Size and Share of LPDDR5X DRAM Market For AI PC and Thin-and-Light Laptop

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.95 Billion |

| Market Size (2031) | USD 5.82 Billion |

| Growth Rate (2026 - 2031) | 8.06% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Analysis of LPDDR5X DRAM Market For AI PC and Thin-and-Light Laptop by Mordor Intelligence

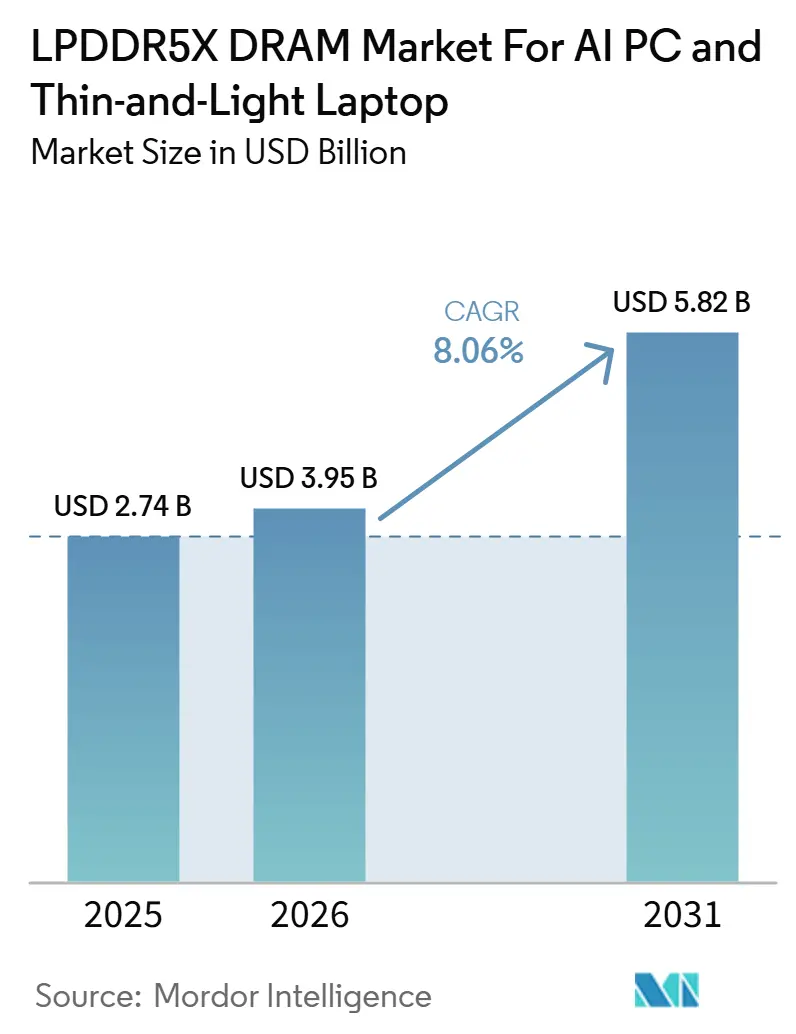

The LPDDR5X DRAM market for AI PC and thin-and-light laptop industry size stood at USD 2.74 billion in 2025 and is projected to reach USD 5.82 billion by 2031, advancing at a CAGR of 8.06% from 2026 to 2031. Microsoft’s Copilot+ PC requirements moved 16 GB memory from an optional upgrade to a baseline hardware threshold for AI-capable notebooks, which created a firmer demand floor across new launches. North America led revenue in 2025 because enterprise buyers moved early on fleet refreshes tied to Copilot+ adoption and the Windows 10 support transition. Demand is also being supported by a rising shift toward higher memory content per device, especially in premium systems that run local AI workloads for content creation, software development, and productivity. At the same time, wafer capacity is being pulled toward higher-value AI server memory, which is tightening LPDDR5X availability for notebook makers and supporting revenue growth through pricing as well as unit demand. The supply base remains concentrated around a few leading chip makers, but new LPDDR5X suppliers in China and Taiwan are starting to widen sourcing options for notebook OEMs.

Key Report Takeaways

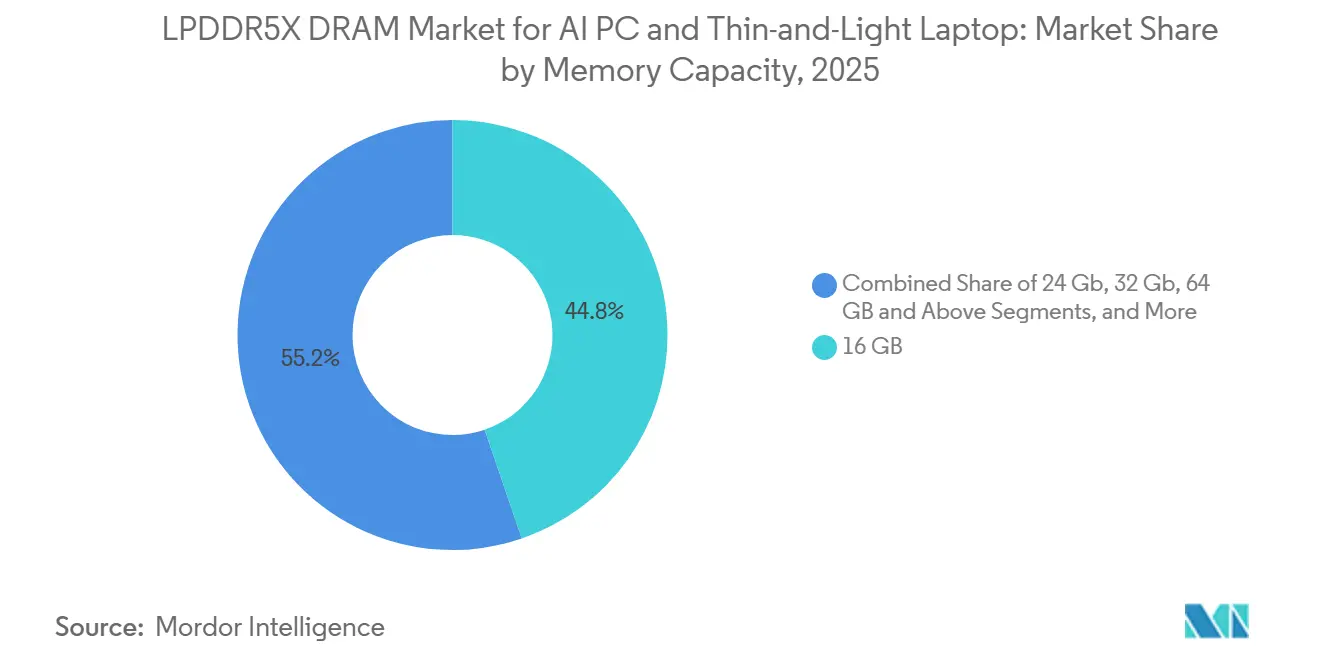

- By memory capacity, 16 GB held 44.78% of revenue share of the LPDDR5X DRAM market for AI PC and thin-and-light laptop industry in 2025, while 64 GB and above is projected to expand at a 9.44% CAGR through 2031.

- By processor platform, x86 accounted for 51.68% share of the LPDDR5X DRAM market for AI PC and thin-and-light laptop industry in 2025, while ARM is projected to record the fastest growth at a 9.65% CAGR through 2031.

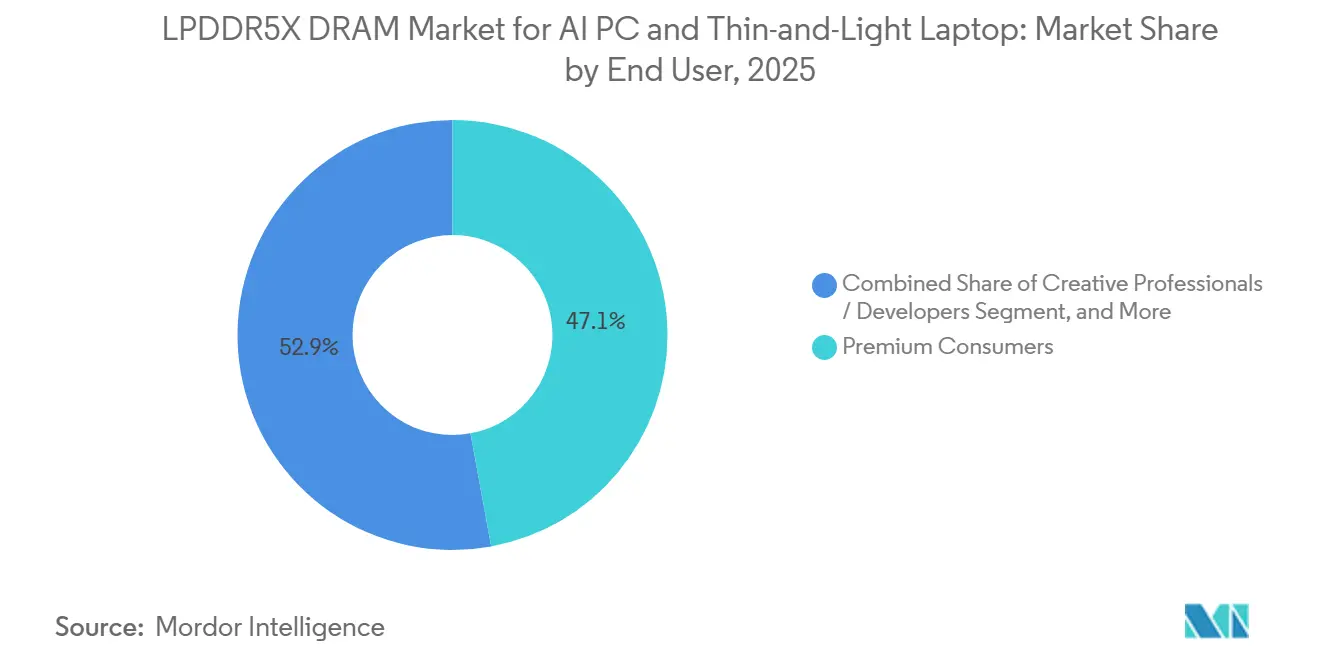

- By end user, premium consumers held 47.12% of revenue share of the LPDDR5X DRAM market for AI PC and thin-and-light laptop industry in 2025, while creative professionals and developers are projected to expand at a 9.11% CAGR through 2031.

