DDR5 DRAM Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 26.51 Billion |

| Market Size (2031) | USD 71.44 Billion |

| Growth Rate (2026 - 2031) | 21.93% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

DDR5 DRAM Market Analysis by Mordor Intelligence

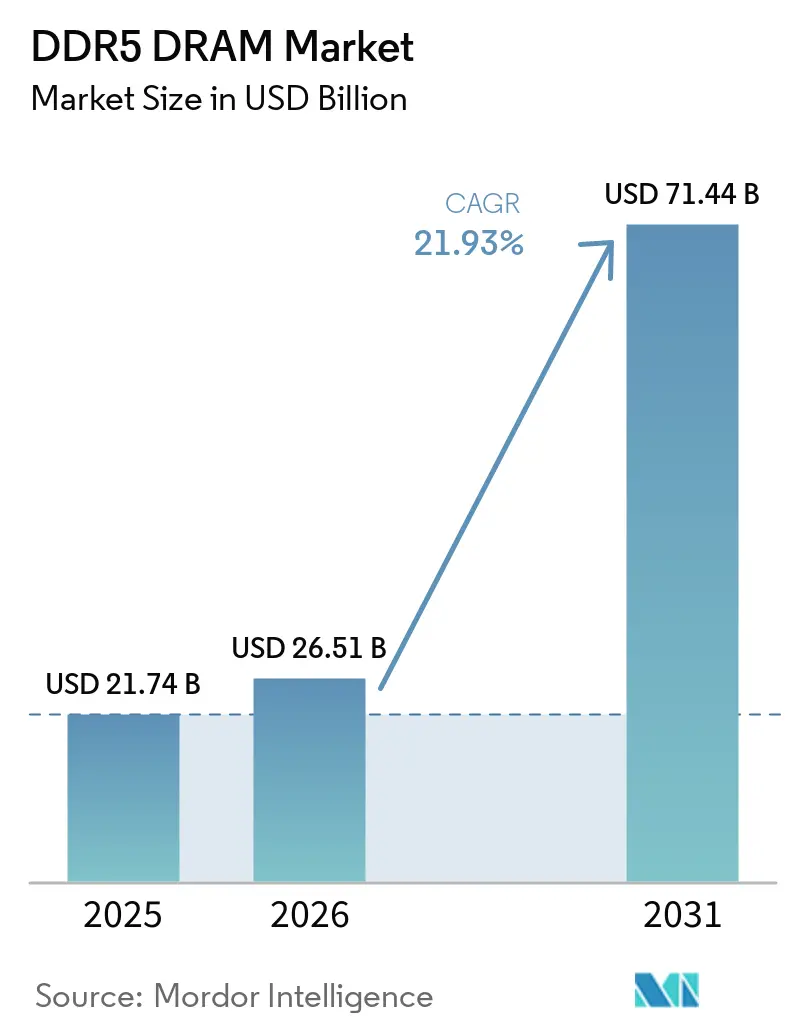

The DDR5 DRAM market size is projected to be USD 21.74 billion in 2025, USD 26.51 billion in 2026, and reach USD 71.44 billion by 2031, growing at a CAGR of 21.9% from 2026 to 2031. The DDR5 DRAM market is being lifted by AI infrastructure spending that is tied to long-cycle server build programs rather than normal seasonal swings in memory demand. High-end server CPU platforms now require DDR5 by design, which is pushing platform migration faster than in earlier memory transitions. The top DRAM manufacturers have moved DDR4 closer to end-of-life, which has reduced the economic case for staying on older platforms and shortened enterprise upgrade timing. Hyperscaler capital commitments already extend well beyond 2026, which is giving the DDR5 DRAM market a steadier demand base than prior upcycles. Supply remains tight because HBM allocation, advanced-node yield limits, and the split between U.S.-aligned and China-focused supply chains continue to support a firmer pricing floor across the DDR5 DRAM market.

Key Report Takeaways

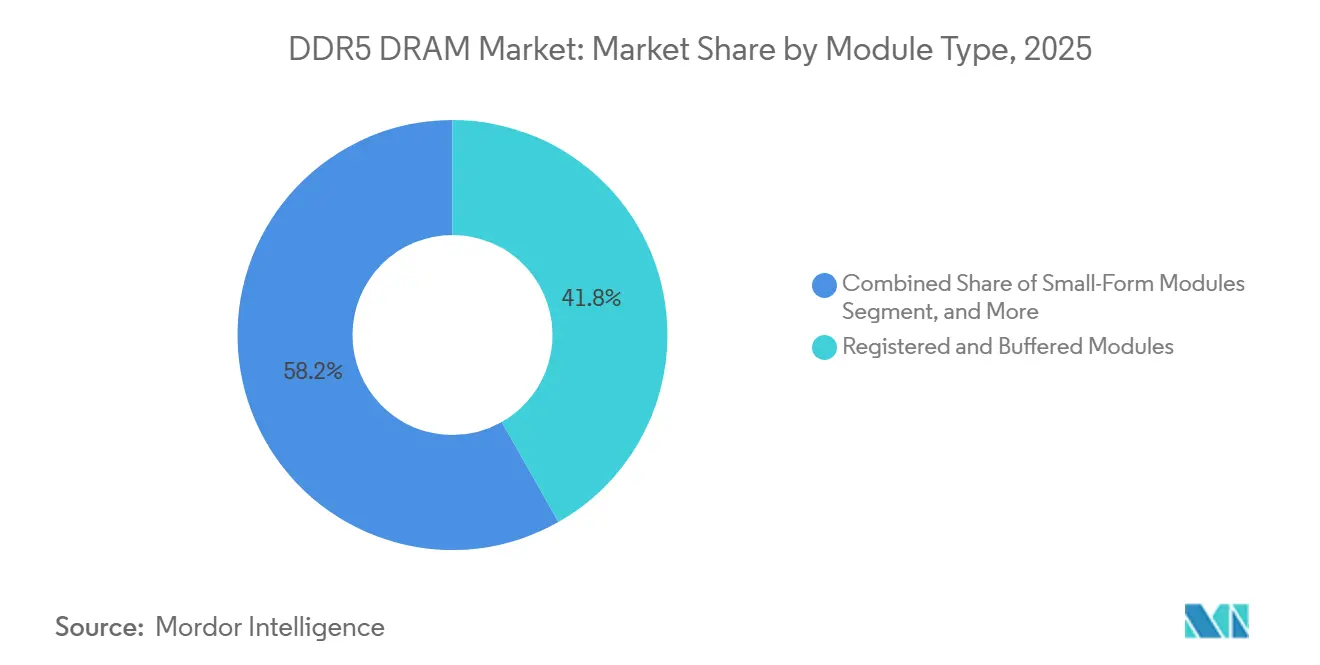

- By module type, Registered and Buffered Modules held 41.8% share in 2025 in the DDR5 DRAM market, while Small-Form Modules are projected to grow at 25.0% CAGR through 2031.

- By capacity, the 24 GB-32 GB tier led with 34.2% share in 2025 in the DDR5 DRAM market, while the above 128 GB tier is forecast to expand at 25.2% CAGR through 2031.

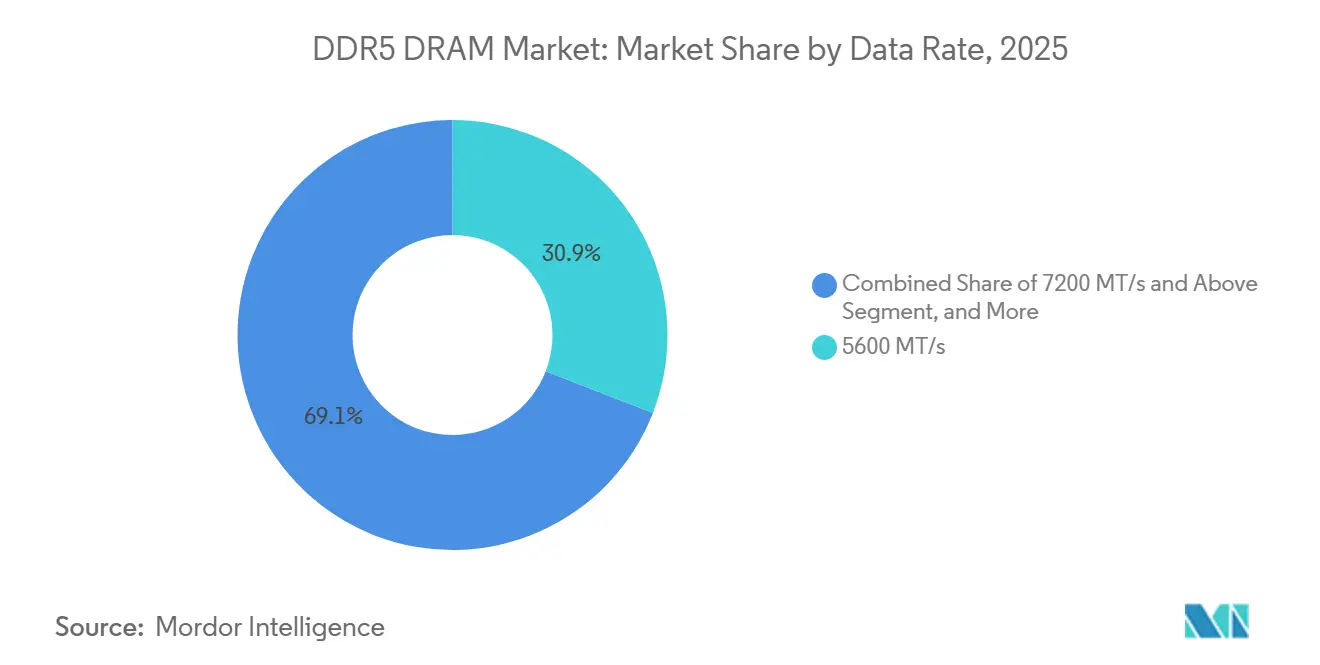

- By data rate, 5600 MT/s accounted for 30.9% share in the DDR5 DRAM market in 2025, while 7200 MT/s and above is projected to record the fastest growth at 24.8% CAGR through 2031.

- By end use, servers and hyperscale data centers represented 45.7% of demand in 2025, while automotive compute platforms are expected to post the highest growth at 23.7% CAGR through 2031.

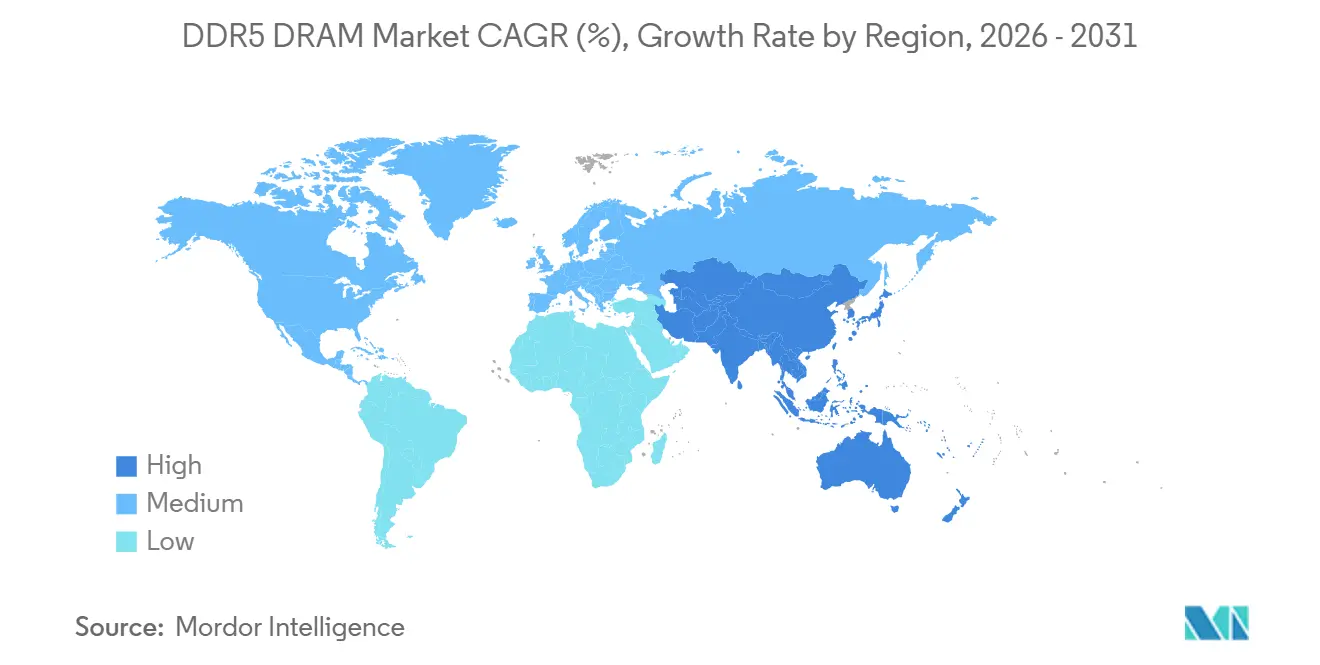

- By geography, Asia-Pacific held 47.4% share in 2025 and is also the fastest-growing regional category with a projected 22.9% CAGR through 2031.

- By supplier concentration, Samsung Electronics, SK hynix, and Micron Technology collectively accounted for over 93% of global DRAM wafer production in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global DDR5 DRAM Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI Server Memory Density Scaling | +4.2% | Global, concentrated in North American and East Asian hyperscaler clusters | Short term (≤ 2 years) |

| DDR5-Only Server CPU Transition | +3.8% | Global, early adoption in North America and East Asia | Medium term (2-4 years) |

| Narrowing DDR5-to-DDR4 Price Gap | +3.5% | Global, with faster adoption in South and Southeast Asia | Short term (≤ 2 years) |

| Bandwidth-Per-Watt Gains For Power-Constrained Data Centers | +3.0% | North America and Europe, where power density regulations apply | Medium term (2-4 years) |

| CXL-Attached Memory Expansion | +2.2% | North America and East Asia, where CXL-compliant server deployment is strongest | Medium term (2-4 years) |

| CAMM2 And Rugged Edge DDR5 Adoption | +1.8% | Global, with early industrial gains in Taiwan, Japan, and Germany | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

AI Server Memory Density Scaling

AI training and inference platforms need more memory density per socket than earlier server designs could support efficiently, and that requirement is changing procurement behavior across the DDR5 DRAM market. Micron stated that its 1γ DRAM node delivers over 30% more bits per wafer than the prior 1β generation, which supports higher-density DDR5 roadmaps without relying only on volume expansion.[1]Micron Technology, “1-Gamma Technology Brief,” Micron Technology, micron.com Higher density per DIMM slot lowers the number of sockets needed for AI workloads, which keeps the DDR5 DRAM market tied closely to accelerator-led infrastructure builds rather than normal server replacement cycles. Micron also framed its 1γ generation around future compute needs, which supports the view that density-tier differentiation is becoming a more durable revenue lever inside the DDR5 DRAM market. This is why capacity bands from 96 GB upward are attracting stronger investment and pricing support than commodity configurations in the DDR5 DRAM market.

DDR5-Only Server CPU Transition

The server CPU transition has moved the DDR5 DRAM market past the stage where DDR4 could remain a practical default for new high-end deployments. AMD documented that EPYC 9005 supports up to 12 channels of DDR5-6000 ECC, while JEDEC continued to advance MRDIMM standards that raise the ceiling for next-generation server memory bandwidth. AMD JEDEC As server platforms become DDR5-native, module validation is no longer a simple volume exercise, because timing, firmware, and platform-specific qualification now matter more in the DDR5 DRAM market. JEDEC’s MRDIMM Gen2 and Gen3 roadmap also shows that the performance path ahead is centered on DDR5 rather than transitional compatibility solutions. This raises the barrier for smaller vendors and shifts more server memory purchasing toward suppliers that can support broad cross-platform qualification inside the DDR5 DRAM market.

Narrowing DDR5-To-DDR4 Price Gap

The DDR5 DRAM market is also benefiting from a smaller price gap with DDR4, because buyers no longer see enough savings in legacy platforms to justify delayed migration. The wider ecosystem now supports higher-speed client and server module standards, which reduces the risk that DDR5 carries a short-lived or premium-only cost structure.[2]JEDEC Solid State Technology Association, “JEDEC Advances DDR5 MRDIMM Ecosystem With New Memory Interface Logic and Expanded MRDIMM Roadmap,” JEDEC, jedec.org As qualification pipelines, power management components, and clocking architectures mature, DDR5 adoption becomes easier to standardize across procurement cycles in the DDR5 DRAM market. Rambus and JEDEC both moved the ecosystem toward more stable client module specifications through 2025 and 2026, which supports the case for broader cost normalization as volumes rise. That shift matters because once cost parity becomes more visible, vendors without active DDR5 roadmaps face exclusion from the DDR5 DRAM market rather than short-term margin pressure.

Bandwidth-Per-Watt Gains For Power-Constrained Data Centers

Bandwidth-per-watt has become a direct buying criterion in the DDR5 DRAM market as power availability tightens across large data center campuses. SK hynix and Intel reported that DDR5 on 4th-generation Intel Xeon Scalable processors delivered 70% higher bandwidth than DDR4-3200 while using 14.4% less power, which improved performance per watt at the server level. The IEA-4E EDNA study also showed that memory remains a material share of server power use and that newer DRAM generations have consistently improved efficiency, which supports the regulatory case for DDR5 adoption.[3]IEA-4E EDNA, “Energy Efficiency of Servers Past and Possible Future Trends,” IEA-4E EDNA, iea-4e.org In practice, that recovered power headroom can be reassigned to accelerators rather than to more general server density, which strengthens the role of DDR5 in AI-oriented rack planning. This makes energy efficiency a multiplier for compute density and supports sustained procurement across the DDR5 DRAM market, especially where power intensity rules shape colocation and enterprise refresh decisions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| HBM Capacity Pull Constraining Conventional DDR5 Supply | -3.2% | Global, most acute in North America and East Asia | Short term (≤ 2 years) |

| EUV Yield And Ramp Challenges On High-Density DDR5 Dies | -2.5% | East Asia and the United States | Medium term (2-4 years) |

| Export-Control And China-Localization Bifurcation | -2.1% | Asia-Pacific, with spillover to global supply chains | Medium term (2-4 years) |

| Qualification Complexity Across CUDIMM, MRDIMM, And CAMM2 | -1.9% | Global, with the highest friction in North America and Europe server procurement | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

HBM Capacity Pull Constraining Conventional DDR5 Supply

The main supply-side restraint in the DDR5 DRAM market is that advanced-node wafer capacity is being pulled toward higher-margin HBM programs at the same time that DDR5 server demand is rising. SK hynix accelerated investment in Yongin Fab 1, with total project commitment of KRW 31 trillion, or USD 21.5 billion, which shows how strongly suppliers are preparing for sustained advanced memory demand rather than short-cycle normalization. Micron’s 1γ roadmap also makes clear that leading-edge process gains are central to future compute products, which implies continued competition for the same advanced manufacturing resources. As long as the best process windows remain scarce, server DDR5 output is likely to stay tighter than end demand would suggest in the DDR5 DRAM market. That supports a firmer pricing floor and tends to favor large integrated manufacturers over branded module vendors that depend on upstream allocation.

EUV Yield And Ramp Challenges On High-Density DDR5 Dies

EUV ramp complexity remains another meaningful restraint for the DDR5 DRAM market because higher-density die transitions are more sensitive to process stability than prior generations. Micron said its 1γ node achieved over 30% more bits per wafer than 1β, but it also noted that additional EUV layers raise process complexity in a non-linear way. That matters most in the 96 GB to 256 GB server module range, where the DDR5 DRAM market is seeing the strongest demand pull from AI platforms and memory-expanded systems. The result is a narrow operating window where suppliers must meet both density and yield targets at the same time, which slows the pace at which high-capacity DDR5 can become widely available. Until yields stabilize more fully, the DDR5 DRAM market is likely to face recurring tightness in the exact tiers that customers want most.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Module Type: Server Buffered Modules Lead While Mobile Form Factors Narrow The Gap

Registered and Buffered Modules held 41.8% share of the DDR5 DRAM market size in 2025, which made them the largest module category during the first stage of platform migration. The DDR5 DRAM market has leaned toward RDIMM, LRDIMM, and MRDIMM demand because hyperscale and enterprise server upgrades came earlier than broad consumer replacement. JEDEC advanced the DDR5 MRDIMM Gen2 standard in April 2026 with a target of 12,800 MT/s and also began work on Gen3 with a 17,600 MT/s direction, which extends the long-range performance roadmap for buffered memory. That standards path matters because MRDIMM adoption is tied to specific platform support, which makes qualification depth more important than simple unit availability in the DDR5 DRAM market. As a result, buffered module competition is becoming more relationship-driven and less purely price-led.

Small-Form Modules are the fastest-growing module type in the DDR5 DRAM market, with a 25.0% CAGR from 2026 to 2031, supported by AI-capable notebooks, compact workstations, and rugged edge systems. JEDEC published the updated CUDIMM and CQDIMM common standard in February 2026, which formalized clocked client modules up to 9,600 MT/s and improved the design base for smaller high-speed form factors. Rambus reinforced that direction in May 2026 by releasing a complete DDR5 9600 client memory module chipset for CUDIMM, CQDIMM, and CSODIMM modules. The DDR5 DRAM industry is therefore seeing faster growth at the edge of the form-factor spectrum, where thinner systems and local AI workloads need more bandwidth without a server-sized footprint. Specialty and industrial modules also keep premium margins because certification, thermal range, and reliability support still matter more than headline pricing in these smaller deployment niches.

By Capacity: High-Density Configurations Drive The Next Server Architecture Cycle

The 24 GB-32 GB segment held 34.2% of the DDR5 DRAM market size in 2025, which kept it as the volume backbone for mainstream server and workstation installs. In the DDR5 DRAM market, this range remains attractive because it balances per-slot cost discipline with enough bandwidth and capacity for broad enterprise workloads. The above 128 GB category is expanding the fastest, at 25.2% CAGR from 2026 to 2031, because AI inference systems need more memory per socket to avoid disaggregation penalties and system complexity. Micron’s 1γ node roadmap, with over 30% more bits per wafer than the prior generation, supports the push toward larger DDR5 modules and a shorter cycle between 128 GB and higher-density server configurations. This is one of the clearest places where the DDR5 DRAM market is moving from volume-led growth to mix-led growth.

The 48 GB-64 GB and 96 GB-128 GB bands are also gaining traction in the DDR5 DRAM market because enterprise refresh cycles now focus more on cost per workload than on the lowest upfront system cost. Astera Labs said its Leo-series CXL 2.0 smart memory controllers support up to 2 TB per card across multiple DDR5-5600 channels, which shows that high-density DIMMs and CXL expansion are now competing for the same workload budgets. That overlap means the 96 GB to 128 GB boundary has become a strategic decision point inside the DDR5 DRAM market, because buyers must choose between larger DIMMs and memory expansion cards. The DDR5 DRAM industry is also seeing the up to 16 GB tier lose relevance as default notebook and desktop configurations move higher. Capacity decisions now shape architecture decisions more directly than in prior client-led memory cycles.

By Data Rate: 5600 MT-S Sets The Current Floor While 7200 MT-S And Above Redefines The Ceiling

The 5600 MT/s tier accounted for 30.9% share in 2025, which made it the largest speed segment across the DDR5 DRAM market. This tier became the practical baseline because it met the needs of mainstream server and consumer PC deployments as DDR5 replaced DDR4 in default platform planning. The 7200 MT/s and above segment is the fastest-growing part of the DDR5 DRAM market size, advancing at 24.8% CAGR from 2026 to 2031 as AI servers and high-end workstations move toward MRDIMM and clocked module architectures. JEDEC’s publication of the JESD82-552 multiplexed rank data buffer standard and the continued MRDIMM roadmap confirm that much higher speed operation is now part of the formal ecosystem path rather than a narrow vendor claim. Rambus also released the first complete DDR5 9600 client chipset in May 2026, which supports a wider commercial path to higher-speed modules beyond the server tier.

The 4800 MT/s tier is moving toward legacy status in the DDR5 DRAM market and is now more relevant in specialty and industrial programs that favor thermal validation over peak throughput. The 6400 MT/s tier is set to remain the core server baseline through much of the forecast period because it fits current performance and qualification needs across broad enterprise deployments. Research published in arXiv found that moving from DDR5-6400 RDIMM to MRDIMM-8800 on Intel Granite Rapids delivered large bandwidth gains and strong performance improvement for bandwidth-bound workloads, with up to 30% server energy savings in the memory-extended bandwidth region. That evidence supports the view that the premium speed tiers in the DDR5 DRAM market are not only headline upgrades, but also a direct efficiency lever for systems with sustained memory utilization. As utilization rises, the speed ladder becomes a bigger revenue driver for suppliers across the DDR5 DRAM market.

By End-Use Application: Hyperscale Governs Demand While Automotive Builds Structural Momentum

Servers and hyperscale data centers held 45.7% of the DDR5 DRAM market share in 2025, which kept them as the leading end-use category. The DDR5 DRAM market remains centered on cloud and AI server demand because those buyers moved first and purchased at scale as platform requirements shifted toward higher bandwidth and density. Automotive compute platforms are the fastest-growing end-use category, with a 23.7% CAGR from 2026 to 2031, as centralized vehicle architectures need compute-grade memory that meets strict reliability and safety thresholds. SK hynix said its automotive LPDDR5X achieved ASIL-D certification under ISO 26262 through TÜV SÜD, which shows how safety qualification is becoming a gatekeeper for memory adoption in advanced vehicle electronics. That makes automotive a structurally distinct growth lane in the DDR5 DRAM market rather than a spillover from consumer memory demand.

Enterprise and workstation demand is also rising because local AI inference systems need larger memory footprints and stronger performance consistency than prior business PCs. The DDR5 DRAM market is benefiting from lower migration friction in desktops and notebooks as the ecosystem matures and price barriers continue to ease. Edge and industrial deployments are widening through CAMM2 and rugged DDR5 designs, while telecom and networking programs are gradually adding DDR5 to newer base station and infrastructure processors. JEDEC’s LPDDR5 CAMM2 connector standard provided the ecosystem with a more consistent path for modular low-profile memory adoption, which supports broader use in compact and purpose-built systems. As a result, the DDR5 DRAM market is expanding across a broader end-use base even while servers remain the main volume anchor.

Geography Analysis

Asia-Pacific accounted for 47.4% of the DDR5 DRAM market size in 2025 and is projected to expand at 22.9% CAGR through 2031, which makes it both the largest and fastest-growing region. The DDR5 DRAM market in Asia-Pacific is anchored by South Korea, where Samsung Electronics and SK hynix remain the core supply-side pillars for advanced DRAM manufacturing. SK hynix committed KRW 31 trillion, or USD 21.5 billion, to Yongin Semiconductor Cluster Fab 1 and accelerated the first cleanroom toward February 2027 operations, which shows how strongly regional capacity planning is aligned with future advanced memory demand. China is also pushing a more localized memory supply chain, which is adding another layer to procurement strategy and regional segmentation inside the DDR5 DRAM market. Taiwan and Japan continue to support the regional value chain through module assembly and advanced packaging, while India is emerging more gradually as a consumer and assembly destination.

North America is the most concentrated demand center in the DDR5 DRAM market because hyperscaler spending on AI servers has kept server memory procurement unusually strong. The region also benefits from a tighter link between infrastructure spending and platform validation, which gives qualified suppliers more predictable order visibility than in past memory upcycles. Long-term agreements and domestic supply security goals are becoming more important in the DDR5 DRAM market here, because large buyers want less exposure to spot-price volatility and less uncertainty around upstream allocation. This demand structure is more stable than the client-led cycles that shaped earlier DRAM transitions.

Europe represents a smaller but more differentiated part of the DDR5 DRAM market, with enterprise, industrial, and automotive-adjacent demand carrying more weight than hyperscale volume. The IEA-4E EDNA study and the SK hynix-Intel case study both support DDR5’s value in energy-sensitive server environments, which fits well with Europe’s stronger emphasis on power efficiency and compliance. Germany, the United Kingdom, and France remain the main demand anchors, while the rest of Europe adds volume more gradually through enterprise refresh activity. Rest of the World remains smaller in the DDR5 DRAM market, but imported branded modules and selected colocation builds are still widening the customer base across the Middle East, Africa, and South America.

Competitive Landscape

The DDR5 DRAM market is split between a highly concentrated die-level structure and a much more fragmented module-level structure. Samsung Electronics, SK hynix, and Micron Technology controlled over 93% of global DRAM wafer production in 2025, which means supply access remains the central competitive advantage in the DDR5 DRAM market. At this level, competition is shaped less by shelf presence and more by fab technology, node execution, and the ability to secure long-duration customer commitments. Micron positioned its 1γ process as a cost-per-bit improvement over the prior generation, with over 30% more bits per wafer, which supports its margin and supply strategy in higher-value DDR5 programs. JEDEC’s work on MRDIMM standards also strengthens vendors that can handle deep silicon characterization and server-grade validation at scale.

At the module level, the DDR5 DRAM market includes more than 17 branded vendors such as Kingston Technology, ADATA, Corsair Gaming, G.SKILL, Innodisk, SMART Modular Technologies, and Apacer. These companies compete more on platform certification, product specialization, and support capability than on wafer economics, because they sit further downstream in the DDR5 DRAM market. One clear strategic move came from Rambus, which released its DDR5 9600 client chipset for CUDIMM, CQDIMM, and CSODIMM modules in May 2026 to support faster AI PC and workstation memory designs. Another came from SK hynix, which completed customer validation of its 96 GB CMM-DDR5 module based on CXL 2.0 and showed both higher capacity and better bandwidth than comparable point-to-point DDR5 configurations.

A third strategic move in the DDR5 DRAM market came from Marvell, which announced the Structera S 30260 in March 2026 to support rack-level memory pooling through CXL switching. Astera Labs also advanced this architecture with its Leo-series CXL smart memory controllers, which broaden the route for memory expansion where DIMM slots are already saturated. These moves show that competition in the DDR5 DRAM market is spreading beyond standard DIMMs and toward memory pooling, memory expansion, and platform-specific qualification. No company in the reviewed vendor set is fully outside the DDR5 DRAM market, although Biwin Storage Technology and Lexar remain more flash-weighted than DRAM-focused when compared with vendors more closely aligned to industrial and specialty DDR5 supply.

DDR5 DRAM Industry Leaders

Samsung Electronics Co., Ltd.

SK hynix Inc.

Micron Technology, Inc.

Nanya Technology Corporation

Winbond Electronics Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Rambus Inc. released its DDR5 9600 Client Memory Module Chipset for CUDIMM, CQDIMM, and CSODIMM modules, incorporating a Gen2 Client Clock Driver, CKD02, supporting up to 9,600 MT/s and a PMIC5120 for power management. The chipset targets next-generation AI PCs, notebooks, and workstations and represents the performance vanguard for consumer-grade DDR5 memory module speeds, signaling a near-term transition well above mainstream 6400 MT/s configurations.

- April 2026: JEDEC published JESD82-552, DDR5 Multiplexed Rank Data Buffer standard, and advanced the MRDIMM Gen2 standard targeting 12,800 MT/s, while initiating MRDIMM Gen3 development toward 17,600 MT/s. The announcements formalize a multi-generation MRDIMM speed roadmap with direct implications for AI server platform memory bandwidth planning.

- March 2026: Marvell Technology announced the Structera S 30260, a 260-lane CXL switch enabling rack-level DDR5 memory pooling alongside Marvell's near-memory accelerators and memory-expansion controllers. Customer sampling is targeted from Q3 2026, with the previous-generation Structera S 20256 CXL 2.0 switch already in production.

- February 2026: Innodisk launched its CXL Add-In Card, HHHL PCIe interface, compact DDR5 RDIMM or RDIMM VLP configuration, for scalable edge AI memory expansion, targeting micro data centers, 5G networking nodes, and smart medical imaging platforms with latency-critical memory requirements.

Global DDR5 DRAM Market Report Scope

The DDR5 DRAM Market refers to the market for fifth-generation double data rate dynamic random-access memory used in computers, servers, data centers, and other high-performance electronic systems. DDR5 offers higher bandwidth, lower power consumption, improved density, and better efficiency than prior DDR generations, making it suitable for AI, cloud computing, gaming, and enterprise workloads.

The DDR5 DRAM Market Report is Segmented by Module Type (Unbuffered Client Modules (DDR5 UDIMM, and CUDIMM, Small-Form Modules (DDR5 SODIMM, CSODIMM, CAMM2, and LPCAMM2), Registered and Buffered Modules (DDR5 RDIMM, LRDIMM, MRDIMM, and Other Buffered Server Memory Modules), and Specialty and Industrial Modules (Ruggedized DDR5 Modules, Industrial-temperature Modules, Embedded/on-board DDR5 Modules)), Small-Form Modules (DDR5 SODIMM, CSODIMM, CAMM2, and LPCAMM2), and More), Capacity (Up to 16 GB, 24-128 GB, 48 GB - 64 GB, 96 GB - 128 GB, and Above 128 GB), Data Rate (4800 MT/s, 5200 MT/s, 5600 MT/s, 6400 MT/s, and 7200 MT/s and Above), End-Use Application (Servers and Hyperscale Data Centers, Enterprise and Workstations, Consumer Desktops, Notebooks and Mobile PCs, Edge and Industrial Systems, Telecom and Networking Infrastructure. and Automotive Compute Platforms), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

| Unbuffered Client Modules (DDR5 UDIMM, and CUDIMM) |

| Small-Form Modules (DDR5 SODIMM, CSODIMM, CAMM2, and LPCAMM2) |

| Registered and Buffered Modules (DDR5 RDIMM, LRDIMM, MRDIMM, and Other Buffered Server Memory Modules) |

| Specialty and Industrial Modules (Ruggedized DDR5 Modules, Industrial-temperature Modules, Embedded/on-board DDR5 Modules) |

| Up to 16 GB |

| 24 GB - 32 GB |

| 48 GB - 64 GB |

| 96 GB - 128 GB |

| Above 128 GB |

| 4800 MT/s |

| 5200 MT/s |

| 5600 MT/s |

| 6400 MT/s |

| 7200 MT/s and Above |

| Servers and Hyperscale Data Centers |

| Enterprise and Workstations |

| Consumer Desktops |

| Notebooks and Mobile PCs |

| Edge and Industrial Systems |

| Telecom and Networking Infrastructure |

| Automotive Compute Platforms |

| Other End-Use Applications |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| Taiwan | |

| India | |

| Rest of Asia-Pacific | |

| Rest of the World |

| By Module Type | Unbuffered Client Modules (DDR5 UDIMM, and CUDIMM) | |

| Small-Form Modules (DDR5 SODIMM, CSODIMM, CAMM2, and LPCAMM2) | ||

| Registered and Buffered Modules (DDR5 RDIMM, LRDIMM, MRDIMM, and Other Buffered Server Memory Modules) | ||

| Specialty and Industrial Modules (Ruggedized DDR5 Modules, Industrial-temperature Modules, Embedded/on-board DDR5 Modules) | ||

| By Capacity | Up to 16 GB | |

| 24 GB - 32 GB | ||

| 48 GB - 64 GB | ||

| 96 GB - 128 GB | ||

| Above 128 GB | ||

| By Data Rate | 4800 MT/s | |

| 5200 MT/s | ||

| 5600 MT/s | ||

| 6400 MT/s | ||

| 7200 MT/s and Above | ||

| By End-Use Application | Servers and Hyperscale Data Centers | |

| Enterprise and Workstations | ||

| Consumer Desktops | ||

| Notebooks and Mobile PCs | ||

| Edge and Industrial Systems | ||

| Telecom and Networking Infrastructure | ||

| Automotive Compute Platforms | ||

| Other End-Use Applications | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| Taiwan | ||

| India | ||

| Rest of Asia-Pacific | ||

| Rest of the World | ||

Key Questions Answered in the Report

How large is the DDR5 DRAM market in 2026?

The DDR5 DRAM market stands at USD 26.51 billion in 2026 and is projected to reach USD 71.44 billion by 2031 at a 21.9% CAGR.

What is driving DDR5 adoption in servers and AI infrastructure?

AI training and inference workloads need higher memory density and bandwidth, while newer server CPU platforms are now centered on DDR5 rather than DDR4.

Which module category leads current demand?

Registered and Buffered Modules led with 41.8% share in 2025 because server and hyperscale deployments were the first major wave of DDR5 adoption.

Which capacity range is growing the fastest?

The above 128 GB tier is the fastest-growing capacity segment, with a projected 25.2% CAGR from 2026 to 2031.

Which region has the strongest position in DDR5 DRAM?

Asia-Pacific led with 47.4% share in 2025 and is also the fastest-growing region, with a projected 22.9% CAGR through 2031.

Why are automotive platforms becoming important for DDR5 suppliers?

Automotive compute platforms are expected to grow at 23.7% CAGR through 2031 because centralized vehicle architectures need memory that meets strict safety and reliability standards.

Page last updated on: