High Speed DDR5 DRAM Module Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

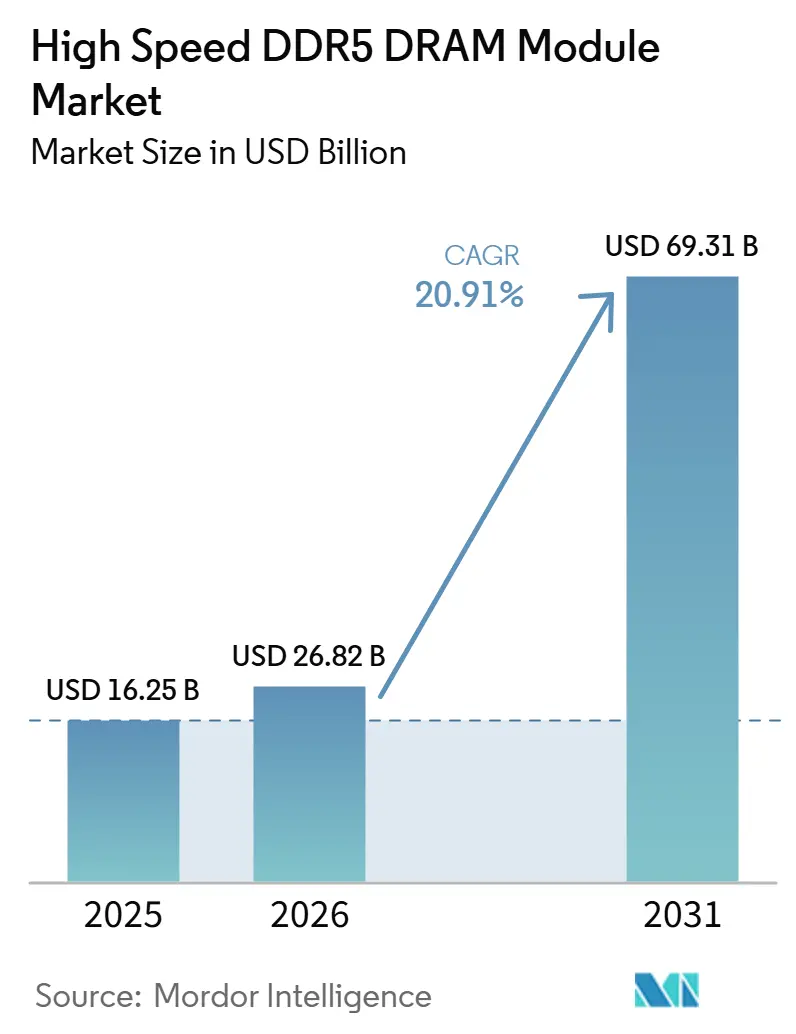

| Market Size (2026) | USD 26.82 Billion |

| Market Size (2031) | USD 69.31 Billion |

| Growth Rate (2026 - 2031) | 20.91% CAGR |

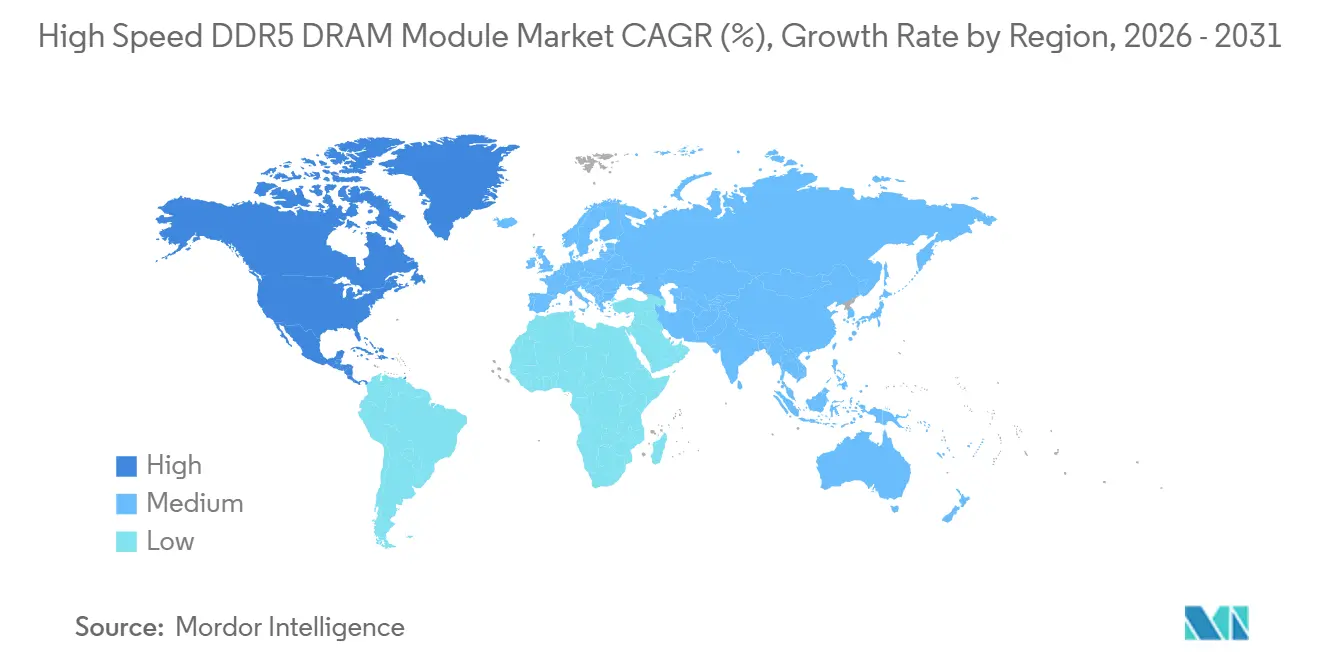

| Fastest Growing Market | North America |

| Largest Market | Asia-Pacific |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

High Speed DDR5 DRAM Module Market Analysis by Mordor Intelligence

The high speed DDR5 DRAM module market size is expected to increase from USD 16.25 billion in 2025 to USD 26.82 billion in 2026 and reach USD 69.31 billion by 2031, growing at a CAGR of 20.91% over 2026-2031. The high speed DDR5 DRAM module market is being shaped by AI inference deployments that require more memory bandwidth and higher per-server capacity than prior server refresh cycles. Pricing in the high speed DDR5 DRAM module market also reflects a tighter supply environment, because advanced DRAM capacity is being directed toward premium memory products and dense server configurations. A wider replacement cycle across DDR4-based servers, workstations, and premium client systems is expanding the addressable base for the high speed DDR5 DRAM module market beyond hyperscale builds alone. Platform validation at higher speeds, combined with on-module power management and signal integrity improvements, is making premium DDR5 modules more practical across cloud, enterprise, creator, and gaming workloads. The strongest opportunities in the high speed DDR5 DRAM module market remain tied to early qualification, secure die supply, higher-density modules, and lower-power designs that help operators scale memory footprints without a proportional rise in energy use.

Key Report Takeaways

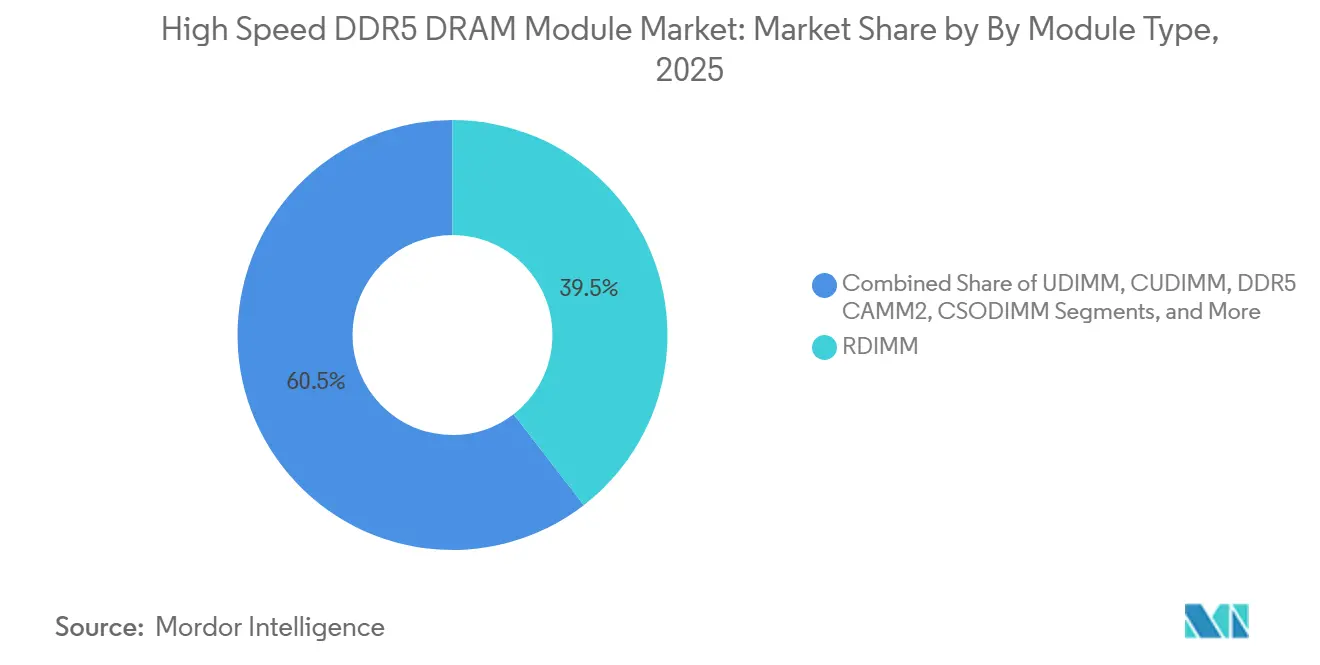

- By module type, RDIMM held 39.54% share of the high speed DDR5 DRAM module market in 2025, while MRDIMM / MCR DIMM is projected to expand at a 22.14% CAGR through 2031.

- By capacity, 64 GB to 96 GB accounted for 30.33% share of the high speed DDR5 DRAM module market in 2025, while capacities above 128 GB are projected to grow at a 22.34% CAGR during 2026-2031.

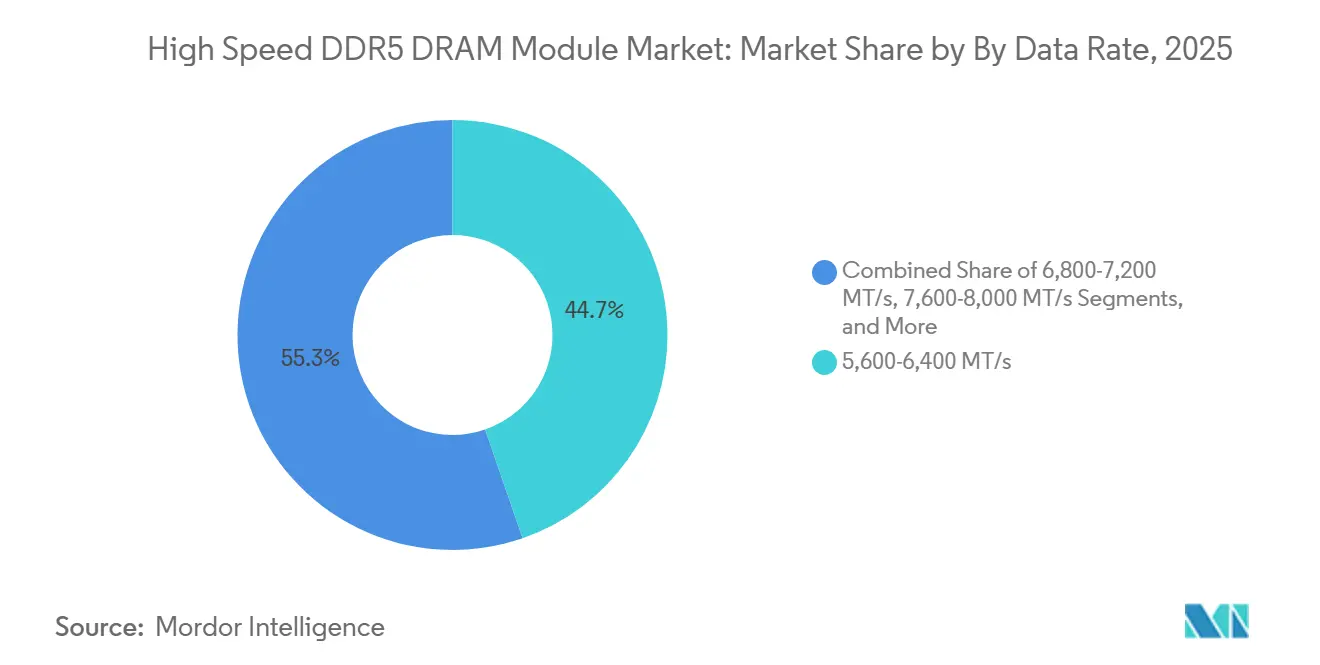

- By data rate, 5,600-6,400 MT/s captured 44.71% share of the high speed DDR5 DRAM module market in 2025, while 8,400-8,800 MT/s is expected to record the fastest growth at a 23.74% CAGR through 2031.

- By end use, hyperscale and cloud data centers held a 42.18% share of the high speed DDR5 DRAM module market in 2025, and the segment is projected to advance at a 23.35% CAGR over 2026-2031.

- By geography, Asia-Pacific led with 53.29% share of the high speed DDR5 DRAM module market in 2025, while North America is projected to expand at a 22.94% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global High Speed DDR5 DRAM Module Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift Toward Higher-Speed Client and Server Memory Platforms | +5.5% | Global, concentrated in North America and East Asia | Short term (≤ 2 years) |

| Rising AI Server and High-Performance Computing Memory Density Requirements | +4.0% | Global | Medium term (2–4 years) |

| DDR4 Replacement Across Mainstream PC and Server Refresh Cycles | +3.5% | Global, with North America and Europe leading enterprise refresh | Medium term (2–4 years) |

| Faster Adoption of On-Module Power Management and Signal Integrity Improvements | +2.5% | Global, with early gains in hyperscale-heavy North America and Asia Pacific | Medium term (2–4 years) |

| Growing Demand for Premium Gaming and Creator Systems | +1.5% | North America, Western Europe, and developed Asia Pacific markets | Short term (≤ 2 years) |

| Qualification of 8,800 MT/s-Class Modules for Next-Generation Platforms | +1.0% | North America and Europe, with spillover to East Asia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising AI Server and High-Performance Computing Memory Density Requirements

The largest demand driver in the high speed DDR5 DRAM module market is the shift from earlier AI build phases toward larger inference clusters that need more main memory close to compute. These server environments depend on large DDR5 RDIMM and MRDIMM pools to support model parameters, longer context windows, and broader memory footprints around accelerators. This changes the demand pattern because memory content per server rises even when shipment growth does not move at the same pace. It also lifts interest in higher-density modules, since operators need more capacity without expanding rack count or power use too quickly. Micron’s May 2026 sampling of 256 GB DDR5 RDIMM modules at speeds up to 9,200 MT/s and with more than 40% lower operating power than two 128 GB modules shows how the high speed DDR5 DRAM module market is moving toward denser configurations for AI infrastructure.

Shift Toward Higher-Speed Client and Server Memory Platforms

The high speed DDR5 DRAM module market is also benefiting from a steady rise in the validated speed floor across new server and client platforms. As system roadmaps move upward, slower DDR5 bins lose share and more volume shifts into premium modules with stronger signal integrity and tighter validation requirements. This keeps demand active across both server and client channels, even though the near-term pull is stronger in server platforms. It also changes product mix, because suppliers gain more room to sell modules with richer module-level functionality and higher performance positioning. JEDEC’s 2026 MRDIMM roadmap, which extends from the newly published DDR5MDB02 standard toward Gen2 modules targeting 12,800 MT/s and Gen3 designs targeting up to 17,600 MT/s, supports the long runway for higher-speed products in the high speed DDR5 DRAM module market.

DDR4 Replacement Across Mainstream PC and Server Refresh Cycles

A separate growth stream in the high speed DDR5 DRAM module market comes from the replacement of DDR4-based systems across mainstream servers, workstations, and premium PCs. This wave is structurally different from AI demand because it is tied to installed-base refresh cycles rather than only new infrastructure build-outs. Many fleets deployed earlier in the decade are now reaching performance and support thresholds that make a transition to DDR5 more practical during the 2025-2028 period. The effect is broader than server memory alone, since new notebooks and workstation designs are also moving toward form factors and speeds that align with newer DDR5 platform roadmaps. This replacement pattern supports a larger and more recurring demand base for the high speed DDR5 DRAM module market, even in customer groups that are not building large AI clusters.

Faster Adoption of On-Module Power Management and Signal Integrity Improvements

Another important support factor for the high speed DDR5 DRAM module market is the shift of more electrical and power-management functions onto the module itself. DDR5 uses on-die ECC, power management integrated circuits, and more advanced module logic to sustain higher speeds with better stability than prior memory generations. These features improve usability in systems that would otherwise face signal integrity limits at premium speed grades. They also increase the content value of each module, which helps suppliers defend pricing in upper-tier products. JEDEC’s publication of JESD82-552 for DDR5 MRDIMM designs in April 2026 formalized part of the interoperability layer needed for this transition, reinforcing the technical base for the high speed DDR5 DRAM module market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher Cost Per Bit Versus Legacy DDR4 Alternatives | -2.0% | Global, most pronounced in price-sensitive SME and mid-tier enterprise segments | Short term (≤ 2 years) |

| Platform Qualification Complexity for Very High Data Rate Modules | -1.5% | North America and Europe, enterprise and mid-tier cloud | Medium term (2–4 years) |

| Thermal Design and Board Routing Constraints at Higher Speeds | -1.0% | Global, primarily enterprise and industrial end-users | Medium term (2–4 years) |

| Dependence on Limited Advanced DRAM Supply and Component Ecosystem | -0.8% | Global, with spillover effects across APAC core and Rest of the World | Short to medium term |

| Source: Mordor Intelligence | |||

Higher Cost Per Bit Versus Legacy DDR4 Alternatives

The main commercial restraint in the high speed DDR5 DRAM module market is the cost gap against legacy DDR4 alternatives. DDR5 modules carry more component content and stricter electrical requirements, which keeps the cost floor above DDR4 even when buyers are not using the full bandwidth advantage. This is especially challenging for mid-tier enterprises and price-sensitive organizations that still run applications with limited performance benefit from premium DDR5 speeds. In these cases, existing DDR4 platforms can remain the more practical option while support life is still available. The result is that the high speed DDR5 DRAM module market grows fastest where performance demands are urgent, while value-focused customers often delay the move to premium DDR5 configurations.

Platform Qualification Complexity for Very High Data Rate Modules

Qualification complexity remains another restraint for the high speed DDR5 DRAM module market, especially in speed tiers above the mainstream ramp. Very high data rate modules need coordinated validation across the module supplier, server manufacturer, platform vendor, firmware stack, and system integrator before full deployment can begin. This creates a time gap between product availability and volume adoption, particularly in enterprise and mid-tier cloud environments. The delay matters because procurement at scale usually follows qualified vendor lists, thermal checks, and workload testing rather than the first sample release. JEDEC’s continuing work on the MRDIMM roadmap helps narrow this risk over time, but the high speed DDR5 DRAM module market still depends on multi-stage platform qualification before the fastest tiers can move into broad production use.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Module Type: RDIMM Anchors Server Demand While MRDIMM Builds the Next Bandwidth Layer

RDIMM held 39.54% of the high speed DDR5 DRAM module market share in 2025, reflecting its deep position in standard two-socket server deployments across enterprise and cloud environments. Its role remains strong because procurement teams already view it as the most established DDR5 server module type for scale deployments. Broad compatibility, mature supply chains, and familiar operational behavior keep RDIMM at the center of current server refresh programs. LRDIMM continues to serve dense memory configurations where load reduction supports larger memory footprints in more specialized server builds.

UDIMM and SODIMM still serve mainstream desktop and notebook needs, while CUDIMM and CSODIMM are becoming more relevant as higher client speeds gain traction across premium systems. DDR5 CAMM2 remained a smaller form factor in 2025, but it is attracting attention in thin workstations and premium laptops where space efficiency matters. MRDIMM / MCR DIMM is the fastest-growing module type in the high speed DDR5 DRAM module market because it addresses the bandwidth limits that standard registered modules eventually face in AI and high-performance server environments. Micron’s 256 GB DDR5 server module sampling and JEDEC’s MRDIMM standards roadmap both point to a broader role for MRDIMM designs as premium server platforms move toward higher sustained bandwidth and denser memory footprints.[1]Micron Technology, Inc., “Micron Redefines AI Performance With Sampling of 256GB DDR5 Server Module,” GlobeNewswire, globenewswire.com

By Capacity: Higher-Density Tiers Gain Weight as AI Inference Expands

The 64 GB to 96 GB tier accounted for 30.33% of the high speed DDR5 DRAM module market size in 2025, making it the current density sweet spot for standard two-socket server deployments. This tier balances channel population, memory footprint, and system cost in a way that works well for broad server rollouts. The 24 GB to 48 GB range still serves mid-range enterprise servers and workstation needs where memory intensity is lower. The 128 GB tier sits between mainstream server builds and heavier AI-oriented configurations, which makes it an important bridge category.

Above-128 GB modules are the fastest-growing capacity tier in the high speed DDR5 DRAM module market because larger inference environments increasingly need more model data to remain resident in system memory. That requirement raises interest in denser modules that can scale capacity without a one-for-one rise in slot usage. Micron’s May 2026 256 GB DDR5 RDIMM sampling validated the technical path for this tier, combining 3D-stacked die architecture, speeds up to 9,200 MT/s, and more than 40% lower operating power than two 128 GB modules. SK hynix’s December 2025 Intel Data Center Certification for its 256 GB DDR5 RDIMM also supports the move toward dense server memory, with the company reporting up to 16% higher inference performance and approximately 18% lower power consumption than its previous-generation 256 GB product.[2]SK hynix Inc., “SK hynix First to Complete Intel Data Center Certification for 32Gb Die-Based 256GB Server DDR5 RDIMM,” PR Newswire, prnewswire.com

By Data Rate: Mainstream Volume Holds Today While Premium Tiers Rise Faster

The 5,600-6,400 MT/s tier accounted for 44.71% of total volume in 2025 because it aligns with the main certification path for current server and client platforms. It benefits from the broadest qualification coverage and from a deeper supply than the highest performance DDR5 bins. The 6,800-7,200 MT/s range serves as the middle step for buyers seeking more bandwidth without moving all the way to the newest premium tiers. The 7,600-8,000 MT/s tier is building relevance in high-end client and workstation systems where additional speed can support premium positioning.

The 8,400-8,800 MT/s tier is the fastest-growing data-rate segment in the high speed DDR5 DRAM module market, supported by server platforms where memory bandwidth is a direct performance limit. This tier is gaining weight because AI inference servers need more bandwidth per socket and because premium module architectures are becoming more standardized. Micron’s DDR5 MRDIMM lineup targets this need directly with capacities from 32 GB to 256 GB and speeds reaching 8,800 MT/s for server deployments. JEDEC’s roadmap toward MRDIMM Gen2 at 12,800 MT/s and Gen3 at up to 17,600 MT/s suggests that the premium speed ladder in the high speed DDR5 DRAM module market will continue to move upward through the forecast period.[3]JEDEC Solid State Technology Association, “JEDEC Advances DDR5 MRDIMM Ecosystem With New Memory Interface Logic and Expanded MRDIMM Roadmap,” Business Wire, businesswire.com

By End-Use Application: Hyperscale Demand Leads While Client and Edge Uses Broaden the Base

Hyperscale and cloud data centers held 42.18% share in 2025, making them both the largest and fastest-growing end-use segment in the high speed DDR5 DRAM module market. Their role is central because AI inference deployments are consuming dense server memory faster than any other customer group. This demand has not only raised module consumption but has also changed allocation patterns across the broader supply chain. Enterprise data centers remain the second-largest end use, supported by DDR4 replacement cycles and a growing interest in private AI infrastructure.

Workstations, gaming PCs, and consumer and commercial notebooks add a separate client growth layer to the high speed DDR5 DRAM module market as faster DDR5 configurations spread into premium systems. These channels do not match hyperscale demand in scale, but they help diversify product mix across form factors and speed grades. Telecom and networking infrastructure remains a stable use case where reliable memory configurations support edge compute and communications equipment refresh cycles. Industrial, embedded, and edge systems are also becoming more relevant as higher-performance local processing creates room for durable, high-speed DDR5 deployments outside the data center.

Geography Analysis

Asia-Pacific held 53.29% of the global high speed DDR5 DRAM module market in 2025, which reflects the region’s combined strength in both upstream production and downstream demand. South Korea remains the anchor at the manufacturing layer because leading memory suppliers continue to shape global DRAM availability from their advanced fabrication base. China is a major demand center within the region, supported by large-scale cloud and AI infrastructure expansion. Taiwan contributes through module assembly and electronics ecosystem depth, while Japan supports critical parts of the advanced materials and packaging chain. Singapore also strengthens the regional profile because it serves as a data center hub for Southeast Asia and supports cross-border technology infrastructure demand.

North America is the fastest-growing geography in the high speed DDR5 DRAM module market during the forecast period. The region benefits from a high concentration of hyperscale AI spending, premium server refresh programs, and strong demand for dense memory configurations in new data center builds. It also gains from domestic manufacturing commitments that can support supply resilience over time. Micron’s May 2026 manufacturing expansion in Manassas, Virginia, backed by more than USD 2 billion in investment and tied to a broader USD 250 billion U.S. manufacturing and R&D commitment through 2035, reinforces North America’s strategic position in memory supply and technology development.

Europe trails Asia Pacific and North America in share, but it continues to generate steady demand from enterprise data center refresh programs, telecommunications infrastructure, and automotive compute platforms. The rest of the World is smaller, but it is expanding as sovereign AI projects, modernization programs, and enterprise refresh activity support new memory demand across multiple regions. The Middle East and Africa are benefiting from regional data center nodes that reduce latency for local digital services, while South America is seeing demand from banking, energy, and government refresh cycles. India also remains relevant over the longer horizon because import substitution efforts could gradually influence sourcing and local ecosystem decisions in the high speed DDR5 DRAM module market.

Competitive Landscape

The high speed DDR5 DRAM module market is moderately to highly consolidated at the die-supply layer and far more fragmented at the module assembly layer. Samsung, SK hynix, and Micron hold structural influence because they supply the DRAM dies that underpin nearly every module shipped into the market. That upstream concentration gives them leverage over pricing, allocation, and the pace at which premium products can scale. At the downstream level, module vendors compete more actively through speed binning, thermal design, aesthetic differentiation, and platform validation. This means the high speed DDR5 DRAM module market combines concentrated control over critical inputs with broader brand-level competition in finished modules.

Strategic behavior in the high speed DDR5 DRAM module market shows that roadmap timing matters as much as raw production scale. Micron moved early in May 2026 by sampling 256 GB DDR5 RDIMM modules built on 1-gamma technology, with speeds up to 9,200 MT/s, positioning the company for denser AI and high-performance server deployments. SK hynix strengthened its position in December 2025 by becoming the first supplier to complete Intel Data Center Certification for a 256 GB DDR5 RDIMM on the Xeon 6 platform, which improved its standing in premium server qualification cycles. These moves matter because early validation and early sampling tend to shape who captures the first wave of production demand in high-value server memory.

The next competitive gap is likely to form around MRDIMM qualification, supply reliability, and the ability to support very high speeds without creating power or thermal penalties that buyers cannot absorb. Suppliers that can align dense module roadmaps with server platform rollouts will have an advantage when procurement shifts from evaluation to full deployment. There is also room for module vendors to build niche strength in industrial, workstation, and CAMM2-oriented applications where ecosystem coverage is still developing. Even so, the high speed DDR5 DRAM module market will remain heavily influenced by the upstream decisions of the few companies that control advanced DRAM supply.

High Speed DDR5 DRAM Module Industry Leaders

Samsung Electronics Co., Ltd.

SK hynix Inc.

Micron Technology, Inc.

Kingston Technology Company, Inc.

Corsair Gaming, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2026: Samsung and SK hynix, alongside the South Korean government, announced a coordinated KRW 800 trillion (approximately USD 518 billion) investment to construct four new memory mega-fabs in South Korea's southwestern region, with the stated objective of doubling domestic DRAM production capacity within five years. The initiative establishes the largest single memory capacity expansion commitment in industry history and will directly determine the global DRAM supply trajectory through 2031.

- July 2026: Samsung and SK hynix announced plans to build high-bandwidth memory packaging fabs in the Chungcheong region as part of a KRW 392 trillion (approximately USD 252.5 billion) industrywide investment alongside government backing, per South Korea's Ministry of Trade, Industry, and Resources. The packaging facilities target HBM and advanced DRAM module production to serve next-generation AI accelerator platforms.

- May 2026: Micron Technology began manufacturing the most advanced DDR4 memory ever produced on US soil at its Manassas, Virginia, facility, backed by more than USD 2 billion in investment. The 1-alpha node delivers approximately 40% higher bit density than the preceding 1z generation and is supported by federal, state, and local incentive programs under the CHIPS and Science Act framework.

- April 2026: JEDEC Solid State Technology Association published JESD82-552 (DDR5MDB02), the Multiplexed Rank Data Buffer standard for DDR5 MRDIMM designs, and confirmed that its JC-45 Committee is nearing completion of the MRDIMM Gen2 module standard targeting 12,800 MT/s, while simultaneously initiating MRDIMM Gen3 standard development targeting up to 17,600 MT/s. The publications provide the interoperability framework for high-bandwidth DDR5 server memory to scale across future Intel Diamond Rapids and AMD EPYC Venice platforms.

Global High Speed DDR5 DRAM Module Market Report Scope

The High Speed DDR5 DRAM Module Market report covers module types, capacities, data rates, end-use applications, and geography. It analyzes UDIMM, CUDIMM, SODIMM, CSODIMM, CAMM2, RDIMM, LRDIMM, and MRDIMM/MCR DIMM across data centers, workstations, gaming PCs, notebooks, industrial and telecom applications in North America, Europe, Asia Pacific, and Rest of World.

The High Speed DDR5 DRAM Module Market Report is Segmented by Module Type (UDIMM, CUDIMM, SODIMM, CSODIMM, DDR5 CAMM2, RDIMM, LRDIMM, and MRDIMM / MCR DIMM), Capacity (Up to 16 GB, 24 GB to 48 GB, 64 GB to 96 GB, 128 GB, and Above 128 GB), Data Rate (5,600-6,400 MT/s, 6,800-7,200 MT/s, 7,600-8,000 MT/s, and 8,400-8,800 MT/s), End-Use Application (Hyperscale and Cloud Data Centers, Enterprise Data Centers, Workstations and Professional Systems, Gaming PCs, Consumer and Commercial PCs/Notebooks, Industrial, Embedded, and Edge Systems, and Telecom and Networking Infrastructure), and Geography (North America, Europe, Asia-Pacific, and Rest of the World). The Market Forecasts are Provided in Terms of Value (USD).

| UDIMM |

| CUDIMM |

| SODIMM |

| CSODIMM |

| DDR5 CAMM2 |

| RDIMM |

| LRDIMM |

| MRDIMM / MCR DIMM |

| Up to 16 GB |

| 24 GB to 48 GB |

| 64 GB to 96 GB |

| 128 GB |

| Above 128 GB |

| 5,600-6,400 MT/s |

| 6,800-7,200 MT/s |

| 7,600-8,000 MT/s |

| 8,400-8,800 MT/s |

| Hyperscale and Cloud Data Centers |

| Enterprise Data Centers |

| Workstations and Professional Systems |

| Gaming PCs |

| Consumer and Commercial PCs/Notebooks |

| Industrial, Embedded, and Edge Systems |

| Telecom and Networking Infrastructure |

| North America | |

| Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| Taiwan | |

| Rest of Asia-Pacific | |

| Rest of the World |

| By Module Type | UDIMM | |

| CUDIMM | ||

| SODIMM | ||

| CSODIMM | ||

| DDR5 CAMM2 | ||

| RDIMM | ||

| LRDIMM | ||

| MRDIMM / MCR DIMM | ||

| By Capacity | Up to 16 GB | |

| 24 GB to 48 GB | ||

| 64 GB to 96 GB | ||

| 128 GB | ||

| Above 128 GB | ||

| By Data Rate | 5,600-6,400 MT/s | |

| 6,800-7,200 MT/s | ||

| 7,600-8,000 MT/s | ||

| 8,400-8,800 MT/s | ||

| By End-Use Application | Hyperscale and Cloud Data Centers | |

| Enterprise Data Centers | ||

| Workstations and Professional Systems | ||

| Gaming PCs | ||

| Consumer and Commercial PCs/Notebooks | ||

| Industrial, Embedded, and Edge Systems | ||

| Telecom and Networking Infrastructure | ||

| By Geography | North America | |

| Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| Taiwan | ||

| Rest of Asia-Pacific | ||

| Rest of the World | ||

Key Questions Answered in the Report

What is the current and forecast value of the high speed DDR5 DRAM module market?

The high speed DDR5 DRAM module market reached USD 16.25 billion in 2025, grew to USD 26.82 billion in 2026, and is forecast to reach USD 69.31 billion by 2031 at a 20.91% CAGR.

Which module type leads demand in high speed DDR5 DRAM modules?

RDIMM led with 39.54% share in 2025 because it remains the standard choice for broad server deployments across enterprise and cloud environments.

Why are above-128 GB DDR5 modules gaining momentum so quickly?

They are gaining momentum because AI inference deployments require higher in-socket memory density, and suppliers are now validating 256 GB-class products for production server use.

Which data-rate tier currently dominates and which one is rising the fastest?

The 5,600-6,400 MT/s tier led with 44.71% in 2025, while the 8,400-8,800 MT/s tier is projected to grow the fastest through 2031.

Which region leads the high speed DDR5 DRAM module market, and which one is expanding the fastest?

Asia-Pacific held the largest share at 53.29% in 2025, while North America is expected to record the fastest growth during the forecast period.

What is shaping competition among suppliers in this space?

Competition is being shaped by upstream DRAM die concentration, early server-platform qualification, dense module roadmaps, and the ability to support higher speeds without major power or thermal penalties.

Page last updated on: