LPDDR5 DRAM Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 5.23 Billion |

| Market Size (2031) | USD 7.89 Billion |

| Growth Rate (2026 - 2031) | 8.72% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

LPDDR5 DRAM Market Analysis by Mordor Intelligence

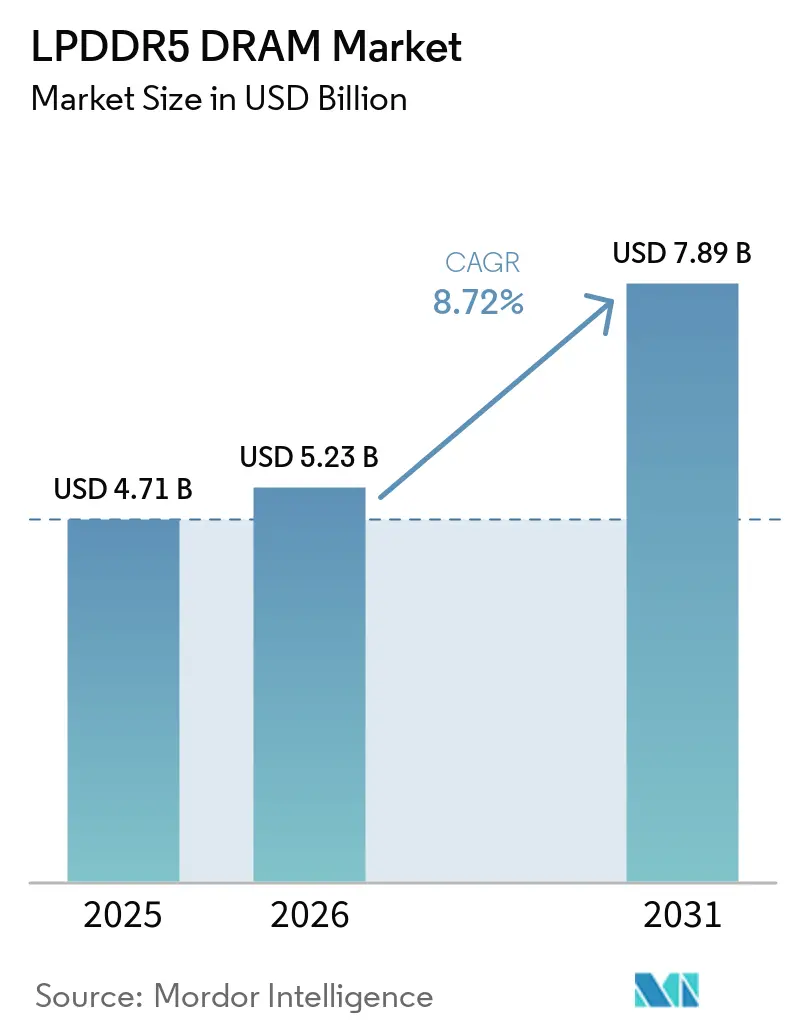

The LPDDR5 DRAM market size is expected to increase from USD 4.71 billion in 2025 to USD 5.23 billion in 2026 and reach USD 7.89 billion by 2031, growing at a CAGR of 8.72% over 2026-2031. The main demand push comes from on-device AI in flagship smartphones, where memory baselines are moving from 12 GB toward 16 GB to support multimodal large language model workloads and real-time imaging at the edge. LPDDR5X accounted for a major share of revenue in 2025, indicating the installed base has already shifted firmly toward the higher-bandwidth standard rather than treating it as a niche premium option. On the supply side, the phase-down of LPDDR4X by major Korean and U.S. suppliers narrowed the price gap with next-generation mobile DRAM and reduced a major adoption barrier for mid-range device makers. Demand is now spreading across notebooks, automotive compute, and AI inference hardware, which gives the LPDDR5 DRAM market more than one growth engine through 2031. Competition remains highly concentrated among Samsung Electronics, SK hynix, and Micron Technology, while CXMT is intensifying pricing pressure in the mid-market tier, and HBM-related wafer shifts keep supply conditions tight.

Key Report Takeaways

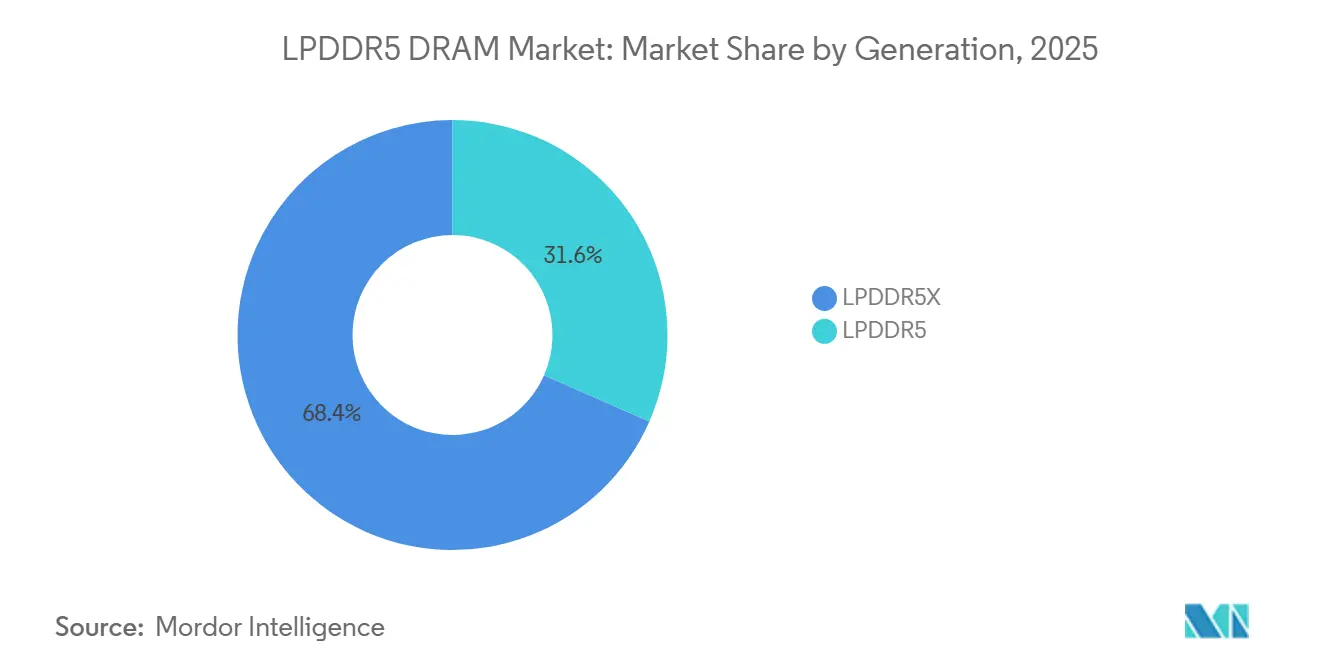

- By generation, LPDDR5X accounted for 68.42% of revenue in 2025 and is projected to grow at a 9.12% CAGR through 2031 in the LPDDR5 DRAM market.

- By product configuration, Package-on-Package/On-Package LPDDR DRAM held 47.98% of revenue in 2025, while LPDDR5/LPDDR5X Modular Memory Formats are projected to expand at a 9.52% CAGR through 2031.

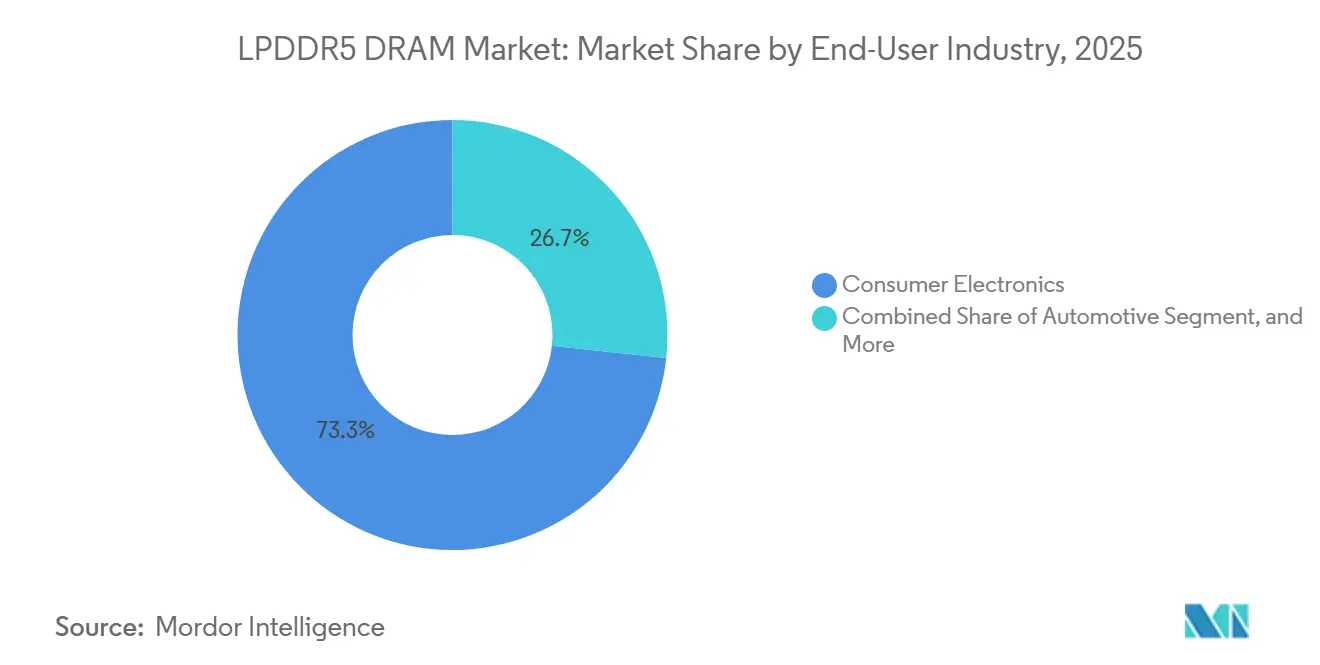

- By end-user industry, consumer electronics held 73.29% of revenue in 2025, while data center and cloud infrastructure are projected to expand at a 9.68% CAGR through 2031 in the LPDDR5 dynamic random access memory (DRAM) market.

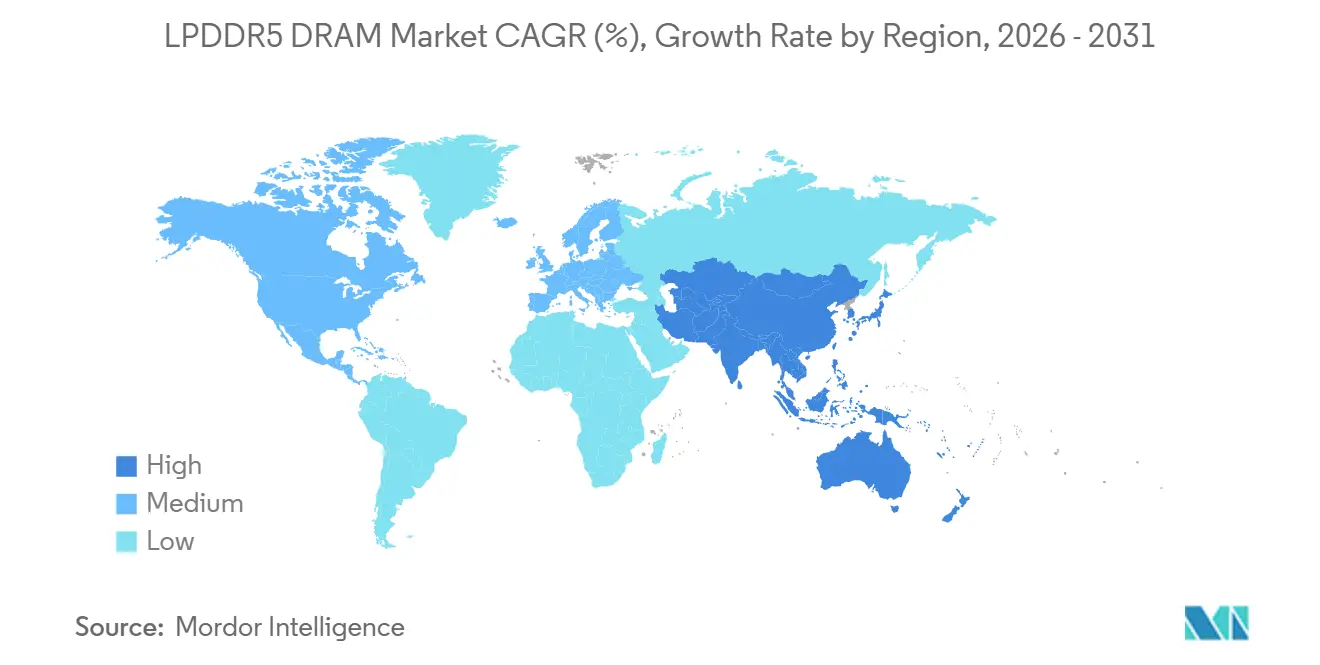

- By geography, Asia-Pacific held 67.08% of revenue in 2025, while Europe is projected to expand at a 9.47% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global LPDDR5 DRAM Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| On-Device AI Smartphone DRAM Content Uplift | +2.8% | Global, with Asia-Pacific core, China, South Korea, Taiwan | Short term (≤ 2 years) |

| LPDDR4X Supply Squeeze Accelerating LPDDR5X Migration | +2.2% | Global | Short term (≤ 2 years) |

| AI PC and Thin-and-Light Notebook Adoption | +1.5% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Automotive Centralized E/E and ADAS Memory Demand | +1.1% | Europe, Japan, South Korea, China | Medium term (2-4 years) |

| LPDDR5X Use in AI Inference Accelerators | +0.8% | North America, Europe | Medium term (2-4 years) |

| Thinner High-Density Packages Enabling Ultra-Slim Devices | +0.5% | Global, with Asia-Pacific manufacturing core | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

On-Device AI Smartphone DRAM Content Uplift

The LPDDR5 DRAM market is gaining strong momentum from on-device AI, because newer flagship phones now need higher throughput and lower power draw for local language, vision, and imaging workloads. Micron began shipping qualification samples of its 1γ LPDDR5X in June 2025 at 10.7 Gbps, with 20% power savings over 1β DRAM and a 0.61 mm package thickness, aimed at 2026 flagship smartphones. Micron also said the node delivered a 30% improvement in LLM query response time and a 50% reduction in translation latency when running the Llama 2 model on mobile hardware, which directly links memory gains to user-visible AI performance. Samsung started mass production of 12nm-class 12 GB and 16 GB LPDDR5X packages in August 2024 at 0.65 mm, with 9% lower thickness and 21% better heat resistance than the prior generation, which helped smartphone vendors balance performance and thermal design. These combined advances are pushing the LPDDR5 dynamic random access memory (DRAM) market deeper into AI-focused handset programs faster than a typical replacement cycle would allow.

LPDDR4X Supply Squeeze Accelerating LPDDR5X Migration

The LPDDR5 DRAM market is also moving ahead because device makers are losing the option to rely on LPDDR4X for long new design cycles in consumer products. Samsung and Micron both center their current mobile low-power DRAM offerings on LPDDR5X, indicating that supplier roadmaps now position the newer standard at the core of product planning rather than at the edge of premium demand.[1]Micron Technology, “Micron Ships World’s First 1γ (1-Gamma)-Based LPDDR5X, Enabling Rich Mobile AI Experiences,” Nasdaq, nasdaq.com That shift matters because the earlier price and sourcing gap between LPDDR4X and LPDDR5X is no longer as wide as it was when mid-range brands first evaluated migration. CXMT entered LPDDR5X mass production in May 2025 with 8,533 Mbps and 9,600 Mbps products, and it moved a 10,667 Mbps version into customer sampling in 2026, adding a new supply option for Chinese OEMs and raising competitive pressure in the mid-tier. As a result, the LPDDR5 DRAM market is shifting into a narrower upgrade window where platform refresh timing and supplier availability now matter as much as pure component pricing.

AI PC and Thin-And-Light Notebook Adoption

The LPDDR5 DRAM market is gaining a second structural growth leg from AI PCs and thinner notebooks, where low-power memory is becoming a standard pairing for local AI compute. Dell launched its redesigned XPS 13 in 2026 with LPDDR5X-7467 memory, demonstrating how premium thin-and-light systems are moving toward the newer standard without sacrificing portability. Lenovo extended LPCAMM2 with LPDDR5X into the ThinkBook 14+ and 16+ range in 2026, moving the format beyond premium workstations and into broader notebook volumes where replaceability now matters more than before. AMD also said its 6th-generation EPYC "Verano" server CPU will support LPDDR5X SOCAMM2 modules in AI rack-scale systems, which connects notebook-led modular adoption with future infrastructure use cases. This shift is widening the LPDDR5 DRAM market beyond soldered mobile designs and making upgradeable low-power memory relevant in both client and data center systems.

Automotive Centralized E/E and ADAS Memory Demand

The LPDDR5 DRAM market is benefiting from the move toward centralized vehicle compute, because newer automotive platforms need more memory bandwidth and tighter safety qualification than earlier domain-based systems. Micron said central compute units for Level 2+ ADAS use 4 GB to 16 GB of DRAM per SoC, while platforms nearing Level 4 autonomy require memory bandwidth above 1 TB per second, which highlights how quickly memory demand rises with software-defined vehicle architectures. SK hynix received ISO 26262 ASIL-D certification from TÜV SÜD for its automotive LPDDR5X in January 2026, with SPFM of 99% or higher and LFM of 90% or higher, which strengthens its position in safety-critical vehicle programs. Micron’s LPDDR5X with direct-link ECC also achieved ISO 26262 ASIL-D certification and delivered a 15-25% increase in bandwidth over conventional in-line ECC schemes, making the product more attractive for high-reliability architectures. These qualification barriers keep the LPDDR5 DRAM market more concentrated in automotive programs than in mainstream consumer devices.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| SoC Compatibility Limits in Entry and Mid-Tier Devices | -1.3% | Asia-Pacific, India, Southeast Asia, South America, Middle East and Africa | Short term (≤ 2 years) |

| HBM-Led Wafer Reallocation and Price Inflation | -0.9% | Global | Medium term (2-4 years) |

| Real-World Bandwidth Shortfall Versus Headline Specs | -0.5% | Global | Long term (≥ 4 years) |

| Automotive Qualification and Long-Lifecycle Validation Drag | -0.3% | Europe, North America, Japan | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

SoC Compatibility Limits in Entry and Mid-Tier Devices

The biggest near-term limit on the LPDDR5 DRAM market remains SoC compatibility in entry-tier and low-cost smartphones. JEDEC documentation makes clear that LPDDR5X is part of a newer memory standard stack, so devices without compatible memory controllers cannot migrate to it through simple memory substitution.[2]JEDEC Solid State Technology Association, “LPDDR, GDDR, and HBM for Auto AI Applications,” JEDEC, jedec.org This leaves a large installed base of 4G and lower-cost 5G designs on LPDDR4X or base LPDDR5, even when the pricing gap to LPDDR5X narrows. The effect is strongest in South and Southeast Asia, South America, and the Middle East and Africa, where the sub-USD 100 and USD 150-250 handset bands still account for meaningful unit volumes. Until compatible 5G platforms spread deeper into those price tiers, the LPDDR5 DRAM market will stay weighted toward premium and upper-mid devices.

HBM-Led Wafer Reallocation and Price Inflation

The LPDDR5 DRAM market also faces supply pressure because advanced DRAM capacity is being pulled toward AI-related products that command higher value per package. Intel said its Crescent Island data center GPU will use up to 480 GB of LPDDR5X, indicating that large accelerator platforms now compete directly with mobile and PC products for advanced low-power memory. AMD has also positioned LPDDR5X SOCAMM2 as a power-focused memory option for future AI rack-scale servers, which broadens infrastructure demand for the same ecosystem. As more high-value AI systems adopt LPDDR5X, handset and notebook makers face tighter lead times and stronger contract-pricing pressure in cost-sensitive designs. This keeps the LPDDR5 DRAM market exposed to supply volatility even as its demand base becomes more diverse.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Generation: LPDDR5X Leads in Value and Growth

LPDDR5X held 68.42% of the LPDDR5 DRAM market share in 2025 and is projected to expand at a 9.12% CAGR through 2031, making it the leading generation and the fastest-growing one. That position stems from the way flagship smartphones, AI PCs, and centralized automotive compute platforms now favor higher-bandwidth memory interfaces for AI-capable workloads. Micron began shipping qualification samples of its 1γ LPDDR5X in June 2025 at 10.7 Gbps with a 0.61 mm package thickness, directly supporting thinner 2026 mobile and notebook designs. LPDDR5 remained relevant in mid-tier systems and longer-cycle automotive programs where migration to LPDDR5X has not yet fully passed through qualification and controller support.

SK hynix announced in March 2026 that it had developed 1c-node LPDDR6 with a base speed above 10.7 Gbps and 20% better power efficiency than LPDDR5X, with supply scheduled to begin in the second half of 2026. That roadmap matters, but it does not displace current volume demand because LPDDR5X remains the production standard for the 2026-2028 shipping window. In the LPDDR5 DRAM industry, this keeps value concentrated in the premium layer, where bandwidth, thermal behavior, and package thickness most strongly influence device positioning. It also means LPDDR5 continues to function as a bridge standard rather than a full-fledged competitor in the LPDDR5 DRAM market.

By Product Configuration: On-Package Designs Hold Scale While Modules Open New Paths

Package-on-Package/On-Package LPDDR DRAM held 47.98% of the LPDDR5 DRAM market size in 2025, while modular memory formats are projected to expand at a 9.52% CAGR through 2031. The leading share reflects how smartphones and tablets still depend on close processor-memory integration to reduce signal latency and conserve board space. Samsung’s August 2024 launch of 0.65 mm 12nm-class LPDDR5X packages set a visible benchmark for thin, thermally resilient on-package designs in mobile hardware. This keeps on-package architecture central to the LPDDR5 DRAM market, where compact form factors still dominate unit volumes.

At the same time, LPCAMM2 and SOCAMM2 are changing upgrade economics inside the LPDDR5 DRAM market by bringing low-power memory into replaceable notebook and server modules. Lenovo introduced the LPCAMM2 LPDDR5X-8533 in its ThinkBook 14+ and 16+ lines in 2026, bringing the format into more mainstream laptop volumes. AMD said its 6th-generation EPYC "Verano" platform will support LPDDR5X SOCAMM2, with Micron, Samsung, and SK hynix developing conforming products for AI rack-scale systems. In the LPDDR5 DRAM industry, this matters because modular formats widen the addressable base without changing the low-power performance profile that made LPDDR attractive in the first place. MCP and uMCP products still support dense 5G handsets and cost-sensitive mobile designs, while discrete board-mounted parts remain relevant in embedded systems that require separate thermal and service layouts.

By End-User Industry: Consumer Devices Anchor Volume While Infrastructure Drives Growth

Consumer electronics accounted for 73.29% of the LPDDR5 DRAM market size in 2025, while data center and cloud infrastructure are projected to expand at a 9.68% CAGR through 2031. The largest share still comes from smartphones, tablets, laptops, and gaming handhelds, where LPDDR5X content growth is lifting memory value per device. Intel detailed Crescent Island in June 2026, featuring up to 480 GB of LPDDR5X for enterprise AI inference, marking the first large-scale commercial accelerator design built around this memory type. Cadence also introduced a 9,600 Mbps LPDDR5X memory IP system with Microsoft RAIDDR ECC for enterprise and data center applications in January 2026, showing that supporting infrastructure is now being built around higher-reliability LPDDR deployments.

This shift gives the LPDDR5 DRAM market a new growth vector that had little scale just 3 years earlier. Automotive demand is also rising as centralized E/E architecture and functional safety certification push qualified LPDDR5X deeper into ADAS and autonomous control programs. Industrial and embedded demand is emerging in robotics, smart cameras, and edge computing platforms, where low-power memory supports localized processing and compact thermal design. The end-user mix, therefore, keeps the LPDDR5 DRAM market anchored in consumer device volumes, even as future growth tilts toward enterprise inference and automotive compute.

Geography Analysis

Asia-Pacific accounted for 67.08% of the LPDDR5 DRAM market in 2025, making the region the clear center of both production and downstream device assembly. The region combines Samsung and SK hynix supply in South Korea, CXMT capacity in China, and major packaging and electronics manufacturing activity across Taiwan and wider Asia-Pacific.[3]ChangXin Memory Technologies, “CXMT Announces LPDDR5X Mass Production,” CXMT, cxmt.com China remains the most strategically sensitive sub-market because CXMT confirmed in October 2025 that its 8,533 Mbps and 9,600 Mbps LPDDR5X products had entered mass production in May 2025, while a 10,667 Mbps version moved into customer sampling in 2026. South Korea remains central to the LPDDR5 DRAM market because Samsung and SK Hynix continue to push the roadmap through thinner packages, automotive certification, and the first public steps toward LPDDR6. Japan and the rest of Asia-Pacific add demand through automotive electronics, industrial systems, and contract manufacturing, which pull components from the same regional supply base.

Europe is projected to expand at a 9.47% CAGR through 2031, giving it the fastest regional pace in the LPDDR5 dynamic random access memory (DRAM) market. Growth comes from premium automotive platforms moving toward centralized E/E systems, rising enterprise AI PC deployments, and hyperscale data center expansion in Frankfurt, Amsterdam, and Dublin. The region also benefits from a strong automotive electronics base that values ASIL-D-qualified memory, keeping LPDDR5X relevant in premium vehicle compute platforms. Public and private semiconductor investment supports Europe’s strategic ambitions, even though meaningful domestic LPDDR output remains limited in the near term.

North America remains a major specification center for the LPDDR5 DRAM market, as regional chip designers are shaping processor platforms that increasingly require LPDDR5X in AI-native systems. AI PC demand in the United States supports procurement as notebook designs from leading platform vendors move low-power memory into commercial refresh cycles. The rest of the world, including South America, the Middle East, and Africa, contributes a smaller revenue base where LPDDR4X still dominates entry-tier devices and LPDDR5X adoption depends on broader 5G platform diffusion. This regional pattern keeps production concentrated in Asia-Pacific while design influence and future enterprise uptake spread more broadly across North America and Europe.

Competitive Landscape

Samsung Electronics, SK hynix, and Micron Technology remain the core competitive group in the LPDDR5 DRAM market because they control the most advanced LPDDR5X production capacity and set the performance direction for leading mobile DRAM. Their positions are supported by process node progress, packaging capability, and close coordination with major computing platforms. Samsung began mass production of 12nm-class 12 GB and 16 GB LPDDR5X packages at 0.65 mm in August 2024, improving thickness by 9% and heat resistance by 21% over the prior generation.[4]Samsung Electronics Co., Ltd., “Samsung Electronics Begins Mass Production of Industry’s Thinnest LPDDR5X DRAM Packages for On-Device AI,” Samsung Newsroom, news.samsung.com Micron followed with 1γ LPDDR5X qualification samples in June 2025 at 10.7 Gbps, with 20% lower power consumption than 1β DRAM, and a 0.61 mm package targeting 2026 flagship devices. SK hynix strengthened its competitive position in January 2026 by securing ASIL-D certification for automotive LPDDR5X, which raised its credibility in safety-critical vehicle programs.

The LPDDR5 DRAM market is now moving from a triopoly toward a broader top tier as CXMT builds commercial scale in China. CXMT said its 8,533 Mbps and 9,600 Mbps LPDDR5X products entered mass production in May 2025, while its 10,667 Mbps version moved into customer sampling in 2026. That move gives Chinese OEMs a more credible domestic supply option and adds price pressure in the mid-market layer of the LPDDR5 DRAM market. Nanya Technology remains more focused on trailing-edge LPDDR5 positions, which limits its ability to challenge the leading LPDDR5X suppliers at scale.

White-space opportunities in the LPDDR5 dynamic random access memory (DRAM) market sit mainly in automotive safety-qualified memory, SOCAMM2 server modules, and future processing-in-memory directions. AMD’s 6th-generation EPYC Verano platform has already created an early incentive for Micron, Samsung, and SK hynix to develop conforming LPDDR5X SOCAMM2 products for AI rack-scale deployments. LPCAMM2 and related standards are also enabling greater module-level differentiation, opening the door for specialized manufacturers and assemblers even when DRAM die supply remains concentrated. This leaves the LPDDR5 DRAM market highly concentrated at the die level, but somewhat more open in modules, packaging, and application-specific design wins.

LPDDR5 DRAM Industry Leaders

Samsung Electronics Co., Ltd.

SK hynix Inc.

Micron Technology, Inc.

ChangXin Memory Technologies, Inc.

Nanya Technology Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Intel detailed the GPU specifications for its Crescent Island data center at Computex 2026, featuring up to 480 GB of LPDDR5X memory on a Xe3P architecture targeting enterprise AI inference workloads, with customer sampling planned for the second half of 2026. The design marks the first large-scale deployment of LPDDR5X in a commercial AI accelerator GPU, prioritizing cost-per-GB and energy efficiency over high-bandwidth memory alternatives.

- April 2026: AMD published details of its 6th-generation EPYC Verano server CPU, available in 2027, with support for LPDDR5X SOCAMM2 modules in AI rack-scale configurations. Micron Technology, Samsung Electronics, and SK hynix are all confirmed to be developing conforming SOCAMM2 products. The announcement establishes LPDDR5X as a viable complement to DDR5 RDIMMs in power-optimized data center deployments.

- April 2026: OPENEDGES Technology secured its first license for LPDDR6/5X memory subsystem IP targeting automotive, robotics, and edge server SoC platforms, reflecting growing fabless chip designer demand for LPDDR5X-capable memory IP beyond the established DRAM manufacturers.

- March 2026: SK hynix announced the successful development of 16Gb LPDDR6 DRAM on its sixth-generation 10nm-class, 1c process, achieving a base operating speed exceeding 10.7 Gbps, 33% faster and 20% more power-efficient than existing LPDDR5X, with mass production preparations targeted for the first half of 2026 and supply commencement in the second half.

Global LPDDR5 DRAM Market Report Scope

The LPDDR5 DRAM Market refers to the global market for Low-Power Double Data Rate 5 (LPDDR5) memory technologies, including LPDDR5 and LPDDR5X, designed to deliver high-speed data transfer, low power consumption, and enhanced memory bandwidth for performance-intensive computing applications. LPDDR5 DRAM serves as a critical memory component in modern electronic systems, enabling faster processing, improved energy efficiency, and support for advanced workloads such as artificial intelligence, machine learning, high-resolution imaging, edge computing, autonomous systems, and next-generation wireless communications.

The LPDDR5 DRAM Report is Segmented by Generation (LPDDR5, and LPDDR5X), Product Configuration (Discrete/Board-Mounted LPDDR DRAM Components, Package-on-Package/On-Package LPDDR DRAM, MCP/uMCP-Based LPDDR DRAM, and LPDDR5/LPDDR5X Modular Memory Formats), End-user Industry (Consumer Electronics, Automotive, Industrial and Embedded, IT and Telecommunications, and Data Center and Cloud), and Geography (North America, Europe, Asia-Pacific, and Rest of the World). The Market Forecasts are Provided in Terms of Value (USD).

| LPDDR5 |

| LPDDR5X |

| Discrete / Board-Mounted LPDDR DRAM Components |

| Package-on-Package / On-Package LPDDR DRAM |

| MCP / uMCP-Based LPDDR DRAM |

| LPDDR5 / LPDDR5X Modular Memory Formats |

| Consumer Electronics |

| Automotive |

| Industrial and Embedded |

| IT and Telecommunications |

| Data Center and Cloud Infrastructure |

| North America | |

| Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| Taiwan | |

| Rest of Asia-Pacific | |

| Rest of the World |

| By Generation | LPDDR5 | |

| LPDDR5X | ||

| By Product Configuration | Discrete / Board-Mounted LPDDR DRAM Components | |

| Package-on-Package / On-Package LPDDR DRAM | ||

| MCP / uMCP-Based LPDDR DRAM | ||

| LPDDR5 / LPDDR5X Modular Memory Formats | ||

| By End-user Industry | Consumer Electronics | |

| Automotive | ||

| Industrial and Embedded | ||

| IT and Telecommunications | ||

| Data Center and Cloud Infrastructure | ||

| By Geography | North America | |

| Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| Taiwan | ||

| Rest of Asia-Pacific | ||

| Rest of the World | ||

Key Questions Answered in the Report

What is the current and forecast size of the LPDDR5 DRAM market?

The LPDDR5 DRAM market stood at USD 4.71 billion in 2025 and stands at USD 5.23 billion in 2026. It is projected to reach USD 7.89 billion by 2031 at a CAGR of 8.72% over 2026-2031.

Which generation leads demand in this space?

LPDDR5X led the market with 68.42% of revenue in 2025 and is also the fastest-growing generation, with a projected CAGR of 9.12% through 2031.

Why is smartphone demand so important for LPDDR5 DRAM?

On-device AI in flagship phones is raising memory requirements from 12 GB toward 16 GB, which increases content per device and keeps smartphones as the core volume driver.

Which end-user segment is growing the fastest?

Data center and cloud infrastructure is the fastest-growing end-user segment, with a projected CAGR of 9.68% through 2031, driven by AI inference accelerators that use LPDDR5X for power-efficient memory capacity.

Which region dominates LPDDR5 DRAM demand and supply?

Asia-Pacific led with 67.08% revenue share in 2025 because the region combines key production hubs in South Korea and China with major downstream device manufacturing across Asia.

What is the main barrier to broader adoption in lower-cost devices?

The biggest near-term barrier is SoC compatibility. Entry-tier and many low-cost 5G handsets still lack controllers that support LPDDR5X, so migration cannot happen through pricing alone.

Page last updated on: