Organic Edible Oil Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

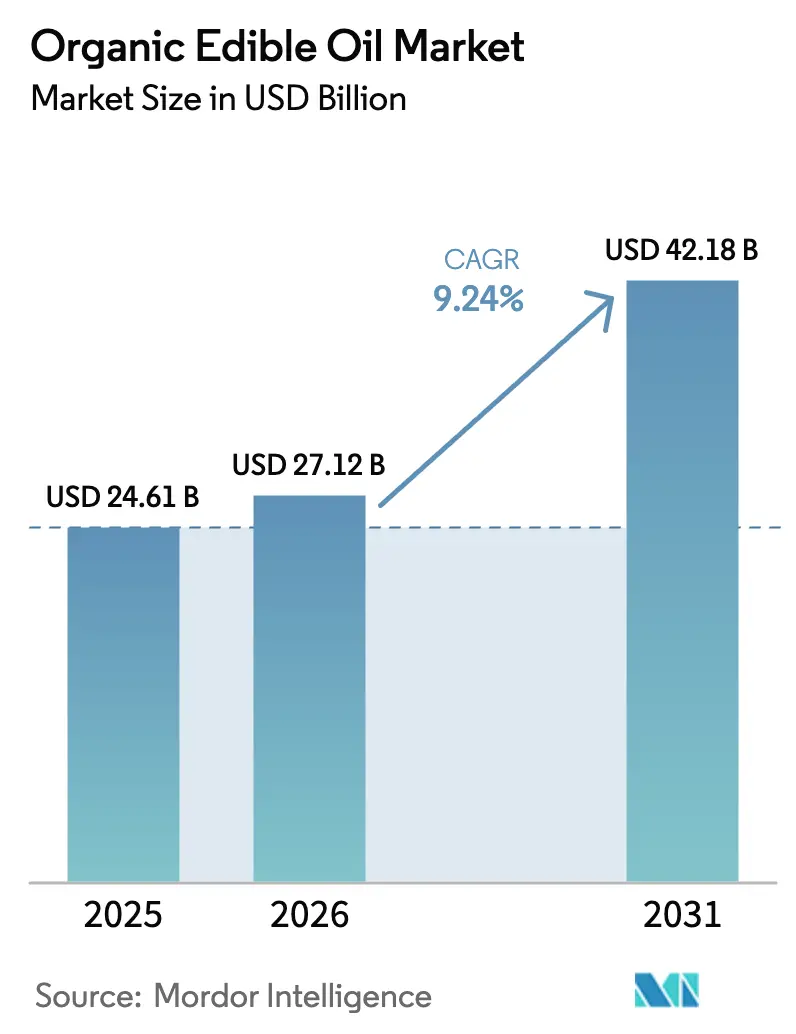

| Market Size (2026) | USD 27.12 Billion |

| Market Size (2031) | USD 42.18 Billion |

| Growth Rate (2026 - 2031) | 9.24% CAGR |

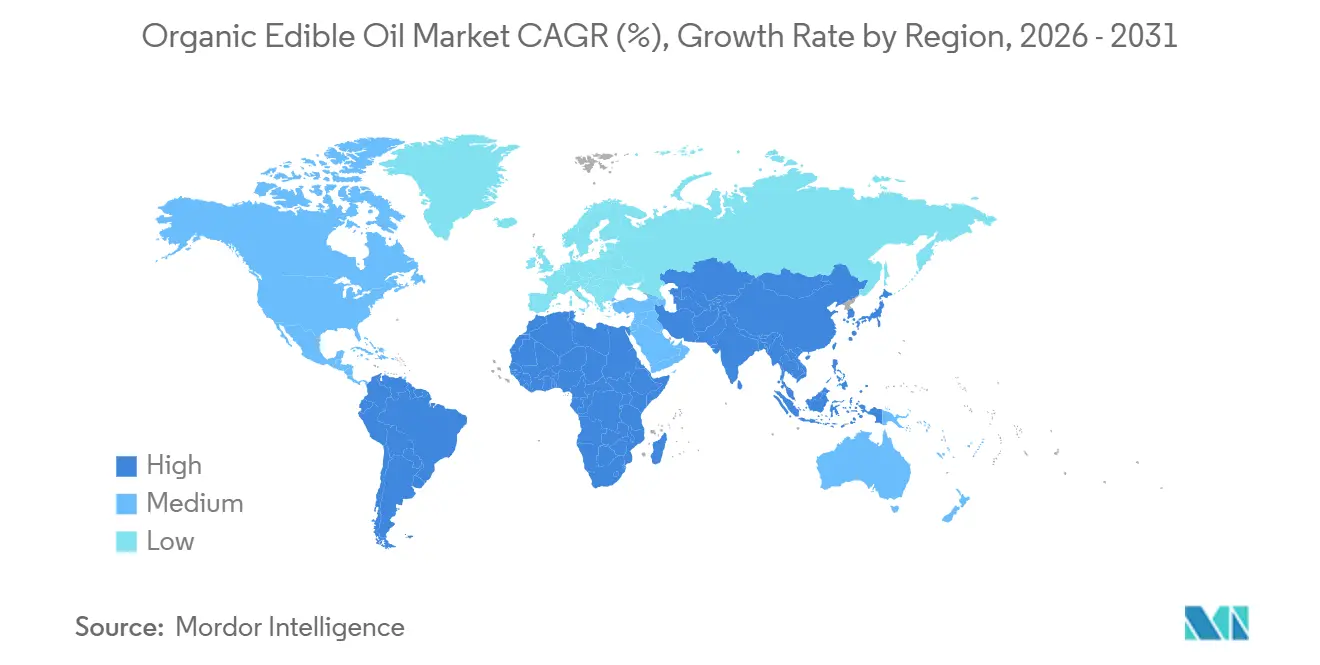

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Organic Edible Oil Market Analysis by Mordor Intelligence

The organic edible oil market size is projected to expand from USD 24.61 billion in 2025 and USD 27.12 billion in 2026 to USD 42.18 billion by 2031, registering a CAGR of 6.73% between 2026 and 2031. This surge in demand is driven by consumers moving away from chemical extractions, the adoption of cold-pressed technologies, and increased retail access to premium non-GMO products. While olive oil leads in value, processors are shifting focus to higher-margin oils like avocado, sesame, and specialty nut oils, prized for their resilience against oxidative breakdown during deep frying. Government incentives promoting organic acreage conversion, coupled with ESG-aligned investments in solvent-free extraction platforms, are alleviating historical supply constraints. Concurrently, online grocery platforms, notably quick-commerce apps in urban Asia, are simplifying purchases and bolstering repeat subscriptions for premium oils. The competitive landscape is moderately intense, with multinational giants vying for shelf space, while direct-to-consumer brands leverage single-origin narratives and blockchain traceability to build consumer trust.

Key Report Takeaways

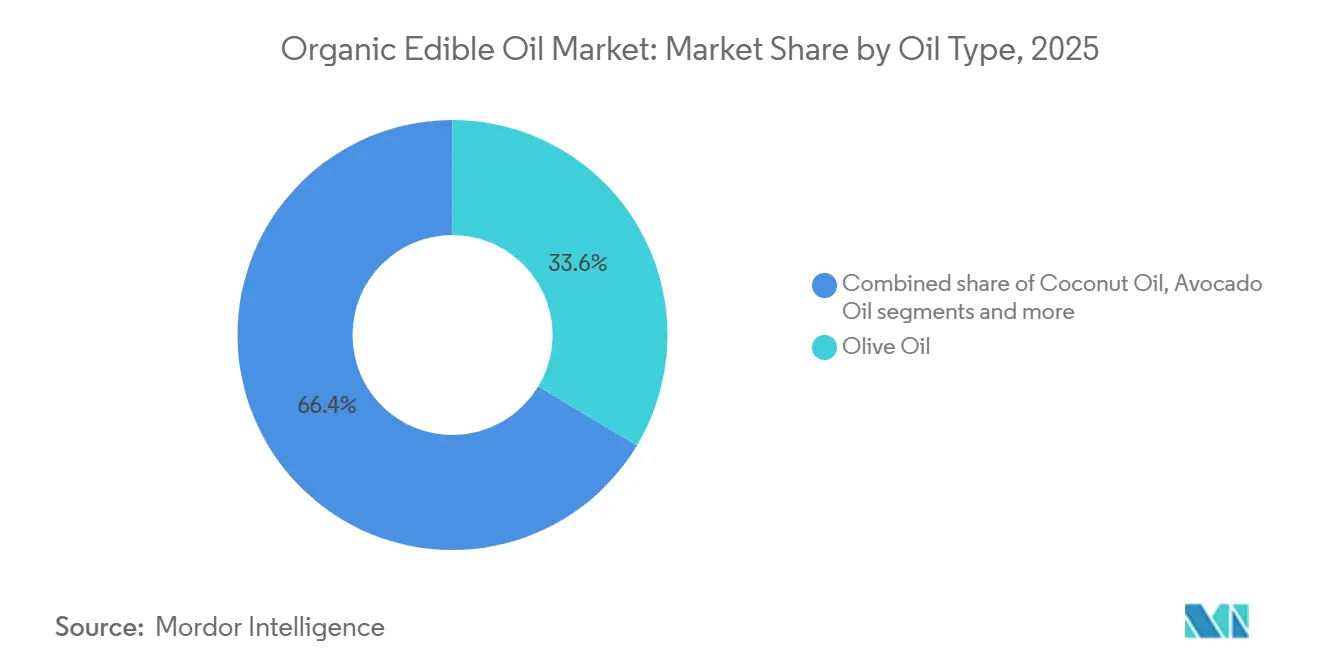

- By oil type, olive oil led with 33.59% of the organic edible oil market share in 2025, while avocado oil is forecast to post a 7.48% CAGR through 2031.

- By packaging, bottles accounted for 65.69% share of the organic edible oil market size in 2025, and cans are advancing at a 7.07% CAGR to 2031.

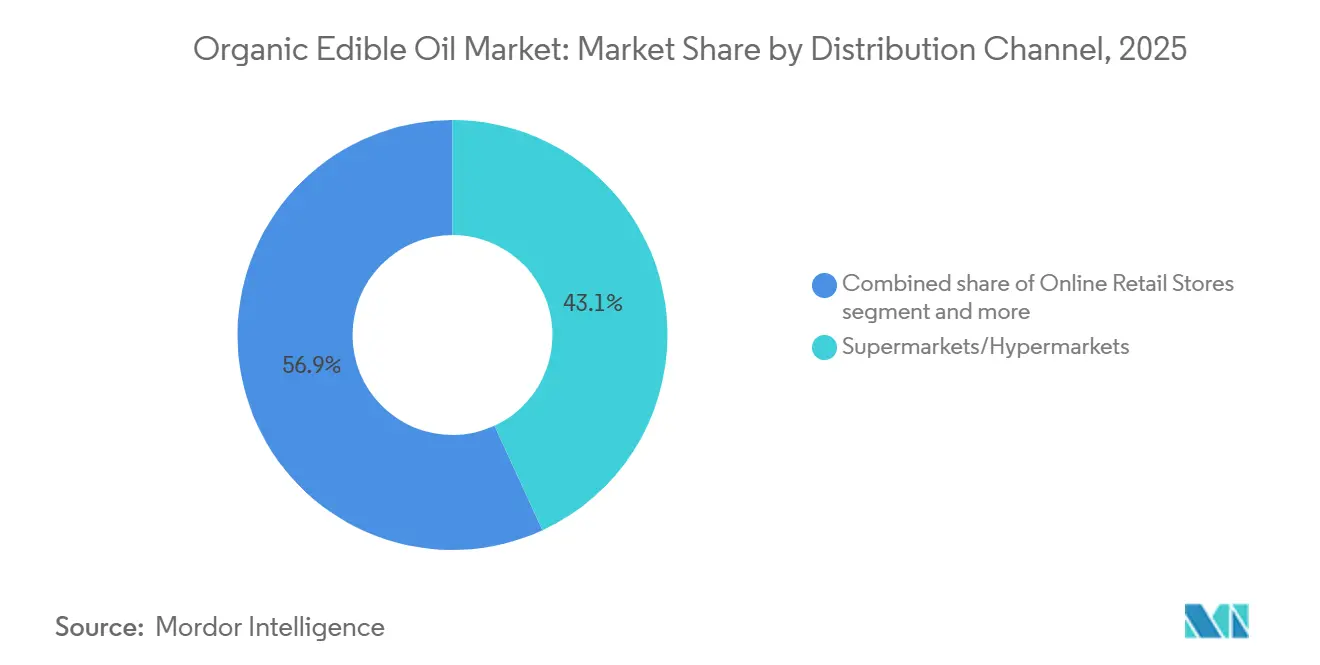

- By distribution, supermarkets and hypermarkets captured 43.12% revenue in 2025; online retail is projected to expand at a 7.20% CAGR through 2031.

- By geography, Europe commanded 37.40% value in 2025, whereas Asia-Pacific is set to grow at a 7.58% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Organic Edible Oil Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising health-conscious consumer base shifts to clean-label oils | +1.2% | Global, with the strongest uptake in North America, Europe, and urban Asia-Pacific | Medium term (2-4 years) |

| Government incentives are expanding certified organic acreage | +0.9% | North America and Europe, emerging in India and Brazil | Long term (≥ 4 years) |

| Premiumization of culinary oils in mature food markets | +0.8% | North America, Western Europe, Japan | Medium term (2-4 years) |

| Rapid growth of e-commerce and D2C grocery fulfilment | +1.1% | Global, led by Asia-Pacific and North America | Short term (≤ 2 years) |

| Blockchain-enabled traceability boosts consumer trust | +0.5% | Europe (olive oil), Asia-Pacific (sesame oil), and gradual global adoption | Long term (≥ 4 years) |

| ESG-driven investment in cold-press and supercritical extraction | +0.7% | North America, Europe, with technology transfer to South America and the Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising health-conscious consumer base shifts to clean-label oils

Retailers and foodservice operators are reshaping their procurement strategies, increasingly favoring oils that are free from chemical solvents, trans fats, and genetically modified organisms. This shift, accelerated by post-pandemic wellness trends, sees consumers meticulously examining ingredient lists. Many are turning away from hexane-extracted oils, opting instead for expeller-pressed or cold-pressed variants that better preserve native antioxidants and essential fatty acids. Indian D2C brand Gramiyaa, for instance, saw its revenue jump from INR 10.9 crore (USD 1.3 million) in FY24 to INR 18.7 crore (USD 2.2 million) in FY25. This growth is attributed to their stringent quality control measures, which encompass batch-level testing and QR-coded traceability. The push for clean labels isn't confined to retail; foodservice operators are revamping their menus to spotlight organic oils. This is especially true for high-heat applications, where refined avocado oil, boasting a 500°F smoke point, outshines traditional canola or soybean oils. In Japan, while cooking oil consumption has dipped due to price inflation, premium olive and sesame oils have held their ground. Middle- and high-income households continue to favor these oils, valuing the perceived health benefits, as highlighted by Agriculture Canada[1]Source: Agriculture and Agri-Food Canada, “Japan Oilseeds and Products Annual 2026,” agr.gc.ca .

Government incentives expanding certified organic acreage

Federal and regional programs are easing the financial burden of transitioning to organic farming, a process that usually mandates three years of chemical-free cultivation prior to certification. In 2024 and 2025, the USDA's Environmental Quality Incentives Program, Organic Transition Initiative, and Organic Certification Cost Share Program allocated funds to assist farmers in shifting conventional oilseed acreage to organic production. This move aims to alleviate the supply bottleneck that has hindered market growth. Meanwhile, EU member states have integrated organic farming objectives into their Common Agricultural Policy payments. This strategy encourages rapeseed, sunflower, and olive producers to seek EU Organic certification. In India, the Paramparagat Krishi Vikas Yojana provides financial support for developing organic clusters. However, oilseed farmers' adoption of this initiative lags behind their counterparts in cereals and pulses. While these programs aim to offset the opportunity cost of reduced yields during the transition, the three-year gap between program enrollment and achieving a certified harvest suggests that any relief in supply will only be realized in the medium to long term.

Premiumization of culinary oils in mature food markets

In North America, Western Europe, and Japan, affluent consumers are increasingly viewing cooking oils as culinary essentials rather than mere commodities. This shift has spurred a growing demand for single-origin, estate-bottled, and flavored organic oils. For instance, Oliva Dorado, a direct-to-consumer brand, offers single-estate organic extra virgin olive oil sourced from Zaragoza, Spain. This oil boasts a lab-verified polyphenol content of 407 mg/kg and features harvest-date labeling for enhanced traceability. The trend of premiumization is especially evident in the olive oil sector. Here, consumers are willing to pay a staggering 200% to 300% premium for certified organic extra virgin olive oil compared to conventional refined grades. Similarly, in the avocado oil market, cold-pressed organic variants are priced between USD 15.99 to USD 19.99 for a 27-ounce bottle, overshadowing the USD 8 to USD 10 price tag of conventional refined avocado oil. In a nod to this premiumization trend, La Tourangelle introduced an 800 ml squeezable bottle of 100% pure avocado oil in October 2024. The brand is eyeing home cooks who desire restaurant-quality fats for sautéing and finishing their dishes. However, this premiumization trend isn't immune to economic fluctuations. In Japan, sluggish growth in disposable income has curtailed the adoption of premium oils. Yet, with forecasts suggesting an 8% income growth from 2023 to 2028, there's potential for a resurgence in demand, especially if inflation rates stabilize, as noted by Agriculture Canada.

Rapid growth of e-commerce and D2C grocery fulfilment

Online retail channels are eroding the distribution edge that established brands once held with supermarket shelf space. This shift allows startups to connect directly with consumers, leveraging subscription models and rapid delivery services. In FY25, Gramiyaa's revenue streams were diverse: 34% came from quick commerce, 32% from marketplaces, 14% from its own website, and 20% from physical retail. This underscores the multi-channel strategy imperative for organic oil brands. Chosen Foods, boasting a 70% national retail penetration across roughly 22,500 U.S. storefronts, is simultaneously bolstering its e-commerce footprint on platforms like Amazon and Thrive Market, targeting consumers who favor home delivery of bulk organic oils. Indian quick commerce platforms, like Blinkit and Zepto, are revolutionizing the market by fulfilling orders in just 10 to 15 minutes. This rapid service alleviates the challenges of purchasing heavy oil bottles and encourages spontaneous buys of premium organic variants. Furthermore, e-commerce offers a unique advantage: D2C brands can gather first-party data on repurchase rates and flavor preferences, guiding product development in ways traditional wholesale models fall short.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High production costs and premium pricing | -0.8% | Global, most acute in price-sensitive Asia-Pacific and Latin America | Short term (≤ 2 years) |

| Limited certified organic oilseed supply | -0.9% | Global, with acute shortages in sunflower, rapeseed, and sesame | Medium term (2-4 years) |

| Competition from conventional oils | -0.6% | Emerging markets in Asia-Pacific, Africa, and South America | Long term (≥ 4 years) |

| Fraud and adulteration risk with testing gaps | -0.4% | Europe (olive oil), Asia (sesame oil), and global premium segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High production costs and premium pricing

Middle- and low-income markets find organic oils less affordable due to production costs being 40% to 60% higher than conventional oils. This price hike is attributed to factors like organic certification, lower crop yields, manual harvesting, and chemical-free extraction. Farms certified for organic oilseeds avoid synthetic fertilizers and pesticides, leading to a 20% to 30% drop in per-hectare yields compared to their conventional counterparts. Additionally, organic certification fees, annual inspections, and the need for segregated storage infrastructure introduce fixed costs that challenge small-scale farmers. Cold-press extraction, while favored for its purity, yields 10% to 15% less oil per kilogram of seed than methods like high-temperature screw pressing or hexane extraction, pushing up production costs per liter. These production inefficiencies are mirrored in retail prices. In the Asia-Pacific region, where disposable income growth lags behind food inflation, price sensitivity is pronounced. For instance, Japan's cooking oil market saw double-digit price surges, leading consumers to opt for cheaper blended oils and curtail their overall consumption. In response, processors are trialing "half-use" formulations, blending organic oils with conventional ones to achieve competitive pricing while still promoting clean-label claims. However, this strategy could potentially alienate purist consumers.

Limited certified organic oilseed supply

Global demand for organic oilseeds is outstripping certified acreage, creating feedstock shortages that constrain processor capacity and inflate raw material costs. Organic sunflower seed supply in Europe and North America has not expanded in line with demand for organic sunflower oil, forcing processors to import from Ukraine and Argentina at elevated freight costs and geopolitical risk. Organic rapeseed and canola acreage in Canada and the EU remains a small fraction of total oilseed plantings, as farmers prioritize higher-margin organic wheat and soybeans over oilseeds with lower per-hectare returns. Sesame oil processors in Asia face similar bottlenecks; organic sesame cultivation requires labor-intensive weeding and pest management, deterring smallholder adoption in India and Myanmar. The 3-year transition period required for organic certification delays supply responses to price signals, meaning that even if farmers begin converting acreage in 2026, certified organic oilseeds will not reach the market until 2031. Processors are responding by offering forward contracts and technical assistance to farmers willing to transition, but these programs require upfront capital that smaller mills lack.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Oil Type: Avocado Oil Disrupts Olive Dominance

In 2025, olive oil held a 33.59% share of the organic edible oil market, reflecting its strong appeal in Mediterranean cuisines and established supply chains in Spain, Italy, and Greece. Avocado oil, the fastest-growing oil type, is projected to expand at a 7.48% CAGR from 2026 to 2031, driven by its heat stability for frying, neutral flavor appealing to non-Mediterranean consumers, and monounsaturated fat profile aligning with ketogenic and paleo diets. Coconut oil remains popular in South and Southeast Asia for traditional cooking and in North America for baking and personal care, though concerns over its saturated fat content limit growth in health-conscious segments. Sunflower, sesame, and almond oils cater to niche culinary and cosmetic markets, with sesame oil particularly strong in Japanese and Korean cuisines. Canola oil, despite its omega-3 benefits, faces challenges from anti-GMO sentiment, as most conventional canola is genetically modified. Organic non-GMO canola oil commands a premium but holds a small market share.

Founded in 2025 in Seville, Spain, the Avocado Oil Manufacturers Association aims to set global quality and sustainability standards for avocado oil and provide access to advanced extraction technologies. This highlights the industry's recognition of avocado oil's potential to rival olive oil in premium markets. In August 2024, Chosen Foods launched a 27-ounce squeeze bottle of 100% pure avocado oil, priced between USD 15.99 and USD 19.99, targeting consumers seeking gluten-free, glyphosate-residue-free, Non-GMO Project certified oils with a 500°F smoke point for high-heat cooking. Olive oil producers are emphasizing polyphenol content, single-estate origins, and early-harvest flavors to differentiate extra virgin olive oil from commodity avocado oil. However, avocado oil's versatility, especially for deep frying, gives it a structural advantage over olive oil.

By Packaging Type: Cans Gain on Sustainability

In 2025, bottles led the organic edible oil packaging market with a 65.69% share, driven by consumer familiarity, ease of pouring, and compatibility with retail shelves. From 2026 to 2031, cans are expected to grow at a 7.07% CAGR, the fastest among packaging formats. Brands are adopting cans to extend shelf life, prevent light-induced oxidation, and reduce plastic waste. Metal cans effectively block oxygen and ultraviolet light, preserving polyunsaturated fats and antioxidants that degrade in clear glass or PET bottles. This makes cans ideal for high-value cold-pressed oils, where rancidity is a major concern. Jars cater to small-batch producers and gift packaging, while pouches and bag-in-box systems serve foodservice and bulk retail. Sustainability mandates are driving the shift to cans, with European retailers phasing out single-use plastics. Aluminum cans also offer higher recycling rates compared to mixed-material bottles with plastic caps and labels.

In August 2024, Chosen Foods launched a squeeze bottle innovation, introducing flexible HDPE bottles that reduce material use and improve portion control compared to rigid glass bottles. The squeeze format appeals to home cooks with its one-handed operation and precise drizzling but lacks the premium aesthetic of glass bottles, which command higher shelf prices. Cans face challenges in premium markets, where glass bottles symbolize quality and authenticity. For example, single-estate olive oil producers in Spain and Italy resist cans due to perceived downmarket associations, despite their superior product protection. Regulatory compliance for food-contact materials adds complexity, with EU standards requiring migration testing for metal can coatings, increasing costs for smaller packers.

By Distribution Channel: Online Retail Captures Subscription Demand

Supermarkets and hypermarkets captured 43.12% of organic edible oil distribution in 2025, leveraging high foot traffic, impulse purchase opportunities, and the ability to offer taste samples and in-store promotions. Online retail will expand at 7.20% CAGR from 2026 to 2031, the fastest distribution channel, driven by subscription models that lock in repeat purchases, quick-commerce platforms that deliver within hours, and direct-to-consumer brands that bypass wholesale markups. Convenience stores and specialty stores serve top-up purchases and curated assortments, respectively, while other channels include foodservice distributors and farm-direct sales. The shift to online is most pronounced in urban Asia-Pacific markets, where quick-commerce penetration is highest, and in North America, where Amazon and Thrive Market have established dedicated organic grocery categories.

Gramiyaa's channel mix, 34% quick commerce, 32% marketplaces, 14% D2C website, 20% physical retail, illustrates the multi-channel imperative for organic oil brands seeking to maximize reach while controlling margins. Quick commerce platforms such as Blinkit and Zepto in India fulfill orders within 10 to 15 minutes, reducing the friction associated with purchasing heavy oil bottles and enabling impulse purchases of premium organic variants. Subscription models are particularly effective for organic oils, where consumers exhibit high brand loyalty once they identify a preferred flavor profile and price point; Oliva Dorado offers subscription options that deliver single-estate organic extra virgin olive oil on a recurring schedule, reducing customer acquisition costs and improving lifetime value Oliva Dorado. Traditional supermarkets are responding by expanding online pickup and delivery services, but their cost structures, real estate, labor, and inventory holding place them at a disadvantage relative to digital-native competitors operating from centralized fulfillment centers.

Geography Analysis

In 2025, Europe commanded a 37.40% share of the organic edible oil market, bolstered by stringent EU organic labeling, the allure of Mediterranean olive groves, and retailers' preference for premium single-estate SKUs. German and French consumers are pivoting from seed-oil blends to cold-pressed rapeseed variants, further energizing the region’s organic edible oil market. While CAP subsidies for organic conversion mitigate farmer risks, water scarcity in Spain and Italy poses challenges to future volume growth. Meanwhile, Eastern Europe's lower land costs are drawing private-equity investments into sunflower and flaxseed conversions, with an eye on meeting Northern Europe's demand peaks by 2029.

Asia-Pacific is set to lead with the highest regional CAGR of 7.58% through 2031, fueled by rising middle-class incomes, urbanization, and heightened food-safety concerns in China, India, and Japan. China's fragmented certification landscape muddies consumer trust, paving the way for blockchain-verified imports from Australia and Canada. Urban millennials in India are increasingly opting for cold-pressed groundnut and sesame oils over refined palmolein, though price disparities hinder rural adoption. Japan's cooking-oil market, on track to hit USD 1.92 billion by 2029 with a 5.2% CAGR, showcases a shift towards premiumization, as shoppers prioritize quality over price, drawn by functional claims, polyphenol content, and smoke-point labeling[2]Source: Agriculture and Agri-Food Canada, “Canada–Japan Agri-Food Trade Data 2026,” agr.gc.ca .

North America stands tall as a consumption titan, with the U.S. leading in organic avocado and olive oil absorption. Canada emerges as a key organic canola supplier to Asia, leveraging CPTPP tariff preferences, though its acreage expansion grapples with climatic uncertainties and certification delays. In South America, Brazil and Argentina are channeling investments into expeller-pressed sunflower and soybean conversions, yet face hurdles in export reliability due to logistics and certification issues. The Middle East witnesses a burgeoning demand in the gourmet retail segments of the UAE and Saudi Arabia; however, wider regional acceptance is stymied by price sensitivities and a nascent cold-chain infrastructure.

Competitive Landscape

The competitive landscape is moderately fragmented. Global players like Cargill, CHO GROUP, Fresh Del Monte, and Newman’s Own, Inc. span the spectrum from oilseed origination and milling to bottling, ensuring they secure feedstock and achieve economies of scale. In 2025, these giants collectively represented roughly one-third of the global revenue. However, nimble direct-to-consumer entrants are chipping away at this share, spotlighting their emphasis on provenance and chemical-free extraction. In March 2025, Fresh Del Monte bolstered its vertical integration by acquiring Avolio, an avocado oil processor based in Uganda[3]Source: Fresh Del Monte Produce Inc., “Fresh Del Monte Acquires Majority Stake in Avolio,” freshdelmonte.com. This move not only allowed them to convert grade-B fruit into a premium oil but also mitigated risks associated with raw material supply. Meanwhile, U.S. brands are expanding their horizons, introducing flavored avocado dips and vinaigrettes, and capitalizing on their established oil reputation to tap into these lucrative condiment markets.

Investments in technology are reshaping cost dynamics. Firms utilizing supercritical CO₂ extraction methods are achieving yields that surpass those of mechanical pressing by up to 8 percentage points, thereby closing the retail price gap with traditional oils. In premium markets, blockchain traceability is becoming a standard expectation, prompting smaller producers to band together through cooperatives. Marketing strategies are increasingly favoring digital platforms, with partnerships with micro-influencers proving more effective than traditional TV ads in reaching millennial consumers. Global retailers are increasingly demanding supply-chain resilience, especially multi-origin sourcing strategies that mitigate climate risks. This demand is putting pressure on specialists tied to single countries, pushing them to either diversify their estates or secure long-term offtake agreements.

While barriers to entry are moderate, challenges persist. Costs associated with certification, the need for capital-intensive extraction equipment, and the necessity of established distributor relationships tend to favor industry incumbents. Yet, the organic edible oil market presents opportunities, especially in under-explored varietals like high-oleic sunflower and toasted black sesame. This opens doors for niche players aiming for premium shelf placements. Although retailer private labels heighten price competition, they also enhance consumer access and familiarity with the category, potentially broadening the market for branded innovators.

Organic Edible Oil Industry Leaders

Cargill Incorporated

CHO GROUP

Dcoop

Newman’s Own, Inc.

The Hain Celestial Group, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Chosen Foods launched a new avocado oil-based chili dipping sauce at Natural Products Expo West 2026, made with 100% pure avocado oil and positioned as seed-oil-free. The product is distributed through Walmart, Sprouts, Thrive Market, and Amazon, with additional retailers planned for spring 2026. This expansion into value-added condiments reflects the company's strategy to capture higher margins beyond commodity oils.

- September 2025: Chosen Foods expanded nationwide retail distribution of its 100% Pure Organic Avocado Oil, launching 500 ml bottles at Walmart, Kroger, HEB, Meijer, and Thrive Market; 1 L bottles at Whole Foods Market, Costco (Texas and Midwest clubs), and BJ's Wholesale Club; 4.7 oz Organic Spray at Whole Foods Market and Thrive Market; and 2 L bottles on Amazon. The company reported that avocado oil has sustained over 30% year-over-year growth.

- June 2025: O Olive Oil & Vinegar introduced California's first organic extra virgin olive oil in a chef-style squeeze bottle. The California-based olive oil producer has also launched a premium extra virgin olive oil in the same bottle format. Both products aim to provide convenient kitchen use while maintaining the company's established quality standards in olive oil and wine vinegar production.

Global Organic Edible Oil Market Report Scope

Organic edible oil is a food-grade oil extracted from seeds, fruits, or nuts that have been grown and processed according to strict organic farming standards. The organic edible oil market is segmented by oil type, packaging type, distribution channels, and geography. By oil type, the market is segmented into olive oil, coconut oil, avocado oil, sunflower oil, sesame oil, almond oil, canola oil, and others. By packaging type, the market is segmented into bottles, jars, cans, and others. By distribution channel, the market is segmented into supermarkets/hypermarkets, convenience stores, specialty stores, online retail stores, and others. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Tons).

| Olive Oil |

| Coconut Oil |

| Avocado Oil |

| Sunflower Oil |

| Sesame Oil |

| Almond Oil |

| Canola (Rapeseed) Oil |

| Others |

| Bottles |

| Jars |

| Cans |

| Others |

| Supermarkets/Hypermarkets |

| Convenience Stores |

| Specialty Stores |

| Online Retail Stores |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Sweden | |

| Belgium | |

| Poland | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Thailand | |

| Singapore | |

| Indonesia | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Peru | |

| Chile | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Saudi Arabia | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| Oil Type | Olive Oil | |

| Coconut Oil | ||

| Avocado Oil | ||

| Sunflower Oil | ||

| Sesame Oil | ||

| Almond Oil | ||

| Canola (Rapeseed) Oil | ||

| Others | ||

| Packaging Type | Bottles | |

| Jars | ||

| Cans | ||

| Others | ||

| Distribution Channel | Supermarkets/Hypermarkets | |

| Convenience Stores | ||

| Specialty Stores | ||

| Online Retail Stores | ||

| Others | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Sweden | ||

| Belgium | ||

| Poland | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Thailand | ||

| Singapore | ||

| Indonesia | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Peru | ||

| Chile | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Saudi Arabia | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large will organic edible oil demand be by 2031?

The organic edible oil market size is expected to reach USD 42.18 billion by 2031, reflecting a 6.73% CAGR from 2026.

Which oil type is growing fastest?

Avocado oil leads growth at a forecast 7.48% CAGR, driven by its 500°F smoke point and monounsaturated profile.

Which region offers the highest expansion opportunities?

Asia-Pacific shows the strongest outlook at 7.58% CAGR thanks to rising middle-class demand in China, India, and Japan.

What packaging trend should suppliers monitor?

Metal cans are scaling rapidly at 7.07% CAGR as brands seek light-barrier protection and higher recycling rates.

Page last updated on: