Size and Share of CMP Slurry and Pads Market For DRAM Manufacturing

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.11 Billion |

| Market Size (2031) | USD 2.06 Billion |

| Growth Rate (2026 - 2031) | 13.16% CAGR |

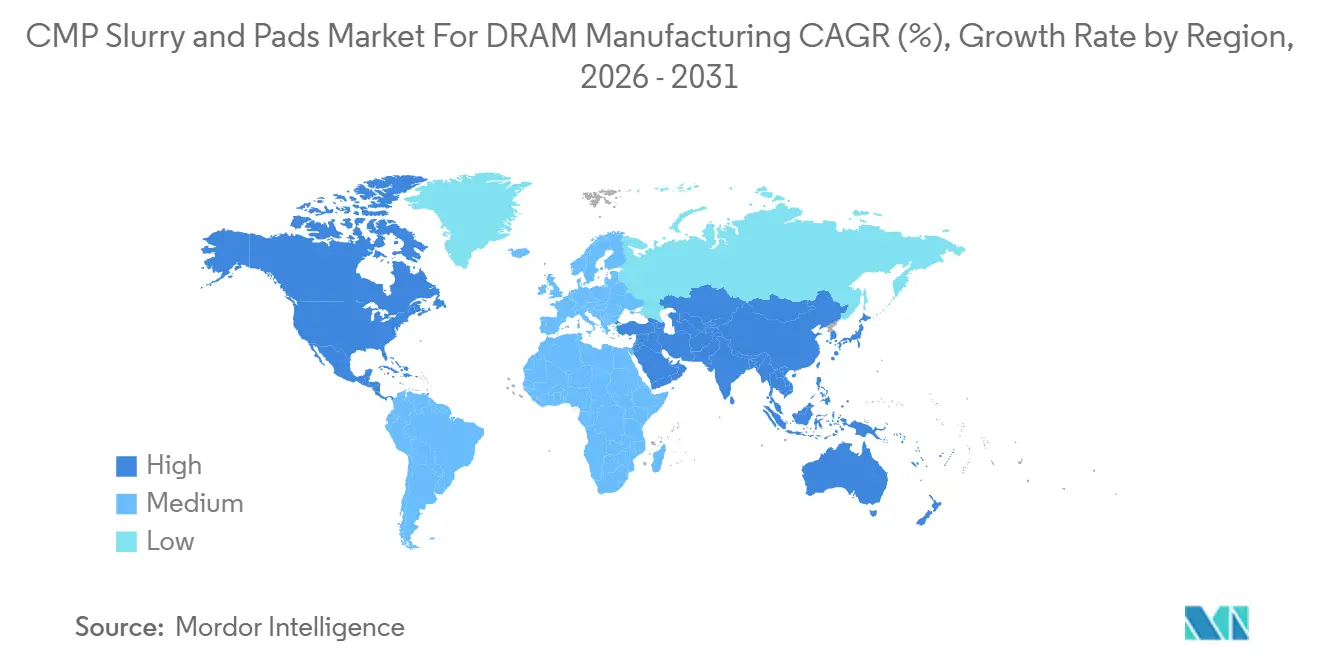

| Fastest Growing Market | North America |

| Largest Market | Asia-Pacific |

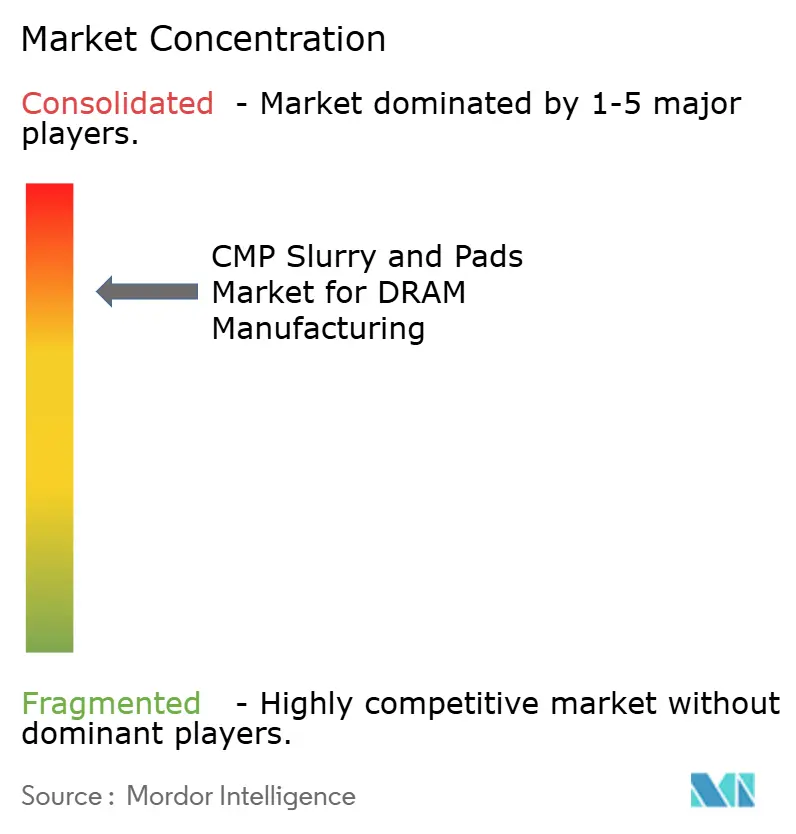

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Analysis of CMP Slurry and Pads Market For DRAM Manufacturing by Mordor Intelligence

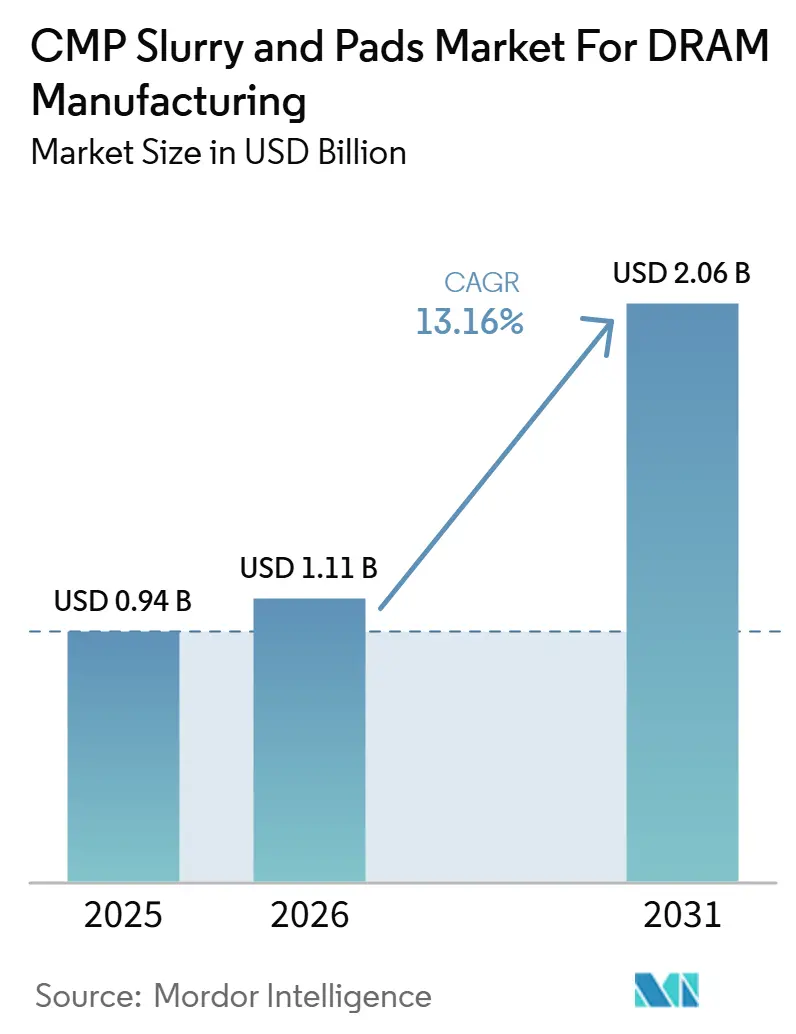

The CMP slurry and pads market for DRAM manufacturing size is projected to be USD 0.94 billion in 2025, USD 1.11 billion in 2026, and reach USD 2.06 billion by 2031, growing at a CAGR of 13.16% from 2026 to 2031. The rise reflects a clear increase in the number of planarization steps needed at sub-10nm DRAM nodes, where tighter patterning rules and more complex material stacks raise slurry intensity per wafer and lift pad requirements across critical polishing stages. Demand from HBM and server DRAM is also lifting the CMP slurry and pads market for DRAM manufacturing because stacked memory structures add polishing steps in through-silicon via formation, backside thinning, and advanced packaging flows that do not exist at the same depth in conventional DRAM lines. New fab construction in major memory hubs is shortening the interval between equipment installation and production ramp, which increases the value of pre-qualified consumables and favors suppliers that already hold approved positions inside leading fabs. The market is also moving toward premium chemistries because EUV-linked process layers need lower particle counts, lower scratch levels, and tighter surface roughness control than older node flows, which narrows the usable supplier base even when overall wafer demand is rising. Competitive conditions therefore remain active but not fragmented, because long qualification cycles protect incumbents while regional suppliers, especially in Asia, continue to gain ground first at mature nodes and then at selected advanced steps.

Key Report Takeaways

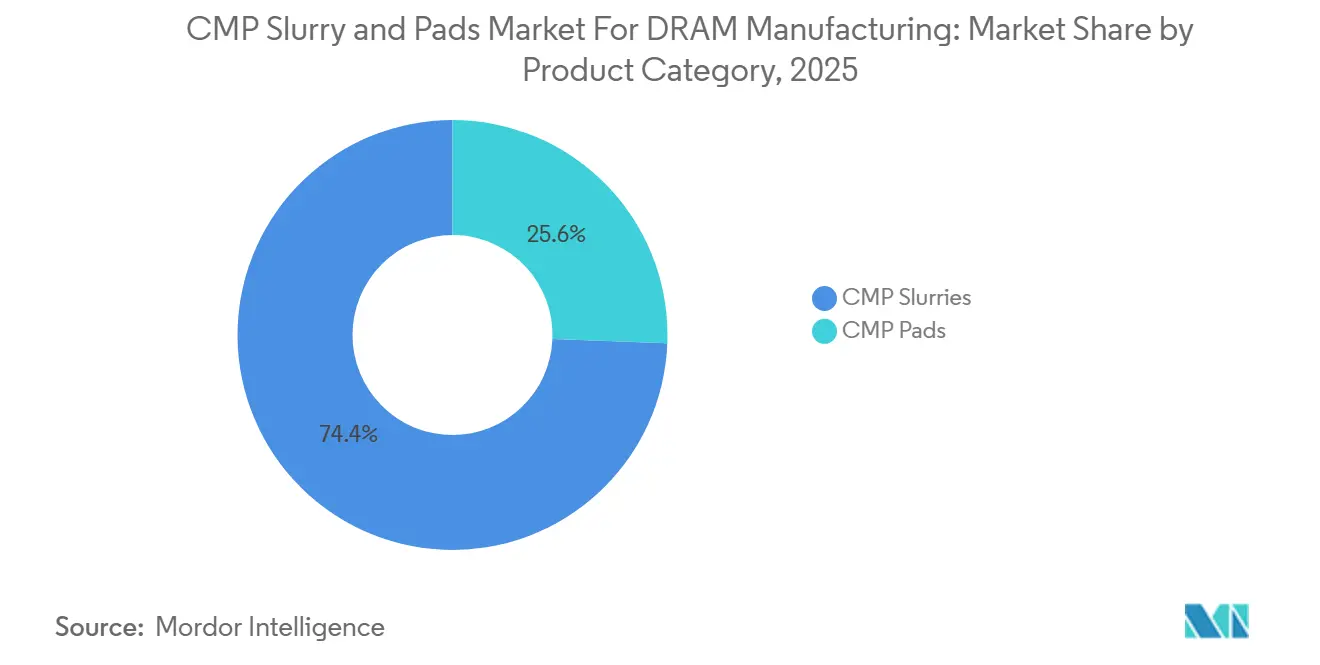

- By product category, CMP slurries held 74.38% of the CMP slurry and pads market for DRAM manufacturing in 2025, and the same segment is projected to expand at a 14.22% CAGR through 2031.

- By abrasive type, colloidal silica slurries accounted for 44.61% share in 2025, while nano-engineered slurries are projected to grow at a 15.08% CAGR through 2031.

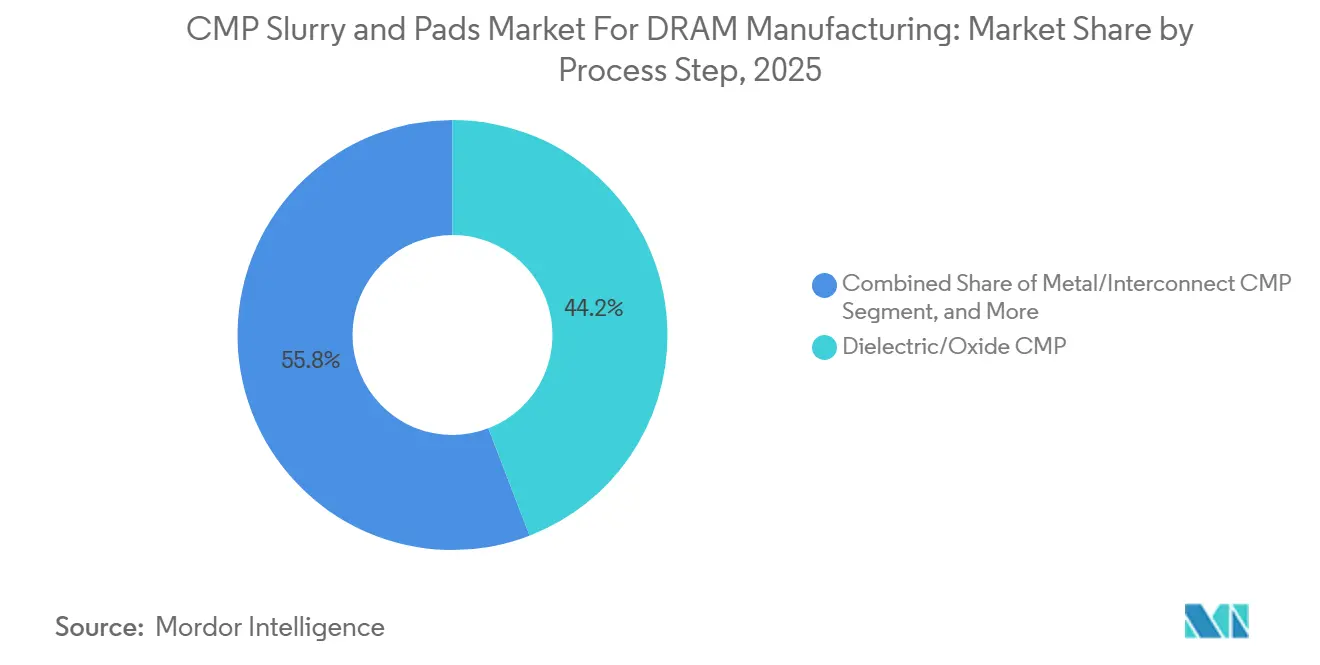

- By process step, dielectric and oxide CMP accounted for 44.16% of the market in 2025, while capacitor stack and DRAM cell structure CMP are expected to grow at a 14.65% CAGR through 2031.

- By geography, Asia-Pacific captured 89.46% share in 2025, while North America is projected to post the fastest regional expansion at a 14.87% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Insights and Trends of CMP Slurry and Pads Market For DRAM Manufacturing

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising CMP Step Count in Advanced DRAM Nodes | +3.5% | Global, concentrated in South Korea, Taiwan, Japan | Medium term (2-4 years) |

| Faster HBM and DRAM Capacity Additions | +3.0% | South Korea, Taiwan, North America | Short term (≤ 2 years) |

| Shift to 300 mm Memory Wafer Production | +2.0% | APAC core, spill-over to North America | Medium term (2-4 years) |

| Tight Defectivity Targets Inherited from EUV-Enabled Integration | +1.5% | South Korea, Japan, Taiwan | Medium term (2-4 years) |

| Qualification Pull from Memory Fabrication Consolidation | +0.8% | Global, with early gains in North America and Europe | Short term (≤ 2 years) |

| Expanding Use of Chemistries Tuned for Low-Scratch Polishing | +0.6% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising CMP Step Count in Advanced DRAM Nodes

The strongest structural support for the CMP slurry and pads market for DRAM manufacturing comes from the steady increase in polishing steps required as DRAM makers move deeper into sub-10nm integration. Advanced cell structures now incorporate more complex oxide, nitride, metal, and capacitor interfaces, increasing the number of surfaces that must be planarized within narrow tolerance windows during front-end processing. The same research shows that selectivity requirements for oxide-to-nitride stacks in advanced memory structures can exceed 500:1, which pushes fabs toward engineered ceria, composite abrasives, and tighter additive control rather than standard formulations. That change matters because every additional step multiplies slurry use per wafer, even before any new fab starts production, so the CMP slurry and pads market for DRAM manufacturing grows with process complexity and wafer volume. The material transition from tungsten to molybdenum in leading wordline structures also expands the chemistry requirements, because removal behavior, oxidation control, and defect sensitivity differ from those in older tungsten-heavy flows described in the original draft. As a result, suppliers that can meet advanced-node removal, selectivity, and defect targets are positioned to capture more value per qualified step, not only more volume across a larger installed base.

Faster HBM and DRAM Capacity Additions

Faster capacity additions in HBM and advanced DRAM are driving near-term demand for CMP slurry and pads in the DRAM manufacturing market, as new lines require qualified consumables from the first production lots onward. Industry conference material on HBM shows that stacked memory is gaining a larger share of total DRAM revenue, supporting higher polishing intensity per wafer as through-silicon via and stacking flows expand across the product mix. HBM manufacturing uses extra CMP passes for TSV copper fill, wafer thinning, and stack preparation, so a larger HBM mix lifts slurry demand even when total wafer starts do not rise at the same pace. Supplier behavior already reflects this shift, as Qnity launched the Emblem CMP pad platform for HBM and AI computing applications and paired that launch with a long-term supply agreement with SK hynix. Applied Materials and SK hynix also announced a long-term collaboration to develop next-generation DRAM and HBM manufacturing processes, with new materials and complex integration schemes named as core work areas. Taken together, these moves show that the CMP slurry and pads market for DRAM manufacturing is being shaped not only by more memory demand, but also by a richer process mix that requires more specialized consumables per finished device.

Shift to 300 Mm Memory Wafer Production

The shift toward 300 mm memory wafer production continues to strengthen the CMP slurry and pads market for DRAM manufacturing because every major advanced capacity project is centered on that wafer format. Micron signed a letter of intent in 2026 to purchase the Tongluo site in Taiwan, and the company framed the acquisition around a faster path to future DRAM output from a 300 mm-capable manufacturing base. The economic logic is straightforward: a 300 mm wafer offers much more usable area than a 200 mm wafer, increasing consumable demand per polishing pass and raising the value of stable process control across wider surfaces. The production footprint around these wafer lines is also becoming more localized, and that favors suppliers with nearby manufacturing, local technical teams, and shorter logistics paths into major memory clusters. FUJIFILM expanded its Kumamoto CMP slurry capacity and stated that the site was positioned to support growing semiconductor materials demand near the regional production base. Entegris has followed the same direction in the United States through larger domestic manufacturing and technology center plans, which shows that the CMP slurry and pads market for DRAM manufacturing is being organized around proximity, process support, and faster customer response.

Tight Defectivity Targets Inherited From EUV-Enabled Integration

Tighter defectivity targets from EUV-enabled DRAM integration are pushing the CMP slurry and pads market for DRAM manufacturing toward premium, low-defect formulations. Samsung presented results at SPIE Advanced Lithography and Patterning 2026 that demonstrated 10nm and sub-10nm DRAM patterning using high-NA EUV, confirming that advanced lithography is moving from feasibility work into manufacturing-relevant process conditions.[1]Samsung Electronics, “Advancing DRAM Patterning High-NA EUV Lithography for 10nm and Beyond Node Technologies,” SPIE Advanced Lithography and Patterning 2026, spie.org Once EUV enters the pattern flow, a scratch, particle, or roughness defect after CMP can propagate into a yield-limiting pattern issue, which raises the penalty for any slurry or pad variation that once would have been acceptable. The original draft noted particle counts below 0.05 particles per cm² and surface roughness below 0.15 nm, and those thresholds explain why legacy commodity abrasives are losing fit at critical layers. Peer-reviewed CMP research also confirms that advanced memory integration is moving toward more demanding material interfaces and tighter selectivity control, which supports a premium mix shift inside the CMP slurry and pads market for DRAM manufacturing. This is why suppliers with stronger particle-size control, contamination management, and formulation stability hold an advantage when fabs qualify materials for EUV-adjacent DRAM layers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Long Qualification Cycles for Fab Approval | -1.8% | Global | Medium term (2-4 years) |

| Cost Pressure from Memory Cyclicality | -1.4% | Global | Short term (≤ 2 years) |

| Formulation Sensitivity to Localized Supply Chain Interruptions | -0.7% | APAC core, North America | Medium term (2-4 years) |

| Limited Differentiation Outside High-End Memory Nodes | -0.4% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Long Qualification Cycles for Fab Approval

Long qualification cycles remain the clearest structural brake on the CMP slurry and pads market for DRAM manufacturing because new materials cannot move quickly from lab success into revenue at leading memory fabs. The peer-reviewed record shows that advanced CMP development must demonstrate control of removal rate, selectivity, defect performance, and post-polish cleanliness across demanding multi-material structures, which naturally extends approval timelines. In practice, suppliers often need to work jointly with the fab to tune pad conditioning, slurry chemistry, and cleaning conditions for a specific process stack and tool set, so qualification becomes a development exercise rather than a purchasing event. Even when a challenger offers better technical performance, the revenue window can narrow if the material reaches approval late in a node cycle or only after the customer has locked key steps to existing suppliers. The result is that the CMP slurry and pads market for DRAM manufacturing can show strong long-term demand while still remaining difficult for new suppliers to penetrate at the most valuable advanced-node positions.

Cost Pressure from Memory Cyclicality

Memory cyclicality also constrains the CMP slurry and pads market for DRAM manufacturing because material demand is closely tied to wafer starts and fab utilization. When DRAM supply loosens and selling prices come under pressure, manufacturers often react by adjusting input volumes and pushing suppliers for cost reductions, which transfers financial stress down the consumables chain as described in the original draft. That matters because slurry production uses high-purity materials, dedicated equipment, and contamination controls that do not scale down easily during weak periods. Suppliers with broader customer exposure across memory, logic, and packaging are therefore better positioned to absorb swings than vendors that rely too heavily on a narrow DRAM customer set. Entegris described rising unit-driven volumes from advanced manufacturing processes in its 2026 results, highlighting the upside when the cycle is favorable but also showing how closely performance is linked to customer production intensity. FUJIFILM has likewise framed CMP as part of a broader semiconductor materials strategy, which helps reduce the impact of any single end-use downturn on the business case for continuing investment.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Category: Slurries Hold the Larger Value Pool Across DRAM Polishing Steps

CMP slurries captured 74.38% share of the CMP slurry and pads market for DRAM manufacturing in 2025, and the segment is also projected to expand at a 14.22% CAGR through 2031. That lead reflects the chemical specificity of DRAM polishing flows, in which oxide, tungsten, barrier, and cell-structure steps all depend on tailored removal behavior that cannot be achieved solely through mechanical polishing. The original draft also linked slurry demand to the rising number of process steps per wafer, which means advanced-node migration increases slurry consumption even before new fab output comes online. A January 2026 peer-reviewed paper supports this view by showing that advanced multi-material memory structures require extreme selectivity control, thereby increasing dependence on engineered chemistries rather than broad, low-cost formulations. FUJIFILM stated that it held a 46% global share in both copper bulk and copper barrier CMP slurry and set a goal to more than double total CMP slurry revenue by FY2030, with emphasis on DRAM and HBM packaging, underscoring how central this category is to supplier strategy.

CMP pads held the remaining portion of the CMP slurry and pads market for DRAM manufacturing, but their demand curve differs because replacement is tied more closely to pad life, groove health, and tool installation than to chemistry load per polishing step. The segment still benefits from DRAM and HBM complexity, especially where advanced packaging and hybrid bonding require tighter flatness and lower defectivity across copper-dielectric surfaces. Qnity launched its Emblem CMP pad platform specifically for HBM and AI computing applications and paired that product move with a long-term supply agreement with SK hynix, which shows how pad suppliers are targeting the highest-growth memory uses. South Korean suppliers are also expanding pad work into hybrid bonding, where the tolerance window is much tighter than in legacy memory flows and where pad design becomes more directly linked to yield protection. This keeps pads as a smaller but strategically important part of the CMP slurry and pads market for DRAM manufacturing, especially when customers need application-specific products rather than broadly interchangeable consumables.

By Abrasive Type: Engineered Formulations Gain Ground At Advanced Nodes

Colloidal silica slurries accounted for 44.61% of the market in 2025, making them the largest chemistry group in the CMP slurry and pads market for DRAM manufacturing by abrasive type. Their scale stems from a long qualification history, broad process fit, and strong adaptability across oxide, metal, and capacitor-related polishing steps in mainstream DRAM production. FUJIFILM's front-end slurry portfolio also presents colloidal silica as a low-defect option for dielectric and STI use, which supports its established position in high-volume production settings.[2]FUJIFILM Electronic Materials, “Front End CMP Slurries,” FUJIFILM Electronic Materials, fujifilm.com The chemistry remains deeply embedded because fabs value known removal behavior and broad process familiarity when yields are under pressure during node migration. Even so, the CMP slurry and pads market for DRAM manufacturing is moving beyond legacy silica-only demand, as the most advanced layers now require tighter roughness control, lower scratch risk, and better particle stability than broad commodity systems typically offer.

Nano-engineered slurries are projected to grow at a 15.08% CAGR through 2031, making them the fastest-growing segment of the CMP slurry and pads market for DRAM manufacturing. The original draft connected that expansion to precision-engineered particle architectures for sub-10nm DRAM and hybrid bonding, where morphology and surface chemistry matter more than simple abrasive loading. Ceria-based slurries also remain important, especially in STI and other oxide-to-nitride environments where high selectivity protects stop layers and supports uniform planarization across complex front-end stacks. Fumed silica and other hybrids still serve narrower needs such as more aggressive polish-back steps, but research and capital are clearly shifting toward engineered abrasive systems that can support the next phase of the CMP slurry and pads market for DRAM manufacturing.

By Process Step: Capacitor Complexity Raises the Growth Profile

Dielectric and oxide CMP held 44.16% share in 2025, which made it the largest application group within the CMP slurry and pads market for DRAM manufacturing market size. This lead stems from the simple fact that every DRAM flow uses repeated oxide planarization in shallow trench isolation and interlayer dielectric formation, regardless of whether the wafer runs on a mature node or a leading-edge architecture. The segment therefore provides a large and stable base for suppliers, as demand remains broad even as the product mix shifts across device generations. It is also the most qualified application area, meaning long customer histories and incumbent positions remain important even as new, advanced nodes enter production. At the same time, EUV-linked process tightening is raising defect expectations in what had once been a relatively mature application set, so oxide CMP is no longer insulated from the premiumization trend visible across the CMP slurry and pads market for DRAM manufacturing.

Capacitor stack and DRAM cell structure CMP is projected to expand at a 14.65% CAGR, making it the fastest-growing application layer in the CMP slurry and pads market for DRAM manufacturing. That growth reflects the rising structural complexity of embedded DRAM capacitors as manufacturers work to preserve capacitance while cell dimensions keep shrinking across sub-10nm nodes. The original draft described cylinder-over-pillar and dual-crown structures that require polishing of alternating oxide-nitride multilayers, and that kind of stack intensifies selectivity demands beyond what many standard formulations can reliably support. Tungsten and contact CMP remains important because filled contact structures still require high step counts, while metal and interconnect CMP benefits from denser logic-in-periphery design and added metallization in supporting circuits. Other applications such as barrier layer CMP and poly-silicon CMP stay smaller in volume, yet they remain technically important because over-polish control, mixed-material planarity, and angstrom-level uniformity can decide whether the broader CMP slurry and pads market share for DRAM manufacturing shifts toward a supplier with a deeper specialty portfolio.

Geography Analysis

Asia-Pacific held 89.46% share in 2025, which made it the core regional base for the CMP slurry and pads market for DRAM manufacturing market share. That concentration mirrors the location of the main DRAM production ecosystem, where South Korea, Taiwan, and Japan anchor advanced memory capacity, supplier support, and process know-how across multiple generations of DRAM manufacturing. South Korea remains the largest consumer in the region because Samsung Electronics and SK hynix operate the most significant advanced-node production facilities and continue to drive process development toward HBM and leading-edge DRAM flows. Taiwan adds strategic weight through Micron's manufacturing expansion path, while Japan matters both as a semiconductor materials production base and as a long-standing location for slurry development and specialty manufacturing. The regional structure also gives Asia-Pacific an advantage in process support because many suppliers place plants, application teams, and technical service functions close to customer fabs to shorten qualification and troubleshooting cycles.

China is also becoming more relevant within the CMP slurry and pads market for DRAM manufacturing, even though the region still trails the leading memory hubs in qualified advanced-node supply. The clearest sign is the progress of domestic consumables companies that are first winning business at mature nodes and then using that operating record to pursue more demanding accounts. Hubei Dinglong reported 2025 CMP polishing pad revenue of CNY 1.09 billion (USD 153.5 million), with year-over-year growth of 52.34%, and the provincial department also noted small-batch supply to a mainstream foreign logic manufacturer in April 2025. That development matters because it shows Chinese suppliers are no longer limited to local replacement demand and are beginning to test acceptance beyond domestic fabs. Over time, this could make pricing and qualification dynamics in the broader CMP slurry and pads market for DRAM manufacturing more competitive, especially in mid-range process steps where technical barriers are lower than at the most advanced DRAM layers.

North America is projected to expand at a 14.87% CAGR through 2031, which makes it the fastest-growing region in the CMP slurry and pads market for DRAM manufacturing. Growth is tied to a stronger domestic semiconductor manufacturing push, new technology center investments, and greater emphasis on local materials support for advanced-node production. Entegris reported 2026 first-quarter sales growth tied to increasing unit-driven volumes from the most advanced manufacturing processes and is expanding its U.S. manufacturing and R&D footprint, including work tied to CMP slurries and pads.[3]Entegris, “Entegris Reports Results for First Quarter of 2026,” Business Wire, businesswire.com Europe remains smaller, but FUJIFILM's investment in Belgium for new CMP slurry facilities shows that regional semiconductor demand is sufficient to justify localized supply capability.

Competitive Landscape

The competitive structure of the CMP slurry and pads market for DRAM manufacturing is consolidated at the top, where a limited group of global suppliers holds qualified positions at leading memory fabs, while a broader regional field competes more actively at mature nodes and in adjacent applications. FUJIFILM, Entegris, Resonac, and DuPont de Nemours, Inc. remain the most visible names in the original draft because they combine manufacturing scale, materials science capability, and customer access across critical polishing steps. Their advantage is not just product breadth, because qualification history, clean manufacturing, local technical service, and the ability to support joint development matter just as much as nominal portfolio size. This is why the CMP slurry and pads market for DRAM manufacturing has not fragmented despite clear demand growth, since new suppliers still face a long path from technical promise to production approval. The field stays competitive, but the most valuable positions remain protected by performance requirements that are hard to meet consistently across advanced DRAM layers.

Leading suppliers are also using concrete strategic moves to deepen their positions in the CMP slurry and pads market for DRAM manufacturing. FUJIFILM has expanded slurry capacity in Kumamoto and invested in Belgium, which supports its local production model and improves supply responsiveness near customer clusters. Entegris is building out U.S. manufacturing and a technology center with CMP scope, while its 2026 results tied business momentum to advanced process volumes, which shows that commercial gains are being linked directly to customer node migration. Qnity used its Emblem launch and the SK hynix supply agreement to strengthen its HBM and AI memory positioning, which is a direct response to where future premium pad demand is expected to form.[4]DuPont de Nemours, “Qnity and SK Hynix Sign Long-Term CMP Pad Supply Agreement,” DuPont News Release, dupont.com These steps show that competition is being shaped less by spot pricing and more by geographic proximity, co-development depth, and readiness for the most demanding process transitions.

The next layer of competition in the CMP slurry and pads market for DRAM manufacturing is forming around advanced packaging, hybrid bonding, and the rise of Chinese domestic suppliers. FUJIFILM stated that hybrid bonding CMP slurry for advanced packaging was under sample evaluation at major HBM manufacturers, which points to a product area where qualification wins can reshape future share. Resonac launched the US-JOINT R&D center in Silicon Valley with multiple industry partners to shorten development cycles for next-generation packaging, which could speed the route from concept work to customer evaluation for new CMP-related materials. Hubei Dinglong has also moved beyond local substitution and now presents itself as a supplier with four CMP process material categories, which adds pressure in the lower and middle tiers of the market. The overall picture is a market where top suppliers still control the hardest qualifications, but competitive pressure is broadening as new technologies create fresh entry points and regional suppliers improve their execution.

Leaders of CMP Slurry and Pads Market For DRAM Manufacturing

Fujifilm Corporation

Entegris, Inc.

DuPont de Nemours, Inc.

Resonac Holdings Corporation

Hubei Dinglong Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Entegris, Inc. reported first-quarter 2026 net sales of USD 811.9 million, an increase of 5% year over year, with its Materials Solutions segment, which includes CMP slurries and pads, generating USD 351.1 million. Management cited "increasing unit-driven volumes related to the industry's most advanced manufacturing processes" as the primary growth driver.

- March 2026: Applied Materials, Inc. and SK hynix Inc. announced a long-term technology collaboration agreement to jointly develop next-generation DRAM and HBM manufacturing processes, with engineers from both companies co-locating at Applied's EPIC Center in Silicon Valley. The program focuses on new materials, complex integration schemes, and HBM-class advanced packaging, with CMP process development explicitly included as a core workstream.

- January 2026: Fujimi Incorporated commenced execution of its JPY 55 billion (USD 375.3 million) multi-year capital investment program, introducing new CMP slurry production lines for high-purity silica and ceria at its Japan and Taiwan facilities. The program targets expanded global supply capacity to serve accelerating demand from advanced DRAM and logic node customers.

- August 2025: Entegris, Inc. announced plans for USD 700 million in domestic U.S. R&D expenditure, raising its total planned U.S. manufacturing and R&D investment to USD 1.4 billion. A portion of the investment will develop its Aurora, Illinois, location into a U.S. Technology Center focused on CMP slurries, pads, deposition materials, and cleans.

Scope of Report on CMP Slurry and Pads Market For DRAM Manufacturing

The CMP slurry and pads market for DRAM manufacturing covers the chemical-mechanical planarization (CMP) consumables used in the fabrication of dynamic random-access memory (DRAM) chips. The market scope includes CMP slurries and polishing pads used across DRAM wafer processing steps to achieve surface planarity, remove material, and control defects during semiconductor manufacturing.

The CMP Slurry and Pads Market for DRAM Manufacturing Report is Segmented by Product Category (CMP Slurries, and CMP Pads), Abrasive Type (Ceria-Based Slurries, Colloidal Silica Slurries, Fumed Silica Slurries, Nano-Engineered Slurries, and Other Abrasive Types), Process Step (Dielectric/Oxide CMP, Tungsten/Contact CMP, Metal/Interconnect CMP, Capacitor Stack/DRAM Cell Structure CMP, and Other Process Steps), and Geography (North America, Europe, Asia-Pacific, and Rest of the World). Market Forecasts Are Provided in Terms of Value (USD).

| CMP Slurries |

| CMP Pads |

| Ceria-Based Slurries |

| Colloidal Silica Slurries |

| Fumed Silica Slurries |

| Nano-Engineered Slurries |

| Other Abrasive Types |

| Dielectric/Oxide CMP |

| Tungsten/Contact CMP |

| Metal/Interconnect CMP |

| Capacitor Stack/DRAM Cell Structure CMP |

| Other Process Steps |

| North America | |

| Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| Taiwan | |

| Rest of Asia-Pacific | |

| Rest of the World |

| By Product Category | CMP Slurries | |

| CMP Pads | ||

| By Abrasive Type | Ceria-Based Slurries | |

| Colloidal Silica Slurries | ||

| Fumed Silica Slurries | ||

| Nano-Engineered Slurries | ||

| Other Abrasive Types | ||

| By Process Step | Dielectric/Oxide CMP | |

| Tungsten/Contact CMP | ||

| Metal/Interconnect CMP | ||

| Capacitor Stack/DRAM Cell Structure CMP | ||

| Other Process Steps | ||

| By Geography | North America | |

| Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| Taiwan | ||

| Rest of Asia-Pacific | ||

| Rest of the World | ||

Key Questions Answered in the Report

What is the current and future size of the CMP slurry and pads market for DRAM manufacturing?

The market was valued at USD 0.94 billion in 2025, is projected to reach USD 1.11 billion in 2026, and is forecast to reach USD 2.06 billion by 2031 at a 13.16% CAGR.

Which product category leads demand in DRAM CMP consumables?

CMP slurries led with 74.38% share in 2025 and are also the faster-growing product category, supported by higher chemistry intensity across advanced-node and HBM process flows.

Why is HBM increasing demand for CMP materials?

HBM adds more CMP steps through TSV copper fill, backside thinning, and stack preparation, so slurry and pad demand rises with memory stacking even when wafer growth is moderate.

Which slurry chemistry is growing the fastest?

Nano-engineered slurries are projected to grow at a 15.08% CAGR through 2031 because advanced DRAM layers need tighter roughness control and lower defectivity than legacy abrasive systems.

Which application step is expanding the fastest?

Capacitor stack and DRAM cell structure CMP is projected to grow at a 14.65% CAGR, reflecting more complex embedded capacitor structures at shrinking DRAM geometries.

Which region offers the strongest growth outlook?

North America is projected to post the fastest regional CAGR at 14.87% through 2031, supported by local manufacturing expansion and new investments in semiconductor materials capability.

Page last updated on: