Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

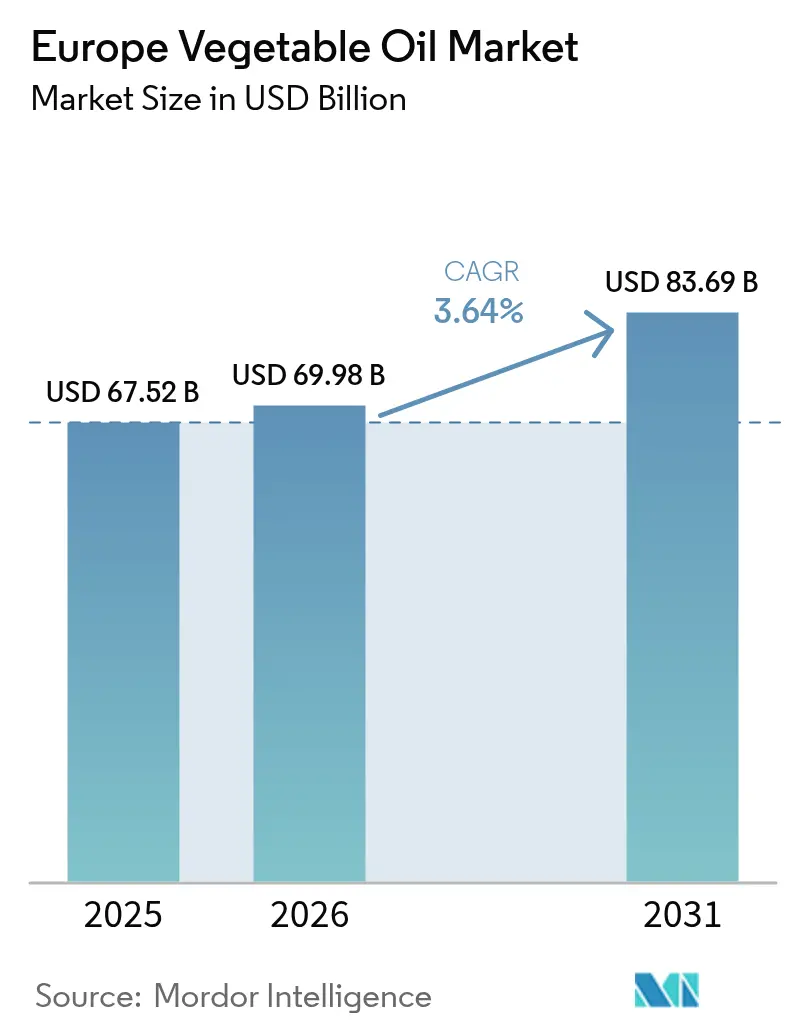

| Base Year Market Size (2025) | USD 67.52 Billion |

| Market Size (2026) | USD 69.98 Billion |

| Market Size (2031) | USD 83.69 Billion |

| Growth Rate (2026 - 2031) | 3.64% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Vegetable Oil Market Analysis by Mordor Intelligence

The Europe Vegetable Oil Market size is projected to be USD 67.52 billion in 2025, USD 69.98 billion in 2026, and reach USD 83.69 billion by 2031, growing at a CAGR of 3.64% from 2026 to 2031. Momentum stems from dietary shifts toward poly- and monounsaturated lipids, rapid scaling of hydrotreated vegetable oil (HVO) and biodiesel plants under RED III, and premium pricing for feedstocks eligible for sustainable aviation fuel (SAF) blending mandates. Germany’s Energiewende subsidies, Italy’s rebound in olive-oil harvests, and Rotterdam’s import-hub status collectively reinforce demand while also exposing supply chains to climate, regulatory, and geopolitical shocks. Consolidation among crushers exemplified by the 2024 Bunge-Viterra merger tightens upstream bargaining power, yet specialty refiners differentiate through organic, cold-pressed, and structured lipid offerings. EU-wide counterfeiting crackdowns and deforestation-traceability rules add compliance costs that favor scale players with audited supply chains.

Key Report Takeaways

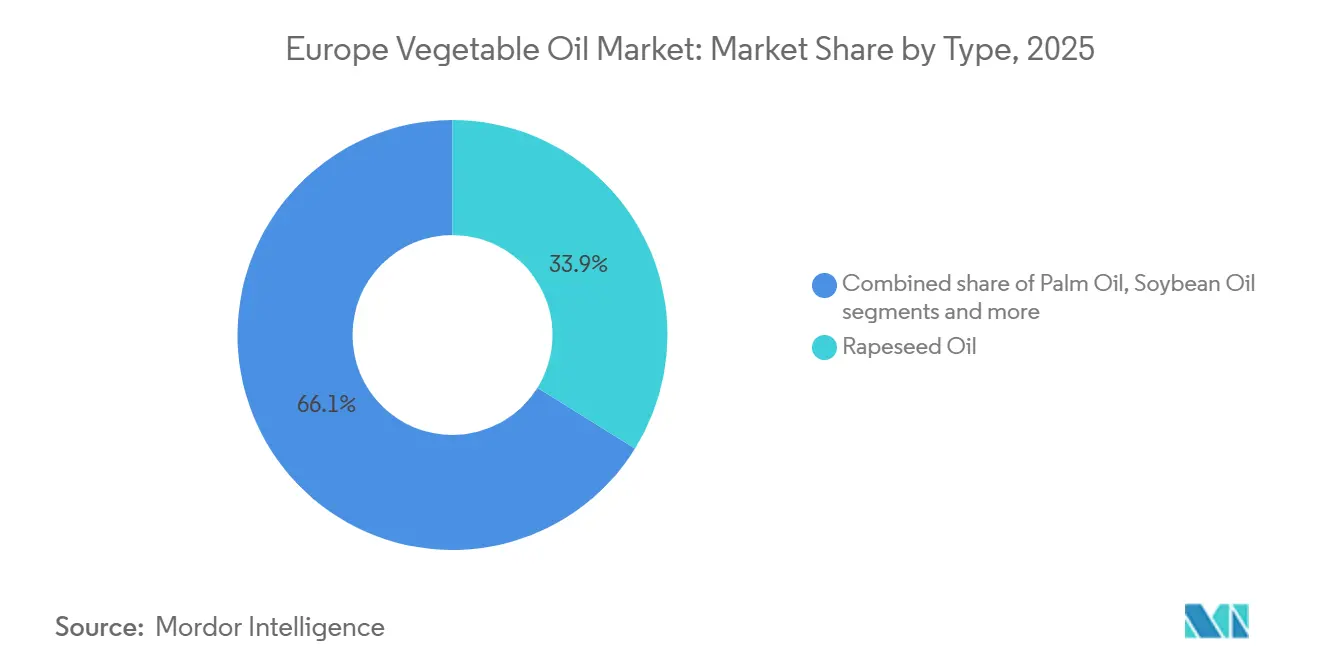

- By product type, rapeseed oil led with 33.86% revenue share in 2025, whereas palm oil is forecast to expand fastest at a 4.35% CAGR through 2031.

- By nature, conventional grades held 76.45% of value in 2025, while organic oils are poised to grow at a 4.87% CAGR to 2031.

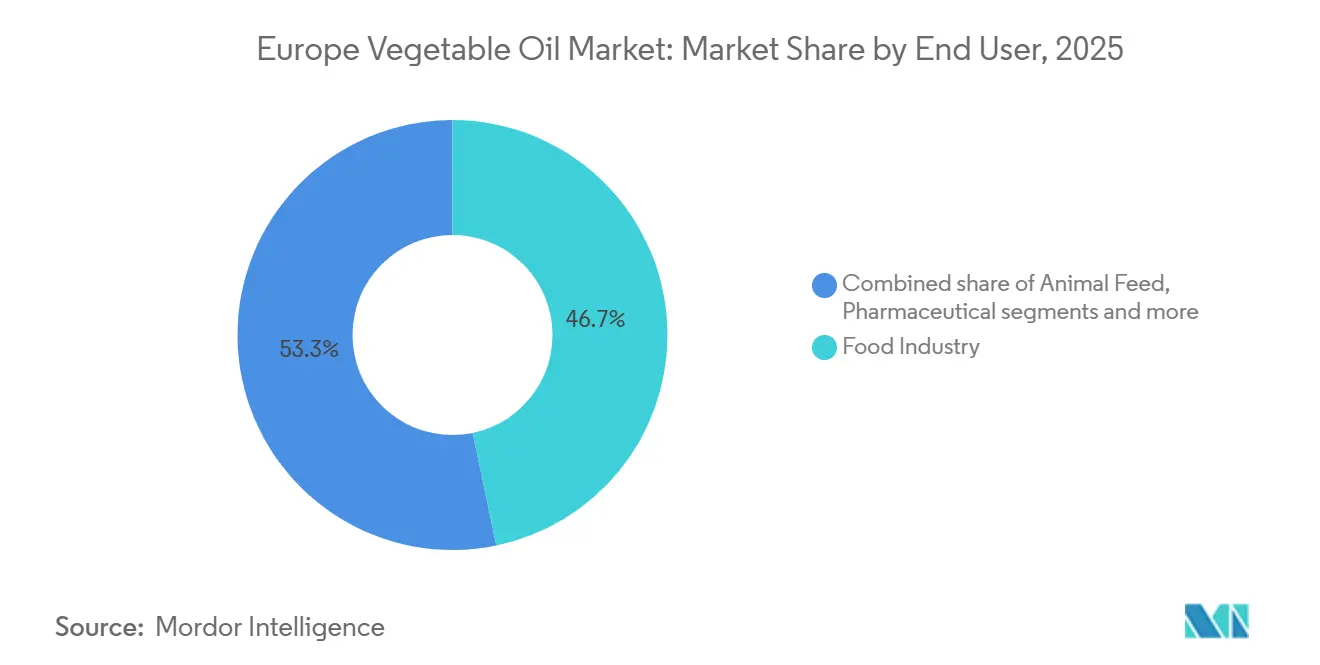

- By end user, the food industry accounted for 46.74% of spend in 2025, whereas biofuels are advancing at a 5.02% CAGR across 2026-2031.

- By geography, Italy contributed 19.08% of regional sales in 2025, while Germany is projected to register the quickest expansion at 4.65% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Vegetable Oil Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising health consciousness favoring heart-healthy oils rich in omega-3 and omega-6 fatty acids | +0.9% | Pan-European, strongest in Germany, Netherlands, Nordics | Medium term (2-4 years) |

| Increasing demand for sustainable and biodegradable oils in industrial applications | +0.7% | Germany, France, Belgium (industrial clusters) | Long term (≥ 4 years) |

| Growth in organic and cold-pressed oils for premium food segments | +0.6% | Western Europe (Germany, France, UK, Netherlands) | Medium term (2-4 years) |

| Shift toward plant-based diets and healthier cooking alternatives | +0.8% | Pan-European, led by UK, Germany, Netherlands | Short term (≤ 2 years) |

| Stringent EU sustainability directives and circular economy initiatives | +1.0% | All EU member states, strongest enforcement in Northern Europe | Long term (≥ 4 years) |

| Technological advancements in extraction and refining processes | +0.5% | Germany, Netherlands, France (processing hubs) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising health consciousness favoring heart-healthy oils rich in omega-3 and omega-6 fatty acids

Growing health awareness among European consumers is significantly driving demand in the vegetable oil market, particularly for oils recognized for their cardiovascular benefits. Shoppers are increasingly choosing oils high in omega‑3 and omega‑6 fatty acids, known to support heart health and maintain healthy cholesterol levels. Varieties like rapeseed, sunflower, and flaxseed oils are witnessing higher adoption due to their favorable nutrient composition and lower levels of saturated fats. This shift is reinforced by a rising focus on preventive nutrition, balanced diets, and functional foods that promote overall wellness. Food producers are responding by incorporating these healthier oils into reformulated products to meet clean-label and health-focused expectations. Enhanced nutritional labeling and awareness campaigns across Europe further guide consumers toward better choices. Consequently, heart-healthy vegetable oils are experiencing strong and sustained growth in both retail and foodservice sectors.

Increasing demand for sustainable and biodegradable oils in industrial applications

The European vegetable oil market is witnessing strong growth driven by increasing demand for sustainable and biodegradable oils in industrial applications. Industries are actively shifting toward plant-based oils for lubricants, hydraulic fluids, and other industrial uses to reduce environmental impact and comply with evolving regulations. The updated EU Circular Economy Action Plan (2024) plays a pivotal role in this transition, mandating that 65% of industrial lubricants and hydraulic fluids sold after 2027 must be biodegradable within 28 days under OECD 301B test protocols[1]Source: European Commission, “Circular Economy Act”, environment.ec.europa.eu. This regulatory push is encouraging manufacturers to adopt renewable, eco-friendly oils that are both efficient and sustainable. Additionally, rising corporate commitments to sustainability and carbon reduction are boosting the preference for biodegradable vegetable oil-based alternatives over conventional petroleum-based products. Technological advancements in refining and formulation have also improved the performance and stability of these oils in industrial settings.

Growth in organic and cold-pressed oils for premium food segments

The European vegetable oil market is being increasingly driven by the growing demand for organic and cold-pressed oils in premium food segments. Consumers are showing a strong preference for high-quality, minimally processed oils that offer superior flavor, nutritional benefits, and clean-label appeal. According to The World of Organic Agriculture report, Europe’s organic retail sales climbed to approximately EUR 58.7 billion in 2024, up 4.1 % from 2023, highlighting sustained consumer interest in organic products as part of health-focused diets[2]Source: The World of Organic Agriculture report, “The Future is Organic”, fibl.org. This trend is particularly evident in the premium food and gourmet segments, where chefs, restaurants, and discerning households prioritize oils such as cold-pressed olive, rapeseed, and sunflower for their purity and nutrient content. Producers are responding with targeted product launches and specialty packaging to cater to this niche yet rapidly growing demand. The emphasis on natural processing methods and organic certification is enhancing brand credibility and consumer trust.

Shift toward plant-based diets and healthier cooking alternatives

The European vegetable oil market is increasingly propelled by the rising popularity of plant-based diets and healthier cooking choices. Between 2024 and 2025, flexitarian and vegan lifestyles expanded significantly across Europe, with the European Vegetarian Union reporting that 10% of the EU population now identifies as vegetarian or vegan, and another 30% actively limits meat consumption[3]Source: European Vegetarian Union, “Standing for sustainable food systems in the EU”, euroveg.eu. This shift has fueled demand for vegetable oils as nutritious, plant-derived alternatives to animal fats in everyday cooking and food preparation. Oils such as sunflower, rapeseed, and olive are particularly favored for their health benefits, including beneficial fatty acids and low saturated fat content. The trend is also supported by growing consumer interest in clean-label and minimally processed ingredients. Food producers are increasingly reformulating products and offering plant-forward options to meet these preferences. Consequently, the adoption of plant-based diets and healthier cooking practices is emerging as a key driver of vegetable oil consumption in both retail and foodservice segments across Europe.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing counterfeit or adulterated oil products | -0.5% | Southern Europe (Italy, Spain, Greece) with spillover to broader EU | Short term (≤ 2 years) |

| Consumer shift toward low-fat diets reducing overall oil consumption | -0.3% | Northern Europe (Germany, UK, Nordics) | Medium term (2-4 years) |

| Fluctuating raw material supply due to weather variability and crop failures | -0.7% | Pan-European, acute in Central/Eastern Europe (Poland, Romania, Hungary) | Short term (≤ 2 years) |

| Competition from emerging alternatives like olive oil and seed oils | -0.4% | Mediterranean region (Italy, Spain, France) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing counterfeit or adulterated oil products

The European vegetable oil market is being constrained by the growing prevalence of counterfeit and adulterated products. These fraudulent oils not only diminish nutritional quality but also pose potential health risks to consumers, including exposure to contaminants and inferior ingredients. Practices such as blending premium oils with cheaper substitutes erode consumer confidence and can damage the reputation of established brands. Complex supply chains, particularly for imported oils, make monitoring and enforcement difficult, creating opportunities for unscrupulous actors. While regulators and industry bodies are increasing testing, certification, and traceability efforts, ensuring compliance remains challenging and resource-intensive. Rising consumer demand for authentic, certified, and traceable oils is pushing manufacturers to strengthen quality control measures. Consequently, the issue of adulterated and counterfeit oils continues to act as a notable restraint on market growth and consumer trust.

Consumer shift toward low-fat diets reducing overall oil consumption

The European vegetable oil market is also restrained by a growing consumer shift toward low-fat diets, which has led to a reduction in overall oil consumption. Heightened awareness of obesity, cardiovascular health, and calorie intake has prompted many consumers to limit the use of cooking oils in everyday meals. This trend is particularly evident in urban and health-conscious populations, where portion control and low-fat cooking methods such as steaming or grilling are increasingly preferred. Retailers have reported a rising demand for reduced-oil or oil-free food products, which has impacted conventional oil sales volumes. Additionally, the popularity of alternative cooking mediums, including non-stick sprays and plant-based butter substitutes, further limits traditional oil usage. Despite the nutritional benefits of certain oils, this health-driven behavior continues to suppress overall market growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Rapeseed Dominance Anchors Food and Fuel Demand

Rapeseed oil accounted for the largest revenue share in the European vegetable oil market in 2025, capturing 33.86% of total sales. Its leading position is supported by strong domestic production across key European countries, which ensures stable supply and pricing advantages. The oil’s widespread use in both household cooking and food processing applications further reinforces its dominance. Additionally, rapeseed oil is widely perceived as a healthier alternative due to its favorable fatty acid profile, including low saturated fat content. The growing preference for locally sourced and non-GMO edible oils in Europe has also contributed to its sustained demand.

Palm oil is projected to be the fastest-growing product segment in the European vegetable oil market, expanding at a CAGR of 4.35% through 2031. This growth is primarily driven by its cost-effectiveness and high yield efficiency compared to other vegetable oils. Palm oil’s functional properties, such as stability at high temperatures and long shelf life, make it highly suitable for processed foods and bakery applications. Increasing demand from the food manufacturing sector, particularly for confectionery and ready-to-eat products, is further accelerating its adoption. Despite regulatory scrutiny and sustainability concerns, certified sustainable palm oil initiatives are helping maintain its acceptance in the European market.

By Nature: Conventional Scale Versus Organic Premiums

Conventional vegetable oils accounted for the largest share of the European market in 2025, representing 76.45% of total value. Their dominance is primarily attributed to widespread availability, established supply chains, and comparatively lower price points than organic alternatives. Conventional oils are extensively used across retail, foodservice, and industrial food processing sectors, ensuring consistent bulk demand. Large-scale agricultural production and efficient refining infrastructure across Europe further support their strong market penetration. In addition, private-label offerings and competitive pricing strategies by major retailers have reinforced consumer preference for conventional grades.

Organic vegetable oils are projected to be the fastest-growing segment, registering a CAGR of 4.87% through 2031. This growth is driven by increasing consumer awareness regarding health, sustainability, and clean-label food products. Rising demand for chemical-free and non-GMO food ingredients is encouraging both retailers and manufacturers to expand their organic portfolios. Government support for organic farming practices and stricter food safety standards across Europe are also contributing to segment expansion. Moreover, premiumization trends and higher disposable incomes are enabling consumers to opt for organic variants despite their higher price points.

By End User: Food Industry Scale Versus Biofuel Momentum

The food industry represented the largest end-user segment in the European vegetable oil market, accounting for 46.74% of total spending in 2025. This dominance is driven by the extensive use of vegetable oils in food processing applications such as bakery, confectionery, snacks, sauces, and ready-to-eat meals. Oils serve as essential ingredients for frying, emulsification, flavor enhancement, and texture improvement, making them indispensable to manufacturers. The strong presence of packaged and convenience food consumption across Europe further sustains high demand from this segment. In addition, the expansion of private-label food products and premium processed foods continues to support volume growth.

The biofuels segment is projected to be the fastest-growing end-user category, advancing at a CAGR of 5.02% between 2026 and 2031. Growth in this segment is largely supported by Europe’s strong regulatory framework promoting renewable energy and carbon reduction targets. Vegetable oils are widely used as feedstock in biodiesel production, driving consistent industrial demand. Increasing investments in sustainable fuel alternatives and circular economy initiatives are further accelerating adoption. Additionally, rising concerns over fossil fuel dependency and greenhouse gas emissions are prompting governments and industries to expand biofuel blending mandates.

Geography Analysis

Italy accounted for the largest share of the European vegetable oil market in 2025, contributing 19.08% of total regional sales. The country’s strong position is supported by its well-established food processing sector and deep-rooted culinary culture that heavily relies on vegetable oils. High consumption across households, HoReCa channels, and packaged food manufacturers sustains consistent demand. Italy’s extensive production and refining capabilities, particularly in olive and blended oils, further reinforce its market leadership. Additionally, the country’s export-oriented processed food industry drives bulk procurement of vegetable oils as key ingredients. As a result, Italy continues to represent a major revenue-generating hub within the regional market.

Germany is projected to register the fastest growth in the European vegetable oil market, expanding at a CAGR of 4.65% through 2031. The country’s growth is driven by rising demand for plant-based and sustainable food products, which has increased vegetable oil consumption across food manufacturing. Germany’s strong biofuel industry also contributes significantly to incremental demand, particularly for rapeseed and other feedstock oils. Increasing health awareness among consumers is encouraging a shift toward high-quality and specialty oils. Furthermore, advancements in food processing technologies and innovation in clean-label formulations are supporting market expansion. Consequently, Germany is expected to strengthen its position as a high-growth market during the forecast period.

Other major European markets, including the United Kingdom, France, and Spain, also play important roles in shaping regional demand dynamics. The United Kingdom demonstrates steady consumption driven by its large packaged food and quick-service restaurant sectors, alongside growing interest in healthier and organic oil variants. France benefits from a strong processed food and gourmet cooking culture, which supports demand for premium and specialty vegetable oils. Spain, with its significant edible oil production base and Mediterranean dietary patterns, remains a substantial contributor to regional consumption. Additionally, these countries are increasingly aligning with sustainability and biofuel mandates, which further stimulate industrial demand.

Competitive Landscape

The European vegetable oils market is characterized by a moderately fragmented competitive landscape, with the presence of several multinational corporations alongside strong regional and domestic players. While a few leading companies command notable market shares, no single participant dominates the market entirely. This structure fosters competitive pricing, continuous product innovation, and differentiated portfolio strategies. Large players benefit from vertically integrated supply chains and established distribution networks, whereas smaller firms compete through niche positioning and specialty offerings. The coexistence of private-label brands further intensifies competition across retail channels.

Competition in the market is primarily driven by product diversification, sustainability initiatives, and strategic partnerships. Companies are increasingly investing in certified sustainable sourcing, particularly for palm and rapeseed oil, to align with stringent European regulatory standards. Innovation in organic, non-GMO, and cold-pressed variants has become a key differentiator among premium brands. In addition, manufacturers are strengthening their foothold through mergers, acquisitions, and collaborations to expand geographic reach and processing capabilities. Pricing strategies remain critical, especially in conventional oil categories where margins are comparatively tighter.

Furthermore, evolving consumer preferences toward healthier and environmentally responsible products are reshaping competitive strategies. Companies are emphasizing transparency, traceability, and clean-label claims to build trust and brand loyalty. The growing importance of biofuels and industrial applications has also diversified revenue streams, encouraging firms to balance food and non-food segments. Retail consolidation across Europe has increased the bargaining power of large supermarket chains, further influencing supplier negotiations. Meanwhile, local producers leverage regional sourcing and authenticity to maintain relevance in domestic markets.

Europe Vegetable Oil Industry Leaders

Bunge Ltd.

Wilmar International

Louis Dreyfus Company

Archer Daniels Midland Company

Cargill, Incorporated

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Beyond Oil's exclusive distributor, Pilpel Hungary Kft., has made a significant move by placing an advance order of 21,600 kg of Beyond Oil's product. This order comes well ahead of Pilpel's 2026 commitment, underscoring the heightened traction and adoption of Beyond Oil's offerings in Central European markets.

- June 2025: Eni made its inaugural export of vegetable oil, sourced from rubber tree residues in Côte d'Ivoire. This initiative not only dovetails with Eni's overarching decarbonization agenda but also champions the sustainable evolution of local agricultural supply chains. As a result, farming communities stand to gain from enhanced economic diversification and increased income streams. The ISCC-EU certified vegetable oil is earmarked for advanced biofuel production, playing a pivotal role in the broader transport decarbonization narrative.

- April 2025: Repsol and Bunge have forged a strategic alliance, aiming to bolster renewable fuel initiatives across Europe. By harnessing intermediate crops such as camelina and safflower, the duo targets a significant emission reduction of up to 90% when juxtaposed with traditional diesel. This ambitious goal is set to be achieved through cutting-edge production technologies, namely advanced HVO and SAF.

Europe Vegetable Oil Market Report Scope

Vegetable oil is a light-colored, odorless, flavorless cooking oil that can be used for cooking, frying, and salad dressings. The European vegetable oil market is segmented by product type, nature, application, and geography. Based on product type, the market is segmented into palm oil, soybean oil, rapeseed oil, sunflower oil, olive oil, coconut oil and other types. Based on nature, the market is segmented into conventional and organic. Based on the application, the market is segmented into food industry, animal feed, pharmaceutical, biofuels, beauty and personal care and others. Based on geography, the market is segmented into Spain, the United Kingdom, France, Germany, Italy, Spain, Netherlands, Poland, Belgium, Sweden and the Rest of Europe. The market sizes and forecasts are provided in terms of value (USD) and volume (Tons) for all the above mentioned segments.

By Product Type

| Palm Oil |

| Soybean Oil |

| Rapeseed Oil |

| Sunflower Oil |

| Peanut Oil |

| Coconut Oil |

| Olive Oil |

| Other Types |

By Nature

| Conventional |

| Organic |

By End User

| Food Industry | Food Processing Industry | Margarine and Spreads |

| Snacks Foods | ||

| Ready Meals | ||

| Others | ||

| Foodservice/HoReCa | ||

| Retail | ||

| Animal Feed | ||

| Pharmaceutical | ||

| Biofuels | ||

| Beauty and Personal Care | ||

| Others |

By Country

| Germany |

| United Kingdom |

| Italy |

| France |

| Spain |

| Netherlands |

| Poland |

| Belgium |

| Sweden |

| Rest of Europe |

| By Product Type | Palm Oil | ||

| Soybean Oil | |||

| Rapeseed Oil | |||

| Sunflower Oil | |||

| Peanut Oil | |||

| Coconut Oil | |||

| Olive Oil | |||

| Other Types | |||

| By Nature | Conventional | ||

| Organic | |||

| By End User | Food Industry | Food Processing Industry | Margarine and Spreads |

| Snacks Foods | |||

| Ready Meals | |||

| Others | |||

| Foodservice/HoReCa | |||

| Retail | |||

| Animal Feed | |||

| Pharmaceutical | |||

| Biofuels | |||

| Beauty and Personal Care | |||

| Others | |||

| By Country | Germany | ||

| United Kingdom | |||

| Italy | |||

| France | |||

| Spain | |||

| Netherlands | |||

| Poland | |||

| Belgium | |||

| Sweden | |||

| Rest of Europe | |||

Key Questions Answered in the Report

How big will European demand for vegetable oil be in 2031?

The Europe vegetable oil market size is forecast to hit USD 83.69 billion by 2031, advancing at a 3.64% CAGR from 2026.

Which oil type currently leads sales value?

Rapeseed oil holds the top position with 33.86% of 2025 value, favored for its local agronomy and balanced fatty-acid profile.

What end-use segment is growing fastest?

Biofuels post the strongest momentum at a 5.02% CAGR thanks to EU renewable-energy mandates and HVO refinery build-out.

Why is Germany the fastest-growing market?

Germany’s aggressive decarbonization policy and investment in advanced biofuel capacity drive a 4.65% CAGR through 2031.

What policy drives biofuel demand for vegetable oils?

RED III and ReFuelEU Aviation mandates require higher renewable content in road and jet fuels, boosting HVO and SAF feedstock needs.

Page last updated on: