Tooth Regeneration Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

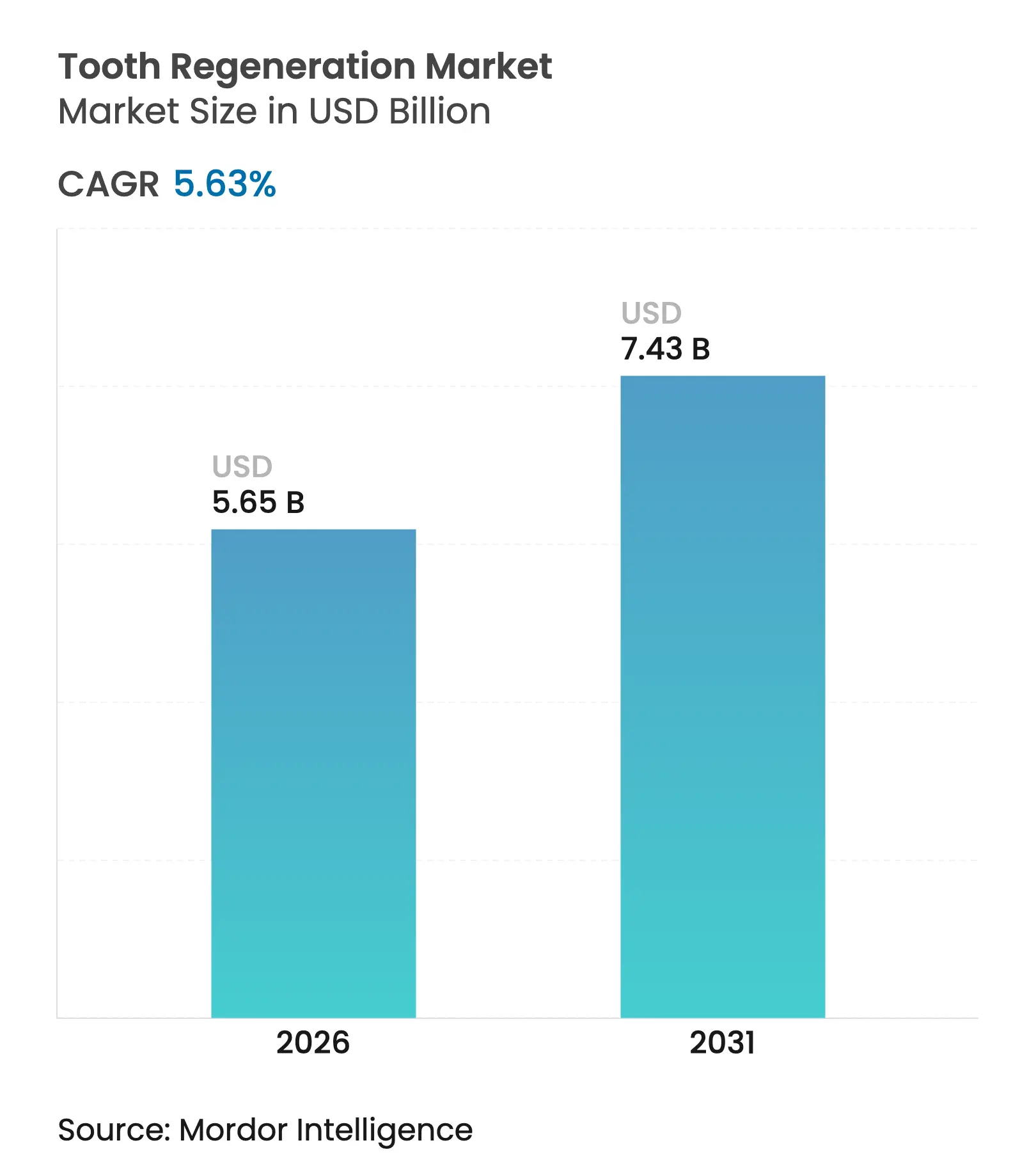

| Market Size (2026) | USD 5.65 Billion |

| Market Size (2031) | USD 7.43 Billion |

| Growth Rate (2026 - 2031) | 5.63 % CAGR |

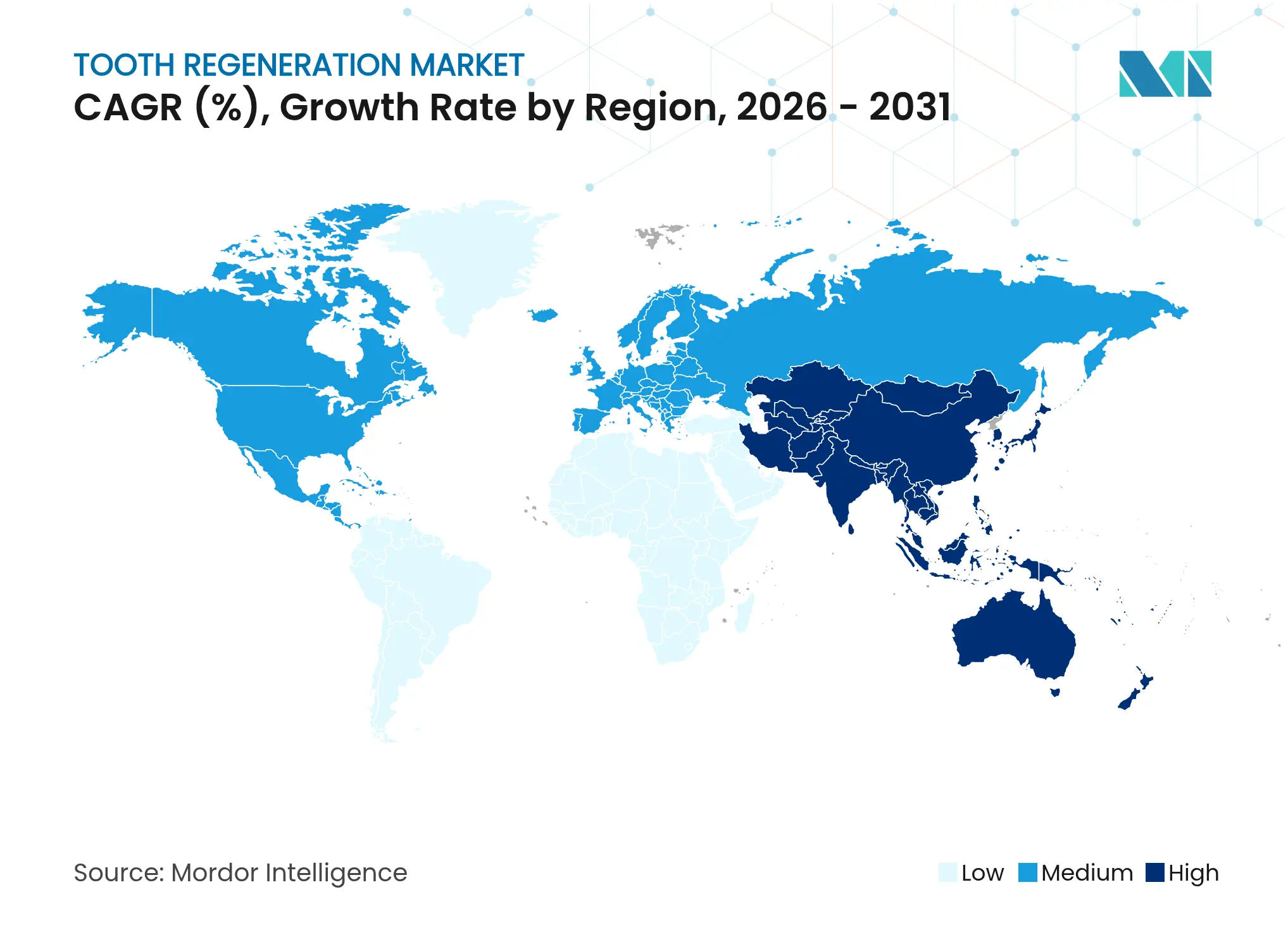

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Tooth Regeneration Market Analysis by Mordor Intelligence

The tooth regeneration market size was valued at USD 5.35 billion in 2025 and estimated to grow from USD 5.65 billion in 2026 to reach USD 7.43 billion by 2031, at a CAGR of 5.63% during the forecast period (2026-2031). Rising clinical validation of biologically driven approaches, exemplified by Toregem BioPharma’s first-in-human TRG-035 study that began in September 2024, underscores growing confidence in therapies that stimulate natural odontogenesis. The tooth regeneration market benefits from demographic ageing, surging demand for aesthetic dentistry and supportive regulatory frameworks in leading economies. North America anchors early adoption due to mature reimbursement systems, whereas Asia-Pacific is accelerating on the back of favorable fast-track pathways and prolific venture activity. Technology momentum centres on stem-cell platforms that dominate revenue, while molecular therapeutics and AI-guided scaffold optimisation enter an aggressive scale-up phase. Venture capital worth USD 400.2 million flowed into oral-health start-ups during 2024, reinforcing investor conviction in next-generation dental biotechnology.

Key Report Takeaways

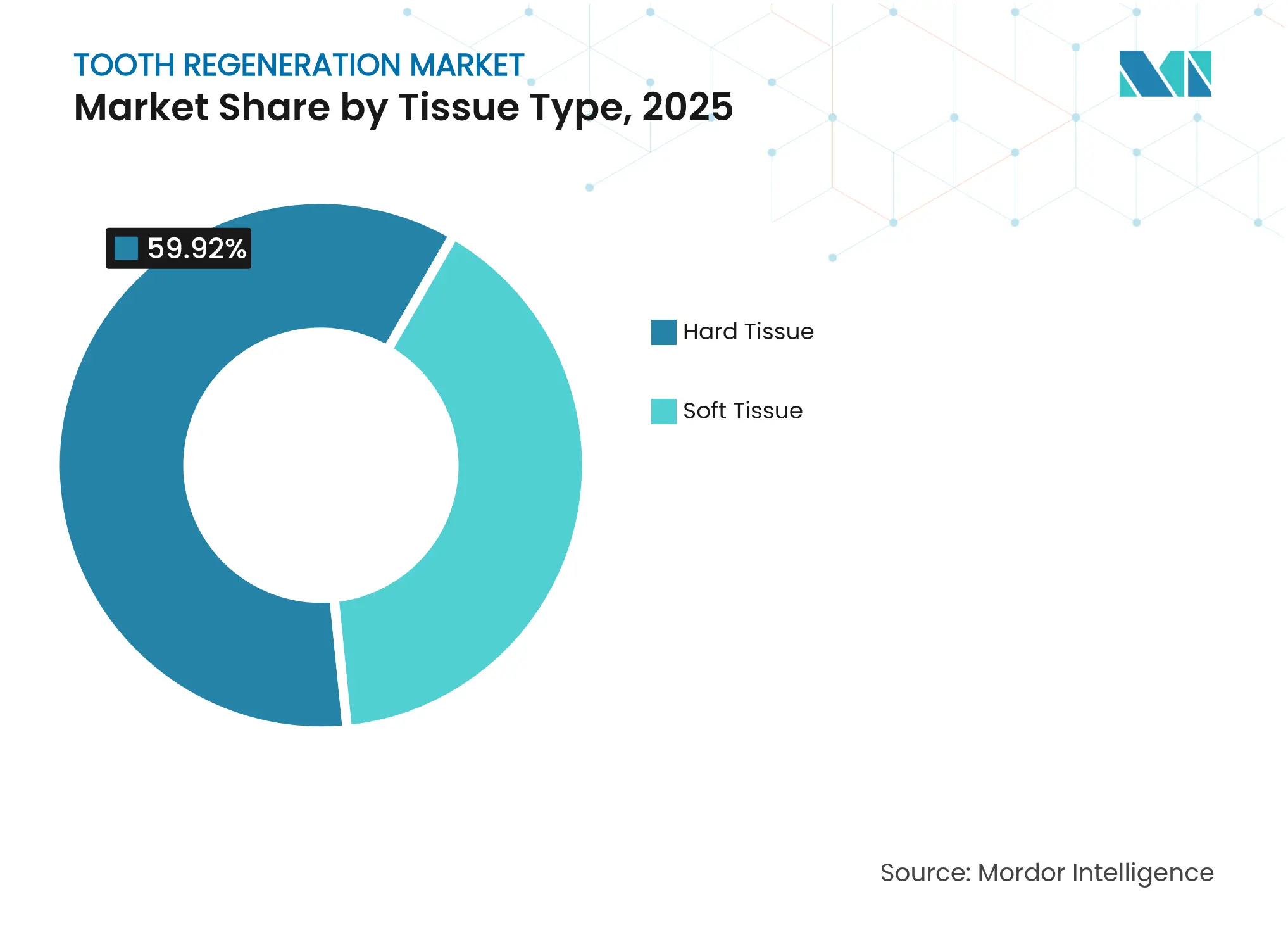

- By tissue type, hard-tissue applications captured 59.92% of tooth regeneration market share in 2025, whereas soft-tissue solutions are projected to climb at a 14.78% CAGR through 2031.

- By technology, stem-cell platforms held 43.02% of revenue in 2025, while small-molecule and peptide modalities are poised for an 18.09% CAGR to 2031.

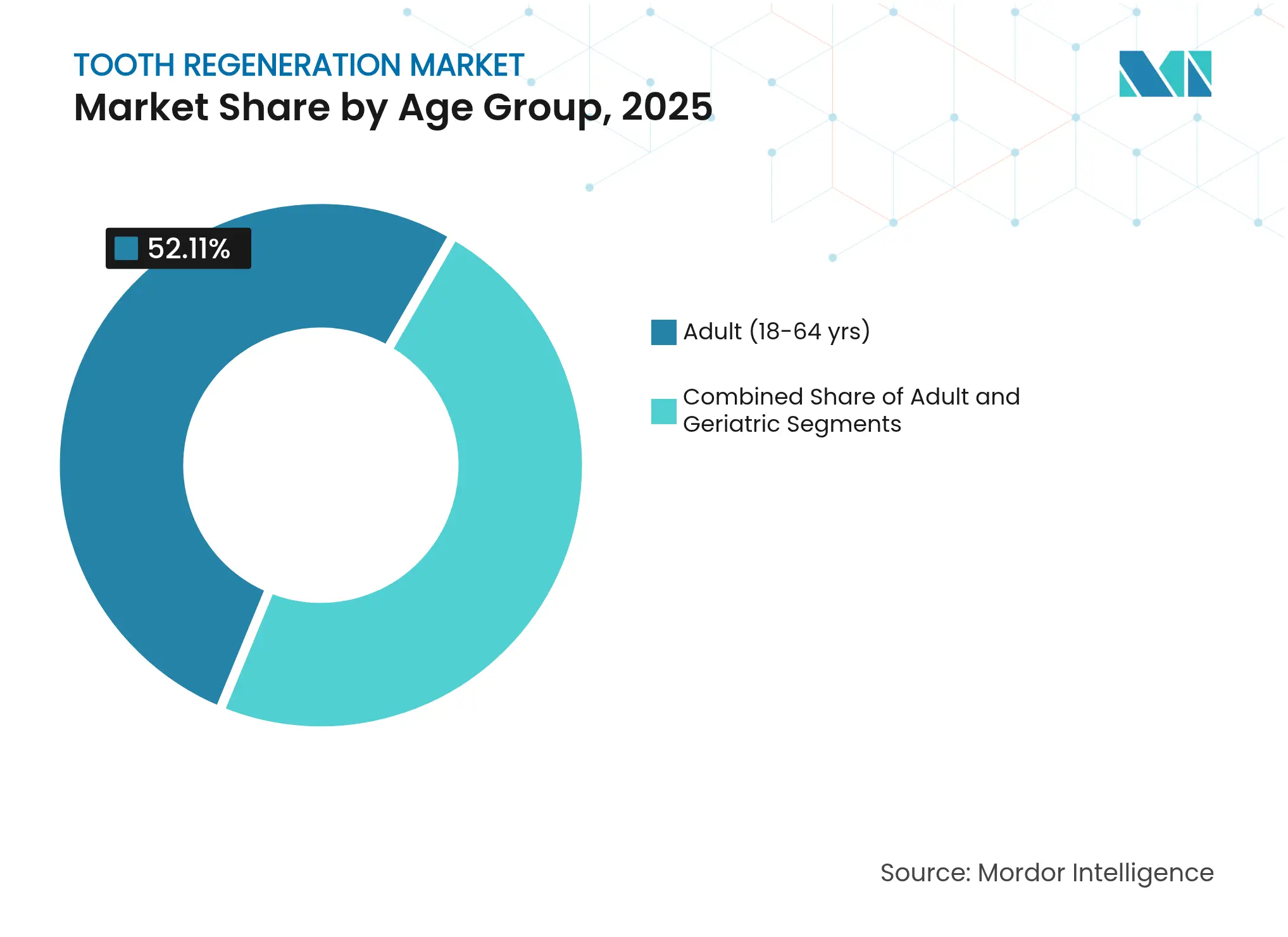

- By age group, adults accounted for 52.11% of demand in 2025; the paediatric segment is forecast to expand at 16.12% CAGR across 2026-2031.

- By end user, specialised dental and maxillofacial clinics commanded 51.58% of the 2025 revenue pool, whereas academic and research institutes will experience the fastest 16.95% CAGR.

- By geography, North America led with 40.12% revenue share in 2025, while Asia-Pacific is projected to record the highest 15.22% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Tooth Regeneration Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rising prevalence of dental disorders

Rising prevalence of dental disorders

| +1.5% | Global; higher in ageing populations of North America & Europe | Long term (≥ 4 years) | (~) % Impact on CAGR Forecast:

+1.5%

| Geographic Relevance:

Global; higher in ageing populations of North America

& Europe

| Impact Timeline:

Long term (≥ 4 years)

|

Rapid advances in regenerative-medicine toolkits

Rapid advances in regenerative-medicine toolkits

| +2.1% | Global; early uptake in Asia-Pacific & North America | Medium term (2-4 years) | |||

Increasing geriatric population worldwide

Increasing geriatric population worldwide

| +0.8% | Global; concentrated in developed markets | Long term (≥ 4 years) | |||

Growing demand for aesthetic dentistry & smile

restoration

Growing demand for aesthetic dentistry & smile

restoration

| +1.2% | North America & Europe, expanding to Asia-Pacific | Medium term (2-4 years) | |||

Fast-track regulatory designations for dental

tissue-engineered products

Fast-track regulatory designations for dental

tissue-engineered products

| +0.6% | North America, Europe, Japan | Short term (≤ 2 years) | |||

Acceleration of venture funding in dental biotech

start-ups

Acceleration of venture funding in dental biotech

start-ups

| +0.9% | Global; clustered in North America & Asia-Pacific | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Rising Prevalence of Dental Disorders

Tooth-loss incidence escalates as caries and periodontal disease remain among the most common chronic conditions worldwide. More than 280 million older adults experienced oral disorders in 2024, underscoring the long-term public-health burden[1]Rakhee Patel & Jennifer Gallagher, “Healthy ageing and oral health: priority, policy and public health,” Nature Reviews, nature.com. Such morbidity drives payers and clinicians to prioritise treatments that preserve natural dentition rather than resort to implants. Epidemiological studies link tooth loss with compromised nutrition and systemic metabolic disorders, nudging policymakers to integrate oral regeneration into holistic health programmes. The tooth regeneration market therefore positions itself not merely as a restorative alternative but as a preventive solution that can lower lifetime expenditure on prosthetics and manage comorbidities. Commercial pipelines now include targeted hard-tissue drugs and bioactive strips aimed at early-stage lesions, broadening therapeutic reach into minimally invasive care.

Rapid Advancements in Regenerative-Medicine Toolkits

The toolbox underpinning regenerative dentistry has widened from scaffold-plus-cells models to data-driven discovery. Machine-learning algorithms are optimising stem-cell differentiation conditions, shortening lab cycles and improving lot-to-lot consistency. Breakthrough work using small molecules to coax ameloblast-like cells from embryonic stem cells demonstrates the feasibility of cell-free protocols that bypass complex cell banking. Three-dimensional bioprinting replicates hierarchical enamel–dentin structures, while exosome therapy offers lower immunogenicity and easier logistics compared with whole-cell delivery. Growth-factor research, such as FGF9’s role in enamel formation, reflects deeper mechanistic insight that supports precision dosing. Collectively, these advances accelerate translation, reduce cost of goods over time and expand indications—from single-tooth replacement to full-arch restoration.

Increasing Geriatric Population Worldwide

Global life expectancy continues to rise, yet edentulism prevalence remains stubbornly high among seniors. Age-related bone loss, polypharmacy-induced xerostomia and diet changes compound oral frailty. Because conventional implants face higher failure rates in osteoporotic jaws, regenerative dentistry offers clinicians an option that restores both soft and hard tissues concurrently. Early technology adopters in the United States, Germany and Japan report growing wait-lists from senior patients seeking biologically integrated solutions. With United Nations forecasts pointing to 1.6 billion individuals aged ≥ 65 by 2050, the tooth regeneration market sees a built-in demand curve that stretches well beyond the current forecast window.

Growing Demand for Aesthetic Dentistry & Smile Restoration

Cosmetic considerations now influence treatment choice almost as strongly as clinical need. Natural-tissue solutions command premium pricing because they avoid color-matching issues and deliver proprioceptive feedback absent in prosthetics. Large dental-technology vendors pivot toward chair-side platforms that integrate CAD/CAM scanners with regenerative biomaterials, seeking to offer same-day biologic restorations. Dentsply Sirona’s capital allocation report highlights digital workflow integration as a cornerstone of product strategy, underscoring how aesthetics and efficiency converge to reshape clinical preference. Parents of paediatric patients also gravitate toward lasting fixes that spare children repeated interventions, further expanding addressable volumes.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High development costs of tooth-regeneration technologies

High development costs of tooth-regeneration technologies

| -1.8% | Global; greater in emerging markets | Long term (≥ 4 years) | (~) % Impact on CAGR Forecast:

-1.8%

| Geographic Relevance:

Global; greater in emerging markets

| Impact Timeline:

Long term (≥ 4 years)

|

Shortage of skilled regenerative-dentistry professionals

Shortage of skilled regenerative-dentistry professionals

| -0.7% | Global; acute in Asia-Pacific & emerging markets | Medium term (2-4 years) | |||

Immunogenicity & vascularisation challenges in

whole-tooth bioengineering

Immunogenicity & vascularisation challenges in

whole-tooth bioengineering

| -1.1% | Global | Long term (≥ 4 years) | |||

Fragmented IP landscape for multiphase scaffold

innovations

Fragmented IP landscape for multiphase scaffold

innovations

| -0.5% | Global; densest in North America & Europe | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

High Development Costs of Tooth-Regeneration Technologies

Clinical programmes face extended timelines because outcome assessment must demonstrate both hard- and soft-tissue maturation, often across multiyear follow-up. Manufacturing personalised scaffolds or autologous cell constructs remains capital intensive, especially under GMP conditions. Toregem’s decision to outsource bioprocessing to WuXi Biologics illustrates the economies sought through specialised CDMOs. Smaller ventures rely heavily on NIH, EU Horizon or AMED grants, signalling financing hurdles that could slow diversification of the tooth regeneration industry pipeline. Cost pressures remain a deterrent for payers in lower-income economies, delaying wide reimbursement and dampening near-term uptake.

Shortage of Skilled Regenerative-Dentistry Professionals

Procedures require cross-disciplinary expertise blending periodontology, tissue engineering and advanced imaging. Training programmes lag behind innovation velocity, producing a bottleneck that is particularly acute outside top academic centres. Continuous-education bodies in North America have begun certificate courses, yet faculty shortages limit class capacity. Asia-Pacific nations see similar gaps, and although Japan leads clinical trials, practitioner density remains low in other regional markets, constraining procedure volumes.

Segment Analysis

By Tissue Type: Hard-Tissue Dominance Drives Market Foundation

Hard-tissue applications controlled 59.92% of the tooth regeneration market in 2025, reflecting the critical role of enamel, dentin and alveolar bone in masticatory function. Early regulatory clarity for mineralised biomaterials enabled commercialisation of bioactive cements and remineralising agents that bridge restorative and regenerative care. Next-generation pulp-capping compounds foster endogenous dentinogenesis, a trend reinforced by in-vitro evidence demonstrating superior bond strength and calcium-ion release. Manufacturers embed nano-hydroxyapatite and bio-silicate ions into matrices that mimic natural crystal orientation, improving load distribution and longevity.

Soft-tissue regeneration, although representing a smaller 2025 baseline, will outpace the overall tooth regeneration market at a 14.78% CAGR. Growth arises from stem-cell-derived exosomes that promote periodontal ligament regeneration through miR-184-mediated PPARα-Akt-JNK signalling. Periodontal-disease prevalence drives demand for therapies that rebuild ligamentous support and preserve proprioceptive feedback. Clinicians increasingly pursue dual-tissue protocols—hard-tissue scaffold topped with cell-laden hydrogels—to deliver holistic restoration in a single intervention. By 2031, manufacturers anticipate chair-side kits containing both mineralised granules and exosome vials, cutting surgical time and enhancing standardisation across care settings.

Note: Segment shares of all individual segments available upon report purchase

By Technology: Stem-Cell Platforms Lead Innovation Landscape

Stem-cell modalities accounted for 43.02% of revenue during 2025 and remain clinically trusted for pulp-cap, socket-fill and partial-root procedures. Dental-pulp stem-cells, periodontal ligament stem-cells and SHED lines exhibit high odontogenic potential, providing rich secretomes that modulate inflammation and recruit host progenitors. Regulatory familiarity with autologous cells supports reimbursement eligibility, cementing their commercial primacy. Clinicians deploy point-of-care centrifuges to harvest and re-implant pulp tissue, shortening chair time and improving patient acceptance.

Small-molecule and peptide-induced regeneration runs at an 18.09% CAGR, the fastest across the technology stack. Proof-of-concept data show that Wnt agonists or BMP-like peptides trigger enamel and dentin deposition without living-cell carriers, simplifying supply logistics. Molecular protocols integrate neatly with digital dentistry workflows: chair-side delivery via hydrogel pens or slow-release micro-capsules calibrated by intraoral scanners. Scaffold-based constructs benefit from multimaterial 3D printers that deposit ceramic and polymer layers in gradients matching native tooth modulus. Growth-factor concentrates—particularly platelet-rich fibrin—remain staples for socket preservation, yet clinical preference is gradually shifting toward synthetically produced nano-factors with longer shelf life and batch consistency. Combined, these trends diversify the tooth regeneration market size across multiple pay-points, reducing revenue concentration risk.

By Age Group: Adult Segment Anchors Current Demand

Adults between 18 and 64 years held 52.11% of 2025 revenue because caries and trauma peak during working age, spurring immediate restorative need. Employers increasingly include dental regeneration in corporate insurance packages as a means to lower absenteeism from chronic oral pain. Premium insurance tiers reimburse for biologic rather than prosthetic interventions, nudging clinics to stock regenerative inventory. The adult segment is also receptive to hybrid models—initial biologic restoration followed by cosmetic veneers—blending aesthetic appeal with biologic preservation.

Paediatrics, while contributing a smaller slice today, expands at 16.12% CAGR, the fastest across age cohorts. Congenital tooth agenesis, amelogenesis imperfecta and molar-incisor hypoplasia create demand for treatments that avoid lifelong prosthetic cycles. Ongoing TRG-035 trials plan a paediatric extension once adult safety is established. Research on microRNA-27a shows that manipulating osteogenic pathways during early craniofacial development can prevent secondary deformities. The geriatric cohort remains growth-positive yet slower, constrained by comorbidity management and implant-retained prosthesis incumbency.

Note: Segment shares of all individual segments available upon report purchase

By End User: Specialised Clinics Drive Clinical Adoption

Specialised dental and maxillofacial clinics represented 51.58% of spending in 2025 because they house the microscopes, centrifuges and imaging tools required for regenerative interventions. Multisite groups deploy AI-powered radiograph analysis to triage cases suitable for regenerative therapy, raising treatment acceptance and throughput. Business models that couple chair-side bioprinting with same-day crowns support attractive margins, encouraging further investment in training and equipment.

Academic and research institutes are forecast at 16.95% CAGR through 2031, reflecting grant-funded pilot programmes and early-stage human trials. Teaching hospitals integrate scaffold design into undergraduate curricula, accelerating knowledge diffusion into community practices. General hospitals remain significant for trauma reconstruction but grow more modestly as outpatient clinics siphon elective procedures. Industry observers anticipate convergence: hospital systems acquiring specialist chains to secure referral pathways and broaden regenerative capacity.

Geography Analysis

North America dominated revenue with 40.12% of the tooth regeneration market in 2025. A mature insurance ecosystem, widespread CBCT imaging infrastructure and robust venture funding create favourable conditions for early adoption. The region accounted for the majority of the USD 400.2 million oral-health venture capital tallied in 2024, with investors attracted to scalable digital-biologic hybrids. State dental boards are updating scope-of-practice rules to allow hygienists to apply bioactive materials, widening patient access and accelerating diffusion.

Asia-Pacific is the fastest climber at a projected 15.22% CAGR. Japan’s pro-innovation regulatory stance, crystallised in the 2024 commencement of human TRG-035 trials, positions the nation as a lighthouse market. China’s prolific patent filings around graphene-reinforced implants reflect domestic ambitions to bypass imported prosthetics and leapfrog into biologic solutions. Australia and South Korea invest in translational institutes that bridge university research and clinic application, seeking to seed local manufacturing hubs for tooth-germ constructs.

Europe records steady progress supported by strong public-health systems and research depth. Institutions such as King’s College London advanced lab-grown tooth prototypes capable of self-repair, signaling a future alternative to amalgam or resin fillings. Pan-EU clinical-trial networks coordinate multicentre safety studies, expediting pooled evidence for reimbursement dossiers. Emerging markets in the Middle East, Africa and Latin America register growing awareness, but infrastructure and specialist scarcity presently temper uptake. Nevertheless, multinational vendors partner with regional distributors to pilot chair-side exosome kits, anticipating demand escalation as GDP-per-capita rises.

Competitive Landscape

Market Concentration

Market rivalry remains moderate, characterised by a blend of dental-device multinationals, biotech start-ups and academic spin-outs. Top players leverage established manufacturing, regulatory and distribution capabilities to integrate biologic products into conventional workflows. Dentsply Sirona embeds regenerative cements within its digital chair-side ecosystem, aiming to lock clinicians into end-to-end proprietary platforms. Straumann invests in biomaterial R&D to complement its implant franchise, hedging against a future where living-tissue regeneration may cannibalise titanium sales.

Emerging ventures concentrate on niche indications such as paediatric tooth-germ generation or peptide-based enamel repair. Partnerships with contract manufacturers like WuXi Biologics enable capital-efficient scale-up for clinical supplies. Intellectual-property portfolios focus on small-molecule libraries and AI-derived scaffold architectures, forming defensive moats that attract strategic investors. The competitive narrative increasingly values data assets—digital impressions linked to clinical outcomes—which feed algorithmic design loops and heighten switching costs for practitioners.

Collaboration across academia and industry accelerates translation. Multisite consortia share GMP facilities to reduce under-utilisation, while teaching hospitals spin out start-ups that licence platform technologies back to device manufacturers. Despite consolidation pressure, the wide variety of tissue targets and delivery routes allows multiple value propositions to coexist, keeping barriers to entry moderate and fostering a vibrant innovation pipeline that continuously redefines best practice.

Tooth Regeneration Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: King’s College London published breakthrough findings in ACS Macro Letters on lab-grown teeth that self-repair and integrate into mandibular bone.

- September 2024: Toregem BioPharma commenced Phase I trials of TRG-035 at Kyoto University Hospital, the world’s first human study for a tooth-regeneration drug.

Table of Contents for Tooth Regeneration Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Rising Prevalence Of Dental Disorders

- 4.2.2Rapid Advancements In Regenerative Medicine Toolkits

- 4.2.3Increasing Geriatric Population Worldwide

- 4.2.4Growing Demand For Aesthetic Dentistry & Smile Restoration

- 4.2.5Fast-Track Regulatory Designations For Dental Tissue-Engineered Products

- 4.2.6Acceleration Of Venture Funding In Dental Biotech Start-Ups

- 4.3Market Restraints

- 4.3.1High Development Costs Of Tooth-Regeneration Technologies

- 4.3.2Shortage Of Skilled Regenerative-Dentistry Professionals

- 4.3.3Immunogenicity & Vascularisation Challenges In Whole-Tooth Bioengineering

- 4.3.4Fragmented IP Landscape For Multiphase Scaffold Innovations

- 4.4Porter's Five Forces Analysis

- 4.4.1Bargaining Power of Buyers/Consumers

- 4.4.2Bargaining Power of Suppliers

- 4.4.3Threat of New Entrants

- 4.4.4Threat of Substitute Products

- 4.4.5Intensity of Competitive Rivalry

5. Market Size & Growth Forecasts (Value, USD)

- 5.1By Tissue Type

- 5.1.1Hard Tissue

- 5.1.2Soft Tissue

- 5.2By Technology

- 5.2.1Stem-cell Therapy Platforms

- 5.2.2Scaffold-based Regeneration

- 5.2.3Growth-factor & Gene-activated Constructs

- 5.2.4Small-molecule & Peptide-induced Regeneration

- 5.3By Age Group

- 5.3.1Pediatric (?17 yrs)

- 5.3.2Adult (18-64 yrs)

- 5.3.3Geriatric (?65 yrs)

- 5.4By End User

- 5.4.1Hospitals

- 5.4.2Specialised Dental & Maxillofacial Clinics

- 5.4.3Academic & Research Institutes

- 5.5Geography

- 5.5.1North America

- 5.5.1.1United States

- 5.5.1.2Canada

- 5.5.1.3Mexico

- 5.5.2Europe

- 5.5.2.1Germany

- 5.5.2.2United Kingdom

- 5.5.2.3France

- 5.5.2.4Italy

- 5.5.2.5Spain

- 5.5.2.6Rest of Europe

- 5.5.3Asia-Pacific

- 5.5.3.1China

- 5.5.3.2Japan

- 5.5.3.3India

- 5.5.3.4South Korea

- 5.5.3.5Australia

- 5.5.3.6Rest of Asia-Pacific

- 5.5.4Middle East and Africa

- 5.5.4.1GCC

- 5.5.4.2South Africa

- 5.5.4.3Rest of Middle East and Africa

- 5.5.5South America

- 5.5.5.1Brazil

- 5.5.5.2Argentina

- 5.5.5.3Rest of South America

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1Institut Straumann AG

- 6.3.2Dentsply Sirona Inc.

- 6.3.3ZimVie Inc.

- 6.3.4BioHorizons Implant Systems Inc.

- 6.3.5Solventum Corporation

- 6.3.6Integra LifeSciences Holdings Corp.

- 6.3.7RevBio Inc.

- 6.3.8WuXi Biologics & Toregem Biopharma

- 6.3.9Nobel Biocare Services AG

- 6.3.10Geistlich Pharma AG

- 6.3.11Kuraray Noritake Dental Inc.

- 6.3.12CollPlant Biotechnologies Ltd.

- 6.3.13Medtronic plc

- 6.3.14Organogenesis Holdings Inc.

- 6.3.15Stemodontics LLC

- 6.3.16Botiss Biomaterials GmbH

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-need Assessment

Global Tooth Regeneration Market Report Scope

As per the report's scope, tooth regeneration refers to developing new dental tissues to replace a lost or damaged tooth. The process involves stimulating the growth of new enamel, dentin, and other components to restore the structure and function of a fully developed tooth.

The tooth regeneration market is segmented by type (hard tissue and soft tissue), age (pediatric, adult, and geriatric), end user (hospitals, dental clinics, and others), and geography (North America, Europe, Asia-Pacific, the Middle East and Africa, and South America). The report offers the value (USD) for all the above segments. The report also covers the estimated market sizes and trends for 17 countries across significant regions globally.