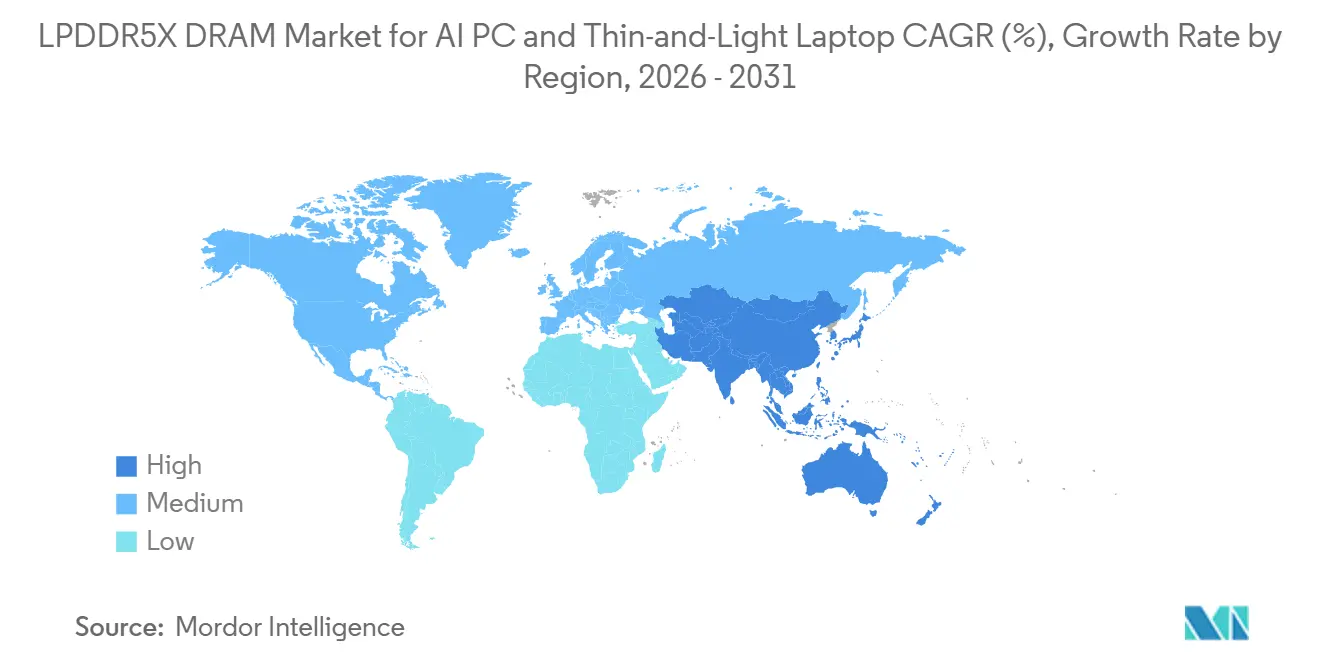

- By geography, North America held 62.28% share of the LPDDR5X DRAM market for AI PC and thin-and-light laptop industry in 2025, while Asia-Pacific is projected to expand at a 9.89% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Insights and Trends of LPDDR5X DRAM Market For AI PC and Thin-and-Light Laptop

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Copilot+ 16 GB Memory Floor | +2.2% | Global, with early gains in North America and Europe | Short term (≤ 2 years) |

| AI Notebook Penetration Lifting DRAM Content | +1.8% | Global, APAC core, spillover to Middle East and Africa | Medium term (2-4 years) |

| LPDDR5X Bandwidth and Power Edge Over DDR5 | +1.4% | Global, concentrated in North America and Asia Pacific | Medium term (2-4 years) |

| Premium AI Notebook Refresh Across x86 and ARM Platforms | +1.1% | North America and Europe, early gains in Japan and South Korea | Short term (≤ 2 years) |

| LPCAMM2 Making LPDDR More Serviceable in PCs | +0.6% | North America and Europe initially, expanding to Asia Pacific | Medium term (2-4 years) |

| On-Package Memory Freeing Battery and Thermal Budget | +0.4% | Global, with priority in Asia Pacific device manufacturing hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Copilot+ 16 GB Memory Floor Creates A Structural DRAM Demand Baseline

Microsoft’s Copilot+ PC certification made 16 GB of DDR5 or LPDDR5 memory a hard minimum for qualifying AI notebooks, and that shifted memory from an optional upgrade into a platform requirement.[1]Microsoft, “Copilot+ PCs and Windows PCs: Differences?,” Microsoft Windows Learning Center, microsoft.com. In procurement practice, 16 GB now works as the starting point instead of the final destination. Many enterprise buyers are already leaning toward 24 GB and 32 GB configurations because local AI features now sit beside regular productivity workloads throughout the day. Microsoft’s Copilot+ feature set, including experiences such as Recall, Click to Do, and live translation, keeps more of the AI workload on the device and strengthens the case for higher memory footprints over time. This keeps baseline LPDDR5X demand tied to every compliant notebook that enters the refresh cycle in the LPDDR5X DRAM market for AI PC and thin-and-light laptop industry.

AI Notebook Penetration Lifting DRAM Content Per Device

The LPDDR5X DRAM market for AI PC and thin-and-light laptops is being lifted by rising memory content per device, not only by the number of notebooks shipped. NVIDIA’s RTX Spark platform raised the ceiling by supporting up to 128 GB of unified LPDDR5X for local AI workloads in premium Windows laptops.[2]Microsoft and NVIDIA, “NVIDIA and Microsoft Reinvent Windows PCs for the Age of Personal AI,” NVIDIA Investor Relations / Microsoft Blog, investor.nvidia.com. That pushed the upper boundary far beyond the 16 GB Copilot+ floor and made high-capacity configurations more relevant to premium buyers. Creative professionals and developers are the clearest expression of this shift because large context windows, code assistants, and content tools all compete for local memory at the same time. This content-per-unit expansion helps revenue hold up even when system pricing limits broader volume adoption.

LPDDR5X Bandwidth And Power Edge Over DDR5

LPDDR5X has a clear system advantage over DDR5 in thin-and-light notebooks where power and heat matter most. Micron reported 77% lower DRAM power and up to 36% higher bandwidth in its March 2025 technical brief, which reinforced why premium notebook designs continue to favor LPDDR5X in space- and battery-constrained systems.[3]Micron Technology, “Low Power in the Data Center Technical Brief,” Micron Technology, micron.com. JEDEC’s JESD209-5C standard supports data rates from 8,533 to 10,667 Mbps, which gives enough headroom for integrated GPU and NPU workloads to run together in modern AI notebooks.[4]JEDEC, “LOW POWER DOUBLE DATA RATE (LPDDR) 5/5X,” JESD209-5C, jedec.org. Lower I/O voltage also gives notebook designers more thermal room for compute blocks and battery life targets in the LPDDR5X DRAM market for AI PC and thin-and-light laptop industry. SK hynix’s LPDDR6 roadmap points to the next generation, but it also confirms that LPDDR5X remains the working standard for high-performance thin-and-light systems across the current forecast window.

Premium AI Notebook Refresh Across x86 And ARM Platforms

Competition between x86 and ARM has shortened refresh cycles in premium notebooks and widened the addressable base for advanced memory. Microsoft kept Copilot+ qualification aligned to systems with 16 GB memory and NPUs rated at 40 or more TOPS, which pushed vendors on both architectures toward stronger baseline memory specifications. NVIDIA and Microsoft also expanded the ARM Windows opportunity with RTX Spark systems expected from ASUS, Dell, HP, Lenovo, Microsoft Surface, and MSI in fall 2026. At the same time, x86 suppliers kept pace with AI PC platform requirements, which reduced the risk that LPDDR5X adoption would depend on only one processor camp. This cross-platform refresh pattern supports stronger premium memory adoption across a broader notebook base.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| DRAM and CPU Price Spikes Inflating Notebook BOMs | -1.6% | Global, most severe in price-sensitive markets, including Southeast Asia and South America | Short term (≤ 2 years) |

| HBM-Led Capacity Shifts Tightening Client LPDDR5X Supply | -1.2% | Global, production capacity concentrated in South Korea and the United States | Medium term (2-4 years) |

| Soldered and On-Package Memory Limits Upgradeability | -0.8% | Global, particularly consumer markets in Asia Pacific | Medium term (2-4 years) |

| Windows on ARM and AI Software Fragmentation Risk | -0.5% | North America and Europe, where enterprise software stacks are most complex | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

DRAM And CPU Price Spikes Compressing OEM And Consumer Notebook Budgets

Rising memory and processor costs are putting direct pressure on notebook bills of materials and narrowing the room for aggressive configuration upgrades. When the jump from 16 GB to 32 GB LPDDR5X becomes harder to absorb, OEMs may hold more models at the Copilot+ minimum instead of pushing higher specifications. Samsung indicated that near-term supply relief remains difficult even as it planned to invest heavily in facilities in 2026 and accelerate the move toward 1c DRAM. Education and public sector buyers are especially exposed because fixed procurement budgets leave less room to absorb component inflation. This pressure does not erase demand, but it can slow the mix shift toward higher-capacity notebooks in the LPDDR5X DRAM market for AI PC and thin-and-light laptop industry.

HBM-Led Capacity Reallocation Constraining Client LPDDR5X Availability

Memory suppliers continue to prioritize advanced products tied to AI server demand, and that tightens LPDDR5X availability for notebook OEMs. Samsung and SK hynix both directed 2026 investment toward advanced memory capacity for AI demand, which showed how supplier priorities were being reshaped by data center economics. That leaves notebook brands with weaker allocation positions more exposed to spot buying and margin pressure. Relief is likely to take time because Nanya’s new Taishan plant is expected to enter volume production in the second half of 2027, while later fab additions from SK hynix also point to a delayed supply response. The result is a supply constraint that looks structural through the medium term rather than purely cyclical in the LPDDR5X DRAM market for AI PC and thin-and-light laptop industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Memory Capacity: Higher DRAM Tiers Gain Ground As On-Device AI Inference Scales

The 16 GB tier held 44.78% share of the LPDDR5X DRAM market for AI PC and thin-and-light laptop industry in 2025, while the 64 GB and above tier is projected to expand at a 9.44% CAGR through 2031. That pattern shows a clear split between the compliance floor and the premium workload ceiling. The 16 GB configuration remains the main volume anchor because it satisfies Copilot+ requirements and still fits tighter notebook budgets. At the same time, 24 GB, 32 GB, and 48 GB options are filling the middle of the range as OEMs try to balance AI performance, power use, and selling price.

JEDEC’s LPDDR5X standard supports per-die densities that make higher-capacity multi-chip packages possible without a matching increase in board footprint, which helps mid-tier and premium designs scale up more efficiently. NVIDIA’s RTX Spark platform, with up to 128 GB of unified LPDDR5X, widened the upper end of the notebook memory envelope and gave premium AI laptops a new capacity reference point. Framework’s Laptop 13 Pro also showed that LPCAMM2 can bring user-replaceable LPDDR5X into thin notebook designs, which supports wider adoption of higher capacities over a system’s life cycle. The memory mix inside the LPDDR5X DRAM market for AI PC and thin-and-light laptop is therefore widening at both the baseline tier and the premium tier.

By Processor Platform: x86 Retains Volume Leadership While ARM Accelerates

x86 platforms accounted for 51.68% of revenue share of the LPDDR5X DRAM market for AI PC and thin-and-light laptop industry in 2025, while ARM is projected to record the faster expansion at a 9.65% CAGR through 2031. The x86 lead still reflects its broad installed base in commercial, education, and small business notebooks, where software compatibility remains critical. That installed base gives Intel and AMD a strong position in near-term AI PC rollouts, especially when fleet buyers want minimal workflow disruption. ARM, however, is moving from a narrower story into a broader platform contest as more suppliers target premium Windows notebooks and high-efficiency laptop designs.

NVIDIA’s RTX Spark added a second major ARM Windows route into premium notebooks, while Apple’s MacBook line continues to reinforce LPDDR5X as a standard feature in high-end ARM laptop design. Windows on ARM still faces a software readiness gap in enterprise environments, but ARM’s AppReady program is aimed at speeding native application support and easing that barrier over time. Microsoft’s Copilot+ framework applies the same baseline memory and NPU thresholds across architectures, which means the memory requirement does not favor x86 or ARM on its own. For the LPDDR5X DRAM industry, that keeps processor competition focused on performance, efficiency, and software readiness rather than on memory eligibility.

By End User: Premium Consumers Anchor Revenue While Creative Workloads Lift Growth

Premium consumers held 47.12% share of the LPDDR5X DRAM market for AI PC and thin-and-light laptop industry in 2025, while creative professionals and developers are projected to expand at the fastest 9.11% CAGR through 2031. Premium buyers moved early because they were more willing to pay for high-ASP notebooks with stronger AI features and higher memory configurations. Creative professionals and developers are growing faster because generative design tools, coding assistants, and local inference workflows all push memory demand beyond entry configurations. Enterprise and commercial buyers remained the second-largest group as the Windows 10 support deadline compressed corporate refresh activity into a tighter purchasing cycle.

Public programs also supported demand in institutional channels, including Canada’s fiscal 2026 allocation of CAD 450 million, which was equivalent to USD 333 million, for AI PCs. That created a meaningful opening for education and public sector purchases, even though these accounts remain more sensitive to configuration cost than premium consumer buyers. Small business and prosumer customers remain the most exposed to BOM pressure because they lack the scale advantages that large enterprises use in procurement. This keeps the end-user mix tilted toward groups that either value premium performance or can justify the cost through productivity gains.

Geography Analysis

North America held 62.28% of global revenue in 2025, giving it the largest position in the LPDDR5X DRAM market for AI PC and thin-and-light laptop. The region moved early because enterprise fleets adopted Copilot+ notebooks sooner and because the Windows 10 support transition narrowed the refresh window for many organizations. A U.S. federal endpoint directive issued in March 2025 also added public-sector momentum by pushing civilian agencies toward AI-capable systems. Premium consumers and creative users in the region also moved faster into 32 GB and above configurations, which raised average memory content per notebook. Canada added another layer of structural support through a fiscal 2026 AI PC procurement allocation of CAD 450 million, which was equivalent to USD 333 million.

Asia-Pacific is projected to expand at a 9.89% CAGR through 2031, making it the fastest-growing geography within the LPDDR5X DRAM market for AI PC and thin-and-light laptop industry size by region. The region combines two powerful roles because it is both the main production base for advanced memory and a rising demand center for AI notebooks. South Korea and Taiwan remain central to supply through Samsung, SK hynix, and Nanya, while China is building a more domestic LPDDR5X chain around CXMT and local notebook OEMs. CXMT began mass production of LPDDR5X in October 2025, and later reporting indicated that its parts were being sampled by Chinese notebook makers, which strengthened the regional supply story. Japan and South Korea are also important on the demand side because enterprise refresh activity and premium consumer adoption remain active in both markets.

Europe and the Rest of the World represent smaller shares today, but they remain strategically important for future mix quality. In Europe, regulated sectors such as financial services, automotive, and professional services have a stronger reason to favor on-device AI processing, which supports notebooks with larger LPDDR5X configurations. The Middle East and Africa and South America still form a smaller demand pool, with government procurement and premium consumer purchases in Gulf Cooperation Council countries standing out as the clearest near-term pockets. South America is likely to remain more price sensitive, which means adoption can rise while higher-capacity memory mixes still lag North America and parts of Europe.

Competitive Landscape

The LPDDR5X DRAM market for AI PC and thin-and-light laptop industry is concentrated at the chip production layer, where Samsung Electronics, SK hynix, and Micron Technology continue to hold the strongest positions. Their advantage comes from capital scale, advanced process capability, and long qualification cycles that make it hard for new entrants to move quickly. Supply diversification started to improve when CXMT entered LPDDR5X mass production in October 2025 and when Nanya broadened its role in advanced DRAM supply discussions during 2026. At the module and distribution layer, competition is more fragmented among companies such as ADATA, Innodisk, BIWIN, Team Group, and Longsys/FORESEE, where supply access and regional reach matter more than core memory design. This split creates a market that is tight and concentrated upstream but much looser downstream.

Several strategic moves show how leading suppliers are trying to extend that advantage. Micron shipped the first 1γ-node LPDDR5X samples at 10.7 Gbps in June 2025, which gave it an early process leadership signal in advanced low-power DRAM. SK hynix answered by completing 1c-node LPDDR6 development in March 2026, which showed how quickly the next performance benchmark is being prepared beyond LPDDR5X. Samsung also pushed LPDDR5X-PIM work forward in 2026, aiming to embed more processing capability inside memory for AI inference use cases. These moves show that competition is no longer only about supplying bits, but also about shaping the next notebook memory architecture in the LPDDR5X DRAM market for AI PC and thin-and-light laptop industry.

Another area of competition is serviceability. Framework’s Laptop 13 Pro demonstrated that LPCAMM2 can pair LPDDR5X efficiency with user-replaceable memory in a thin notebook form factor. JEDEC’s CAMM2 standard gives suppliers a formal path to serve repairability-focused users and enterprise buyers that care about lifetime upgrade flexibility. That creates room for memory suppliers that can support soldered, on-package, and modular LPDDR5X approaches at the same time. Framework remains more relevant as a downstream adoption catalyst than as a DRAM supplier, while interface and controller IP companies such as Rambus sit closer to the enabling layer of the broader ecosystem.

Leaders of LPDDR5X DRAM Market For AI PC and Thin-and-Light Laptop

Samsung Electronics Co., Ltd.

SK hynix Inc.

Micron Technology, Inc.

Nanya Technology Corporation

ChangXin Memory Technologies, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Nvidia announced the RTX Spark superchip at Computex 2026, featuring up to 128 GB of unified LPDDR5X memory connected via a 600 GB/s NVLink-C2C link and 1 petaflop of FP4 AI compute on a 3nm Grace Blackwell SoC. Devices from ASUS, Dell, HP, Lenovo, Microsoft Surface, and MSI are expected in fall 2026, establishing LPDDR5X as the unified memory standard for premium ARM-based Windows AI laptops.

- May 2026: Nanya Technology confirmed extended multi-year LPDDR5X supply contracts with OEM customers as the memory shortage deepens, and disclosed a completed NTD 78.7 billion (USD 2.49 billion) capital raise to fund construction of a new Taishan District plant expected to enter volume production in the second half of 2027.

- April 2026: SK Hynix commenced mass production of the 192 GB SOCAMM2, based on its 1c-node LPDDR5X process, delivering more than double the bandwidth and over 75% improved power efficiency versus conventional RDIMM, designed specifically for Nvidia's Vera Rubin GPU platform.

- April 2026: Framework Computer launched the Laptop 13 Pro with LPCAMM2 LPDDR5X-7467 memory in 16 GB, 32 GB, and 64 GB configurations, the first thin-and-light consumer notebook to pair LPCAMM2 upgradeability with LPDDR5X efficiency, starting at USD 1,199 for the DIY edition.

Scope of Report on LPDDR5X DRAM Market For AI PC and Thin-and-Light Laptop

The LPDDR5X DRAM Market for AI PC and Thin-and-Light Laptop Industry refers to the market for next-generation low-power DRAM used in devices that need both high memory speed and energy efficiency. It includes memory chips and modules designed for smartphones, tablets, ultra-thin laptops, automotive systems, and AI edge devices.

The LPDDR5X DRAM Market for AI PC and Thin-and-Light Laptop Industry Report is Segmented by Processor Platform (x86 Platforms, and ARM Platforms), Memory Capacity(16 GB, 24 GB, 32 GB, 48 GB, and 64 GB and Above), End User (Premium Consumers, Enterprise / Commercial Users, Creative Professionals and Developers, Education and Public Sector, and Small Business / Prosumer Users), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

| x86 Platforms |

| ARM Platforms |

| 16 GB |

| 24 GB |

| 32 GB |

| 48 GB |

| 64 GB and Above |

| Premium Consumers |

| Enterprise / Commercial Users |

| Creative Professionals and Developers |

| Education and Public Sector |

| Small Business / Prosumer Users |

| North America | |

| Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| Taiwan | |

| Rest of Asia-Pacific | |

| Rest of the World |

| By Processor Platform | x86 Platforms | |

| ARM Platforms | ||

| By Memory Capacity | 16 GB | |

| 24 GB | ||

| 32 GB | ||

| 48 GB | ||

| 64 GB and Above | ||

| By End User | Premium Consumers | |

| Enterprise / Commercial Users | ||

| Creative Professionals and Developers | ||

| Education and Public Sector | ||

| Small Business / Prosumer Users | ||

| By Geography | North America | |

| Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| Taiwan | ||

| Rest of Asia-Pacific | ||

| Rest of the World | ||

Key Questions Answered in the Report

How large is the LPDDR5X DRAM market for AI PC and thin-and-light laptop?

The market stood at USD 2.74 billion in 2025 and is projected to reach USD 5.82 billion by 2031, growing at an 8.06% CAGR from 2026 to 2031.

Why is 16 GB such an important configuration in AI notebooks?

Microsoft's Copilot+ PC standard made 16 GB the minimum qualifying memory level, so it now acts as the baseline for compliant AI notebooks rather than a premium option.

Which memory capacity tier is growing the fastest?

The 64 GB and above tier is projected to expand at a 9.44% CAGR through 2031, reflecting stronger demand for local AI inference and heavier multitasking workloads.

Which processor platform is gaining momentum faster, x86 or ARM?

X86 led revenue in 2025 with a 51.68% share, but ARM is projected to grow faster at a 9.65% CAGR as more premium AI notebook designs enter the market.

Which region leads current demand and which one is growing the fastest?

North America led with 62.28% revenue share in 2025, while Asia-Pacific is expected to post the fastest growth at a 9.89% CAGR through 2031.

What is the biggest risk to higher LPDDR5X adoption in notebooks?

The main risk is supply and cost pressure, because memory capacity is being pulled toward AI server products and that can keep notebook LPDDR5X prices elevated.

Page last updated on: