for setting mix between hospitals, ambulatory surgical centers, and specialty clinics. Once that demand pool is formed, average selling prices are applied using a practical split between reusable instruments (modeled through replacement rates) and single-use items (modeled through per-procedure usage).

Inputs that matter in this market include the number of cosmetic and reconstructive procedures performed, the share of minimally invasive and energy-based techniques that change tool preference, sterilization and infection-control practices that influence disposable adoption, price differences between handheld and electrosurgical categories, and import dependence in markets with limited local manufacturing. Forecasts are produced using scenario analysis anchored to procedure growth expectations and expert views on adoption timing, and results are then checked with selective bottom-up approximations such as sampled product-level price points, distributor channel checks, and supplier revenue exposure where disclosures allow. Where coverage gaps exist for smaller private suppliers, we use conservative penetration assumptions and validate them through follow-up expert feedback before finalizing totals.

Data Validation & Update Cycle

Outputs are validated through triangulation across independent signals such as procedure counts, care setting expansion, and observed pricing movement in catalogs and tenders, and then any large variances are reviewed and reconciled. If a sub-segment grows faster than the procedure pool would suggest, the model is revisited to confirm that mix shifts such as higher electrosurgical adoption are truly supported.

Before sign-off, the model and assumptions go through multiple analyst reviews, and re-contacts are triggered when expert feedback conflicts with desk indicators or when a material event changes supply or demand. Reports are refreshed annually, with interim updates when major regulatory actions, pricing shocks, or procedure-volume changes are observed, and a final pre-delivery pass is completed so the numbers reflect the latest view.

Mordor Intelligence's Plastic Surgery Instruments Market Size Versus Other Published Estimates

Published market values for plastic surgery instruments can differ even when the topic name looks identical, because each publisher draws the line differently on what is counted and how demand is rebuilt from procedure activity. Differences are also created by the year chosen as the base, the way prices are converted across currencies, and how fast single-use and energy-based tools are assumed to penetrate routine practice.

The main gap comes from whether electrosurgical systems and procedure-linked accessory devices are included alongside handheld tools, where Mordor Intelligence counts these categories only when they are used directly inside cosmetic and reconstructive plastic surgery workflows, and keeps adjacent consumables like sutures and implants out of scope. Some estimates lean more on broad surgical equipment spending and then apply a share assumption, which can inflate totals in countries where outpatient clinics dominate and instrument replacement cycles are longer. Others may use a conservative price curve that does not reflect premium mix in high-volume aesthetic hubs, or they may not refresh procedural volume inputs after visible demand shifts.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.61 B (2025) | |

| Global Consultancy A | USD 1.51 B (2024) | Uses a different base year and frames product scope around broad handheld and electrosurgery groups without clearly separating procedure-specific plastic surgery use from wider surgical instrument demand, which can shift the counted pool. |

| Industry Publisher B | USD 1.38 B (2025) | Applies slower adoption and pricing progression for higher-value electrosurgical instruments and disposable kits, and the longer forecast horizon often relies on higher-level assumptions that are not consistently reconciled back to procedure volumes. |

The spread across published values is mostly explained by what gets included around electrosurgery, how procedure volumes are translated into instrument usage, and how replacement cycles are treated across care settings. By keeping scope tied to procedure-relevant instrument categories and using check points like procedure activity and setting mix, our estimate stays easier to trace and repeat when assumptions need to be updated.

Key Questions Answered in the Report

What is the current size of the plastic surgery instruments market?

The market is valued at USD 1.73 billion in 2026.

How fast is the plastic surgery instruments market expected to grow?

It is projected to expand at a 7.50% CAGR, reaching USD 2.48 billion by 2031.

Which product segment is growing the quickest?

Electrosurgical instruments lead with a 9.77% CAGR due to precision and reduced operative times.

Why is Asia-Pacific considered the growth engine for plastic surgery instruments?

The region benefits from medical tourism, rising incomes, and supportive demographics, resulting in a 13.05% CAGR.

What restraints could slow market expansion?

Post-operative infection risks and the high capital cost of energy-based systems exert the greatest downward pressure.

Which companies are leading in technological innovation?

Johnson & Johnson, Stryker, and Medtronic drive progress through acquisitions, AI integration, and articulated instrumentation advances.

Page last updated on: